Demulcent Eye Drops Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.41 Billion |

| Market Size (2031) | USD 3.31 Billion |

| Growth Rate (2026 - 2031) | 6.60% CAGR |

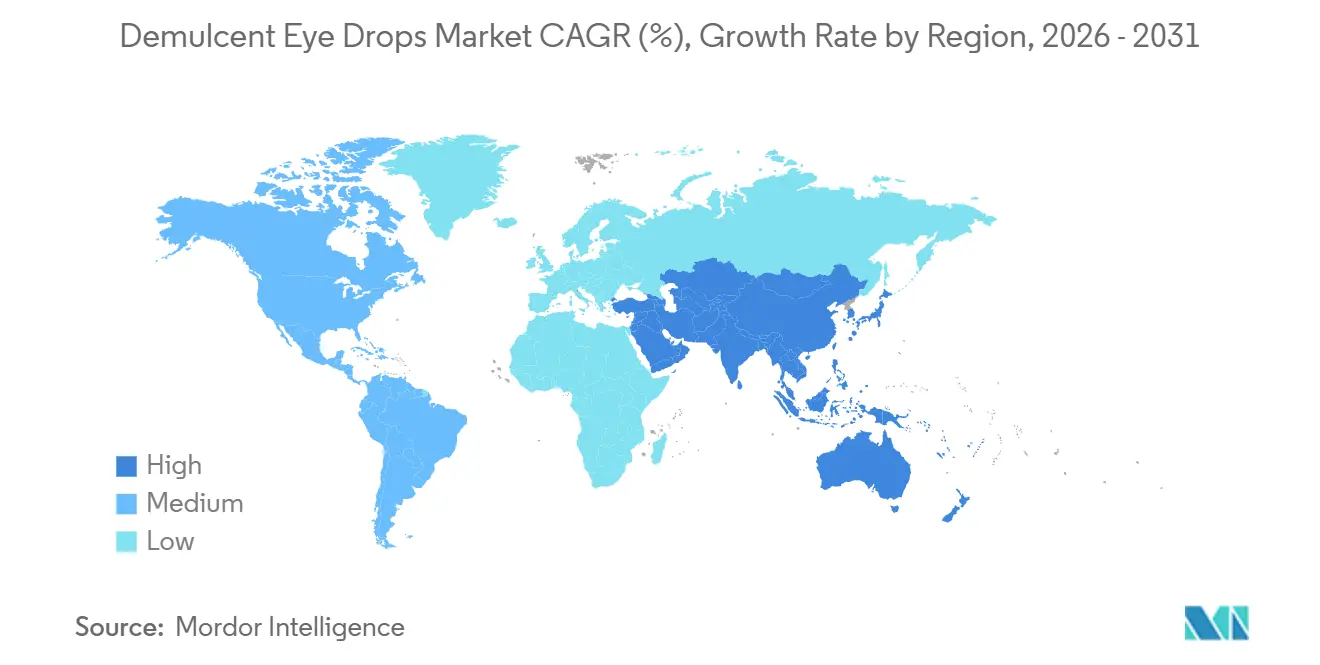

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Demulcent Eye Drops Market Analysis by Mordor Intelligence

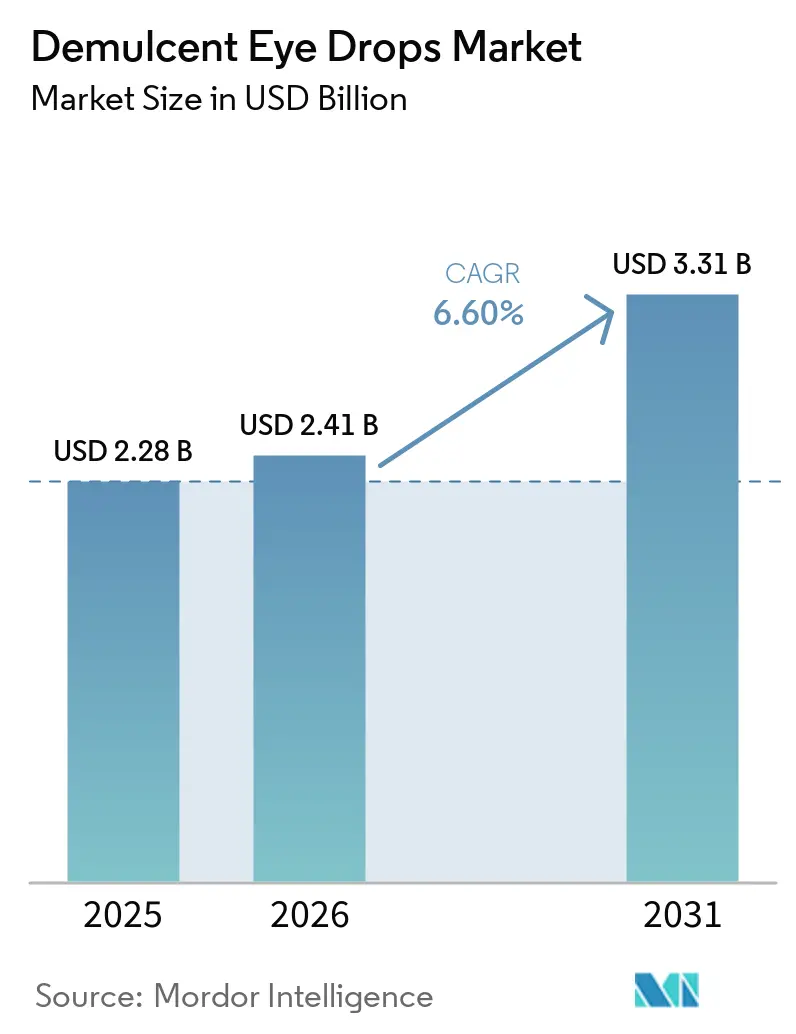

The Demulcent Eye Drops Market size is expected to increase from USD 2.28 billion in 2025 to USD 2.41 billion in 2026 and reach USD 3.31 billion by 2031, growing at a CAGR of 6.60% over 2026-2031.

Momentum in the demulcent eye drops market reflects a decisive pivot toward preservative-free multi-dose systems that sustain adherence and reduce contamination concerns. Regulatory scrutiny has intensified since 2023, sharpening the focus on sterility assurance and improving quality expectations across over-the-counter manufacturers. Product design has responded with one-way valves and sterile-filter technology that maintain integrity without benzalkonium chloride, creating headroom for premium formulations and safer long-term use. Online and hybrid channels are reshaping distribution economics for chronic-use products, while clinical practice continues to promote preservative-free options for sensitive ocular surfaces. Production capacity in growth markets is scaling to meet rising urban screen time, contact-lens use, and post-procedure care requirements.

Key Report Takeaways

- By formulation, preservative-free multi-dose systems led with 39.47% revenue share in 2025 and are set to grow at 8.78% CAGR through 2031.

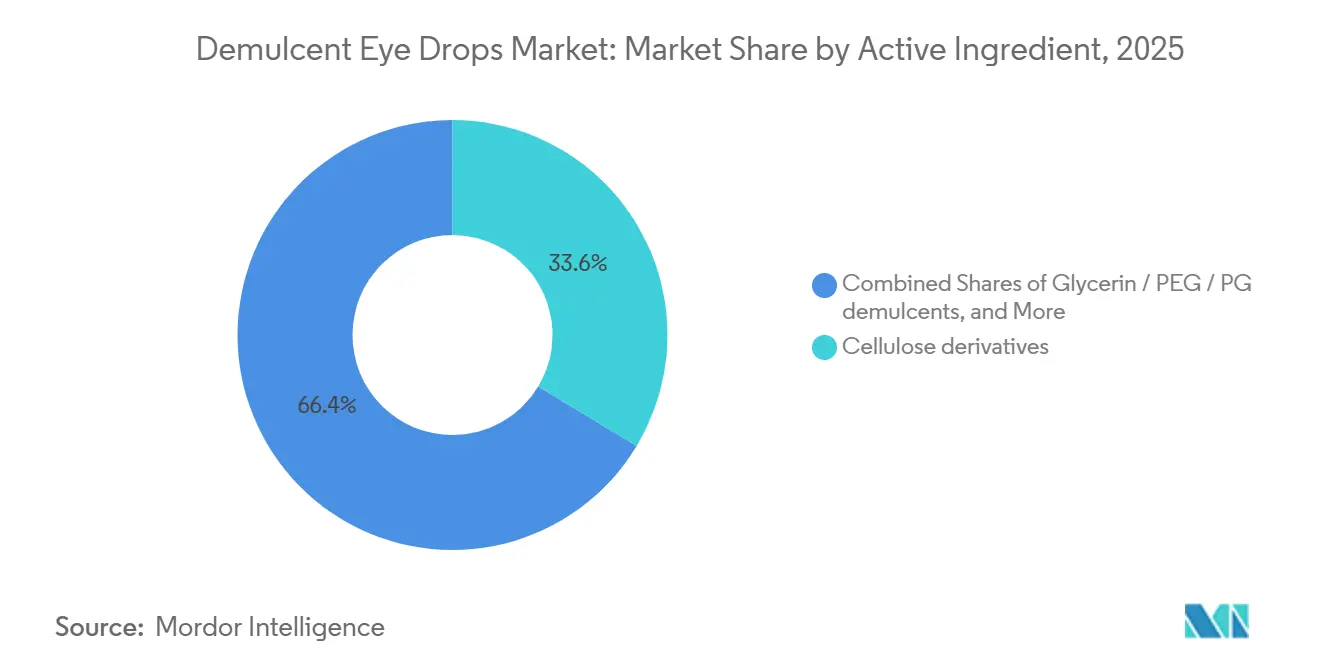

- By active ingredient, cellulose derivatives accounted for 33.63% share in 2025, while sodium hyaluronate is projected to advance at 9.24% CAGR over 2026-2031.

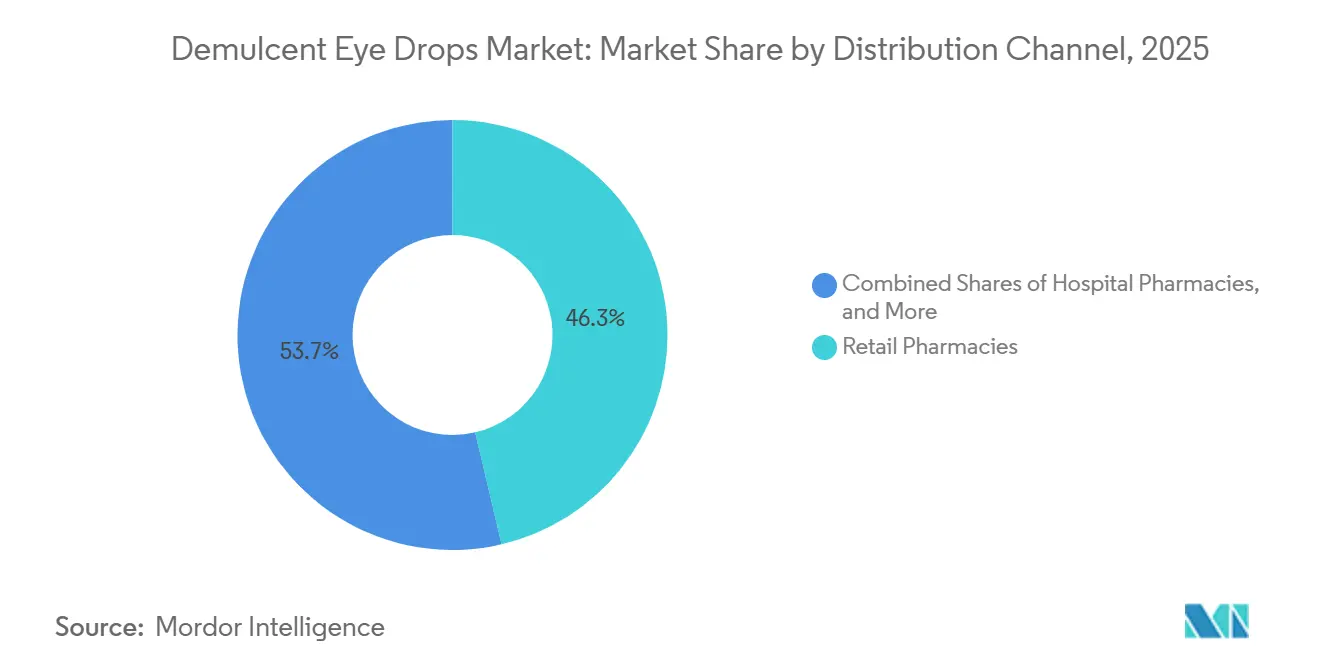

- By distribution channel, retail pharmacies held 46.34% in 2025 and online channels recorded the fastest growth outlook at 8.45% CAGR to 2031.

- By geography, North America commanded 36.47% in 2025 and Asia-Pacific is expected to post a 9.34% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Demulcent Eye Drops Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging Populations and Prolonged Screen-time Intensify Dry Eye Episodes and Lubricant Drop Usage | +1.8% | Global, with early gains in North America, EU core, APAC metros | Medium term (2-4 years) |

| Rapid Shift to Preservative-free Formats, Notably Multi-dose Preservative-free (MDPF) Bottles | +2.1% | North America and EU regulatory push, APAC adoption lags 18-24 months | Short term (≤ 2 years) |

| Expansion of Online/Omnichannel Pharmacy and DTC Fulfillment for OTC Eye Lubricants | +0.9% | North America lead, EU fragmented, APAC nascent except China and India | Medium term (2-4 years) |

| Rising Contact Lens Wear and Post-procedure Ocular Surface Care Increase Drop Intensity | +1.0% | APAC core markets including Japan and South Korea with spillover to Southeast Asia | Long term (≥ 4 years) |

| PF Multi-dose Bottle Designs Reduce Contamination Fears and Boost Daily Use | +1.3% | Global, premium tier in North America and EU with mid-tier rollout in APAC | Short term (≤ 2 years) |

| Biomimetic Excipients Enable Premiumization and Regimen Bundling | +1.2% | North America, EU5 with Japan as early adopter and China tier-1 cities emerging | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Aging Populations and Prolonged Screen-time Intensify Dry Eye Episodes and Lubricant Drop Usage

An aging base and digital lifestyles expand the addressable user pool for lubricating drops beyond the traditional senior cohort. In the United States, 49.5 million adults reported vision difficulty in 2026, including 3.8 million with severe trouble, which signals sustained reliance on accessible therapies for daily symptom relief[1]Facts and Figures on Adults with Vision Loss from the NHIS,” American Foundation for the Blind, afb.org. Population data from South Korea indicate an 8.88% dry-eye prevalence over five years with higher rates among women and older adults, reinforcing the role of demulcents in supportive care pathways in universal coverage settings[3]“A nationwide population-based study on epidemiologic characteristics and treatment patterns of dry eye disease in South Korea,” Scientific Reports, nature.com. Younger cohorts are contributing more to demand as screen exposure rises, with U.S. survey findings showing half of teens record 4 or more hours of non-school screen time per day and report associated health stressors that can reduce blink frequency and disrupt tear film stability. Global screen health assessments place Gen Z daily exposure at 9 hours and link heavy use to higher digital eye strain incidence[2]“World Screen Health Report 2026,” Eyesafe, eyesafe.com, while high myopia prevalence figures in East Asia compound ocular surface stressors that increase lubricant use. Professional organizations also highlight unmet burden, with recent education partnerships underscoring the scale of dry-eye symptoms and the role of consistent at-home care.

Rapid Shift to Preservative-free Formats, Notably Multi-dose Preservative-free (MDPF) Bottles

Preservative-free multi-dose designs address the discomfort and long-term ocular risk associated with benzalkonium chloride and related agents, without reintroducing handling friction tied to unit-dose vials. Modern containers deploy one-way valves, closed-system filters, or collapsible inner reservoirs that maintain sterility for months after opening without chemical preservatives and enable frequent daily use patterns that support adherence. Product launches since 2024 have moved decisively into this space, including preservative-free multi-dose offerings with vitamin enrichment and antioxidant systems that broaden positioning at retail across major chains and online marketplaces.

European clinical practice content and clinic guidance favor preservative-free regimens for chronic users to protect corneal integrity, which nudges category mix toward MDPF formats for long-term use. Heightened sterility oversight after 2023 contamination events and follow-on actions in 2026 has further aligned regulatory signals with these packaging choices by tightening expectations on manufacturers’ assurance of sterility. The demulcent eye drops market has responded with greater investment in aseptic filling and packaging technologies that scale MDPF availability across price points.

Expansion of Online/Omnichannel Pharmacy and DTC Fulfillment for OTC Eye Lubricants

Chronic-use, low-complexity therapies align with direct-to-consumer pharmacy and subscription models that remove benefit design hurdles and cut refill friction. Programs that simplify access to chronic ocular therapies via mail-order partners illustrate how digital fulfillment reduces administrative checks and can compress out-of-pocket variability for commercially insured users. Subscription storefronts are extending this model into scheduled shipments for commonly used lubricants with strong user ratings and recurring engagement. These channels improve continuity for users who prefer home delivery and for those who combine OTC lubricants with prescription regimens. Telehealth pathways are also increasing point-of-prescription alignment with fulfillment, which encourages trial of preservative-free options where clinicians expect better long-term tolerability. The demulcent eye drops market is adapting merchandising and pack sizes to serve these digital-first behaviors and to match subscription cadence with daily use intensity.

Rising Contact Lens Wear and Post-procedure Ocular Surface Care Increase Drop Intensity

Contact-lens users and patients undergoing refractive or cataract procedures often require frequent lubrication during recovery and may continue use beyond immediate care windows. New product launches for comorbid conditions associated with long-term lens wear underscore how ocular surface management intersects with pharmacologic care and supportive demulcent use. Clinic data from Korea show higher dry-eye prevalence in older female cohorts, with near work time correlating with symptom risk, a pattern that typically raises reliance on preservative-free hyaluronate and similar formulations.

Clinical guidance in Japan recommends sodium hyaluronate preservative-free drops where chronic therapy causes irritation, while German practice content cautions against long-term exposure to preservatives for frequent users, both reinforcing preservative-free choices for sensitive eyes. The demulcent eye drops market is also seeing more regimen bundling across biomimetic excipients and dosing forms that support epithelial stability during higher-intensity use periods. Manufacturer investments in regional capacity signal ongoing preparation for long-term demand from lens wearers, post-procedure patients, and heavy screen users in urban markets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Heightened Sterility/Quality Incidents Elevate Compliance, Testing, and Recall Risks | -0.7% | North America FDA enforcement with EU spillover and uneven APAC application | Short term (≤ 2 years) |

| Limited Head-to-head Superiority, Brand Switching and Private-label Pressure Commoditize | -0.6% | Global, acute in North America and EU mature pharmacy chains | Medium term (2-4 years) |

| Trade or Tariff Shocks and GMP Upgrades Inflate COGS for Demulcents and Packaging | -0.4% | North America import dependent with China export tariffs | Medium term (2-4 years) |

| Capital-intensive Aseptic Filling and PF Packaging Slow Smaller Entrants and Launches | -0.5% | Global with smaller regional players in APAC and LatAm most exposed | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Heightened Sterility/Quality Incidents Elevate Compliance, Testing, and Recall Risks

The industry faces tighter oversight following contamination-linked outbreaks and subsequent enforcement actions that raised the bar on sterility assurance. In March 2026 regulators flagged over 3.1 million bottles for lack of sterility assurance, reinforcing concerns that some facilities had persistent microbiological control gaps despite prior warnings. Earlier in 2023, multi-state outbreaks caused severe injuries and fatalities, which catalyzed a wide review of OTC eye drop manufacturing and inspection cycles. The combined effect has been higher capital spending on aseptic equipment, more robust environmental monitoring, and mandatory third-party sterility audits that lengthen time-to-market. Smaller firms and some contract manufacturers face strain from these upgrades, which can lead to portfolio rationalization or delayed launches. The demulcent eye drops market therefore tilts toward incumbents with validated sterile production and quality systems that can absorb compliance overhead and maintain scale.

Limited Head-to-head Superiority, Brand Switching and Private-label Pressure Commoditize

Basic cellulose and entry-level hyaluronate formulations often show limited clinical differentiation in everyday use, which encourages pharmacy chains to introduce equivalent private-label options at lower prices. Store brands source identical actives from contract manufacturers and package them in similar multi-dose bottles, fostering price-led switching among non-adherent or cost-sensitive users. Survey and merchandising patterns in mature markets show that OTC selection often reflects price and availability more than physician instruction, outside premium combinations or biomimetic excipients.

Generic pathways and monograph-based approvals accelerate the speed of entry, compressing margins for standard profiles and narrowing shelf advantages for branded incumbents. In several Asia markets where clinician prescribing remains influential, premium brands maintain stronger positions, although national efforts to control spending can still foster generic uptake over time. Company disclosures point to portfolio strategies that focus on higher-margin hybrids and adjuncts where differentiation is clearer and where direct generic substitution is less intense.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Active Ingredient: Sodium Hyaluronate Climbs as Cellulose Derivatives Anchor Volume

Cellulose derivatives held 33.63% share in 2025, reflecting a wide installed base, low per-dose cost, and consistent inclusion across pharmacy assortments. The demulcent eye drops market continues to rely on these polymers for day-to-day relief in moderate symptom clusters and for users who prefer familiar textures and predictable handling. Higher-viscosity carboxymethylcellulose can increase residence time on the ocular surface for overnight or severe-dryness regimens, while hydroxypropyl methylcellulose suits users who need clarity for immediate activity after dosing. Sodium hyaluronate is accelerating at 9.24% CAGR over 2026-2031 as high molecular weight grades lower friction, bind water effectively, and support epithelial stability, creating perceived comfort advantages over commodity polymers. Disclosures in U.S. product labels indicate that even generic CMC formulations often include hyaluronate as an inactive excipient, a signal of how the market prefers lubricity and conditioning characteristics associated with HA. In South Korea, prescribing patterns show strong use of single-use hyaluronate for sensitive eyes, aligning with long-standing clinician emphasis on preservative-free delivery.

The demulcent eye drops market now layers biomimetic excipients such as trehalose and HP-guar to extend comfort and address evaporative dryness and surface stress beyond basic lubrication. Oil-in-water emulsions and water-free vehicles are expanding roles in meibomian gland dysfunction as they stabilize the lipid layer and slow tear evaporation, which complements aqueous-focused agents. Guidelines in German practice literature recommend hyaluronic acid for dryness sensations and panthenol for irritation or surface micro-injury, pointing to an ingredient-first approach for daily relief. Company pipelines in Asia emphasize higher-concentration secretagogues and next-generation agents that can integrate with supportive demulcent regimens, and this supports continued category depth through the forecast period. he demulcent eye drops industry is positioned to balance cellulose-based volume anchors with hyaluronate-led premium tiers that reinforce overall category value without disrupting access.

By Formulation: MDPF Bottles Lead Share and Growth, Squeezing Preserved Multi-dose

Preservative-free multi-dose bottles captured 39.47% of 2025 sales and are forecast to post 8.78% CAGR to 2031, outpacing preserved multi-dose and unit-dose formats. The demulcent eye drops market has rewarded closure systems that prevent backflow and air ingress so sterility is preserved naturally for months, which reduces the need for benzalkonium chloride and minimizes epithelial irritation and contact dermatitis risk in frequent users. Heightened enforcement in 2026 underscored how sterility assurance is a core constraint in OTC lines and validated MDPF systems as a safer long-horizon configuration for heavy users and sensitive eyes. New preservative-free launches include vitamin-enriched and antioxidant-enhanced options with distribution across national retailers and e-commerce platforms, which make these formats more accessible to new users and refillers. European clinic content and Japanese clinical guidance keep recyclability, comfort, and long-term safety at the center of recommendations for chronic use, indirectly reinforcing MDPF as a preferred mainstream choice.

Unit-dose formats retain roles in post-operative care and for highly sensitive patients, but they are losing share to MDPF where convenience and waste reduction matter for daily regimens. Pharmacy guidance in Japan highlights that single-use minis must be discarded after opening, which adds handling steps and material volume, whereas MDPF bottles support repeat dosing from a sterile reservoir that reduces user errors. Clinician practices in Korea show older patients often prefer bottled formulations for ease, while doctors reserve single-use vials where infection risk is a more immediate concern. The demulcent eye drops market is also impacted by medical device quality frameworks because many MDPF assemblies fall under ISO 13485 expectations, which increases barriers for new entrants. Over time, this favors incumbents that can validate aseptic filling, stability, and component compatibility at scale, protecting growth in preservative-free multi-dose lines.

By Distribution Channel: Retail Pharmacy Share Erodes as Online Gains Velocity

Retail pharmacies held 46.34% of sales in 2025 and remain the principal touchpoint for impulse purchases, immediate symptom relief, and refills that align with prescription services in-store. National chains and regionals maintain broad shelves with OTC lubricants and adjacent prescription therapies that enable side-by-side counseling and bundling. The demulcent eye drops market is gradually diversifying its routes to consumers as direct-to-consumer fulfillment trims friction for chronic users and offers predictable delivery cycles. The online channels on the other hand, recorded the fastest growth outlook at 8.45% CAGR to 2031. Partnerships that remove prior authorization pain points and coordinate mail-order shipping for dry-eye prescriptions show how access models are evolving for ocular surface care households. Subscription storefronts that auto-ship lubricants strengthen adherence and reduce gaps in daily use, and user adoption metrics suggest this approach is becoming durable for chronic symptom clusters.

Hospital pharmacies and specialty clinics will continue to serve complex ocular care needs such as serum drops or higher-strength immunomodulators, but their role in first-line demulcent adoption is narrower. The demulcent eye drops market also reaches contact-lens wearers at optical retailers, yet category education and regimen differentiation remain strongest where clinicians and pharmacists reinforce preservative-free benefits for frequent users. Regulatory context shapes the channel mix by country, with U.S. OTC monographs enabling direct shelf access and Japan typically routing preservative-free hyaluronate through prescription channels first before later OTC availability at lower concentrations. Capacity investments by leading manufacturers and packaging improvements are expanding SKU breadth for online markets, which further supports the steady shift of chronic-use lubricants into mail-order and subscription formats.

Geography Analysis

North America accounted for 36.47% share in 2025 as clinicians, payers, and retailers converged on wider access to preservative-free options across OTC and prescription-adjacent formats. In the United States, population statistics show that tens of millions of adults report vision difficulty, which underscores the large base of consumers who seek accessible daily relief through lubricants. Recalls in 2023 and again in 2026 heightened public awareness of sterility standards and catalyzed more robust oversight of manufacturers, a trend that supports established brands with validated aseptic lines. Expansion investments by leading companies in the region point to ongoing commitment to domestic supply reliability and scaled throughput capacity for preservative-free lines[4]“Alcon Expands Manufacturing in West Virginia With $81 Million Investment,” Vision Monday, visionmonday.com. The demulcent eye drops market continues to reflect premiumization in product formulation and packaging with extensive presence across national retail and e-commerce.

Asia-Pacific is expected to deliver a 9.34% CAGR through 2031 as older demographics, urban lifestyles, and higher screen exposure elevate symptom intensity and frequency. Large-scale manufacturing projects in China are timed to bring substantial sterile capacity online by 2027, which aligns production with rising domestic demand for preservative-free daily-use drops. South Korea’s nationwide data show elevated dry-eye prevalence, particularly among women and older age groups, which supports the use of preservative-free single-use hyaluronate in clinical practice. In India, contact-lens growth and urban air quality challenges amplify ocular surface stress and expand the need for daily lubrication products in volume-led price tiers. Japan’s guidance encourages preservative-free hyaluronate in sensitive or chronic regimens, and this practice structure complements the adoption of MDPF and single-use lines across use cases. The demulcent eye drops market is prepared to balance volume growth with packaging advances that serve high-frequency users across tiered price points.

Europe balances mature demand with continued innovation in preservative-free systems and specialized formulations. Clinical guidance in Germany recommends hyaluronic acid for dryness and panthenol for irritation while cautioning against prolonged use of preservatives, especially in frequent users, which supports continued share for preservative-free ranges. Health systems differ in how they route dry-eye therapies across reimbursement channels and OTC, which results in varied mix between pharmacy-led sales and clinician-directed prescribing. Portfolio moves in Europe include acquisitions that expand local ophthalmology offerings across five major markets and broaden access to dry eye and related therapies, with integration plans aimed at improving scale and distribution efficiency. The demulcent eye drops market also benefits from research partnerships in the region designed to advance disease-modifying approaches that complement daily lubrication and comfort regimens. Together, these drivers create a stable foundation for preservative-free lines, biomimetic excipients, and dosing configurations that better match long-term symptom management.

Competitive Landscape

Competitive intensity remains high as the top five suppliers together represent a significant but not dominant share, and retailer brands continue to press on margins in standard formulations. Strategic disclosures indicate a shift toward premium hybrids and next-generation excipients in daily regimens, as seen in plans to pair anti-inflammatory mechanisms with water-free vehicles for evaporative symptoms and to position launches later in the decade. Capacity projects in China demonstrate how leading incumbents are preparing for sustained volume growth in preservative-free and sterile-packaged products, which can reinforce supply resiliency in high-growth urban markets. The demulcent eye drops market is also observing increased alignment between clinician guidance and retail assortments, which accelerates the shift toward preservative-free multi-dose systems in higher usage cohorts.

Recent product launches at national retailers reflect premium repositioning, such as vitamin-enriched and antioxidant-loaded preservative-free formulations that aim to improve day-one comfort and repeat purchase intent. These moves complement adjacent categories like oral supplements designed to influence tear film quality and to reduce surface stress, although such adjuncts do not replace the need for frequent lubrication in heavy screen or evaporative conditions. Mergers and acquisitions have expanded European ophthalmology franchises with dozens of branded products that address dry eye, glaucoma, and specialty nutraceuticals, with integration targeted to increase operating leverage and cross-market access. The demulcent eye drops market benefits indirectly from these transactions as companies streamline distribution and scale manufacturing for preservative-free systems across geographies.

Partnerships between manufacturers and research institutes in Asia reflect the long-term pursuit of disease-modifying therapies that can coexist with supportive demulcent regimens. These initiatives fund translational pipelines in ocular surface disease and help align clinic-based innovation with future commercial production runs. Capacity expansion and domestic manufacturing investment in North America also support continuity of supply in sterile packaging, strengthening consumer confidence after high-profile recalls. The demulcent eye drops market remains open to disruption from delivery-device advances and micro-dose platforms that can further reduce waste and improve dosing precision, while near-term competition will likely concentrate on preservative-free growth, DTC-ready pack sizes, and regimen-linked product families.

Demulcent Eye Drops Industry Leaders

AbbVie (Allergan)

Alcon

Bausch + Lomb

Santen Pharmaceutical Co., Ltd.

Laboratoires Théa

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Lupin completed its acquisition of VISUfarma B.V. from GHO Capital Partners for an enterprise value of approximately EUR 190 million (USD 205.2 million), expanding its European ophthalmology portfolio with over 60 branded products across Italy, UK, Spain, Germany, and France; the transaction adds differentiated dry-eye, glaucoma, and specialty nutraceutical SKUs to Lupin's existing specialty-care platform and is expected to be accretive to growth and margin profiles.

- December 2025: Santen Pharmaceutical and the Singapore Eye Research Institute launched SONIC 2.0, a three-year SGD 21 million (USD 15.5 million) joint research initiative to accelerate translational development of disease-modifying therapies for glaucoma; ocular surface diseases including dry eye, myopia, and presbyopia.

Global Demulcent Eye Drops Market Report Scope

The demulcent eye drops market comprises over‑the‑counter and prescription ophthalmic products formulated with lubricating and moisture‑retaining agents that soothe, protect, and hydrate the ocular surface to relieve symptoms of dry eye and ocular irritation. These products are widely used for routine eye comfort, chronic dry eye management, contact‑lens–related dryness, and post‑procedural care, driven by rising screen exposure, aging populations, and increasing preference for preservative‑free formulations.

The demulcent eye drops market is segmented by active ingredient into glycerin, polyethylene glycol, and propylene glycol demulcents, cellulose derivatives, sodium hyaluronate, oil‑based emulsion tears, polyvinyl alcohol or povidone, and dextran 70 combinations, by formulation comprising preserved multi‑dose, preservative‑free unit‑dose, and preservative‑free multi‑dose systems, by distribution channel including retail pharmacies, hospital pharmacies, online channels, ophthalmic and optical stores, and supermarkets and hypermarkets. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Glycerin / PEG / PG demulcents |

| Cellulose derivatives |

| Sodium hyaluronate (HA) |

| Oil-based Emulsion Tears |

| Polyvinyl Alcohol / Povidone |

| Dextran 70 Combinations |

| Preserved multi-dose |

| Preservative-free unit-dose (vials) |

| Preservative-free multi-dose (MDPF) |

| Retail Pharmacies |

| Hospital Pharmacies |

| Online Channels |

| Ophthalmic & Optical Stores |

| Supermarkets & Hypermarkets |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Active Ingredient | Glycerin / PEG / PG demulcents | |

| Cellulose derivatives | ||

| Sodium hyaluronate (HA) | ||

| Oil-based Emulsion Tears | ||

| Polyvinyl Alcohol / Povidone | ||

| Dextran 70 Combinations | ||

| By Formulation | Preserved multi-dose | |

| Preservative-free unit-dose (vials) | ||

| Preservative-free multi-dose (MDPF) | ||

| By Distribution Channel | Retail Pharmacies | |

| Hospital Pharmacies | ||

| Online Channels | ||

| Ophthalmic & Optical Stores | ||

| Supermarkets & Hypermarkets | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size and growth outlook for the demulcent eye drops market?

The demulcent eye drops market size reached USD 2.28 billion in 2025 and is projected to reach USD 3.31 billion by 2031 at a 6.6% CAGR.

Which formulation is growing the fastest within demulcent eye drops?

Preservative-free multi-dose bottles lead growth with an 8.78% CAGR through 2031, supported by sterile-closure systems that enable months-long use without preservatives.

Which active ingredients are most important in demulcent eye drops?

Cellulose derivatives anchor volume with 33.63% share in 2025, while sodium hyaluronate is the fastest-growing ingredient at 9.24% CAGR through 2031 due to superior moisture binding and comfort.

How are distribution channels changing for demulcent eye drops?

Retail pharmacies held 46.34% share in 2025, while online and direct-to-consumer channels are expanding as subscription and mail-order programs improve convenience for chronic users.

Which regions lead demand for demulcent eye drops today?

North America led with 36.47% share in 2025, while Asia-Pacific is expected to be the fastest-growing region through 2031 as capacity expands and clinical adoption of preservative-free formats increases.

What regulatory or quality factors are shaping the demulcent eye drops landscape?

Recalls in 2023 and 2026 heightened sterility expectations and compliance costs, favoring manufacturers with validated aseptic production and preservative-free multi-dose packaging systems.

Page last updated on: