Dental Compressors Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

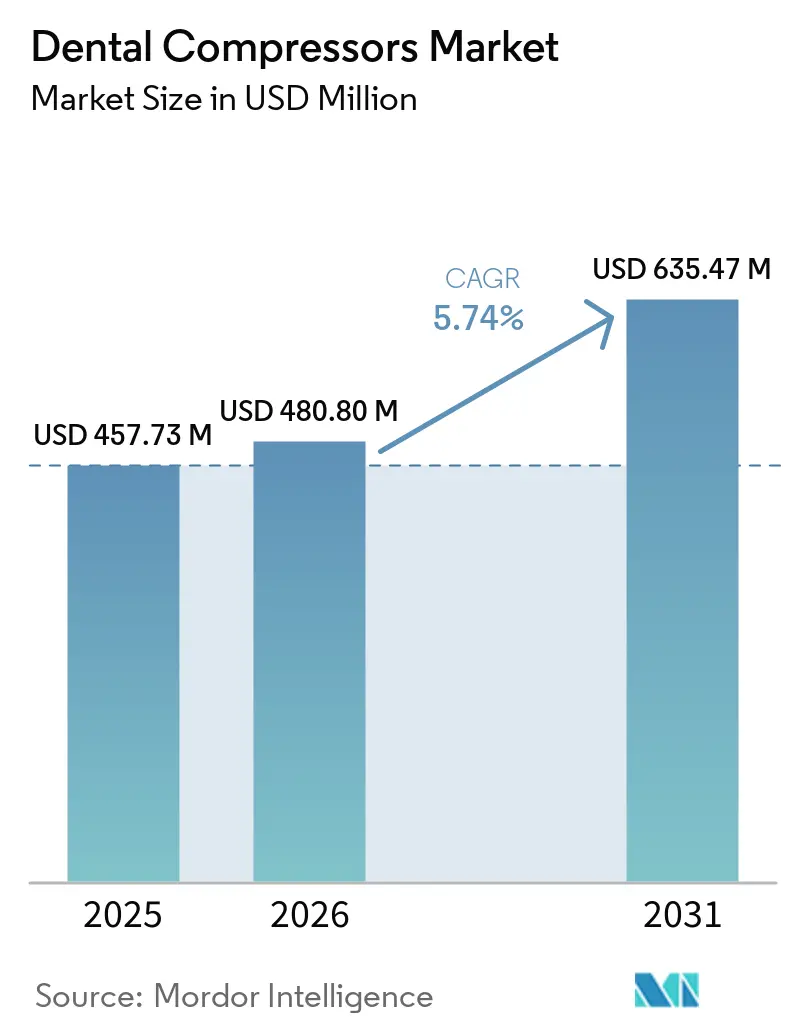

| Market Size (2026) | USD 480.80 Million |

| Market Size (2031) | USD 635.47 Million |

| Growth Rate (2026 - 2031) | 5.74% CAGR |

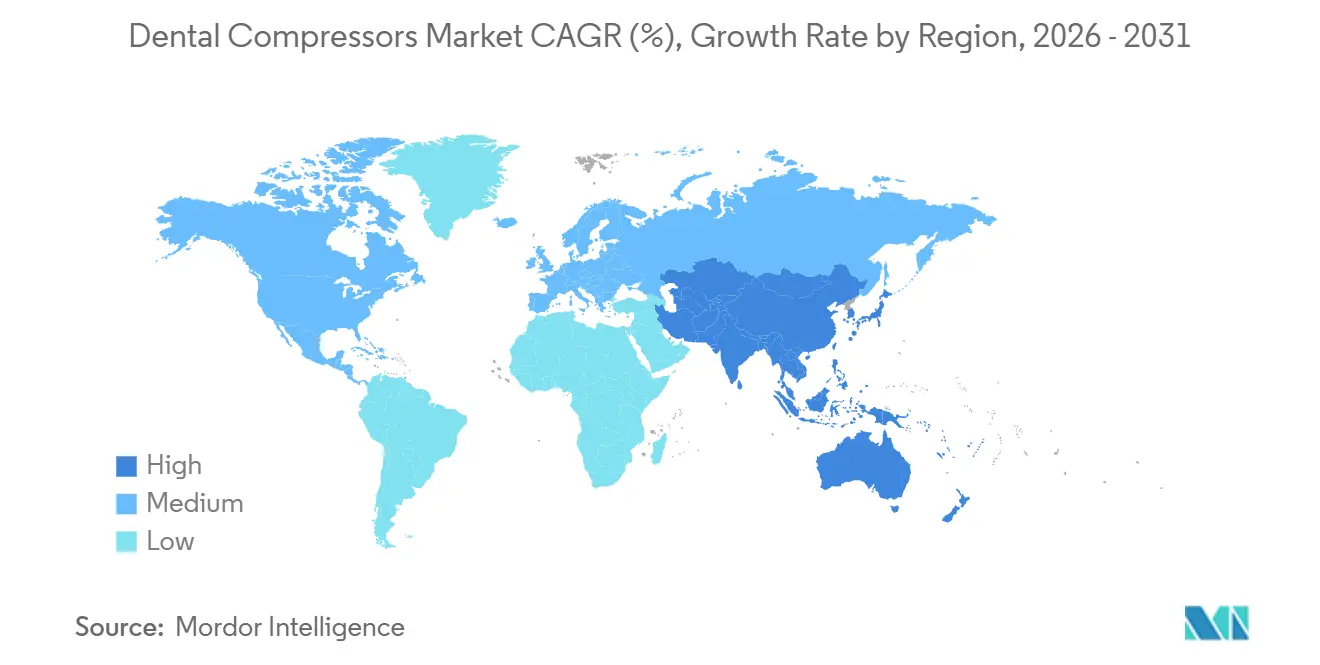

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Dental Compressors Market Analysis by Mordor Intelligence

The Dental Compressors Market size was valued at USD 457.73 million in 2025 and is estimated to grow from USD 480.80 million in 2026 to reach USD 635.47 million by 2031, at a CAGR of 5.74% during the forecast period (2026-2031).

Stricter infection control rules and clearer classification of clinical compressed air as a regulated input have shifted procurement toward oil free systems that deliver clean and dry air across routine and advanced dental workflows. The dental compressors market is also benefiting from DSO network growth that standardizes equipment specifications at scale and favors vendors with nationwide service and digital monitoring capabilities, which supports more predictable uptime and documentation. Growth in CAD/CAM milling and other digital dentistry workloads requires ultra dry, stable supply with lower dew points than older dryer technologies can sustain, prompting upgrades in clinics and labs that run longer duty cycles. Subscription models and IoT monitoring add predictable costs and earlier interventions, which reduce emergency callouts and strengthen vendor relationships, further supporting long term demand in the dental compressors market.

Key Report Takeaways

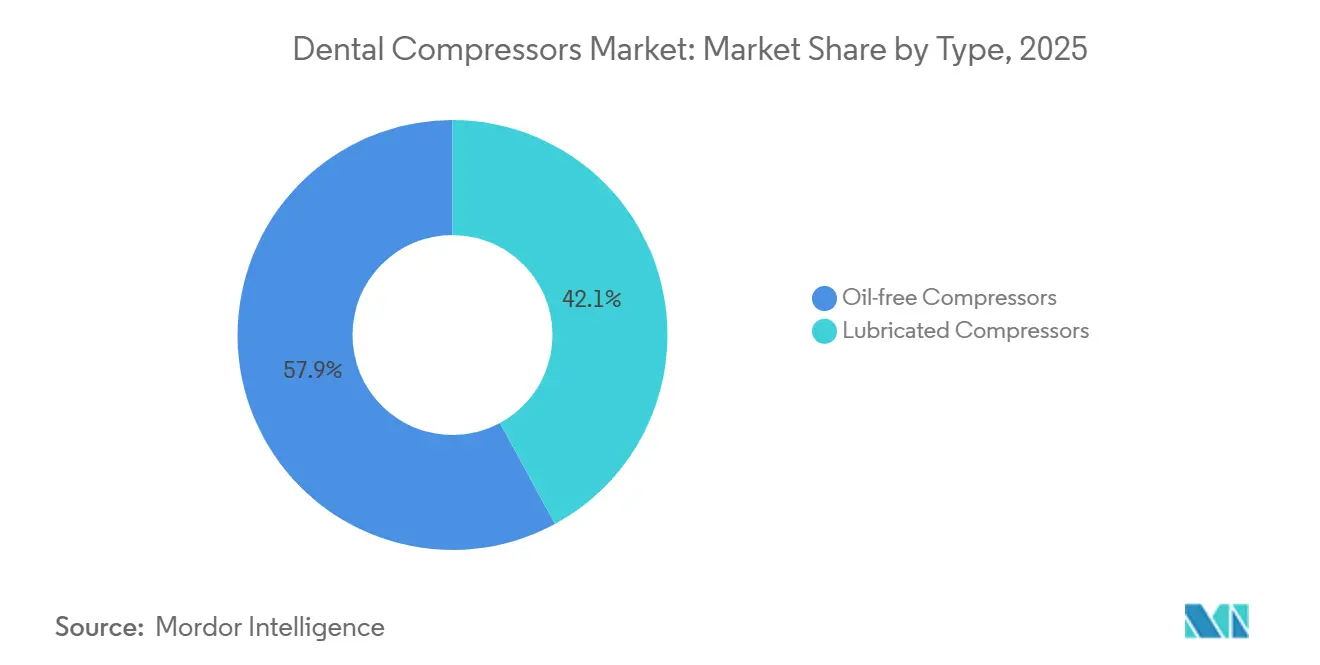

- By type, oil free systems led with 57.9% revenue share in 2025. Lubricated units are projected to expand at a 6.24% CAGR through 2031.

- By technology, desiccant based systems commanded 64.65% share in 2025 and are projected to grow at a 5.95% CAGR through 2031.

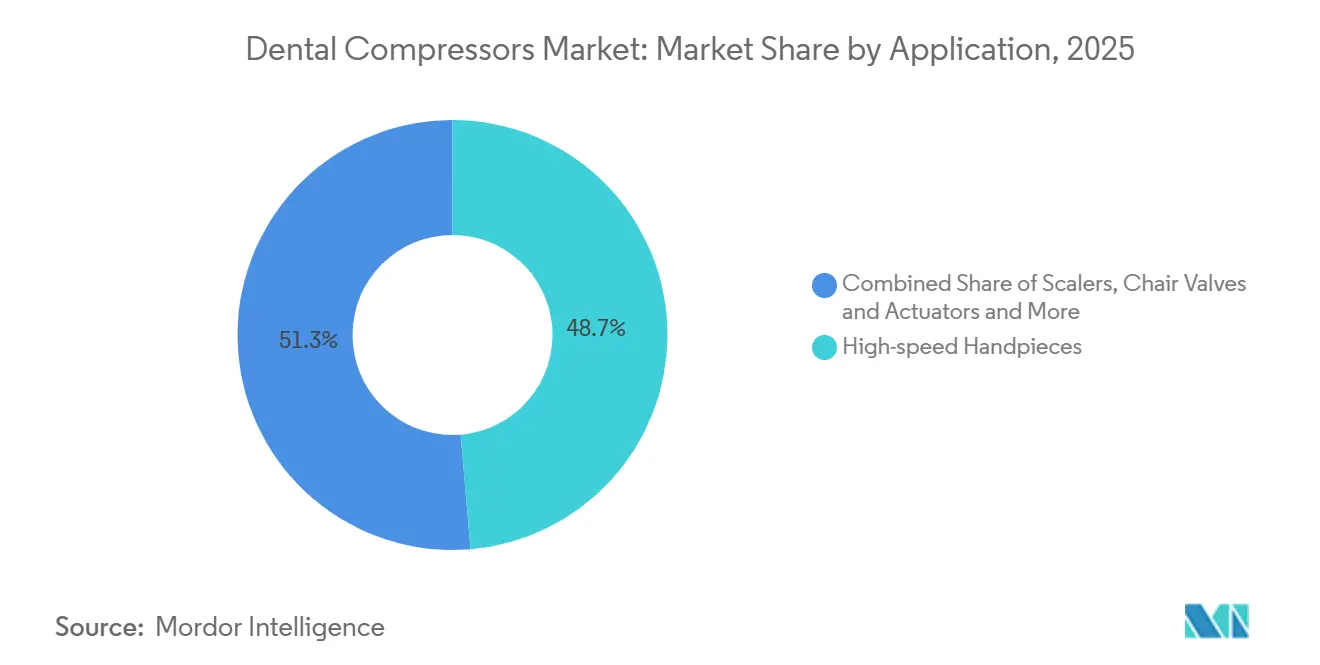

- By application, high speed handpieces accounted for 48.67% share in 2025 and are advancing at a 6.02% CAGR through 2031.

- By end user, dental clinics and hospitals held 43.56% share in 2025 and are projected to grow at a 6.12% CAGR through 2031.

- By geography, North America held 47.42% share in 2025, while Asia Pacific is projected at a 6.36% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Dental Compressors Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Infection‑control shift to oil‑free, clean, dry air | +1.2% | Global, with accelerated enforcement in EU (MDR) and U.S. (FDA) | Medium term (2-4 years) |

| Rising dental procedures and equipment upgrades | +0.9% | North America, Europe core, spillover to APAC urban corridors | Medium to long term (3+ years) |

| DSO consolidation and multi‑chair clinic expansion | +1.4% | North America dominance, nascent in Western Europe and GCC | Short to medium term (≤ 3 years) |

| Regulatory standards elevating air‑quality requirements | +0.8% | U.S. (FDA 510(k)), EU (MDR), NHS England (HTM 2022), Australia (AS 2896:2021) | Medium term (2-4 years) |

| CAD/CAM milling needs ultra‑dry, stable compressed air | +0.6% | Global labs, concentrated in Germany, Italy, U.S., China manufacturing hubs | Medium to long term (3+ years) |

| Predictive maintenance and smart monitoring adoption | +0.4% | DSO chains and academic centers in North America, Western Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Infection Control Shift to Oil-Free, Clean, Dry Air

Stricter sterilization protocols and the formal treatment of clinical compressed air as a regulated input have reduced tolerance for oil carryover and moisture across procedures. EU MDR and ISO 22052, which translate compressed air purity rules into dental practice language, have pushed clinics toward oil-free designs with multi-stage filtration and validated dryers. In the U.S., 2024 guidance on air-powered handpieces reinforced performance and reprocessing expectations that depend on clean, dry air at the point of use.

These compliance anchors have changed procurement from “facility infrastructure” to “clinical quality,” which favors oil-free compressors that natively meet purity targets under ISO 8573-1 classes used in dental operatory air. The net effect on the dental compressors market is higher baseline specifications for dryness and purity, and an emphasis on documented validation within routine maintenance logs. Regulators and clinical guidance authors increasingly expect practices to show evidence that upstream air quality supports sterilization outcomes, encouraging standardization on oil-free systems with dew point control and fine coalescing filters[1]Centers for Disease Control and Prevention, “Sterilization and Disinfection,” CDC, cdc.gov.

Rising Dental Procedures and Equipment Upgrades

DSO networks continue to expand capacity and open new clinics, and these buildouts come with standardized compressor specifications and centralized maintenance plans. Heartland Dental reported opening 105 practices across 22 states in 2024 and added dozens of new locations in the first half of 2025, which locked in consistent air quality targets across a growing estate. This level of programmatic growth supports volume purchasing of oil-free compressors with membrane or desiccant dryers and shifts the dental compressors market toward fleets managed with cloud monitoring and documented service events.

Network operators also retrofit legacy systems acquired through practice affiliations to align with newer moisture and oil thresholds common in adhesive dentistry and high-speed handpieces. Expanded digital diagnostics and imaging usage rely on stable pressure delivery upstream of turbines, a factor that further aligns equipment procurement with standardized compressor setups. The result is steady replacement activity alongside greenfield installs, which reinforces predictable growth patterns for vendors that can support regional distribution and timely service coverage in the dental compressors market[2]Heartland Dental, “Heartland Dental Celebrates a Year of Growth and Innovation in 2024,” Heartland Dental, heartland.com.

DSO Consolidation and Multi Chair Clinic Expansion

Standardized multi-operatory designs often require tandem aggregates, integrated dryers, and larger tank volumes that preserve pressure during peak demand. Configurations from established OEMs combine oil-free compression with desiccant drying to achieve dew points suited for bonding, endodontic work, and extended duty cycles in high-throughput settings. Centralized monitoring helps regional coordinators schedule predictive maintenance during low-volume windows, which limits unplanned downtime and preserves clinical schedules at scale.

Operators benefit from simplified SKUs and consistent service kits, which lower training overhead and speed part availability across the network. Vendors that can ensure fast response and remote diagnostics win preferred supplier status because they can document compliance and uptime metrics alongside routine maintenance. As these factors compound, the dental compressors market continues to reward manufacturers that package oil-free performance, intelligent drying, and fleet monitoring in a unified offer for DSO customers.

Regulatory Standards Elevating Air Quality Requirements

Compressed air purity in dental practice is shaped by particle counts, total oil, and water content, which together define classes under ISO 8573-1 that clinics often cite in equipment policies. Newer guidance also links compressed air to reprocessing and device performance, so upstream contamination and moisture can undermine clinical claims and sterilization outcomes if not controlled at the source. In England, HTM 2022 sets test points and acceptance thresholds for periodic audits, which has encouraged providers to install sampling ports and adopt quarterly or semiannual validations for air quality.

Australia’s AS 2896 requires annual validation and documentation, which has given rise to service packages where accredited providers test dew point, particles, and oil vapor and integrate the results into practice records. These rules push practices to document point of use performance, not just nameplate specifications, and they place dryers and filters at the center of compliance. The cumulative effect keeps the dental compressors market pointed toward oil-free platforms with multi-stage filtration and verifiable dew point control suitable for clinical audit programs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront cost and lifecycle TCO of oil‑free systems | -0.7% | Emerging markets in APAC, Latin America, Africa, budget‑conscious solo practices globally | Short to medium term (≤ 3 years) |

| Maintenance burden of filters/dryers and consumables | -0.4% | Small‑to‑mid‑size practices without facility technicians, global impact | Medium term (2-4 years) |

| Space and noise constraints in small practices | -0.2% | Urban practices in high‑rent districts, Japan, South Korea, Hong Kong, Singapore | Medium term (2-4 years) |

| Shift toward electric handpieces lowers air demand | -0.3% | Markets with strong prosthodontic/endodontic digital adoption, Northern Europe, Japan | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront Cost and Lifecycle TCO of Oil Free Systems

Oil free compressors often carry higher purchase prices than lubricated alternatives, and that differential can be meaningful for solo practices and clinics that prioritize upfront capex. Desiccant dryers add recurring spend because cartridges need periodic replacement, while membrane dryers reduce consumables but can add to initial cost. Buyers sometimes underestimate filter replacement frequency and the energy impact of pressure drops across multi stage filtration, which complicates TCO calculations and delays oil free conversions. Where financing terms are limited or leasing options are scarce, sticker shock can favor lubricated systems paired with downstream coalescing and carbon filtration.

In regions with many small clinics, this dynamic slows the pace of upgrades even as regulations and clinical policies favor oil free systems and documented air quality performance. Vendors have responded with extended service intervals and monitoring features that curb premature changeouts, but purchase price sensitivity remains an inhibitor in parts of the dental compressors market.

Maintenance Burden of Filters/Dryers and Consumables

Compliance with particle, oil, and water purity thresholds depends on multi stage treatment that requires regular inspection and replacement, which adds time and cost for smaller practices. Where filter checks slip or ΔP readings are not tracked, moisture ingress or oil vapor breakthrough can undermine handpiece reliability and reprocessing outcomes. Clinics without dedicated technicians often push maintenance to the point of visible symptoms or pressure sag, which raises the risk of unplanned downtime and collateral repairs.

Documenting changeouts, dew point readings, and maintenance events is also a compliance burden in markets that require proof of validation, and manual record keeping consumes staff time. IoT monitoring helps by logging cycles, filter status, and dryer performance, but adoption is uneven among solo and two chair practices. These factors create an ongoing barrier to optimized air quality and steady operations, especially for resource constrained clinics in the dental compressors market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Oil-Free Systems Lead on Safety; Lubricated Compressors Gain in Training Facilities

Oil-free compressors held 57.9% share in 2025 as clinics oriented procurement toward infection control, bonding sensitivity, and validated dryness, a posture that has sustained leadership in the dental compressors market. Oil-free designs also simplify proof of purity because they remove lubricants from upstream air and reduce the risk of oil vapor breakthrough that can compromise composite bonding or sterile instrument handling. OEM updates that extend service intervals and improve cooling efficiency have strengthened reliability narratives for oil-free platforms. These products are also paired more often with desiccant or hybrid dryers that reach lower dew points suited to bonding and CAD/CAM operations, reinforcing their position as the default for high utilization practices. In regions where audits require documented testing or validation, clinics often favor oil-free options with built-in sampling points and straightforward proof frameworks. These practices stabilize demand patterns in the dental compressors market for oil-free fleets in clinics, hospitals, and academic centers.

Lubricated compressors remain important in training centers and large academic settings that need higher aggregate flow for many operatories and budget for lower upfront capex over long payback windows, and this cohort is projected to grow at 6.24% CAGR through 2031 within the dental compressors market. These installations typically rely on multi stage oil removal and carbon adsorption to meet oil vapor thresholds at the point of use, an approach that can work when documentation is rigorous and maintenance is on schedule. Over time, membrane dryers and longer life filters may narrow lifecycle costs relative to oil free platforms, but purchase price and availability often drive near term choices. Many academic centers also maintain redundancy in central plants, and the combination of larger tanks and careful filtration supports a range of procedures and student training cycles. This creates a practical niche for lubricated units that can still meet purity targets when well maintained. The result is a stable dual track configuration where oil free dominates private practice, while selected institutions continue to deploy lubricated technology alongside robust filtration in the dental compressors market.

By Technology: Desiccant Systems Dominate; Membrane Units Gain in Continuous Use Segments

Desiccant based systems commanded 64.65% share in 2025 because they achieve lower dew points that align with bonding and milling requirements, which underpins leadership in the dental compressors market. Clinics and labs that operate for extended hours value the safety margin created by -30°C to -40°C dew points that protect turbines and precision milling outcomes under fluctuating humidity. Vendors have refined cartridge media and designed intelligent sequencing to extend service intervals and maintain stable dew points across longer periods. RFID tagged cartridges and IoT dashboards also help staff replace desiccant at the right time, which reduces premature changeouts and clarifies spend. These steps make desiccant solutions more predictable for managers who need to defend budgets and sustain uptime. The above trends reinforce a durable role for desiccant platforms, especially in multi chair clinics, hospitals, and labs that depend on continuous or high duty operation in the dental compressors market.

Membrane dryers appeal to small and mid size clinics that want zero consumable operation, steady performance without regeneration cycles, and quieter acoustic profiles that suit urban practices. These systems reduce maintenance touch points and avoid purge air losses, which makes them compelling in water scarce or energy sensitive regions. For most climates, membrane dryers deliver very dry air that satisfies routine clinical needs when combined with high efficiency coalescing filtration, and they simplify daily operations by removing cartridge changes from PM calendars. In hybrid configurations, membrane pre drying can be paired with downstream polishing to reach lower dew points without the energy penalty associated with frequent desiccant regeneration. As clinics add IoT monitoring and visibility into dew point trends, they can tune maintenance to actual conditions, which reduces waste and improves performance predictability. These practical advantages explain why membrane and hybrid architectures are gaining adoption alongside desiccant leadership in the dental compressors market.

By Application: Handpieces Remain Core; CAD/CAM Air Supply Surges as Milling Penetrates Labs

High speed handpieces accounted for 48.67% of applications in 2025 and are projected to grow at 6.02% CAGR through 2031 as turbine reliability improves and clinics maintain larger active fleets. Practices that add higher speed units with tighter moisture thresholds upgrade compressors and dryers to protect ceramic bearings and maintain torque performance at consistent pressures. These choices align with infection control rules that link reliable sterilization to stable upstream air quality, elevating compressor and dryer systems from facilities to clinical infrastructure. Clinics that schedule multiple hygiene or restorative chairs in overlapping blocks rely on sustained flow and pressure to keep instruments at spec during busy hours. Handpiece cycles and predictable sterilization between patients have also driven adoption of monitoring and service contracts that minimize downtime risk. All these factors bolster application leadership for handpieces and stabilize demand for upgrades in the dental compressors market.

CAD/CAM milling air supply is the fastest expanding use case by installed base velocity, driven by lab automation and chairside adoption that require ultra dry air and reliable pressure under continuous operation. Suppliers recommend desiccant or hybrid dryers and larger aggregates where multiple mills run at once, and they warn that moisture or contamination increases tool wear and defect rates. Labs that consolidate regional work into central hubs deploy tandem compressors and automated monitoring to reduce downtime and keep shift based production on schedule. Clinics with single milling units often adopt membrane dryers to reduce consumables and simplify PM while still meeting dew point targets for the use case. As the balance of restorative production moves toward digital fabrication and 24 hour workflows, milling ready configurations shape compressor specifications in both clinics and labs. These patterns concentrate growth in air supply designed for digital workflows, which increases upgrade cycles and long term spend in the dental compressors market.

By End User: Clinics and Hospitals Dominate; Labs Gain as In House Milling Scales

Dental clinics and hospitals held 43.56% in 2025 and are projected to grow at 6.12% CAGR as DSOs extend networks and hospital outpatient dentistry scales capacity. These providers treat compressor assets as capital equipment that must support clinical documentation, uptime targets, and lower total maintenance exposure. Larger operators rely on IoT monitoring, centralized dashboards, and service contracts that blend equipment and support to maintain compliance and reliability. Hospital dental departments and academic centers often specify redundancy and automatic crossover to avoid interruptions during aerosol generating procedures, which raises the bar on compressor and dryer design. In markets with audit requirements or insurance tie ins to documented maintenance, these users adopt validation workflows that include periodic testing and record keeping. This gives an advantage to vendors that integrate sampling ports, monitoring, and reporting features as part of a unified offer in the dental compressors market.

Dental laboratories and academic institutes trail clinics in total share but outspend per site due to multi mill configurations, 24 hour operation, and lower dew point requirements tied to digital fabrication. Labs budget for tandem oil free compressors and desiccant or hybrid dryers that hold dew point under continuous workloads, and they integrate telemetry that helps pre stage parts and schedule PM during low volume windows. As chairside milling reduces certain outsourced volumes, commercial labs respond with automation, robotic blank handling, and instrumentation that benefits from clean, dry, and stable supply. Academic centers add monitoring for both chairs and compressors to predict seal wear and reduce downtime during high student throughput. These environments highlight the need for robust air quality and planned service, which continues to steer investment toward oil free, monitored systems. Over time, the weight of these operational and compliance needs will sustain steady orders in the dental compressors market among labs and institutes.

Geography Analysis

North America captured 47.42% share in 2025, supported by DSO density, documented sterilization protocols, and procurement standards that embed compressor performance and maintenance into clinical quality. Leading operators continue to open clinics and retrofit acquired practices, which keeps demand steady for oil free platforms with membrane or desiccant drying. Suppliers serving the region focus on fast response times, broad service coverage, and cloud monitoring that integrates with practice dashboards. These elements support both compliance requirements and uptime targets in busy multi chair clinics. The concentration of large networks also favors subscription models and unified service plans that spread costs and enable predictable maintenance scheduling across fleets. These patterns reinforce North America’s leadership within the dental compressors market.

Europe remains a significant region anchored by active OEMs and installers in Germany, Italy, and neighboring markets, and by sustained compliance checks that push for validated point of use performance. NHS England’s HTM 2022 framework and routine testing have driven clinics to adopt desiccant or hybrid drying, add sampling ports, and schedule regular audits. Vendors in the region emphasize oil free designs and documentation workflows that streamline record keeping for inspections. Italy and neighboring Mediterranean markets see strong positioning from local manufacturers and distributors that combine compressors, suction, and accessories with regional service density. Central Europe’s OEM base also supports export demand and product development that influences specification preferences globally. These features keep Europe central to product innovation and installed base upgrades in the dental compressors market.

Asia Pacific is projected to grow at a 6.36% CAGR to 2031 as dental school expansions and public sector investments in several countries require oil free air and documented maintenance for teaching clinics. Market education and digital dentistry adoption contribute to equipment upgrades that call for lower dew points and tighter moisture thresholds. Labs in manufacturing hubs add multi mill cells that operate with high duty cycles, which points to desiccant and hybrid drying choices and larger oil free aggregates. Distributors differentiate with installation, validation, and training packages aligned to local standards, and they add monitoring to simplify documentation in clinics that run many operatories. As more systems move to cloud dashboards, asset managers improve visibility into filter and dryer status and align service with actual conditions. These shifts continue to raise the specification floor and seed demand in developing corridors of the dental compressors market.

Competitive Landscape

The dental compressors market is moderately fragmented, with an incumbent core of OEMs and strong regional specialists that compete on reliability, compliance support, service coverage, and IoT integration. Vendors have accelerated platform updates that extend service intervals and cut wear while holding delivery rates, which sustains oil-free leadership in clinical environments. IoT enablement is now a priority because large operators want cloud monitoring, remote diagnostics, and automated service tickets, which lock in preferred supplier relationships. Product portfolios that bundle compressors with suction, chairs, and smart dashboards create one-stop offers that simplify procurement and increase switching costs. Vendors that maintain broad parts availability and fast on-site response are best positioned to capture multi-site fleets. These factors favor brands that combine oil-free performance, validated drying, and digital monitoring when serving enterprise customers in the dental compressors market.

Recent corporate milestones and awards highlight the emphasis on innovation and digital integration. Recognition for innovation leadership and design underscores the role of platform R&D and software in driving adoption. Regionally targeted distribution expansions shorten lead times and improve service density, which benefits clinics that operate under compliance checks with tight scheduling. Cloud dashboards that unify compressor status with other operatory devices strengthen the business case for integrated ecosystems. Subscription bundles that wrap hardware, IoT, and service into monthly plans reduce upfront cost and support predictable lifecycle management. These strategic levers are reshaping how buyers evaluate vendors and accelerating long-term shifts in the dental compressors market[3]Dürr Dental, “DÜRR DENTAL ist Deutschlands Innovations‑Champion 2025,” Dürr Dental, duerrdental.com.

Product strategies continue to emphasize oil-free compressors paired with desiccant or hybrid dryers, quiet operation, smaller footprints, and embedded telemetry for fleet managers. Vendors differentiate with extended warranties, validated filtration stacks that meet ISO 8573-1 targets, and dashboards that log dew point, pressure, and filter status for audits. In North America, offerings such as AirStar NEO pair oil-free compression and integrated monitoring for clinics that need reliable sterilization support and simplified documentation. In Europe, platform updates such as the Tornado relaunch target longer service intervals and reduced wear while preserving output at lower noise levels. Combined, these product moves align with clinical demands and compliance expectations, and they reinforce vendor positioning in the dental compressors market.

Dental Compressors Industry Leaders

Midmark Corporation

Dürr Dental

Air Techniques

Kaeser Kompressoren

DENTALEZ

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: The German Design Council jury decided to bestow one of the coveted German Design Awards on the NEW Tornado dental compressor by DÜRR DENTAL SE from Bietigheim Bissingen. It won this award in the “Excellent Product Design” category.

- April 2025: Dürr Dental received WirtschaftsWoche's "Germany's Innovation Champion 2025" award (first place among medium sized companies), recognizing its VistaSoft AI integrated software for automatic caries detection, smart compressor connectivity via VistaSoft Monitor, and continuous R&D investment in digital solutions and sustainable technologies showcased at IDS 2025 Cologne.

Global Dental Compressors Market Report Scope

As per the scope of the report, a dental compressor is a device that supplies compressed air to dental equipment. It is used in dental clinics to power tools such as air turbines, suction devices, and other pneumatic instruments. Dental compressors are designed to provide a steady, clean, and dry stream of compressed air to ensure the proper functioning of dental tools and maintain hygiene standards.

The dental compressors market is segmented by type into oil-free compressors and lubricated compressors. By technology, it is categorized into desiccant-based compressors and membrane-based compressors. By application, the market is divided into high-speed handpieces, scalers, chair valves and actuators, and CAD/CAM milling systems, air supply. By end user, it includes dental clinics and hospitals, dental laboratories, and academic & research institutes. By geography, the market is analyzed across North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Oil-free Compressors |

| Lubricated Compressors |

| Desiccant-based Compressors |

| Membrane-based Compressors |

| High-speed Handpieces |

| Scalers |

| Chair Valves and Actuators |

| CAD/CAM Milling Systems Air Supply |

| Dental Clinics and Hospitals |

| Dental Laboratories |

| Academic & Research Institutes |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Type | Oil-free Compressors | |

| Lubricated Compressors | ||

| By Technology | Desiccant-based Compressors | |

| Membrane-based Compressors | ||

| By Application | High-speed Handpieces | |

| Scalers | ||

| Chair Valves and Actuators | ||

| CAD/CAM Milling Systems Air Supply | ||

| By End User | Dental Clinics and Hospitals | |

| Dental Laboratories | ||

| Academic & Research Institutes | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the dental compressors market size outlook and growth through 2031?

The dental compressors market size is projected at USD 480.80 million in 2026 and is forecast to reach USD 635.47 million by 2031, supported by a 5.74% CAGR over 2026-2031.

Which region leads current demand in the dental compressors market?

North America led with a 47.42% share in 2025 due to DSO density, documented sterilization protocols, and standardized procurement that favors oil-free, audited systems.

Which product type is leading and which is expanding faster?

Oil-free systems led with 57.9% share in 2025, while lubricated units in select institutional settings are projected to grow at 6.24% CAGR to 2031 alongside robust filtration.

What compliance frameworks most affect buying decisions in the dental compressors market?

ISO 8573-1 purity classes, ISO 22052 dental-specific requirements, FDA guidance on air-powered handpieces, HTM 2022 testing in England, and Australia's AS 2896 annual validation shape specifications and documentation.

How are digital workflows changing compressor and dryer specifications?

CAD/CAM milling and high-utilization labs favor -20°C to -40°C dew points, tandem aggregates, and IoT monitoring to sustain cycle times and protect tool life under continuous duty.

What role do IoT and subscriptions play in dental compressor procurement?

Cloud monitoring reduces unplanned downtime and automates service tickets, and subscription bundles that include equipment and service smooth cash flow and simplify compliance for multi-site operators.

Page last updated on: