Dental Laboratory Welders Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

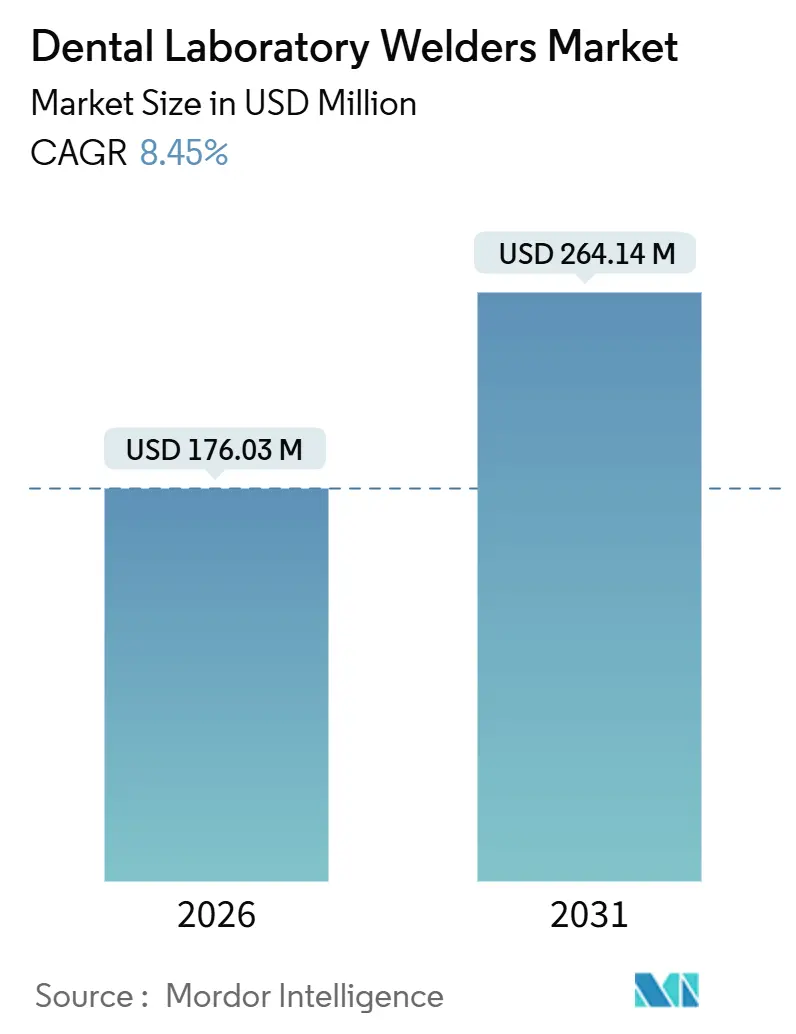

| Market Size (2026) | USD 176.03 Million |

| Market Size (2031) | USD 264.14 Million |

| Growth Rate (2026 - 2031) | 8.45% CAGR |

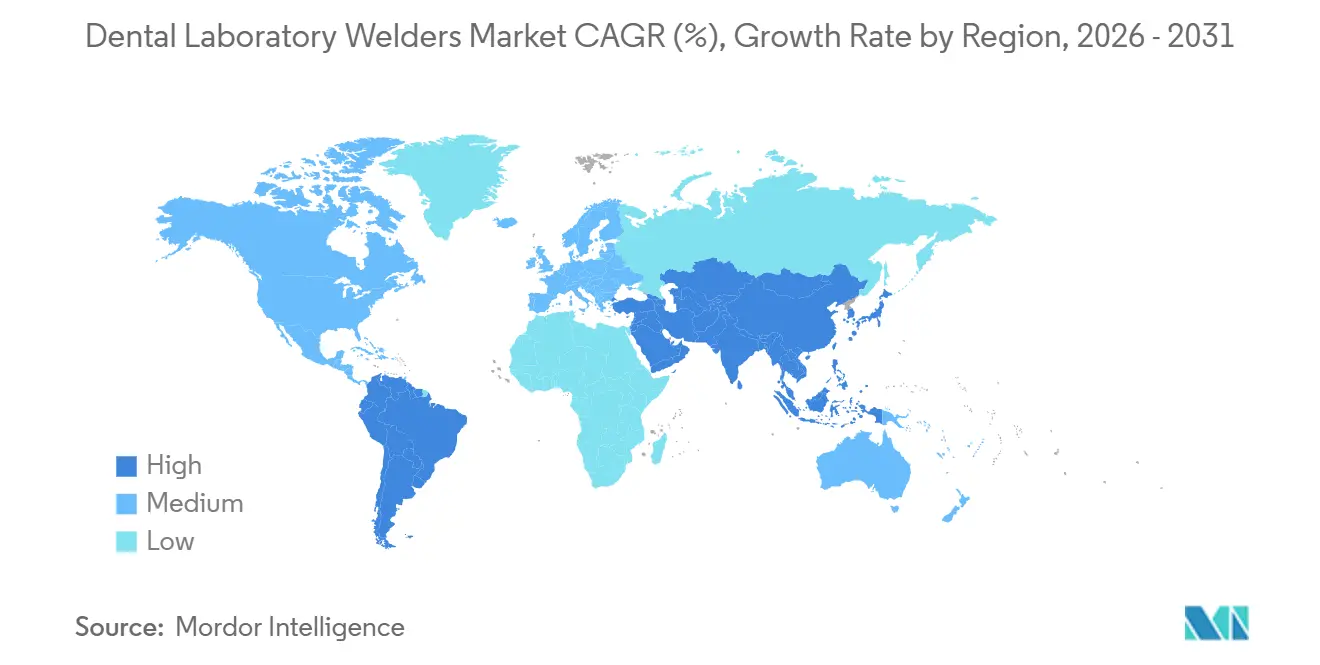

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Dental Laboratory Welders Market Analysis by Mordor Intelligence

The Dental Laboratory Welders Market size is estimated at USD 176.03 million in 2026, and is expected to reach USD 264.14 million by 2031, at a CAGR of 8.45% during the forecast period (2026-2031).

Momentum derives from three converging forces: a larger base of implant-supported restorations, a maturing digital-workflow ecosystem that raises expectations for micron-level accuracy, and a clear cost-of-quality advantage when laser or plasma replaces legacy resistance or TIG welding. Labs that have embraced computer-aided milling and additive manufacturing now need welders who can keep pace with near-net-shape components, boosting demand for automated and robotic platforms. Chairside protocols inside dental clinics further broaden the Dental Laboratory Welders market by bringing compact, portable units into the operatory, shortening case timelines, and opening new revenue streams. Strategic investments in AI-driven parameter optimization add another growth layer by reducing scrap, speeding up training, and unlocking payback on premium equipment.

Key Report Takeaways

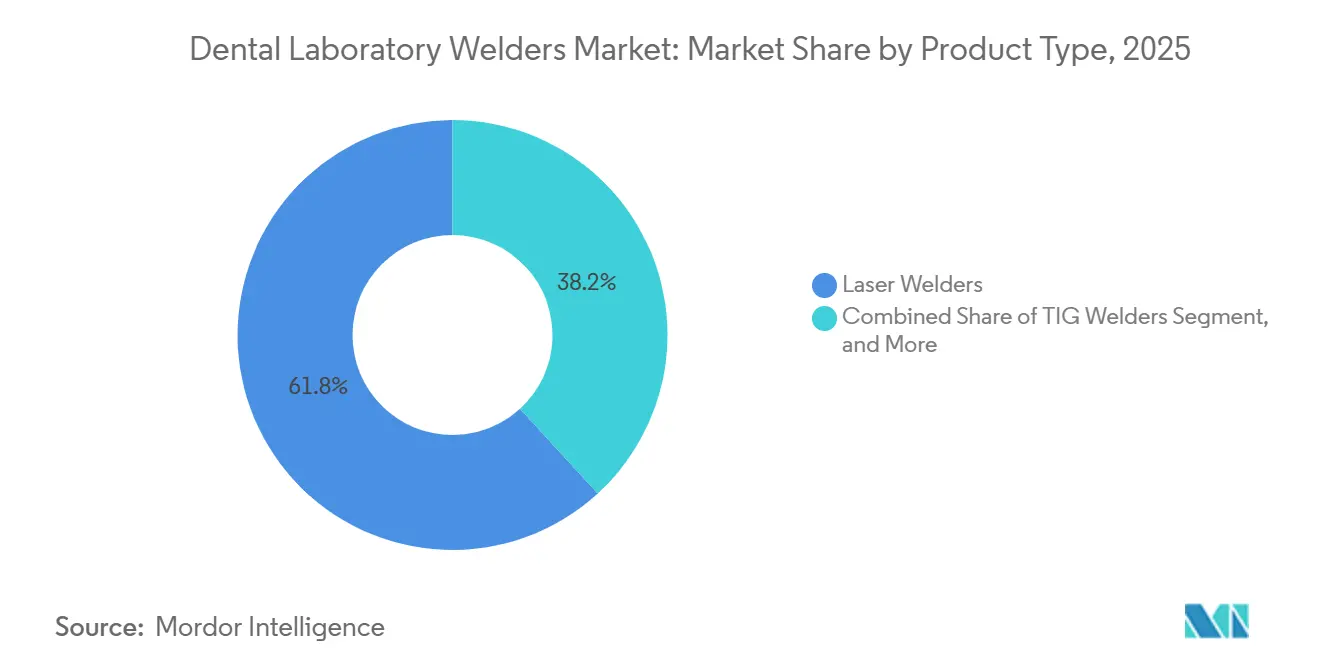

- By product type, laser units led with 61.83% of the dental laboratory welders market share in 2025, while plasma units are set to expand at a 10.34% CAGR to 2031.

- By technology, manual systems held 54.07% of the dental laboratory welders market in 2025, yet automatic and robotic platforms will grow at a 11.31% CAGR during the forecast period.

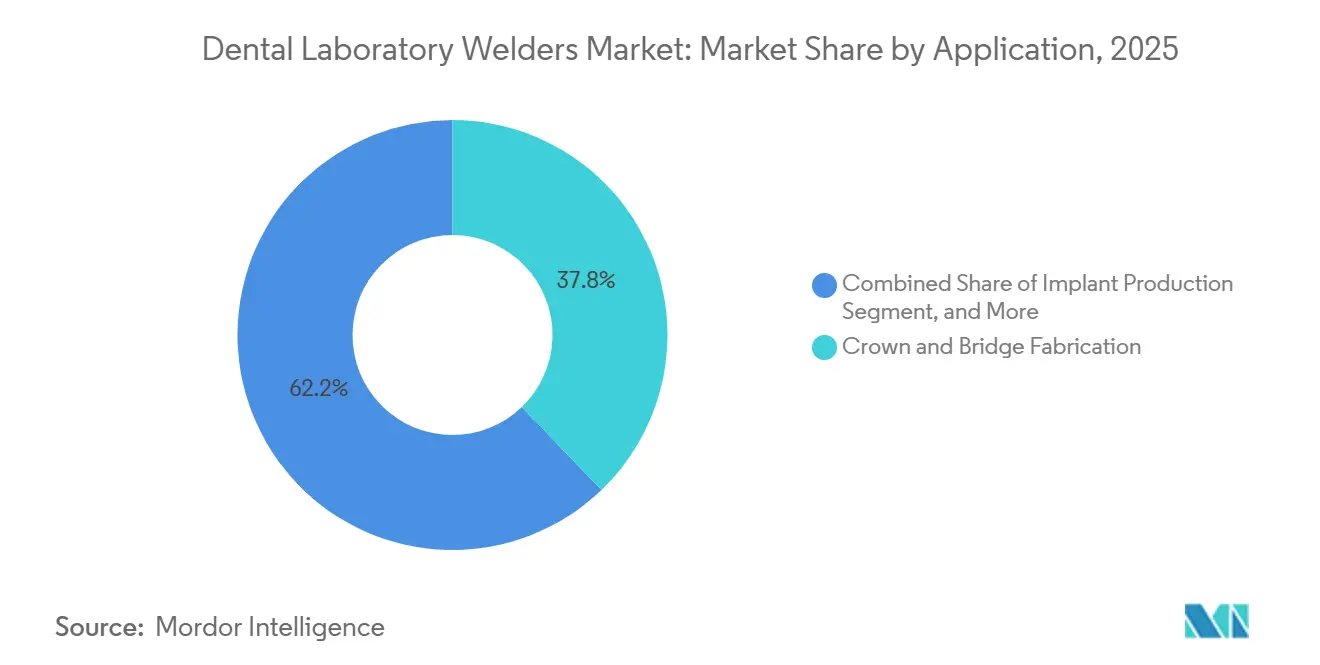

- By application, crown and bridge work delivered 37.82% revenue share in 2025; implant restoration and repair is advancing at a 14.09% CAGR through 2031.

- By end user, dental laboratories accounted for 51.79% of 2025 revenue, but the clinic segment is on track for a 12.02% CAGR, driven by same-day dentistry workflows.

- By geography, North America captured 37.83% of 2025 sales, whereas Asia-Pacific is poised for the fastest 14.93% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Dental Laboratory Welders Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Volume of Implant-Supported Restorations | +2.1% | Global, with concentration in North America, Western Europe, and urban Asia-Pacific hubs | Medium term (2-4 years) |

| Rapid CAD/CAM Adoption in Dental Labs | +1.8% | Global, led by North America and Europe; accelerating in China, India, South Korea | Short term (≤ 2 years) |

| Precision & Lower Re-Work Rates of Laser Welding | +1.5% | Global, particularly North America and EU where labor costs justify premium equipment | Medium term (2-4 years) |

| Proliferation of Portable Chairside Welders | +1.3% | North America, Western Europe, with emerging+ adoption in GCC and urban Latin America | Short term (≤ 2 years) |

| AI-Driven Parameter Optimisation Improving Uptime | +0.9% | North America, Germany, Japan; early pilots in China | Long term (≥ 4 years) |

| Outsourced Refurbishment of High-Value Prosthetics | +0.7% | North America, Western Europe; nascent in Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Volume of Implant-Supported Restorations

Clinical adoption of guided surgery has raised placement accuracy above 90%, widening the candidate pool for multi-unit cases and boosting weld demand.[1]Journal of Prosthodontics, “Guided Implant Surgery and Accuracy Outcomes,” wiley.com United States laboratories alone produced more than 2.3 million implant-supported crowns annually as of 2025, each requiring at least one welded junction. The multiplier effect means equipment often runs for more than two shifts, and manual TIG processes struggle to meet 48-hour turnaround promises. Zirconia abutments bonded to titanium bases impose strict thermal limits, so fiber-laser and micro-plasma platforms dominate because they minimize heat-affected zones. This sustained procedural volume firmly anchors the dental laboratory welders market.

Rapid CAD/CAM Adoption in Dental Labs

Digital workflows reached 68% penetration among North American labs in 2024, with 3D printing trimming lead times by up to 60%.[2]National Association of Dental Laboratories, “2024 Industry Survey,” nadl.org Near-net-shape parts emerging from mills or printers still require welding of clasps or bars, shifting the technician's role toward finishing and inspection rather than wax-up. Stronger lab-clinic data exchange, documented to improve communication by over 70%, and a higher penalty for any weld defect that triggers a remake raise the bar for weld quality. Hybrid machines, such as TRUMPF’s TruPrint 1000, fuse additive and welding processes in a single chamber, cutting total cycle time by 40%. As capital investments amortize with rising volumes, the incremental cost of a precision welder declines, accelerating the replacement of resistance systems and expanding the dental laboratory welders market.

Precision and Lower Rework Rates of Laser Welding

Laser welding produces beads narrower than 0.5 mm with a sub-1 mm heat-affected zone, versus 2–3 mm with TIG, preserving alloy properties and slashing scrap by up to 25%.[3]MDPI, “Laser Welding in Dentistry: Applications and Advantages,” mdpi.com European technicians earning EUR 35 per hour validate a USD 25,000 laser purchase if annual rework hours fall by 200, giving payback within 18 months. Handheld devices like IPG Photonics’ LightWELD also enable intraoral repairs, generating clinic revenue with minimal chair time. The capability profile strengthens the economic case for high-precision equipment and drives unit growth within the dental laboratory welders market.

Proliferation of Portable Chairside Welders

Benchtop units occupy less than 0.3 m² and run on standard power, making them ideal for chairside adjustments and for mobile or rural care settings. Same-day dentistry, now covering about 30% of single-unit anterior restorations in North America, leverages these portable lasers to compress a traditional 7-day cycle into 90 minutes. This functional convenience broadens the buyer base beyond laboratories and injects new demand channels into the dental laboratory welders market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital & Maintenance Cost of Laser Welders | -1.2% | Global, most acute in price-sensitive markets (India, Southeast Asia, Latin America) | Short term (≤ 2 years) |

| Shortage of Skilled Dental Technicians | -0.9% | North America, Western Europe, Japan; emerging in urban China | Medium term (2-4 years) |

| Tightening Limits on In-Lab Particulate Exposure | -0.6% | North America (OSHA), EU (EN standards), Australia | Medium term (2-4 years) |

| Supply Risk for High-Power Laser Diodes | -0.4% | Global, with concentration risk in East Asian semiconductor fabs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capital and Maintenance Cost of Laser Welders

Entry-level lasers start around USD 16,220 and climb to USD 40,000 or more for industrial models, while annual service contracts add 8–12% to the purchase price. In markets where technician wages run USD 3–8 per hour, the business case weakens, prolonging the life of TIG or resistance units. Financing hurdles persist because welders are often viewed as a back-end expense rather than revenue generators. These economic factors temporarily temper adoption, limiting top-line growth in the dental laboratory welders market in price-sensitive regions.

Shortage of Skilled Dental Technicians

Median technician age now exceeds 50 in North America and Western Europe, and enrollment in accredited programs has fallen about 25% over the past decade. Laser welding requires competence in pulse modulation and thermal management, skills beyond traditional training. The limited talent pool inflates wages and leaves smaller labs unable to staff adequately, restricting the pace at which new equipment can be utilized effectively. Automation mitigates the gap but introduces additional capital burden, posing a structural headwind for the dental laboratory welders market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Laser Dominance Masks Plasma’s Precision Gains

Laser systems commanded 61.83% of the dental laboratory welders market in 2025, primarily due to their sub-0.5 mm bead width and controlled heat input, which are well-suited to titanium and cobalt-chromium alloys. The dental laboratory welders market size for plasma units, however, is projected to outpace others with a 10.34% CAGR because micro-plasma torches weld thin zirconia-titanium hybrids without cracking ceramics. TIG units keep a foothold among independent labs in India and Latin America, where lower wages make longer cycle times tolerable. MIG and spot processes remain niche, serving orthodontic appliances and legacy clasp repairs.

Plasma’s renewed relevance rests on torches operating below 10 amps, which allow technicians to weld 0.3 mm titanium foils used in overdenture frameworks. Lower ultraviolet output also eases eye-safety compliance, cutting ancillary costs. Vendors such as Alpha Laser have introduced dual-head machines that toggle between laser and plasma mid-job, reducing setup times by 30%. As zirconia-based esthetic restorations gain favor, plasma welding is set to chip away at lasers’ lead within the Dental Laboratory Welders market.

By Technology: Automation Narrows the Manual-Skill Premium

Manual equipment still held 54.07% of the dental laboratory welders market share in 2025, reflecting the global installed base of small laboratories. Yet automated and robotic platforms will post an 11.31% CAGR as service organizations centralize 500–1,000 weekly cases under one roof. Automatic cells deliver ±0.1 mm positional repeatability and integrate inspection cameras that cut rework.

Portable and desktop lasers meet the needs of clinics seeking chairside workflows. Units such as IPG’s LightWELD or Sunstone’s Orion LZR achieve payback inside 18 months at modest monthly volumes. Manual systems will persist where case geometry varies widely, but AI-assisted vision is improving each year, gradually eroding that safe harbor. The technology mix, therefore, continues to evolve, adding volume and diversity to the dental laboratory welders market.

By Application: Implant Repair Outpaces New Fabrication

Crown and bridge cases generated 37.82% of 2025 revenue, yet implant restoration and repair is growing faster at 14.09% CAGR, lifted by the expanding installed base of implants placed over the last two decades. The dental laboratory welders market size for implant components also benefits from guided-surgery protocols that need custom abutments and bars.

Repair economics favor welding: a full-arch replacement can exceed USD 3,000, whereas repair costs a fraction of that. Outsourcing partners using robotic welding cells process complex refurbishments within 48 hours, freeing in-house capacity for higher-margin new work. Intraoral laser units further compress timelines by repairing fractures without removing prosthetics, tightening the clinic-laboratory loop, and invigorating demand in the dental laboratory welders market.

By End-User: Clinics Gain as Chairside Capabilities Mature

Dental laboratories retained 51.79% of 2025 revenue, but clinics will record a 12.02% CAGR as chairside mills and portable lasers enable single-visit restorations. Clinics adopting portable systems can weld fractured clasps in-office, eliminating shipment delays and capturing incremental revenue.

Hospitals and academic centers hold roughly one-fifth of sales because residency programs incorporate digital welding modules into training. Laboratories respond by moving up the complexity ladder, investing in robotic cells to handle multi-unit bars and complex frameworks. This specialization keeps them relevant even as clinics secure a growing slice of the dental laboratory welders market.

Geography Analysis

North America accounted for 37.83% of 2025 sales and maintains leadership through consolidated dental service organizations that operate centralized labs equipped with robotic welders. FDA Class II regulations extend product-launch cycles by up to 18 months, moderating the pace at which AI-enabled welders hit the market. Same-day dentistry has penetrated almost one-third of anterior single-unit cases, prompting clinics to purchase handheld lasers and benchtop platforms. Canada and Mexico add price arbitrage traffic; labs in border cities serve U.S. patients seeking lower fees, further expanding the regional dental laboratory welders market.

Asia-Pacific is the fastest-growing region, with a 14.93% CAGR, buoyed by China’s dental device expansion from RMB 71.2 billion in 2024 to RMB 166.7 billion by 2030. India, Thailand, and Malaysia ride a medical tourism wave, investing in laser welders to serve inbound patients at 40–60% lower prices than Western prices. Japan and South Korea capture premium segments that demand ±0.1 mm repeatability, and their higher wage levels make automation economically sensible. Lower wages in India and parts of Southeast Asia slow laser adoption, yet overall procedure volumes lift the Dental Laboratory Welders market across the region.

The Medical Device Regulation tightens post-market surveillance, favoring vendors with ISO 13485 systems and slowing the entry of low-cost manufacturers. EN particulate limits mirror U.S. OSHA rules, pressuring labs to upgrade extraction when using TIG and driving migration toward laser and plasma systems that emit fewer particulates. Southern Europe’s fragmented lab landscape limits capital absorption, but Northern Europe’s automation push offsets that weakness and sustains the dental laboratory welders market.

Competitive Landscape

Five leading suppliers, IPG Photonics, Alpha Laser, Sisma, LaserStar Technologies, and Sunstone Engineering, indicate a moderately concentrated dental laboratory welders market. IPG’s in-house diode production shortens lead times by roughly 25% when supply chains tighten, giving it an edge during allocation shortages. Sunstone and LaserStar target the benchtop and portable tiers, with prices ranging from USD 16,220 to USD 22,500, winning small-lab and chairside accounts.

Software is becoming the main battleground. Vendors bundling cloud dashboards for utilization tracking and predictive maintenance gain stickiness that commodity hardware alone cannot secure. TRUMPF’s hybrid TruPrint 1000 merges additive and welding processes in a single cell, compressing production steps and setting a benchmark for integrated workflows. New entrants from China and South Korea offer private-label lasers at discounts up to 40%, courting labs in price-sensitive geographies, but still lag on certification depth and after-sales service. Compliance costs under ISO 13485 and IEC 60601-1 remain a barrier, making scale and regulatory expertise valuable assets in the dental laboratory welders market.

Dental Laboratory Welders Industry Leaders

Ivoclar

Primotec

LaserStar Technologies

IPG Photonics

Schütz Dental

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Catalis Dental Lab Partners ("Catalis") announced two significant milestones in its nationwide expansion: the acquisition of Revolution Dental Lab in Sandy, Utah, and the opening of a new East Coast Digital Design Center in Jacksonville, Florida.

- May 2025: Dandy released Live Design Review, a real-time video collaboration feature that connects dentists with lab technicians during crown design.

- May 2025: Leixir and Heartland Dental renewed a four-year agreement covering laboratory services for more than 3,000 supported dentists nationwide.

Global Dental Laboratory Welders Market Report Scope

Dental laboratory welders are specialized precision welding devices used in dental laboratories to join, repair, or fabricate metallic components of dental restorations and prostheses. These systems enable high-accuracy, low-heat welding of materials such as cobalt-chromium, titanium, stainless steel, gold alloys, and other dental alloys commonly used in crowns, bridges, frameworks, implant abutments, partial dentures, orthodontic appliances, and implant-supported restorations.

The Dental Laboratory Welders Market Report is Segmented by Product Type (Laser Welders, TIG Welders, MIG Welders, Plasma Welders, Spot Welders), Technology (Manual, Automatic/Robotic, Portable/Desktop), Application (Crown & Bridge Fabrication, Implant Production, Implant Restoration & Repair, Other Applications), End-user (Dental Laboratories, Dental Clinics, Hospitals, Academic & Research Institutes), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

| Laser Welders |

| TIG Welders |

| MIG Welders |

| Plasma Welders |

| Spot Welders |

| Manual |

| Automatic/Robotic |

| Portable/Desktop |

| Crown & Bridge Fabrication |

| Implant Production |

| Implant Restoration & Repair |

| Other Applications (Orthodontic Component Welding, Partial Denture Frameworks, etc.) |

| Ambulatory Surgical Centers |

| Dental Laboratories |

| Dental Clinics |

| Hospitals |

| Academic & Research Institutes |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Laser Welders | |

| TIG Welders | ||

| MIG Welders | ||

| Plasma Welders | ||

| Spot Welders | ||

| By Technology | Manual | |

| Automatic/Robotic | ||

| Portable/Desktop | ||

| By Application | Crown & Bridge Fabrication | |

| Implant Production | ||

| Implant Restoration & Repair | ||

| Other Applications (Orthodontic Component Welding, Partial Denture Frameworks, etc.) | ||

| Ambulatory Surgical Centers | ||

| By End-user | Dental Laboratories | |

| Dental Clinics | ||

| Hospitals | ||

| Academic & Research Institutes | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the dental laboratory welders market?

The dental laboratory welders market size stood at USD 176.03 million in 2026 and is forecast to reach USD 264.14 million by 2031.

How fast is demand for plasma welders growing relative to laser systems?

Plasma welders are projected to post a 10.34% CAGR through 2031, outpacing the broader market and gaining share in zirconia-hybrid applications.

Which region is expected to expand the fastest?

Asia-Pacific is forecast to grow at a 14.93% CAGR, driven by China’s rapid investment in dental devices and the growth of medical tourism across India and Southeast Asia.

Why are clinics becoming a larger buyer of welding equipment?

Portable chairside laser units enable same-day crown repairs and adjustments, providing clinics with a 12.02% CAGR growth path as they integrate milling and welding into the operatory.

What is the main factor that restrains small laboratories from upgrading to lasers?

High upfront costs starting at USD 16,220 and ongoing maintenance contracts add 8–12% annually, stretching budgets for micro-labs with fewer than 3 technicians.

Page last updated on: