DDOS Protection and Mitigation Security Market Size and Share

Market Overview

| Study Period | 2025 - 2031 |

|---|---|

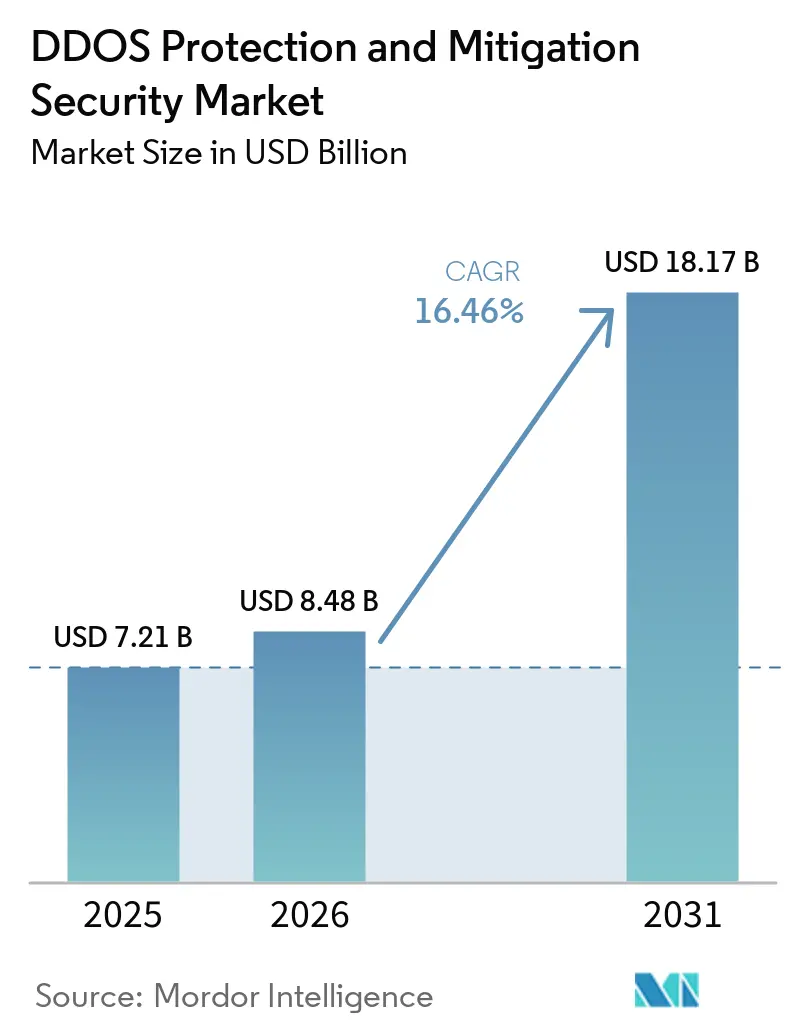

| Market Size (2026) | USD 8.48 Billion |

| Market Size (2031) | USD 18.17 Billion |

| Growth Rate (2026 - 2031) | 16.46% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

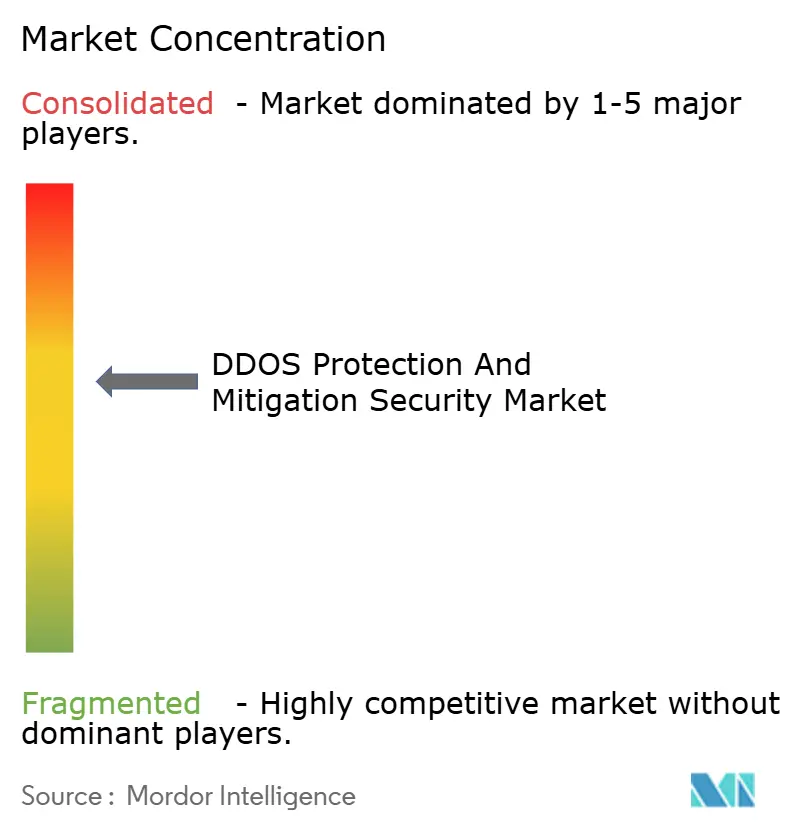

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

DDOS Protection and Mitigation Security Market Analysis by Mordor Intelligence

The DDoS protection and mitigation security market size is projected to be USD 7.21 billion in 2025, USD 8.48 billion in 2026, and reach USD 18.17 billion by 2031, growing at a CAGR of 16.46% from 2026 to 2031. Heightened attack sophistication, illustrated by a 111% surge in incidents during 2024, accelerates enterprise investment in multi-layered protection platforms. Cloud-first security mandates, the growing appeal of on-demand scrubbing capacity, and the rapid commoditization of attack tools collectively reinforce demand momentum. Meanwhile, AI-driven detection engines and behaviour analytics mature, allowing vendors to differentiate on automated response speed rather than raw bandwidth alone. Competitive focus therefore shifts toward integrated, cloud-native architectures that unify network, application, and DNS safeguards for latency-sensitive use cases.

Key Report Takeaways

- By component, services commanded 46.33% revenue share in 2025, while software solutions are projected to advance at an 18.16% CAGR through 2031.

- By deployment mode, cloud platforms captured 63.21% of the DDoS protection and mitigation security market share in 2025, whereas hybrid strategies are expected to expand at 18.24% CAGR to 2031.

- By organization size, large enterprises held a 69.84% spending share in 2025; however, the SME segment is forecast to accelerate at a 17.88% CAGR through 2031.

- By end-user industry, IT and telecom led with a 28.19% revenue share in 2025, while e-commerce and retail are projected to grow at an 18.19% CAGR over the forecast horizon.

- By geography, North America retained a 39.61% share in 2025; the Asia-Pacific region is set to record the fastest regional CAGR at 17.93% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global DDOS Protection and Mitigation Security Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in Sophisticated Multi-Vector Attacks | +3.2% | Global, with concentration in North America and Europe | Short term (≤ 2 years) |

| Proliferation of IoT and Edge Devices | +2.8% | Asia-Pacific core, spill-over to North America and Europe | Medium term (2-4 years) |

| Rapid Adoption of Cloud-Based Services | +2.1% | Global, led by North America and Europe | Short term (≤ 2 years) |

| Mandates for Zero-Trust Architecture | +1.9% | North America and EU, expanding to Asia-Pacific | Medium term (2-4 years) |

| Growing Availability of DDoS-for-Hire Services | +1.7% | Global, particularly affecting SME segments | Short term (≤ 2 years) |

| Integration of AI for Real-Time Mitigation | +1.4% | North America and Europe, early adoption in Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in Sophisticated Multi-Vector Attacks

Google mitigated an unprecedented 398 million HTTP/2 rapid-reset requests per second in August 2024, demonstrating how modern campaigns blend volumetric, protocol, and application vectors.[1]Google LLC, “Largest DDoS Attack in History Mitigated by Google Cloud,” cloud.google.com Attackers are increasingly exploiting protocol quirks that bypass rate-limiting, compelling organizations to adopt behavioral analytics that profile legitimate traffic instead of relying solely on static signatures. Recorded average remediation costs of USD 2.5 million per incident underscore why enterprise security budgets increased by 45% year-over-year in 2024. As attacks traverse network, application, and DNS layers simultaneously, buyers prioritize unified visibility across vectors. Accordingly, the DDoS protection and mitigation security market favors platforms supplying correlated telemetry rather than standalone appliances.

Proliferation of IoT and Edge Devices

Cisco projects 29.3 billion connected devices by 2030, each of which could be a potential node in a botnet.[2]Cisco Systems, “2024 Cybersecurity Readiness Index,” cisco.com Industrial IoT rollouts magnify attack surfaces, yet many operational technology networks still lack inline mitigation. Edge workloads complicate legacy scrubbing, because detouring traffic to distant centers breaches the sub-10 millisecond latency envelope critical for industrial control. Manufacturing companies, therefore, procure on-premises or hybrid hardware, keeping inspection proximate to machines while reserving cloud capacity for volumetric overflow. The same dynamic arises in 5G network slices, where targeted assaults on specific service tiers necessitate fine-grained policy enforcement at the edge.

Rapid Adoption of Cloud-Based Services

Seventy-six percent of AWS enterprise customers now consume native security services, underscoring a shift from capital-expenditure (capex)- heavy hardware to elastic mitigation pools.[3]Amazon Web Services, “AWS Shield Advanced Service Overview,” aws.amazon.com Cloud scrubbing scales automatically during attack bursts, eliminating idle capacity costs. Azure’s DDoS Protection Standard absorbed multi-terabit floods in 2024 without user intervention, validating the economic rationale for cloud migration. Nonetheless, multi-tenant environments introduce shared-infrastructure exposure, spurring demand for isolation controls and dedicated protection instances. EU organizations implementing the NIS2 directives are increasingly defaulting to providers offering certified, regionally resident scrubbing nodes.

Mandates for Zero-Trust Architecture

OMB M-22-09 obliges U.S. federal agencies to embed DDoS mitigation within zero-trust frameworks by 2024. The directive cascades through defense contractors and state entities, reinforcing baseline adoption. Similar policy pressure emerges from Europe’s NIS2 mandate, creating synchronized procurement waves that favor vendors already cleared for government work. Requirements for continuous traffic validation and identity-centric segmentation reward suppliers integrating AI-driven analytics that adapt to contextual risk.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost of Advanced Mitigation Solutions | -1.8% | Global, particularly affecting SME segments | Medium term (2-4 years) |

| Limited Awareness Among SMEs | -1.2% | Global, concentrated in emerging markets | Short term (≤ 2 years) |

| False Positive Concerns in Automated Defenses | -0.9% | North America and Europe, early adopters of AI systems | Medium term (2-4 years) |

| Evolving Encryption Standards Hindering Traffic Inspection | -0.7% | Global, with regulatory emphasis in EU and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Cost of Advanced Mitigation Solutions

Enterprise-grade platforms, which require annual commitments of USD 50,000 to USD 500,000, price out many SMEs. The total cost of ownership doubles once training and tuning are added, nudging budget-constrained firms toward partial coverage that relies on firewalls alone. While vendors respond with pay-as-you-go tiers, functional gaps persist between simplified offerings and AI-rich premium bundles. The resulting bifurcation segments the DDoS protection and mitigation security market around spending power rather than threat exposure.

Limited Awareness Among SMEs

Kaspersky research finds that 38% of SME leaders underestimate their risk, despite a rising frequency of attacks. Generalist IT staff often misclassify malicious surges as routine traffic spikes, which can delay responses. Industry associations and public-sector campaigns aim to bridge knowledge gaps, but outreach is hindered in emerging economies where cybersecurity resources are scarce. Without broader education, SME adoption may lag, tempering near-term market velocity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Lead Integration Complexity

Services captured 46.33% of the DDoS protection and mitigation security market share in 2024, emphasizing how skill shortages compel outsourcing. Managed service providers supply 24/7 monitoring and incident response that 78% of organizations find difficult to sustain in-house. The DDoS protection and mitigation security market size allocation toward software, however, is rising fastest, with AI-enabled platforms forecast to grow at an 18.16% CAGR through 2031. Adaptive algorithms learn attack patterns in real time, automatically retuning mitigation thresholds, a feature that hardware appliances alone cannot emulate. Yet hardware remains vital for microsecond-sensitive sectors such as high-frequency trading, where deterministic latency is paramount. Hybrid service-plus-software bundles therefore emerge, offering managed expertise around customer-controlled policy engines. This combination allows clients to maintain oversight while delegating 24/7 operations to specialized personnel.

Hardware vendors address margin pressure by embedding accelerators and telemetry feeds into appliances that integrate directly with cloud scrubbing pools. Cloudflare’s Magic Transit processed 32 million HTTP requests per second during peak events, evidencing how cloud queuing complements on-premises packet filtering. As regulatory audits demand end-to-end traceability, integrated solutions that log traffic across services, software, and hardware elements gain procurement preference. Consequently, services remain the revenue anchor, software the growth engine, and hardware the latency hedge in an ecosystem increasingly orchestrated from unified dashboards.

By Deployment Mode: Cloud Dominance Accelerates

Cloud deployments accounted for 63.21% of 2024 revenue, reflecting buyers' preference for elastic economics. Volumetric mitigation in hyperscale clouds costs 60-70% less than comparable on-premises capacity when factoring in purchase, depreciation, and staffing. AWS Shield Advanced auto-scales to absorb terabit-class floods with no capacity planning, validating the utility model. Nevertheless, the DDoS protection and mitigation security market size encompasses niches where data sovereignty and sub-millisecond latency necessitate local inspection, particularly in payment clearing or industrial automation.

Hybrid patterns consequently prevail. Two-thirds of large enterprises blend cloud bandwidth with on-premises intelligence, ensuring that application-layer filtering remains closest to the origin servers. Edge computing amplifies the need for distributed policy coherence because traffic now traverses cloud, core, and edge. Vendors competing for new deployments must therefore supply centrally orchestrated platforms that detect once and enforce everywhere. As 5G rollouts increase the number of edge nodes, the architecture mix further favors cloud bursting backed by local enforcement.

By Organization Size: SME Adoption Accelerates Despite Constraints

Large organizations accounted for 69.84% of global spending in 2024, largely due to their extensive security staffing and compliance obligations. Yet, SMEs represent the fastest expansion path, with the segment forecasted to grow at a 17.88% CAGR through 2031. The shift arises because low-cost DDoS-for-hire portals enable unskilled actors to launch attacks, steadily raising SME risk exposure. Managed security service providers step into the void, delivering enterprise-grade defense as an operational expenditure. Cisco’s outcomes survey shows SMEs outsourcing mitigation enjoy 23% stronger security efficacy than peers running in-house setups.

Cost-optimized cloud bundles further democratize access, positioning the DDoS protection and mitigation security market size for broader distribution. Even so, funding limitations remain acute: 43% of small businesses still allocate insufficient cybersecurity budgets, slowing full-funnel conversion. Vendors winning SME mindshare, therefore, simplify onboarding, automate compliance mapping, and package transparency dashboards that minimize administrative burden.

By End-User Industry: E-Commerce Drives Growth Acceleration

IT and telecom providers accounted for 28.19% of revenue in 2024, reflecting their dual exposure as both network operators and high-value targets. Service level agreements promising 99.99% uptime elevate contractual liability, making comprehensive mitigation non-negotiable. E-commerce and retail, however, are projected to record an 18.19% CAGR through 2031, buoyed by peak-season application-layer assaults that trigger cart abandonment and brand erosion. For online retailers, even seconds of downtime translate directly into lost sales and customer defection, pushing adoption of pre-integrated web-application firewalls and bot management modules within broader DDoS suites.

Financial institutions remain heavy investors because Basel III and PCI DSS frameworks enforce continuous availability and transaction integrity, often mandating redundancies across multiple scrubbing vendors. The healthcare and government segments exhibit steady volume growth as privacy statutes tighten and critical infrastructure guidelines evolve. Across industries, buyers prize integrated reporting that aligns with audit checklists, leading vendors to embed compliance templates across sector-specific dashboards.

Geography Analysis

North America retained 39.61% of global revenue in 2025, anchored by consistent federal spending that tops USD 18 billion annually. Large cloud vendors and start-ups clustered in Silicon Valley accelerate product cycles, allowing local buyers to pilot emerging features early. Canada reflects a similar level of maturity, bolstered by critical infrastructure guidelines that align with U.S. zero-trust frameworks.

The Asia-Pacific region registers the swiftest expansion, with the DDoS protection and mitigation security market size in the region projected to grow at a 17.93% CAGR through 2031. China’s Cybersecurity Law requires localized data residency, prompting hybrid deployments that blend domestic scrubbing centers with international backbone capacity. India’s Digital India initiative raised federal cyber outlays 34% in 2024, reflecting a policy pivot from perimeter defense toward proactive resilience. Japan prioritizes manufacturing uptime and smart-factory continuity, creating sizable opportunities for low-latency hardware adjuncts.

Europe’s NIS2 directive imposes October 2024 deadlines for resilience across critical infrastructure. Procurement cycles are consequently expected to concentrate in 2024-2025 as operators seek certified, EU-domiciled scrubbing nodes. Nordic countries lead in cloud adoption, while Germany favors hybrid architectures to satisfy strict data-protection statutes. The Middle East and Africa show nascent growth driven by smart-city megaprojects and national oil company digitization, but face skills shortages that slow penetration. South America gradually scales adoption as banking regulation tightens, yet currency volatility can defer capital spending.

Competitive Landscape

The market remains moderately concentrated. Cloudflare expanded revenue 30% to USD 1.3 billion in 2024 by bundling content delivery, zero-trust access, and DDoS defense into a single edge platform. Akamai’s USD 3.8 billion top line underscores a similar full-stack strategy that couples security with compute at edge points. Hyperscale cloud providers, such as Amazon Web Services, Microsoft, and Google, integrate DDoS mitigation as native platform features, thereby reinforcing customer lock-in by eliminating the need for separate procurement.

Specialized vendors differentiate through AI-driven analytics and industry-specific modules. Radware targets financial services with ultra-low-latency appliances, while Neustar emphasizes DNS-centric mitigation for gaming and trading workloads. Recent acquisitions, such as Akamai-Guardicore for micro-segmentation and F5-Volterra for edge security, signal a race to integrate adjacent capabilities into broader zero-trust narratives.

Barriers to entry heighten as government contracts demand security clearances and compliance certifications, steering volume toward incumbents. Yet white-space opportunities persist around 5G slice protection and hybrid edge-cloud orchestration, where agile start-ups can out-innovate slower platform giants.

DDOS Protection and Mitigation Security Industry Leaders

Cloudflare Inc.

Akamai Technologies Inc.

Amazon Web Services Inc.

Microsoft Corporation

Google LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Microsoft introduced Azure Sovereign DDoS Protection for the European Union, providing dedicated in-region scrubbing aligned with NIS2 and GDPR requirements while guaranteeing 99.99% uptime through multi-zone redundancy.

- June 2025: Akamai commissioned new scrubbing centers in Mumbai and São Paulo, adding 5 Tbps of regional capacity and expanding its global footprint to 60 mitigation sites optimized for low-latency traffic diversion.

- March 2025: Amazon Web Services released Shield Advanced Edge AI, embedding machine-learning models into 450 border locations to cut detection latency below 100 microseconds for volumetric attacks exceeding 20 million packets per second.

- January 2025: Cloudflare activated its Quantum DDoS Defense upgrade, integrating post-quantum cryptography with real-time signatureless detection across its 310 global edge locations, raising total on-demand mitigation capacity to 300 Tbps.

Global DDOS Protection and Mitigation Security Market Report Scope

| Hardware |

| Software |

| Services |

| On-Premises |

| Cloud |

| Small and Medium Enterprises |

| Large Enterprises |

| IT and Telecom |

| BFSI |

| Government |

| E-Commerce and Retail |

| Healthcare |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Component | Hardware | ||

| Software | |||

| Services | |||

| By Deployment Mode | On-Premises | ||

| Cloud | |||

| By Organization Size | Small and Medium Enterprises | ||

| Large Enterprises | |||

| By End-User Industry | IT and Telecom | ||

| BFSI | |||

| Government | |||

| E-Commerce and Retail | |||

| Healthcare | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is the projected value of the DDoS protection and mitigation security market in 2031?

It is forecast to reach USD 18.17 billion by 2031.

How fast is the market expected to grow between 2026 and 2031?

The projected CAGR is 16.46%.

Which deployment mode leads current adoption?

Cloud platforms hold 63.21% revenue share.

Which end-user industry is expanding the quickest?

E-commerce and retail is forecast to grow at an 18.19% CAGR through 2031.

Why are SMEs becoming key buyers?

Affordable cloud bundles and rising attack exposure drive the SME segment, projected at a 17.88% CAGR.

Which region will witness the fastest growth?

Asia-Pacific is expected to expand at 17.93% CAGR through 2031.

Page last updated on: