CXL Memory Pooling and Disaggregated Infrastructure Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.39 Billion |

| Market Size (2031) | USD 5.42 Billion |

| Growth Rate (2026 - 2031) | 31.28% CAGR |

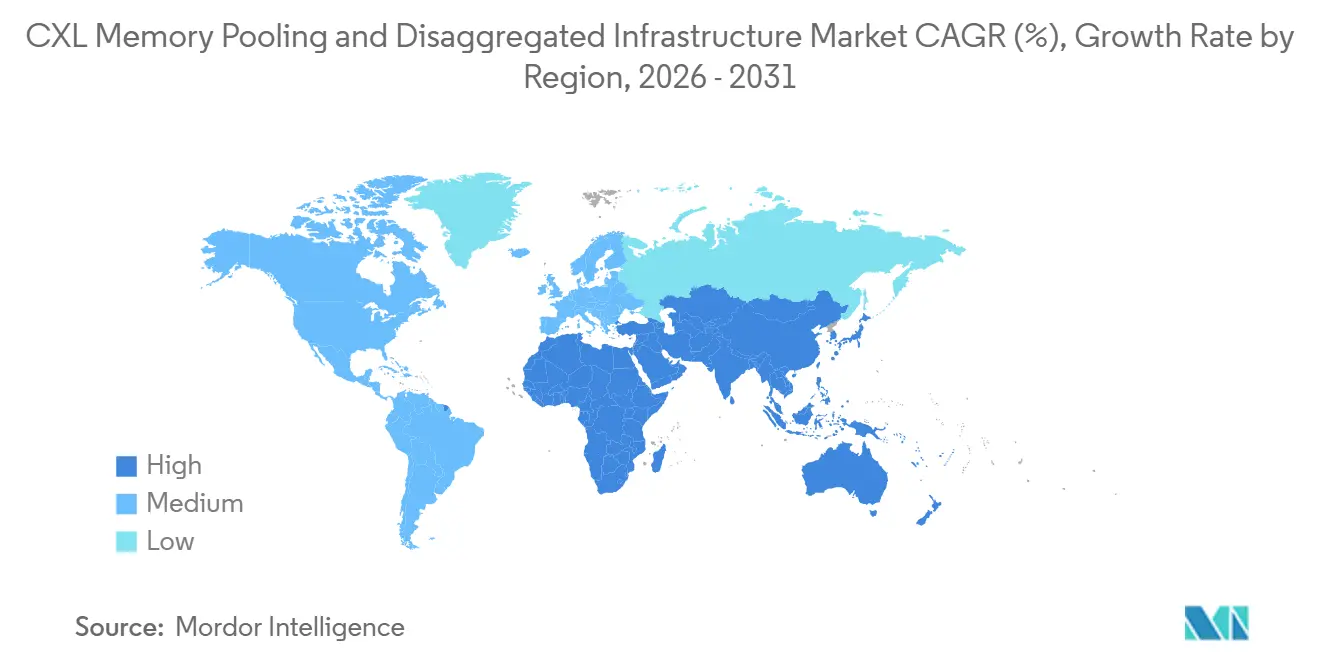

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

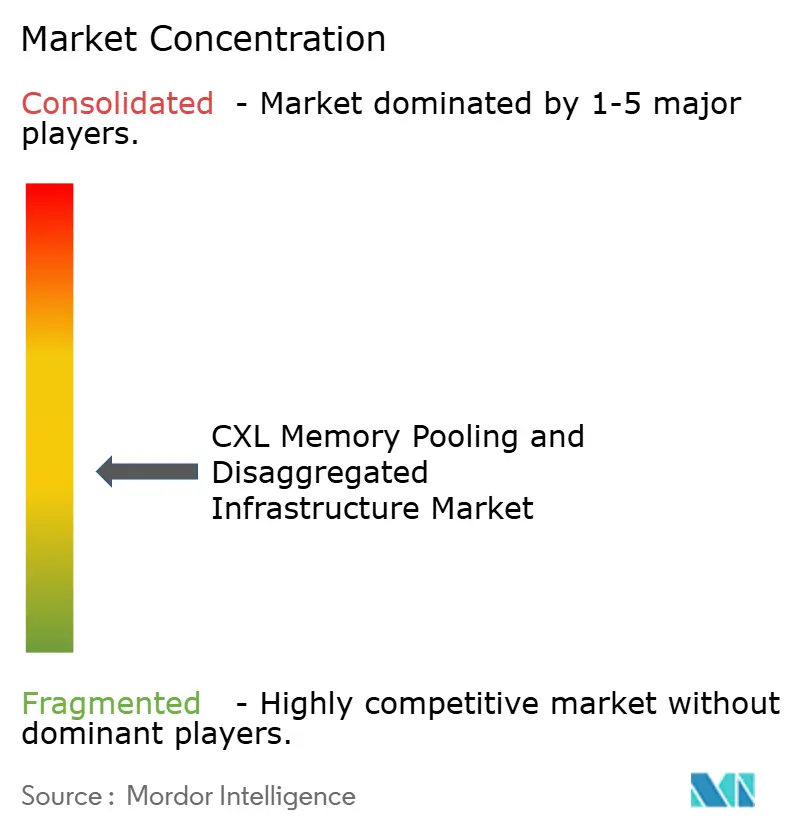

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

CXL Memory Pooling and Disaggregated Infrastructure Market Analysis by Mordor Intelligence

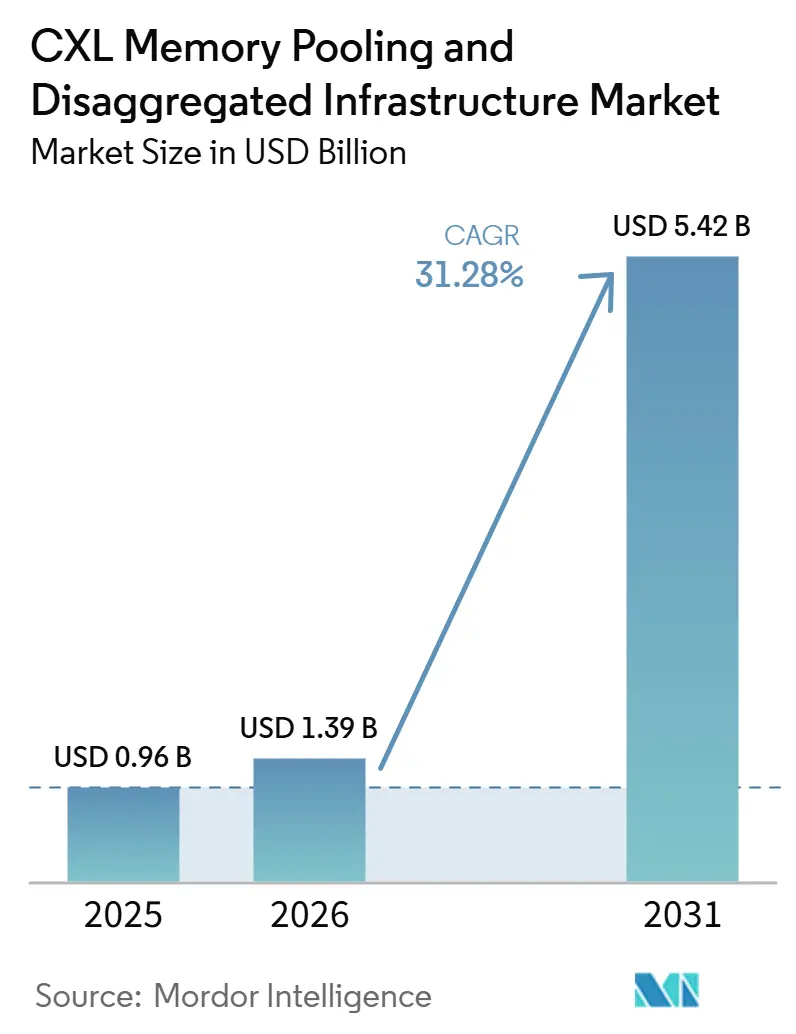

The CXL Memory Pooling and Disaggregated Infrastructure Market size is projected to be USD 0.96 billion in 2025, USD 1.39 billion in 2026, and reach USD 5.42 billion by 2031, growing at a CAGR of 31.28% from 2026 to 2031. The CXL Memory Pooling and Disaggregated Infrastructure Market is advancing as AI infrastructure faces a clear mismatch between rising accelerator density and the DRAM capacity available in conventional servers. CXL addresses that gap by providing CPUs, GPUs, and custom accelerators with memory-semantic access at far lower latency than NVMe-based methods, making shared and disaggregated memory commercially practical for large AI clusters. Competition is widening at the silicon, system, and software layers, as memory suppliers add controllers to modules and connectivity vendors move further into switching and orchestration. Near-term adoption still depends on the timing of next-generation server CPUs and on how quickly software licensing and chargeback models mature for shared-memory environments. The same CXL memory pooling and disaggregated infrastructure market is also opening a second demand layer beyond hyperscalers, as sovereign AI requirements, edge micro data centers, and DDR4 reuse strategies create space for smaller rack-scale deployments alongside sustainability-driven procurement.

Key Report Takeaways

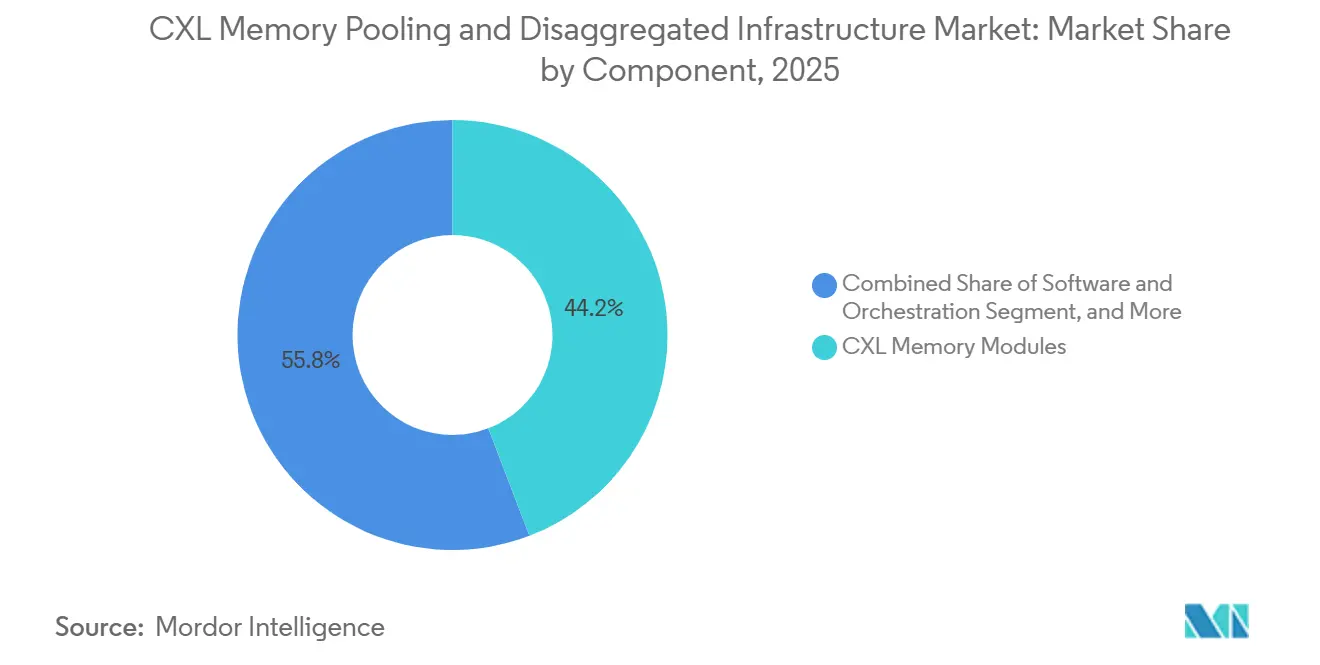

- By component, CXL Memory Modules led with a 44.17% share of CXL memory pooling and disaggregated infrastructure market in 2025, while CXL Switches are projected to expand at a 32.57% CAGR through 2031.

- By deployment architecture, Memory Expansion held 68.81% share of the CXL memory pooling and disaggregated infrastructure market in 2025, while Memory Pooling recorded the highest projected CAGR at 33.42% through 2031.

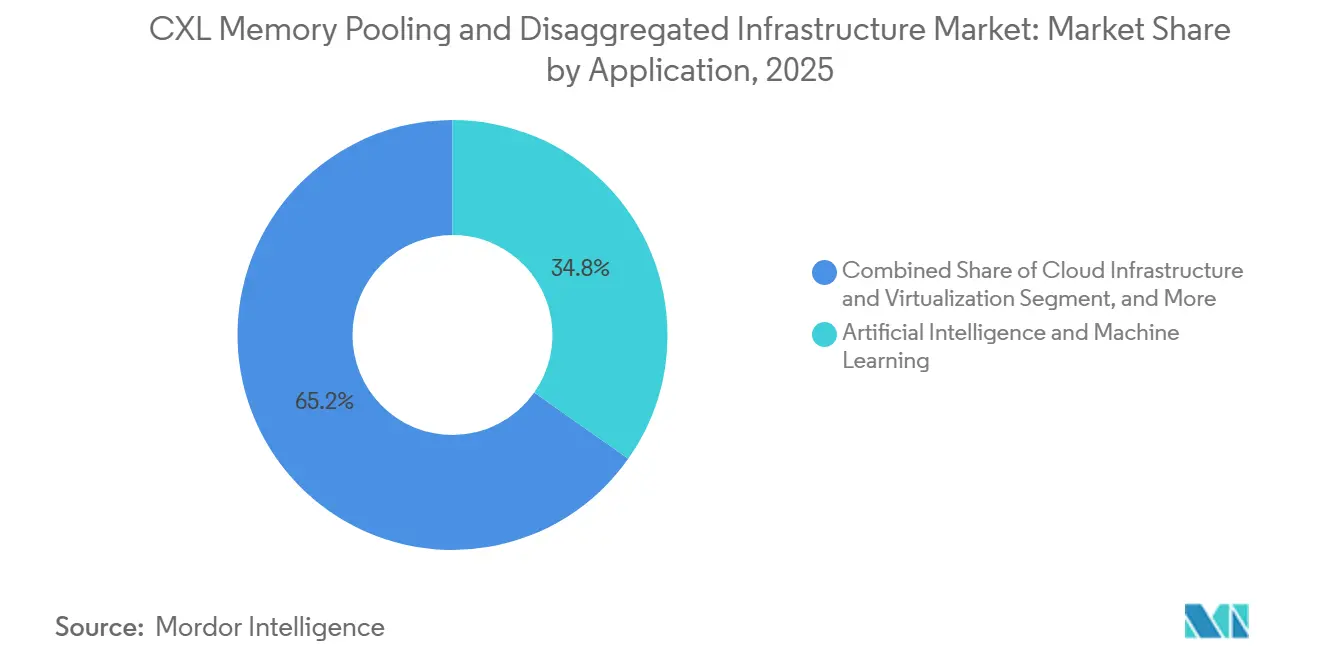

- By application, Artificial Intelligence and Machine Learning accounted for 34.77% share in 2025, while Cloud Infrastructure and Virtualization are projected to grow at a 31.78% CAGR through 2031.

- By geography, North America held 38.69% share in 2025, while Asia-Pacific is expected to record the fastest regional CAGR of 34.12% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global CXL Memory Pooling and Disaggregated Infrastructure Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AI Cluster Memory Wall Pressure | +8.5% | Global | Short term (≤ 2 years) |

| Hyperscale Shift to Composable Infrastructure | +7.2% | North America and Europe | Medium term (2-4 years) |

| Standardization of CXL 3.x and 4.0 Fabric Features | +5.8% | Global | Medium term (2-4 years) |

| Energy Efficiency and Rack Utilization Gains from Memory Pooling | +4.0% | Global, with early gains in North America and Asia-Pacific | Medium term (2-4 years) |

| Fabric-Level Telemetry and NUMA-Aware Software Orchestration | +2.5% | North America and Europe | Long term (≥ 4 years) |

| Procurement Preference for Shared Memory in Sovereign AI and Edge Micro Data Centers | +2.0% | Middle East and Africa, Europe, and Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

AI Cluster Memory Wall Pressure

The gap between accelerator throughput and on-server DRAM capacity is the strongest immediate force behind adoption in the CXL memory pooling and disaggregated infrastructure market. DDR5 server memory costs stood at USD 30-40 per GB in 2026, while AI workloads are doubling memory needs every 18 months, which made simple DIMM-based scaling expensive for hyperscalers and enterprise AI operators alike. Shared CXL pools let KV cache demand extend beyond local DRAM at near-DRAM latency, helping avoid GPU underuse and reducing inference cost per token. This pressure is especially visible in inference systems, where token economics depend heavily on memory efficiency rather than on raw training throughput alone. Penguin Solutions launched the first production-ready CXL-based KV cache server in March 2026, with up to 11 TB of CXL-based memory and 10x faster speeds than NVMe-based approaches, demonstrating that commercial deployments had moved beyond the pilot stage.

Hyperscale Shift to Composable Infrastructure

Hyperscalers are restructuring data center procurement around composable pools where memory, compute, and accelerators can be provisioned independently and moved as workloads change. That shift is tied to GPU utilization economics and rack-density limits, pushing the CXL memory pooling and disaggregated infrastructure market toward rack-scale designs rather than server-bound memory expansion alone. This change raises demand for switching fabrics that can make shared memory a standard rack component rather than a niche attachment. Astera Labs said its Scorpio X-Series 320-lane Smart Fabric Switch entered the production ramp in H2 2026 and cuts AllReduce latency by at least 50%, providing operators with a practical path toward larger pooled deployments.[1]Astera Labs, Inc., “Astera Labs Extends Leadership in Open, AI Scale-Up Networking With New 320 Lane Scorpio X-Series Smart Fabric Switch,” Astera Labs, asteralabs.com As these fabrics become more common in AI racks, the marginal cost of adding disaggregated memory tiers falls, making the software case for dynamic memory allocation easier to justify.

Standardization of CXL 3.x and 4.0 Fabric Features

Protocol standardization is turning technical feasibility into a broader commercial opportunity for the CXL memory pooling and disaggregated infrastructure market. The CXL 4.0 specification was released in November 2025 and doubled bandwidth to 128 GT/s with no added latency, aligned the physical layer with PCIe 7.0, and added bundled port capabilities and stronger memory RAS features. Those RAS and security features matter because shared memory across cloud and enterprise security domains requires a stronger reliability and compliance base than earlier versions offered. Full backward compatibility across prior CXL versions lowers replacement risk for infrastructure operators and supports phased deployment across mixed hardware estates. By 2025, the ecosystem had expanded to more than 190 vendors, widening interoperability pathways and shortening qualification timelines for OEMs and buyers across the supply chain. This makes standardization a commercial gate for multi-tenant and multi-vendor deployments, rather than just a technical upgrade cycle.

Energy Efficiency and Rack Utilization Gains from Memory Pooling

Memory overprovisioning remains a major source of waste in AI data centers, and CXL pooling addresses that problem by replacing stranded per-server DRAM with memory that can be allocated across workloads as needed. Simulations indicated that CXL memory pooling can cut memory power consumption by 20-30% and improve memory utilization by up to 50%, which strengthens the efficiency case for the CXL memory pooling and disaggregated infrastructure market beyond simple capacity expansion. The same model also changes life-cycle economics, as older DDR4 can be reused as a CXL-attached expansion rather than being retired when servers move to DDR5 platforms. Marvell said this reuse path could help avoid up to 66 billion kilograms of CO2 emissions and 36,376 US tons of e-waste, which gave procurement teams a clearer sustainability argument alongside cost savings. As enterprises tie infrastructure purchases more closely to power use and carbon outcomes, energy efficiency is becoming a practical buying factor for the CXL memory pooling and disaggregated infrastructure market rather than a secondary benefit.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Interoperability Gaps Across CXL Generations and Vendor Stacks | -3.5% | Global | Short term (≤ 2 years) |

| Limited Volume Availability of Production-Qualified CXL Type 3 and Switch Ecosystems | -2.8% | Global | Short term (≤ 2 years) |

| Software Licensing Friction in Pay-Per-Use Disaggregated Models | -1.5% | North America and Europe | Medium term (2-4 years) |

| Memory Latency Sensitivity in Production AI and HPC Workloads | -1.2% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Interoperability Gaps Across CXL Generations and Vendor Stacks

Interoperability remains a real brake on procurement even as standardization improves. Research showed that the CXL cache-coherence protocol still lacks mechanisms to guarantee safe interoperability across heterogeneous host architectures with different memory consistency models, forcing platform-device qualification on a pair-by-pair basis. That raises engineering cost for buyers who want multi-vendor pools and do not have the internal validation capacity of hyperscalers. The issue is sharper at the fabric layer, where switch implementations are still maturing and where production-ready topologies are not yet fully uniform across vendors. As a result, the CXL memory pooling and disaggregated infrastructure market is progressing fastest, where buyers can control hardware combinations closely and absorb longer qualification cycles.

Limited Volume Availability of Production-Qualified CXL Type 3 and Switch Ecosystems

Supply-side readiness is still limiting how quickly demand can convert into revenue. Samsung delayed mass production of CXL 3.1-based CMM-D modules to 2027, while Intel Diamond Rapids is not expected until Q2-Q3 2027, and AMD EPYC Venice is targeted for H2 2026, indicating that next-stage pooling depends heavily on the processor roadmap and memory supplier readiness. SK hynix and Micron had advanced their CXL 3.1 work to the R&D stage, but the broad production-readiness base was still not in place, confirming that the bottleneck was ecosystem-wide rather than vendor-specific. Operating system and hypervisor support also remains uneven, with Linux support improving sooner than some proprietary environments, which keeps part of the enterprise base on the sidelines for now. This shifts a share of expected CXL memory pooling and disaggregated infrastructure market revenue from 2026 and 2027 into the later years of the forecast period rather than preventing adoption altogether.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Modules Lead While Switches Define the Next Architecture Upgrade Cycle

CXL Switches are the fastest-growing component in the CXL memory pooling and disaggregated infrastructure markett, with a 32.57% CAGR through 2031, as architecture moves from single-server expansion toward rack-level shared memory fabrics. Marvell announced the Structera S 30260, a 260-lane CXL 3.0 switch developed through the XConn Technologies acquisition, and said sampling would begin in Q3 2026, making it the first switch purpose-built for AI rack-scale memory pooling. The switch ramp is closely tied to CPU platform readiness because multi-host fabric features require newer processor generations, which are arriving through 2026 and 2027. That keeps near-term switch volumes modest even as the CXL memory industry positions this category for stronger revenue concentration later in the forecast period.

CXL Memory Modules commanded 44.17% share of the CXL memory pooling and disaggregated infrastructure market size in 2025, supported by Type 3 memory expander adoption on CXL 2.0-capable server platforms. Samsung’s July 2026 evaluation showed that CXL memory maintained 92% of DRAM performance in 8-GPU configurations while delivering much larger capacity, which is influencing hyperscaler qualification work for AI servers. SK hynix completed customer validation of its 96 GB CMM-DDR5 module in April 2025, delivering a 50% capacity increase and a 30% bandwidth improvement to 36 GB/s over DDR5, while a 128 GB version remained under validation. Controllers are drawing more competition as Montage Technology’s CXL 3.1 Memory eXpander Controller gained support from AMD and Intel, while orchestration software remains smaller today but is likely to become a recurring revenue layer as pay-per-use memory pools mature.

By Deployment Architecture: Expansion Dominates but Pooling Sets the Strategic Direction

Memory Expansion held 68.81% of the CXL memory pooling and disaggregated infrastructure market share in 2025 because CXL 1.1 and 2.0 deployments are simpler and connect the host CPU directly to Type 3 memory devices, eliminating the need for a switch fabric. Intel’s 5th Gen Xeon platform delivered CXL Type 3 support, while AMD EPYC Turin supports CXL 2.x, and that installed server base is where most current expansion deployments are concentrated. This architecture continues to generate the largest absolute revenue because production-qualified CXL 2.0 modules are more available than newer pooled configurations. Even within this mature segment, usage is shifting from basic capacity expansion toward second-tier placement for latency-tolerant data, indicating that the CXL memory pooling and disaggregated infrastructure market is already changing how expansion is used.

Memory Pooling is the fastest-growing deployment architecture, with a 33.42% CAGR through 2031, as CXL 3.x switching moves toward commercial production. Microsoft Research demonstrated at NSDI 2026 that sparse CXL pod topologies achieved communication latency 3.2x lower than in-rack RDMA, strengthening the economic case for switched pooling in hyperscale environments.[2]Microsoft Research, “Octopus, Enhancing CXL Memory Pods via Sparse Topology,” NSDI, microsoft.com The business model is also shifting from capital spent per server to utilization-based memory allocation, creating room for orchestration vendors to monetize pooled memory as a service layer on top of standard hardware. Other deployment models, including tiered memory and service-oriented configurations, remain early and will depend on how software control, billing, and platform support develop over time.

By Application: AI and ML Anchor Near-Term Revenue While Cloud Virtualization Accelerates

Artificial Intelligence and Machine Learning held a 34.77% share in 2025, making it the largest application segment in the CXL memory pooling and disaggregated infrastructure market, as LLM inference depends heavily on KV cache capacity. Samsung’s July 2026 evaluation showed stable CXL memory behavior when KV cache demand exceeded local DRAM capacity in multi-GPU settings, supporting its use in production inference environments. This matters because memory capacity, rather than compute throughput alone, often becomes the rate-limiting factor in large inference systems. Agentic AI workloads with changing context window sizes are also likely to increase memory demand faster than static LLM deployments, which supports a wider use case for pooled CXL memory over time.

Cloud Infrastructure and virtualization are projected to grow at a 31.78% CAGR through 2031, which makes it the fastest-growing application in the CXL memory pooling and disaggregated infrastructure market. Astera Labs said Microsoft Azure’s CXL memory preview used Leo CXL Smart Memory Controllers on M-Series virtual machines, indicating that public cloud deployment had entered a commercially visible stage. In-memory databases and real-time analytics also remain important, as peer-reviewed testing found that CXL memory with weighted interleaving reduced loaded latency during database scans. High-performance computing needs more selective deployment because current CXL devices produced 2-6x latency slowdowns on bandwidth-sensitive workloads, which makes NUMA-aware data placement a software requirement rather than a hardware-only fix.

Geography Analysis

North America held a 38.69% share in 2025, making it the largest regional market for CXL memory pooling and disaggregated infrastructure industry. That lead reflected capital spending by AWS, Microsoft Azure, Google Cloud, and Meta, all of which were early backers of the CXL ecosystem and are already moving into production deployment. Astera Labs said its Leo CXL Smart Memory Controllers were validated on Microsoft Azure M-Series virtual machines in 2025, marking a clear step from pilot work toward production-ready public cloud infrastructure. Meta’s Vistara project showed that older DDR4 DIMMs from retired servers can be repurposed alongside DDR5 production systems via CXL, reducing memory costs and supporting a lower carbon footprint in hyperscale environments. Demand in the region is also supported by regulated sectors seeking on-premises AI inference capacity for data sovereignty and compliance purposes.

Asia-Pacific is projected to expand at a 34.12% CAGR through 2031, which makes it the fastest-growing geography in the CXL memory pooling and disaggregated infrastructure market. The region benefits from the supply-side concentration of memory manufacturers and ODM capacity in South Korea and Taiwan, while large data center investments are also expanding across China, Japan, South Korea, India, and Australia. Samsung said in July 2026 that it was treating CXL as its next major memory priority, with AMD EPYC Venice-based sample validation planned after September 2026 and commercial production targeted for Q1 2027. SK hynix also demonstrated CMM-DDR5 at CFMS 2026 and is developing its own controllers for CXL 3.0 and 3.1 devices, which supports a stronger regional supply chain position. India’s public support for data center growth and Japan’s national AI computing efforts suggest that regional demand is building alongside manufacturing strength rather than trailing it.

Europe maintained a meaningful share in 2025, as sovereign AI goals and data residency rules favored on-premises disaggregated memory deployment in enterprise and public sector environments. The EU-backed CAPE project is integrating PCIe Gen 5 and Gen 6 fabric with CXL support for dynamic memory pooling in edge micro data centers, which shows how sovereign compute programs are creating non-hyperscale adoption paths.[3]CAPE Project, “CAPE Update #5, EMDC, Edge Micro Data Center,” CAPE Project, cape-project.eu South America and the Middle East and Africa remain smaller today, but government-backed sovereign AI programs and colocation expansion are creating a future demand path that fits rack-scale and edge-oriented CXL deployment models. This means the CXL memory pooling and disaggregated infrastructure market is likely to develop a broader edge layer outside the hyperscale footprint over the latter part of the forecast period.

Competitive Landscape

The CXL memory pooling and disaggregated infrastructure market remains moderately fragmented at the overall component level, although switching silicon is showing clearer signs of concentration. Marvell’s 2025 acquisition of XConn Technologies gave it a combined base in PCIe 6.0 and CXL 3.0 switching, and the company used that platform in March 2026 to release pin-compatible PCIe and CXL switch designs that reduce customer hardware development work. That move matters because rack-scale pooling depends on a smaller set of fabric specialists than the broader module and controller layers do. Marvell has also used hardware-based inline memory compression in its Structera platform, which can raise effective DRAM capacity without software CPU involvement and creates a harder-to-copy silicon advantage. As a result, the most concentrated part of the competitive field is not the module layer, but the switching and fabric control layer that enables pooled architectures.

Memory IDMs such as Samsung, SK hynix, and Micron are competing on module capacity, bandwidth, and controller integration while also validating products with server OEMs. That closes some of the open space for smaller pure-play module vendors because buyers increasingly want validated bundles rather than isolated parts. The software layer is less crowded, and it remains one of the few parts of the CXL memory pooling and disaggregated infrastructure market where recurring revenue could scale meaningfully as allocation, telemetry, and billing become more important. Panmnesia presented a silicon-proven unified CXL controller and a port-based routing switch at ISCA 2026, which showed that the controller and switching layer is still open to technically capable new entrants even as scale requirements rise. Server OEMs are also moving from passive adoption to active co-design, which should broaden enterprise distribution while reducing the differentiation window for independent hardware vendors.

Astera Labs strengthened its position in 2026 by moving the Scorpio X-Series Smart Fabric Switch into production ramp, which added another specialized scale-up fabric option for hyperscale and AI deployments. Montage Technology also widened the controller field when its CXL 3.1 Memory eXpander Controller gained endorsements from AMD and Intel, which helped validate third-party controller supply outside IDM in-house approaches.[4]Montage Technology, “Montage Technology Introduces CXL 3.1 Memory eXpander Controller to Empower Next-Generation Data Center Infrastructure,” Business Wire, businesswire.com These moves show that the market is not controlled by a single vendor group, even though a smaller set of firms is building stronger influence in switch silicon and platform validation. Competitive position in the CXL memory pooling and disaggregated infrastructure market still depends as much on ecosystem timing and interoperability readiness as it does on product performance alone.

CXL Memory Pooling and Disaggregated Infrastructure Industry Leaders

Marvell Technology, Inc.

Astera Labs, Inc.

Samsung Electronics Co., Ltd.

Micron Technology, Inc.

SK Hynix Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Astera Labs announced the Scorpio X-Series 320-lane Smart Fabric Switch, the industry's largest open memory-semantic fabric switch, reducing AllReduce latency by at least 50%, with production ramp in H2 2026 targeting a merchant scale-up switch silicon market projected at USD 20 billion by 2030.

- March 2026: Marvell Technology announced the Structera S 30260, a 260-lane CXL 3.0 switch built on XConn Technologies IP at OFC 2026, with sampling beginning Q3 2026, the device is the first CXL switch purpose-built for rack-level AI memory pooling and is pin-compatible with Marvell's PCIe 6.0 switch, reducing customer development costs.

- March 2026: Penguin Solutions launched the industry's first production-ready CXL-based KV cache server, delivering up to 11 TB of CXL-based memory at speeds 10x faster than NVMe-based approaches, directly addressing LLM inference memory bottlenecks and offering a new tier of cluster memory supplementing HBM and system DRAM.

- November 2025: The CXL Consortium released CXL 4.0, doubling bandwidth to 128 GT/s with zero added latency, introducing bundled port capabilities and memory RAS enhancements, and aligning with the PCIe 7.0 physical layer while maintaining full backward compatibility from CXL 1.0 onward.

Global CXL Memory Pooling and Disaggregated Infrastructure Market Report Scope

The CXL Memory Pooling and Disaggregated Infrastructure Market refers to the market for compute express link (CXL)-enabled solutions that allow organizations to pool, share, and dynamically allocate memory resources across servers and infrastructure environments. The market scope includes CXL-based memory pooling hardware, software, controllers, switches, and related infrastructure solutions used in data centers, cloud environments, high-performance computing, artificial intelligence, and enterprise workloads.

The CXL Memory Pooling and Disaggregated Infrastructure Market Report is Segmented by Component (CXL Memory Modules, CXL Controllers, CXL Switches, and Software and Orchestration), Deployment Architecture (Memory Expansion, Memory Pooling, and Other Deployment Architectures), Application (Artificial Intelligence and Machine Learning, In-Memory Databases and Real-Time Analytics, High-Performance Computing and Scientific Computing, Cloud Infrastructure and Virtualization, and Other Applications), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| CXL Memory Modules |

| CXL Controllers |

| CXL Switches |

| Software and Orchestration |

| Memory Expansion |

| Memory Pooling |

| Other Deployment Architectures |

| Artificial Intelligence and Machine Learning |

| In-Memory Databases and Real-Time Analytics |

| High-Performance Computing and Scientific Computing |

| Cloud Infrastructure and Virtualization |

| Other Applications |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| Taiwan | |

| India | |

| Rest of Asia-Pacific | |

| South America | |

| Middle East and Africa |

| By Component | CXL Memory Modules | |

| CXL Controllers | ||

| CXL Switches | ||

| Software and Orchestration | ||

| By Deployment Architecture | Memory Expansion | |

| Memory Pooling | ||

| Other Deployment Architectures | ||

| By Application | Artificial Intelligence and Machine Learning | |

| In-Memory Databases and Real-Time Analytics | ||

| High-Performance Computing and Scientific Computing | ||

| Cloud Infrastructure and Virtualization | ||

| Other Applications | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| Taiwan | ||

| India | ||

| Rest of Asia-Pacific | ||

| South America | ||

| Middle East and Africa | ||

Key Questions Answered in the Report

What is the current and forecast value of the CXL Memory Pooling and Disaggregated Infrastructure Market?

The CXL Memory Pooling and Disaggregated Infrastructure Market was valued at USD 0.96 billion in 2025, stands at USD 1.39 billion in 2026, and is forecast to reach USD 5.42 billion by 2031.

What is driving the adoption of CXL memory in AI infrastructure?

The main driver is the memory gap between fast accelerators and limited server DRAM. CXL helps serve overflow memory needs at much lower latency than NVMe-based alternatives.

Which application leads to demand for CXL memory solutions?

Artificial Intelligence and Machine Learning led with 34.77% share in 2025 because LLM inference and KV cache workloads depend heavily on memory capacity.

Which deployment model is growing fast for CXL-based memory?

Memory Pooling is the fastest-growing deployment architecture, with a 33.42% CAGR through 2031, as shared rack-level memory fabrics become more practical.

Which region is leading and which one is growing fastest?

North America led with 38.69% share in 2025, while Asia-Pacific is projected to grow fastest at a 34.12% CAGR through 2031.

Why are switches becoming so important in this space?

Switches are enabling the move from simple memory expansion to multi-host pooled memory. That is why CXL Switches are projected to grow at a 32.57% CAGR through 2031.

Page last updated on: