Customer Journey Orchestration Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

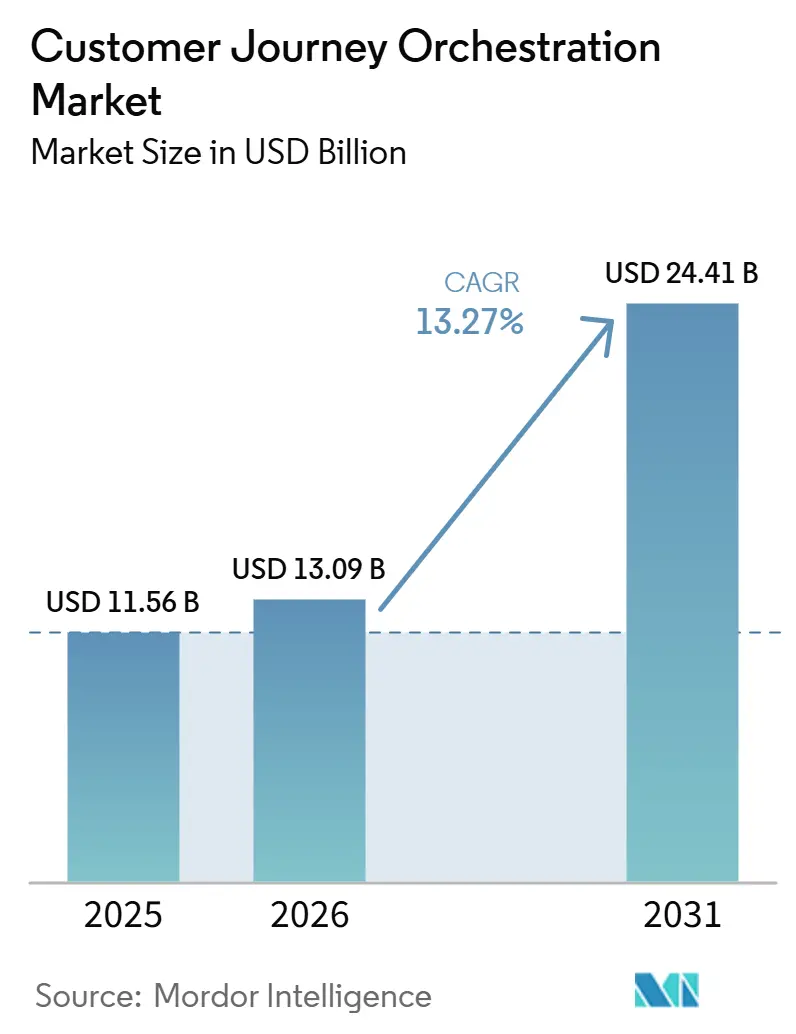

| Market Size (2026) | USD 13.09 Billion |

| Market Size (2031) | USD 24.41 Billion |

| Growth Rate (2026 - 2031) | 13.27% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Customer Journey Orchestration Market Analysis by Mordor Intelligence

The customer journey orchestration market size is projected to be USD 11.56 billion in 2025, USD 13.09 billion in 2026, and reach USD 24.41 billion by 2031, growing at a CAGR of 13.27% from 2026 to 2031. The current growth path of the customer journey orchestration market is shaped by the move from batch campaign execution to real-time interaction management across marketing, service, and commerce environments. Demand is also rising because enterprises want AI systems that can decide the next action in the moment instead of relying on fixed journey paths built in advance. Cloud-based experience platforms are making that shift easier because they reduce infrastructure effort and help teams work from a more unified customer view. At the same time, data residency, consent controls, and auditability are moving closer to the center of buying decisions, especially in regulated sectors. Competition in the customer journey orchestration market now reflects that split, with large platform vendors using installed ecosystems to defend share while AI-native vendors compete on speed, flexibility, and narrower use cases.

Key Report Takeaways

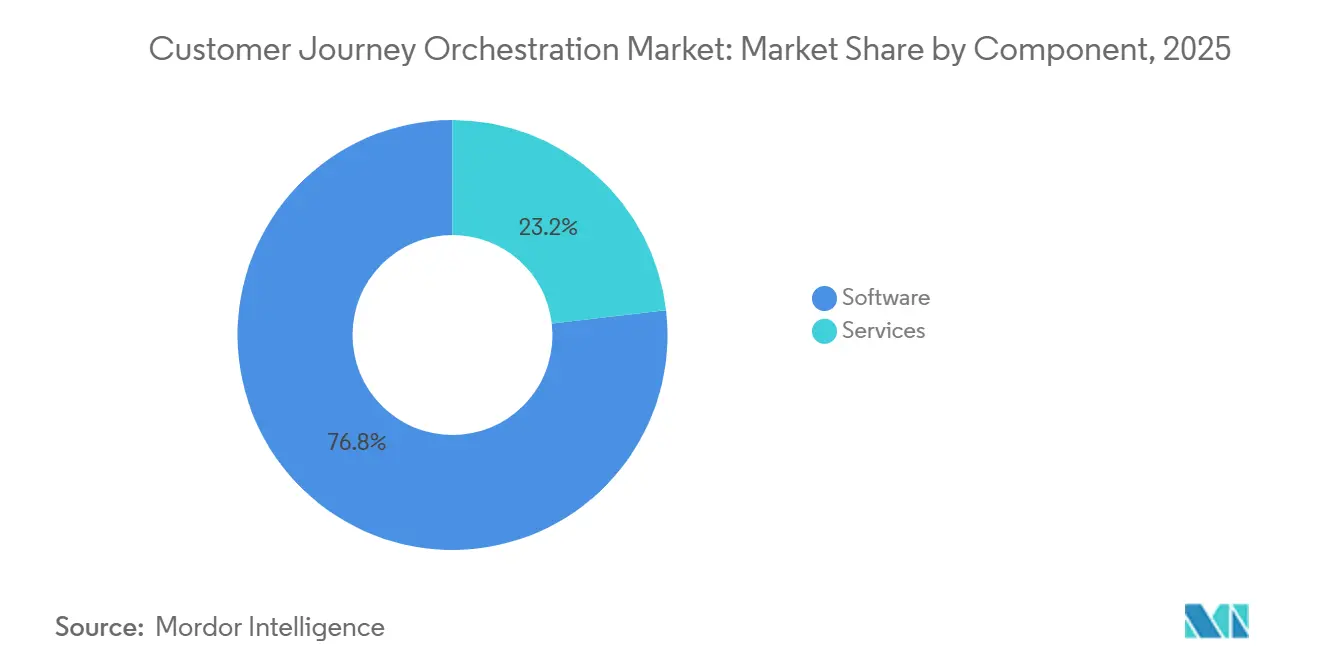

- By component, software held 76.84% share in the customer journey orchestration market in 2025, while services are projected to expand at 15.92% CAGR through 2031.

- By deployment mode, cloud accounted for 61.63% share of the customer journey orchestration market size in 2025, while on-premises is projected to grow at 15.37% CAGR through 2031.

- By application, customer journey design and experience management accounted for 27.48% share of the customer journey orchestration market size in 2025, while journey optimization is projected to advance at 17.84% CAGR through 2031.

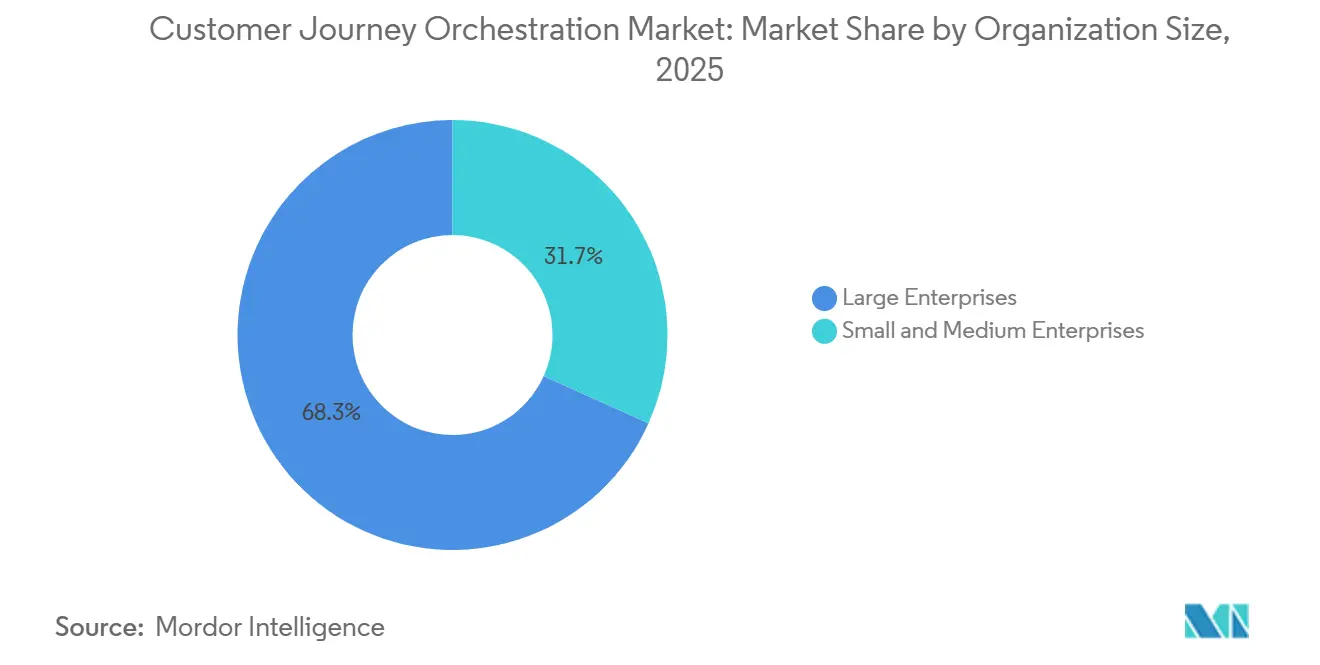

- By organization size, large enterprises held 68.26% share in 2025, while small and medium enterprises are projected to expand at 16.58% CAGR through 2031.

- By end user industry, BFSI held 24.81% share in 2025, while healthcare is projected to grow at 17.21% CAGR through 2031.

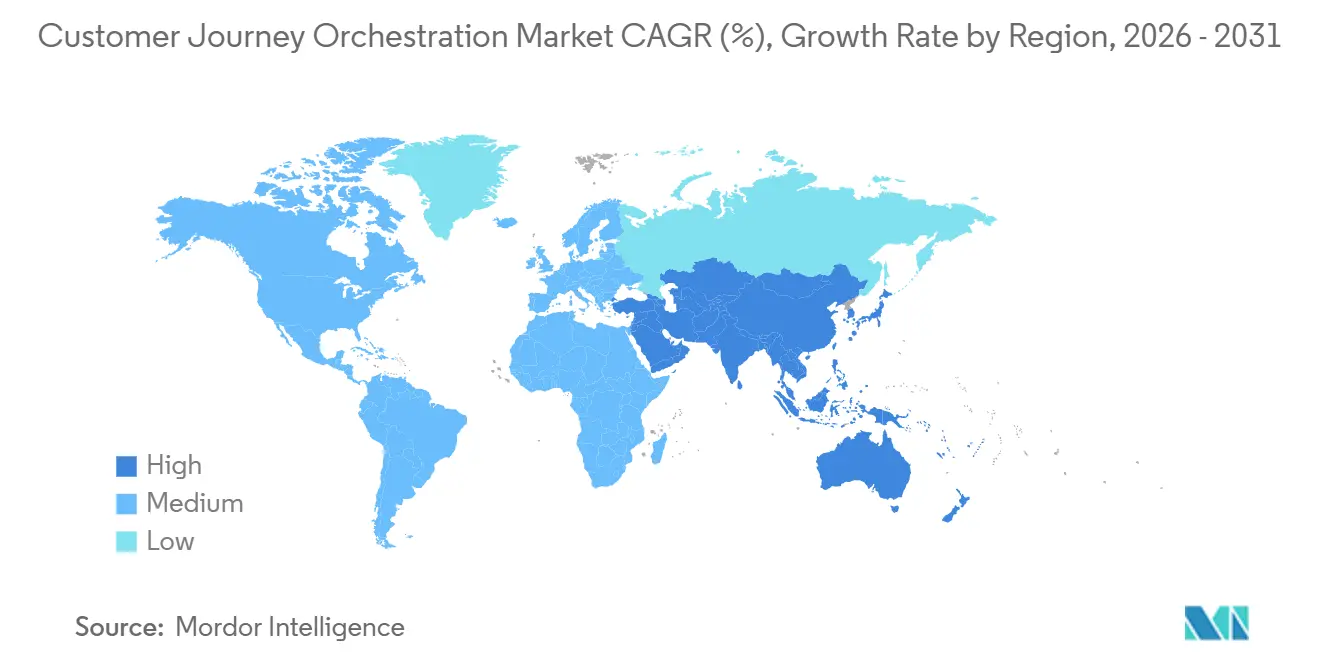

- By geography, North America held 39.18% of the customer journey orchestration market share in 2025, while Asia-Pacific is projected to grow at 18.43% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Customer Journey Orchestration Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising Demand for Real-Time Personalized Journeys | +3.5% | Global, with intensity in North America, Europe, and Asia-Pacific core | Short term (≤ 2 years) |

| Growing Need to Unify Fragmented Customer Data Across Touchpoints | +2.8% | Global, most acute in North America and the European Union where CDP investment is highest | Medium term (2-4 years) |

| Expansion of AI-Driven Decisioning and Next-Best-Action Automation | +2.3% | North America and the European Union core, with spillover to Asia-Pacific and Middle East and Africa | Medium term (2-4 years) |

| Increasing Adoption of Cloud-Native Customer Experience Stacks | +1.9% | Global, strongest in North America, the United Kingdom, and Australia | Short term (≤ 2 years) |

| Rising Pressure to Improve Conversion in High-Consideration Digital Journeys | +1.4% | North America, Europe, and developed Asia-Pacific including Japan, South Korea, and Australia | Short term (≤ 2 years) |

| Lower-Lift Orchestration Use Cases Emerging in Mid-Market Enterprises | +1.1% | Global, with early adoption gains in North America, DACH, and Southeast Asia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Real-Time Personalized Journeys

Real-time personalization is moving from an optional feature to a core operating requirement in the customer journey orchestration market because static campaigns are not meeting rising customer expectations across digital channels. Enterprises increasingly want systems that can react to current behavior, recent purchases, channel context, and service history within the same interaction window. Adobe reinforced this shift in September 2025 when it announced the general availability of AI agents for customer experience transformation, including Journey Agent in Adobe Journey Optimizer that creates and orchestrates journeys across web, mobile, app, and email based on defined goals. Twilio pushed the same direction in May 2026 with Conversation Orchestrator, Conversation Memory, and Conversation Intelligence, all built to preserve customer context and support coordinated AI and human interactions across channels.[1]Twilio, “Infrastructure for the Agentic Era, Everything We Launched at SIGNAL 2026,” Twilio Blog, twilio.com As more vendors center their product roadmaps on real-time orchestration, the customer journey orchestration market is moving toward continuous engagement models rather than campaign-by-campaign execution.

Growing Need to Unify Fragmented Customer Data Across Touchpoints

Fragmented customer data remains one of the clearest barriers to useful orchestration in the customer journey orchestration market because signals often sit across separate CRM, commerce, service, and analytics systems. When those records do not connect, journey logic becomes incomplete, and the next action is based on partial context instead of the full relationship. Adobe addressed this problem in March 2025 through the launch of Experience Platform Agent Orchestrator, supported by partnerships with Acxiom, AWS, Genesys, IBM, Microsoft, SAP, ServiceNow, and Workday to enable coordinated execution across customer service, enterprise resource planning, collaboration, and data management environments. That vendor behavior shows that buyers are not only evaluating decisioning quality, but they are also testing how well a platform can sit across the existing enterprise stack. This keeps ecosystem breadth close to the center of competition in the customer journey orchestration market, especially in large accounts with multiple legacy platforms.

Expansion of AI-Driven Decisioning and Next-Best-Action Automation

The customer journey orchestration market is also advancing because rule-based branching is giving way to systems that evaluate context in real time and decide the next best action across channels. This matters because fixed decision trees often break when customer behavior changes faster than journey designs can be updated. Oracle made that direction explicit in April 2026 with Fusion Agentic Applications for CX, including a Sales Command Center for continuous next-best-action execution and a Marketing Command Center that launches the next best growth program using unified enterprise signals.[2]Oracle, “Oracle Introduces Fusion Agentic Applications for Customer Experience,” Oracle News, oracle.com Braze moved on a similar path in April 2026 with BrazeAI Operator and BrazeAI Agent Console, both designed to support more autonomous campaign creation, personalization, and delivery. As AI decisioning becomes more embedded, the customer journey orchestration market is shifting toward platforms that can combine policy controls, customer context, and execution speed inside one governed workflow.

Increasing Adoption of Cloud-Native Customer Experience Stacks

Cloud-native deployment keeps expanding in the customer journey orchestration market because it reduces infrastructure effort and makes product updates easier to absorb across large user bases. Subscription pricing also lowers the barrier to entry for buyers who want to pilot orchestration without a long hardware or data center cycle. Adobe supported this approach in April 2026 with CX Enterprise, an end-to-end agentic AI system built to work across Adobe Experience Cloud and major cloud and model partners, including AWS, Google Cloud, IBM, Microsoft, NVIDIA, Anthropic, and OpenAI. Braze added a related signal through EU hosting on Google Cloud for BrazeAI Decisioning Studio, showing how cloud expansion is now being shaped by regional compliance requirements as much as by scale efficiency. This mix of agility and controlled deployment continues to support cloud-led growth in the customer journey orchestration market, even while regulated buyers keep some workloads closer to their own governed environments.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Integration Complexity With Legacy CRM, CDP, and Marketing Systems | -2.6% | Global, most severe in North America and Europe where legacy system density is highest | Long term (≥ 4 years) |

| Data Privacy, Consent, and Governance Constraints | -2.1% | European Union under GDPR, North America under CCPA and CPRA, and Asia-Pacific under PIPL, APPI, and PDPA | Long term (≥ 4 years) |

| Difficulty Proving Incremental ROI Across Siloed Business Units | -1.5% | Global | Medium term (2-4 years) |

| Shortage of Specialized Journey Design and Analytics Talent | -0.9% | Global, acute in emerging Asia-Pacific markets and South America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Integration Complexity with Legacy CRM, CDP, and Marketing Systems

Integration complexity is still a meaningful brake on the customer journey orchestration market because many large organizations are trying to connect new orchestration layers to older CRM, marketing, commerce, and service systems. Those environments were often not designed to emit customer signals in real time, which slows implementation and keeps activation fragmented. The partner-heavy structure of Adobe Experience Platform Agent Orchestrator shows how much value buyers place on certified integrations across customer service, enterprise applications, collaboration tools, and data environments. SAP and Google Cloud also expanded their partnership in April 2026 to support multi-agent AI across SAP Engagement Cloud, SAP CX, Joule, and Gemini Enterprise, which reflects the wider market need to bridge established enterprise systems with newer orchestration and AI workflows. Until integration becomes simpler across those environments, the customer journey orchestration market will continue to face longer enterprise sales cycles and more selective rollouts in complex accounts.

Data Privacy, Consent, and Governance Constraints

Privacy and consent rules are reshaping the customer journey orchestration market because personalization quality depends on the lawful collection, storage, and activation of customer data. Buyers in regulated sectors now want journey execution systems that can prove where data came from, how it is being used, and whether consent rules were honored at each step. PossibleNOW responded to that need in July 2025 by expanding its MyPreferences Decision Service into Salesforce Marketing Cloud through a native embed in Journey Builder for real-time consent, preference, and zero-party data management. Braze added another compliance signal in April 2026 by launching EU hosting on Google Cloud for BrazeAI Decisioning Studio so that real-time customer decisioning data processed by the tool no longer leaves the European Union region. As consent and residency rules become harder to separate from day-to-day execution, the customer journey orchestration market is rewarding vendors that embed governance into the platform rather than treating it as a later add-on.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Platforms Anchor Revenue While Services Accelerate

Software held 76.84% share in the customer journey orchestration market in 2025, which reflects the platform-led nature of enterprise spending in this category. Buyers continue to allocate most value to journey builders, real-time decisioning engines, customer data connectors, and the core orchestration layer that sits across channels. This also shows that enterprises still prefer reusable systems of engagement over one-off custom builds when they modernize customer experience operations. The installed software base matters because recurring platform revenue gives vendors more room to fund AI features, compliance controls, and deeper ecosystem integration.

Services are projected to grow at 15.92% CAGR through 2031, making them the faster-moving component as deployment and governance needs become harder to manage with internal teams alone. That expansion is tied to implementation, system integration, managed operations, training, and optimization work that follows platform adoption across more business units. The customer journey orchestration market is seeing a broader shift here because AI-enabled deployment requires new operating practices around model oversight, journey testing, and content management. As a result, services are growing not because software is weakening, but because enterprise buyers increasingly need outside support to activate software value at scale.

By Deployment Mode: Cloud Leads But Regulated Demand Reshapes the Mix

Cloud accounted for 61.63% share of the customer journey orchestration market size in 2025, which shows that most deployments still favor scalable and centrally updated environments. Enterprises value the lower infrastructure burden, the faster release cycle, and the easier access to prebuilt AI features that cloud deployment usually provides. This keeps cloud at the center of new rollouts, especially for companies that want faster time to value across marketing, service, and commerce teams. The current structure of the customer journey orchestration market, therefore, still leans toward cloud as the default architecture for broad enterprise adoption.

On-premises is projected to expand at 15.37% CAGR through 2031, which creates an unusual pattern where the largest model and the fastest-growing model are not the same. The shift is linked to data sovereignty, sector-specific compliance, and buyer caution around moving sensitive decisioning data outside controlled environments. Braze responded to that pressure in April 2026 through EU hosting on Google Cloud for BrazeAI Decisioning Studio, a move aimed directly at European data residency needs. Hybrid deployment is gaining relevance for the same reason because many buyers want cloud-based inference and coordination while keeping selected customer records or regulated workflows closer to their own governed systems.

By Application: Journey Design Stays Foundational While Optimization Expands Faster

Customer journey design and experience management held 27.48% share in 2025, giving it the largest application position in the customer journey orchestration market. That lead reflects the fact that many enterprises begin with mapping, visibility, and experience design before they invest further in optimization and more advanced automation. Design tools help organizations identify drop-off points, understand channel handoffs, and create a shared structure for customer-facing processes. In practical terms, this application area often becomes the first step because companies need a common journey framework before they can manage next-best-action logic at scale. The customer journey orchestration market still depends on that sequencing because design maturity often shapes how effectively later optimization investments perform.

Journey optimization is projected to grow at 17.84% CAGR through 2031, making it the fastest-growing application as earlier platform buyers move from setup to continuous improvement. That change suggests the market is entering a more operational phase where value depends less on initial journey creation and more on constant tuning across channels and decision points. Twilio supported that movement in May 2026 with the launch of Conversation Orchestrator, Conversation Memory, and Conversation Intelligence, all aimed at preserving context and improving coordinated customer interactions across AI and human touchpoints. Adobe also reinforced automation-led execution in September 2025 with Journey Agent in Adobe Journey Optimizer, which can create and orchestrate journeys based on stated goals and observed drop-off signals.

By Organization Size: Large Enterprises Lead While SMEs Gain Ground

Large enterprises held 68.26% share in 2025, which shows that the customer journey orchestration market still draws most revenue from buyers with broad customer bases, multiple business units, and multi-country operating models. These organizations have more urgent needs around cross-channel coordination, customer retention, and large-scale personalization. They also tend to have the budget and internal sponsorship needed to connect orchestration with CRM, service, analytics, and commerce systems. That combination keeps large enterprises in the lead even as the market opens further to smaller buyers.

Small and medium enterprises are projected to grow at 16.58% CAGR through 2031, which points to a meaningful reduction in the technical barriers that once limited adoption. No-code and low-code interfaces, simpler deployment models, and more packaged AI features are making orchestration more accessible to smaller teams. The customer journey orchestration market is therefore widening beyond the traditional enterprise core and moving into use cases where speed and usability matter as much as platform depth. Compliance needs also support that expansion because smaller firms increasingly prefer structured tools for consent and engagement workflows rather than manual approaches that are harder to govern.

By End User Industry: BFSI Leads While Healthcare Gains Speed

BFSI held 24.81% share in 2025, which made it the largest end-user segment in the customer journey orchestration market. Banks and insurers continue to invest because onboarding, product cross-sell, service resolution, and retention all benefit from more coordinated journey execution across digital and assisted channels. The value of each customer relationship is high in BFSI, so even modest improvements in completion rates or retention can justify larger platform spending. This keeps the segment ahead in current revenue terms and supports continued investment in governed next-best-action environments. It also fits the wider pattern of the customer journey orchestration market, where sectors with large customer data sets and frequent service touchpoints tend to move first.

Healthcare is projected to grow at 17.21% CAGR through 2031, making it the fastest-growing end-user vertical in the market. Growth is being driven by the move from reactive communication toward patient and member engagement that is more timely, more personalized, and better aligned with care pathways. Pegasystems stated in 2025 that AI orchestration in healthcare can improve upsell performance, increase engagement, and support more tailored outreach across health plan experiences.[3]Pegasystems, “Beyond the Transaction, How AI Orchestration Improves Healthcare Outcomes,” Pega Insights, pega.com The segment is also being shaped by compliance because buyers want native audit logging, consent tracking, and data minimization controls built into journey execution rather than layered on later.

Geography Analysis

North America held 39.18% of the customer journey orchestration market share in 2025, which kept the region in the lead. The region benefits from early enterprise adoption, high technology spending, and the presence of many of the largest software vendors serving customer experience and CRM workflows. A large installed base of enterprise applications also makes North America a natural launch market for orchestration features that extend across marketing, service, and commerce. The customer journey orchestration market in the United States remains especially active because major platform vendors continue to build AI-led roadmaps around enterprise data and cross-channel engagement. At the same time, state-level privacy rules are pushing buyers to pay closer attention to consent governance and data activation boundaries.

Europe remains important in the customer journey orchestration market because enterprise demand is strong, but deployment choices are shaped more heavily by privacy, residency, and audit requirements. Germany, the United Kingdom, and France continue to anchor regional demand, especially in BFSI and telecommunications, where customer interactions are frequent and regulated. Braze addressed this environment in April 2026 with EU hosting on Google Cloud for BrazeAI Decisioning Studio, so that real-time decisioning data no longer leaves the European Union region. The region, therefore, remains one of the clearest examples of how regulatory structure can reshape platform architecture in the customer journey orchestration market.

Asia-Pacific is projected to expand at 18.43% CAGR through 2031, making it the fastest-growing geography in the customer journey orchestration market. China, India, Japan, South Korea, and Australia are the main demand centers, supported by large digital user bases and rising expectations for real-time engagement. Mobile-first behavior across much of the region is pushing vendors to support orchestration models that are less dependent on traditional email-heavy engagement patterns. Southeast Asia adds another layer of momentum because messaging-led commerce and app-centric service behavior require orchestration that can react quickly across high-volume digital touchpoints. The same opportunity is drawing attention to localization and data governance, since regional privacy rules and residency expectations are becoming harder to separate from product design.

Competitive Landscape

The customer journey orchestration market shows moderate concentration at the top, with Salesforce, Adobe, Oracle, SAP, and Microsoft occupying much of the large-enterprise conversation through broader customer experience and CRM suites. Their advantage comes from installed relationships, integration depth, and the ability to bundle orchestration with data, service, analytics, and campaign tools. That position is important because buyers with complex environments often prefer vendors that can reduce integration burden across the wider stack. Even so, the customer journey orchestration market remains open enough for specialist vendors to compete when speed, usability, or sector focus matters more than suite breadth. This is why the top tier continues to face pressure from both specialist orchestration providers and AI-native engagement platforms.

Competitive behavior in 2026 has been shaped most clearly by the move toward agentic AI. Adobe introduced CX Enterprise in April 2026 as an end-to-end system for customer lifecycle execution that combines brand intelligence, engagement intelligence, and broad cloud and model interoperability. Oracle launched Fusion Agentic Applications for CX in April 2026 to support coordinated AI agents across sales, marketing, and service tasks within Oracle Fusion Cloud Applications.[4]Oracle, “Oracle Introduces Fusion Agentic Applications for Customer Experience,” Oracle News, oracle.com SAP and Google Cloud expanded their partnership in April 2026 so joint customers can deploy multi-agent AI across SAP CX and Gemini Enterprise environments. Braze added BrazeAI Operator and BrazeAI Agent Console in April 2026, which pushed more autonomous campaign and personalization capabilities into its platform.

The competitive structure also reflects a widening split between broad suites and focused execution models. Twilio used SIGNAL 2026 to position conversation continuity and AI-human handoff coordination as a differentiator in customer interaction management. PossibleNOW focused on consent and zero-party data control inside Salesforce Marketing Cloud, which shows that narrower governance-led capabilities can still claim strategic relevance in the customer journey orchestration market. The strongest white space remains in compliance-aware orchestration for sectors such as healthcare and financial services where generic governance frameworks do not always map neatly to operating needs. Vendors that combine workflow speed with embedded controls are likely to compete more effectively as enterprise buying criteria move beyond message delivery and into governed decision execution.

Customer Journey Orchestration Industry Leaders

Salesforce, Inc.

Adobe Inc.

Oracle Corporation

Microsoft Corporation

IBM Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: MoEngage launched Merlin AI Custom Agents on June 3, 2026, enabling lifecycle marketers and CRM teams to build custom workflow agents atop MoEngage data and tools with full visibility and marketer-defined guardrails, and simultaneously opened its MCP server so customers can connect external AI tools including Claude and ChatGPT to MoEngage data and workflows without custom integration.

- May 2026: Twilio announced at SIGNAL 2026 on May 6 the general availability of its new Conversations Layer, comprising Twilio Conversation Orchestrator, Twilio Conversation Memory, and Twilio Conversation Intelligence, collectively powering continuity across the full customer interaction lifecycle.

- April 2026: Oracle introduced Fusion Agentic Applications for CX on April 9, 2026, deploying coordinated teams of specialized AI agents across sales, marketing, and service, all built into Oracle Fusion Cloud Applications and operating within existing enterprise security and governance frameworks.

- April 2026: Adobe unveiled CX Enterprise at Adobe Summit 2026, an end-to-end agentic AI system for the full customer lifecycle, featuring Adobe Brand Intelligence and Adobe Engagement Intelligence, with deep interoperability across AWS, Anthropic, Google Cloud, IBM, Microsoft, NVIDIA, and OpenAI, and marketing agent integrations natively embedded within ChatGPT Enterprise, Gemini Enterprise, and Microsoft 365 Copilot.

- April 2026: SAP and Google Cloud expanded their partnership to enable joint enterprise customers to deploy multi-agent AI through integrations between SAP Engagement Cloud, SAP CX, and Joule solutions and Google Gemini Enterprise, allowing agents to execute complex marketing strategies from high-level objectives with availability to customers in H2 2026.

Global Customer Journey Orchestration Market Report Scope

The customer journey orchestration market includes platforms and solutions that enable organizations to design, manage, and optimize end-to-end customer journeys across multiple channels in real time. These solutions integrate customer data, use analytics and AI-driven decisioning, and automate personalized interactions to ensure consistent coordination across every touchpoint, including marketing, sales, service, and retention. The market supports enterprises in improving customer experience, strengthening engagement, and delivering data-driven personalization across industries such as retail, banking, telecom, travel, and healthcare.

The Customer Journey Orchestration Market Report is Segmented by Component (Software, and Services), Deployment Mode (Cloud, On-Premises, and Hybrid), Application (Customer Journey Design and Experience Management, Campaign Management, Personalization, Analytics and Reporting, and Journey Optimization), Organization Size (Large Enterprises, and Small and Medium Enterprises), End User Industry (BFSI, Retail and E-Commerce, IT and Telecommunications, Healthcare, Travel and Hospitality, Media and Entertainment, and Other End User Industries), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| Cloud |

| On-Premises |

| Hybrid |

| Customer Journey Design and Experience Management |

| Campaign Management |

| Personalization |

| Analytics and Reporting |

| Journey Optimization |

| Large Enterprises |

| Small and Medium Enterprises |

| BFSI |

| Retail and E-Commerce |

| IT and Telecommunications |

| Healthcare |

| Travel and Hospitality |

| Media and Entertainment |

| Other End User Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Component | Software | ||

| Services | |||

| By Deployment Mode | Cloud | ||

| On-Premises | |||

| Hybrid | |||

| By Application | Customer Journey Design and Experience Management | ||

| Campaign Management | |||

| Personalization | |||

| Analytics and Reporting | |||

| Journey Optimization | |||

| By Organization Size | Large Enterprises | ||

| Small and Medium Enterprises | |||

| By End User Industry | BFSI | ||

| Retail and E-Commerce | |||

| IT and Telecommunications | |||

| Healthcare | |||

| Travel and Hospitality | |||

| Media and Entertainment | |||

| Other End User Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current and forecast value of the customer journey orchestration?

The Customer Journey Orchestration market stood at USD 11.56 billion in 2025, and USD 13.09 billion in 2026 and is forecast to reach USD 24.41 billion by 2031, growing at a 13.27% CAGR.

Which region leads global demand for customer journey orchestration platforms?

North America led in 2025 with 39.18% share, supported by early enterprise adoption, strong software spending, and deep vendor presence.

Which region is growing the fastest through 2031?

Asia-Pacific is projected to grow at 18.43% CAGR through 2031 as mobile-first engagement and digital commerce scale across large consumer bases.

Which application area is expanding the fastest?

Journey Optimization is expected to grow at 17.84% CAGR through 2031 as buyers move from journey setup into ongoing performance improvement and decision automation.

Which end user segment is moving the fastest?

Healthcare is projected to grow at 17.21% CAGR through 2031 as patient and member engagement becomes more proactive, personalized, and compliance-aware.

What is the main barrier slowing adoption in large enterprises?

Integration with legacy CRM, CDP, and marketing systems remains a major barrier because it slows deployment and makes real-time execution harder to coordinate.

Page last updated on: