CXL Signal Conditioner and Retimer IC Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.19 Billion |

| Market Size (2031) | USD 3.32 Billion |

| Growth Rate (2026 - 2031) | 22.77% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

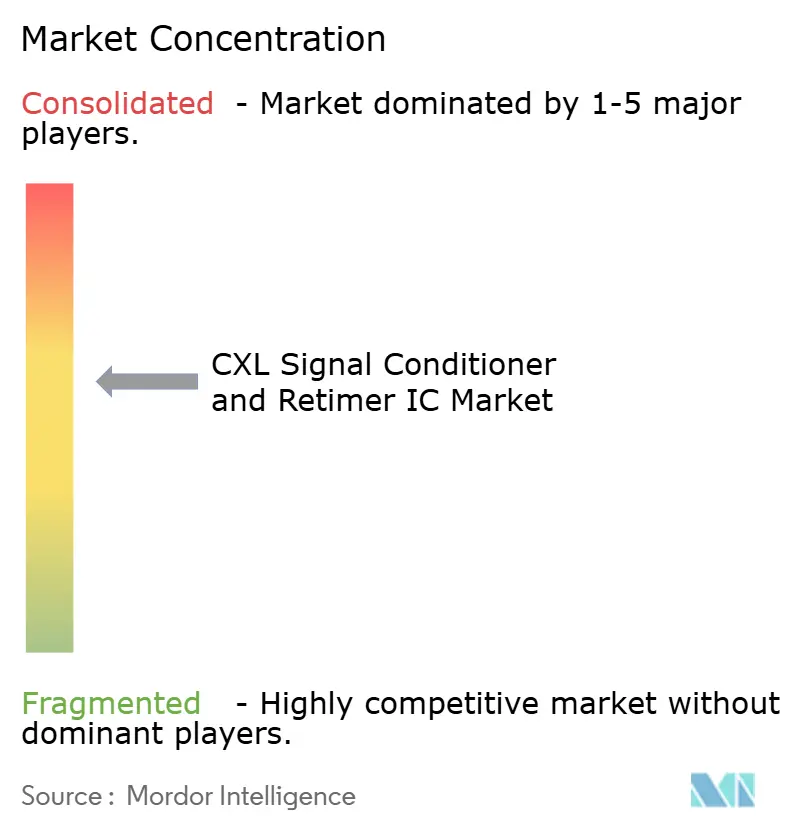

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

CXL Signal Conditioner and Retimer IC Market Analysis by Mordor Intelligence

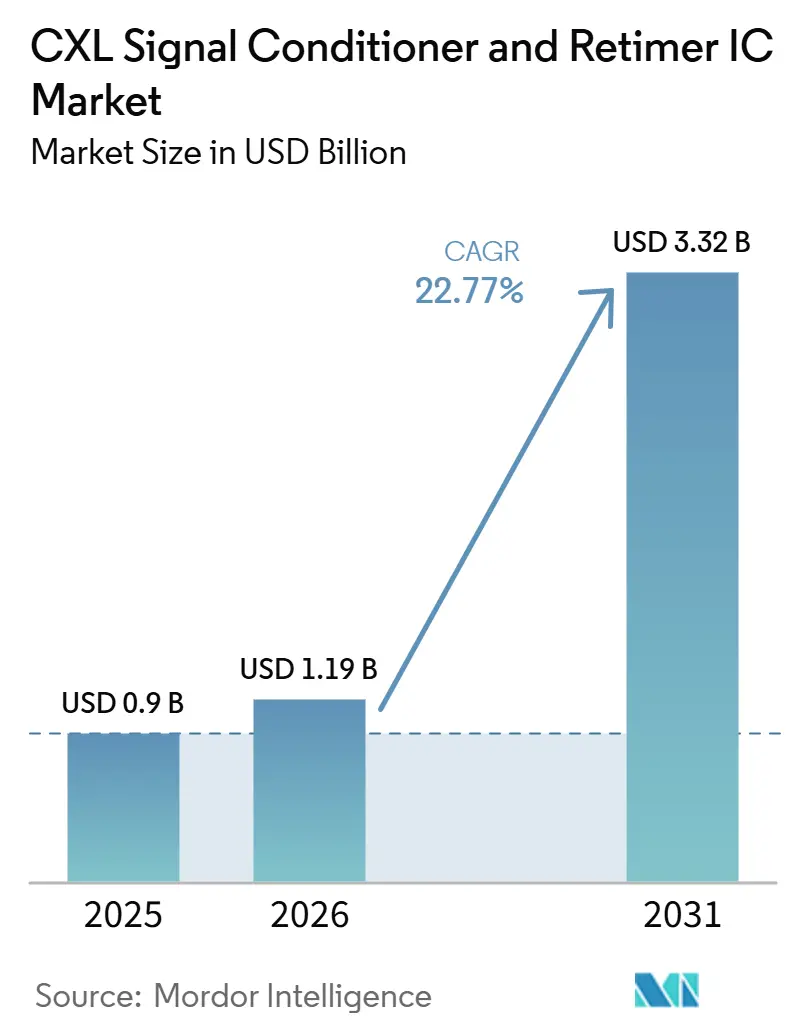

The CXL signal conditioner and retimer IC market size is projected to be USD 0.90 billion in 2025, USD 1.19 billion in 2026, and reach USD 3.32 billion by 2031, growing at a CAGR of 22.77% from 2026 to 2031. The 2025 base reflected a market that had already moved into commercial scale because PCIe 5.0 and CXL 2.0 AI server platforms were being deployed in volume across hyperscale clusters. The 2026 transition is centered on the PCIe 6.0 production ramp, where signal integrity limits at 64 GT/s over standard PCB materials make external retimers a required part of AI server board design. This shift is not a routine step from one PCIe generation to the next because shorter usable trace reach moves retimers into positions that had earlier relied on passive routing and expands silicon content per server. CXL-based memory expansion, pooling, and switch-based fabrics add further demand because they increase the number of links that need signal recovery across the rack and server architecture. The CXL signal conditioner and retimer IC market also remains shaped by North American hyperscale deployment strength, fast supply chain scaling in Asia-Pacific, and a competitive structure where established vendors benefit from deep qualification positions while newer participants try to enter through performance, cable integration, and interoperability readiness.

Key Report Takeaways

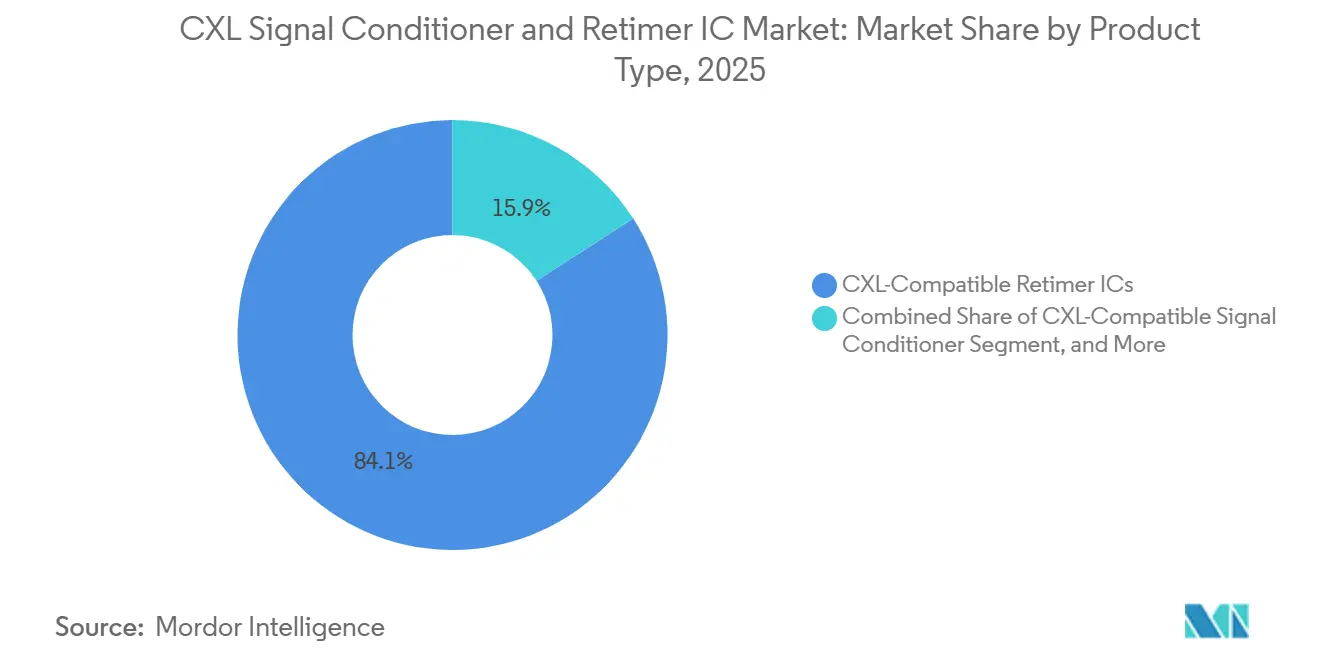

- By product type, CXL-compatible retimer ICs captured 84.12% share of the CXL signal conditioner and retimer IC market size in 2025, while active signal-conditioning ICs are projected to expand at a 23.37% CAGR through 2031.

- By PCIe/CXL generation compatibility, PCIe 5.0 and CXL 1.x-2.0 compatible ICs held 66.83% share in 2025, while PCIe 6.0 and CXL 3.x compatible ICs are expected to record the highest CAGR at 23.54% through 2031.

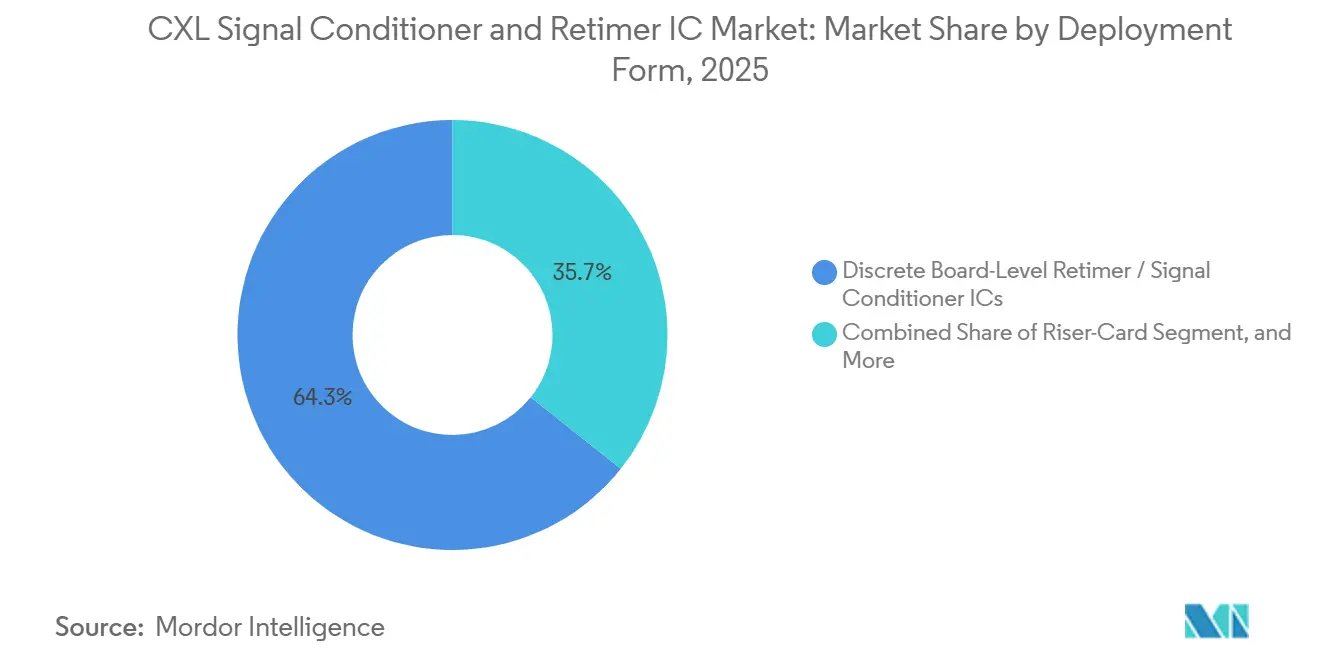

- By deployment form, discrete board-level retimer and signal conditioner ICs accounted for 64.31% share in 2025, while active electrical cable and smart cable module embedded ICs are projected to grow at a 23.49% CAGR through 2031.

- By application, AI and GPU accelerator servers represented 52.96% share of the CXL signal conditioner and retimer IC market size in 2025, while CXL memory expansion and memory pooling platforms are projected to advance at a 24.32% CAGR through 2031.

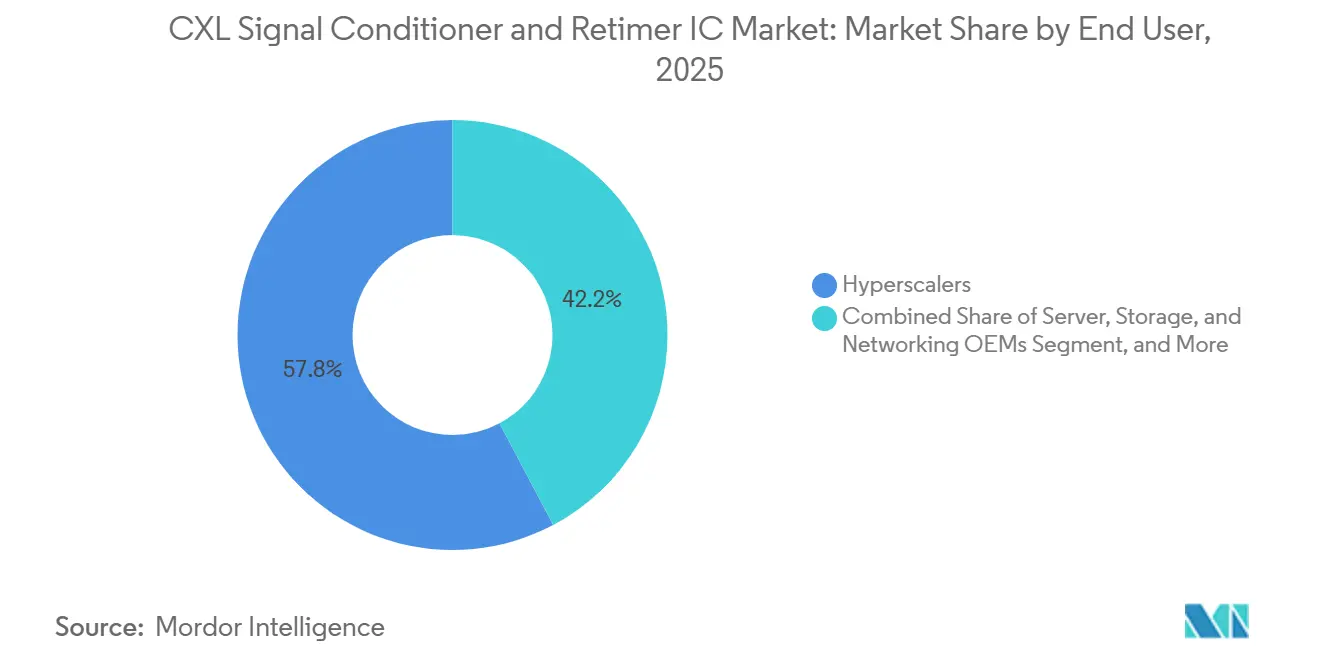

- By end user, hyperscalers held 57.77% share in 2025, while cloud service providers and neocloud providers are expected to expand at a 24.13% CAGR through 2031.

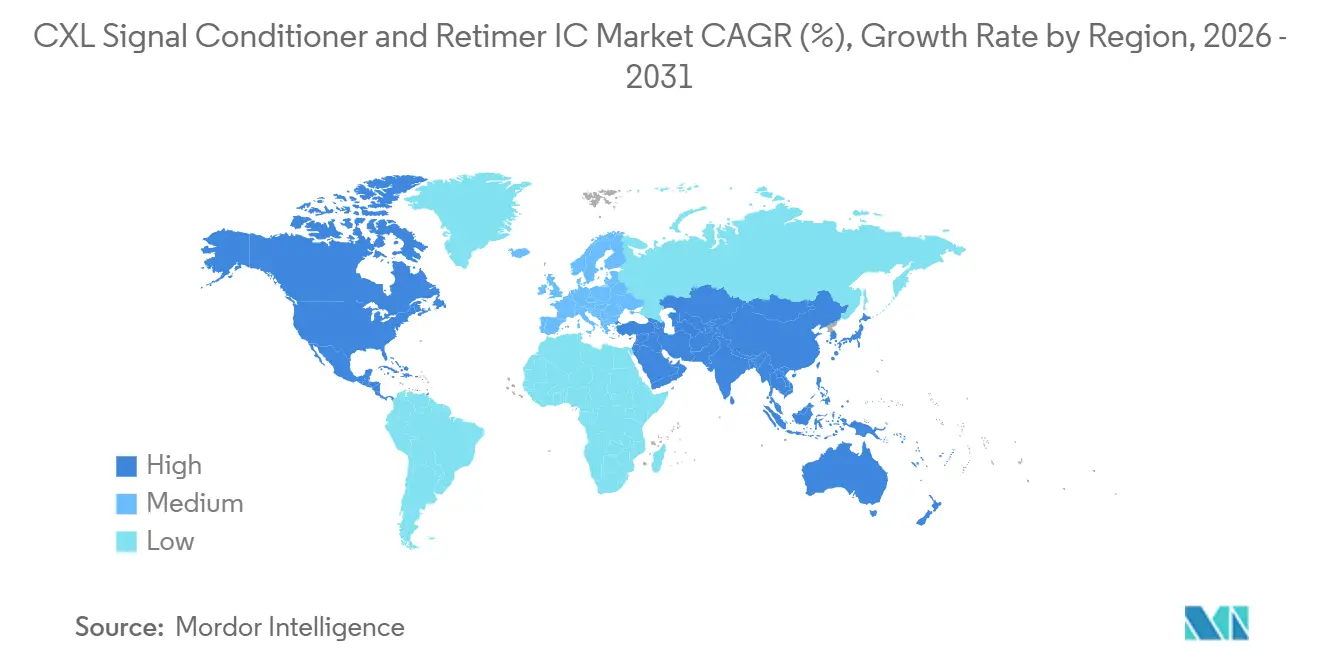

- By geography, North America accounted for 49.07% share of the CXL signal conditioner and retimer IC market size of global demand in 2025, while Asia-Pacific is projected to post the fastest CAGR at 23.77% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global CXL Signal Conditioner and Retimer IC Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AI server rack densification raising channel loss budgets | +5.5% | Global, with core concentration in North America and Asia-Pacific hyperscale clusters | Short term (≤ 2 years) |

| PCIe 6.0 and CXL 3.0 adoption forcing protocol-aware signal recovery | +4.8% | Global, led by North America OEM platforms and Asia-Pacific ODM supply chains | Short term (≤ 2 years) |

| Hyperscale memory pooling needs expanding low-latency CXL connectivity demand | +4.2% | North America and Europe, with secondary adoption in Asia-Pacific neocloud environments | Medium term (2-4 years) |

| Gen 6-capable retimers becoming design-standard in new AI platforms | +3.5% | Global, anchored in North America and Taiwan and South Korea ODM ecosystems | Short term (≤ 2 years) |

| Chiplet-based system architectures increasing board-to-board interconnect count | +2.1% | Global, especially relevant in Asia-Pacific chiplet design and packaging hubs | Medium term (2-4 years) |

| Interoperability testing costs raising switching costs for qualified suppliers | +1.4% | Global, with the heaviest burden in North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

AI Server Rack Densification Is Raising Channel Loss Budgets

Modern AI accelerator racks had already moved past 150 kW per rack for 72-GPU systems by 2025, and Microsoft Research showed that accelerator rack power was rising much faster than general compute and storage racks.[1]Microsoft Research, “Designing Datacenter Power Delivery Hierarchies for the AI Era,” arXiv, ar5iv.labs.arxiv.org That power shift matters for the CXL signal conditioner and retimer IC market because denser racks place more high-speed links in tighter thermal and physical layouts. At PCIe 6.0 speeds, reach limits on standard board materials become severe enough that signal recovery can no longer be treated as optional in many server paths. The result is not only higher unit demand, but also broader placement across GPU-to-CPU, GPU-to-memory, and GPU-to-network links inside advanced AI systems. As rack architectures move toward larger power envelopes over the next several years, the need for deterministic link integrity is expected to keep supporting the CXL signal conditioner and retimer IC market across new platform generations.

PCIe 6.0 and CXL 3.0 Adoption Is Forcing Protocol-Aware Signal Recovery

The move from PCIe 5.0 to PCIe 6.0 changed retimer requirements because PAM4 signaling and FLIT-based operation raise the technical burden on link recovery devices. That change supports the CXL signal conditioner and retimer IC market because vendors now have to meet stricter latency, compliance, and interoperability targets across AI and memory fabrics. Microchip Technology launched PCIe 6.0 and CXL 3.1 retimers in June 2026 with sub-12 ns pin-to-pin latency, which shows how low-latency compliance has become a central buying factor for advanced deployments. The CXL Consortium also released the CXL 4.0 specification in November 2025, which means product cycles are tightening even as CXL 3.x enters broader deployment.[2]CXL Consortium, “Developing a Robust CXL Compliance Program,” Compute Express Link Consortium Blog, computeexpresslink.org That shorter standards window favors suppliers that can move quickly from design to certification and then to volume shipment. It also keeps protocol-aware signal recovery at the center of the CXL signal conditioner and retimer IC market as server platforms move deeper into Gen 6 and prepare for later generations.

Hyperscale Memory Pooling Needs are Expanding Demand for Low-Latency CXL Connectivity

Microsoft Research showed that up to 25% of DRAM in large cloud clusters could become stranded when compute and memory are not balanced, and it also found that CXL-based pooling can cut aggregate DRAM needs by 7% and reduce server cost by 3.5%. Those economics matter directly to the CXL signal conditioner and retimer IC market because every memory pooling architecture depends on stable, low-latency, high-speed CXL links. Microsoft Research also proposed sparse-topology memory pods in 2026, which reinforces the movement from concept work toward practical deployment design. Marvell added to that direction in March 2026 by announcing a 260-lane CXL 3.x switch built for shared memory scaling up to 48 TB and 4 TB/s of cumulative bandwidth.[3]Marvell Technology, Inc., “Marvell Launches Next-Generation CXL Switch, Enabling Memory Pooling to Break Through the AI Memory Wall,” Marvell Newsroom, marvell.com Once these deployments expand, retimer demand will not stay limited to host boards because it also extends into switch paths, module links, and fabric-level interconnect layers. That broadens the addressable opportunity for the CXL signal conditioner and retimer IC market beyond the AI server count alone.

Gen 6-Capable Retimers are Becoming Design-Standard in New AI Platforms

Astera Labs said in May 2025 that its Aries 6 PCIe and CXL Smart DSP Retimers had completed qualification with leading AI and cloud server customers and were moving into volume production with next-generation platform rollouts. The company then reported Q1 2026 revenue of USD 308.4 million, up 93% year over year, which reflected volume ramps across multiple AI platforms at leading hyperscale customers. That pattern matters for the CXL signal conditioner and retimer IC market because once a Gen 6 retimer is qualified inside a platform, switching vendors often triggers another long validation cycle. Marvell also stated that its combined active electrical cable and retimer revenue would double in fiscal 2027 compared with fiscal 2026, which points to broader design-win conversion into shipment volume. The result is a design-standard effect where qualified suppliers gain more durable positions over the life of a platform generation. That effect supports both volume visibility and competitive discipline inside the CXL signal conditioner and retimer IC market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High validation burden for PCI-SIG and CXL compliance delaying design wins | -1.8% | Global, with the longest cycles in North America and Europe OEM supply chains | Medium term (2-4 years) |

| Rapid standard revisions increasing product obsolescence risk | -1.5% | Global, with acute exposure for Asia-Pacific ODMs under shorter lifecycle expectations | Long term (≥ 4 years) |

| Power dissipation and thermal constraints limiting deployment in dense server boards | -1.2% | Global, most acute in North America AI cluster deployments above 150 kW per rack | Medium term (2-4 years) |

| On-die PHY improvement and integrated CPU support reducing standalone retimer demand over time | -0.9% | Global, concentrated in North America platform choices by major CPU suppliers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Validation Burden for PCI-SIG and CXL Compliance Delays Design Wins

PCI-SIG and CXL compliance requirements add multiple layers of testing before a retimer can convert from silicon availability into revenue-bearing platform approval. The CXL Consortium’s compliance framework uses structured test events and interoperability phases that require vendors to validate against ecosystem hardware and reference systems. That sequence extends the time between product completion and commercial deployment, which narrows the revenue window available for each generation in the CXL signal conditioner and retimer IC market. The burden is heavier for smaller vendors because they usually have fewer dedicated compliance teams and less lab capacity to shorten iteration cycles. This tends to reinforce the position of suppliers that already hold multi-generation certification experience and customer trust. The outcome is a market where technical performance matters, but qualification readiness often determines who reaches volume deployment first.

Rapid Standard Revisions Increase Product Obsolescence Risk

The CXL roadmap has moved quickly, and the release of CXL 4.0 in November 2025 shows how fast suppliers must update product planning even while CXL 3.x still scales into production. This pace creates a real challenge for the CXL signal conditioner and retimer IC market because custom silicon development cycles can run close to the commercial life of one standards generation. A delayed platform ramp can therefore leave vendors with qualified products that face shrinking deployment windows before the next revision becomes the focus. Suppliers have responded by broadening compatibility, and Microchip stated that its XpressConnect family supports PCIe Gen 3 through Gen 6 on the same silicon. That approach reduces some lifecycle risk, but it does not remove the pressure created by rapid changes in platform requirements and customer qualification roadmaps. The net effect is that product timing remains almost as important as product performance in the CXL signal conditioner and retimer IC market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Retimers Hold the Core While Active Conditioning Builds a New Growth Layer

CXL-compatible retimer ICs held 84.12% of the product type segment in 2025, which kept them firmly at the center of CXL signal conditioner and retimer IC market demand. That large share reflected their required role on AI server baseboards, cable assemblies, and memory expansion hardware wherever full protocol-aware regeneration was needed at Gen 5 and Gen 6 speeds. The base also remained stable because hyperscalers generally validate retimer suppliers over long cycles, which makes approved devices harder to replace once a platform enters production. In practical terms, the high 2025 share shows that the CXL signal conditioner and retimer IC industry still depended first on full retiming rather than simpler conditioning approaches. It also shows that product leadership in this market is tied closely to qualification depth, not only to raw lane performance.

Signal conditioner and redriver ICs remained relevant in shorter-reach applications such as riser cards, storage backplanes, and enterprise add-in boards where full retimer capability is not always required. Active signal-conditioning ICs are projected to grow at a 23.37% CAGR through 2031, which makes them the fastest-growing product type in the CXL signal conditioner and retimer IC market size by segment. That growth comes from their use in active electrical cable assemblies and smart cable modules that extend PCIe 6.0 signals across inter-rack copper links. Montage Technology expanded that product direction in January 2026 when it launched a PCIe 6.x and CXL 3.x active electrical cable solution developed with cable manufacturers in China and validated with CPUs, xPUs, PCIe switches, and NICs. The move matters because it shifts part of the opportunity from board sockets to cable-based interconnect layers. It also broadens the addressable product mix inside the CXL signal conditioner and retimer IC market without reducing the central role of retimers on performance-critical links.

By PCIe/CXL Generation Compatibility: Gen 5 Supply Still Carries Scale While Gen 6 Sets the Growth Profile

PCIe 5.0 and CXL 1.x-2.0 compatible ICs held 66.83% of this segment in 2025, which meant legacy-to-current generation platforms still accounted for most shipment volume. That position reflected continuing production of Hopper-generation AI servers and the large installed base already present in hyperscale and neocloud data centers. The CXL signal conditioner and retimer IC market therefore entered 2026 with a strong demand tail from existing server generations even as new platforms prepared for Gen 6 transition. That installed base matters because replacement cycles in large cloud environments do not happen instantly, and validated systems keep generating demand over several quarters. It also helps explain why the market did not shift fully to the newest compatibility tier as soon as the next specification became available.

PCIe 6.0 and CXL 3.x compatible ICs are projected to grow at a 23.54% CAGR through 2031, which makes them the fastest-moving compatibility category in the CXL signal conditioner and retimer IC market. Their growth is tied to the 2026 production ramp of newer AI server platforms and to the technical need for stricter signal recovery at 64 GT/s. Intel’s PCIe 6.0 Retimer Supplemental Footprint also supports a more upgrade-friendly path by enabling pin-compatible retimer transitions across generations, which lowers redesign friction for server developers. Broadcom’s BCM85667 retimer product brief highlighted compliance with that footprint, which shows how vendors are positioning around platform continuity as much as performance. Multi-generation designs have therefore become a practical procurement option for ODMs and OEMs that want to extend qualification value across multiple product cycles. The result is a compatibility segment where current volume still leans toward Gen 5, but future growth is increasingly defined by Gen 6 adoption and broader backward-compatible design strategies.

By Deployment Form: Board-Level Hardware Holds the Installed Base While Cable-Embedded Designs Gain Momentum

Discrete board-level retimer and signal conditioner ICs accounted for 64.31% of deployment-form demand in 2025, giving them the leading position within the CXL signal conditioner and retimer IC market share by form factor. That leadership came from their essential role on server baseboards where link lengths between CPUs, GPUs, NVMe controllers, and CXL memory controllers move beyond the reach that can be supported without signal regeneration. Board-level designs also remain the first place where hyperscalers and OEMs qualify retimer behavior because those layouts define core platform stability. As a result, this form factor still anchors most current revenue even as new cable-based and chassis-based placements expand. It remains the most direct expression of how tighter signal budgets convert into higher silicon content inside modern AI servers.

Riser-card and add-in-board embedded ICs continued to serve systems where GPUs connect through extended slots and separate riser assemblies, which gave them a steady role in disaggregated platform layouts. Active electrical cable and smart cable module embedded ICs are projected to post the fastest CAGR at 23.49% through 2031, showing that the CXL signal conditioner and retimer IC market is widening beyond the motherboard. Astera Labs said its Aries 6 Smart Cable Modules support PCIe 6.x and CXL 3.x signal reach up to 7 meters over copper active electrical cables, which directly addresses multi-rack and adjacent-rack AI cluster layouts. That matters because growing cluster scale and rack power density limits increasingly push compute fabrics across physical boundaries that passive copper cannot handle reliably. Connector-, backplane-, and chassis-embedded designs add another layer of demand in high-density switch and storage systems where conditioning is built into the midplane. Together, these forms show that deployment diversity is rising even though board-level hardware still carries the largest revenue base in the CXL signal conditioner and retimer IC market.

By Application: AI Servers Lead Current Volume While Memory Pooling Creates The Fastest Expansion Path

AI and GPU accelerator servers accounted for 52.96% of application demand in 2025, which made them the largest application base in the CXL signal conditioner and retimer IC market. That share reflected large-scale deployment of accelerated server systems at hyperscale sites where high-speed connectivity is required across compute, storage, and memory subsystems. Astera Labs said its Aries retimers had already been deployed in volume across Hopper and HGX platforms and were ramping with Blackwell-generation systems, which shows how closely retimer demand tracks the AI server build cycle. High-performance computing and supercomputing platforms also added meaningful demand because they use composable and fabric-based designs that place heavy requirements on signal integrity. This keeps AI compute platforms at the center of near-term shipment scale even as other applications broaden.

CXL memory expansion and memory pooling platforms are projected to grow at a 24.32% CAGR through 2031, which gives them the strongest forward growth profile in the CXL signal conditioner and retimer IC market size by application. Microsoft Research showed that pooling can reduce stranded DRAM and lower total server cost, which gives cloud operators a concrete reason to move beyond pilot deployments. Microsoft’s later work on sparse-topology memory pods added practical architecture guidance that supports broader deployment planning. Marvell’s Structera S 30260 switch added another layer to that opportunity by supporting 260 lanes, up to 48 TB of shared memory, and 4 TB/s of cumulative bandwidth for CXL memory pooling fabrics. Each pooling topology requires retimers at multiple points, including host ports, switch paths, and memory-side connections, which raises retimer count per rack well above a simple server-node view. This is why memory pooling is expected to expand faster than other applications even though AI servers still hold the largest current revenue share.

By End User: Hyperscalers Define Volume Demand While Neoclouds Push Faster Adoption Cycles

Hyperscalers held 57.77% of end-user demand in 2025, giving them the largest customer base within the CXL signal conditioner and retimer IC market. Their lead came from first-wave adoption of PCIe 6.0 AI systems and early movement toward CXL memory pooling, both of which carry high retimer content per deployment. Hyperscalers also shape qualification standards because their platform requirements often determine which footprints, compliance levels, and cable designs move into broader production. That influence extends through OEM and ODM channels, which means a hyperscale design win can support volume across several linked supply chain tiers. In that sense, hyperscalers do not just buy more units, they also set the technical template for the wider CXL signal conditioner and retimer IC industry.

Cloud service providers and neocloud providers are projected to grow at a 24.13% CAGR through 2031, which makes them the fastest-growing end-user group in the CXL signal conditioner and retimer IC market. Marvell reported record fiscal 2026 revenue of USD 8.195 billion and said its aggregate active electrical cable and retimer revenue would double in fiscal 2027, a signal that advanced cloud-oriented deployments are broadening across its customer base. Neocloud operators often move quickly because they compete on AI throughput and infrastructure efficiency, so they can adopt newer interconnect designs at a faster pace than some larger buyers. Server, storage, and networking OEMs remain the channel that converts hyperscaler and cloud requirements into recurring component orders, especially through manufacturing networks in Taiwan and Southeast Asia. ODMs also rely heavily on pre-qualified reference boards and interoperability support from IC vendors, which strengthens vendors that invest in evaluation kits and lab infrastructure. HPC centers, research institutions, and large enterprises form a smaller but widening demand layer that is expected to absorb more CXL-enabled platforms as the installed base matures.

Geography Analysis

North America accounted for 49.07% of global demand in 2025, which gave the region the largest position in the CXL signal conditioner and retimer IC market share. The region remained the main center for hyperscale AI data center build-outs, and that kept it at the front of current retimer consumption. It also carried outsized architectural influence because U.S.-based hyperscalers often set platform requirements that later flow into OEM and ODM supply chains across Asia. This means North American demand affects not only local shipments, but also the qualification paths and product priorities of global suppliers.

Europe held a meaningful role through Germany, the United Kingdom, and France, where supercomputing centers, large private cloud environments, and server design operations supported demand for advanced interconnect hardware. The region did not match North America on absolute scale, but it remained relevant because composable infrastructure and memory efficiency are increasingly important in enterprise and research deployments. That gives the CXL signal conditioner and retimer IC market a stable European demand base tied more to architecture adoption than to sheer cloud build volume. Europe also matters in qualification and platform engineering because design centers and infrastructure operators influence how server platforms are configured for performance and efficiency.

Asia-Pacific is projected to post the fastest CAGR at 23.77% through 2031, which makes it the fastest-growing geography in the CXL signal conditioner and retimer IC market size by region. China is strengthening local retimer participation, and Montage Technology has already sampled PCIe 6.x and CXL 3.x retimers and launched an active electrical cable solution aimed at next-generation data center interconnects. Taiwan remains central through its ODM and IC design ecosystem, while South Korea is important because memory and module ecosystems there support downstream CXL deployment. Japan also contributes through signal-conditioning and timing component capabilities within the wider server connectivity chain. South America and Middle East and Africa remain smaller today, but both are structurally relevant over the forecast period as regional cloud and sovereign AI infrastructure deployments create additional pull for high-speed server hardware. As platform costs normalize and qualification capabilities spread, these regions are expected to take a larger role in later-stage CXL server and memory-fabric deployments.

Competitive Landscape

The CXL signal conditioner and retimer IC market is moderately concentrated, with Astera Labs, Broadcom, and Marvell holding the deepest positions in hyperscale and advanced AI platform qualification. Their advantage comes from more than product breadth because they also benefit from proven interoperability, customer design support, and earlier access to volume deployments. Astera Labs strengthened that position by moving Aries 6 retimers and smart cable modules into volume production with leading AI and cloud customers in 2025. Broadcom reinforced its standing through the BCM85667, a PCIe Gen 6 and CXL 3.1 retimer built on 5 nm geometry and aligned with the Intel PCIe 6.0 Supplemental Footprint. Marvell widened its position by combining retimers, active electrical cable endpoints, and CXL switch capabilities in a broader connectivity portfolio.

The competitive pattern is shaped by hyperscaler multi-sourcing requirements, which means even strong incumbents rarely operate alone on major platforms. That creates room for challengers such as Microchip Technology and Montage Technology to win positions where customers want a second or third qualified source. Microchip’s June 2026 retimer launch was one such move because it paired low latency with diagnostic integration, which directly targets hyperscale requirements for link health visibility and system-level management. Montage Technology made another strategic move in January 2026 by extending from retimer chips into active electrical cable solutions, which allowed it to address a wider part of the interconnect stack. These moves show that competition is no longer only about standalone lane recovery because vendors are also trying to capture system-level positions in cable, switch, and memory-fabric environments.

The market also shows a split between broad analog and connectivity suppliers on one side and pure-play high-speed interconnect specialists on the other. The first group can compete on scale, portfolio range, and existing OEM relationships, while the second group often focuses on latency, platform software, and faster ecosystem support. White-space opportunities remain in PCIe 7.0 and CXL 4.0 preparation, active optical cable integration, and switch-adjacent retimer architectures where leadership is not yet fixed. That is important because the CXL signal conditioner and retimer IC market is still early enough for product architecture choices to reshape future share positions. Vendors that can maintain overlapping generation roadmaps while supporting qualification across boards, cables, and fabrics are likely to hold the strongest long-term positions. Vendors that fail to keep pace with standard revisions or ecosystem testing may remain technically capable but commercially sidelined.

CXL Signal Conditioner and Retimer IC Industry Leaders

Broadcom Inc.

Astera Labs, Inc.

Marvell Technology, Inc.

Texas Instruments Incorporated

Renesas Electronics Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Microchip Technology commercially launched XpressConnect PCIe 6.0 and CXL 3.1 retimers, delivering sub-12 ns pin-to-pin latency approximately 80% below the PCIe 6.0 specification ceiling, with link bifurcation support for 1×16, 2×8, and 4×4 configurations. The product integrates with Microchip's ChipLink diagnostic ecosystem for in-production link monitoring and targets memory expansion and resource disaggregation across complex AI fabrics, competing directly with Astera Labs and Broadcom in hyperscale design-ins.

- May 2026: Astera Labs reported record Q1 2026 revenue of USD 308.4 million (93% year-over-year, 14% quarter-over-quarter) and launched the Scorpio X-Series 320-lane Smart Fabric Switch for frontier AI lab workloads, featuring Hypercast and In-Network Compute capabilities with up to 2x improvement in collective operations. Q2 2026 revenue guidance was set between USD 355 million and USD 365 million, with Scorpio P-Series PCIe 6 Fabric Switch volume ramps expected across multiple hyperscale customers in H2 2026.

- March 2026: Marvell Technology announced the Structera S 30260 CXL 3.x switch at OFC 2026, offering 260 lanes, support for 16 to 32 CPUs or GPUs, up to 48 TB of shared memory, and 4 TB/s cumulative bandwidth, with customer sampling guided for Q3 2026. The announcement made Marvell the first vendor with a CXL portfolio spanning all three product categories, memory expansion, memory acceleration, and memory pooling, each requiring Alaska P PCIe and CXL retimers for reach extension.

- January 2026: Montage Technology launched its PCIe 6.x and CXL 3.x active electrical cable solution, jointly designed with leading cable manufacturers in China and validated through interoperability tests with CPUs, xPUs, PCIe switches, and NICs. The solution targets supernode interconnect architectures for hyperscalers and high-performance server platforms, extending the company's PCIe 6.x retimer portfolio into cable-form-factor deployments and representing a commercial milestone for Chinese active electrical cable retimer supply.

Global CXL Signal Conditioner and Retimer IC Market Report Scope

The Global CXL Signal Conditioner and Retimer IC Market refers to the industry segment focused on the design, production, and deployment of integrated circuits (ICs) that enhance signal integrity and reliability in Compute Express Link (CXL) systems by conditioning and retiming high-speed data transmissions.

The CXL Signal Conditioner and Retimer IC Market Report is Segmented by Product Type (CXL-Compatible Retimer ICs, CXL-Compatible Signal Conditioner / Redriver ICs, and CXL-Compatible Active Signal-Conditioning ICs), PCIe/CXL Generation Compatibility (PCIe 5.0 / CXL 1.x-2.0 Compatible, PCIe 6.0 / CXL 3.x Compatible, PCIe 7.0 / CXL 4.0 Compatible, and Multi-Generation Backward-Compatible ICs), Deployment Form (Discrete Board-Level Retimer / Signal Conditioner ICs, Riser-Card and Add-In-Board Embedded ICs, Active Electrical Cable and Smart Cable Module Embedded ICs, and Connector-, Backplane-, and Chassis-Embedded ICs), Application (AI and GPU Accelerator Servers, High-Performance Computing and Supercomputing Systems, Hyperscale and Cloud Compute Servers, CXL Memory Expansion and Memory Pooling Platforms, Enterprise and Private Cloud Servers, CXL Fabric Switches and Composable Infrastructure, Storage, JBOF, and CXL-Enabled Storage Appliances, and Active Electrical Cable and Rack-Scale Interconnect Platforms), End User (Hyperscalers, Cloud Service Providers and Neocloud Providers, Server, Storage, and Networking OEMs, ODMs and System Platform Manufacturers, HPC Centers, Research Institutions, and Supercomputing Facilities, Large Enterprises and Private Cloud Operators, and Telecom, Edge Cloud, and Colocation Operators), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The Market Forecasts Are Provided in Terms of Value (USD).

| CXL-Compatible Retimer ICs |

| CXL-Compatible Signal Conditioner / Redriver ICs |

| CXL-Compatible Active Signal-Conditioning ICs |

| PCIe 5.0 / CXL 1.x-2.0 Compatible |

| PCIe 6.0 / CXL 3.x Compatible |

| PCIe 7.0 / CXL 4.0 Compatible |

| Multi-Generation Backward-Compatible ICs |

| Discrete Board-Level Retimer / Signal Conditioner ICs |

| Riser-Card and Add-In-Board Embedded ICs |

| Active Electrical Cable and Smart Cable Module Embedded ICs |

| Connector-, Backplane-, and Chassis-Embedded ICs |

| AI and GPU Accelerator Servers |

| High-Performance Computing and Supercomputing Systems |

| Hyperscale and Cloud Compute Servers |

| CXL Memory Expansion and Memory Pooling Platforms |

| Enterprise and Private Cloud Servers |

| CXL Fabric Switches and Composable Infrastructure |

| Storage, JBOF, and CXL-Enabled Storage Appliances |

| Active Electrical Cable and Rack-Scale Interconnect Platforms |

| Hyperscalers |

| Cloud Service Providers and Neocloud Providers |

| Server, Storage, and Networking OEMs |

| ODMs and System Platform Manufacturers |

| HPC Centers, Research Institutions, and Supercomputing Facilities |

| Large Enterprises and Private Cloud Operators |

| Telecom, Edge Cloud, and Colocation Operators |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Southeast Asia | |

| Rest of Asia-Pacific | |

| South America | |

| Middle East and Africa |

| By Product Type | CXL-Compatible Retimer ICs | |

| CXL-Compatible Signal Conditioner / Redriver ICs | ||

| CXL-Compatible Active Signal-Conditioning ICs | ||

| By PCIe/CXL Generation Compatibility | PCIe 5.0 / CXL 1.x-2.0 Compatible | |

| PCIe 6.0 / CXL 3.x Compatible | ||

| PCIe 7.0 / CXL 4.0 Compatible | ||

| Multi-Generation Backward-Compatible ICs | ||

| By Deployment Form | Discrete Board-Level Retimer / Signal Conditioner ICs | |

| Riser-Card and Add-In-Board Embedded ICs | ||

| Active Electrical Cable and Smart Cable Module Embedded ICs | ||

| Connector-, Backplane-, and Chassis-Embedded ICs | ||

| By Application | AI and GPU Accelerator Servers | |

| High-Performance Computing and Supercomputing Systems | ||

| Hyperscale and Cloud Compute Servers | ||

| CXL Memory Expansion and Memory Pooling Platforms | ||

| Enterprise and Private Cloud Servers | ||

| CXL Fabric Switches and Composable Infrastructure | ||

| Storage, JBOF, and CXL-Enabled Storage Appliances | ||

| Active Electrical Cable and Rack-Scale Interconnect Platforms | ||

| By End User | Hyperscalers | |

| Cloud Service Providers and Neocloud Providers | ||

| Server, Storage, and Networking OEMs | ||

| ODMs and System Platform Manufacturers | ||

| HPC Centers, Research Institutions, and Supercomputing Facilities | ||

| Large Enterprises and Private Cloud Operators | ||

| Telecom, Edge Cloud, and Colocation Operators | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Southeast Asia | ||

| Rest of Asia-Pacific | ||

| South America | ||

| Middle East and Africa | ||

Key Questions Answered in the Report

What is the current and forecast value of the CXL signal conditioner and retimer IC market?

The CXL signal conditioner and retimer IC market was valued at USD 0.90 billion in 2025, is valued at USD 1.19 billion in 2026, and is forecast to reach USD 3.32 billion by 2031 at a 22.77% CAGR.

Which product category leads demand for these ICs?

CXL-compatible retimer ICs led product demand with 84.12% share in 2025 because they are required in many Gen 5 and Gen 6 high-speed server links.

Which application is growing the fastest through 2031?

CXL memory expansion and memory pooling platforms are projected to grow the fastest at a 24.32% CAGR, supported by hyperscaler interest in reducing stranded DRAM and improving memory efficiency.

Which end-user group is the largest buyer today?

Hyperscalers were the largest end-user group with 57.77% share in 2025 because they lead AI server deployment and early CXL memory pooling adoption.

Which region offers the strongest growth outlook?

Asia-Pacific is projected to grow the fastest at a 23.77% CAGR through 2031, supported by regional server manufacturing, local supplier development, and expanding AI infrastructure.

What is driving vendor competition in this space?

Competition is shaped by Gen 6 qualification depth, hyperscaler multi-sourcing needs, cable and switch integration, and the ability to manage fast-moving PCIe and CXL standards.

Page last updated on: