Dental Air Abrasion Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 197.16 Million |

| Market Size (2031) | USD 272.55 Million |

| Growth Rate (2026 - 2031) | 6.69% CAGR |

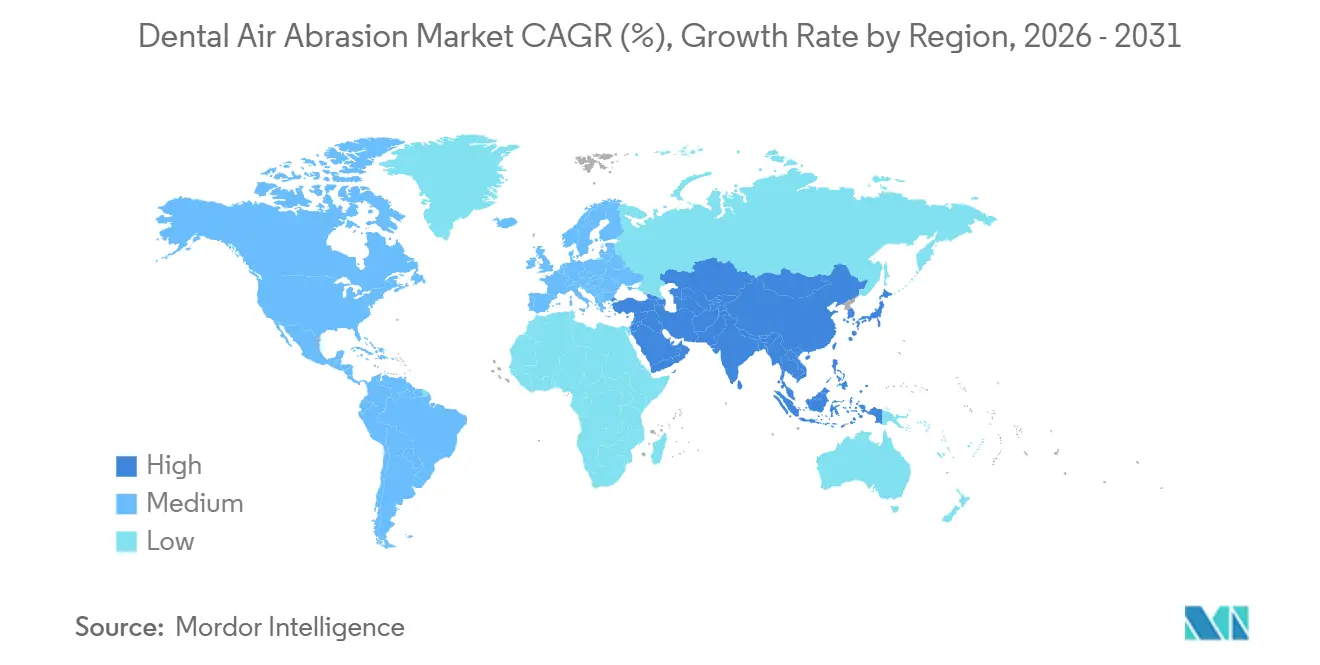

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Dental Air Abrasion Market Analysis by Mordor Intelligence

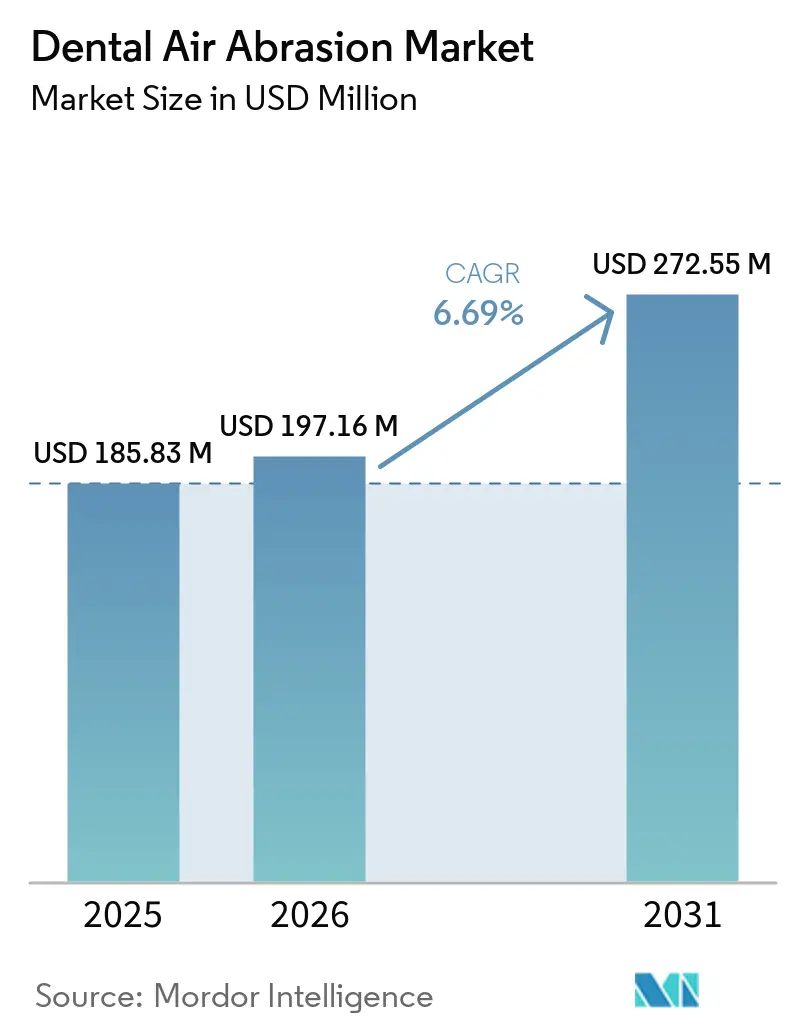

The Dental Air Abrasion Market size is projected to be USD 185.83 million in 2025, USD 197.16 million in 2026, and reach USD 272.55 million by 2031, growing at a CAGR of 6.69% from 2026 to 2031.

Patient preference for drill-free care, post-pandemic infection-control mandates, and the integration of kinetic micro-preparation into same-day CAD/CAM workflows are converging into a durable demand cycle. Practices that adopt air abrasion lower chair-time per restoration, open new preventive revenue streams, and improve case acceptance among pediatric and anxious cohorts. Innovation in bio-active abrasive media is recasting the procedure from a purely mechanical cut to a therapeutic step that deposits remineralizing ions. Portable cordless systems extend the dental air abrasion market into outreach dentistry, while digitally controlled devices log real-time parameters that support value-based reimbursement. Competitive intensity stays moderate because incumbents hold regulatory clearances and broad distribution, yet nimble entrants exploit white spaces such as implant maintenance and single-use cartridges.

Key Report Takeaways

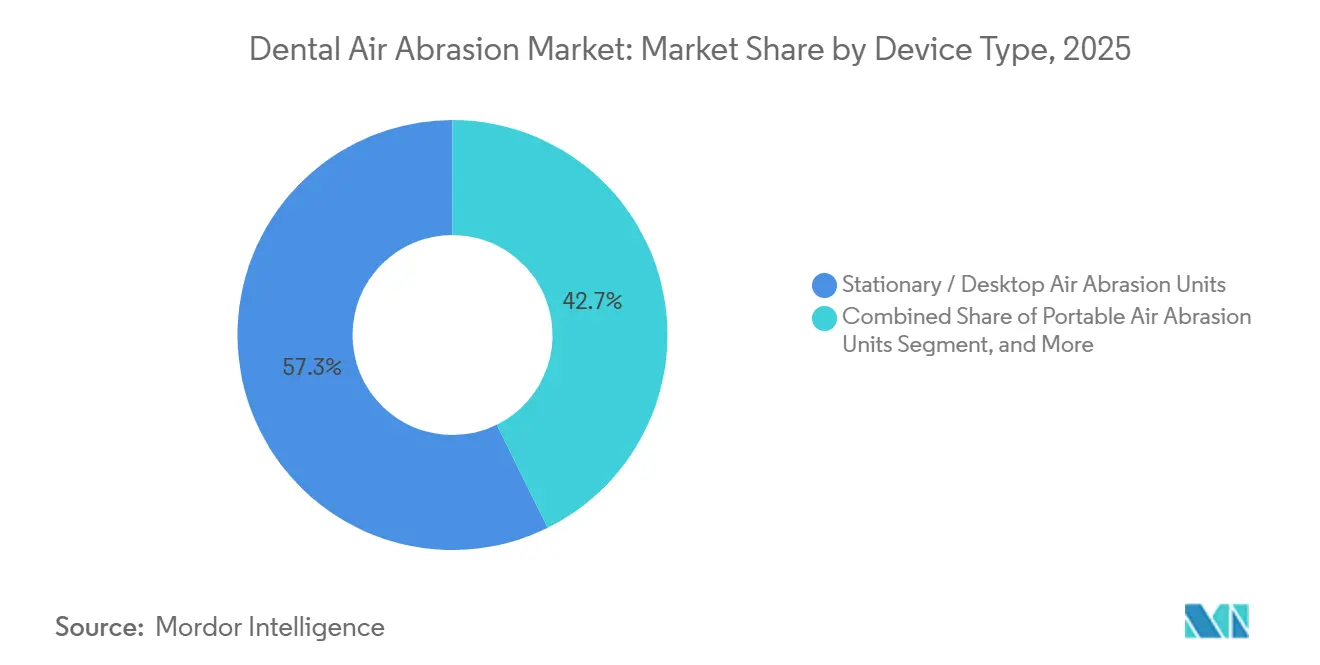

- By device type, stationary desktop systems led with 57.32% of the dental air abrasion market share in 2025. Portable cordless units are advancing at a 6.98% CAGR through 2031, the fastest growth within the segment.

- By control technology, mechanical pneumatic devices held 58.94% share of the Dental air abrasion market size in 2025. Digitally controlled smart devices are growing at a 7.09% CAGR, the highest among all technologies.

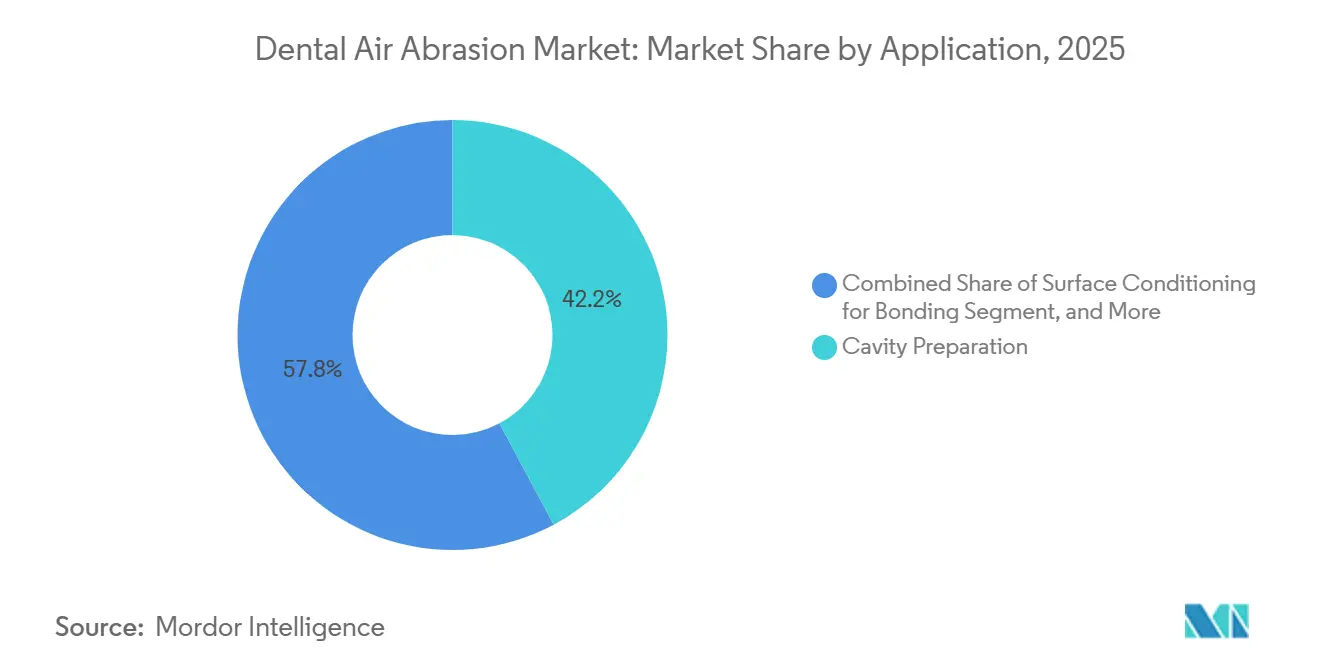

- By application, cavity preparation accounted for 42.21% of revenue in 2025, while orthodontic debonding and enamel cleansing are forecast to expand at a 7.36% CAGR to 2031.

- By abrasive media, aluminum-oxide powders commanded 37.03% of the dental air abrasion market share in 2025, but bio-active media will rise at an 8.38% CAGR, the quickest within abrasive types.

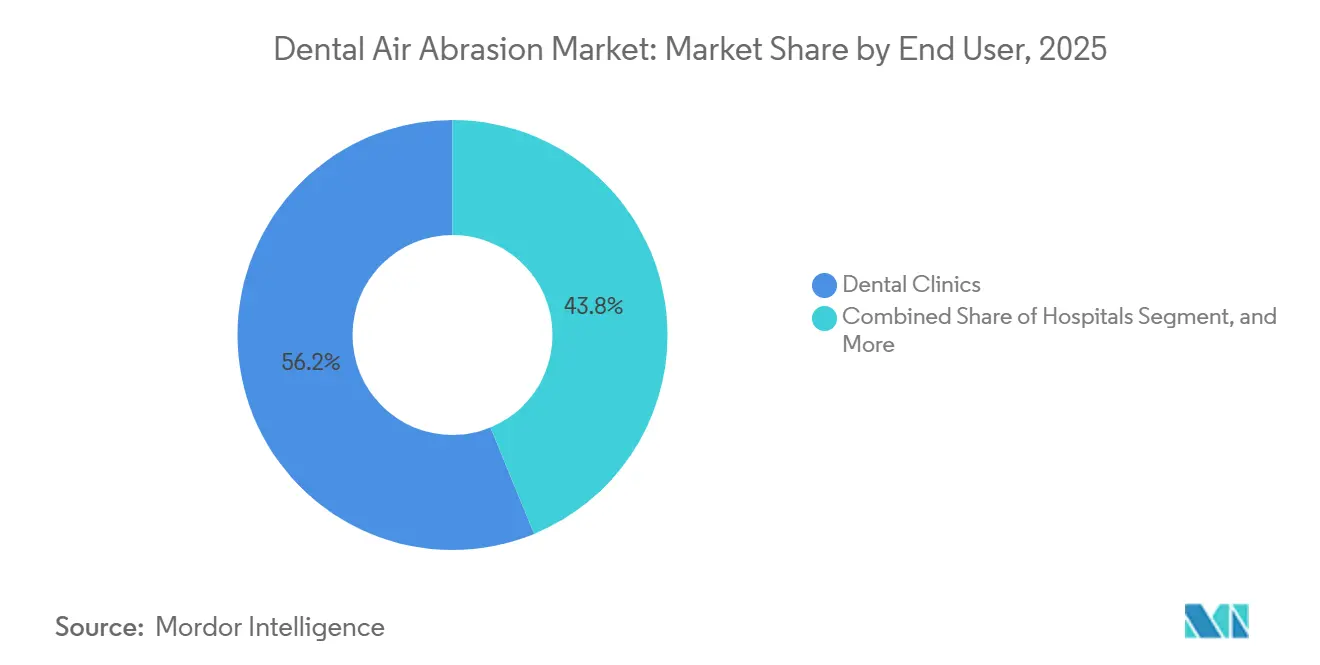

- By end user, dental clinics captured 56.18% of end-user installations in 2025, whereas mobile and community dentistry services are set to climb by an 8.22% CAGR through 2031.

- By geography, North America led with 37.23% revenue share in 2025; Asia-Pacific records the highest regional CAGR at 6.87% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Dental Air Abrasion Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Preference for Minimally Invasive Drill-Free Dentistry | +1.2% | North America and Western Europe | Medium term (2–4 years) |

| Growing Adoption in Pediatric and Anxious Patient Care | +0.9% | Global, strong in Asia-Pacific | Short term (≤ 2 years) |

| Integration with Digital Dentistry and CAD / CAM Workflows | +1.4% | North America and Europe | Medium term (2–4 years) |

| Expansion of Portable Cordless Units in Outreach Dentistry | +0.8% | Rural Asia-Pacific and Africa | Long term (≥ 4 years) |

| Regulatory Push for Aerosol Reduction and Infection Control | +1.1% | Global, led by CDC and EU norms | Short term (≤ 2 years) |

| Emergence of Bio-Active Abrasive Media Enabling Remineralization | +1.3% | North America and Japan | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Rising Preference for Minimally Invasive Drill-Free Dentistry

Air abrasion removes early enamel lesions without the vibration, heat, or acoustic stress of rotary burs, trimming patient anxiety scores by 42% in a 2024 meta-analysis.[1]Journal of Dentistry, “Patient Anxiety in Air Abrasion,” journals.elsevier.com American Dental Association guidelines issued in 2025 endorse the modality for Class I and II lesions, creating reimbursement parity that accelerates uptake. Practices adopting the technique record double-digit gains in elective sealant acceptance, improving revenue per chair hour without adding operative complexity.

Growing Adoption in Pediatric and Anxious Patient Care

A 2025 trial showed that 68% of children aged 6-12 chose air abrasion over drills, allowing restorations without anesthesia and cutting sedation use by 31%.[2]Pediatric Dentistry Journal, “Behavioral Compliance Study,” aapd.org The gentler sensory profile also benefits geriatric and special-needs cohorts, broadening the Dental air abrasion market among caregivers focused on behavioral compliance.

Integration with Digital Dentistry and CAD/CAM Workflows

Air abrasion roughens enamel in under 20 seconds and yields 23% higher shear bond strength for lithium-disilicate crowns versus acid etch, enhancing same-day restoration reliability. Digitally enabled handpieces log pressure and exposure time directly into electronic charts, easing medico-legal documentation and bolstering value-based quality metrics.

Expansion of Portable Cordless Units in Outreach Dentistry

Rechargeable devices bring minimally invasive care to sites without grid power. A WHO pilot in rural India lifted sealant coverage by 47% once the setup time dropped below 10 minutes.[3]World Health Organization, “Global Oral Health Strategy 2025-2030,” who.int Governments in Southeast Asia and Africa fold these devices into school and refugee programs, turning technology into an equity lever for universal oral-health targets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital and Consumable Costs for Smaller Practices | -0.7% | Global, acute in price-sensitive APAC & South America | Short term (≤ 2 years) |

| Limited Cutting Efficiency Versus Rotary Drills for Deep Lesions | -0.5% | Global, particularly in high-caries-burden populations | Medium term (2–4 years) |

| Aerosol Safety Concerns Amid Strict Post-COVID Regulations | -0.4% | North America & EU compliance zones, spillover to APAC | Short term (≤ 2 years) |

| Competition From Alternative Technologies | -0.3% | Global, with concentration in technologically advanced markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capital and Consumable Costs for Smaller Practices

Entry systems cost USD 8 000–15 000, and each procedure adds roughly USD 3 in powder and tips, squeezing margins where reimbursement is low. Leasing models exist, yet many owners worry about vendor lock-in and rising per-use fees, delaying purchases in price-sensitive regions.

Limited Cutting Efficiency for Deep Lesions

A 2024 comparative study reported air abrasion taking more than triple the time of burs for dentin deeper than 2 mm. Therefore, clinicians must maintain drills in parallel, which dilutes workflow simplification. Research into higher-pressure nozzles continues, but regulators watch micro-fracture risk, slowing deployment.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Portability Reshapes Field Deployment

Stationary desktop systems held 57.32% dental air abrasion market share in 2025. They maintain precise flow control that large private practices favor for bulk restorative throughput. Portable cordless units, expanding at a 6.98% CAGR, unlock remote programs and corporate on-site screenings. Declining battery costs and MEMS pressure sensors now allow 60 psi output for 90 minutes, supporting 30 pediatric sealants before a recharge.

Clinics leverage portable kits for pop-up wellness events that broaden patient funnels. Public health agencies in Canada and Australia embed them in fly-in teams serving Indigenous communities. Regulatory bodies apply the same safety standards to field units, giving decision makers confidence to allocate grant funding.

By Control Technology: Digital Interfaces Drive Precision

Mechanical pneumatic devices controlled 58.94% of revenue in 2025 owing to proven reliability and affordable maintenance. Yet smart devices rise at 7.09% CAGR as insurers and regulators request traceable procedural data. A U.S. service organization found that integrated systems cut charting time 40% and reduced abrasive waste 18%, trimming consumables spend for high-volume operators.

Remote diagnostics, firmware updates, and automatic usage logs bolster uptime and medico-legal defense. As fee schedules evolve toward quality metrics, smart pressure modulation that curbs enamel over-ablation becomes a differentiator.

By Application: Orthodontic Debonding Gains Momentum

Cavity preparation remained the workhorse at 42.21% of demand in 2025. However, orthodontic debonding and enamel cleansing display the highest growth at 7.36% CAGR. After bracket removal, air abrasion eliminates residual adhesive while preserving 28% more enamel than bur techniques. Implant surface decontamination is a niche but expanding space as aging populations receive more fixtures that require gentle maintenance.

Chairside hygiene teams use the same handpiece for stain removal, bonding prep, and sealant conditioning, which spreads fixed costs across multiple billable codes. This versatility supports procurement decisions in small and mid-sized practices.

By Abrasive Media: Bio-Active Formulations Disrupt Incumbents

Aluminum-oxide powders held 37.03% share in 2025 due to low price and universal compatibility. Glycine and erythritol cater to periodontal maintenance when enamel preservation is paramount. A Caries Research trial showed a 41% reduction in white-spot progression using calcium-phosphate air abrasion. Such outcomes fit preventive reimbursement models that pay for disease arrest, not just restoration.

Early movers segment their portfolio, offering both inert and therapeutic powders, which encourages continuous consumable revenue while differentiating on clinical performance.

By End User: Mobile Services Outpace Traditional Clinics

Dental clinics generated 56.18% of installations in 2025 thanks to high patient volumes and staff trained in minimally invasive workflows. Hospitals deploy air abrasion mainly in pediatric and special-needs units to avoid general anesthesia. Academic centers test novel abrasive formulations, feeding clinical evidence that informs purchasing across the Dental air abrasion industry.

Mobile and community dentistry services grow at 8.22% CAGR, backed by school sealant mandates and geriatric outreach. A Kenyan pilot reached 120 children daily, triple the drill-based rate, because portable units slash setup overhead. Jurisdictions now allow hygienists to operate air abrasion under general supervision, boosting workforce reach.

Geography Analysis

North America secured 37.23% of the dental air abrasion market share in 2025 on the strength of insurance parity and ADA endorsement. Public programs in Canada roll portable systems into Indigenous outreach, supporting universal coverage. Mexico’s emerging middle class drives cosmetic bonding demand yet keeps price pressure on manufacturers.

Asia-Pacific posts the quickest growth at 6.87% CAGR through 2031. China’s Five-Year Health Plan subsidizes minimally invasive kits for township clinics, while India’s school sealant campaign targets 50 million children with portable air abrasion. Japan’s implant-heavy elderly population needs low-scratch biofilm removal; domestic firms such as NSK invest in dedicated production lines. Australia relies on fly-in provisions for remote communities, where battery systems reduce aircraft payload.

Europe combines mature private demand in Germany and the United Kingdom with government-sponsored prevention pilots in France and Spain. GCC countries standardize air abrasion to differentiate premium clinic chains. South America shows patchy adoption: Brazil funds riverine mobile units for Amazon communities, though fiscal swings temper volume; Argentina’s medical tourism market promotes air abrasion in aesthetic packages.

Competitive Landscape

Dentsply Sirona, 3M, and KaVo Kerr leverage global distribution, bundled consumables, and 510(k) clearances to secure group practice deals. Mid-sized innovators such as Crystalmark, Danville Materials, and TPC focus on niche offerings from single-use cartridges to peri-implantitis powders. Patent filings remain active; Bien-Air’s 2024 MEMS pressure sensor could become a new benchmark if commercialized.

Strategic moves in 2026 underline the shift toward digital and preventive value. Dentsply Sirona released a system that syncs with Primescan to auto-record parameters, slicing charting by 35%. 3M embedded protocols in cloud software that nudge clinicians toward minimally invasive codes. KaVo Kerr gained FDA clearance for calcium-phosphate powder, entering the therapeutic arena.

Start-ups capture white space in veterinary dentistry and outreach kits. Subscription models surface, though cost predictability remains a barrier for small offices. OEM collaborations with software vendors create ecosystems that could lock customers through integrated workflow, nudging the market toward platform competition rather than pure hardware rivalry.

Dental Air Abrasion Industry Leaders

3M

Dentsply Sirona

Ivoclar Vivadent

Midmark Corporation

Bien-Air Dental

- *Disclaimer: Major Players sorted in no particular order

Global Dental Air Abrasion Market Report Scope

The dental air abrasion market focuses on non-invasive, drill-less dentistry instruments that use a high-speed stream of aluminum oxide particles, driven by compressed air, to remove tooth decay, stains, and prepare tooth surfaces.

The dental air abrasion market report is segmented by device type, application, control technology, abrasive media, and end user. By device type, the market is segmented into portable air abrasion units and stationary / desktop air abrasion units. By control technology, the market is segmented into mechanical (pneumatic) devices and digitally-controlled / smart devices. By application, the market is segmented into cavity preparation, stain & plaque removal/prophylaxis, surface conditioning for bonding & sealants, orthodontic debonding & enamel cleansing, and other applications. By abrasive media, the market is segmented into aluminum-oxide powders, glycine/erythritol low-abrasive powders, and bio-active / remineralizing powders. By end users, the market is dental clinics, hospitals, academic & research institutes, and mobile & community dentistry services. By geography, the market is segmented into North America, Europe, Asia-Pacific, MEA, and South America. The report offers the value (in USD million) for the above segments.

| Portable Air Abrasion Units |

| Stationary / Desktop Air Abrasion Units |

| Mechanical (Pneumatic) Devices |

| Digitally-Controlled / Smart Devices |

| Cavity Preparation |

| Stain & Plaque Removal / Prophylaxis |

| Surface Conditioning for Bonding & Sealants |

| Orthodontic Debonding & Enamel Cleansing |

| Other Applications (Implant Maintenance, Peri-implantitis Management, etc.) |

| Aluminum-oxide Powders |

| Glycine / Erythritol Low-abrasive Powders |

| Bio-active / Remineralising Powders |

| Dental Clinics |

| Hospitals |

| Academic & Research Institutes |

| Mobile & Community Dentistry Services |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Device Type | Portable Air Abrasion Units | |

| Stationary / Desktop Air Abrasion Units | ||

| By Control Technology | Mechanical (Pneumatic) Devices | |

| Digitally-Controlled / Smart Devices | ||

| By Application | Cavity Preparation | |

| Stain & Plaque Removal / Prophylaxis | ||

| Surface Conditioning for Bonding & Sealants | ||

| Orthodontic Debonding & Enamel Cleansing | ||

| Other Applications (Implant Maintenance, Peri-implantitis Management, etc.) | ||

| By Abrasive Media | Aluminum-oxide Powders | |

| Glycine / Erythritol Low-abrasive Powders | ||

| Bio-active / Remineralising Powders | ||

| By End User | Dental Clinics | |

| Hospitals | ||

| Academic & Research Institutes | ||

| Mobile & Community Dentistry Services | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large will the dental air abrasion market be by 2031?

The dental air abrasion market size is forecast to reach USD 272.55 million by 2031, growing at a 6.69% CAGR.

Which region is expanding fastest in air-abrasion adoption?

Asia-Pacific leads growth with a 6.87% CAGR through 2031 due to government preventive-care drives and rising disposable income.

What device type is gaining momentum among mobile clinics?

Portable cordless systems are advancing at 6.98% CAGR as outreach dentistry seeks equipment free of grid power and water lines.

Which application shows the strongest growth to 2031?

Orthodontic debonding and enamel cleansing posts the fastest rise at 7.36% CAGR because it preserves more enamel after bracket removal.

What share do digitally controlled devices hold?

Mechanical units still dominate, but smart platforms are on track as clinics demand traceable procedural data.

Page last updated on: