Market Overview

| Study Period | 2018 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

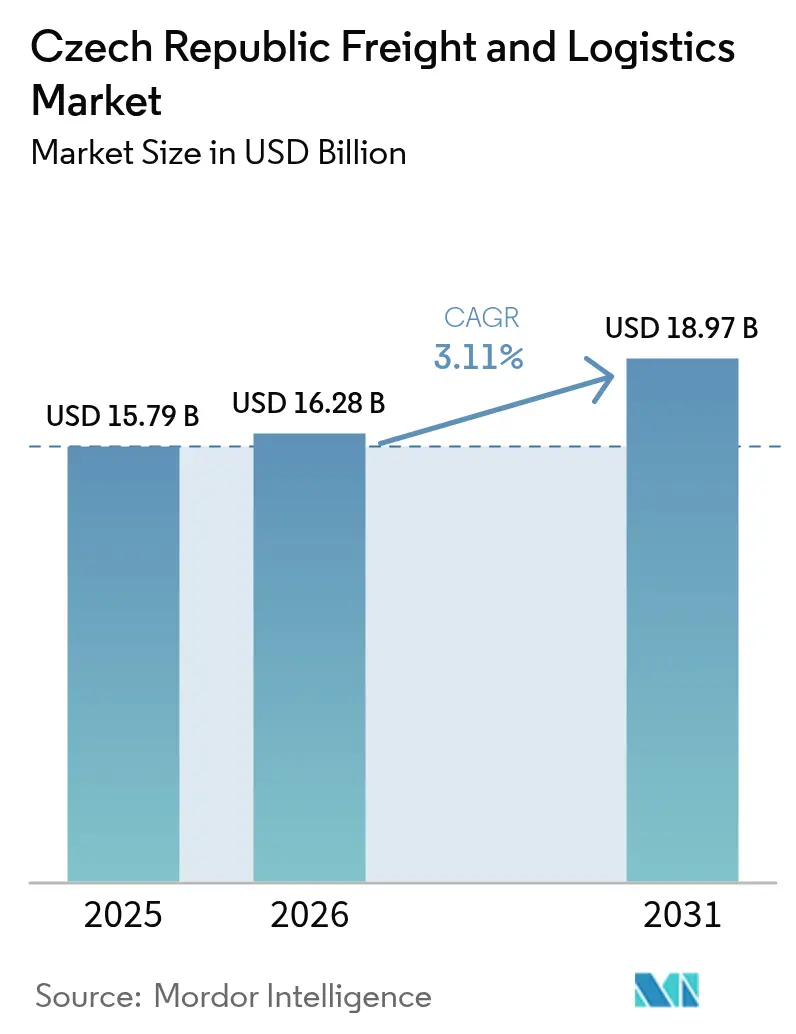

| Base Year Market Size (2025) | USD 15.79 Billion |

| Market Size (2026) | USD 16.28 Billion |

| Market Size (2031) | USD 18.97 Billion |

| Growth Rate (2026 - 2031) | 3.11% CAGR |

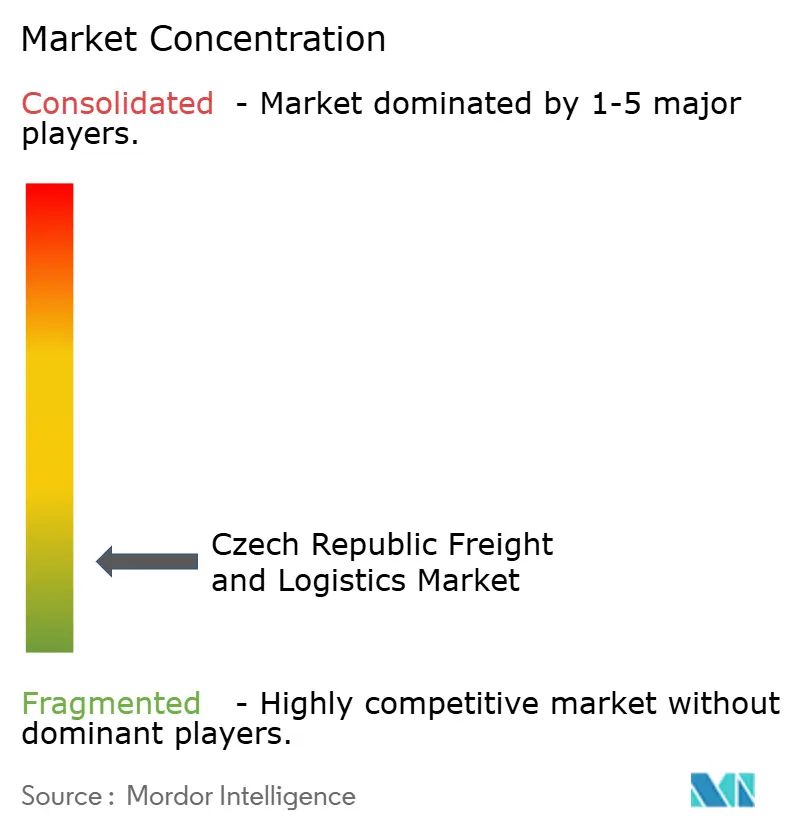

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Czech Republic Freight And Logistics Market Analysis by Mordor Intelligence

The Czech Republic freight and logistics market size in 2026 is estimated at USD 16.28 billion, growing from 2025 value of USD 15.79 billion with 2031 projections showing USD 18.97 billion, growing at 3.11% CAGR over 2026-2031. This outlook reflects a mature, yet resilient sector supported by record CZK 160 billion (USD 7.14 billion) of public works spending on road and rail, expanding near-shoring activity from German and Central European manufacturers, and strong e-commerce demand that lifted online retail sales to USD 8.1 billion in 2025. At the same time, rising motorway tolls, persistent driver shortages of roughly 20,000 positions, and tight industrial real-estate availability continue to challenge cost structures, stimulate automation investments, and gradually channel cargo toward rail and inland waterways. The Czech Republic’s central location on core TEN-T corridors, coupled with the forthcoming tri-modal Ostrava Mosnov hub, sustains its role as a preferred gateway for cross-border flows into Germany, Austria, Poland, and Slovakia. Consolidation is accelerating, most notably DSV’s EUR 14.3 billion (USD 15.78 billion) purchase of DB Schenker, while digital customs platforms, AI-enabled warehousing, and EU Green Deal incentives are reshaping competitive benchmarks[1]“Overview: Transport news and innovations for 2025,” Ministry of Transport of the Czech Republic, md.gov.cz.

Key Report Takeaways

- By logistics function, freight transport led with 45.22% revenue share in 2025; courier, express, and parcel (CEP) is projected to log the fastest 3.48% CAGR of the Czech Republic freight and logistics market size between 2026-2031.

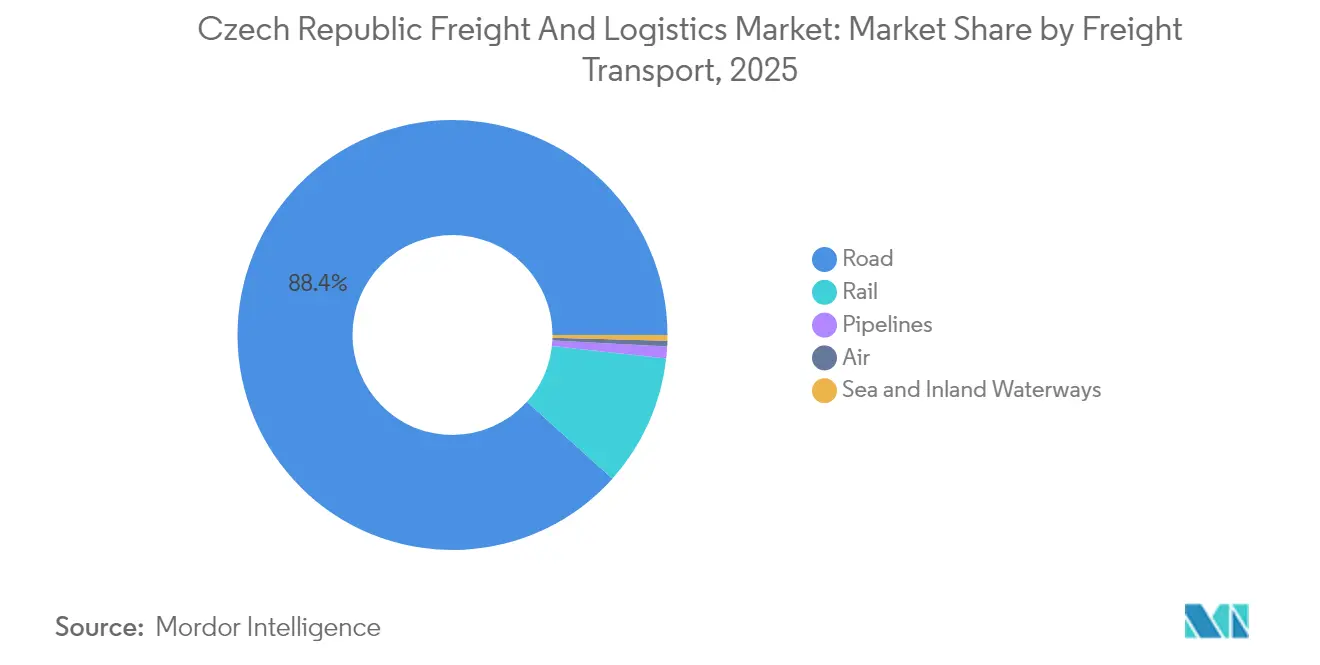

- By freight transport mode, road freight transport retained 88.35% share in 2025, while air freight transport is poised to expand at a 3.42% CAGR between 2026-2031.

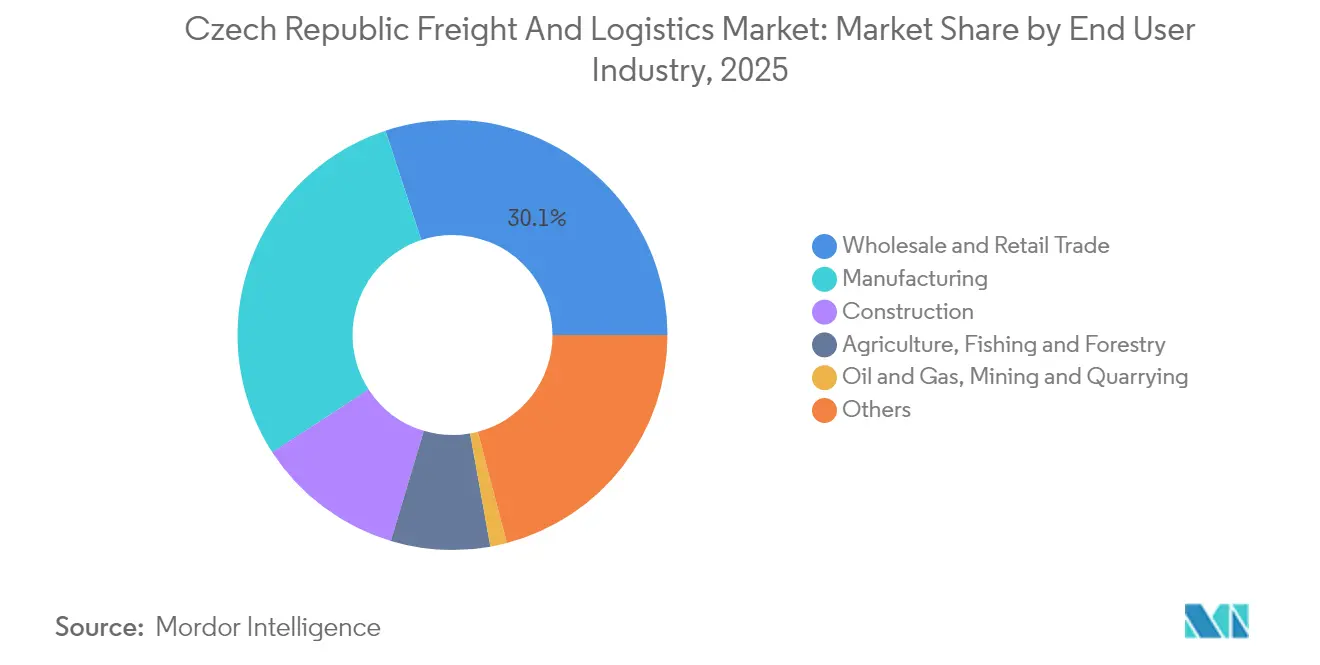

- By end user industry, wholesale and retail trade held 30.05% of the Czech Republic freight and logistics market share in 2025; manufacturing is forecast to grow at a 3.31% CAGR between 2026-2031.

- By CEP service type, domestic parcels captured a 62.30% revenue share in 2025, whereas international parcels is expected to advance at a 3.59% CAGR between 2026-2031.

- By freight forwarding, air freight forwarding accounted for a 49.60% revenue share in 2025; sea and inland waterways freight forwarding is projected to rise at a 3.22% CAGR between 2026-2031.

- By warehousing and storage type, non-temperature-controlled facilities dominated with 92.05% revenue share in 2025; temperature-controlled facilities are expected to register a 3.27% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Czech Republic Freight And Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Near-shoring of German and CEE manufacturing supply chains driving growth | +0.8% | Border regions with Germany and Austria | Medium term (2–4 years) |

| Accelerated digital transformation and logistics automation adoption | +0.6% | Prague, Brno, nationwide networks | Short term (≤ 2 years) |

| Record CZK 160 bn (~USD 7.14 bn) public-works budget for road and rail (2025) | +0.5% | National TEN-T corridors | Long term (≥ 4 years) |

| EU Green Deal subsidies support intermodal shift and E-truck pilot projects | +0.3% | Major freight corridors | Medium term (2–4 years) |

| Implementation of digital customs single‑window reducing border dwell time | +0.2% | Principal border crossings | Short term (≤ 2 years) |

| Tri-modal Ostrava Mosnov logistics hub set for commissioning in 2027 | +0.2% | Moravian-Silesian Region, spillover to Slovakia and Poland | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Near-Shoring of German and CEE Manufacturing Supply Chains

German automotive and machinery firms continue relocating component production within 500 km of OEM plants, channeling new volumes into Czech cross-border lanes. BMW’s logistics complex in Mosnov illustrates this influx, while semiconductor and battery suppliers replicate the model to hedge geopolitical risk. The ensuing demand surge benefits full-truck-load operators, pallet networks, and value-added warehousing, though forecasts factor in potential volume loss if Germany’s insolvency wave trims procurement budgets.

Accelerated Digital Transformation and Logistics Automation Adoption

Labor scarcity and e-commerce fulfillment pressures are prompting operators to deploy AI warehouse management, IoT fleet telematics, and autonomous sorting. Investments topping EUR 500 million (USD 551.82 million) since 2024 have delivered 15-25% efficiency gains for early adopters. Zasilkovna’s Z-BOT pickup network, Rohlik Group’s Veloq fulfillment engine, and the EU Single Window customs platform collectively shorten cycle times and free capacity while mitigating border dwell lags[2]“Information Society in Figures 2024,” Czech Statistical Office, czso.cz.

Record CZK 160 Billion (USD 7.14 Billion) Public-Works Budget for Road and Rail (2025)

Government funding underpins 100 km of new motorways, modernization of rail hubs, and the Brno–Prerov high-speed segment that frees freight paths on legacy lines. The Prague Ring Road expansion will absorb 70,000–80,000 vehicles daily by 2030, easing urban congestion and trimming drayage mileage for metropolitan distribution centers.

EU Green Deal Subsidies for Intermodal Shift and E-Truck Pilots

Policy incentives reimburse operators for combined-transport costs and electrified fleets, cutting door-to-door rates by an estimated 10% over seven years. CD Cargo’s purchase of 25 electric locomotives and 200 wagons, DHL’s carbon-neutral warehouse retrofits, and Ostrava Mosnov’s tri-modal gateway all align with 90% emission-reduction targets by 2050.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Acute driver shortage limits fleet capacity and operational expansion | –0.7% | Nationwide industrial belts | Short term (≤ 2 years) |

| Rising motorway tolls increase operating costs for transporters | –0.4% | All long-haul road corridors | Short term (≤ 2 years) |

| Persistently low warehouse vacancy driving record‑high rents | –0.3% | Prague and Brno metro areas | Medium term (2–4 years) |

| Brno urban HGV restrictions expand last-mile delivery costs | –0.2% | Brno and surrounding municipalities | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Acute Driver Shortage Limiting Fleet Capacity

Roughly 20,000 vacancies, in line with a regional deficit of 400,000 drivers, curb fleet utilization and inflate wages above CZK 41,739 (USD 1,864.42) per month. Recruitment of non-EU labor from the Philippines mitigates gaps but adds onboarding costs and training lead times, while demographic attrition continues to exceed 8% annually. Delivery delays and higher spot rates ripple through retail replenishment and just-in-time manufacturing schedules[3]“Driver shortage crisis deepens across Europe 2024,” European Transport Workers’ Federation, etf-europe.org.

Rising Motorway Tolls Increasing Operating Costs

The 5% toll hike effective January 2025 raises per-kilometer charges to as high as EUR 0.33 (USD 0.36) for EURO VI tractor-trailers, coinciding with fuel at USD 1.63 per liter. Smaller haulers struggle to pass through costs, prompting route re-optimization toward rail or bi-modal solutions on high-volume corridors. CO₂-rating surcharges now apply even to zero-emission trucks, narrowing operating savings and reinforcing the case for scale economies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End User Industry: Manufacturing Drives Growth Amid Retail Resilience

Wholesale and retail trade accounted for 30.05% of the Czech Republic freight and logistics market share in 2025, underpinned by e-commerce penetration of 18.5% and a dense network of 1.3 million m² of retail parks. Manufacturing is projected to record a 3.31% CAGR (2026-2031), buoyed by OnSemi’s USD 2 billion silicon-carbide plant and automotive recovery, positioning the segment to capture incremental cross-border tonnage and value-added warehousing demand.

Construction and Agriculture maintain steady lift factors through infrastructure spending and food-chain distribution, while Oil & Gas logistics benefit from the TAL pipeline expansion that cuts dependency on Russian crude. The Czech Republic freight and logistics market size for manufacturing is expected to rise in tandem with global supply-chain re-design, keeping contract logistics growth ahead of GDP. Wholesale and Retail providers seek same-day urban delivery, micro-fulfillment, and omnichannel returns processing, adding margin pressure but fueling demand for automation and temperature-controlled capacity for fresh groceries. Export-oriented manufacturers leverage predictive analytics and vendor-managed inventory to offset input-price volatility, reinforcing the need for multimodal, resilient networks.

By Logistics Function: Freight Transport Dominates Amid CEP Acceleration

Freight transport accounted for 45.22% of the Czech Republic freight and logistics market share in 2025, underscoring its foundational role in supporting export-oriented manufacturing and intra-EU trade. Road freight transport retained an 88.35% slice of freight transport revenue thanks to dense highway links and flexible scheduling that rival modes cannot match. Rail moved significant volume and is expected to grow as new electric locomotives and intermodal wagons come online. Pipeline flows remain strategic for refined-product distribution, while sea and inland waterways contributed less volume through Danube corridors that offer lower-carbon bulk transport. Air freight focused on semiconductor equipment, pharmaceuticals, and high-value automotive components funneled through Prague’s Vaclav Havel Airport.

Courier, Express, and Parcel is the fastest-growing logistics function with a 3.48% CAGR (2026-2031) outlook, driven by 18.5% e-commerce penetration and rising demand for next-day deliveries across urban and rural routes. International CEP volumes are projected to expand at 3.59% CAGR (2026-2031), outpacing domestic traffic as cross-border marketplace orders flow from Germany, Austria, and the Balkans. Temperature-controlled warehousing expects a steady 3.27% CAGR (2026-2031), providing pharmaceutical and grocery chains with compliant cold-chain infrastructure. Digitalization accelerates segment efficiency: the New Computerized Transit System Phase 5 now processes more than 85% of transit declarations electronically, trimming clearance times and smoothing door-to-door CEP hand-offs. Collectively, these dynamics keep Freight Transport at the core of the Czech Republic freight and logistics market size while allowing CEP and value-added services to capture incremental growth.

By Courier, Express, and Parcel: International Growth Outpaces Domestic Expansion

Courier, Express, and Parcel services are set to expand at a 3.48% CAGR (2026-2031), outperforming the broader Czech Republic freight and logistics market. Domestic CEP retained 62.30% of volumes in 2025 thanks to Zasilkovna’s 9,900 pickup points and robotic lockers, yet international flows to Germany, Austria, and the Balkans are expected to grow faster at 3.59% between 2026-2031.

Accelerated mobile commerce adoption, 84% online shopper penetration, and digital marketplace integration elevate parcel density across rural routes, spurring investments in automated sorters and AI-driven route engines. The EU Single Window customs interface will further compress clearance times, giving Czech operators a competitive edge in cross-border e-commerce fulfillment.

By Warehousing and Storage: Non-Temperature-Controlled Facilities Dominate Market

Non-temperature-controlled warehouses captured 92.05% of the 2025 segment revenue, mirroring broad-based demand from manufacturing, retail, and distribution. Vacancy below 3% in Prague and Brno pushes rents to record highs, prompting speculative builds and peripheral site development.

Temperature-controlled space is on a 3.27% CAGR (2026-2031) projected trajectory, driven by pharmaceutical cold chains and fresh food delivery. Automation, robotic pick systems, AS/RS technology, and AI inventory tools mitigate labor shortages, while carbon-neutral retrofits such as DHL’s Pohorelice site align with EU sustainability mandates.

By Freight Transport: Road Dominance Faces Intermodal Competition

Road freight transport remained the backbone with 88.35% revenue share in 2025, though the Czech Republic's freight and logistics industry is witnessing incremental rail uptake through CD Cargo’s electrified fleet and new intermodal wagons. Air freight transport is anticipated to record a 3.42% CAGR (2026-2031), propelled by semiconductor equipment imports and outbound high-tech exports.

Rail freight’s projected 111.8 million tons by 2030 underscores gradual structural change, while pipeline and inland waterways retain niche but strategic roles in energy and bulk commodities. Toll surcharges and carbon pricing are nudging shippers to blend modes, yet road flexibility and last-mile convenience ensure its continued predominance.

By Freight Forwarding: Air Freight Forwarding Services Lead Despite Modal-Shift Pressures

Air freight forwarding represented 49.60% of segment revenue in 2025, reflecting Prague Airport’s status as a regional gateway for high-value electronics, automotive parts, and pharmaceuticals. The Czech Republic freight and logistics market size for air freight forwarding is expected to climb steadily, even as Green Deal incentives encourage modal diversification.

Sea and inland-waterway freight forwarding, currently smaller in value, is poised for the quickest 3.22% CAGR (2026-2031) via Danube linkages that offer cost-efficient bulk transport. Digital freight platforms, NCTS Phase 5 paperless transit, and DSV’s post-merger network optimization are enhancing multimodal connectivity and visibility across the supply chain.

Geography Analysis

Prague anchors the Czech Republic freight and logistics market thanks to Vaclav Havel Airport’s cargo facilities and D1/D5 highway spurs into Germany and Austria. Zero vacancy for luxury retail on Parizska Street and consistent 1–3% annual rent growth confirm sustained demand for prime urban space. Brno serves advanced manufacturing clusters but faces heavier last-mile costs from urban HGV restrictions that shift fulfillment to peri-urban warehouses.

Ostrava’s forthcoming tri-modal hub leverages its border-zone placement and university talent base, offering rail, road, and air synergies attractive to automotive and heavy-industry shippers. The Plzen region mirrors Prague’s industrial real-estate appetite, benefiting from West Bohemia University’s engineering pipeline and direct motorway links.

Cross-border flows capitalize on the EU Single Window customs platform, reducing document duplication and accelerating throughput. METRANS operates over 650 weekly trains across 20 terminals, progressing toward CO₂-neutral traction and expanding network resiliency. Trade statistics with 2023 exports at USD 253.3 billion and imports at USD 228.9 billion underscore the scale of logistics volumes funneled through Czech corridors.

Regulatory Landscape

The Czech freight and logistics framework is anchored by the Road Transport Act (Act No. 111/1994 Sb.), with oversight mechanics updated through Act No. 130/2025 Sb., which reorganized state supervision and shifted selected duties to the Road Transport Inspection (Inspekce silnicni dopravy). At the strategic level, the Ministry of Transport sets sector priorities through the Freight Transport Concept for 2024-2035, approved under Government Resolution No. 1006 on December 20, 2023, and focused on efficiency, sustainability, and intermodal freight development across key corridors.

Cross-border and controlled-goods movements continue to be governed under EU customs rules. The Customs Administration (Celni sprava CR) is responsible for customs, excise, and supervision of selected products during production, storage, and transport. In April 2026, the Ministry of Transport issued updates via the Transport and Tariff Gazette (Prepravni a tarifni vestnik 7/2026), reflecting ongoing tariff and operational notices relevant to carriers and forwarders operating within the Czech Republic and across EU lanes.

Value Chain Analysis

The Czech Republic freight and logistics value chain begins with shippers in manufacturing and wholesale and retail, followed by freight forwarders, integrators, and road hauliers that dominate domestic distribution. Rail operators and intermodal terminal networks support cross-border flows on TEN-T corridors. Downstream, contract logistics providers and warehouse operators, including e-commerce fulfillment teams, deliver storage, picking, packaging, returns, and value-added services, then route parcels and pallets into CEP and last-mile networks anchored by depots, pickup points, and lockers.

Operational productivity is shaped by three enabling layers. First, infrastructure and terminals, where projects such as the modernized container terminal at Prerov-Horni Mostenice (opened by OBB Rail Cargo Group in June 2026, expanded to 36,000 m2 and 3,000 TEU handling capacity) broaden rail-linked distribution options. Second, digital border and compliance processes, including customs-system upgrades such as e-Dovoz changes effective May 18, 2026, which enable more automated 24/7 goods release for authorized declarants. Third, warehouse automation, illustrated by KVADOS Group implementing 4D Shuttle automated warehousing at an Alza.sk logistics center (February 2026) and Packung installing a fully automated packaging line for Notino (March 2026). Labor availability (drivers and warehouse staff) and tight industrial real estate in core markets remain the main constraints, keeping emphasis on technology-led throughput gains rather than footprint expansion alone.

Competitive Landscape

The sector exhibits moderate fragmentation: the six largest operators accounted for roughly one-third of 2024 revenue, generating healthy but narrowing margins amid cost inflation. DSV’s acquisition of DB Schenker creates a USD 45.9 billion revenue leader with nearly 160,000 staff, targeting DKK 9 billion (USD 1.33 billion) in annual synergies via network consolidation and shared digital platforms. Scale advantages extend to procurement leverage and cross-selling of contract logistics, air-sea forwarding, and last-mile services.

Domestic innovators compete through technology. Rohlik Group’s Veloq platform automates grocery fulfillment, shrinking order-to-door times, while Zasilkovna’s self-service lockers mitigate the driver gap and cut parcel handover costs. Sustainability credentials are rising in tender criteria; Raben Group and DHL deploy alternative-fuel trucks and carbon-neutral warehouses to win shippers keen on meeting corporate ESG targets.

Market entrants eye niche opportunities in cold-chain, time-critical pharma, and heavyweight e-commerce returns, but face barriers from high warehouse rents, labor constraints, and capital-intensive automation. Consolidation momentum is likely to persist as toll escalations and CO₂ charges favor operators with multimodal coverage and optimized asset utilization.

Czech Republic Freight And Logistics Industry Leaders

DSV A/S (Including DB Schenker)

Raben Group (Including Raben Logistics Czech, sro)

Geis Group (Including Geis CZ, sro)

AGROFERT AS (Including Logistics Solution AS)

CMA CGM Group (Including CEVA Logistics)

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Active public programs and infrastructure commitments are creating white space for intermodal and rail-linked logistics offerings, particularly on core TEN-T lanes that feed Czech export-import flows. The state allocated a record EUR 3 billion for railway infrastructure in 2026, and Sprava zeleznic continues to contract for node upgrades, including a CZK 10 billion agreement (October 2025) with a consortium that includes OHLA ZS, Subterra, and Elektrizace zeleznic to modernize the Hradec Kralove railway hub. Terminal upgrades such as OBB Rail Cargo Group modernizing Prerov-Horni Mostenice in June 2026 support near-term development of rail-first or rail-assisted products, including shuttle services, cross-dock near terminals, and combined-transport solutions that ease road-cost pressure from tolls and labor shortages.

Digitization and compliance modernization also open room in cross-border e-commerce fulfillment and time-sensitive shipments, where process speed and transparency help differentiate providers. The government approved the Strategy for the Development of Services Based on Cooperative Intelligent Transport Systems (C-ITS) for 2026-2031 in April 2026, indicating deeper integration between vehicles, infrastructure, and digital services for traffic and safety management. On the border-processing side, the Czech Customs Administration updated e-Dovoz effective May 18, 2026 to automate goods release for authorized declarants on a 24/7 basis, supporting operators that can connect brokerage, visibility, and warehouse execution into a single workflow. Separately, statutory cities in the TEN-T network are required to prepare Sustainable Urban Logistics Plans by 2027, which creates a defined window for last-mile, micro-fulfillment, and low-emission delivery concepts aligned to municipal rules and shipper ESG requirements.

Recent Industry Developments

- June 2026: OBB Rail Cargo Group opened a modernized container terminal at Prerov-Horni Mostenice, expanding the site to 36,000 m2 and lifting handling capability to 3,000 TEU. The upgrade strengthens rail-linked distribution options for shippers using Czech east-west corridors and supports more reliable intermodal routings for cross-border flows.

- April 2025: DSV completed its acquisition of DB Schenker for EUR 14.3 billion, combining two large forwarding and contract logistics networks under one group. The deal accelerates consolidation in Czech forwarding and contract logistics, raising competitive pressure around network density, digital platforms, and procurement scale.

- July 2024: DACHSER opened a new 4,000 m2 warehouse facility in the Czech Republic to improve shipment consolidation and delivery efficiency across Central Europe. The added capacity supports tighter lead times for regional distribution and provides a platform for value-added services alongside linehaul operations.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this methodology, the market covers revenue earned from moving, handling, and storing goods within the Czech Republic, including transport, forwarding, warehousing, and related value-added logistics services provided to business customers.

Scope exclusions: Passenger transport, pure vehicle leasing without freight service, and non-logistics manufacturing value-add are not counted.

Segmentation Overview

- End User Industry

- Agriculture, Fishing, and Forestry

- Construction

- Manufacturing

- Oil and Gas, Mining and Quarrying

- Wholesale and Retail Trade

- Others

- Logistics Function

- Courier, Express, and Parcel (CEP)

- By Destination Type

- Domestic

- International

- By Destination Type

- Freight Forwarding

- By Mode of Transport

- Air

- Sea and Inland Waterways

- Others

- By Mode of Transport

- Freight Transport

- By Mode of Transport

- Air

- Pipelines

- Rail

- Road

- Sea and Inland Waterways

- By Mode of Transport

- Warehousing and Storage

- By Temperature Control

- Non-Temperature Controlled

- Temperature Controlled

- By Temperature Control

- Other Services

- Courier, Express, and Parcel (CEP)

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the Czech Republic demand context and to anchor assumptions that can be checked against public data series. We relied on official statistics and transport indicators such as Czech Statistical Office releases, Eurostat freight and warehousing series, and Ministry of Transport publications, which help track activity by mode and broad service intensity.

Trade and industrial signals were also reviewed because they shape shipment frequency and warehousing needs, using sources such as UN Comtrade, WTO trade indicators, and OECD macro and industry statistics, followed by company annual reports, investor presentations, and reputable press coverage for directional capacity and investment moves. In a few cases, paid subscriptions were used only to speed up company financial screening, shipment level trade checks, and freight rate context for validation. The desk sources listed above are illustrative only, and many other public references were used to collect data, validate outliers, and clarify definitions.

Primary Interviews and Surveys

Primary work was used to pressure-test what the desk sources could not fully explain, especially service mix, pricing behavior, and how contracts split between transport, forwarding, and warehousing. We spoke with logistics service providers, freight forwarders, warehouse operators, and large shipper-side logistics teams across the Czech Republic so our assumptions on utilization, typical shipment flows, and value-added services could be confirmed in plain language.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 26% | CXOs: 14% | APAC: 46% |

| Mid tier: 55% | Functional/Unit leaders: 26% | EMEA: 33% |

| Smaller Players: 19% | Managers: 60% | Americas: 21% |

Market-Sizing & Forecasting

Sizing starts with a top-down build that reconstructs the national logistics revenue pool from transport activity and services demand signals, and then it is allocated across freight transport, forwarding, warehousing, and value-added services. To keep the totals realistic, we corroborated the result with selective bottom-up approximations, such as sampled price per shipment or per pallet position multiplied by volumes, plus channel checks with operators that focus on key lanes and industrial clusters.

A few practical inputs were emphasized because they are traceable and can be updated each year, including freight volumes by mode, cross-border trade throughput, industrial production trends tied to automotive and manufacturing, warehouse capacity additions and occupancy patterns, and observed changes in contracted rates and surcharges. Where smaller operators do not disclose enough financial detail, gaps were handled using peer averages and capacity proxies, followed by interviews to confirm whether the implied revenue per unit looked realistic.

For forecasting, scenario analysis was used around two main levers, trade and industrial output, and then pricing and service-mix adjustments were applied based on what respondents expect for contract renewals and capacity tightness. The final forecast was checked so growth does not contradict the country's logistics infrastructure constraints and recent investment plans.

Data Validation & Update Cycle

Validation was done through repeated variance checks across independent signals, and we looked for mismatches between modeled revenue, freight movement indicators, and macro activity before results were finalized. Outliers, like unusually high implied pricing or sudden step changes in service mix, were flagged for analyst review and then rechecked through follow-up questions with market participants.

Before sign-off, the model goes through a multi-step review so the definitions, inputs, and calculations stay consistent across the historical and forecast period. The report is refreshed annually, and interim updates are made when material events occur, such as major regulatory changes, sharp fuel cost swings, or large capacity additions. Right before delivery, we run a fresh pass on key inputs so clients receive the latest updated view.

Mordor Intelligence's Czech Republic Freight and Logistics Market Sizing Compared With Other Published Estimates

Published market values for Czech freight and logistics do not always match, and the differences usually come from what gets counted as logistics revenue, what years are used for price and volume, and how cross-border flows are treated.

The main gap drivers in this market are whether courier and parcel revenues sit inside the total, whether contract logistics value-added services are counted separately or folded into transport, and whether warehousing is sized using capacity and occupancy checks or a simple GDP-linked uplift. The table also reflects how currency timing and refresh cadence can move results when fuel and labor costs shift quickly, which then changes billed rates and pass-through surcharges.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 15.79 B (2025) | |

| Trade Journal A | USD 15.79 B (2025) | The figure is repeated without documenting what service lines are included, so it is hard to verify whether courier and parcel, warehousing, and value-added logistics were all consistently counted. |

| Regional Consultancy B | USD 4.40 B (2024) | The estimate appears to focus on a narrower spend pool closer to outsourced logistics (for example, 3PL-type services) and uses a different base year, which can understate the full transport and warehousing revenue captured in our definition. |

Overall, the spread is best explained by scope and year choices, rather than a single math error. By keeping courier and parcel, forwarding, freight transport, warehousing, and value-added services within one consistent revenue view and rechecking pricing against activity indicators, the total stays tied to real operating signals, which is the modeling choice applied by Mordor Intelligence.

Key Questions Answered in the Report

What is the current value of the Czech Republic freight and logistics market?

The sector is valued at USD 16.28 billion in 2026 and is forecast to reach USD 18.97 billion by 2031.

Which logistics function is expanding the fastest in the Czech Republic?

Courier, Express, and Parcel services are projected to grow at a 3.48% CAGR from 2026 to 2031, outpacing other functions.

How significant is road freight transport within Czech logistics?

Road freight transport carries 88.35% of freight share, remaining the dominant mode despite emerging rail and intermodal alternatives.

What key factor is driving future warehouse demand?

Near-shoring of manufacturing and sustained e-commerce growth are tightening vacancy rates and spurring speculative warehouse developments.

How are toll increases affecting operators?

The 5% toll hike tied to CO₂ classes raises per-kilometer costs, pressuring small haulers and encouraging modal diversification toward rail and combined transport.

Which recent investment underscores the country’s logistics hub ambition?

BMW’s construction of a hi-tech logistics center in Mosnov, launched in May 2025, highlights ongoing commitment to the Czech multimodal infrastructure.

Page last updated on: