Decentralized Clinical Trials Contract Research Organization (CRO) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

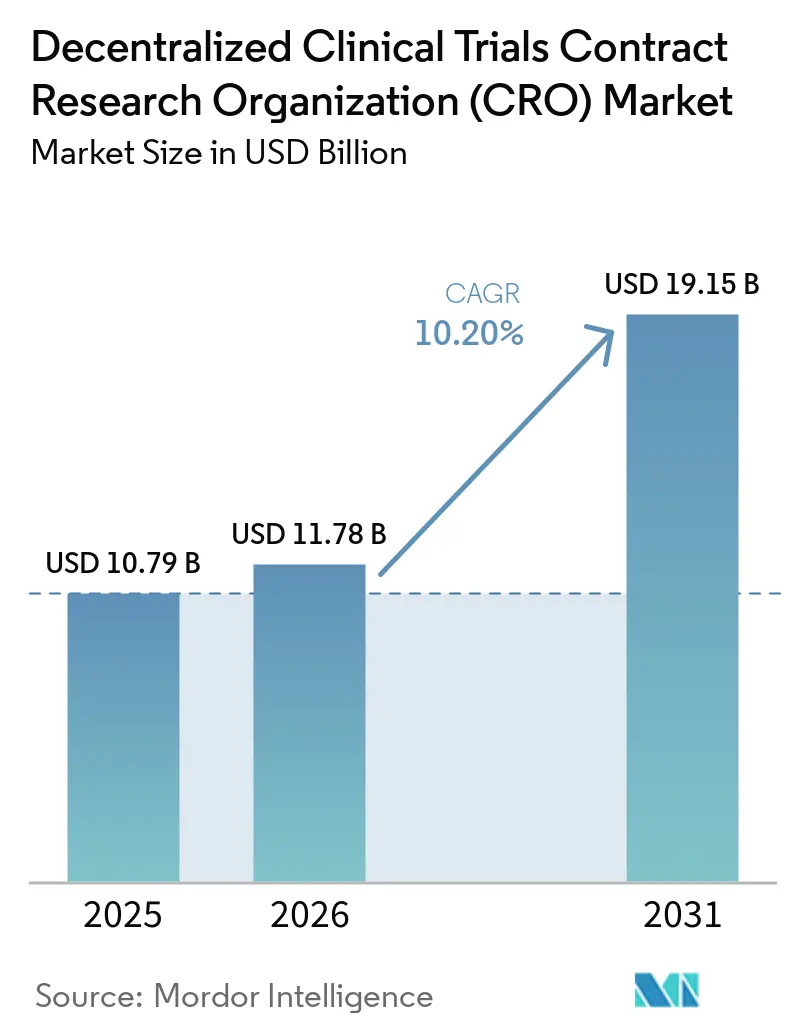

| Market Size (2026) | USD 11.78 Billion |

| Market Size (2031) | USD 19.15 Billion |

| Growth Rate (2026 - 2031) | 10.20% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

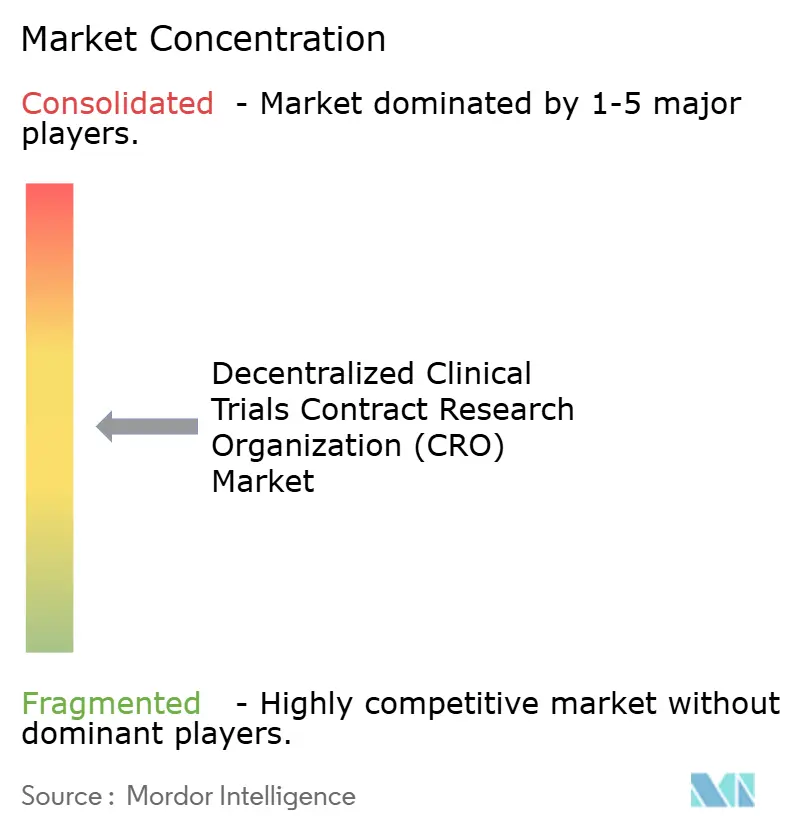

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Decentralized Clinical Trials Contract Research Organization (CRO) Market Analysis by Mordor Intelligence

The Decentralized Clinical Trials Contract Research Organization Market size is projected to expand from USD 10.79 billion in 2025 and USD 11.78 billion in 2026 to USD 19.15 billion by 2031, registering a CAGR of 10.20% between 2026 to 2031.

Sponsors are shifting toward patient-centric enrollment models that compress timelines and trim fixed site costs, while regulators in the United States, Europe, and China have issued guidance that legitimizes remote data capture, telemedicine visits, and hybrid consent. Full-service CROs remain the largest revenue contributors, yet modular eClinical software is eroding their contract share as sponsors license platforms directly and purchase functional services à la carte. Continuous investment in artificial-intelligence recruitment engines and wearable-sensor integration underscores the market’s technology pivot, even as cybersecurity risks and data-privacy fragmentation add budgetary and compliance burdens. On balance, rising therapeutic complexity and the need for real-world evidence keep growth firmly positive despite cost headwinds and talent shortages.

Key Report Takeaways

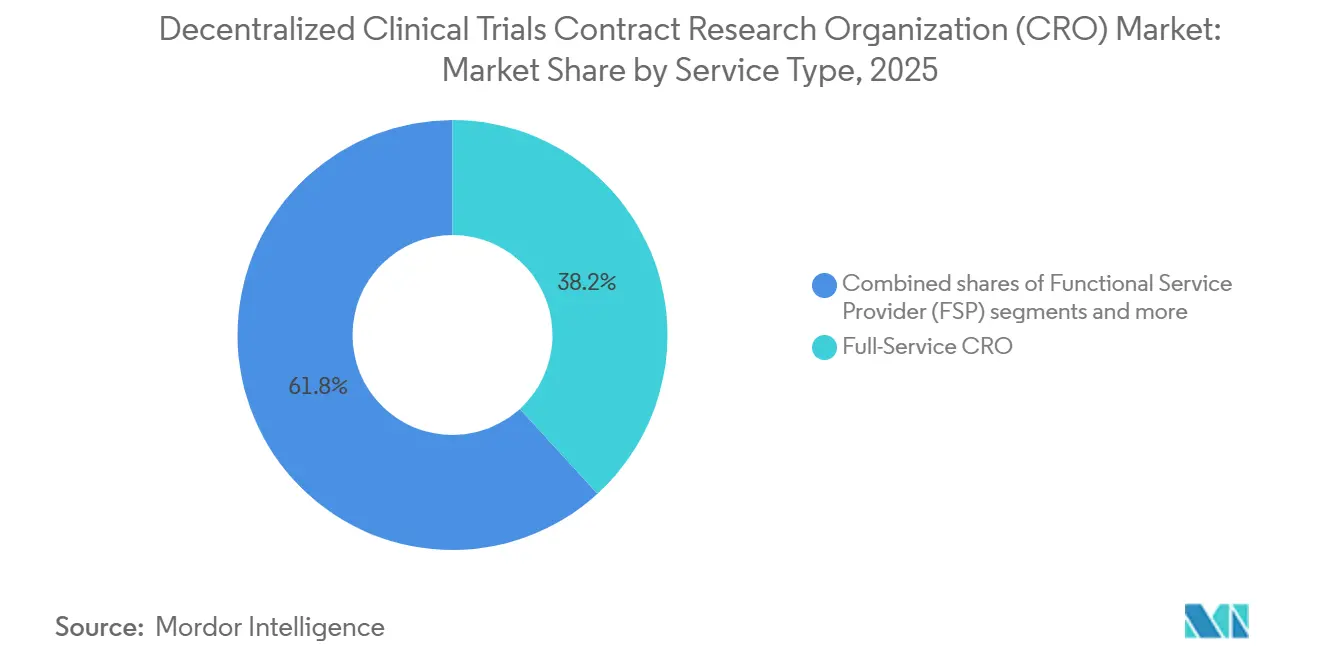

- By service type, full-service CROs led with 38.23% revenue share in 2025; eClinical platform provision is forecast to expand at a 12.00% CAGR through 2031.

- By the trial phase, Phase III commanded 55.23% revenue share in 2025; Phase IV post-marketing surveillance is advancing at an 11.50% CAGR through 2031.

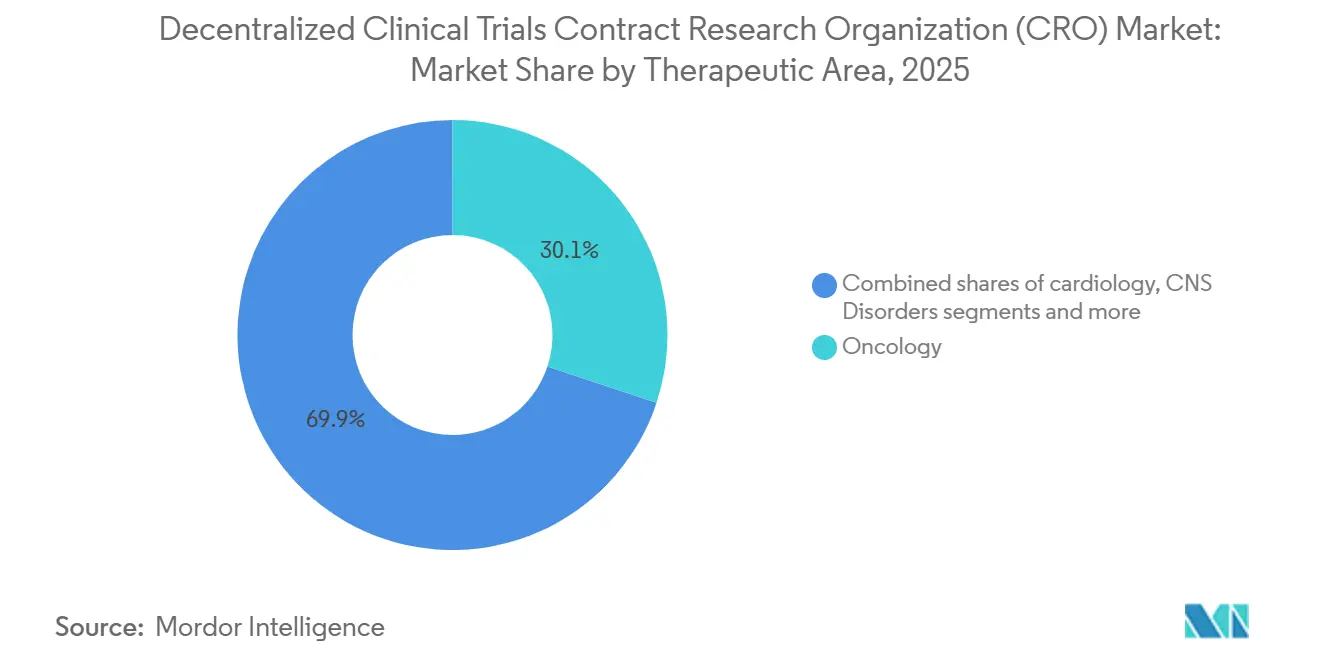

- By therapeutic area, oncology captured 30.00% of 2025 revenue; rare diseases are projected to grow at an 11.20% CAGR through 2031.

- By end-user, pharmaceutical and biotechnology companies accounted for 60.12% of 2025 spending; small and mid-sized sponsors are set to expand at an 11.25% CAGR through 2031.

- By geography, North America held 40.00% market share in 2025; Asia-Pacific is poised for a 10.80% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Decentralized Clinical Trials Contract Research Organization (CRO) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sponsor push for patient-centric, faster recruitment models | +2.8% | Global, early adoption in North America and Western Europe | Medium term (2-4 years) |

| Rapid cloud eClinical platform adoption | +2.3% | Global, strongest in North America and Asia-Pacific tech hubs | Short term (≤2 years) |

| Regulatory green lights for hybrid/decentralized designs | +1.9% | North America, Europe, and expanding to Asia-Pacific | Medium term (2-4 years) |

| CRO investment in AI-driven RWD recruitment engines | +1.5% | North America, Europe, China, India | Medium term (2-4 years) |

| Home-health nursing networks for last-mile procedures | +1.2% | North America, Western Europe, and urban Asia-Pacific | Long term (≥4 years) |

| LEO-satellite connectivity for rural data streaming | +0.5% | Rural regions worldwide, pilots in North America and Australia | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Sponsor Push for Patient-Centric, Faster Recruitment Models

Site-visit burden is the leading cause of screen failure and mid-study dropout, so sponsors are redesigning protocols around participant convenience. FDA guidance documents published in 2024 indicate that patient-centric approaches cut enrollment timelines by 30-40% versus traditional designs [1]U.S. Food and Drug Administration, “Decentralized Clinical Trials for Drugs, Biological Products, and Devices,” fda.gov.

Pharmaceutical companies now embed patient advisory boards during protocol drafting, allocate 20-25% of recruitment budgets to concierge services such as home phlebotomy, and rely on CRO networks of mobile nurses to deliver investigational products directly to participants. These tactics resonate most in chronic-disease studies where adherence underpins statistical power, giving CROs with established home-health resources a defensible edge. Venture-backed biotechs lacking in-house engagement infrastructure are the fastest adopters, underpinning the 11.25% CAGR forecast for small and mid-sized sponsors.

Rapid Cloud eClinical Platform Adoption

Unified cloud environments have moved from optional to essential as sponsors demand real-time data visibility and adaptive protocol control. Veeva Systems logged USD 676.2 million in R&D cloud revenue for Q3 FY 2025, a 15% year-over-year increase fueled by migrations from on-premise tools to its Vault Clinical suite [2]Veeva Systems, “Q3 FY 2025 Earnings Report,” ir.veeva.com. Medidata, Oracle, and other vendors now integrate wearable streams, ePROs, and tele-visit archives into single audit trails, trimming reconciliation labor by 40-50%. Sponsors increasingly license these platforms directly, then tap functional providers for niche tasks, accelerating platform revenue growth at a 12.00% CAGR and pressuring full-service CROs to form white-label partnerships or acquire technology assets.

Regulatory Green-Lights for Hybrid / Decentralized Designs

The FDA’s September 2024 guidance codified acceptable practices for remote consent, telemedicine investigator visits, and home specimen collection, eliminating ambiguity that once deterred cautious sponsors. The European Medicines Agency issued parallel recommendations with GDPR safeguards, while China’s NMPA cut median review times for decentralized protocols to 60 days, signaling official support for hybrid designs [3]European Commission, “General Data Protection Regulation Compliance,” ec.europa.eu. India’s CDSCO similarly cleared remote consultations for non-invasive studies. These synchronized policies allow multinational sponsors to meet diverse regulatory expectations through one harmonized protocol, rewarding CROs that have built deep regulatory-affairs capabilities across regions.

CRO Investment in AI-Driven RWD Recruitment Engines

Artificial-intelligence models now mine electronic health records, claims, and registries to flag eligible patients with up to 87% accuracy, well above manual chart reviews. IQVIA integrates data from 1.5 billion anonymized patient records, giving sponsors predictive enrollment velocity and dynamic budget control. Parexel’s dropout-risk algorithms trigger retention interventions before withdrawals occur, and Labcorp’s machine-learning screeners shorten oncology trial screening time by 42%. Early adopters report double-digit time-to-market savings, reinforcing AI investment as a strategic priority for all top-tier CROs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cross-border data-privacy & cyber-security gaps | -1.8% | Global, acute in Europe and cross-border trials | Short term (≤2 years) |

| Fragmented Asia-Pacific / LATAM regulatory pathways | -1.3% | Asia-Pacific and LATAM key markets | Medium term (2-4 years) |

| Digital-skill shortage at trial sites | -0.9% | Community sites worldwide, emerging markets worst hit | Medium term (2-4 years) |

| Wearable-sensor kit price inflation | -0.7% | Global, all sponsors using remote devices | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Cross-Border Data-Privacy & Cyber-Security Gaps

Healthcare data breaches surged in Q1 2024, with 145 incidents exposing over 90 million records and stalling trial timelines by up to six months. Europe’s GDPR requires data to stay within EU borders unless equivalent protections are proven, forcing sponsors to run separate cloud instances and adding 10-15% to IT budgets. The United States operates under a patchwork of state laws, such as CCPA, complicating multi-state consent workflows. Sponsors now mandate penetration tests, cyber-insurance, and data-residency clauses within CRO contracts, but residual risk could push conservative studies psychiatric and pediatric trials back toward traditional, site-based designs.

Fragmented Asia-Pacific / LATAM Regulatory Pathways

Unlike FDA–EMA coordination, Asia-Pacific and Latin America each follow divergent approval rules that extend trial startup by 6-12 months. China’s NMPA often requests domestic bridging studies even when global Phase III data are available. India’s CDSCO permits remote consultations, yet state-level telemedicine limits add uncertainty. Brazil’s ANVISA and Argentina’s ANMAT hold independent, lengthy review timelines of 180–240 days. These frictions favor large CROs with mature regulatory-affairs teams and raise entry barriers for smaller providers trying to expand outside their home regions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Platform Providers Capture Margin as Sponsors Unbundle Contracts

Full-service vendors commanded 38.23% of the decentralized clinical trials CRO market share in 2025, reflecting the historical bias for single-vendor accountability. The decentralized clinical trials CRO market size tied to eClinical platform provision is projected to widen quickly as this niche records a 12.00% CAGR, powered by direct licensing deals with pharmaceutical IT teams. In parallel, functional specialists in recruitment or data analytics underbid full-service rivals by 20-30% on discrete work packages, gaining traction among cost-sensitive sponsors. Platform providers, therefore, sit at the fulcrum of the value chain, capturing high-margin subscription fees while allowing sponsors to cherry-pick operational partners.

Patient-recruitment services now hold a significant portion of total study budgets, a share expected to climb as competitive pipelines hinge on speed to first-patient-first-visit. Data-management houses embed AI to automate safety signals, letting sponsors amend eligibility mid-stream without halting enrollment. As a defensive move, full-service CROs have launched acquisition sprees to secure proprietary tech, yet integration risks threaten near-term margins. Stand-alone software vendors face their own challenge: convincing sponsors that elegant code can substitute for years of operational know-how when trials turn complex.

By Trial Phase: Post-Marketing Surveillance Gains as Regulators Demand Real-World Evidence

Phase III trials collected 55.23% of the decentralized clinical trials CRO market revenue in 2025, underpinned by big-ticket oncology and rare-disease protocols often budgeted above USD 50 million. Real-world evidence mandates are, however, tilting growth toward Phase IV surveillance, which is advancing at an 11.50% CAGR. Regulators on both sides of the Atlantic accept electronic health records and insurance claims as valid endpoints, letting sponsors replace high-cost observational visits with continuous remote monitoring. This shift lifts the decentralized clinical trials CRO market size tied to post-approval studies and draws interest from payers keen on longitudinal safety data.

Early-phase studies remain partly sheltered from decentralization because dose escalation demands intensive, onsite safety surveillance. Even so, hybrid Phase II models that blend site-based procedures with tele-visits are gaining ground as wearable devices mature. CROs that master the operational choreography of synchronizing in-person biopsies with cloud-based ePRO uploads will hold clear leverage in bids for high-value adaptive programs.

By Therapeutic Area: Rare Diseases Leverage Decentralized Designs to Enroll Dispersed Patients

Oncology retained a 30.1% revenue share in 2025 after telemedicine protocols for chemotherapy support proved workable at scale. Continuous device-based monitoring of side effects improves data density and broadens access for rural and elderly patients, cementing oncology’s dominance. The decentralized clinical trials CRO market size linked to rare diseases, however, is rising faster, with an 11.20% CAGR as orphan-drug sponsors chase geographically scattered populations that rarely live near academic centers. Wearable diagnostics and home-visiting nurses make it feasible to hit enrollment targets when only a few thousand eligible patients exist worldwide.

Cardiology studies increasingly rely on remote ECG patches and blood-pressure cuffs, though calibration and battery life still provoke queries from cautious regulators. Central nervous system protocols lag in full decentralization because many cognitive assessments require investigator observation, but electronic symptom diaries and caregiver reports are gaining approval as supportive endpoints. Across all therapeutic areas, CROs capable of layering tele-health, logistics, and device management under a single governance framework will win disproportionate bids.

By End-User: Small Biotechs Drive Demand for Turnkey Virtual-Trial Services

Large pharmaceutical and biotechnology companies supplied 60.12% of 2025 spending, but their procurement teams are fragmenting contracts across multiple vendors to secure best-in-class capabilities. Meanwhile, the decentralized clinical trials CRO market benefits from a fresh cohort of venture-backed biotechs that outsource nearly 100% of clinical operations and are forecast to expand at an 11.25% CAGR. These lean enterprises seek turnkey packages that blend regulatory strategy, platform access, and patient-engagement services under one invoice. Medical-device makers experiment with in-home usability studies that dovetail naturally with decentralized designs, reinforcing device-sector demand. Academic centers, though smaller in wallet size, gravitate toward low-cost eClinical tools, expanding the user mix further. CROs now calibrate sales playbooks to sponsor maturity: white-glove project-management bundles for first-time clinical researchers and modular, self-service portals for global pharma that want data control. Providers failing to tailor their offer risk being squeezed either by technology natives on price or by full-service giants on scope.

Geography Analysis

North America contributed 40.00% of decentralized clinical trials CRO market revenue in 2025 as FDA guidance resolved regulatory uncertainty and cloud infrastructure remained robust. U.S. sponsors dominate global R&D budgets and often pilot hybrid protocols domestically before global rollout, while Canada benefits from geographic proximity and Mexico attracts Hispanic-focused studies with cost relief. The decentralized clinical trials CRO market size in the region grows steadily, though cybersecurity insurance premiums and HIPAA audits inflate operating costs.

Asia-Pacific is the clear growth engine, set for a 10.80% CAGR through 2031. China shortened decentralized-protocol review timelines to 60 days in 2024, spurring 1,476 trial registrations in 2023 and an even higher tally in 2025. India leveraged labor costs 50-60% below U.S. levels and updated telemedicine rules to open its tier-2 and tier-3 cities to remote trials. Japan and Australia remain cautious but are piloting limited remote-monitoring frameworks. Regional CROs such as WuXi AppTec and Novotech thrive on proximity and local-language operations, although proposed U.S. legislation like the BIOSECURE Act clouds future U.S.–China collaboration.

Europe enjoys harmonized EMA guidance and established tele-health adoption, yet GDPR forces sponsors to operate Europe-only cloud instances, adding 10-15% to IT budgets. Germany, the United Kingdom, and France lead uptake, with Germany’s BfArM reimbursing digital-health applications. Latin America and the Middle East & Africa remain nascent. Brazil’s 180-day ANVISA review cycle and inconsistent connectivity hold back regional expansion, while Gulf states’ pilot programs focus mainly on diabetes and oncology, indicating potential but slow maturation.

Competitive Landscape

The decentralized clinical trials CRO market is moderately concentrated: IQVIA, Laboratory Corporation, ICON, Parexel, and Syneos Health capture the majority of global revenue. To defend margin, full-service giants have bought eClinical platforms and recruitment specialists. Recent examples include ICON’s USD 150 million Asia-Pacific network expansion and Labcorp’s AI matching engine. IQVIA’s USD 1.59 billion Technology Solutions segment evidences the pivot toward data as a service.

Pure-play software vendors such as Medidata, Veeva, and Oracle bypass intermediaries and partner directly with sponsors, capturing a significant percentage of contract value for platform subscriptions. Functional specialists, Premier Research in rare-disease recruitment or Worldwide Clinical Trials with blockchain consent exploit white-space niches that big CROs often overlook. Private-equity ownership of Parexel and the take-private of Syneos Health signal investor conviction that wider portfolios and scale synergies can lift EBITDA.

Regional challengers are also active. WuXi AppTec and Tigermed ride China’s policy tailwinds, though U.S.-centric sponsors are wary of potential restrictions. Novotech and PSI CRO leverage lower-cost Asia-Pacific hubs, while Science 37’s pivot to a hybrid model after overextension highlights execution risks. Across the board, differentiation now hinges on proprietary data, AI recruitment, and the breadth of home-health networks more than on geographic office count.

Decentralized Clinical Trials Contract Research Organization (CRO) Industry Leaders

IQVIA

Laboratory Corporation

ICON

Parexel

Syneos Health

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Keith Tode appointed as executive vice president at AMC Health to strengthen its strategic leadership and operational capabilities in decentralized clinical trials.

- January 2025: ICON plc rolled out four AI solutions iSubmit, Mapi Research Trust COA, FORWARD+, and OMR AI Navigation Assistant, to streamline startup, document management, and resource forecasting.

- January 2025: IQVIA partnered with a nationwide home-health network covering 40 U.S. states to support invasive procedures in Phase III oncology programs.

Global Decentralized Clinical Trials Contract Research Organization (CRO) Market Report Scope

As per the scope of the report, the decentralized clinical trials contract research organization (CRO) is a specialized partner that manages clinical research using a patient-centric, technology-enabled model rather than relying on traditional physical sites.

The Decentralized Clinical Trials Contract Research Organization (CRO) Market is segmented by service type, trial phase, therapeutic area, end users, and geography. By service type, the market is categorized into Full-Service CRO, Functional Service Provider (FSP), patient recruitment & retention, data management & analytics, and eClinical Platform Provision. By the trial phase, the market is divided into Phase I, Phase II, Phase III, and Phase IV / Post-marketing. By therapeutic area, it is segmented into oncology, cardiology, CNS disorders, rare diseases, and others. By End Users, the segmentation includes pharmaceutical & biotechnology companies, medical device companies, academic & research institutes, and small & mid-sized sponsors. Geographically, the market is segmented across North America, Europe, Asia-Pacific region, the Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Full-Service CRO |

| Functional Service Provider (FSP) |

| Patient Recruitment & Retention |

| Data Management & Analytics |

| eClinical Platform Provision |

| Phase I |

| Phase II |

| Phase III |

| Phase IV / Post-Marketing |

| Oncology |

| Cardiology |

| CNS Disorders |

| Rare Diseases |

| Others |

| Pharmaceutical & Biotechnology Companies |

| Medical Device Companies |

| Academic & Research Institutes |

| Small & Mid-Sized Sponsors |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Service Type | Full-Service CRO | |

| Functional Service Provider (FSP) | ||

| Patient Recruitment & Retention | ||

| Data Management & Analytics | ||

| eClinical Platform Provision | ||

| By Trial Phase | Phase I | |

| Phase II | ||

| Phase III | ||

| Phase IV / Post-Marketing | ||

| By Therapeutic Area | Oncology | |

| Cardiology | ||

| CNS Disorders | ||

| Rare Diseases | ||

| Others | ||

| By End-User | Pharmaceutical & Biotechnology Companies | |

| Medical Device Companies | ||

| Academic & Research Institutes | ||

| Small & Mid-Sized Sponsors | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the decentralized clinical trials CRO market in 2026?

The decentralized clinical trials CRO market size is expected to reach USD 11.78 billion in 2026.

What CAGR is forecast for decentralized trials CRO providers between 2026 and 2031?

A 10.20% CAGR is projected for 2026-2031.

Which region is expanding fastest for decentralized trial services?

Asia-Pacific is forecast to grow at a 10.80% CAGR through 2031, outpacing all other regions.

Which service type is gaining share fastest?

EClinical platform provision is expected to record a 12.00% CAGR, reflecting direct licensing by sponsors.

Why are Phase IV studies an attractive growth area?

Regulators now mandate real-world evidence, and decentralized surveillance cuts per-patient monitoring costs by up to 50%.

Page last updated on: