Data Center And AI Server Printed Circuit Board Market Size and Share

Market Overview

| Study Period | 2026 - 2031 |

|---|---|

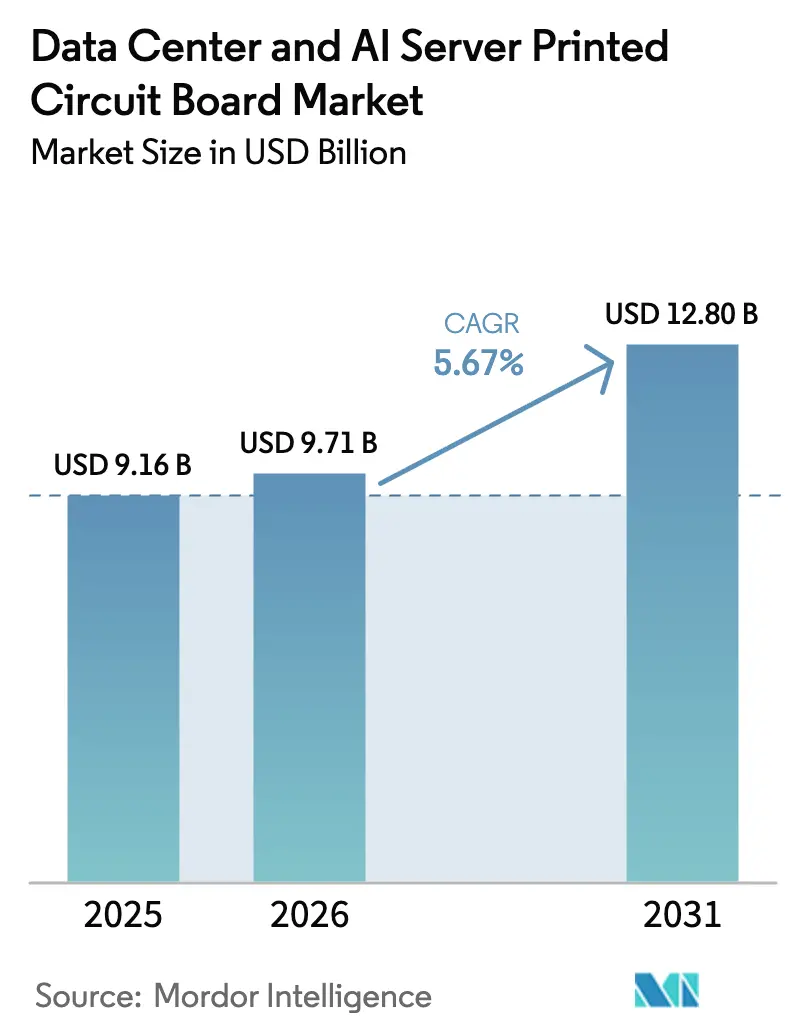

| Market Size (2026) | USD 9.71 Billion |

| Market Size (2031) | USD 12.80 Billion |

| Growth Rate (2026 - 2031) | 5.67% CAGR |

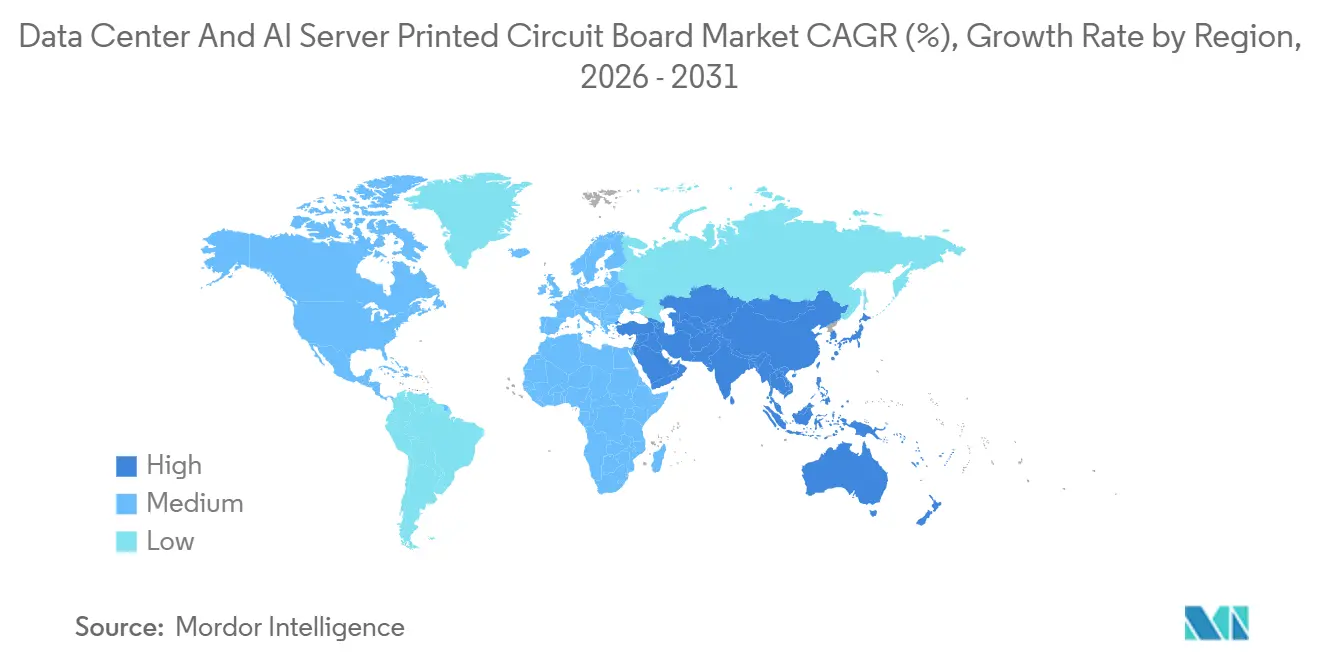

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Data Center And AI Server Printed Circuit Board Market Analysis by Mordor Intelligence

The Data Center And AI Server Printed Circuit Board Market size in 2026 is estimated at USD 9.71 billion, growing from 2025 value of USD 9.16 billion with projections showing USD 12.80 billion, growing at 5.67% CAGR over 2026-2031. Sustained capital spending on inference-optimized GPU and ASIC clusters, the migration to 800 GbE switch architectures, and a steep rise in rack-level thermal loads are expanding server refresh frequency and creating a larger installed base of high-layer-count boards. Shorter design-qualification windows, now averaging 12 months instead of the historical 18-24 months, are forcing fabricators to accelerate process upgrades, especially in laser-drilled micro-via and modified semi-additive lines. Asia-Pacific continues to dominate new capacity announcements because suppliers co-locate close to IC substrate fabs and copper-clad laminate mills, while U.S. export controls are re-routing Chinese demand to domestic vendors, amplifying near-term regional tightness. Suppliers that master high-speed low-loss laminates, embedded power rails, and glass-core pilots are positioned to capture co-packaged optics demand as 1.6 Tbps and 3.2 Tbps interface roadmaps move toward volume adoption.

Key Report Takeaways

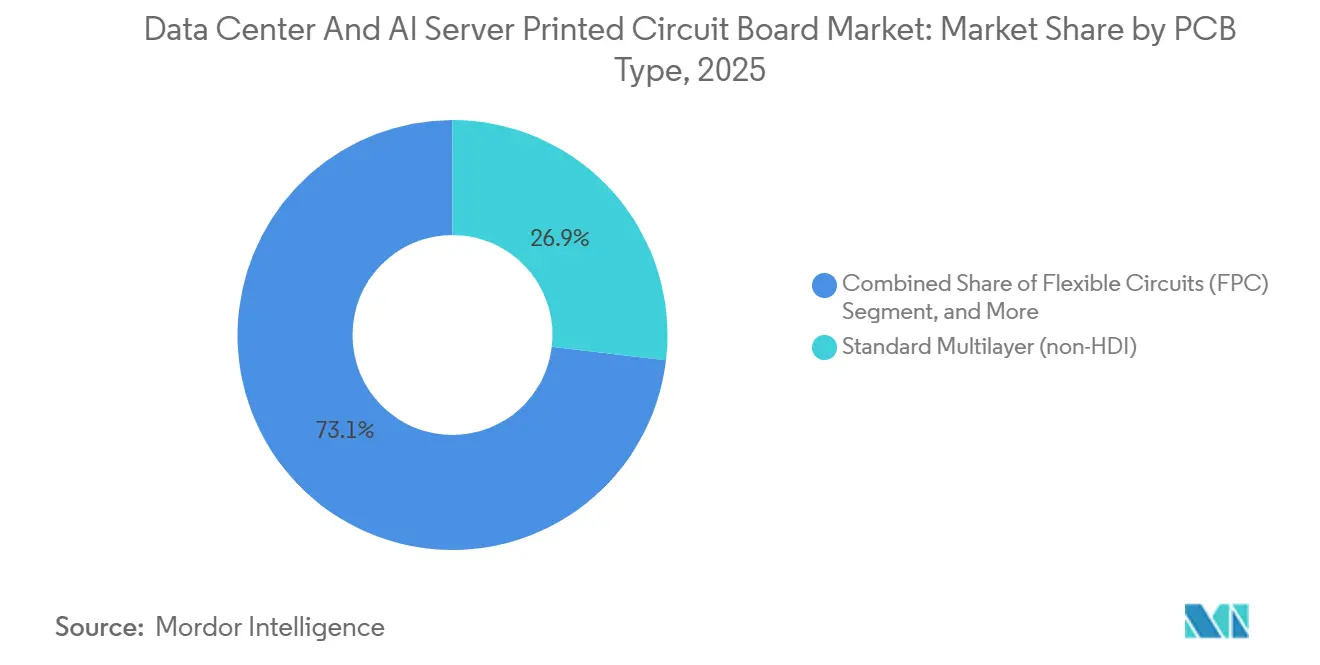

- By pcb type, standard multilayer captured 26.87% of the Data Center and AI Server Printed Circuit Board Market share in 2025, while flexible circuits are expanding at a 5.99% CAGR through 2031.

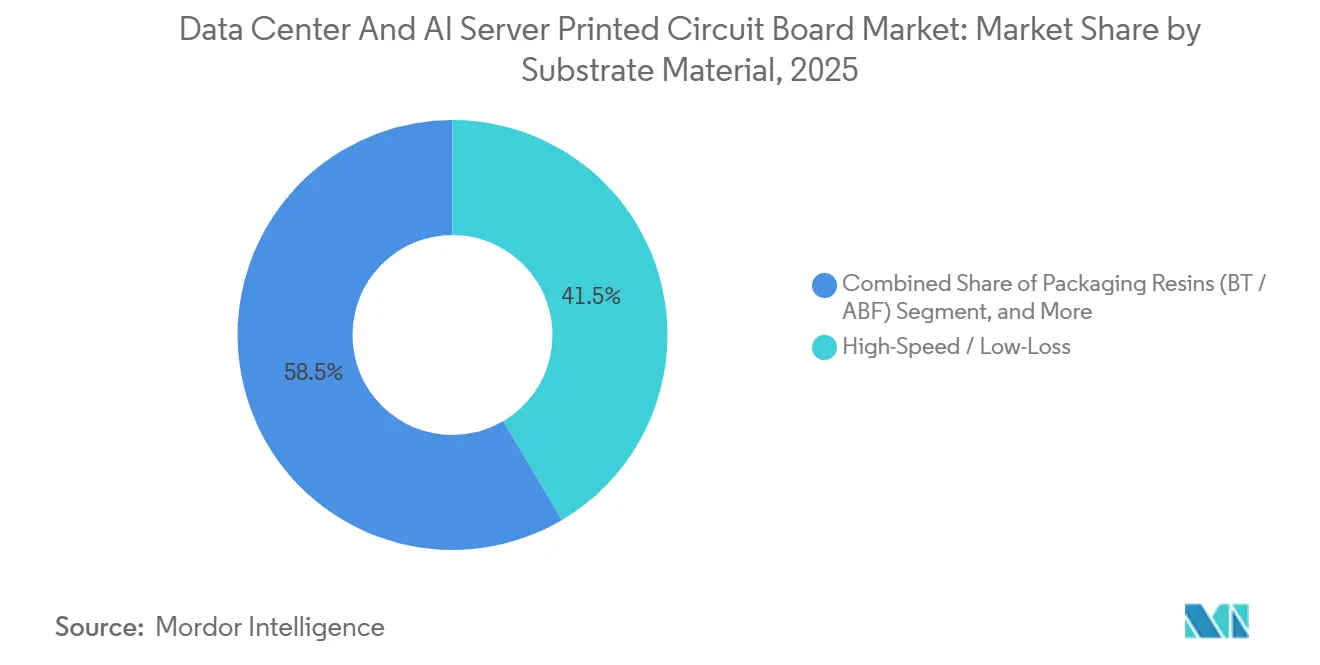

- By substrate material, high-speed low-loss laminates held 41.50% share of the Data Center and AI Server Printed Circuit Board Market size in 2025 and are advancing at a 6.63% CAGR through 2031.

- By geography, Asia-Pacific led with 82.54% revenue share in 2025; Asia-Pacific recorded the highest projected CAGR among developed regions at 6.25% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Data Center And AI Server Printed Circuit Board Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in AI Accelerator Adoption in Hyperscale Data Centers | +1.20% | Global, with concentration in North America and Asia-Pacific | Medium term (2-4 years) |

| Growing Rack Power Density Necessitating High-Performance PCBs | +0.90% | Global, led by North America and Western Europe | Short term (≤ 2 years) |

| Transition to Co-Packaged Optics Driving HDI and IC Substrate Demand | +0.80% | Asia-Pacific core, spill-over to North America | Medium term (2-4 years) |

| Rapid Expansion of Liquid Cooling Infrastructure | +0.70% | North America and Europe, emerging in China | Short term (≤ 2 years) |

| Emergence of Glass Core and Embedded Power Rail Technologies | +0.50% | Japan, South Korea, Taiwan | Long term (≥ 4 years) |

| On-site Renewable Energy Integration Enhancing Demand for High-Thermal PCBs | +0.30% | Global, early gains in Nordic Europe and US West Coast | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in AI Accelerator Adoption in Hyperscale Data Centers

Hyperscale’s installed more than 3.5 million AI accelerators during 2025, a 180% jump from 2024, and each new GPU card requires 32-layer boards with impedance-controlled differential pairs. NVIDIA H200 and AMD MI325X reference designs both rely online-and-space widths below 10 µm, compelling suppliers to adopt modified semi-additive processes that raise capital outlays but increase yield for sub-15 µm geometries. Meta disclosed that PCB procurement alone consumed roughly 8% of its USD 9.2 billion Q3 2025 AI infrastructure spend. The compression of design cycles is motivating fabricators to stock multiple high-speed laminate SKUs and dedicate quick-turn cells to GPU carrier and retimer boards, shrinking prototype lead time to less than six weeks. As hyperscale budgets remain skewed to inference clusters, the Data Center and AI Server PCB market should see recurring volume pull every two quarters instead of the prior 18-month rhythm.

Growing Rack Power Density Necessitating High-Performance PCBs

Average rack density reached 18 kW in Tier-3 facilities during 2025, and liquid-cooled deployments exceeded 40 kW, pushing PCB copper weights toward 3-4 oz and necessitating polyimide laminates rated above 180 °C glass-transition temperature.[1]Uptime Institute, “Global Rack Density Survey 2025,” uptimeinstitute.com Higher current loads also trip IEC 62368-1 creep-clearance thresholds, forcing redesigns of power connectors that delay qualifications up to three months.[2]International Electrotechnical Commission, “IEC 62368-1 Amendment 3,” iec.ch Voltage-drop mitigation now begins at the board-level by embedding 0.3 mm-pitch thermal vias beneath VRM stages, which lifts substrate cost by 15-20% but gives operators extra 5-7 °C thermal headroom. Board reliability targets escalate to 3,000 charge-discharge cycles for racks paired with on-site battery storage, removing low-cost FR-4 from the approved vendor list. These shifts collectively widen demand for premium high-Tg epoxy and polyimide blends within the Data Center and AI Server PCB market.

Transition to Co-Packaged Optics Driving HDI and IC Substrate Demand

Co-packaged optics reached volume shipment in 2025 and eliminates discrete pluggable transceivers, shrinking switch motherboard area by 30% and cutting power 20-25%. Implementation requires IC substrates with embedded optical waveguides and via densities above 10,000 vias/cm², creating yield challenges that keep first-pass success around 60-70%. Unimicron’s 14-layer CPO substrate, qualified in 2025, leverages 25 µm line-and-space traces and laser-drilled micro-vias to meet the thermal budget. Broad adoption hinges on OIF’s interface standard that harmonizes mechanical and thermal constraints, allowing switch OEMs to dual-source substrates. As 1.6 Tbps designs ramp in 2026, HDI and IC substrate suppliers with proven CPO capabilities will capture disproportionate share inside the Data Center and AI Server PCB market.

Rapid Expansion of Liquid Cooling Infrastructure

More than 120,000 racks incorporated direct-to-chip cold plates in 2025, a 220% leap from the prior year. Immersion cooling crossed 8% share of new AI cluster builds, cutting total facility energy use and increasing physical server density. Liquid exposure necessitates conformal coating and underfill steps that add two to three weeks of lead time and push boards into IPC-6012 Class 3L qualification, a hurdle only a subset of tier-1 suppliers can clear.[3]IPC, “IPC-6012E Class 3L Requirements,” ipc.org Polyimide laminates with thermal expansion coefficients below 15 ppm/°C mitigate solder fatigue as servers shuttle between hot-swap servicing and steady-state operation. The incremental capital burden favors fabricators that already maintain Class 3 wet labs and reliability chambers, tightening competition and accelerating consolidation across the Data Center and AI Server PCB market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply Chain Bottlenecks for ABF Substrates | -0.60% | Global, acute in Asia-Pacific and North America | Short term (≤ 2 years) |

| High CapEx Requirements for Advanced HDI Lines | -0.40% | Global, most pronounced in Europe and Southeast Asia | Medium term (2-4 years) |

| Geopolitical Export Controls on AI Chipsets | -0.30% | China, indirect impact on global supply chains | Medium term (2-4 years) |

| Reliability Concerns with Ultra-Thin Copper Foils | -0.20% | Global, concentrated in high-frequency applications | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Supply Chain Bottlenecks for ABF Substrates

Ajinomoto Build-up Film remains irreplaceable for most 2.5D and 3D AI accelerator packages, yet 2025 capacity additions trail demand by 12-18 months. Hyperscale’s now place volume commitments a year in advance and accept 40-week lead times that ripple through board procurement schedules, constraining near-term growth. Intel publicly cited ABF shortages for delaying Granite Rapids Xeon launches, underscoring the systemic exposure. Price increases of 18-22% since early 2024 force mid-tier PCB vendors to either absorb margin compression or concede volumes, reinforcing share concentration among vertically integrated suppliers. Until new Ajinomoto lines reach full output by Q3 2027, the Data Center and AI Server Printed Circuit Board Market must navigate periodic substrate scarcity.

High CapEx Requirements for Advanced HDI Lines

Greenfield HDI plants capable of 10 µm line-and-space geometries need USD 150-250 million per site, far above the USD 70-90 million typical for standard multilayer lines. AT&S poured EUR 400 million (USD 440 million) into its Chongqing campus, yet first-year utilization stayed below 60% because customer qualifications span 12-18 months. Rising interest rates pushed average borrowing costs to 9-11% by late 2025, stretching ROI horizons to nine years and delaying brownfield upgrades for many suppliers. The elevated capital barrier constricts the entry of regional players, clusters HDI capacity among ten or fewer firms, and slows technology diffusion across the broader Data Center and AI Server PCB market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By PCB Type: Flexible Circuits Expand Server Design Freedom

Flexible circuits advanced at a 5.99% CAGR through 2031, outpacing every other category as edge servers and micro-data-center appliances demand foldable interconnects that collapse z-height in compact chassis. Standard multilayer boards retained a 26.87% share of the Data Center and AI Server Printed Circuit Board Market size in 2025 because their cost-efficiency fits high-volume server motherboards and backplanes. Nevertheless, HDI penetration is rising steadily where 112 Gbps PAM-4 signalling forces tighter impedance windows. IC substrates enjoy tailwinds from chiplet architectures that bridge multiple silicon dies on organic interposers, while rigid-flex boards combine bend radius compliance with heavy copper power planes for liquid-cooled assemblies. Samsung Electro-Mechanics’ 16-layer any-layer HDI launch reduces cycle time by 20% and signals supplier readiness for 15 µm geometries, a threshold that standard multilayer vendors struggle to hit. The convergence of rigid, flex, and IC substrate capabilities encourages hyperscalers to consolidate sourcing under a few full-stack fabricators, deepening vendor-customer co-development ties and reinforcing volume visibility.

Rigid 1-2-sided boards remain staples for power modules, yet growth is limited to low-single digits as operators migrate to higher-efficiency VRM stages mounted on more complex substrates. Other niche types such as metal-core and ceramic boards together hold less than 5% share but play an outsize role in high-voltage power supplies and RF front ends. Fabricators that scale flexible-circuit know-how into rigid-flex and HDI variants are well positioned when liquid-cooling retrofits call for boards capable of dynamic articulation during maintenance. As server architectures grow modular, the Data Center and AI Server Printed Circuit Board market demands form-factor fluidity flexibility that standard multilayer incumbents must adopt or risk share loss to more adaptable substrate types.

By Substrate Material: Low-Loss Laminates Support Next-Gen Signalling

High-speed low-loss laminates captured 41.50% of the Data Center and AI Server Printed Circuit Board Market share in 2025 and are clocking a 6.63% CAGR to 2031 because board-level links now exceed 56 Gbps and often scale to 112 Gbps. FR-4 retains scale in cost-sensitive I/O cards, but its dissipation factor above 0.012 limits reach in next-gen switches. Polyimide substrates, offering Tg above 250 °C and Df below 0.003, increasingly populate liquid-cooled servers that endure thermal excursions from maintenance cycles. Packaging resins such as bismaleimide-triazine and ABF together hold nearly 12% share and remain vital for AI accelerators pairing HBM stacks with compute dies.

Rogers’ RO4835T laminate, commercialized mid-2025, achieves 0.0037 Df while maintaining FR-4 compatibility, shortening qualification loops and underscoring the premium that hyperscale’s place on drop-in process adoption. Metal-core and ceramic options, while below 8% revenue, provide irreplaceable thermal pathways in kilowatt-class power supplies. Suppliers that can drive spindle speeds above 120k rpm without delamination are best placed to commercialize next-gen low-loss materials at scale. As signalling rates lift again to 224 Gbps PAM-4, low-loss blends will become table-stakes for every high-value layer stack inside the Data Center and AI Server Printed Circuit Board market.

Geography Analysis

Asia-Pacific owned 82.54% of 2025 revenue and is tracking a 6.25% CAGR through 2031. Taiwan’s Hsinchu and Tainan hubs feed over 70% of TSMC’s organic substrates, letting Unimicron and Nan Ya PCB ship within 10 weeks versus 14-16 weeks for imports. China added roughly 2.5 million m² of HDI capacity across Guangdong and Jiangsu during 2025 to backfill boards now barred from foreign GPU shipments. Japan guards intellectual property in glass-core laminates and ultra-thin copper foil, yet high labour costs dampen volume ramp. South Korea’s any-layer HDI push yields 30% thinner boards and keeps Samsung Electro-Mechanics and LG Innotek on the bleeding edge, while Thailand and Vietnam absorb relocated standard multilayer lines but lack engineers for sub-25 µm processes.

North America with growth clustered in aerospace, defense, and medical prototypes were ITAR and quality standards command price premiums. TTM’s eight U.S. sites anchor quick-turn volume and benefit from steady defense demand, mitigating exposure to commodity price swings. The CHIPS and Science Act devoted minimal direct aid to PCBs, sustaining local dependence on Asian imports for high-volume runs. Hyperscale’s cluster new sites around renewable corridors in the Pacific Northwest and Texas, demanding boards with wide thermal envelopes and weather-proof coatings.

Europe held about 6% share, spearheaded by AT&S and NCAB Group. Green-Deal initiatives catalyse EV and renewable-grid rollouts that depend on high-reliability boards, but REACH and Ecodesign compliance inflate manufacturing costs by up to 12%. AT&S’s investment in Chongqing underlines Europe’s modest domestic upside versus Asia’s demand gravity. Brazil and Argentina together sit below 2% share, aligned to local auto and appliance assembly that primarily sources standard multilayer boards. The near-shoring tilt to Mexico helps North America but only marginally shifts global market weight away from Asia.

Across these regions, hyperscalers seek proximity to substrate fabs, renewable energy, and advanced packaging houses, creating clustering effects that reinforce Asia-Pacific’s primacy yet keep brownfield upgrades alive in North America and Europe to hedge geopolitical risk. Such spatial dynamics continue to steer procurement volumes and pricing power within the Data Center and AI Server Printed Circuit Board Market.

Competitive Landscape

The Data Center and AI Server Printed Circuit Board Market remains moderately fragmented, with the top five suppliers, TTM Technologies, Ibiden, AT&S, Unimicron, and Samsung Electro-Mechanics, controlling roughly 35% of 2025 revenue. Tier-1 players differentiate through HDI and IC substrate roadmaps, while tier-2 firms chase high-mix standard multilayer volumes. Vertical integration into copper-clad laminate gives Kingboard and Shengyi 10-15% cost cushions that they leverage during material crunches. Patent filings in glass-core substrates and embedded power rails are concentrated in Japan and South Korea, signalling future wedge technologies. Supplier consolidation by hyperscalers shifts bargaining leverage toward buyers, who now lock in capacity via co-investment clauses and multi-year take-or-pay contracts.

White-space remains in rigid-flex solutions for liquid-cooled servers, where traditional HDI vendors lack flex expertise. Chinese entrants like Shennan Circuits and Zhen Ding Technology capitalize on state subsidies to scale HDI fast, compressing lag to tier-1 performance metrics. Design-automation aided by AI trims routing cycles from weeks to hours, turning EDA integration into a procurement criterion as critical as manufacturing capability. Compliance with IPC-6012 Class 3 and 3L standards demands capital-intensive test suites, filtering out under-invested shops and nudging the industry toward moderate consolidation. Overall, competitive intensity is rising but remains balanced between cost-centric challengers and technology-driven incumbents.

Data Center And AI Server Printed Circuit Board Industry Leaders

Unimicron Technology Corp.

Ibiden Co., Ltd.

ATandS AG

TTM Technologies Inc.

Samsung Electro-Mechanics Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Unimicron completed a USD 320 million expansion at its Kunshan plant, adding 1.2 million m² of annual HDI capacity aimed at AI-server boards.

- December 2025: Samsung Electro-Mechanics secured a three-year, USD 850 million any-layer HDI contract with a major North American hyperscaler, including joint R&D on embedded power rails.

- November 2025: AT&S received EUR 180 million (USD 198 million) in Chinese subsidies to enlarge its Chongqing IC-substrate campus, with production slated for Q2 2027.

- October 2025: Ibiden partnered with Corning to co-develop glass-core substrates targeting commercial launch in 2028.

Global Data Center And AI Server Printed Circuit Board Market Report Scope

The Data Center and AI Server Printed Circuit Board Market Report is Segmented by PCB Type (Standard Multilayer, Rigid 1-2 Sided, HDI, Flexible Circuits, IC Substrates, Rigid-Flex, Other Types), PCB Materials (Copper Clad Laminate, High-Density Packaging Substrate), Substrate Material (Glass Epoxy FR-4, High-Speed Low-Loss, Polyimide, Packaging Resins, Other Materials), and Geography (North America, Europe, Asia-Pacific, South America). The Market Forecasts are Provided in Terms of Value (USD).

| Standard Multilayer (Non-HDI) |

| Rigid 1-2 Sided |

| High-Density Interconnect (HDI) |

| Flexible Circuits (FPC) |

| IC Substrates (Package Substrates) |

| Rigid-Flex |

| Other PCB Types |

| Glass Epoxy (FR-4) |

| High-Speed / Low-Loss |

| Polyimide (PI) |

| Packaging Resins (BT / ABF) |

| Other Substrate Materials |

| North America | United States |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Taiwan | |

| Southeast Asia | |

| Rest of Asia-Pacific | |

| Rest of World |

| By PCB Type | Standard Multilayer (Non-HDI) | |

| Rigid 1-2 Sided | ||

| High-Density Interconnect (HDI) | ||

| Flexible Circuits (FPC) | ||

| IC Substrates (Package Substrates) | ||

| Rigid-Flex | ||

| Other PCB Types | ||

| By Substrate Material | Glass Epoxy (FR-4) | |

| High-Speed / Low-Loss | ||

| Polyimide (PI) | ||

| Packaging Resins (BT / ABF) | ||

| Other Substrate Materials | ||

| By Geography | North America | United States |

| Rest of North America | ||

| Europe | United Kingdom | |

| Germany | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Taiwan | ||

| Southeast Asia | ||

| Rest of Asia-Pacific | ||

| Rest of World | ||

Key Questions Answered in the Report

What is the projected value of the Data Center and AI Server Printed Circuit Board Market by 2031?

The market is forecast to reach USD 12.80 billion by 2031.

Which PCB type is growing fastest in data-center applications?

Flexible circuits are expanding at a 5.99% CAGR as edge servers adopt foldable interconnects.

Why are high-speed low-loss laminates gaining share?

They maintain signal integrity above 56 Gbps and already hold 41.50% share, growing at 6.63% CAGR.

How concentrated is global PCB production geographically?

Asia-Pacific accounts for 82.54% of 2025 revenue and will continue leading growth at a 6.25% CAGR.

What is the main supply-chain risk through 2027?

ABF substrate shortages, with lead times extending to 40 weeks, remain the top bottleneck.

Page last updated on: