CXL Fabric Switch IC Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 52.81 Million |

| Market Size (2031) | USD 157.21 Million |

| Growth Rate (2026 - 2031) | 24.38% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

CXL Fabric Switch IC Market Analysis by Mordor Intelligence

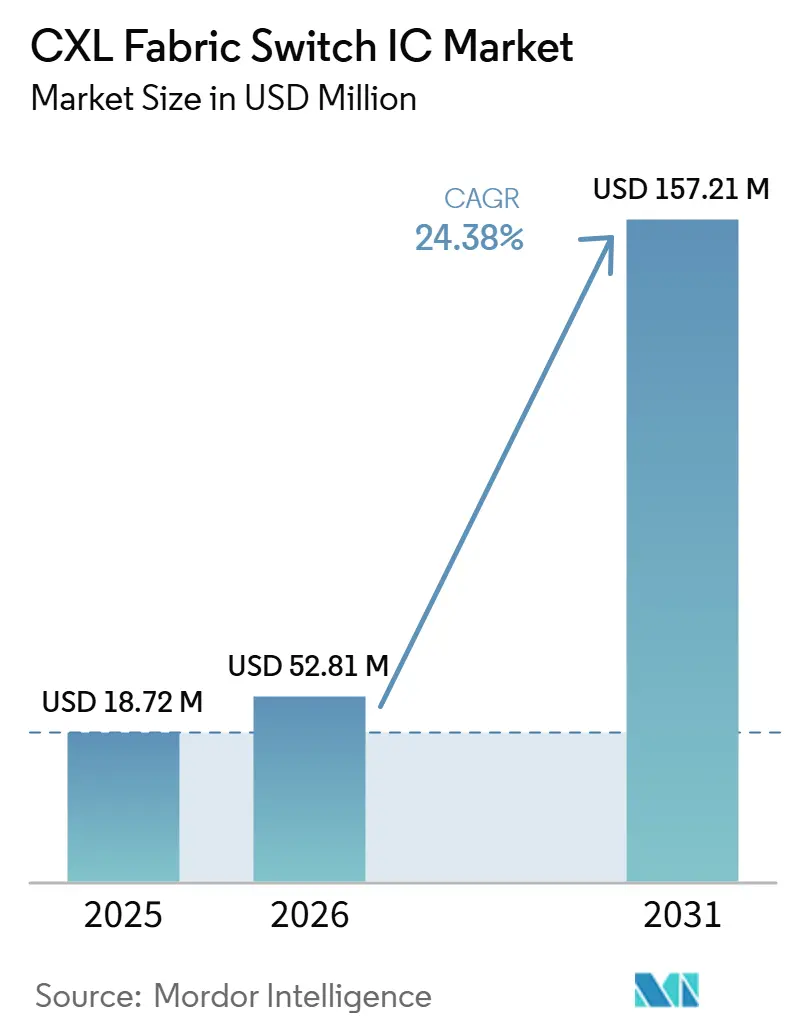

The CXL fabric switch IC market size is projected to be USD 18.72 million in 2025, USD 52.81 million in 2026, and reach USD 157.21 million by 2031, growing at a CAGR of 24.38% from 2026 to 2031. The sharp step-up into 2026 reflected hyperscaler qualification programs moving from evaluation into production deployment. The CXL fabric switch IC market is gaining momentum because AI infrastructure is being limited by memory access efficiency as much as by raw compute availability. The CXL fabric switch IC market also benefits from rack-scale memory pooling, which enables operators to share coherent memory across compute nodes rather than overprovisioning each server. Competition in the CXL fabric switch IC market remains focused on a small group of vendors with active product calendars, while buyers continue to compare open CXL fabrics with proprietary scale-up interconnect paths. The strongest opportunity for the CXL fabric switch IC market remains next-generation AI infrastructure, where memory efficiency, cluster utilization, and composable system design increasingly shape capital spending decisions.

Key Report Takeaways

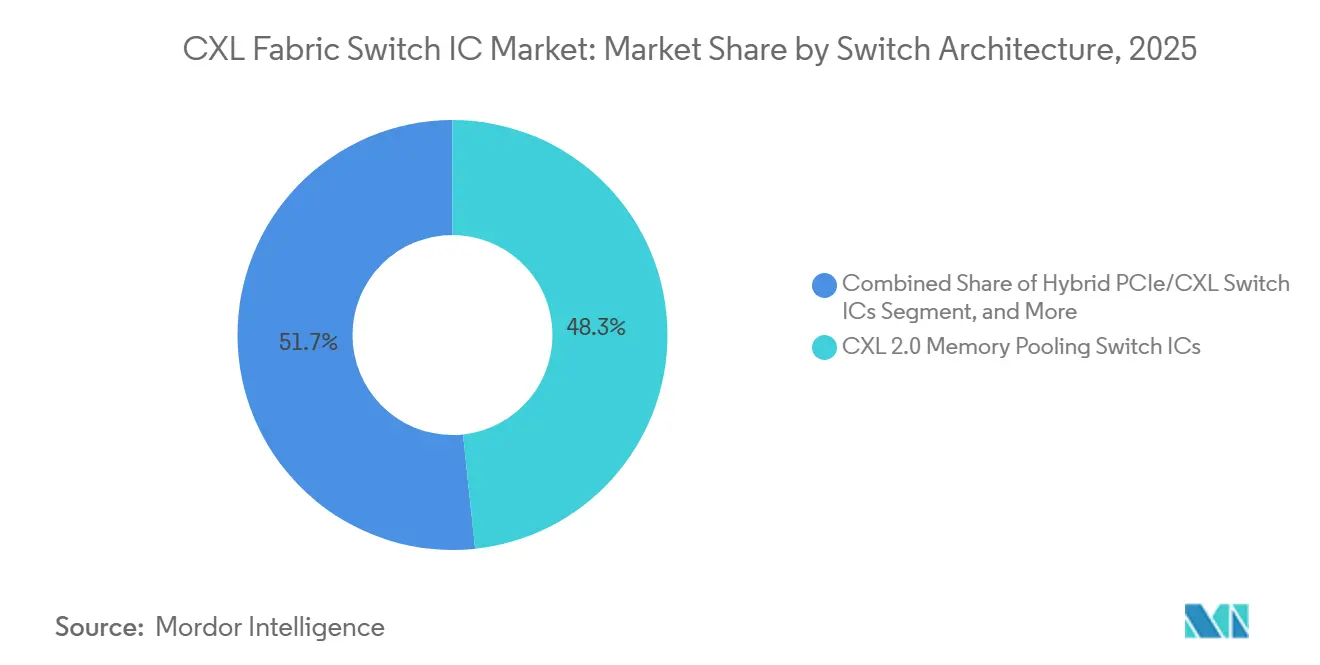

- By switch architecture, CXL 2.0 memory pooling switch ICs held 48.32% share of the CXL fabric switch IC market size in 2025, while CXL 3.x fabric switch ICs are projected to expand at 25.37% CAGR through 2031.

- By lane count, the 65-128-lane configuration held 51.64% of revenue in 2025, while 129-256-lane designs are projected to grow at 25.28% CAGR through 2031.

- By CXL specification, CXL 2.0 accounted for 79.13% share of the CXL fabric switch IC market size in 2025, while CXL 3.1 and CXL 3.2 are projected to expand at 25.18% CAGR through 2031.

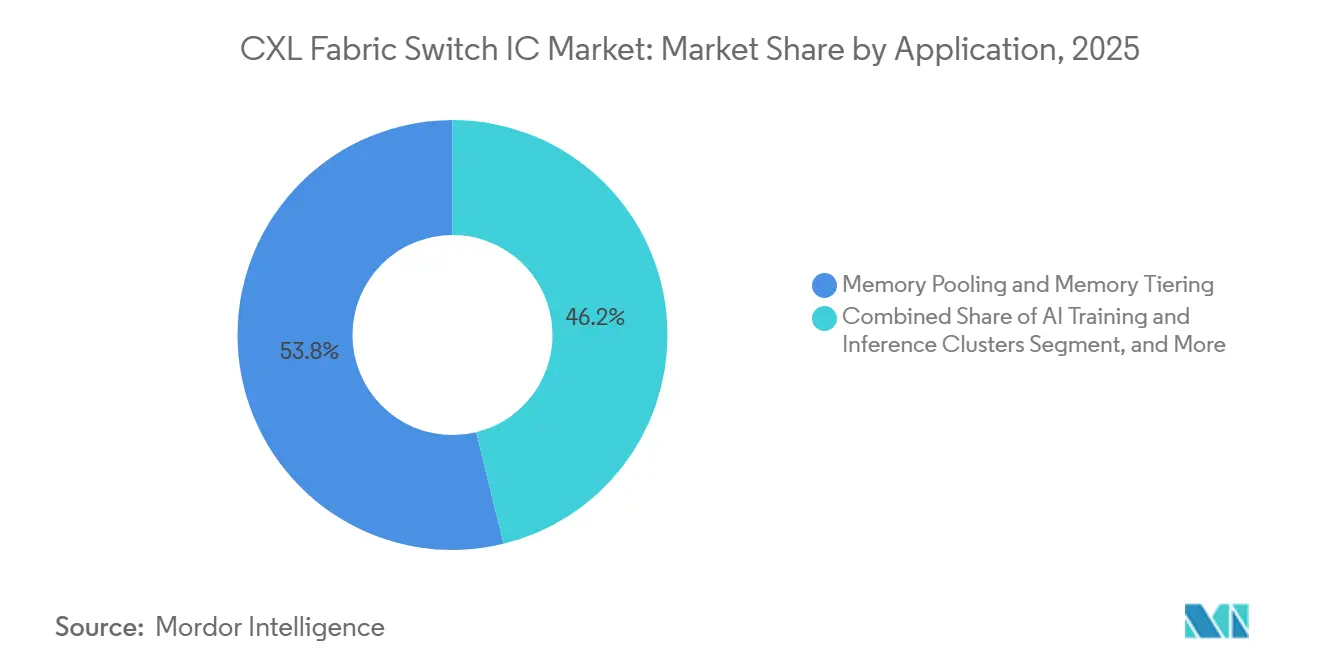

- By application, memory pooling and memory tiering accounted for 53.81% of the CXL fabric switch IC market size in 2025, while AI training and inference clusters are projected to expand at 25.77% CAGR through 2031.

- By customer type, hyperscalers and cloud service providers held 56.73% of the CXL fabric switch integrated circuit (IC) market share in 2025, while neocloud and GPU cloud providers are projected to grow at 27.62% CAGR through 2031.

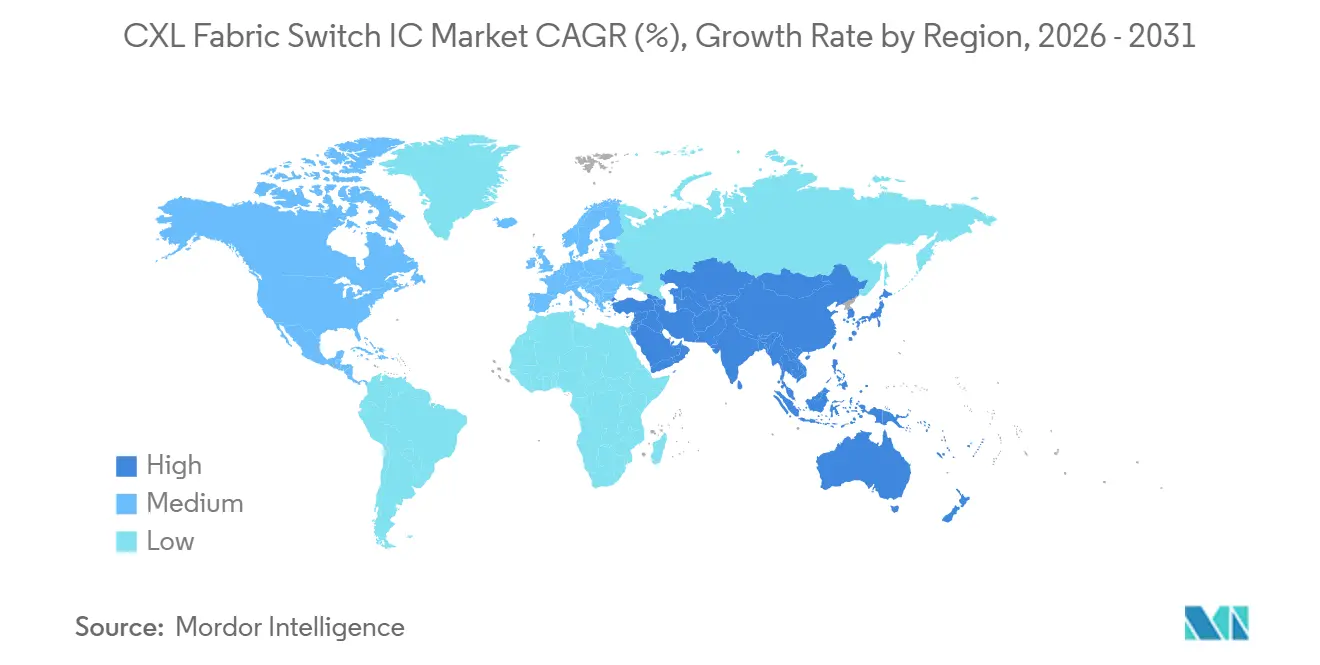

- By geography, North America accounted for 59.28% share of the CXL fabric switch IC market size in 2025, while Asia-Pacific is projected to expand at a 25.36% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global CXL Fabric Switch IC Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AI and LLM Memory Wall Pressure | +5.8% | Global, highest intensity in North America and Asia-Pacific | Short term (≤ 2 years) |

| Disaggregated and Composable Data Center Adoption | +4.2% | North America and Europe, with spillover to Asia-Pacific | Medium term (2-4 years) |

| Migration to CXL 3.x and Fabric-Scale Memory Pooling | +3.8% | Global, led by North America hyperscalers | Medium term (2-4 years) |

| Rack-Scale GPU and Accelerator Utilization Optimization | +3.0% | North America and Asia-Pacific, especially South Korea and Japan | Short term (≤ 2 years) |

| Port Density and Latency Advantages Over Proprietary Scaling Approaches | +2.0% | North America and Asia-Pacific | Long term (≥ 4 years) |

| Early Hyperscaler Qualification of CXL Switch Silicon | +1.5% | North America, with early gains in select Asia-Pacific hyperscalers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

AI and LLM Memory Wall Pressure is the Primary Demand Catalyst

GPU utilization during LLM inference decode phases can stall at 30%-40% when systems wait on high-bandwidth memory transfers rather than on compute resources. That bottleneck shifts buyer focus from raw accelerator counts toward memory access efficiency at the rack level. In the CXL fabric switch IC market, this matters because switch silicon allows coherent pooled memory to sit outside each server without breaking host access patterns. A March 2026 Cornell study reported that a near-DRAM-performance KV cache is served via CXL memory pools in the SGLang inference framework. That result broadens the addressable market for the CXL fabric switch IC beyond training clusters into production inference environments. As AI fleets scale, the CXL fabric switch IC market becomes more relevant wherever operators want higher utilization from expensive GPU assets.

Disaggregated and Composable Data Center Adoption Reshapes the Fabric Layer

Disaggregated infrastructure separates compute, memory, and storage resources, which turns the fabric layer into a core system choice rather than an optional attachment. Marvell introduced the Structera S 30260 in March 2026 for rack-level memory pooling across CPUs, GPUs, and accelerators, showing that merchant silicon suppliers are aligning their roadmaps with composable system design.[1]Marvell Technology, “Marvell Launches Next-Generation CXL Switch, Enabling Memory Pooling to Break Through the AI ‘Memory Wall’,” Marvell Technology, marvell.com Astera Labs said its Scorpio X-Series smart fabric switch was built for open memory-semantic scale-up networking and began shipping to leading hyperscalers in May 2026. SK hynix completed customer validation of its CXL 2.0-based CMM-DDR5 module in April 2025, supporting the broader move toward deployable, pooled-memory systems. The CXL fabric switch IC market, therefore, benefits when data center buyers seek memory resources that can be shared, reassigned, and expanded with less stranded capacity. That also widens the commercial path for the CXL fabric switch integrated circuit (IC) market from hyperscaler builds toward OEM-led and accelerator-led system architectures.

Migration to Cxl 3.x and Fabric-Scale Memory Pooling Opens the Multi-Rack Tier

Migration from CXL 2.0 to CXL 3.x is opening the next revenue layer of the CXL fabric-switch IC market, as larger fabrics require richer switching behavior. Panmnesia announced sample availability of its PCIe 6.0-CXL 3.2 fabric switch in November 2025 and described it as the first fabric switch silicon to fully implement CXL 3.2 with port-based routing support. Panmnesia then said in April 2026 that it had supplied pre-release silicon of its PCIe 6.4-CXL 3.2 fusion switch to early access partners. Marvell launched the Structera S 30260 260-lane CXL 3.0 switch in March 2026 with an aggregate bandwidth of up to 4 TB/s and customer sampling planned for Q3 2026. These steps show that suppliers are preparing the CXL fabric switch IC market for larger fabrics that go beyond early memory-expansion use cases. Vendors that secure design wins during this transition can influence server and rack architectures for multiple refresh cycles.

Rack-Scale GPU and Accelerator Utilization Optimization Raises Strategic Priority

Rack-scale AI clusters reward higher utilization because idle accelerators still consume capital and power even when model throughput falls short. Astera Labs said its Scorpio X-Series 320-lane smart fabric switch includes Hypercast in-network compute engines that accelerate AllReduce operations by up to 2x. The same announcement said the product had already started shipping to leading hyperscalers in May 2026, indicating that buyers now treat switch silicon as a performance lever in AI clusters. The CXL fabric switch IC market also benefits when in-network processing reduces host-side traffic and helps tighten synchronization across larger training jobs. This makes switch selection more strategic than in earlier PCIe expansion designs, where the device mostly served as a passive connectivity layer. As cluster size increases, the CXL fabric switch IC market should benefit from platforms that boost usable GPU output without requiring the same increase in local memory.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited Platform And Ecosystem Maturity At Scale | -4.8% | Global, highest friction in Asia-Pacific and Europe | Short term (≤ 2 years) |

| High Silicon, Packaging, And Validation Cost | -3.5% | Global | Medium term (2-4 years) |

| Interoperability And Qualification Complexity Across Vendors | -2.8% | Global, amplified in multi-vendor deployments | Medium term (2-4 years) |

| Competitive Pressure From Proprietary Interconnect Architectures | -2.2% | North America, with spillover to Asia-Pacific hyperscalers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Limited Platform and Ecosystem Maturity Constrain Near-Term Scale Deployment

The CXL fabric switch IC market still depends on the coordinated readiness of CPUs, memory modules, and switch silicon, which slows broad deployment even when one layer is technically ready. Marvell highlighted interoperability across major memory and CPU platforms in September 2025, showing that broad ecosystem validation remained a central commercial milestone rather than a routine checklist item. SK hynix also announced customer validation of its CXL 2.0-based CMM-DDR5 module in April 2025, reinforcing that memory-side qualification continued to shape deployment timing. Each qualification step can lengthen the path from sampling to volume orders, especially when hyperscalers test the full stack under workload-specific conditions. Smaller vendors face greater pressure because they depend on external platform roadmaps that they do not control. Until more servers, memory modules, and software stacks mature together, the CXL fabric switch IC market is likely to expand in uneven waves rather than along a straight adoption curve.

High Silicon, Packaging, and Validation Costs Limit New Entrants

High silicon and validation costs still limit the number of vendors that can compete aggressively in the CXL fabric switch IC market. Marvell's January 2026 agreement to acquire XConn Technologies for USD 540 million highlighted the value of established PCIe and CXL switch capabilities. That transaction also suggested that scale, engineering depth, and product readiness can outweigh the standalone path for smaller specialists. Panmnesia said in April 2026 that it had secured pre-release engagement with early access partners while pushing toward mass production, which underlines how long new entrants may need to fund development before revenue broadens.[2]Panmnesia, “Panmnesia Supplies Pre-Release Silicon of PCIe 6.4-CXL 3.2 Fusion Switch,” Panmnesia, panmnesia.com Advanced lane counts, tight latency targets, and repeated customer validation programs all add to the commercial burden. The result is a CXL fabric switch IC market in which technical promise alone does not guarantee sustained participation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Switch Architecture: Cxl 2.0 Leads While 3.x Defines The Next Revenue Curve

CXL 2.0 memory pooling switch ICs held 48.32% of the CXL fabric switch IC market size in 2025, while CXL 3.x fabric switch ICs are projected to expand at 25.37% CAGR through 2031. That 2025 lead reflected the installed base of Intel Sapphire Rapids and AMD Genoa and Bergamo server platforms that already exposed CXL 2.0 host interfaces. Hybrid PCIe and CXL devices still carry strategic value because many buyers want flexibility during the transition from memory expansion toward fuller fabric deployment. Marvell's March 2026 launch paired a 260-lane CXL 3.0 switch with a pin-compatible 260-lane PCIe 6.0 switch, which supports that transitional design logic in a single hardware footprint. AI scale-up memory-semantic designs and custom or semi-custom switch ICs remain early-stage categories, but they matter because a few large operators want tighter control over memory subsystem efficiency.

The architecture shift is not simply a version update, because it changes the topology from single-level switching toward multi-hop fabric behavior. Panmnesia said its fabric-switch silicon fully implements CXL 3.2 with port-based routing support, directly addressing the routing demands of larger fabrics. That matters for the CXL fabric switch IC market because current CXL 2.0 devices in production cannot be turned into full CXL 3.x multi-hop fabrics solely through software changes. As a result, early adopters of first-generation CXL are still likely to return to the market for a second procurement cycle. The long-term path also leaves room for custom programs that allow hyperscalers to differentiate on memory behavior rather than on switch count alone.

By Lane Count: Higher-Density Configurations Support Rack-Scale Economics

The 65-128-lane configuration accounted for 51.64% of revenue in 2025, while the 129-256-lane segment is projected to grow at a 25.28% CAGR through 2031. The 65-128-lane range aligns with current hyperscaler rack designs that connect 8-16 accelerator nodes via a single switch tier. Up-to-32-lane and 33-64-lane products still serve enterprise data centers, edge deployments, and pilot programs where cost and power remain central buying factors. At the upper end, Astera Labs said its Scorpio X-Series smart fabric switch shipped with 320 lanes, placing it above-256-lane products at the performance frontier of AI scale-up clusters. The commercial direction of the CXL fabric switch IC market, therefore, favors denser fabrics, where operators want fewer hops and broader node reach.

The lane-count mix is shifting because larger AI clusters benefit from higher-radix topologies that reduce latency for training traffic. Astera Labs said its Scorpio P-Series PCIe switches accounted for 10% of total company revenue in 2025, demonstrating that high-performance switching already carried meaningful commercial weight before the X-Series ramp. That revenue signal encourages switch vendors to keep expanding density rather than treating high-lane-count devices as niche products. Neocloud and GPU cloud providers are also standardizing rack reference designs around denser connectivity layers, which should pull more demand into the 129-256-lane range. Lower-lane devices should still keep volume relevance where practical deployment economics matter more than the largest fabric ambition.

By CXL Specification: CXL 2.0 Dominates While 3.1 and 3.2 Set The Growth Pace

CXL 2.0 accounted for 79.13% of revenue in 2025, while CXL 3.1 and CXL 3.2 are projected to expand at 25.18% CAGR through 2031. That 2025 concentration reflected the maturity of host platforms that exposed CXL 2.0 natively across current server generations. CXL 3.0 occupies a bridge position because it extends switching capability beyond 2.0 while sitting ahead of full 3.2-scale routing maturity. Marvell's March 2026 launch of a 260-lane CXL 3.0 switch shows that suppliers are actively addressing this bridge stage rather than waiting for the entire ecosystem to move at once. Panmnesia's November 2025 sample announcement and April 2026 pre-release program then pushed the CXL fabric switch IC market further toward full 3.2 implementation.

Specification shifts matter because memory-side readiness and switch-side capability must move together before large deployments can scale. SK hynix completed customer validation of its CXL 2.0-based CMM-DDR5 module in April 2025, which supported the current generation of deployments already tied to 2.0 ecosystems. The CXL fabric switch integrated circuit (IC) market is therefore likely to see uneven adoption across 3.x revisions until a wider set of host platforms and modules matures together. Suppliers that are already positioned for 3.2 can use that gap to pursue early design wins while parts of the broader supply chain catch up. Interoperability work is likely to remain central throughout this transition, as cross-platform certification still shapes actual deployment timing.

By Application: Memory Pooling Leads While AI Clusters Expand Fastest

Memory pooling and memory tiering accounted for 53.81% of the CXL fabric switch IC market in 2025, while AI training and inference clusters are projected to expand at a 25.77% CAGR through 2031. That lead came from the need to improve DRAM utilization across mixed-workload server fleets where static allocation still leaves meaningful stranded capacity. A March 2026 Cornell study reported that a near-DRAM-performance KV cache is served via CXL memory pools in the SGLang inference framework. That finding supports a stronger growth path for AI clusters because inference workloads can benefit from externalized memory without the same penalty buyers normally expect from higher memory tiers. Composable infrastructure, memory sharing, and dynamic capacity allocation form the next adoption layer for the CXL fabric switch IC market as operators seek greater software-defined control over resources.

HPC and scientific computing should contribute on a longer timeline because public-sector and laboratory procurement cycles move more slowly than hyperscale deployments. Database and in-memory workloads can benefit from CXL-attached DRAM, which provides a lower-latency tier than NVMe-based storage for less frequently accessed data pages. Other data center workloads are likely to adopt more gradually because they are less tightly constrained by memory bandwidth economics. The CXL fabric switch IC market, therefore, expands first where memory imbalance is already a visible cost problem rather than a theoretical architecture issue. Early hyperscaler deployment patterns are likely to influence how quickly broader enterprise application groups follow.

By Customer Type: Hyperscalers Anchor Revenue While Neoclouds Grow Fastest

Hyperscalers and cloud service providers held 56.73% of the CXL fabric switch IC market share in 2025, while neocloud and GPU cloud providers are projected to expand at 27.62% CAGR through 2031. Hyperscalers remain the main qualification gateway because their server roadmaps, software stacks, and procurement scale shape which switch devices reach volume shipments. Neocloud operators are growing faster because their homogeneous GPU fleets reduce the integration friction that slows legacy enterprise environments. OEMs and ODMs remain important because validated system designs can shorten deployment time for buyers who do not want to qualify every component independently. AI server and accelerator vendors are also emerging as a separate procurement tier, especially where memory disaggregation is being planned alongside accelerator-heavy builds.

Enterprise data centers still move more slowly because refresh cycles and incumbent procurement structures limit the pace of platform shifts. HPC and research organizations evaluate CXL fabric over longer public funding and system-integration timelines. Telecom operators represent an earlier-stage opportunity where shared memory pools can support more disaggregated edge compute environments. Panmnesia said in April 2026 that it had supplied pre-release silicon to early access partners and was targeting mass production in H2 2026, which supports future system design activity beyond the largest cloud accounts. The customer mix keeps the CXL fabric switch IC market anchored in hyperscale demand while still widening the future channel base.

Geography Analysis

North America accounted for 59.28% of global revenue in 2025, making it the largest regional market for CXL fabric switch ICs. That lead reflected the concentration of major hyperscalers and several of the most commercially active switch silicon suppliers in the same region. Astera Labs reported Q1 2026 revenue of USD 308.4 million, up 93% year over year, with its Scorpio switch families acting as the primary growth engine.[3]Astera Labs, “Astera Labs Reports First Quarter 2026 Financial Results,” Astera Labs, asteralabs.com That commercial momentum shows that North American qualification activity is already converting into meaningful shipment growth. Canada and Mexico add smaller but relevant infrastructure channels as regional data center capacity broadens.

Asia-Pacific is projected to expand at a 25.36% CAGR through 2031, making it the fastest-growing regional segment of the CXL fabric switch IC market. South Korea plays a dual role, combining memory ecosystem development with direct demand for CXL-enabled infrastructure. SK hynix validated its CXL 2.0-based CMM-DDR5 module in April 2025, and Panmnesia said in April 2026 that it had supplied pre-release CXL 3.2 switch silicon to early access partners. That proximity between memory and switch development can shorten ecosystem learning cycles and speed practical deployment readiness. China, Japan, and Southeast Asia add further demand through AI infrastructure buildouts and public technology programs.

Europe, South America, and the Middle East and Africa held smaller positions in 2026, but each followed a different adoption path inside the CXL fabric switch IC market. Europe is tied more closely to enterprise AI upgrades and public HPC programs. South America is likely to track enterprise server refresh cycles more than hyperscale procurement in the near term. The Middle East and Africa offer greenfield opportunities for new AI facilities to move directly toward later-generation CXL designs if ecosystem readiness improves on schedule.

Competitive Landscape

The CXL fabric switch IC market remained moderately concentrated in 2026, with Marvell Technology and Astera Labs holding the largest commercial footprints. Marvell announced a definitive agreement in January 2026 to acquire XConn Technologies for USD 540 million in cash and stock. That move added PCIe and CXL switch capability and also strengthened Marvell's broader scale-up interconnect engineering base. Astera Labs reported full-year 2025 revenue of USD 852.5 million, up 115% year over year, with Scorpio PCIe switch ramps as a primary contributor.[4]Astera Labs, “Astera Labs Reports Fourth Quarter and Full Year 2025 Financial Results,” Astera Labs, asteralabs.com Those two companies, therefore, entered 2026 with the clearest commercial momentum in the CXL fabric-switch IC market.

Panmnesia stood out as the most technically differentiated challenger because it pursued full CXL 3.2 implementation with port-based routing support. The November 2025 sample announcement and April 2026 pre-release silicon program showed a faster push on advanced specification support than most of the field. The broader ecosystem also includes IP suppliers, memory vendors, and system integrators, but merchant-switch silicon remains concentrated among a smaller group of vendors. Competitive advantage in the CXL fabric switch IC market increasingly comes from protocol depth, validation progress, and alignment with hyperscaler roadmaps. That keeps barriers high for late entrants even when demand expands quickly.

White-space remains in in-network compute, multi-protocol convergence, and software-led composable fabric control. Astera's in-network compute feature set and Marvell's pin-compatible switch strategy show how vendors are broadening the role of the switch beyond simple port aggregation. Panmnesia's early-access path gives it a chance to influence future architecture choices if volume production follows planned timelines. The CXL fabric switch integrated circuit (IC) market still leaves room for challengers, but durable leadership will depend on shipping credibility, ecosystem alignment, and repeat qualification wins.

CXL Fabric Switch IC Industry Leaders

Astera Labs, Inc.

Montage Technology Co., Ltd.

Microchip Technology Incorporated

Rambus Inc.

Marvell Technology, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Astera Labs announced and began shipping its Scorpio X-Series 320-lane smart fabric switch to leading hyperscalers. The product integrated Hypercast in-network compute engines that accelerated AllReduce collective operations by up to 2x, with a planned volume production ramp for H2 2026.

- April 2026: Panmnesia supplied pre-release silicon of its PCIe 6.4-CXL 3.2 fusion switch to early access partners. The company said mass production was planned for H2 2026.

- March 2026: Marvell Technology launched the Structera S 30260 260-lane CXL 3.0 switch and the Structera S 60260 260-lane PCIe 6.0 switch. The Structera S 30260 delivered aggregate bandwidth of up to 4 TB/s and enabled rack-level memory pooling across CPUs, GPUs, and accelerators, with customer sampling expected in Q3 2026.

- January 2026: Marvell Technology announced a definitive agreement to acquire XConn Technologies for USD 540 million in cash and stock. XConn's PCIe 5.0 and CXL 2.0 switches were in production at the time of announcement, while PCIe 6.0 and CXL 3.1 switches were in sampling.

Global CXL Fabric Switch IC Market Report Scope

The CXL Fabric Switch IC market comprises semiconductor switch integrated circuits (ICs) that enable Compute Express Link (CXL)-based memory pooling, sharing, and fabric connectivity across servers, accelerators, and composable data center infrastructures. These ICs facilitate coherent communication between CPUs, GPUs, memory devices, and other CXL-enabled endpoints, improving resource utilization and scalability for AI and high-performance computing (HPC) workloads. The market includes CXL 2.0 memory-pooling switch ICs, CXL 3.x fabric-switch ICs, hybrid PCIe/CXL switch ICs, AI-scale-up memory-semantic fabric-switch ICs, and custom or semi-custom CXL fabric-switch ICs. It covers solutions across multiple lane-count configurations and CXL specification generations, supporting applications such as memory pooling, composable infrastructure, AI training and inference, HPC, databases, analytics, and other data center workloads. The market serves hyperscalers, cloud providers, server OEMs and ODMs, AI system vendors, enterprise data centers, research organizations, and telecom operators.

The CXL Fabric Switch IC Market Report is Segmented by Switch Architecture (CXL 2.0 Memory Pooling Switch ICs, CXL 3.x Fabric Switch ICs, Hybrid PCIe/CXL Switch ICs, AI Scale-Up Memory-Semantic Fabric Switch ICs, and Custom or Semi-Custom CXL Fabric Switch ICs), Lane Count (Up to 32 Lanes, 33-64 Lanes, 65-128 Lanes, 129-256 Lanes, and Above 256 Lanes), CXL Specification (CXL 2.0, CXL 3.0, CXL 3.1 and CXL 3.2, and CXL 4.0), Application (Memory Pooling and Memory Tiering, Memory Sharing and Dynamic Capacity Allocation, Composable and Disaggregated Infrastructure, AI Training and Inference Clusters, HPC and Scientific Computing, Database, Analytics, and In-Memory Computing, and Other Data-Center Workloads), Customer Type (Hyperscalers and Cloud Service Providers, Neocloud and GPU Cloud Providers, Server OEMs and ODMs, AI Server and Accelerator System Vendors, Enterprise Data-Center Operators, HPC, Research, and Government Organizations, and Telecom Operators and Edge Infrastructure Providers), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| CXL 2.0 Memory Pooling Switch ICs |

| CXL 3.x Fabric Switch ICs |

| Hybrid PCIe/CXL Switch ICs |

| AI Scale-Up Memory-Semantic Fabric Switch ICs |

| Custom or Semi-Custom CXL Fabric Switch ICs |

| Up to 32 Lanes |

| 33-64 Lanes |

| 65-128 Lanes |

| 129-256 Lanes |

| Above 256 Lanes |

| CXL 2.0 |

| CXL 3.0 |

| CXL 3.1 and CXL 3.2 |

| CXL 4.0 |

| Memory Pooling and Memory Tiering |

| Memory Sharing and Dynamic Capacity Allocation |

| Composable and Disaggregated Infrastructure |

| AI Training and Inference Clusters |

| HPC and Scientific Computing |

| Database, Analytics, and In-Memory Computing |

| Other Data-Center Workloads |

| Hyperscalers and Cloud Service Providers |

| Neocloud and GPU Cloud Providers |

| Server OEMs and ODMs |

| AI Server and Accelerator System Vendors |

| Enterprise Data-Center Operators |

| HPC, Research, and Government Organizations |

| Telecom Operators and Edge Infrastructure Providers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Southeast Asia | |

| Rest of Asia-Pacific | |

| South America | |

| Middle East and Africa |

| By Switch Architecture | CXL 2.0 Memory Pooling Switch ICs | |

| CXL 3.x Fabric Switch ICs | ||

| Hybrid PCIe/CXL Switch ICs | ||

| AI Scale-Up Memory-Semantic Fabric Switch ICs | ||

| Custom or Semi-Custom CXL Fabric Switch ICs | ||

| By Lane Count | Up to 32 Lanes | |

| 33-64 Lanes | ||

| 65-128 Lanes | ||

| 129-256 Lanes | ||

| Above 256 Lanes | ||

| By CXL Specification | CXL 2.0 | |

| CXL 3.0 | ||

| CXL 3.1 and CXL 3.2 | ||

| CXL 4.0 | ||

| By Application | Memory Pooling and Memory Tiering | |

| Memory Sharing and Dynamic Capacity Allocation | ||

| Composable and Disaggregated Infrastructure | ||

| AI Training and Inference Clusters | ||

| HPC and Scientific Computing | ||

| Database, Analytics, and In-Memory Computing | ||

| Other Data-Center Workloads | ||

| By Customer Type | Hyperscalers and Cloud Service Providers | |

| Neocloud and GPU Cloud Providers | ||

| Server OEMs and ODMs | ||

| AI Server and Accelerator System Vendors | ||

| Enterprise Data-Center Operators | ||

| HPC, Research, and Government Organizations | ||

| Telecom Operators and Edge Infrastructure Providers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Southeast Asia | ||

| Rest of Asia-Pacific | ||

| South America | ||

| Middle East and Africa | ||

Key Questions Answered in the Report

What is the size of the CXL fabric switch IC market?

The CXL fabric switch IC market was valued at USD 18.72 million in 2025, is projected at USD 52.81 million in 2026, and is forecast to reach USD 157.21 million by 2031 at a 24.38% CAGR.

Which application is generating the most revenue in CXL fabric switch ICs?

Memory pooling and memory tiering led with 53.81% of revenue in 2025, reflecting the immediate value of better DRAM utilization across server fleets.

Which customer group is expanding the fastest in this space?

Neocloud and GPU cloud providers are projected to grow at 27.62% CAGR through 2031, ahead of other customer groups, because their homogeneous accelerator fleets are easier to design around pooled memory.

Why are CXL 3.x switches drawing more attention than CXL 2.0 devices?

CXL 3.x switches support more advanced fabric behavior for larger multi-host and multi-rack designs, while CXL 2.0 still dominates today's installed base with 79.13% of 2025 revenue.

Which region leads current demand and which region is growing fastest?

North America led with 59.28% of revenue in 2025, while Asia-Pacific is projected to grow the fastest at 25.36% CAGR through 2031.

What is the main challenge slowing broader adoption?

The main challenge is ecosystem readiness across CPUs, memory modules, and switch silicon, combined with high validation costs that can delay the move from sampling into volume deployment.

Page last updated on: