CXL Memory Controller IC Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

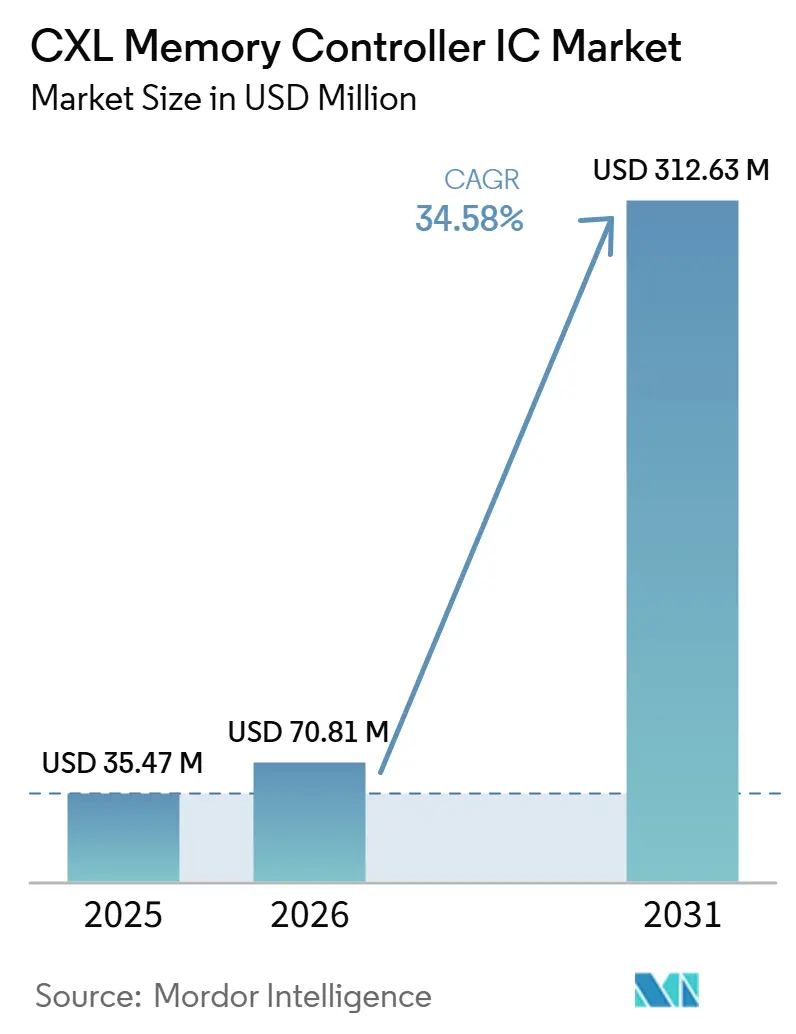

| Market Size (2026) | USD 70.81 Million |

| Market Size (2031) | USD 312.63 Million |

| Growth Rate (2026 - 2031) | 34.58% CAGR |

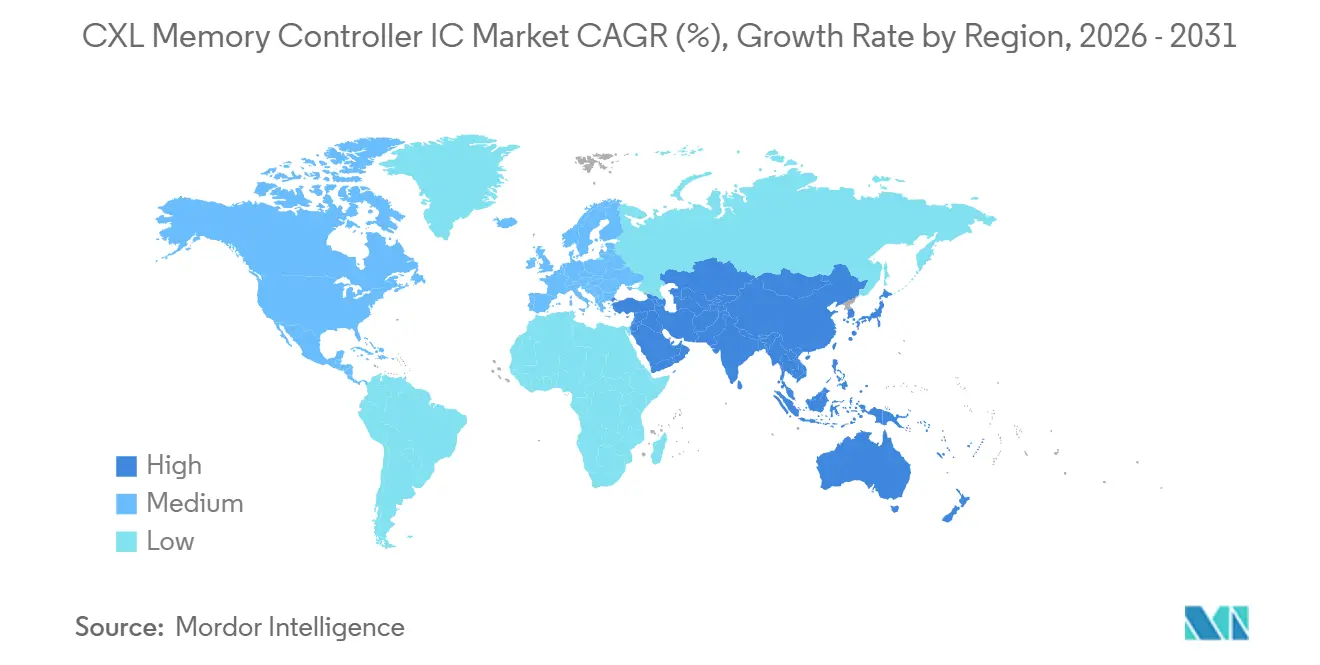

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

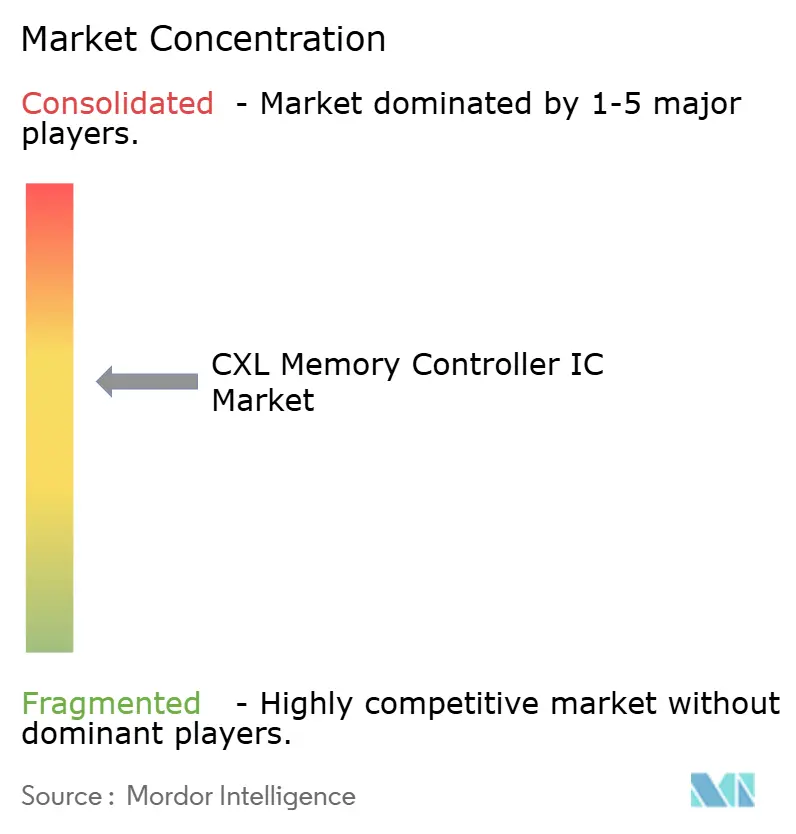

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

CXL Memory Controller IC Market Analysis by Mordor Intelligence

The CXL memory controller IC market size is projected to expand from USD 35.47 million in 2025 and USD 70.81 million in 2026 to USD 312.63 million by 2031, registering a CAGR of 34.58% between 2026 and 2031. The CXL memory controller IC market is moving beyond early testing, as the first commercial cloud deployments have already shown that external coherent memory can be added without changing the host processor design. The CXL memory controller IC market is also benefiting from the way AI server clusters are scaling, because memory bandwidth and capacity needs are rising faster than conventional DDR5 channel expansion can solve. The CXL memory controller IC market remains centered on direct-attached products today, but revenue growth is shifting toward rack-scale memory pooling, higher-performance interfaces, and AI inference use cases that need much larger memory footprints. Competitive outcomes in the CXL memory controller IC market depend on qualification speed, interoperability across CPU and DRAM ecosystems, and the ability to match controller launches with server platform readiness. The CXL memory controller IC market, therefore, has a strong growth outlook, but the pace of commercialization will still be shaped by the transition from limited deployments to repeatable server OEM configurations.

Key Report Takeaways

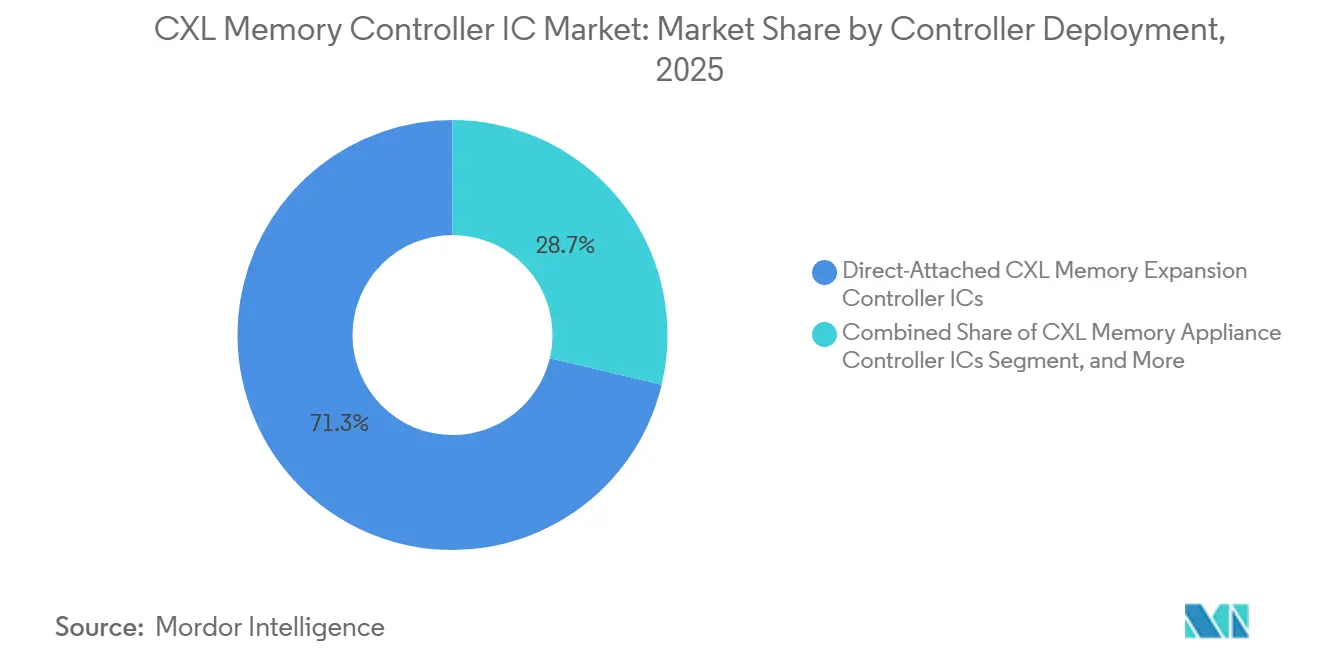

- By controller deployment, direct-attached CXL memory expansion controller ICs held 71.28% share of the CXL memory controller IC market size in 2025, while fabric-attached or rack-scale memory controller ICs are projected to expand at a 35.58% CAGR through 2031.

- By CXL specification, CXL 1.1 and CXL 2.0 accounted for 87.36% of 2025 revenue, while CXL 4.0 is projected to record the highest CAGR at 35.51% through 2031.

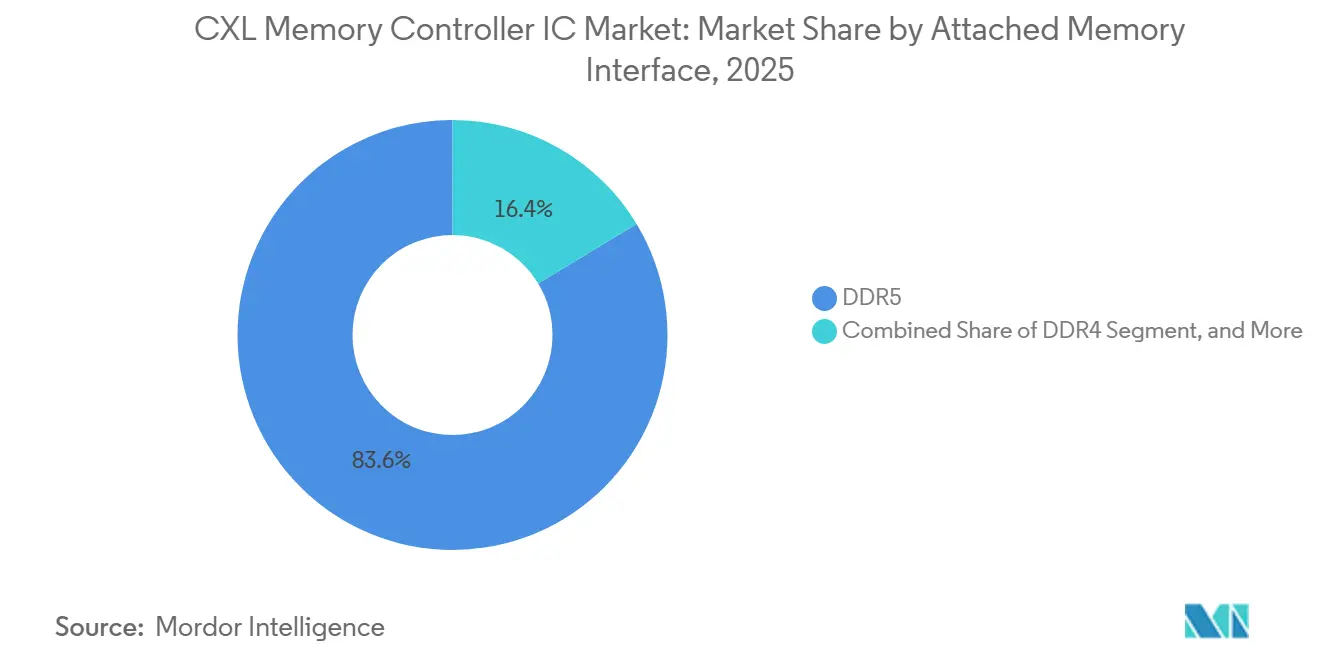

- Through the attached memory interface, DDR5 accounted for 83.63% of segment revenue in 2025, while heterogeneous DRAM and HBM-enabled architectures are projected to expand at a 35.49% CAGR through 2031.

- By endpoint form factor, PCIe add-in cards accounted for 66.14% of revenue in the CXL memory controller integrated circuit (IC) market in 2025, while EDSFF CXL memory modules are projected to grow at a 35.54% CAGR through 2031.

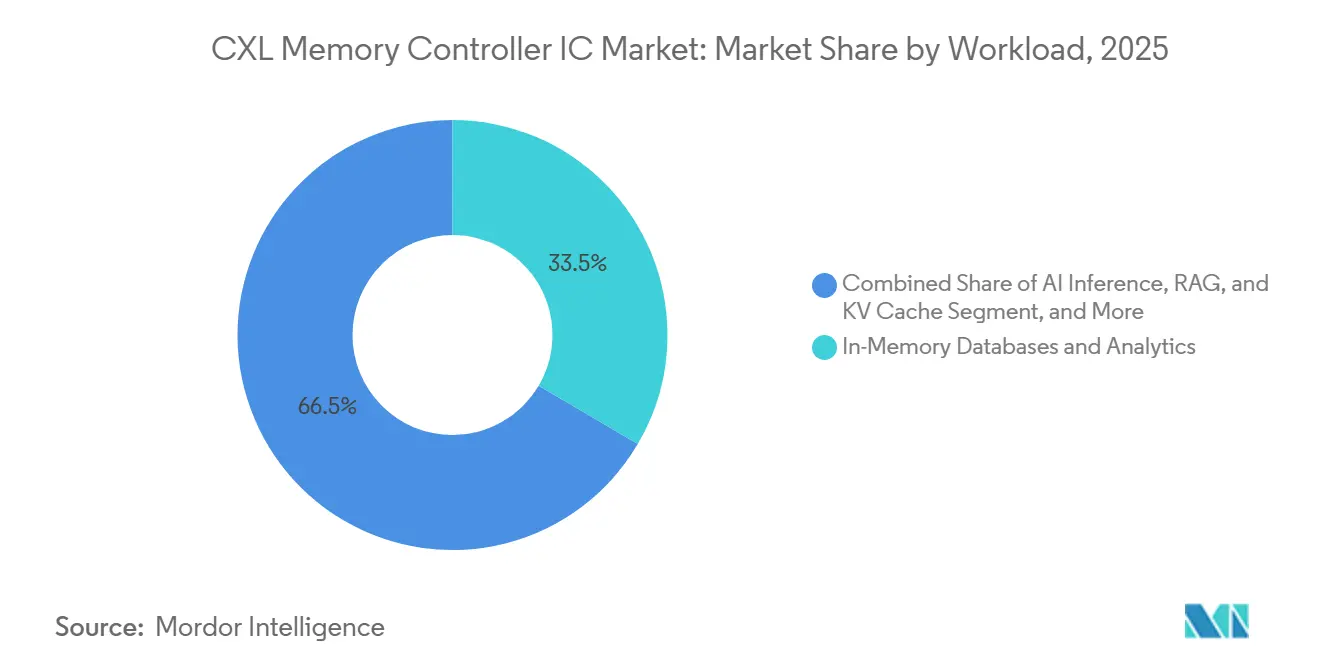

- By workload, in-memory databases and analytics led with 33.47% of revenue in 2025, while AI inference, RAG, and KV Cache workloads are projected to advance at a 35.96% CAGR through 2031.

- By end user, hyperscalers held 68.11% share of the CXL memory controller IC market size in 2025, while cloud service providers are projected to expand at a 35.77% CAGR through 2031.

- By geography, North America accounted for 63.52% share of the CXL memory controller IC market size in 2025, while Asia-Pacific is projected to record the fastest regional CAGR at 35.48% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global CXL Memory Controller IC Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevances | Impact Timeline |

|---|---|---|---|

| AI Server Memory Bandwidth Expansion | +8.0% | Global, with concentration in North America and Asia-Pacific | Short term (≤ 2 years) |

| Hyperscale Adoption of Memory Pooling and Disaggregation | +7.2% | North America and Asia-Pacific core, with spillover to Europe | Medium term (2-4 years) |

| Migration to CXL 2.0 and CXL 3.x Ecosystem | +6.5% | Global | Short term (≤ 2 years) to Medium term (2-4 years) |

| Rack-Level Memory Utilization and TCO Optimization | +4.8% | North America, Asia-Pacific, and Europe | Medium term (2-4 years) |

| Low-Latency Coherent Attach for Accelerators and CPU Memory Expansion | +3.5% | Global, led by North America | Medium term (2-4 years) to Long term (≥ 4 years) |

| Security and RAS Demand in Shared Memory Fabrics | +2.0% | Global, with focus on Europe and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

AI Server Memory Bandwidth Expansion

The strongest demand in the CXL memory controller IC market stems from the widening mismatch between the growth of accelerator compute and the memory bandwidth available in standard server designs.[1]Marvell Technology, “Structera X and A CXL Compression, Making Every Gigabyte Count,” Marvell, marvell.com Server DDR5 still carries a high per-gigabyte cost, and socket pin limits limit how far memory channels can be expanded without a broader platform redesign, making off-processor memory attachment more practical for large AI deployments. CXL addresses that constraint by using the PCIe physical layer to connect coherent memory with low latency, which gives operators more room to scale memory capacity without reworking host silicon. A CXL Consortium benchmark released in October 2025 showed up to 19% higher performance in VectorDB search workloads when CXL-connected DRAM was used instead of a local DRAM-only setup in Milvus RAG clusters. The CXL memory controller IC market is also supported by the growth of large KV caches in inference systems, as longer context windows and higher concurrency can push memory needs into terabyte-per-server ranges. Astera Labs has shown that Leo controllers can offload KV cache demands, lowering serving costs compared to HBM-only memory configurations, which helps explain why hyperscalers have moved these products into live cloud evaluation environments.

Hyperscale Adoption Of Memory Pooling and Disaggregation

Hyperscalers are increasingly shaping the CXL memory controller IC market by turning memory pooling from a lab concept into a production architecture decision. A 2026 deployment study on disaggregated machine learning inference showed that CXL-attached embedding tables could reduce server count by up to 25%, providing data center buyers with a direct operational case for controller silicon adoption at rack scale. Marvell moved this part of the CXL memory controller IC market forward by putting its Structera S 20256 CXL 2.0 switch into production and then announcing the Structera S 30260 with 260 lanes, support for up to 48 TB of shared memory, and 4 TB/s of cumulative bandwidth. These pooling designs matter more than unit volumes alone because they add fabric capability, multi-host support, and more complex reliability features, all of which raise revenue per rack compared with basic expansion controllers. Astera Labs also demonstrated rack-scale memory concepts at the Open Compute Project Global Summit 2025, reinforcing that memory fragmentation is becoming a commercial problem that controller vendors now address directly for cloud and AI fleets. As those reference deployments become standard platform templates, the CXL memory controller IC market is likely to shift from isolated design wins toward broader multi-rack adoption.

Migration To CXL 2.0 and CXL 3.x Ecosystem

The CXL memory controller IC market is being lifted by the speed at which the standard itself is advancing, because each new revision expands the set of memory functions controllers can support. CXL 2.0 established the commercial base for memory pooling, while CXL 3.0 and CXL 3.1 added switching and peer-to-peer memory features that broaden the value of controller silicon beyond single-host expansion. The CXL Consortium then released CXL 4.0 in November 2025 with 128 GT/s bandwidth, bundled ports, native x2 support, and stronger memory RAS functions for larger deployments. Montage Technology reinforced that migration path when it demonstrated its CXL 3.2 M88MX6852 controller running a Dynamic Capacity Device system with live multi-host sharing, which showed that next-generation controller functions are moving closer to practical deployment. Marvell also created a qualification benchmark when its Structera family completed interoperability across both AMD EPYC and Intel Xeon platforms and all 3 major DRAM suppliers. That combination of faster standards movement and broader interoperability keeps the CXL memory controller integrated circuit (IC) market in a repeated upgrade cycle rather than a one-time product transition.

Rack-Level Memory Utilization and TCO Optimization

The CXL memory controller IC market is gaining support because conventional server memory usage remains inefficient, leaving large pools of DRAM idle at the server level while other nodes are constrained. The input shows that conventional memory utilization in many server setups is only 40-60%, suggesting rack-scale sharing can improve how existing memory is used before operators buy more hardware. The same input also points to a 15-20% reduction in total cost of ownership for rack designs where memory demand differs materially across workloads, strengthening the business case for pooled memory architectures. Marvell added to that case by introducing inline compression in Structera X and Structera A, with up to 3.64x data compression and 200 GB/s throughput while retaining XTS-AES 256-bit encryption support. Montage Technology also showed at Flash Memory Summit 2025 that a hybrid server using 512 GB DDR5 and 512 GB CXL memory could deliver 95-100% of the throughput of an all-DRAM configuration, with only 5-10 µs of added application latency. Those outcomes matter because the CXL memory controller IC market is not sold solely on technical novelty, but also on the ability to reduce stranded memory and defer capital spending at rack scale.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ecosystem Interoperability and Validation Complexity | -4.2% | Global, concentrated in North America and Asia-Pacific | Short term (≤ 2 years) |

| High NRE and Silicon Implementation Cost | -3.3% | Global | Medium term (2-4 years) |

| Software Stack Immaturity for Disaggregated Memory | -2.5% | Global | Medium term (2-4 years) |

| Limited Volume Ramp Outside Hyperscale and Premium Server Segments | -1.8% | Rest of the world outside North America and Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Ecosystem Interoperability and Validation Complexity

The CXL memory controller IC market still faces a real commercialization constraint because qualification must happen across CPUs, memory modules, controller silicon, and software layers rather than within a single vendor stack. The delay of Samsung’s CXL 3.1 CMM-D mass production to 2027 shows how a slip in CPU platform timing can slow multiple product roadmaps at once, which pushes controller revenue recognition further out. Research published at ASPLOS 2026 also found that bridges across different cache-coherence architectures still lack standardized interoperability mechanisms, making mixed-vendor deployments harder to validate safely. The input further notes that verification IP updates can require several weeks of engineering work for major CXL sub-features, which turns rapid standards progress into a practical qualification burden for suppliers. Even though the CXL Consortium certification process helps, the overlap of CXL 1.1, 2.0, 3.x, and 4.0 in active roadmaps means the CXL memory controller IC market still carries a heavy multi-version validation load.

High NRE and Silicon Implementation Cost

The CXL memory controller IC market also remains difficult for new entrants because production-grade controller development requires significant design investment, repeated validation effort, and tight synchronization with shifting platform roadmaps. The input makes clear that this burden is one reason the field is still limited to a small number of well-capitalized merchant silicon vendors and integrated memory suppliers. Rambus has publicly described how the business model for direct controller commercialization can become unattractive when customer-specific variants are required, highlighting how feature fragmentation can weaken standard-product economics.[2]Rambus, “Compute Express Link CXL, All You Need to Know,” Rambus, rambus.com That cost pressure becomes more important as the CXL memory controller IC market moves from CXL 2.0 into 3.x and later 4.0, because each revision requires fresh engineering work before revenue follows. The result is a structure in which high development costs act as both a barrier to entry and a reason for some participants to favor IP licensing, partnerships, or vertically integrated module strategies over broad merchant silicon launches.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Controller Deployment: Direct-Attached Leads While Rack-Scale Designs Gain Ground

Direct-Attached CXL Memory Expansion Controller ICs accounted for 71.28% of revenue in 2025, indicating that the CXL memory controller IC market still relies on the simplest commercial deployment model. These controllers fit more easily into existing x86 server environments because they do not require switch silicon or fabric management layers for first-wave adoption. That simplicity matters in the CXL memory controller IC industry because early buyers have prioritized qualification speed and immediate platform compatibility over broader composable memory features. Astera Labs and Montage products both align with this pattern, as the input ties them to DDR5-based controller families that are already undergoing customer qualification for large-scale deployments. The remaining 2025 revenue base sat across memory pooling and sharing controllers, appliance-oriented controller designs, and custom integrated Type-3 controller ASICs that address more specialized deployment needs.

Fabric-Attached or Rack-Scale Memory Controller ICs are projected to grow at a 35.58% CAGR through 2031, making them the most dynamic deployment path in the CXL memory controller IC market. That growth says more than rising unit demand, because these products add switching, multi-host memory sharing, and heavier RAS requirements that are materially more complex than direct-attached expansion devices. Those features support higher average selling prices and give rack-scale platforms a larger revenue footprint per deployment than single-host add-in cards. Marvell’s Structera S 30260 reflects that shift, with support for up to 48 TB of shared memory over 260 lanes and 4 TB/s of cumulative bandwidth for 16 or 32 CPUs or GPUs. The CXL memory controller IC market is therefore moving from a first phase focused on server expansion to a second phase focused on shared memory fabrics that change memory provisioning at the rack level.

By CXL Specification: CXL 2.0 Anchors Current Revenue While Newer Revisions Build

CXL 1.1 and CXL 2.0 accounted for 87.36% of segment revenue in 2025, confirming that the current CXL memory controller IC market remains anchored in the first commercial generation of pooled and expanded memory. Most merchant products already in active production fit this base, as they were designed for the PCIe 5.0 era and focus on practical expansion use cases rather than broader fabric capabilities. Marvell’s Structera family has reinforced that position by achieving interoperability across both major server CPU architectures and all 3 leading DRAM suppliers, providing customers with a clearer path to deployment. Newer CXL 3.x controllers are still building design momentum, but mass production depends on server platform timing and on the maturity of supporting software and validation flows. The CXL memory controller IC market, therefore, continues to monetize CXL 2.0 today while later specifications move through the qualification funnel.

CXL 4.0 is projected to be the fastest-growing specification segment, with a 35.51% CAGR, even though the production window for this part of the CXL memory controller IC market is later in the forecast period. The November 2025 release of the CXL 4.0 specification doubled link speed to 128 GT/s, added bundled ports, native x2-width support, and expanded memory serviceability for larger deployments. Montage Technology also demonstrated Dynamic Capacity Device readiness with live multi-host sharing on its MXC Gen3 silicon, showing that ecosystem development is already moving beyond concept work. The input further notes that Panmnesia has disclosed CXL 4.0 link controller IP with very low round-trip latency targets, indicating that upstream design work is underway even before broad-production silicon arrives. This leaves the CXL memory controller IC market in a position where near-term revenue still comes from mature standards, while future growth rates are being set by early work on later revisions.

By Attached Memory Interface: DDR5 Dominates While Heterogeneous Designs Expand

DDR5 accounted for 83.63% of segment revenue in 2025, making it the clear base memory interface in the CXL memory controller IC market. That lead reflects simple deployment logic, because CXL 2.0 controllers were built around DDR5 speeds already moving into mainstream server adoption. The input also ties this dominance to production readiness, with customer validation of CXL 2.0 DDR5 memory modules reinforcing that DDR5 is the least disruptive path for operators that want more capacity without broader architecture changes. DDR4 and mixed DDR4/DDR5 support still matter in transition environments, where buyers may want to extend legacy memory usage rather than migrate all workloads to the newest platforms. Persistent and non-volatile CXL memory designs also remain part of the mix, but they serve more specialized use cases than the main DDR5 expansion path.

Heterogeneous DRAM and HBM-Enabled Architectures are projected to grow at a 35.49% CAGR through 2031, which shows where performance-oriented parts of the CXL memory controller IC market are heading. The input links grow to a structural bandwidth mismatch because HBM3E can deliver far more bandwidth than DDR5 in demanding AI training and inference environments. Research on the Beluga architecture reported an 89.6% reduction in Time-to-First-Token and a 7.35x throughput gain in vLLM inference when GPU access to pooled CXL memory was used instead of RDMA-based alternatives. Controller design becomes more demanding in these systems because vendors must manage coherence, scheduling, and latency across memory types with very different behavior. That complexity gives the CXL memory controller IC market a higher-value growth lane, since suppliers that can bridge DDR5 capacity expansion with HBM-adjacent performance can command a stronger position in AI-oriented deployments.

By Endpoint Form Factor: Add-In Cards Lead First Deployments While EDSFF Builds

PCIe Add-In Cards accounted for 66.14% of endpoint form factor revenue in 2025, making them the default physical form factor for the current CXL memory controller IC market. Their lead is easy to explain the fit standard server PCIe slots, reduce chassis changes, and support field upgrades during the evaluation and early production phases. This allows buyers to test memory expansion within familiar server designs before committing to more specialized rack layouts. The input also connects several active controller families to this format, including Astera Labs, Montage Technology, and Marvell products used in expansion-focused deployments. DIMM-based add-in cards, memory appliances, and rack-scale composable systems are already part of the mix, but they entail greater adoption complexity and heavier infrastructure requirements.

EDSFF CXL Memory Modules are projected to expand at a 35.54% CAGR through 2031, making them the fastest-growing form factor in the CXL memory controller IC market. Their appeal comes from platform design rather than near-term volume alone, because EDSFF supports denser thermal layouts, front-access serviceability, and higher module concentration per rack. Montage Technology’s M88MX6852 controller supports both E3.S EDSFF and PCIe add-in card formats at PCIe 6.2 and 64 GT/s x8, which shows that vendors are already preparing for this transition. The input further points out that cloud-native OEMs are beginning to align future rack specifications around this direction as platform support matures. That makes EDSFF a forward-looking indicator of where the CXL memory controller integrated circuit (IC) market will move as deployment shifts from qualification hardware to standardized production servers.

By Workload: Databases Lead Today While AI Inference Sets The Pace

In-Memory Databases and Analytics accounted for 33.47% of workload revenue in 2025, indicating that the CXL memory controller IC market first found commercial traction in workloads that already required very large memory footprints. This pattern fits established database environments where expanding memory capacity can produce immediate value without changing the whole application model. Astera Labs linked the Microsoft Azure M-series deployment to use cases such as SAP HANA, machine learning recommendation systems, and big data analytics, which confirms that high-memory enterprise and cloud workloads formed the first visible production base. AI training, GPU-adjacent expansion, and scientific computing also use the technology, but many of those deployments still depend on tighter performance validation and broader rack design changes. Virtualized and cloud-native workloads benefit from dynamic memory allocation as well, but adoption there is likely to broaden after the leading high-memory workloads establish more repeatable deployment patterns.

AI Inference, RAG, and KV Cache workloads are projected to grow at a 35.96% CAGR through 2031, which makes them the fastest-expanding part of the CXL memory controller IC market. The driver here is simple, because larger context windows and higher user concurrency can push KV cache requirements into terabyte ranges per inference server. CXL memory enables systems to add a near-DRAM latency tier without relying solely on expensive HBM capacity, improving the economics of scaled inference. The October 2025 CXL Consortium webinar also showed VectorDB search performance up to 19% better with CXL-connected DRAM, supporting the case for retrieval-heavy RAG environments. As enterprise AI deployment becomes increasingly inference-heavy, the CXL memory controller IC market is likely to gain more from memory efficiency and latency-sensitive serving than from one-time evaluation.

By End User: Hyperscalers Dominate While Cloud Service Providers Accelerate

Hyperscalers accounted for 68.11% of end-user demand in 2025, indicating the CXL memory controller IC market remains driven by a highly concentrated buyer group. Their role extends beyond purchasing volume, as they shape specifications, qualification pathways, and the deployment templates that the rest of the ecosystem follows. That is why merchant controller suppliers focus so heavily on proving interoperability across the CPU, DRAM, and cloud platform combinations that large cloud operators actually use. Enterprises, colocation operators, telecom providers, and research organizations remain relevant, but their adoption has been constrained by the high cost of premium hardware and software readiness. The CXL memory controller IC industry still sees these groups as an important later-stage demand base, especially once rack-scale designs become easier to integrate into standard server offerings.

Cloud Service Providers are projected to grow at a 35.77% CAGR through 2031, which makes them the fastest-rising end-user group in the CXL memory controller IC market. The input describes these buyers as fast followers, because they usually wait for hyperscalers to validate new hardware before deploying it at scale in more standardized fleets. Microsoft Azure’s M-series rollout is important in this respect because it establishes a clear production reference point that other cloud operators can study and adapt. As server OEMs turn CXL support into more repeatable platform options, CSP demand can scale faster without needing the same level of custom co-design seen at the hyperscaler tier. Over time, that could broaden the revenue base of the CXL memory controller IC market, even if the earliest validation still comes from the very largest buyers.

Geography Analysis

North America held 63.52% of the CXL memory controller IC market share in 2025, which makes it the clear center of commercial deployment activity. That lead reflects where hyperscaler spending is concentrated, since the largest cloud infrastructure operators remain the first buyers willing to qualify and deploy new coherent memory technologies. The Microsoft Azure M-series rollout in November 2025 was especially important because it marked the first announced production cloud deployment of CXL-attached memory and moved the region beyond test environments.[3]Astera Labs, “Astera Labs’ Leo CXL Smart Memory Controllers on Microsoft Azure M-Series Virtual Machines Overcome the Memory Wall,” Astera Labs Investor Relations, ir.asteralabs.com The United States also benefits from a strong semiconductor design base, which supports controller development, partner qualification, and tighter links between platform vendors and cloud customers. Canada and Mexico play a smaller but useful role through colocation and regional data center activity tied to North American cloud demand.

Asia-Pacific is projected to record the fastest growth in the CXL memory controller integrated circuit (IC) market size, with a 35.48% CAGR through 2031, making it the most important supply-side growth region. South Korea remains central because Samsung Electronics and SK hynix sit at the heart of CXL-capable memory module development and can influence how much value stays with modules versus merchant controllers. China adds weight through Montage Technology, whose controller roadmap and form factor support give the region a visible merchant silicon presence in the CXL memory controller IC market. Europe is developing from a different angle, with Germany, the United Kingdom, and France tied more closely to sovereign AI programs and high-performance computing efforts than to hyperscale platform leadership. Japan also adds demand through AI infrastructure, robotics, and HPC, while its component and packaging base supports the broader hardware ecosystem for advanced server memory.

South America is still a small part of the CXL memory controller IC market, but the region has a gradual entry path through colocation facilities and hyperscaler edge nodes in countries such as Brazil and Chile. That route matters because localized cloud capacity and data sovereignty needs can create early demand for higher-memory server configurations before broader rack-scale adoption appears. The Middle East and Africa are also in the early phase, with large data center construction programs in Saudi Arabia, the United Arab Emirates, and South Africa building the physical base for later adoption. For now, these regions are more likely to deploy standard DRAM-heavy server designs first, then move to advanced CXL topologies as they become more common in mainstream OEM platforms.

Competitive Landscape

The CXL memory controller IC market is moderately concentrated, with Astera Labs and Marvell Technology holding the strongest merchant silicon positions in the current commercial phase. Astera Labs gained a significant competitive advantage when its Leo Smart Memory Controllers became the silicon foundation for the first production CXL cloud deployment on Microsoft Azure M-series virtual machines.[4]Astera Labs, “Astera Labs’ Leo CXL Smart Memory Controllers on Microsoft Azure M-Series Virtual Machines Overcome the Memory Wall,” Astera Labs Investor Relations, ir.asteralabs.com That move mattered because it gave the company live cloud credibility in a market where many products are still moving from evaluation into billable infrastructure. Marvell differentiated itself through both interoperability and feature breadth, including cross-platform qualification with AMD EPYC and Intel Xeon systems and support across Micron, Samsung, and SK hynix memory solutions. The same company also gained an early feature advantage by introducing inline compression to its shipping CXL memory controller products, thereby strengthening its value proposition for memory cost optimization.

Montage Technology remains the most visible Asia-Pacific merchant controller supplier in the CXL memory controller IC market, and its product direction shows where competitive emphasis is shifting. The launch of the M88MX6852 controller in September 2025 added support for both EDSFF and PCIe add-in card form factors at PCIe 6.2 and 64 GT/s x8, which positions the company for newer server layouts and higher-speed controller cycles. Samsung and SK Hynix also aligned their CMM-D memory roadmaps with that launch, underscoring how closely controller vendors must work with memory suppliers to remain qualified. The next competitive layer is likely to form around rack-scale switching, advanced pooling features, and tighter integration with future memory module roadmaps. That is why Marvell’s Structera S 30260 launch at OFC 2026 was strategically important, since it pushed the competition beyond simple expansion controllers and into shared memory fabrics.

The CXL memory controller IC market still leaves room for specialists, but the most attractive openings sit in narrow technical gaps rather than in broad greenfield entry. Security-hardened controller IP, fabric management layers, and later-generation switching silicon remain the main areas where differentiation can still widen. Rambus has positioned itself around IP licensing rather than mass-market silicon, including controller IP with integrated IDE support for custom chip developers who want CXL capability without building the full stack themselves. Smaller developers working on later-generation controller IP can still become relevant, but they are more likely to matter as partners, licensing targets, or acquisition candidates than as near-term volume leaders. As a result, the CXL memory controller IC market is expected to remain concentrated even as product categories expand, because customer qualification, platform timing, and engineering cost still favor a limited group of established suppliers.

CXL Memory Controller IC Industry Leaders

Astera Labs, Inc.

Montage Technology Co., Ltd.

Microchip Technology Incorporated

Rambus Inc.

Renesas Electronics Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2026: Samsung Electronics delayed mass production of its CXL 3.1 CMM-D memory module to 2027, following Intel Diamond Rapids platform slippage to Q2-Q3 2027 and AMD EPYC Venice's H2 2026 schedule. Customer sample testing on AMD EPYC Venice systems is now planned for after September 2026, compressing the qualification window for CXL 3.1 controller ICs tied to these platforms and effectively pushing broad CXL 3.x market volume into 2027-2028.

- June 2026: Marvell Technology disclosed hardware-based inline memory compression in its Structera X and Structera A CXL controllers, achieving up to 3.64x data compression using LZ4 at 200 GB/s memory bandwidth and XTS-AES 256-bit encryption. Aligned with Open Compute Project specifications, this is the first production CXL memory controller with inline compression as a shipping feature, effectively expanding usable DRAM capacity without additional hardware procurement.

- March 2026: Marvell launched the Structera S 30260, a 260-lane CXL 3.x switch device supporting up to 48 TB shared memory and 4 TB/s cumulative bandwidth for 16 or 32 CPUs or GPUs, at OFC 2026 in Los Angeles. The device was demonstrated live and is expected to begin customer sampling in Q3 2026. The Structera S 20256 CXL 2.0 switch is currently in production.

- November 2025: The CXL Consortium released the CXL 4.0 specification at Supercomputing 2025, doubling link bandwidth from 64 GT/s to 128 GT/s on the PCIe 7.0 physical layer, with zero added latency. The release introduced CXL bundled port capabilities, native x2 width support, and enhanced memory RAS features, targeting multi-rack AI and HPC deployments.

Global CXL Memory Controller IC Market Report Scope

The CXL Memory Controller IC market comprises semiconductor controller integrated circuits (ICs) that enable Compute Express Link (CXL)-based memory expansion, pooling, sharing, and coherent memory communication across AI, cloud, enterprise, and high-performance computing (HPC) platforms. The market includes controller ICs for direct-attached memory expansion, memory pooling, rack-scale memory systems, memory appliances, and custom CXL Type-3 controller ASICs. It covers solutions supporting multiple CXL specification generations, DDR4, DDR5, heterogeneous DRAM/HBM, and persistent memory interfaces, deployed across PCIe add-in cards, DIMM-based CXL modules, EDSFF memory modules, memory appliances, and composable memory systems. The market addresses workloads such as AI training and inference, RAG, HPC, in-memory databases, virtualization, enterprise applications, and telecom edge computing, serving hyperscalers, cloud service providers, enterprises, colocation providers, telecom operators, and government and research organizations.

The CXL Memory Controller IC Market Report is Segmented by Controller Deployment (CXL Memory Appliance Controller ICs, CXL Memory Pooling and Sharing Controller ICs, Fabric-Attached / Rack-Scale Memory Controller ICs, Direct-Attached CXL Memory Expansion Controller ICs, and Custom / Integrated CXL Type-3 Controller ASICs), CXL Specification (CXL 3.0, CXL 3.1/CXL 3.2, CXL 1.1/CXL 2.0, and CXL 4.0), Attached Memory Interface (DDR5, DDR4, DDR4 and DDR5 Multi-Generation Support, Heterogeneous DRAM / HBM-Enabled Architectures, and Persistent / Non-Volatile CXL Memory Architectures), Endpoint Form Factor (PCIe Add-In Cards, DIMM-Based CXL Add-In Cards, EDSFF CXL Memory Modules - E1.S / E3.S, CXL Memory Appliances/Expansion Boxes, and Rack-Scale / Composable Memory Systems), Workload (AI Inference, RAG, and KV Cache, AI Training and GPU-Adjacent Memory Expansion, HPC and Scientific Computing, In-Memory Databases and Analytics, Virtualization and Cloud-Native Workloads, Enterprise Database and ERP, and Telecom Cloud and Edge), End User (Hyperscalers, Cloud Service Providers, Enterprises, Colocation and Managed Hosting Providers, Telecom Operators and Edge Providers, and Government, Research Laboratories, and Supercomputing Centers), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| CXL Memory Appliance Controller ICs |

| CXL Memory Pooling and Sharing Controller ICs |

| Fabric-Attached / Rack-Scale Memory Controller ICs |

| Direct-Attached CXL Memory Expansion Controller ICs |

| Custom / Integrated CXL Type-3 Controller ASICs |

| CXL 1.1 / CXL 2.0 |

| CXL 3.0 |

| CXL 3.1 / CXL 3.2 |

| CXL 4.0 |

| DDR5 |

| DDR4 |

| DDR4 and DDR5 Multi-Generation Support |

| Heterogeneous DRAM / HBM-Enabled Architectures |

| Persistent / Non-Volatile CXL Memory Architectures |

| PCIe Add-In Cards |

| DIMM-Based CXL Add-In Cards |

| EDSFF CXL Memory Modules – E1.S / E3.S |

| CXL Memory Appliances / Expansion Boxes |

| Rack-Scale / Composable Memory Systems |

| AI Inference, RAG, and KV Cache |

| AI Training and GPU-Adjacent Memory Expansion |

| HPC and Scientific Computing |

| In-Memory Databases and Analytics |

| Virtualization and Cloud-Native Workloads |

| Enterprise Database and ERP |

| Telecom Cloud and Edge |

| Hyperscalers |

| Cloud Service Providers |

| Enterprises |

| Colocation and Managed Hosting Providers |

| Telecom Operators and Edge Providers |

| Government, Research Laboratories, and Supercomputing Centers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Southeast Asia | |

| Rest of Asia-Pacific | |

| South America | |

| Middle East and Africa |

| By Controller Deployment | CXL Memory Appliance Controller ICs | |

| CXL Memory Pooling and Sharing Controller ICs | ||

| Fabric-Attached / Rack-Scale Memory Controller ICs | ||

| Direct-Attached CXL Memory Expansion Controller ICs | ||

| Custom / Integrated CXL Type-3 Controller ASICs | ||

| By CXL Specification | CXL 1.1 / CXL 2.0 | |

| CXL 3.0 | ||

| CXL 3.1 / CXL 3.2 | ||

| CXL 4.0 | ||

| By Attached Memory Interface | DDR5 | |

| DDR4 | ||

| DDR4 and DDR5 Multi-Generation Support | ||

| Heterogeneous DRAM / HBM-Enabled Architectures | ||

| Persistent / Non-Volatile CXL Memory Architectures | ||

| By Endpoint Form Factor | PCIe Add-In Cards | |

| DIMM-Based CXL Add-In Cards | ||

| EDSFF CXL Memory Modules – E1.S / E3.S | ||

| CXL Memory Appliances / Expansion Boxes | ||

| Rack-Scale / Composable Memory Systems | ||

| By Workload | AI Inference, RAG, and KV Cache | |

| AI Training and GPU-Adjacent Memory Expansion | ||

| HPC and Scientific Computing | ||

| In-Memory Databases and Analytics | ||

| Virtualization and Cloud-Native Workloads | ||

| Enterprise Database and ERP | ||

| Telecom Cloud and Edge | ||

| By End User | Hyperscalers | |

| Cloud Service Providers | ||

| Enterprises | ||

| Colocation and Managed Hosting Providers | ||

| Telecom Operators and Edge Providers | ||

| Government, Research Laboratories, and Supercomputing Centers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Southeast Asia | ||

| Rest of Asia-Pacific | ||

| South America | ||

| Middle East and Africa | ||

Key Questions Answered in the Report

What is the size outlook for the CXL memory controller IC market?

The CXL memory controller IC market stood at USD 35.47 million in 2025, reached USD 70.81 million in 2026, and is projected to reach USD 312.63 million by 2031 at a 34.58% CAGR.

Which deployment model leads current revenue?

Direct-Attached CXL Memory Expansion Controller ICs led with 71.28% of revenue in 2025 because they fit existing server designs with less deployment complexity.

Which workload is growing the fastest?

AI Inference, RAG, and KV Cache workloads are projected to expand at a 35.96% CAGR through 2031 because inference systems need larger low-latency memory pools.

Why are hyperscalers so important in this space?

Hyperscalers held 68.11% of end-user demand in 2025 and shape qualification, interoperability, and deployment templates for the broader ecosystem.

Which region leads adoption and which region is growing fastest?

North America held 63.52% of revenue in 2025, while Asia-Pacific is projected to post the fastest regional CAGR at 35.48% through 2031.

What gives leading companies an edge in this category?

The strongest advantages come from cross-platform interoperability, faster qualification, rack-scale fabric capability, and features such as compression, memory pooling, and support for newer form factors.

Page last updated on: