CXL PCIe 6.0 PHY IP Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

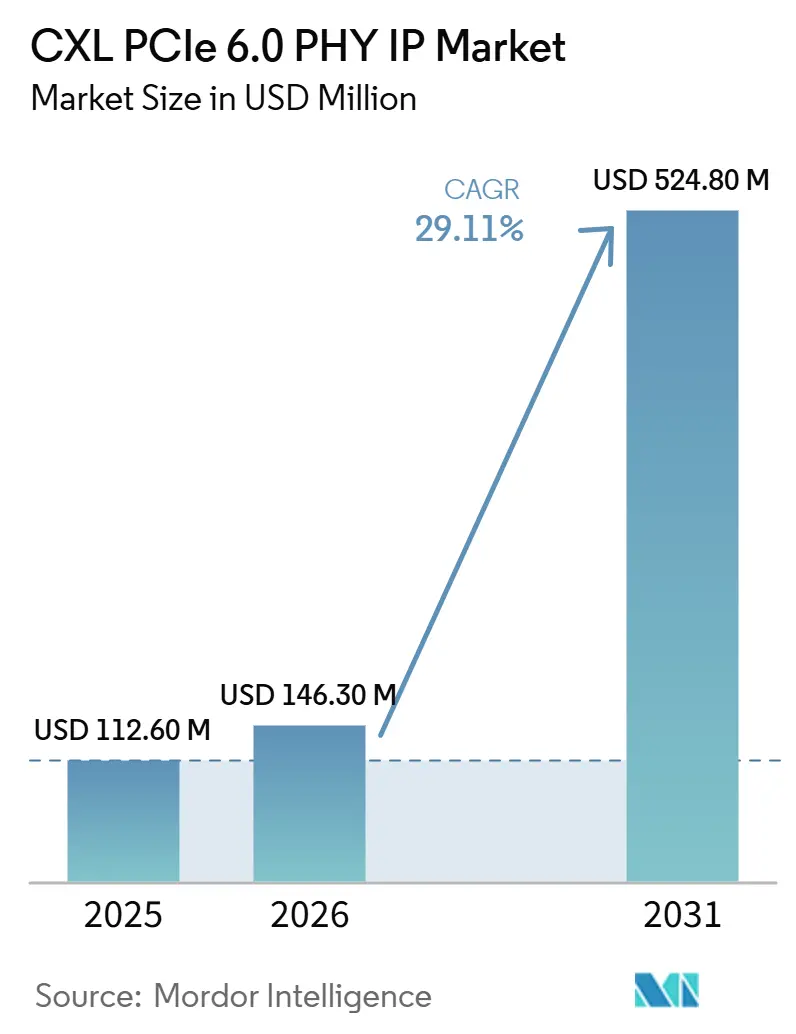

| Market Size (2026) | USD 146.30 Million |

| Market Size (2031) | USD 524.80 Million |

| Growth Rate (2026 - 2031) | 29.11% CAGR |

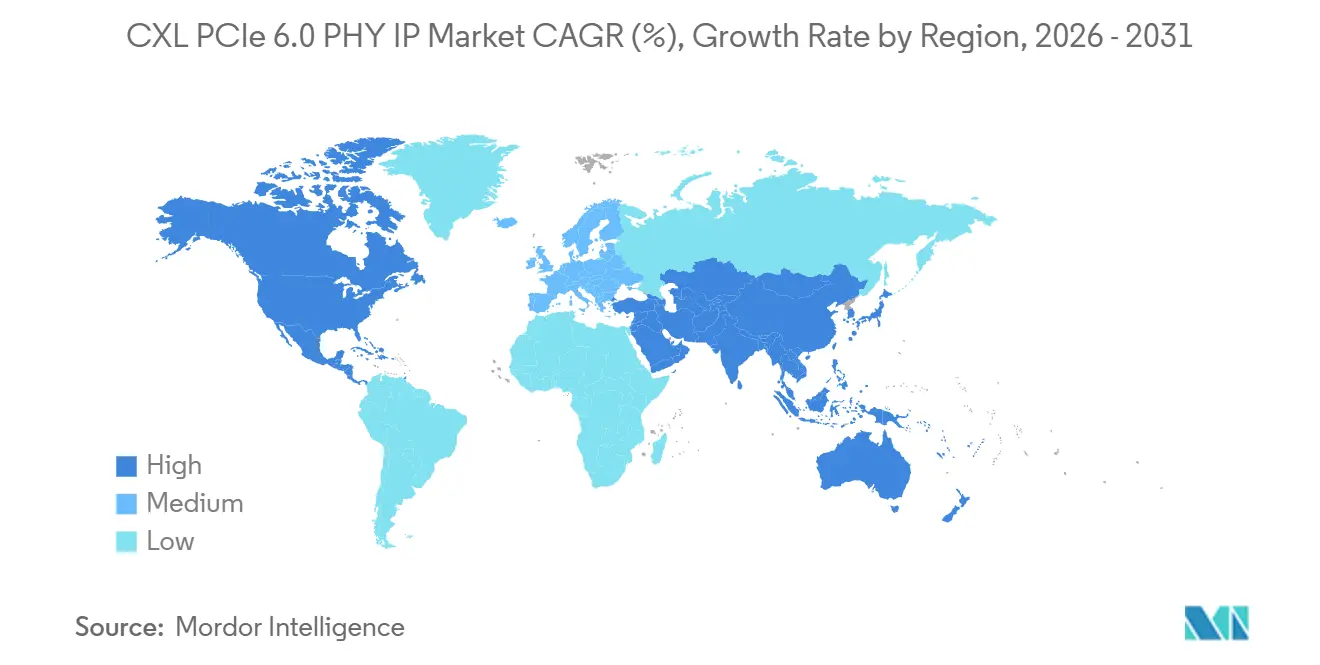

| Fastest Growing Market | North America |

| Largest Market | Asia-Pacific |

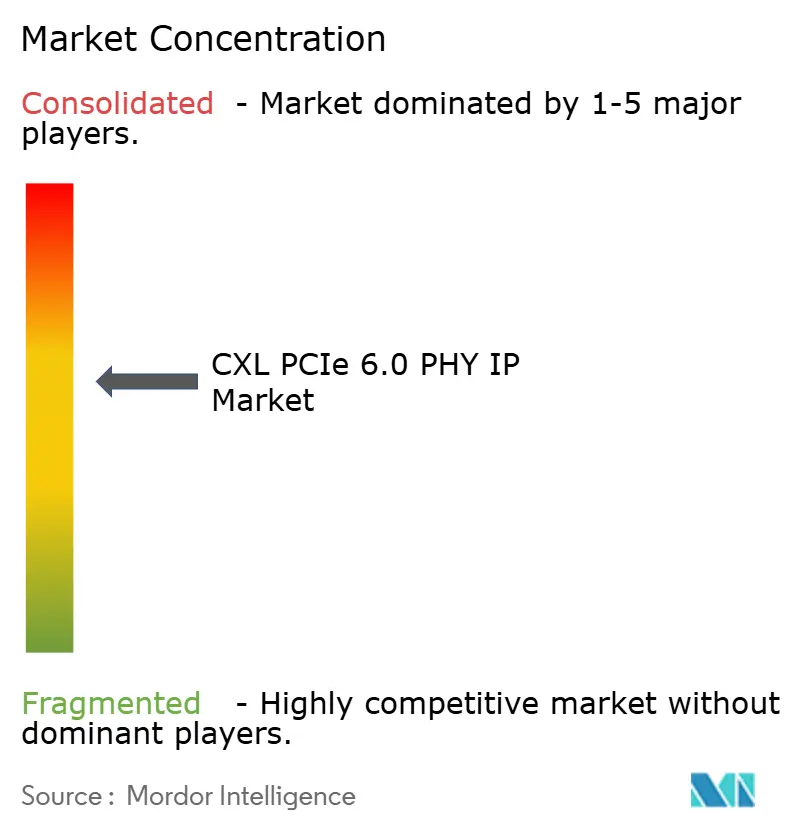

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

CXL PCIe 6.0 PHY IP Market Analysis by Mordor Intelligence

The CXL PCIe 6.0 PHY IP market size is projected to be USD 112.60 million in 2025, USD 146.30 million in 2026, and reach USD 524.80 million by 2031, growing at a CAGR of 29.11% from 2026 to 2031. The CXL PCIe 6.0 PHY IP market is moving quickly because PCIe 6.0 and CXL 3.x now share the same 64 GT/s PAM4 physical layer, which lets chip designers buy one proven PHY block instead of separate interfaces. That shift has raised the value of silicon-proven IP with compliance support, characterization data, and foundry-specific tuning, especially for programs that cannot afford schedule slips at advanced nodes. Demand is also being lifted by AI accelerator and memory expansion designs that need far higher bandwidth and tighter coherency behavior than earlier PCIe generations could support. The CXL PCIe 6.0 PHY IP market also benefits from growing interest in modular licensing models, because many SoC teams want controller flexibility while still shortening analog design risk. The main near-term constraint is ecosystem readiness, since compliance, host platforms, and full production validation are still concentrated among top-tier cloud and AI programs.

Key Report Takeaways

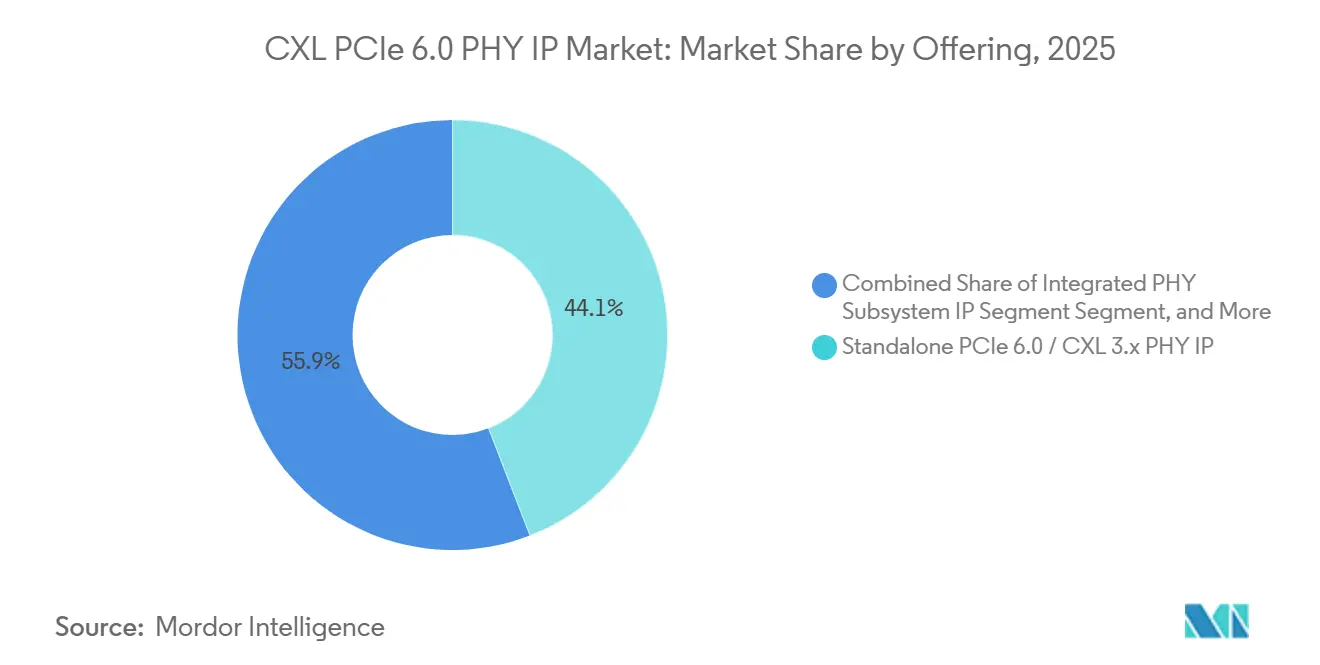

- By offering, standalone PCIe 6.0 and CXL 3.x PHY IP held 44.13% share of the CXL PCIe 6.0 PHY IP market size in 2025, while integrated PHY subsystem IP is projected to expand at a 29.89% CAGR through 2031.

- By protocol capability, PCIe 6.0 PHY IP with CXL 3.0 and CXL 3.1 support captured 48.86% share of the CXL PCIe 6.0 PHY IP market size in 2025, while multi-protocol 64 GT/s PHY IP is expected to grow at a 29.67% CAGR through 2031.

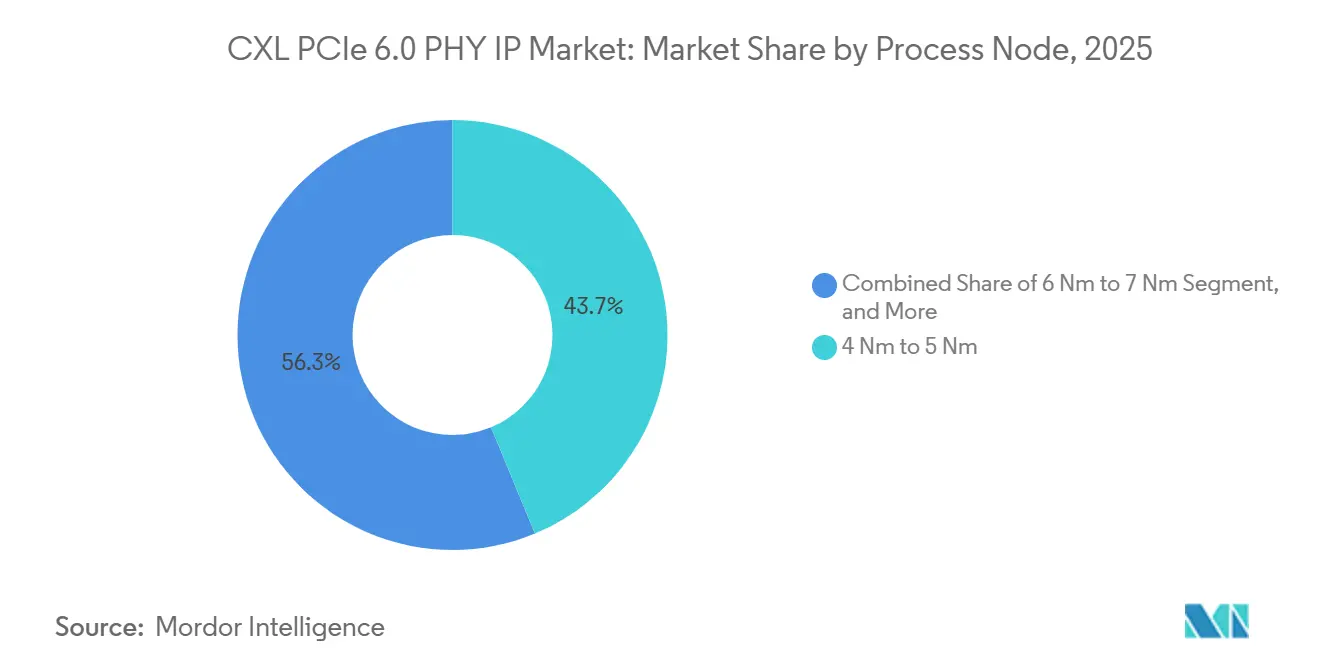

- By process node, 4 nm to 5 nm accounted for 43.73% share of the CXL PCIe 6.0 PHY IP market size in 2025, while 3 nm and below is projected to register a 30.08% CAGR through 2031.

- By IP configuration, x16 and above PHY IP subsystem held 42.61% share of the CXL PCIe 6.0 PHY IP market size in 2025, while x8 PHY IP subsystem is projected to expand at a 29.83% CAGR through 2031.

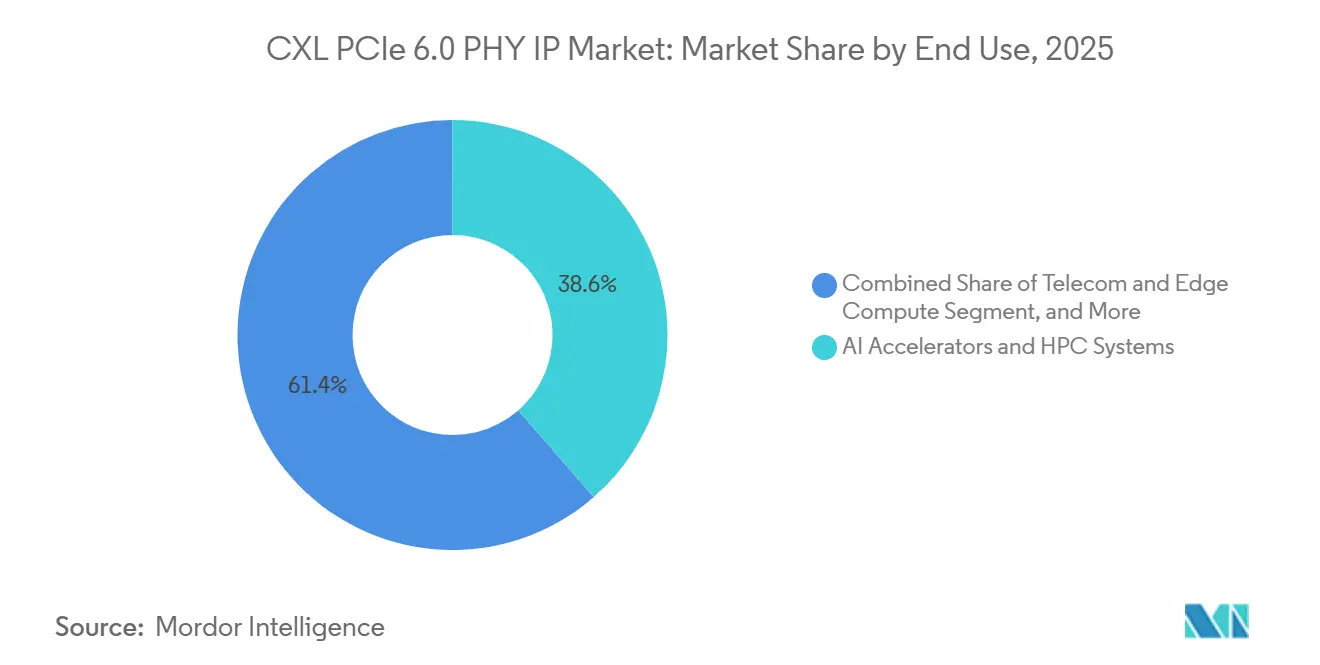

- By end use, AI accelerators and HPC systems represented 38.59% share of the CXL PCIe 6.0 PHY IP market size in 2025, while CXL memory expansion and memory pooling infrastructure is expected to advance at a 30.42% CAGR through 2031.

- By geography, North America held 43.27% share of the CXL PCIe 6.0 PHY IP market size in 2025, while Asia-Pacific is projected to grow at a 30.06% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global CXL PCIe 6.0 PHY IP Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid AI Accelerator and Hyperscale Coherent Memory Demand | +7.8% | Global, with concentration in North America and Asia-Pacific | Short term (≤ 2 years) |

| PCIe 6.0 and CXL Convergence in Next-Generation SoCs | +5.9% | Global, early adoption in North America, spillover to Asia-Pacific and Europe | Short term (≤ 2 years) |

| Shift to PAM4 and Advanced SerDes IP Outsourcing | +4.2% | North America, Europe, Asia-Pacific core | Medium term (2-4 years) |

| Need for Lower-Latency Memory Disaggregation in Data Centers | +3.1% | North America, Asia-Pacific, China, Japan, South Korea | Medium term (2-4 years) |

| Multi-Protocol PHY Reuse Across PCIe, CXL, and Ethernet | +2.2% | Global, with early gains in North America and Taiwan | Medium term (2-4 years) |

| Advanced Node Tapeout Pressure Favors Proven IP Blocks | +1.8% | North America, Asia-Pacific, Taiwan, South Korea | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid AI Accelerator and Hyperscale Coherent Memory Demand

AI accelerator SoC programs have become the main buying trigger for the CXL PCIe 6.0 PHY IP market, and they now carry more weight than a normal server refresh cycle. Hyperscale operators need 64 GT/s lane performance because larger AI clusters place much heavier pressure on memory movement, cache coherence, and rack-scale bandwidth than earlier cloud workloads. CXL 3.0 strengthened that case by extending coherent memory behavior over the PCIe 6.0 physical layer, which made the shared PHY more important in new accelerator designs. Published 2025 research also showed that CXL-attached DRAM with full-duplex channels delivered 55-61% higher bandwidth at balanced read and write ratios than flat DDR5 setups, which gave system architects a more direct performance reason to specify CXL-enabled interfaces.[1]“CXLAimPod, CXL Memory Is All You Need in AI Era,” arXiv, arxiv.org The CXL PCIe 6.0 PHY IP market is benefiting because every accelerator, switch, or memory controller built around that architecture still needs a licensable high-speed physical interface. As AI system design shifts from simple compute scaling to memory-aware scaling, the CXL PCIe 6.0 PHY IP market is seeing stronger pull from programs that want both bandwidth and coherency in a single IP decision.

PCIe 6.0 And CXL Convergence in Next-Generation SoCs

The convergence of PCIe 6.0 and CXL 3.x has turned two earlier procurement paths into one, and that has made the CXL PCIe 6.0 PHY IP market more valuable at the PHY layer. Designers that support both standards in one SoC can now reduce duplication in area and power, which makes a combined PHY block more attractive than separate implementations. Cadence reinforced that direction in June 2025 when it extended its Samsung Foundry relationship to include PCIe 6.0 and CXL 3.2 PHY and controller IP on advanced Samsung nodes.[2]Cadence Design Systems, “Cadence and Samsung Foundry Expand Multi-Year IP Agreement to Advance AI,” Cadence Design Systems, cadence.com Alphawave Semi also showed commercial demand for converged I/O when it taped out a multi-protocol connectivity chiplet that supports PCIe 6.0, CXL 3.1, and 800G Ethernet in mixed modes. Synopsys then demonstrated PCIe 6.x interoperability with Broadcom’s PEX90000 switch at 64 GT/s in June 2025, which showed that the surrounding compliance and interoperability stack was becoming more practical for real design wins. The CXL PCIe 6.0 PHY IP market is therefore being pushed not just by protocol demand, but by a broader design preference for unified physical interfaces that reduce integration risk.

Shift To PAM4 and Advanced SerDes IP Outsourcing

The move from NRZ to PAM4 at 64 GT/s changed the in-house design equation for the CXL PCIe 6.0 PHY IP market because the analog and DSP burden rose sharply. PCIe 6.0 introduced new signal quality requirements such as SNDR and RLM, and that pushed developers toward more advanced receiver and equalization approaches than prior generations needed. Building that capability internally now requires specialized analog engineering, more validation tools, and extra tapeout learning cycles, which many chip teams do not want to absorb on first-generation programs. Credo’s September 2025 launch of 224G PAM4 SerDes IP on TSMC N3 highlighted how specialist SerDes vendors are moving faster to support advanced-node requirements for hyperscale and AI customers.[3]Credo Technology Group, “Credo’s Toucan PCIe Retimer Achieves PCI-SIG Compliance,” Credo Technology Group, credosemi.com The CXL PCIe 6.0 PHY IP market is also seeing stronger outsourcing demand because vendors can package proven IP with characterization and subsystem support, which shortens internal validation work. As a result, the CXL PCIe 6.0 PHY IP market is shifting from a pure performance decision to a risk transfer decision for teams that need proven 64 GT/s execution.

Need For Lower-Latency Memory Disaggregation in Data Centers

The push toward disaggregated memory is expanding the addressable base of the CXL PCIe 6.0 PHY IP market beyond accelerator SoCs alone. AI inference clusters and memory-heavy cloud workloads need much larger DRAM pools than local CPU memory channels can provide, and CXL-based memory expansion is becoming a more practical way to meet that need. IEEE research published in 2026 showed that CXL-based disaggregated memory can support cloud-native database orchestration with near-local memory access performance, which strengthens the case for deployment beyond laboratory testing. A 2025 CXL Consortium webinar also cited up to 19% higher performance with CXL-connected DRAM in vector database search workloads, which linked memory expansion more directly to AI-serving use cases. The CXL PCIe 6.0 PHY IP market benefits because memory expansion controllers, retimers, and fabric switches all depend on the same high-speed PHY building block. That widens the licensing pool and gives the CXL PCIe 6.0 PHY IP market another growth path even when accelerator design cycles temporarily slow.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Validation Cost for PCIe 6.0 PAM4 PHY Compliance | -2.4% | Global, most acute in North America and Europe | Short term (≤ 2 years) |

| Limited Design Wins Outside Tier 1 Hyperscale and AI Programs | -1.6% | Global, particularly affecting Europe, South America, and Middle East and Africa | Medium term (2-4 years) |

| Signal Integrity Challenges at 64 GT/s Raise Integration Risk | -1.1% | Global, most acute in Asia-Pacific high-volume packaging environments | Medium term (2-4 years) |

| Long Tapeout Cycles and Ecosystem Readiness Constraints | -0.8% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Validation Cost for PCIe 6.0 PAM4 PHY Compliance

Validation remains one of the clearest brakes on the CXL PCIe 6.0 PHY IP market because 64 GT/s PAM4 testing needs more expensive tools and more engineering time than earlier PCIe generations. PCIe 6.0 compliance requires different measurement methods and protocol-specific patterns, which adds complexity for transmitter, jitter, and stressed-eye validation. Synopsys responded with an official PCIe 6.x Gold System for pre-FYI compliance testing, but the value of that environment is highest for customers already working with top-tier IP ecosystems. Smaller design teams can struggle to justify the tool cost, lab time, and repeated characterization work that accompany a first PAM4 tapeout. The CXL PCIe 6.0 PHY IP market therefore remains skewed toward large hyperscale and AI-related programs that can absorb that burden more easily. Until broader host availability and test maturity improve, validation cost will continue to slow expansion into second-tier customer groups.

Limited Design Wins Outside Tier 1 Hyperscale and AI Programs

The CXL PCIe 6.0 PHY IP market still relies heavily on a narrow first wave of hyperscale cloud operators and AI accelerator developers for early volume. Many enterprise server, telecom, and mainstream networking programs are still moving through PCIe 5.0 cycles, which means their PCIe 6.0 adoption will arrive later. That delay matters because the CXL PCIe 6.0 PHY IP market needs broader design-win diversity to reduce dependence on a few large customers and a few high-value tapeouts. The restraint is reinforced by the early stage of commercial CXL memory modules and the small installed base of PCIe 6.0-capable host platforms, which limits downstream pull from device and subsystem makers. Vendors are still building around that timing mismatch, and many mid-market buyers appear more focused on readiness and ecosystem proof than on being early adopters. The CXL PCIe 6.0 PHY IP market is likely to stay concentrated in large AI and top-tier cloud programs until that wider platform transition becomes more visible.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Standalone IP Leads While Integrated Subsystems Gain Ground

Standalone PCIe 6.0 and CXL 3.x PHY IP held 44.13% of revenue in 2025, which made it the leading offering in the CXL PCIe 6.0 PHY IP market. That position reflects the preference of advanced SoC teams for modular PHY blocks that can connect with their own controllers or selected third-party logic. Many large chip programs still want freedom at the controller layer because that gives them more control over system architecture, security, workload tuning, and foundry migration. The standalone model also fits well with hyperscaler design strategies that avoid overdependence on a single subsystem stack. In the CXL PCIe 6.0 PHY IP market, that keeps demand high for licensable cores backed by characterization data, compliance support, and process-porting experience. Verification, compliance, and characterization collateral have also become more important inside the standalone category because PAM4 validation can materially lengthen time to deployment. Synopsys highlighted that need with its PCIe 6.x Gold System approach, which gave customers an earlier compliance path before broad commercial host availability. That kind of collateral raises the value of a standalone license because it reduces uncertainty beyond the circuit block itself. It also helps explain why premium PHY vendors can defend pricing even when modular licensing seems simpler on paper. In practice, the leading standalone offer is no longer just a PHY macro, but a risk-managed entry point into high-speed product execution.

Integrated PHY subsystem IP is projected to grow at a 29.89% CAGR through 2031, which makes it the fastest-growing offering in the CXL PCIe 6.0 PHY IP market. This shift reflects a different buyer profile, especially teams handling first-generation PCIe 6.0 or CXL programs with limited internal PAM4 expertise. A bundled controller and PHY shortens integration cycles, reduces debugging overlap across suppliers, and moves more system responsibility to the IP licensor. That model is increasingly attractive for CXL memory controller ASICs, retimers, and DPU programs where the schedule risk of a fragmented stack is high. Cadence’s continued expansion of process-specific PCIe 6.0 and CXL PHY and controller support for Samsung Foundry shows how integrated offerings are becoming more tailored to specific manufacturing paths. In the CXL PCIe 6.0 PHY IP industry, that makes porting, integration, and customization services a stronger revenue layer instead of a secondary add-on. Design teams also see value in receiving one coordinated qualification package rather than building proof across separate PHY and controller vendors. As node transitions accelerate from 5 nm toward 3 nm and below, this subsystem model should keep gaining relevance among buyers that value speed and risk control over maximum architecture flexibility. The result is a CXL PCIe 6.0 PHY IP market where the biggest current revenue sits with modular cores, but the fastest future expansion comes from tightly bundled solutions. That balance is likely to define vendor packaging strategy through the forecast period.

By Protocol Capability: Dual-Mode Support Holds the Lead While Multi-Protocol Reuse Scales

PCIe 6.0 PHY IP with CXL 3.0 and CXL 3.1 support accounted for 48.86% of revenue in 2025, the largest protocol capability share in the CXL PCIe 6.0 PHY IP market. This result is tied to the fact that most advanced data center SoCs now need both standard PCIe connectivity and coherent CXL memory behavior from the same interface. A PCIe-only implementation is no longer sufficient for many server, accelerator, and fabric designs that need memory pooling or coherency features. The CXL 3.0 specification itself makes that linkage structural because the protocol sits on top of the PCIe 6.0 physical interface rather than beside it. That gives dual-mode PHY support a durable advantage in the CXL PCIe 6.0 PHY IP market, especially where server processors and accelerator platforms are being designed for longer roadmap relevance. Buyers also view dual-mode support as a hedge against architecture shifts because it preserves optionality between standard I/O expansion and coherent memory deployment. That means the largest share is not simply a reflection of current demand, but a response to uncertainty in how future platforms will use CXL at scale. In many programs, a dual-mode PHY has become the default starting point rather than a premium upgrade. This is one reason the CXL PCIe 6.0 PHY IP market continues to favor suppliers with broad protocol roadmaps and mature interoperability support. It also reinforces why vendors that can prove both PCIe and CXL readiness hold a stronger position during licensing decisions.

Multi-protocol 64 GT/s PHY IP is projected to grow at a 29.67% CAGR through 2031, and this reflects the widening use of shared SerDes across several standards. Chiplet-based designs, SmartNICs, and DPUs increasingly need PCIe, CXL, and Ethernet support from a unified high-speed infrastructure to limit die area and power. Alphawave Semi’s AlphaCHIP1600-IO chiplet showed that direction clearly by combining PCIe 6.0, CXL 3.1, and 800G Ethernet support in one mixed-mode design. The CXL PCIe 6.0 PHY IP market gains from this pattern because each reusable high-speed lane can serve more product classes and more system roles. Vendors that support such reuse are better placed to win designs where bandwidth is critical but silicon area and thermal limits are tight. PCIe-only PHY IP still holds a steady place in storage controllers and selected automotive compute designs where CXL support is not essential. Even so, the forward demand pattern in the CXL PCIe 6.0 PHY IP market is moving toward flexible lane infrastructure that supports multiple protocols without duplicating analog resources. That trend favors vendors with stronger portfolio breadth and broader compliance coverage instead of narrow single-standard products. Over time, protocol flexibility is likely to matter as much as raw signal performance in many buying decisions. The growth of this segment therefore says as much about system architecture economics as it does about interconnect standards.

By Process Node: 4 nm to 5 nm Generates the Largest Revenue While Sub-3 nm Builds Momentum

The 4 nm to 5 nm range held 43.73% of revenue in 2025, which gave it the leading process position in the CXL PCIe 6.0 PHY IP market size. This range remains central because many active AI SoC, GPU, and server silicon programs are still concentrated on commercially mature advanced nodes with better yield learning and broader ecosystem support. Buyers often prefer this part of the node curve because it offers strong performance while keeping characterization confidence higher than very early sub-3 nm deployments. The CXL PCIe 6.0 PHY IP market therefore still leans on 4 nm and 5 nm for current licensing revenue even as marketing attention shifts to smaller nodes. Proven track records matter here because 64 GT/s PHY integration is sensitive to process behavior, packaging interaction, and equalization tuning. Vendors that have already built mature data around these nodes can reduce uncertainty for customers that are moving fast and taping out large dies. That advantage can matter more than theoretical performance gains when a single schedule miss affects a broader accelerator or server roadmap. It also explains why commercially proven node support remains a strong sales argument across the CXL PCIe 6.0 PHY IP market. In practical terms, the node leader benefits from a combination of demand volume, manufacturing maturity, and lower execution anxiety. These factors should keep 4 nm and 5 nm highly relevant even while future growth shifts lower.

The 3 nm and below segment is projected to grow at a 30.08% CAGR through 2031, making it the fastest-growing node tier in the CXL PCIe 6.0 PHY IP market. This reflects the migration of next-generation AI accelerators and network processors toward tighter power and area envelopes that make sub-3 nm more attractive. At these nodes, PHY risk becomes even more consequential because parasitic behavior, analog margins, and thermal constraints are harder to manage. That is why the CXL PCIe 6.0 PHY IP market increasingly rewards vendors that bring node-specific tuning instead of generic portability claims. Cadence’s expansion of Samsung Foundry-oriented PCIe 6.0 and CXL support and Credo’s N3-based SerDes launch both point to the commercial importance of early advanced-node readiness. The value of a proven PHY rises at smaller geometries because the penalty for analog rework is larger and the number of teams with deep internal expertise is smaller. By contrast, 6 nm to 7 nm and 8 nm to 16 nm remain important for more cost-sensitive programs in networking and industrial uses. Nodes above 16 nm still serve niche designs with legacy requirements and long supply-chain validation cycles. Even so, future mix shift in the CXL PCIe 6.0 PHY IP market is likely to come from the tension between rising performance demands and rising execution risk at sub-3 nm. That makes advanced-node qualification depth a central competitive lever. It also suggests that the fastest growth will favor vendors with strong foundry alignment rather than vendors with only broad theoretical protocol support.

By IP Configuration: Wide-Lane Designs Lead Today While x8 Gains Strength from Memory Expansion

The x16 and above PHY IP subsystem held 42.61% of revenue in 2025, which made it the largest IP configuration in the CXL PCIe 6.0 PHY IP market. This lead is tied to AI accelerator and GPU designs that need the highest per-chip bandwidth and therefore favor the widest lane counts. A single x16 PCIe 6.0 link can deliver 256 GB/s of raw bidirectional bandwidth, which aligns well with memory-hungry compute architectures. Synopsys has emphasized dense x16-capable PHY integration and low package crosstalk in its PCIe 6.x offering, which reflects how important routing quality becomes at that lane count. In the CXL PCIe 6.0 PHY IP market, wide-lane demand also carries a higher value per license because these designs often pair advanced nodes, larger die area, and stricter validation requirements. The configuration therefore contributes strongly to revenue even if the unit count is not the highest across all applications. Smaller lane counts such as x4 and single-lane variants still serve edge systems, test equipment, and selected storage uses. Those configurations form a useful base business, but they do not usually command the same value profile as large accelerator-class interfaces. That gap is why the current revenue leader remains tied to top-end compute rather than broad lower-bandwidth deployment. For now, the largest configuration reflects the concentration of early PCIe 6.0 and CXL demand in high-performance systems.

The x8 PHY IP subsystem is projected to grow at a 29.83% CAGR through 2031, and that makes it the fastest-growing configuration in the CXL PCIe 6.0 PHY IP market. This rise is closely linked to CXL Type 3 memory expansion and memory pooling hardware, where x8 often provides a better balance of bandwidth, power, and board constraints than x16. The CXL PCIe 6.0 PHY IP market size for x8-related memory designs is improving because memory modules and attached infrastructure need scalable links without overextending thermal and form-factor limits. Marvell’s Structera S 30260 reinforced that direction by targeting PCIe 6.0 and CXL 3.x switching for large shared-memory environments with substantial lane density and fabric scale. As memory pooling moves from concept to deployment, x8 becomes more attractive because it supports practical fabric attachment while avoiding some of the physical cost of wider interfaces. Vendors are responding by shaping subsystem offers around lower power-per-lane behavior and faster integration for x8-centered deployments. That gives the CXL PCIe 6.0 PHY IP market another growth path that is different from the traditional accelerator-first story. It also broadens the type of buyer entering the category, especially in memory controller, switch, and retimer programs. Over the forecast period, x8 should benefit from the spread of CXL memory infrastructure into more mainstream data center architectures. This makes it one of the clearest examples of how end-use change can alter PHY configuration demand.

By End Use: AI and HPC Dominate Current Revenue While Memory Pooling Expands Fastest

AI accelerators and HPC systems accounted for 38.59% of revenue in 2025, which made them the largest end-use segment in the CXL PCIe 6.0 PHY IP market. These applications sit at the center of current demand because they combine high bandwidth requirements, advanced nodes, wide-lane configurations, and large license values. In many cases, the PHY is not a peripheral decision but a critical enabler of system-level performance and schedule reliability. The CXL PCIe 6.0 PHY IP market therefore captures outsized value from AI and HPC even when the total number of programs is narrower than in mature server categories. National lab upgrades, hyperscale cluster build-outs, and accelerator competition have all supported this revenue concentration. The use case is especially favorable for vendors because AI accelerator designs often demand premium support around integration, characterization, and compliance. That raises both the technical and commercial weight of each design win. It also explains why suppliers place so much attention on hyperscaler and AI silicon relationships. The end-use leader today reflects not broad market saturation, but the high value of a relatively concentrated customer set. This concentration is likely to continue until broader enterprise platforms shift more meaningfully toward PCIe 6.0 and CXL.

CXL memory expansion and memory pooling infrastructure is projected to grow at a 30.42% CAGR through 2031, which makes it the fastest-growing end-use area in the CXL PCIe 6.0 PHY IP market. Operators are increasingly treating pooled or expandable DRAM as a lower-cost path to memory scale than relying only on more expensive on-package memory strategies. USENIX NSDI 2026 research on switched CXL memory pooling showed that fabric-based memory allocation can deliver practical latency behavior for memory-bandwidth-bound workloads. IEEE research on Pangaea v2 and the 2025 CXL Consortium webinar both added evidence that disaggregated memory can support real cloud-native and AI-serving scenarios rather than only experimental ones. The CXL PCIe 6.0 PHY IP market gains because these deployments require not just one component, but a chain of controllers, retimers, switches, and host interfaces around the same physical layer. General-purpose cloud servers and networking infrastructure should also contribute more over time as platform readiness improves. That makes the future demand mix broader than the present one, even if AI remains the main anchor. The segment’s growth profile suggests that memory architecture change is becoming one of the most important structural drivers in the CXL PCIe 6.0 PHY IP market. It also points to a more diversified customer base by the end of the forecast period. As adoption widens, vendors with strong support for both compute and memory-oriented designs should be in the best position.

Geography Analysis

North America held 43.27% of the CXL PCIe 6.0 PHY IP market share in 2025, which kept it in the leading regional position. The region benefits from a dense concentration of hyperscale cloud operators, accelerator developers, EDA vendors, and independent IP suppliers, most of which remain centered in the United States. That combination shortens the path from architecture selection to licensing, validation, and tapeout in the CXL PCIe 6.0 PHY IP market. Synopsys reported more than 100 PCIe 6.x implementations and more than 3,800 customer tapeouts across seven PCIe generations by 2025, which reflects the maturity of the regional design base. Europe remains important as both a development and end-use region, supported by established IP vendors and automotive compute activity, while Rambus has positioned a complete PCIe 6.0 interface subsystem with CXL 3.0 support for data center and AI SoCs.

Asia-Pacific is projected to grow at a 30.06% CAGR through 2031, which makes it the fastest-growing regional block in the CXL PCIe 6.0 PHY IP market size. Growth is supported by advanced foundry capacity, national AI infrastructure plans, and a stronger regional ecosystem around memory, switching, and validation tools. KIOXIA’s August 2025 prototype of a PCIe 6.0 flash memory module with 5 TB capacity and 64 GB/s bandwidth showed that regional demand extends beyond accelerator silicon into storage-class memory applications. Anritsu’s June 2026 launch of CXL 2.0 and 3.x evaluation solutions for 64 GT/s PAM4 links also showed that compliance infrastructure in Japan is evolving alongside device development. The CXL PCIe 6.0 PHY IP market in Asia-Pacific therefore benefits from both manufacturing depth and a broader supporting tool chain. This matters because buyers often prefer ecosystems where PHY design, packaging, memory innovation, and validation resources are available within the same regional supply network. The region is also well placed to benefit from future memory pooling deployments because of its strong position in semiconductors, storage, and server hardware. As a result, Asia-Pacific is likely to narrow the gap with North America even if it does not overtake it during the forecast period.

South America and Middle East and Africa still represent smaller shares of the CXL PCIe 6.0 PHY IP market, but both regions are linked to longer-term data center and sovereign cloud build-outs. Their current role is limited more by local semiconductor design depth than by end demand for AI and memory infrastructure. Middle East investment programs can still support indirect growth through accelerator procurement, design partnerships, and services linked to large AI infrastructure projects. South America remains earlier in the cycle, though expanding hyperscale presence and interest in domestic semiconductor capability could create a more meaningful pipeline over time. For the CXL PCIe 6.0 PHY IP market, these regions are better viewed as future diversification opportunities than as near-term revenue anchors.

Competitive Landscape

The CXL PCIe 6.0 PHY IP market has a top-heavy structure, with a small leading group holding the strongest position in proven PCIe 6.0 and CXL offerings, while a broader set of challengers competes in selected niches. Synopsys and Cadence Design Systems stand out because they combine controller IP, PHY IP, verification assets, and compliance support in a more complete stack than most rivals. That full-stack position matters in the CXL PCIe 6.0 PHY IP market because customers increasingly want a supplier that can reduce integration friction instead of just providing a fast circuit block. Synopsys strengthened that position by demonstrating live interoperability with Broadcom at PCI-SIG DevCon 2025 and by advancing its official Gold System role for pre-FYI compliance work. Cadence expanded its competitive reach in June 2025 through its broader Samsung Foundry IP agreement, which deepened node-specific relevance for advanced-chip customers. These moves show that the CXL PCIe 6.0 PHY IP market rewards suppliers that pair protocol support with foundry alignment and compliance execution.

Alphawave Semi has emerged as an important challenger in the CXL PCIe 6.0 PHY IP market by pushing multi-protocol connectivity and chiplet-oriented designs. Its AlphaCHIP1600-IO tapeout showed that the company can address PCIe 6.0, CXL 3.1, and 800G Ethernet within one I/O architecture, which is useful in systems where lane reuse and mixed protocol support matter. Alphawave also reported record FY2024 bookings of USD 515.5 million, which signals growing commercial traction even though its scale remains below the largest incumbents. Credo is taking a different route by extending its SerDes strength into adjacent connectivity roles, including advanced-node SerDes IP and retimer products aimed at AI data center links. This makes the CXL PCIe 6.0 PHY IP market competitive in more than one way, because challengers do not need to match the full incumbent stack if they can win in retimers, chiplets, or specialized high-speed subsystems.

White-space opportunity in the CXL PCIe 6.0 PHY IP market is still strongest in sub-3 nm porting, memory-centric controller PHY design, and deeper validation collateral for automotive and industrial use cases. These areas matter because many customers are less constrained by the lack of protocol definitions than by the lack of proven execution at their target node, package, or reliability standard. Rambus has responded to part of that need with a complete PCIe 6.0 interface subsystem for high-performance data center and AI SoCs, which shows that broader subsystem packaging remains a meaningful way to compete. Marvell’s Structera S platform also shows how the broader CXL ecosystem is expanding around shared-memory switching, which supports future demand for PHY vendors that can serve memory-centric fabrics. The competitive pattern therefore suggests a market with clear leaders, but not one that is closed to technically focused entrants. In the CXL PCIe 6.0 PHY IP market, foundry support, compliance readiness, and protocol reuse are becoming as important as analog performance alone. Vendors that can package these capabilities together should continue to hold the strongest pricing and design-win leverage.

CXL PCIe 6.0 PHY IP Industry Leaders

Synopsys Incorporated

Cadence Design Systems, Inc.

Rambus Inc.

Qualitas Semiconductor Co Ltd

Qualcomm Incorporated

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Microchip Technology released the XpressConnect PCIe 6.0 and CXL 3.1 retimer family on June 2, 2026, achieving pin-to-pin latency of less than 12 ns, approximately 80% lower than PCIe 6.0 specifications, to address signal integrity and latency constraints in large-scale AI GPU clusters at 64 GT/s. The family integrated with Microchip’s 3 nm Switchtec PCIe Gen 6 switches to deliver a pre-validated, interoperable fabric.

- June 2026: Marvell showcased the Structera S 30260, a PCIe 6.0 and CXL 3.x switch supporting 16 or 32 CPUs or GPUs across 260 lanes, up to 48 TB of shared memory, and 4 TB/second cumulative bandwidth at OFC 2026, with sampling to customers planned for Q3 2026. The product materially expanded the ecosystem for CXL 3.x-compatible PHY IP at 64 GT/s.

- June 2026: Anritsu launched CXL 2.0 and 3.x evaluation solutions for the BERTWave MP2110A-R, enabling high-precision physical-layer and protocol-level validation for 64 GT/s PAM4 CXL links. The launch reflected growing Japanese semiconductor investment in CXL-specific compliance infrastructure.

- February 2026: Credo Technology Group’s Toucan PCIe retimer, built on 7 nm TSMC process technology, achieved PCI-SIG compliance at 32.0 GT/s, validating interoperability and signal integrity across PCIe 5.0 platforms and enabling confident deployment in PCIe 6.0-capable systems ahead of full Gen 6 commercial host availability.

Global CXL PCIe 6.0 PHY IP Market Report Scope

The CXL PCIe 6.0 PHY IP Market refers to the industry segment focused on the design, licensing, and deployment of physical layer (PHY) intellectual property (IP) cores that enable high-speed data transmission over PCI Express (PCIe) 6.0 interfaces within Compute Express Link (CXL) ecosystems.

The CXL PCIe 6.0 PHY IP Market Report is Segmented by Offering (Standalone PCIe 6.0 / CXL 3.x PHY IP, Integrated PHY Subsystem IP, PHY Verification, Compliance, and Characterization Collateral, and PHY Porting, Integration, and Customization Services), Protocol (PCIe 6.0 PHY IP - PCIe-Only, PCIe 6.0 PHY IP with CXL 3.0 / CXL 3.1 Support, and Multi-Protocol 64 GT/s PHY IP), Process Node (3 Nm and Below, 4 Nm to 5 Nm, 6 Nm to 7 Nm, Nm to 16 Nm, and Above 16 Nm), IP Configuration (Single-Lane PHY IP, x4 PHY IP Subsystem, x8 PHY IP Subsystem, and x16 and Above PHY IP Subsystem), End Use (General-Purpose Data Center and Cloud Servers, AI Accelerators and HPC Systems, CXL Memory Expansion and Memory Pooling Infrastructure, Networking, Switching, DPUs, and Storage Infrastructure, Telecom and Edge Compute, Automotive and Industrial Compute, and Aerospace, Defense, and Other Specialized Compute), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Standalone PCIe 6.0 / CXL 3.x PHY IP |

| Integrated PHY Subsystem IP |

| PHY Verification, Compliance, and Characterization Collateral |

| PHY Porting, Integration, and Customization Services |

| PCIe 6.0 PHY IP - PCIe-Only |

| PCIe 6.0 PHY IP with CXL 3.0 / CXL 3.1 Support |

| Multi-Protocol 64 GT/s PHY IP |

| 3 Nm and Below |

| 4 Nm to 5 Nm |

| 6 Nm to 7 Nm |

| 8 Nm to 16 Nm |

| Above 16 Nm |

| Single-Lane PHY IP |

| x4 PHY IP Subsystem |

| x8 PHY IP Subsystem |

| x16 and Above PHY IP Subsystem |

| General-Purpose Data Center and Cloud Servers |

| AI Accelerators and HPC Systems |

| CXL Memory Expansion and Memory Pooling Infrastructure |

| Networking, Switching, DPUs, and Storage Infrastructure |

| Telecom and Edge Compute |

| Automotive and Industrial Compute |

| Aerospace, Defense, and Other Specialized Compute |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Southeast Asia | |

| Rest of Asia-Pacific | |

| South America | |

| Middle East and Africa |

| By Offering | Standalone PCIe 6.0 / CXL 3.x PHY IP | |

| Integrated PHY Subsystem IP | ||

| PHY Verification, Compliance, and Characterization Collateral | ||

| PHY Porting, Integration, and Customization Services | ||

| By Protocol Capability | PCIe 6.0 PHY IP - PCIe-Only | |

| PCIe 6.0 PHY IP with CXL 3.0 / CXL 3.1 Support | ||

| Multi-Protocol 64 GT/s PHY IP | ||

| By Process Node | 3 Nm and Below | |

| 4 Nm to 5 Nm | ||

| 6 Nm to 7 Nm | ||

| 8 Nm to 16 Nm | ||

| Above 16 Nm | ||

| By IP Configuration | Single-Lane PHY IP | |

| x4 PHY IP Subsystem | ||

| x8 PHY IP Subsystem | ||

| x16 and Above PHY IP Subsystem | ||

| By End Use | General-Purpose Data Center and Cloud Servers | |

| AI Accelerators and HPC Systems | ||

| CXL Memory Expansion and Memory Pooling Infrastructure | ||

| Networking, Switching, DPUs, and Storage Infrastructure | ||

| Telecom and Edge Compute | ||

| Automotive and Industrial Compute | ||

| Aerospace, Defense, and Other Specialized Compute | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Southeast Asia | ||

| Rest of Asia-Pacific | ||

| South America | ||

| Middle East and Africa | ||

Key Questions Answered in the Report

What is the 2026 size of the CXL PCIe 6.0 PHY IP space?

The CXL PCIe 6.0 PHY IP market size stands at USD 146.30 million in 2026 and is projected to reach USD 524.80 million by 2031 at a 29.11% CAGR.

What is driving adoption of PCIe 6.0 and CXL PHY IP in AI systems?

The main driver is the need for higher bandwidth and coherent memory access in AI accelerator clusters, where PCIe 6.0 and CXL share a 64 GT/s PAM4 physical layer.

Which offering category currently leads revenue?

Standalone PCIe 6.0 and CXL 3.x PHY IP led with 44.13% of revenue in 2025 because many SoC teams still prefer modular and controller-flexible designs.

Which end-use area is growing the fastest?

CXL memory expansion and memory pooling infrastructure is the fastest-growing end use, with a projected 30.42% CAGR through 2031.

Which region is currently the largest and which is expanding the fastest?

North America led with 43.27% share in 2025, while Asia-Pacific is projected to post the fastest growth at a 30.06% CAGR through 2031.

Why are integrated subsystem offerings gaining traction?

They reduce integration time and transfer more compliance and validation risk to the vendor, which is valuable for teams entering first-generation PCIe 6.0 and CXL programs.

Page last updated on: