Dental Impression Materials Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

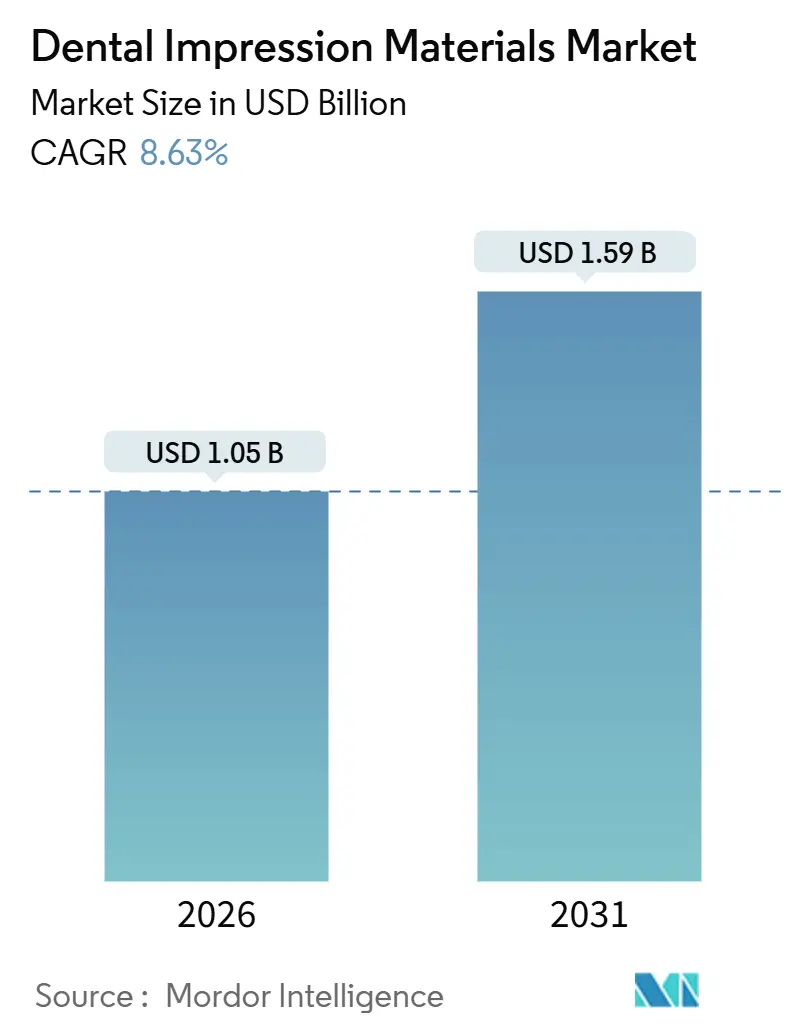

| Market Size (2026) | USD 1.05 Billion |

| Market Size (2031) | USD 1.59 Billion |

| Growth Rate (2026 - 2031) | 8.63% CAGR |

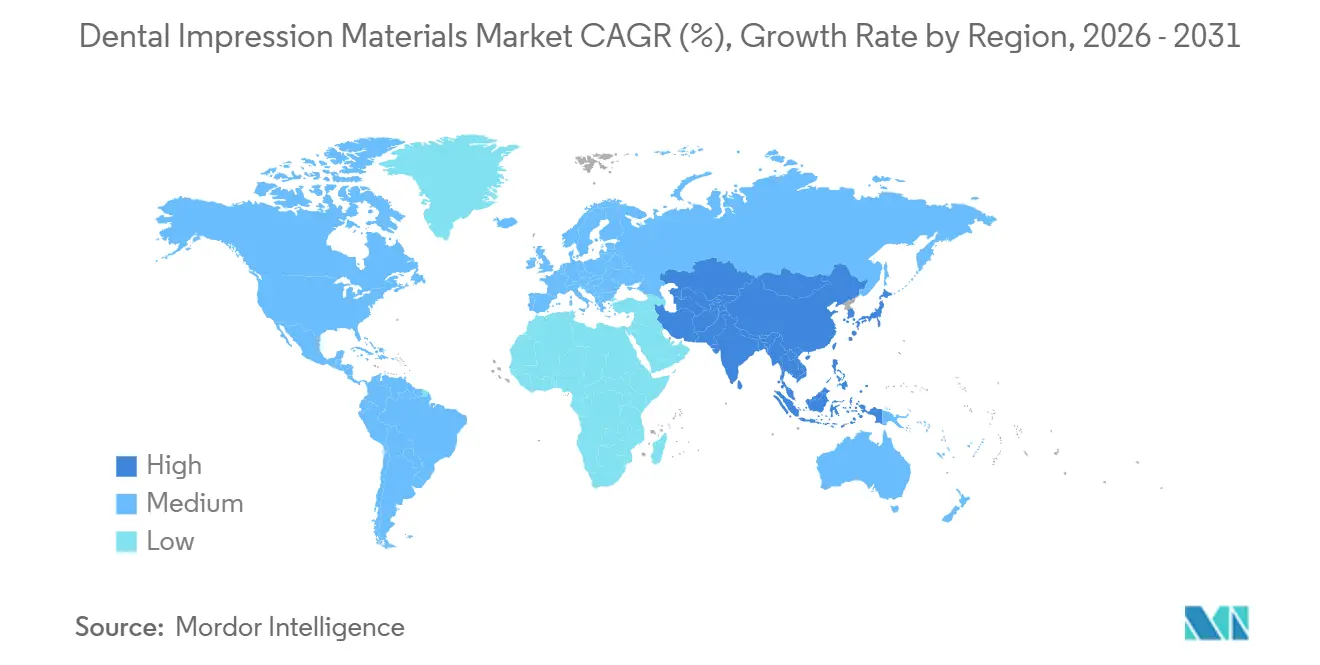

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

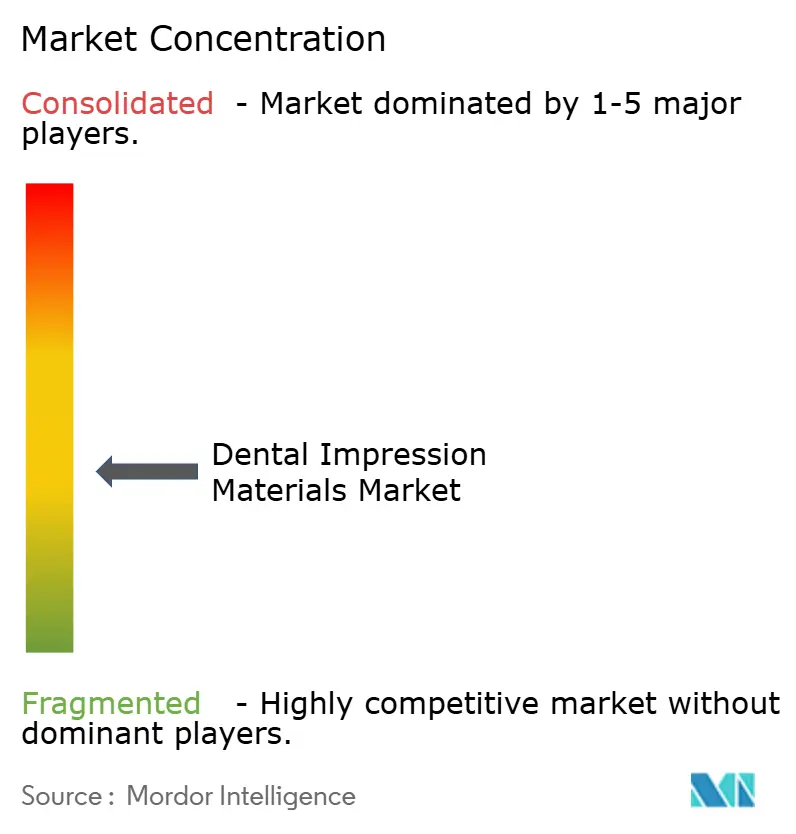

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Dental Impression Materials Market Analysis by Mordor Intelligence

The dental impression materials market is estimated at USD 1.05 billion in 2026. It is projected to reach USD 1.59 billion by 2031, advancing at an 8.63% CAGR during the forecast period, confirming steady expansion in market size and sustained momentum in demand. Growth is tied to the coexistence of conventional elastomeric lines with digital intraoral-scanner workflows, tighter dimensional-stability standards under ISO 4823:2025, and the accelerating volume of implant and cosmetic procedures. Vinyl polysiloxane, polyether, and scannable hybrids are gaining ground because they meet the U.S. Food and Drug Administration's performance criteria issued in September 2024[1]U.S. Food and Drug Administration, “Performance Criteria for Dental Impression Materials,” fda.gov . Asia-Pacific leads volume gains driven by rising disposable incomes, while North America continues to generate the largest revenue share due to high adoption of premium materials and technology bundles. Competitive intensity remains moderate, yet private-equity ownership in distribution and manufacturing broadens cross-selling reach and reinforces pricing discipline. White-space opportunities lie in formulations that bridge analog precision with direct digitization, keeping the dental impression materials market on an upward trajectory.

Key Report Takeaways

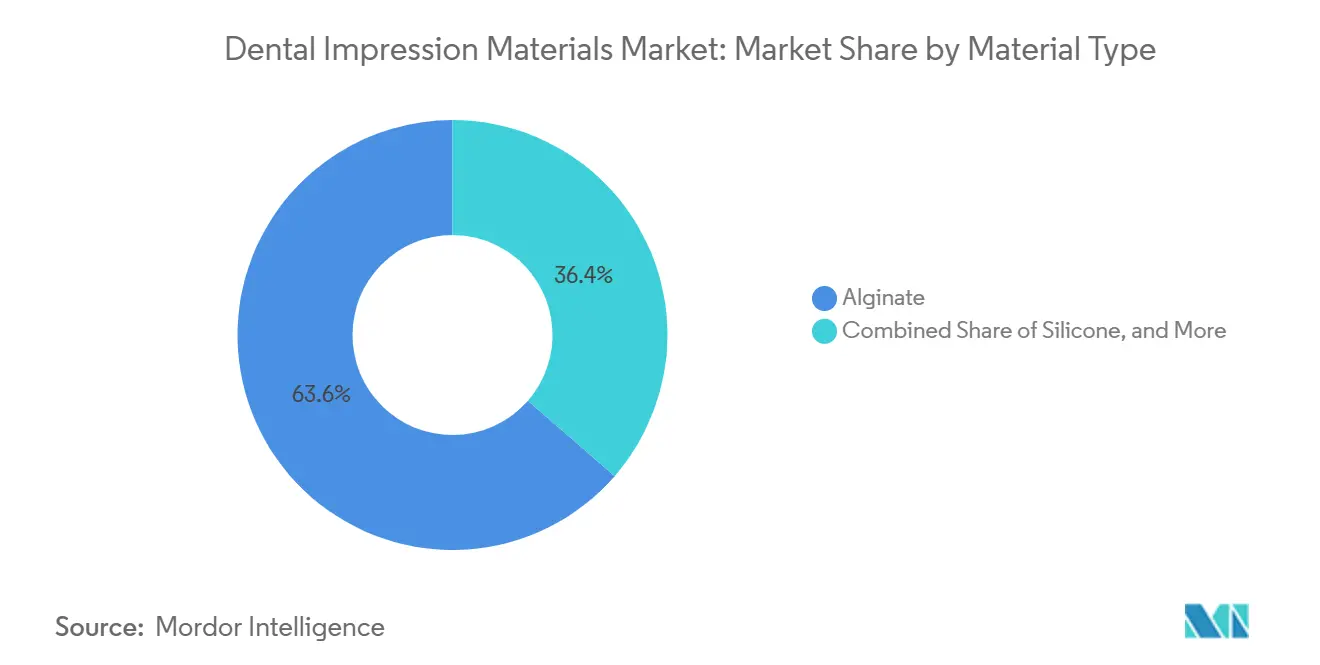

- By material type, alginate led with 63.55% market share in dental impression materials in 2025, while vinyl polysiloxane is advancing at a 9.25% CAGR through 2031 and is the fastest-growing material segment.

- By application, restorative and prosthodontics accounted for 42.53% of revenue in 2025; implantology is expanding at a 9.85% CAGR and is the fastest-growing application.

- By end user, hospitals and clinics accounted for 59.23% of 2025 revenue, yet dental laboratories are growing at an 8.85% CAGR and are the most dynamic channel.

- By geography, North America accounted for 38.13% of revenue in 2025, while Asia-Pacific is forecast to grow at a 9.21% CAGR and is the fastest-growing regional market.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Dental Impression Materials Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Incidence of Dental Disorders | +1.8% | Global, with acute needs in North America and aging populations in Europe and Japan | Medium term (2–4 years) |

| Growing Demand for Cosmetic & Restorative Dentistry | +2.1% | North America, Europe, urban Asia-Pacific (China tier-1 cities, South Korea) | Short term (≤ 2 years) |

| Technological Advances in Impression Materials | +1.5% | Global, with R&D hubs in Germany, United States, Japan | Long term (≥ 4 years) |

| Rapid Adoption of Digital and CAD/CAM-Compatible Workflows | +1.9% | North America, Europe, Australia; spillover to Asia-Pacific dental laboratories | Medium term (2–4 years) |

| Shift toward Eco-Friendly, Sustainable Formulations | +0.7% | Europe (REACH compliance), North America (green procurement policies) | Long term (≥ 4 years) |

| Regional Manufacturing Realignment due to Trade-Tariff Pressures | +0.6% | North America, Europe; supply-chain diversification from China to Mexico, Vietnam | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Incidence of Dental Disorders

Untreated caries and periodontal disease drive higher restorative volumes that depend on accurate impressions. The 2024 National Health and Nutrition Examination Survey reported 20.5% untreated dental decay among U.S. adults aged 20–64 and 15.2% edentulism among seniors, both trends that are steering prosthodontic demand[2]Centers for Disease Control and Prevention, “NHANES 2024 Oral Health Data,” cdc.gov. Implant-supported overdentures require multiple impression stages, and polyether and vinyl polysiloxane materials exhibit 0.05% dimensional change over 7 days, ensuring precision in these complex cases[3]Journal of Prosthetic Dentistry, “Dimensional Stability of Polyether Impressions,” jprosthdent.org. Japan’s population aged 65+ reached 28.8% in 2024, reinforcing regional case loads in geriatric prosthodontics[4]Ministry of Health, Labour and Welfare, “Population Statistics 2024,” mhlw.go.jp.

Growing Demand for Cosmetic and Restorative Dentistry

Social media visibility and rising acceptance of elective procedures have propelled global cosmetic dentistry to a projected USD 56.64 billion by 2034, with annual growth of 7.1%[5]American Academy of Cosmetic Dentistry, “Global Cosmetic Dentistry Analysis 2024–2034,” aacd.com. Hydrophilic VPS captures marginal detail in veneers and all-ceramic crowns, while the new vinyl-polyether silicone maintains dimensional accuracy after disinfectant immersion, supporting laboratory throughput. Higher volumes justify investment in premium VPS systems that shorten chair time, improving patient satisfaction and referral rates.

Technological Advances in Impression Materials

Material science targets shorter setting time and higher tear strength while enabling direct digitization from the impression. Color-shift alginates reduce operator error, and extra-fast VPS sets intraorally in 45 seconds, saving clinical minutes at scale. Desktop scanners now digitize impressions at 20-micron resolution, allowing laboratories to design restorations virtually before pouring models.

Rapid Adoption of Digital and CAD/CAM-Compatible Workflows

Although 39% of laboratory cases arrive as digital scans, 61% still depend on physical impressions, partly because scanners struggle with full arches and edentulous tissue. Hybrid workflows optimize cost by combining conventional impressions taken in clinics with digital design and manufacturing in laboratories, thereby sustaining material demand while elevating accuracy. Partnerships that merge impression materials, printers, and software support this convergence.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost & Limited Reimbursement for Advanced Treatments | -1.4% | Global, acute in United States (private insurance gaps) and emerging markets (out-of-pocket burden) | Short term (≤ 2 years) |

| Substitution Risk from Chairside Intra-Oral Scanning Systems | -1.1% | North America, Europe, urban Asia-Pacific (high scanner penetration in group practices) | Medium term (2–4 years) |

| Dimensional Instability of Traditional Alginate Materials | -0.5% | Global, particularly in humid climates (Southeast Asia, Latin America) | Medium term (2–4 years) |

| Stringent Biocompatibility & Chemical-Safety Regulations | -0.8% | Europe (REACH, MDR 2017/745), North America (FDA premarket review), Japan (PMDA) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Cost and Limited Reimbursement for Advanced Treatments

Typical U.S. dental plans cover only 50% of primary restorative care, and annual maximums of USD 2,000 have not changed in decades, so many patients defer or skip treatment. A 2024 American Dental Association survey found that 32% of adults postponed dental care due to cost, thereby directly lowering impression material volumes.

Substitution Risk from Chairside Intraoral Scanning Systems

Clinical trials show scanners achieve trueness of 0.082 mm versus 0.132 mm for VPS in single-unit crowns, which encourages switch-over in high-volume practices. Yet scanners still struggle with edentulous arches and subgingival margins, so total substitution remains partial. The risk subtracts 1.1 percentage points from the dental impression materials market CAGR.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: VPS Momentum Continues

Alginate accounted for 63.55% dental impression materials market share in 2025, a reflection of low cost and adoption in preliminary casts. Vinyl polysiloxane is advancing at a 9.25% CAGR through 2031, propelled by implant and cosmetic cases that demand sub-50-micron fidelity. Tight ISO 4823:2025 limits reinforce this shift, while polyether holds a stable niche for full-arch implant impressions. Cost-sensitive orthodontic and training settings sustain alginate volumes, but premium segments increasingly select VPS.

VPS gains amplify value growth despite alginate’s volume dominance. Hybrid VPS offers matte finishes that allow direct scanning, bridging analog capture with digital manufacturing. These capabilities underpin rising share for elastomers that meet ISO Type 0 accuracy requirements. Consequently, the dental impression materials market size for VPS is projected to account for a growing portion of total revenue by 2031.

By Application: Implantology Outpaces Restorative Workflows

Restorative and prosthodontics contributed 42.53% of revenue in 2025 and will continue to expand due to aging populations and steady crown and bridge volumes. Implantology, however, is the fastest-growing application at a 9.85% CAGR, since every implant requires multiple precision impressions and premium elastomers. Polyether and VPS rigidity prevents coping movement during removal, securing angular fidelity for implant analogs. As single-tooth and full-arch implants become first-line solutions, the dental impression materials market size allocated to implantology will rise sharply.

Orthodontic aligner makers increasingly use direct scans, which trims per-case material use, yet the segment’s overall growth still adds incremental volumes in regions where scanners remain unaffordable. Forensic, bite registration, and niche uses round out the application mix but add minimal incremental growth.

By End User: Laboratories Accelerate Digital Uptake

Hospitals and clinics purchased 59.23% of material volumes in 2025, since impressions originate chairside. Laboratories, however, are growing at an 8.85% CAGR, driven by investments in scanners that digitize impressions and 3D printers that fabricate models rapidly. As labs digitize, they still rely on high-accuracy physical impressions for full-arch work, reinforcing demand for premium elastomers.

Academic institutes remain small but influential in validating new formulations, such as printed custom trays that reduce material waste by 18% and improve patient comfort by 22%. Clinics will continue to balance scanner adoption with impression purchases, while laboratories accelerate hybrid workflows, supporting steady sales growth across channels.

Geography Analysis

North America accounted for 38.13% of 2025 revenue, driven by high implant volumes and early adoption of fast-setting VPS. FDA guidance that references ISO 4823:2025 has raised compliance costs, creating an entry barrier that favors incumbents. Near-shoring to Mexico shortens lead times and mitigates tariff risk, maintaining a steady supply.

Asia-Pacific is expanding at a 9.21% CAGR due to rising incomes, dental tourism hubs, and government oral health funding in China and India. Japan’s aging population intensifies demand for full-arch prosthodontics, while locally engineered scanners tailored to smaller arch dimensions encourage balanced growth of both physical and digital impressions.

Europe benefits from robust dental insurance systems, but grows more slowly than Asia-Pacific because MDR 2017/745 and REACH compliance add costs, restraining growth in price-sensitive segments. Sustainable, solvent-free elastomers are gaining traction with institutional buyers under ESG mandates. The Middle East and Africa register mid-single-digit market shares but benefit from state-funded implant programs in Saudi Arabia that spur the adoption of premium materials. South America leans on domestic alginate production in Brazil and Argentina to offset currency swings, which caps premium uptake but secures baseline volumes.

Competitive Landscape

The dental impression materials market shows moderate concentration. The top five suppliers—Dentsply Sirona, Envista (under Ares Management), GC Corporation, Ivoclar Vivadent, and Coltene—offer vertically integrated portfolios, spanning impression materials and digital equipment. Envista’s USD 4.6 billion sale to Ares Management in September 2024 enables cross-selling of KaVo Kerr materials and scanners through consolidated distribution. Patterson Companies joined the consolidation when Patient Square Capital acquired it for USD 4.1 billion in December 2024, adding distribution scale that locks in volume rebates.

Innovation centers on scannable VPS and polyether lines that meet ISO Type 0 accuracy. Kerr’s Take 1 Advanced VPS sets in 45 seconds, supporting same-day restorative workflows. Zhermack emphasizes user-friendly color-change alginate, while Kettenbach’s Visalys Temp One-to-One, launched in September 2025, underscores the convenience of single-use mixing. Partnerships, exemplified by Ivoclar and SprintRay, integrate resins and digital design platforms, reinforcing hybrid workflow adoption.

Emerging niches include AI-enhanced scanner software that flags margin capture errors in real time, thereby reducing remakes and material waste. Regulatory hurdles under MDR 2017/745 and FDA 510(k) processes enforce clinical evidence requirements, so smaller innovators often license technology to incumbents instead of building standalone distribution.

Dental Impression Materials Industry Leaders

Dentsply Sirona

GC Corporation

Ivoclar Vivadent

Coltene Holding

Envista Holdings

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Kettenbach Dental introduced VISALYS Temp One-to-One, a time-saving provisional material for chairside workflows.

- March 2025: Ivoclar Vivadent partnered with SprintRay to co-develop printable denture resins optimized for digital design from elastomeric impressions.

- September 2024: The FDA released updated performance criteria mandating ISO 4823:2025 compliance for new impression materials.

Global Dental Impression Materials Market Report Scope

As per the report's scope, dental impression materials are substances used in dentistry to create an accurate negative replica of a patient’s teeth, gums, and oral tissues. These materials capture fine surface details and set within a short time after placement in the mouth. The resulting impression is used to fabricate dental restorations, prostheses, orthodontic appliances, and study models.

The dental impression materials market segmentation includes material type, application, end user, and geography. By material type, the market is segmented into alginate, silicone, polyether, vinyl polysiloxane (VPS), and others. By application, the market is segmented into restorative & prosthodontics, orthodontics, implantology, and others. By end user, the market is segmented into dental hospitals and clinics, dental laboratories, and academic & research institutes. By geography, the global market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD) for the above segments.

| Alginate |

| Silicone |

| Polyether |

| Vinyl Polysiloxane (VPS) |

| Others |

| Restorative & Prosthodontics |

| Orthodontics |

| Implantology |

| Others |

| Dental Hospitals and Clinics |

| Dental Laboratories |

| Academic & Research Institutes |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Material Type | Alginate | |

| Silicone | ||

| Polyether | ||

| Vinyl Polysiloxane (VPS) | ||

| Others | ||

| By Application | Restorative & Prosthodontics | |

| Orthodontics | ||

| Implantology | ||

| Others | ||

| By End User | Dental Hospitals and Clinics | |

| Dental Laboratories | ||

| Academic & Research Institutes | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the dental impression materials market?

The market stands at USD 1.05 billion in 2026 and is projected to reach USD 1.59 billion by 2031.

Which material segment is growing fastest in dental impressions?

Vinyl polysiloxane is the fastest-growing segment with a 9.25% CAGR through 2031.

Why are dental laboratories seeing higher growth than clinics?

Laboratories are investing in scanners and printers that digitize impressions, which boosts throughput and raises material purchases.

How does digital scanning affect demand for traditional impression materials?

Scanners substitute part of single-unit work, yet physical impressions remain necessary for full-arch and implant cases, so overall demand persists.

What regulations influence impression material development in the United States?

FDA guidance from September 2024 requires compliance with ISO 4823:2025 for new elastomeric materials, tightening dimensional-stability thresholds.

Which region is expected to grow fastest for impression materials sales?

Asia-Pacific is projected to expand at a 9.21% CAGR through 2031, driven by rising disposable income and government-backed oral-health programs.

Page last updated on: