CXL Memory Module Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

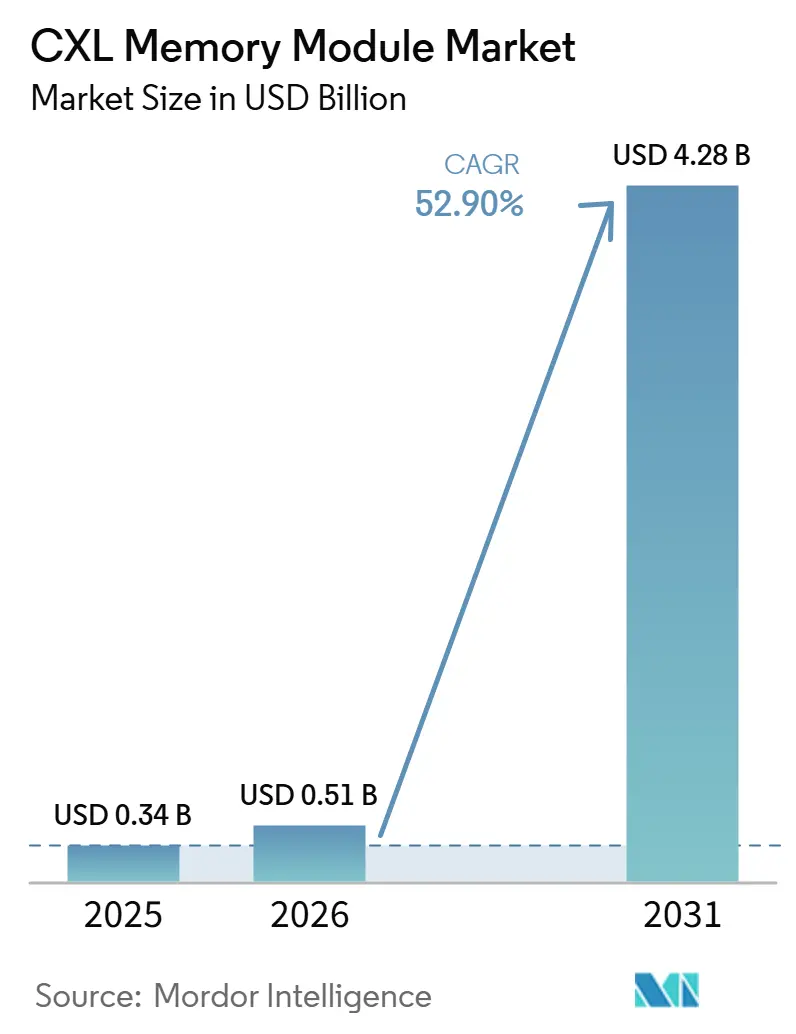

| Market Size (2026) | USD 0.51 Billion |

| Market Size (2031) | USD 4.28 Billion |

| Growth Rate (2026 - 2031) | 52.90% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

CXL Memory Module Market Analysis by Mordor Intelligence

The CXL memory module market size is projected to be USD 0.34 billion in 2025, USD 0.51 billion in 2026, and reach USD 4.28 billion by 2031, growing at a CAGR of 52.90% from 2026 to 2031. The CXL memory module market is entering a commercial phase, as hyperscale qualification work completed in earlier cycles is now supporting broader procurement and deployment decisions. Demand is rising as artificial intelligence inference, large in-memory databases, and dense virtualized workloads keep pushing server memory needs beyond what socket-bound DDR5 layouts can support on their own. The CXL memory module market is also benefiting from the fact that memory expansion, pooling, and tiering are being treated as architectural tools rather than optional add-ons, which changes how operators plan rack design and server utilization. Competition is centered on large memory suppliers that control module production and on controller companies that compete on interoperability, bandwidth efficiency, and effective capacity gains. The near-term pace of the CXL memory module market still depends on software maturity, platform costs, and workload-level latency management, but those barriers are weakening as the ecosystem becomes more standardized and operationally proven.

Key Report Takeaways

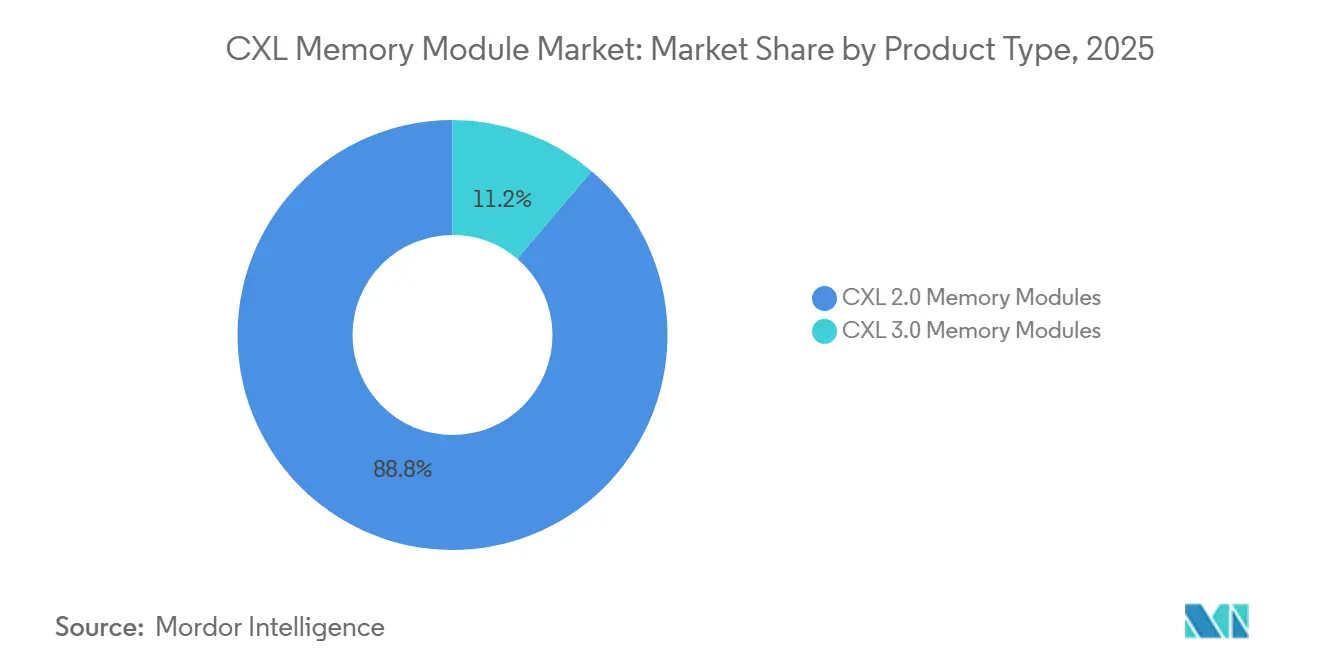

- By product type, CXL 2.0 memory modules held 88.79% share of the CXL memory module market size in 2025, while CXL 3.0 modules are projected to expand at a 53.29% CAGR through 2031.

- By memory technology, DRAM-based CXL modules accounted for 92.14% of segment revenue in 2025, while SCM and persistent memory-based modules are projected to grow at a 53.47% CAGR through 2031.

- By form factor, add-in card modules held 63.42% of the segment share in 2025, while E3.S modules are projected to advance at a 53.41% CAGR through 2031.

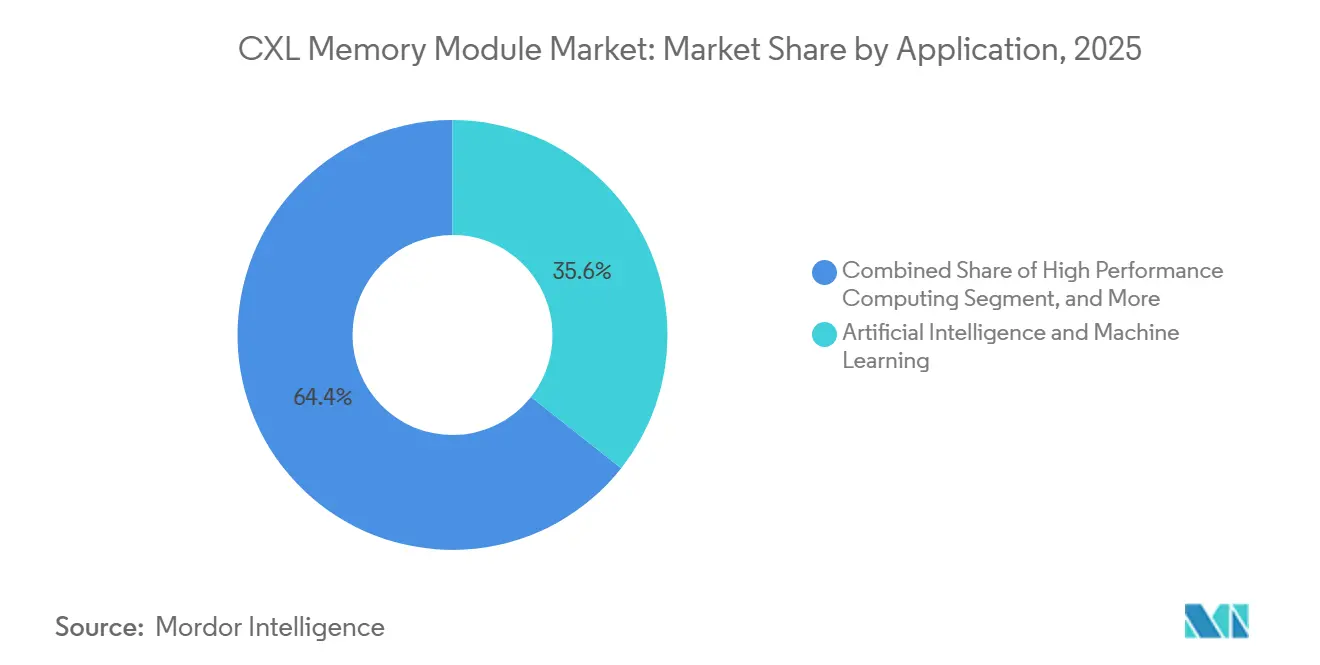

- By application, artificial intelligence and machine learning accounted for 35.64% of segment demand in 2025, while virtualization and cloud are projected to expand at a 53.82% CAGR through 2031.

- By end user, hyperscale data centers held 49.17% of the segment share in 2025, while cloud service providers are projected to record the fastest CAGR at 54.09% through 2031.

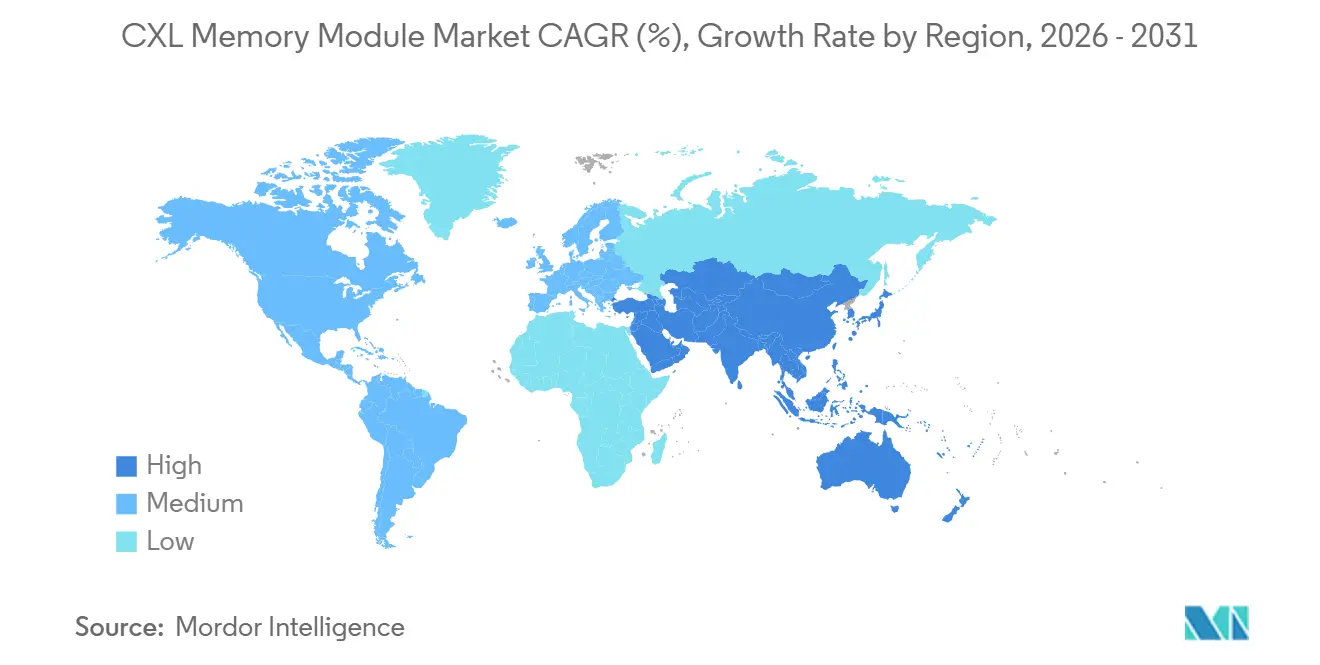

- By geography, North America accounted for 45.37% of revenue in 2025, while Asia-Pacific is projected to grow at a 53.78% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global CXL Memory Module Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising AI Server Memory Density Requirements | +10.2% | Global, concentrated in North America and Asia-Pacific | Short term (≤ 2 years) |

| Shift from DDR-Only Capacity Scaling to CXL Pooling | +9.5% | North America and Asia-Pacific core, spill-over to Europe | Medium term (2-4 years) |

| Rapid Commercialization of CXL 2.0 and CXL 3.0 Ecosystems | +8.8% | Global, with South Korea, Taiwan, and USA as primary hubs | Short term (≤ 2 years) |

| Hyperscale Data Center Demand for Composable Memory Architectures | +7.6% | North America and Asia-Pacific | Medium term (2-4 years) |

| Power and Rack Footprint Pressure from Conventional Overprovisioning | +5.3% | Global, compliance intensity concentrated in Europe and North America | Medium term (2-4 years) |

| Software-Defined Memory Tiering and Orchestration Readiness | +4.2% | North America and Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising AI Server Memory Density Requirements

The CXL memory module market is being driven by the rapid increase in memory demand from artificial intelligence servers, especially for large language model inference and retrieval-heavy workloads. Modern inference environments require large, low-latency memory pools for activation storage and KV cache, and many dual-socket server designs cannot meet those needs solely through DIMM slots. Research published in 2026 showed that pooled CXL memory in SGLang inference clusters delivered performance close to local DRAM for conditional memory retrieval and demonstrated stronger performance than RDMA on sparse access patterns that matter for recommendation and retrieval-augmented generation tasks. This makes the CXL memory module market relevant not only for performance expansion but also for cost control, as operators can add memory headroom without multiplying the accelerator count across every node. The CXL memory module market is therefore gaining support from cloud platforms and inference providers that want more memory density per server before they buy more GPU systems. Microsoft Azure validated that direction in November 2025 when it previewed CXL-backed M-series virtual machines using Astera Labs controllers for memory-intensive enterprise workloads.

Shift from DDR-Only Capacity Scaling to CXL Pooling

The CXL memory module market is also expanding because the older path of scaling memory only through denser DIMMs or more servers becomes increasingly expensive when workloads move into multi-terabyte territory. Samsung stated that its CMM-D 2.0 design delivered 36 GB/s of bandwidth across 128 GB and 256 GB capacities, giving operators a way to attach more memory via PCIe slots on existing server platforms. That path matters because the CXL memory module market addresses stranded capacity, a persistent inefficiency in data centers where a meaningful share of installed memory remains underused at any given time, as research in 2026 described.[1]Daniel S. Berger et al., “CXL in Cloud Practice: Practical Lessons for Incrementally Scaling Deployment,” IEEE Transactions on Computers, pages.cs.wisc.edu Memory pooling changes the operating model by letting administrators match hot and cold memory placement more closely to workload behavior, rather than locking capacity inside each server. The CXL memory module market benefits because that model supports higher utilization, lower overprovisioning, and better scaling discipline across larger fleets. As more operators prioritize total cost of ownership over raw server counts, pooled memory becomes easier to justify as part of a broader infrastructure refresh cycle.

Rapid Commercialization of CXL 2.0 and CXL 3.0 Ecosystems

The CXL memory module market is gaining momentum as the vendor ecosystem moved quickly from lab readiness to commercial validation during 2025 and 2026. Samsung completed CXL 2.0 compliance work, and SK hynix completed customer certification of its CMM-DDR5 96 GB CXL 2.0 product in April 2025, showing that supply-side readiness is no longer limited to roadmap messaging. At the controller level, Marvell announced in April 2025 that its Structera CXL portfolio interoperates successfully with AMD EPYC and 5th Gen Intel Xeon Scalable platforms, removing a major validation concern for enterprise buyers. The CXL memory module market is also benefiting from switch development, because shared memory architectures require more than endpoint readiness to scale across racks. Marvell stated in March 2026 that its next-generation CXL switch supports up to 48 TB of shared memory and 4 TB/s aggregate bandwidth per rack, which directly strengthens the commercial case for larger fabric-based deployments. As more products reach compliance and interoperability milestones, the CXL memory module market becomes easier for OEMs, cloud operators, and enterprise buyers to qualify without taking a single vendor risk.

Hyperscale Data Center Demand for Composable Memory Architectures

The CXL memory module market is supported by hyperscale demand for composable memory, in which capacity is dynamically allocated across compute resources rather than fixed within each server. Research presented in 2026 showed that CXL-based memory pods with sparse topologies supported memory pooling and low-latency inter-server communication, with only a 3% increase in per-server power use compared to switch-based alternatives. Marvell stated that its Structera S 30260 switch reduced latency by 72% compared with RDMA-based memory pooling, directly addressing one of the main objections hyperscalers have raised about shared memory performance at scale. The Open Compute Project also published a logical system architecture for composable memory services, providing buyers with a standards-based framework for framing fabric management and interoperability requirements in procurement programs. The CXL memory module market benefits from this shift because composable memory ceases being a bespoke engineering concept and becomes a repeatable infrastructure layer. Once operators can recover stranded capacity, simplify memory sharing, and tie these benefits to rack economics, the CXL memory module market becomes relevant to a much broader set of deployment decisions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Latency Gap Versus On-Socket DDR5 Memory | -2.8% | Global | Short term (≤ 2 years) |

| High Upfront Cost of CXL-Capable Servers and Modules | -2.1% | Global, most acute in South America, Middle East and Africa, and enterprise segment in Europe | Medium term (2-4 years) |

| Ecosystem Interoperability and Validation Complexity | -1.5% | Global | Medium term (2-4 years) |

| Immature Software Stack for Memory Management and Tiering | -1.0% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Latency Gap Versus On-Socket DDR5 Memory

The CXL memory module market still faces resistance because expanded memory does not match the latency of local DDR5 across all workloads. Research in 2026 found that CXL 2.0 expansion devices on Intel Xeon 6 platforms delivered nominal access latencies of 100 ns to 160 ns, compared with 75 ns for local DDR5, and the resulting slowdown was usually 10% to 18% for tuned applications but could reach 45% in pointer chasing cases at much higher latency levels. That finding matters because it shows the penalty is workload-specific rather than uniform across the CXL memory module market. The same research also showed that the CXL interconnect itself was not the main source of delay, because CPU-side NUMA arbitration and refresh behavior contributed much of the observed overhead. This means deployment success depends on carefully profiling applications and then placing hot and cold data on the right tiers, rather than assuming one memory behavior fits every use case. Meta aligned with that direction in 2026 through its Equilibria framework for fair multi-tenant CXL memory tiering, which reported end-to-end performance gains of up to 52% in production-style workloads.

High Upfront Cost of CXL-Capable Servers and Modules

The CXL memory module market also faces a capital cost hurdle because early deployments depend on new host platforms rather than simple retrofits of older server generations. Buyers need compatible Intel Xeon 6 or later AMD EPYC platforms to deploy at scale, so many organizations see CXL adoption as part of a broader server replacement cycle rather than an isolated memory purchase. That raises the threshold for enterprise accounts, where refresh periods are longer, and memory economics are reviewed over several years rather than a single deployment phase. Marvell argued in 2026 that inline hardware compression on Structera X and A controllers can increase effective DRAM capacity utilization by up to 3.64x without CPU overhead, thereby improving the return on investment for CXL-attached memory when data sets are compressible.[2]Marvell Technology, “Structera X and A CXL Compression: Making Every Gigabyte Count,” Marvell Technology, marvell.com The CXL memory module market still needs more standardized total cost of ownership frameworks because buyers compare module price, controller value, compression gains, power use, and host platform cost in a single decision. Until those models become easier to benchmark across vendors, the CXL memory module market will move fastest in hyperscale and cloud accounts that can absorb larger upfront investments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: CXL 3.0 Modules Gain Ground As Protocol Capability Gap Widens

CXL 2.0 memory modules held 88.79% of the product type segment in 2025, which kept the installed base at the center of the CXL memory module market during the early commercialization phase. That lead reflected the fact that data center deployment of compatible CPU platforms accelerated through 2024 and 2025, so qualification cycles favored products that fit active server generations. The CXL memory module market, therefore, remained anchored in CXL 2.0 because buyers preferred a shorter path from validation to production, especially when large cloud and hyperscale fleets were already building around compatible infrastructure. CXL 3.0 modules are projected to grow at a 53.29% CAGR through 2031, indicating that the protocol gap is becoming a commercial differentiator as shared memory needs become more demanding. The CXL memory module market is shifting here because CXL 3.0 expands the addressable use case set beyond simple memory expansion and into broader rack-level resource sharing.

That transition is tied to capabilities such as multi-host cache coherence, switch-based pooling, and higher effective bandwidth, which become more valuable as deployments move from single-server upgrades to memory fabric designs. Marvell’s March 2026 switch launch showed that the ecosystem needed for CXL 3.x scaling is taking shape, which helps explain why the future growth curve in the CXL memory module market is stronger for the newer protocol generation. Buyers are also paying closer attention to interoperability because a richer protocol is only useful if controllers, hosts, and fabric managers behave consistently across vendors. The CXL memory module market is likely to see CXL 2.0 remain important for near-term deployments while CXL 3.x becomes the preferred path for larger-scale pooling architectures. This creates a phased transition rather than a sudden handoff, which is why both protocol generations remain commercially relevant across the forecast period.

By Memory Technology: DRAM Supremacy Masks Persistent Memory’s Strategic Role

DRAM-based CXL modules accounted for 92.14% of 2025 memory technology demand, making them the core of the CXL memory module market in the current cycle. That concentration reflects manufacturing reality, because established memory makers already have the production base and performance profile needed for AI, HPC, and cloud environments that treat CXL as a high-speed capacity extension. The CXL memory module market also favors DRAM today because hyperscalers and major cloud operators want predictable behavior from a primary expansion tier, and DRAM still aligns best with that requirement. At the same time, SCM and persistent memory-based CXL modules are projected to expand at a 53.47% CAGR, which shows that the CXL memory module market is broadening beyond volatile expansion use cases. Growth in this segment is tied to workloads that value restart speed, checkpointing, resilience, and data retention alongside capacity.

Penguin Solutions stated in January 2026 that its SMART Modular NV-CMM E3.S 2T module had passed CXL compliance testing, and the design combined volatile DRAM, NAND backup, an onboard energy source module, and AES-256 encryption for enterprise data center use. The CXL Consortium also noted that Type 3 devices can expose persistent capacity directly in the host memory map, enabling byte-addressable persistence without the overhead of a block storage workflow. That gives the CXL memory module market a path into in-memory databases, restart-sensitive virtualized systems, and analytical workloads that do not need all data on premium DRAM tiers. NAND and flash-based designs also create a middle layer where cost per gigabyte matters more than peak access speed, especially for colder analytics data. As software improves at handling tiered memory policies, the CXL memory module market should see persistent options shift from specialized products into a more visible strategic tier.

By Form Factor: AIC Leads Near Term While E3.S Reshapes Rack-Scale Deployments

Card modules accounted for 63.42% of 2025 form factor demand, giving them the largest share in the CXL memory module market during the first broad deployment cycle. Their lead is straightforward because PCIe slot availability is common across server fleets, so operators can add CXL capacity without redesigning chassis, cooling layouts, or backplane arrangements. The CXL memory module market benefited from that practicality because AIC-based deployments let buyers move faster through pilots and initial production programs. Astera Labs stated that its Aurora A-Series enabled up to 2 TB per slot with CXL 2.0 pooling support through 4 DDR5 RDIMM slots on a single PCIe card, which shows why the format is attractive for immediate expansion use cases. E3.S is projected to grow at a 53.41% CAGR through 2031, which signals where the CXL memory module market is heading as server designs become more standardized around high-density data center formats.

That shift is supported by products such as Innodisk’s 64 GB E3.S 2T module and SMART Modular’s NV-CMM E3.S platform, both of which use PCIe Gen 5 x8 links and target dense data center environments. E3.S matters to the CXL memory module market because a smaller footprint can support greater memory density per rack unit, a metric that becomes more important as buyers move from server-level upgrades to rack-level pooling plans. The format also aligns more naturally with Open Compute and EDSFF design directions, which helps standardize deployment choices across OEMs and large operators. U.2 and U.3 options still serve legacy environments where newer backplanes are absent, but their structural role in the CXL memory module market is weaker as new server programs standardize on E3.S-oriented designs. Over time, the practical advantage that favored AIC in the first wave is likely to give way to density and system-level design priorities that favor E3.S.

By Application: AI And ML Anchor Demand While Virtualization Drives The Next Expansion Wave

Artificial intelligence and machine learning accounted for 35.64% of 2025 application demand, making them the largest workload group in the CXL memory module market. That share reflects the fact that training clusters and inference servers hit memory ceilings faster than many traditional enterprise workloads, especially when large model serving requires large KV cache footprints. Research in 2026 showed that CXL-pooled memory could support LLM conditional memory retrieval with behavior similar to local DRAM, which is highly relevant to sparse retrieval and recommendation-style tasks. The CXL memory module market is therefore being shaped by AI not only through training infrastructure, but also through production inference systems that need more memory capacity without proportional growth in accelerator count. Virtualization and cloud are projected to expand at a 53.82% CAGR through 2031, pointing to a second growth wave built on broader, more repeatable infrastructure economics.

Microsoft Azure’s November 2025 preview of CXL-backed M-series virtual machines is the clearest reference case here, because it linked memory expansion directly to enterprise workloads such as SAP S/4HANA and large in-memory database operations. The CXL memory module market benefits from cloud virtualization, as each successful deployment can support multiple customer environments through a shared platform design rather than a single workload at a time. HPC also remains important because large-scale simulation and scientific environments can benefit from disaggregated memory without falling back on storage-tier latencies. Database and analytics deployments play a distinct role in the CXL memory module market because they can leverage expanded memory tiers that are materially faster than NVMe while avoiding the full cost of all DRAM architectures. Enterprise application adoption should follow later as certified configurations become easier to buy on standard server lines and as memory-tiering software reduces the management burden for mixed-workload estates.

By End User: Hyperscale Operators Set Qualification Standards While Cloud Service Providers Drive Volume

Hyperscale data centers accounted for 49.17% of 2025 end-user demand, giving them the leading position in the CXL memory module market. That result reflects their dual role as early adopters and as qualification partners whose validation decisions influence the rest of the market. The CXL memory module market has developed around hyperscale infrastructure needs because these operators face the highest memory utilization pressure, and they can justify architectural changes sooner than most enterprise buyers. Their buying behavior also shapes vendor roadmaps, because module suppliers and controller companies need hyperscale proof points before they can scale into wider commercial channels. Cloud service providers are projected to grow at a 54.09% CAGR through 2031, suggesting that the next major demand step in the CXL memory module market will come from resold infrastructure rather than internal fleet use alone.

This matters because a single CXL-enabled cloud deployment can support many downstream customers through memory-rich virtual machines and managed platforms, which makes the demand effect broader than a direct enterprise sale. The CXL memory module market is therefore likely to see CSPs translate hyperscale learning into standardized commercial offerings that reduce adoption friction for business users. Enterprise data centers still represent a meaningful medium-term opportunity, but progress depends on certified server configurations and better operating system-level support for memory tiering and region management. OEM and ODM server makers remain important because they convert technology readiness into purchasable systems that mainstream buyers can deploy with lower integration risk. Research and government installations play a specialized role in the CXL memory module market because memory disaggregation aligns well with simulation-heavy HPC environments, even if those buyers do not drive volume on the same scale as hyperscalers and CSPs.

Geography Analysis

North America accounted for 45.37% of 2025 demand and remained the largest regional contributor to the CXL memory module market in the current cycle. The region leads because the United States hosts the largest hyperscale cloud operators, and those firms were central to early qualification work, server platform rollout, and production-style deployment planning. The CXL memory module market in North America also benefits from a strong controller and platform ecosystem, which makes commercial validation easier across memory suppliers, silicon vendors, and cloud infrastructure operators. Microsoft Azure’s November 2025 preview of CXL-backed M-series virtual machines showed that the region had already moved beyond lab testing into customer-facing deployment for enterprise memory-intensive workloads.[3]Astera Labs, “Astera Labs' Leo CXL Smart Memory Controllers on Microsoft Azure M-series Virtual Machines Overcome the Memory Wall,” Astera Labs, asteraLabs.com Canada benefits from cross-border alignment of cloud infrastructure with US operators, while Mexico remains more relevant through logistics and server assembly linkages than through direct demand at this stage.

Asia-Pacific is projected to expand at a 53.78% CAGR through 2031, making it the fastest-growing regional market for CXL memory modules. South Korea anchors that trajectory because Samsung and SK Hynix remain central to the supply of CXL-capable memory products, and their product activity keeps the regional ecosystem close to the core of commercialization. The CXL memory module market in Asia-Pacific also benefits from its role in component manufacturing, system integration, and controller development, which gives the region influence on both supply and deployment readiness. Japan is building a clear distribution channel for commercial products, including Tekwind’s July 2025 rollout of SMART Modular CXL add-in card products for the local market. India remains an early-stage opportunity in the CXL memory module market, but large hyperscale campus investments lay the groundwork for future generations of servers that can adopt CXL more broadly over time.

Europe holds a smaller share of the CXL memory module market today, but demand is forming around enterprise migration needs, hyperscale data center buildouts, and the search for better memory efficiency in larger cloud and application environments. Germany, the United Kingdom, and France are the most likely demand centers because they combine data center investment, enterprise software scale, and a growing need for higher memory density. The CXL memory module market in Europe should strengthen as buyers move from pilot evaluations toward validated multi-vendor configurations that reduce procurement uncertainty. South America, the Middle East, and Africa remain earlier in the adoption curve, and most near-term access to CXL-enabled infrastructure is likely to come through cloud regions rather than broad on-premises deployments. As cloud service providers widen their CXL-based offerings, these regions can still participate in the CXL memory module market through service consumption before large local hardware fleets emerge.

Competitive Landscape

The CXL memory module market is moderately consolidated and has a layered competitive structure, with large DRAM manufacturers controlling much of the module supply base, while controller providers compete on bandwidth efficiency, interoperability, switching capability, and effective memory utilization. Samsung Electronics, SK hynix, and Micron Technology shape the supply side because the commercialization of memory modules depends heavily on established DRAM design and manufacturing capabilities. A second tier of controller and connectivity players, including Astera Labs, Marvell Technology, Rambus, Microchip Technology, and Montage Technology, competes on how effectively CXL can be integrated into real deployment environments. The CXL memory module market also includes server OEMs such as Dell Technologies, Hewlett Packard Enterprise, Lenovo, and Super Micro Computer, which matter because system certification and integration support influence buying decisions almost as much as component specifications. This structure makes the CXL memory module market concentrated at the supply core, but still open and contested across controllers, platforms, and deployment models.

Marvell has used interoperability and switching as two visible competitive moves in the CXL memory module market. In April 2025, the company announced the successful interoperability of its Structera portfolio with AMD EPYC and 5th Gen Intel Xeon Scalable systems, which gave enterprise buyers a clearer path to multi-platform deployment.[4]Marvell Technology, “Marvell Announces Successful Interoperability of Structera CXL Portfolio with AMD EPYC CPU and 5th Gen Intel Xeon Scalable Platforms,” Marvell Technology, marvell.com In March 2026, Marvell followed with a next-generation CXL switch designed for shared-memory scaling at the rack level, pushing competition beyond endpoint controllers into fabric architecture. In June 2026, the company added another differentiator by stating that Structera X and A controllers can deliver up to 3.64x effective DRAM capacity utilization through inline compression, which shifts buyer attention toward usable capacity economics rather than raw capacity alone. These moves show that competition in the CXL memory module market is not limited to memory density, as vendors are also trying to shape the value each deployed gigabyte delivers.

Astera Labs has taken a different route, focusing on early cloud-deployment proof points in the CXL memory module market. Its November 2025 Azure reference deployment provided a commercially significant validation event, as enterprise buyers often treat hyperscale use as a signal of operational readiness. Standards bodies are also influencing competition because the Open Compute Project and the CXL Consortium continue to reinforce open, interoperable approaches to memory fabrics and persistent memory support. That dynamic rewards vendors that invest in certification and cross-vendor compatibility, making proprietary strategies harder to sustain in the long run. The CXL memory module market is, therefore, competitive in practice, even though supply is concentrated among a small number of memory leaders, because performance, interoperability, and deployment simplicity remain key areas of differentiation.

CXL Memory Module Industry Leaders

Samsung Electronics Co., Ltd.

SK hynix Inc.

Micron Technology, Inc.

Astera Labs, Inc.

Intel Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: NVIDIA and SK hynix announced a multiyear technology partnership to co-develop next-generation memory aligned with NVIDIA's AI infrastructure roadmap, covering CXL and HBM memory for NVIDIA Vera Rubin AI supercomputers and Vera CPU platforms, and extending co-engineering to AI-driven semiconductor design and autonomous fab operations.

- June 2026: Marvell Technology disclosed that Structera X and A CXL memory-expansion controllers achieve up to 3.64x effective DRAM capacity utilization through hardware-based inline compression at line rate, the first such capability submitted to the Open Compute Project in specifications aligned with requirements from Google and Meta.

- March 2026: Marvell announced the Structera S 30260, a 260-lane CXL 3.x switch supporting up to 48 TB of shared memory and 4 TB/s aggregate bandwidth per rack, enabling rack-level composable memory architectures, sampling to hyperscale customers is planned for Q3 2026, with Structera S 20256 CXL 2.0 switch already in full production.

- January 2026: Penguin Solutions' SMART Modular CXL NV-CMM E3.S 2T non-volatile memory module passed CXL Consortium compliance testing and was listed on the CXL Consortium Integrators List, certifying it for enterprise data center deployment with persistent memory, AES-256 encryption, and fast crash-recovery capabilities.

Global CXL Memory Module Market Report Scope

The CXL Memory Module Market comprises memory expansion solutions based on the Compute Express Link (CXL) standard that enable memory pooling, sharing, and tiering across heterogeneous computing environments. These modules leverage the high-speed, low-latency CXL interconnect to extend system memory capacity beyond traditional DDR-attached architectures, improving resource utilization, workload scalability, and overall data center efficiency. CXL memory modules support composable infrastructure by enabling dynamic memory allocation among processors, accelerators, and storage devices, making them critical for artificial intelligence (AI), machine learning (ML), high-performance computing (HPC), cloud computing, and data-intensive enterprise applications.

The CXL Memory Module Market Report is Segmented by Product Type (CXL 2.0 Memory Modules, and CXL 3.0 Memory Modules), Memory Technology (DRAM-Based CXL Memory Modules, NAND/Flash-Based CXL Memory Modules, and SCM/Persistent Memory-Based CXL Modules), Form Factor (E3.S Modules, Add-in Card (AIC) Modules, U.2/U.3 and Other Form Factors), Application (Artificial Intelligence and Machine Learning, High Performance Computing, Database and Analytics, Virtualization and Cloud, and Enterprise Applications), End User (Cloud Service Providers, Hyperscale Data Centers, Enterprise Data Centers, OEM/ODM Server Manufacturers, Research and Government Computing, and Other End Users), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| CXL 2.0 Memory Modules |

| CXL 3.0 Memory Modules |

| DRAM-Based CXL Memory Modules |

| NAND/Flash-Based CXL Memory Modules |

| SCM/Persistent Memory-Based CXL Modules |

| E3.S Modules |

| Add-in Card (AIC) Modules |

| U.2/U.3 and Other Form Factors |

| Artificial Intelligence and Machine Learning |

| High Performance Computing |

| Database and Analytics |

| Virtualization and Cloud |

| Enterprise Applications |

| Cloud Service Providers |

| Hyperscale Data Centers |

| Enterprise Data Centers |

| OEM/ODM Server Manufacturers |

| Research and Government Computing |

| Other End Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| Taiwan | |

| India | |

| Rest of Asia-Pacific | |

| South America | |

| Middle East and Africa |

| By Product Type | CXL 2.0 Memory Modules | |

| CXL 3.0 Memory Modules | ||

| By Memory Technology | DRAM-Based CXL Memory Modules | |

| NAND/Flash-Based CXL Memory Modules | ||

| SCM/Persistent Memory-Based CXL Modules | ||

| By Form Factor | E3.S Modules | |

| Add-in Card (AIC) Modules | ||

| U.2/U.3 and Other Form Factors | ||

| By Application | Artificial Intelligence and Machine Learning | |

| High Performance Computing | ||

| Database and Analytics | ||

| Virtualization and Cloud | ||

| Enterprise Applications | ||

| By End User | Cloud Service Providers | |

| Hyperscale Data Centers | ||

| Enterprise Data Centers | ||

| OEM/ODM Server Manufacturers | ||

| Research and Government Computing | ||

| Other End Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| Taiwan | ||

| India | ||

| Rest of Asia-Pacific | ||

| South America | ||

| Middle East and Africa | ||

Key Questions Answered in the Report

What is the current and future size of the CXL memory module space?

The CXL memory module market size is projected at USD 0.51 billion in 2026 and is forecast to reach USD 4.28 billion by 2031, growing at a 52.90% CAGR over 2026 to 2031.

What is driving adoption of CXL memory modules in servers?

The main demand drivers are AI inference memory density, virtualization growth, and the shift from fixed server memory layouts to pooled and composable architectures.

Which product generation leads today and which one is growing faster?

CXL 2.0 led with 88.79% share in 2025 because it matched active server platforms, while CXL 3.0 is projected to grow faster at a 53.29% CAGR as pooling and switching use cases expand.

Why are hyperscalers and cloud providers important in this category?

Hyperscale data centers held 49.17% of end user demand in 2025, and cloud service providers are projected to grow at a 54.09% CAGR because one deployment can support many customer workloads.

Which application area creates the strongest demand right now?

AI and machine learning led with 35.64% share in 2025, reflecting strong demand from training and inference systems that need more memory capacity than DIMM only designs can usually provide.

Which region is most important for growth over the next 5 years?

North America led with 45.37% share in 2025, but Asia-Pacific is projected to post the fastest growth at a 53.78% CAGR because of its strong memory supply base and expanding deployment ecosystem.

Page last updated on: