CT/NG Testing Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

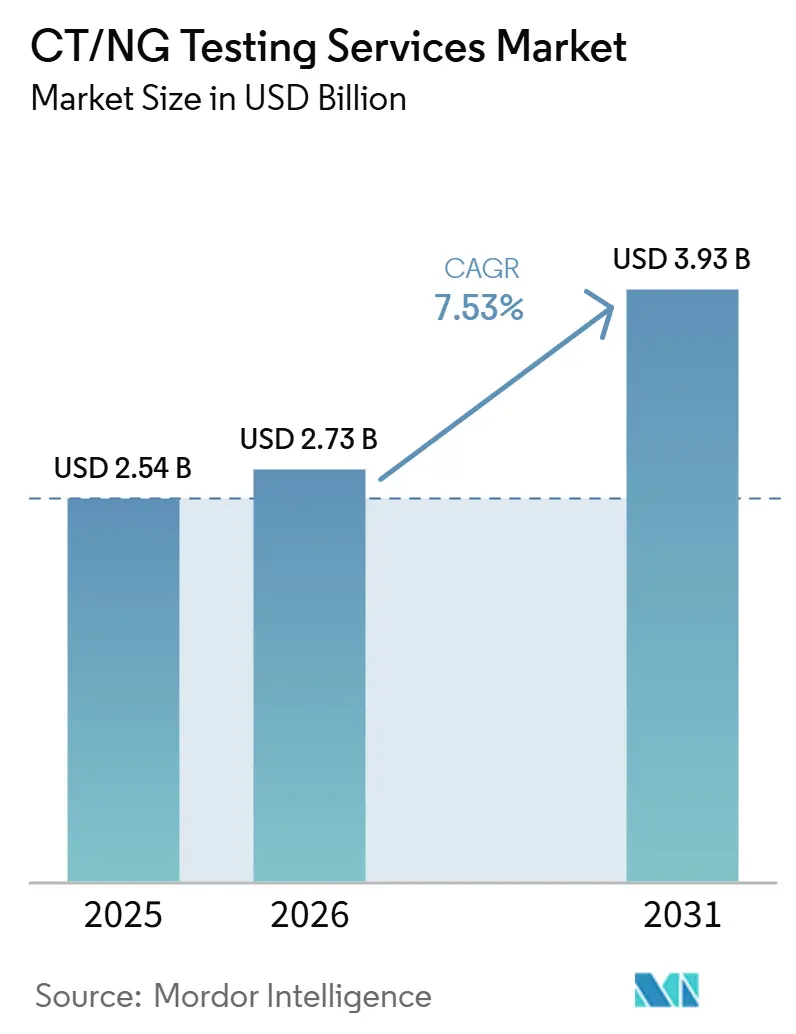

| Market Size (2026) | USD 2.73 Billion |

| Market Size (2031) | USD 3.93 Billion |

| Growth Rate (2026 - 2031) | 7.53% CAGR |

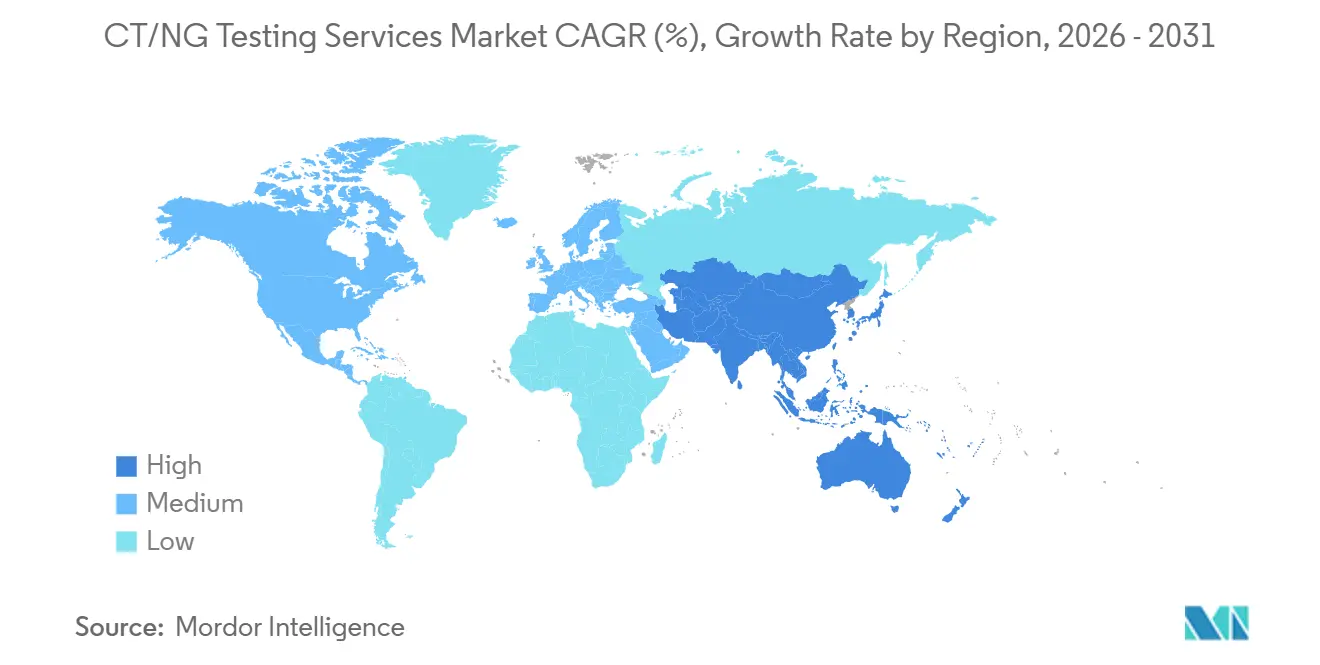

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

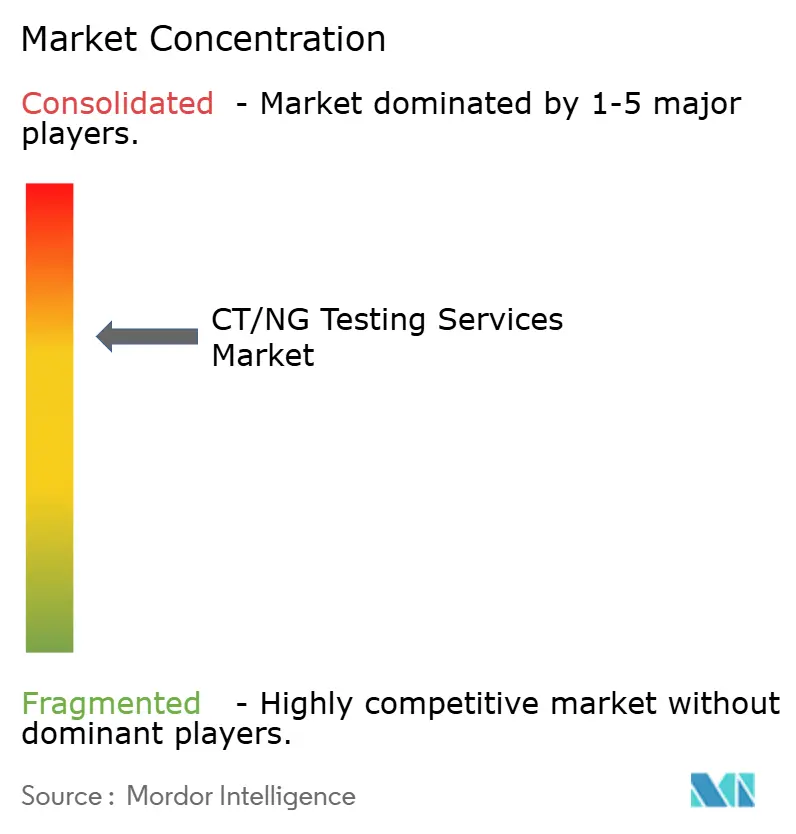

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

CT/NG Testing Services Market Analysis by Mordor Intelligence

The CT/NG Testing Services Market size is projected to expand from USD 2.54 billion in 2025 and USD 2.73 billion in 2026 to USD 3.93 billion by 2031, registering a CAGR of 7.53% between 2026 to 2031.

The CT/NG testing services market is expanding even as reported case counts have softened in some countries, because screening frequency, preventive testing, and repeat testing are rising faster than incidence reporting. The CDC recorded 1.52 million chlamydia cases and 543,000 gonorrhea cases in the United States in 2024, down 8% and 10% from 2023, yet this did not reduce the policy and reimbursement logic for routine screening programs. The CT/NG testing services market is also supported by the shift from symptom-led diagnosis to organized screening across young women, high-risk groups, and extragenital testing pathways, which increases billable test events per person. Product strategy in the CT/NG testing services market is moving toward multiplex molecular assays, self-collection formats, and home-linked care models that lower collection friction while raising the value of each encounter. Competitive activity in the CT/NG testing services market is centered on scaling direct-to-consumer access, strengthening lab infrastructure, and using regulatory compliance as a barrier that favors larger operators with broader menus and stronger capital bases.

Key Report Takeaways

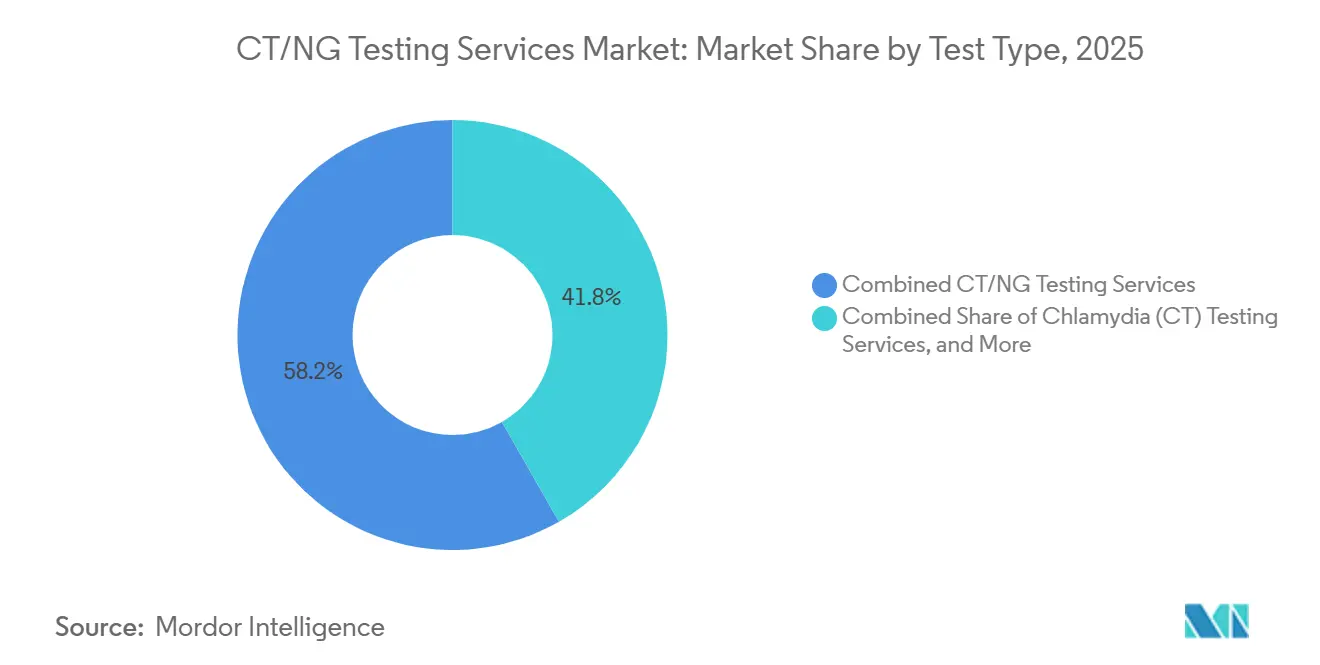

- By test type, combined CT/NG testing services held 58.24% of the CT/NG testing services market share in 2025, while chlamydia testing services are forecast to expand at an 8.12% CAGR through 2031.

- By technology, NAAT services accounted for 73.67% share of the CT/NG testing services market size in 2025, while culture-based testing services recorded the highest projected CAGR at 8.94% through 2031.

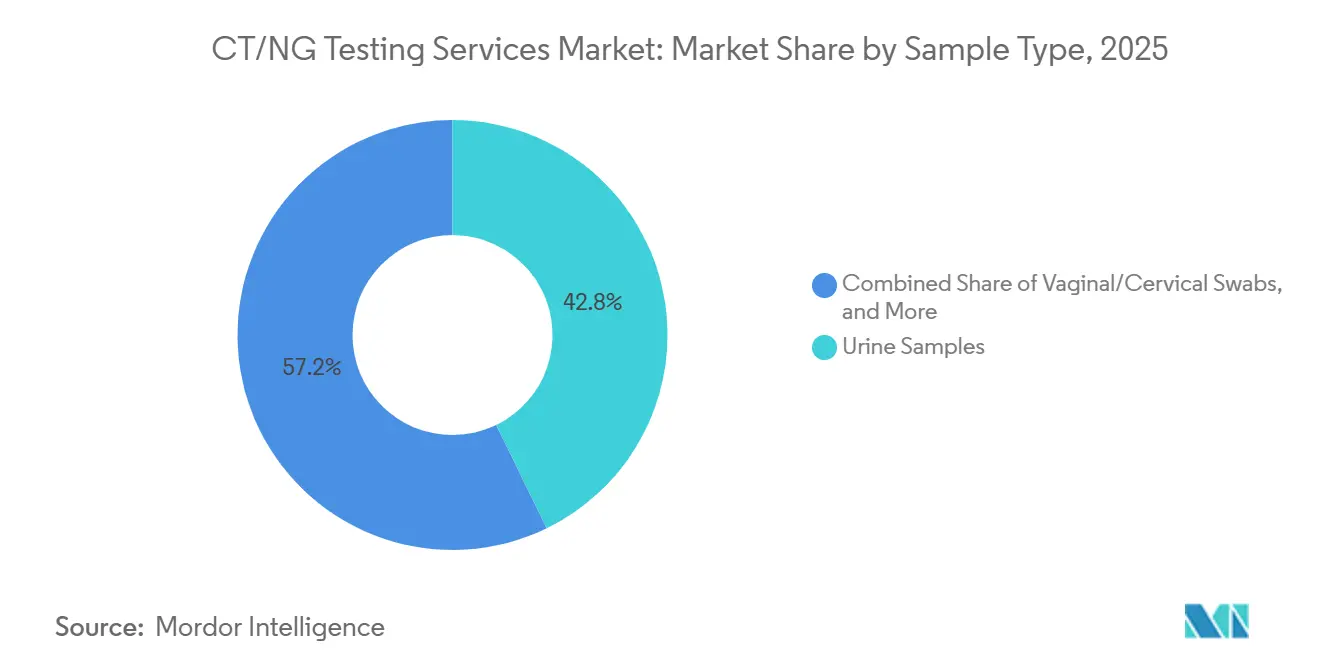

- By sample type, urine samples led with 42.78% share of the CT/NG testing services market size in 2025, while vaginal and cervical swabs are projected to grow at a 9.37% CAGR through 2031.

- By testing mode, centralized laboratory testing held 63.19% revenue share in 2025, while at-home collection and laboratory testing services are projected to advance at a 10.65% CAGR through 2031.

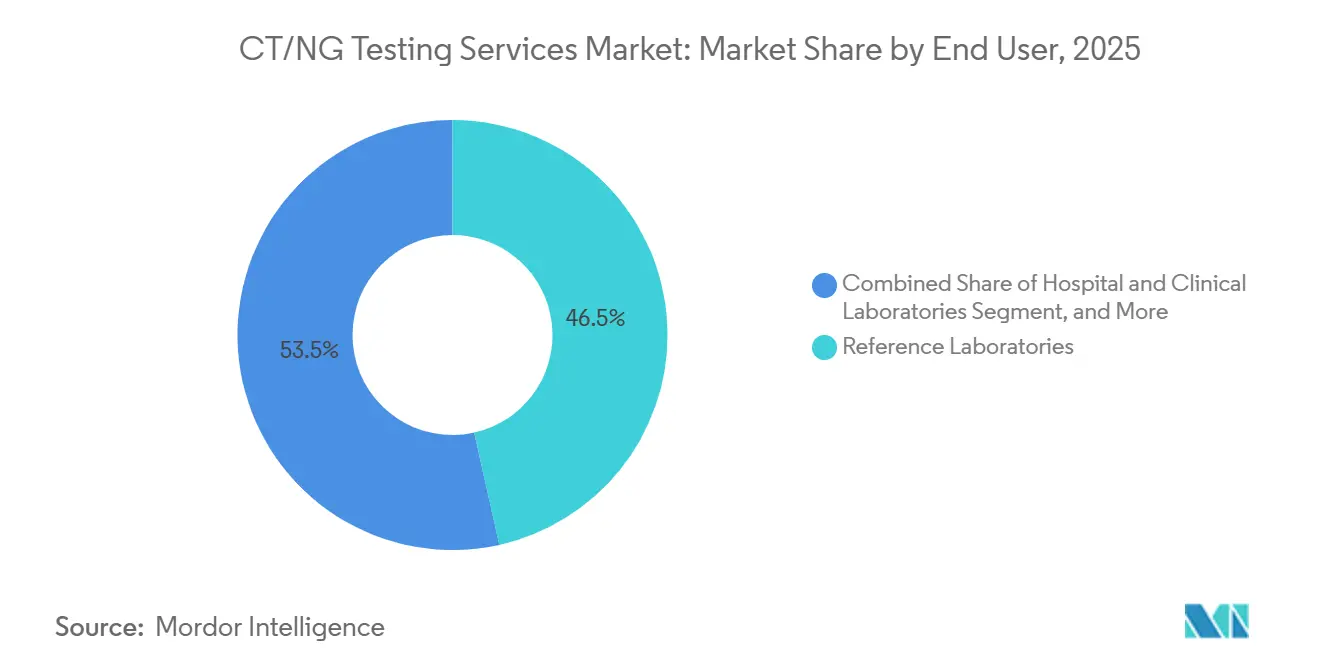

- By end user, reference laboratories accounted for 46.52% share in 2025, while hospital and clinical laboratories are forecast to grow at an 11.76% CAGR through 2031.

- By geography, North America commanded 39.55% of the CT/NG testing services market share in 2025, whereas Asia-Pacific is projected to expand at a 12.38% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global CT/NG Testing Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Asymptomatic Infection Burden Expands Screened Population | +1.8% | Global, strongest in Sub-Saharan Africa, South Asia, and Southeast Asia | Long term (≥ 4 years) |

| Broader Screening Mandates for Sexually Active Under-25 Populations | +1.5% | North America and Europe | Short term (≤ 2 years) |

| Multiplex CT/NG Panels Increase Revenue Per Encounter | +1.2% | North America and Europe | Medium term (2-4 years) |

| Home Collection and Telehealth-Fulfilled Testing Adoption | +1.0% | North America, with spillover to the United Kingdom and Australia | Short term (≤ 2 years) |

| Extragenital Testing Expansion in High-Risk Screening Protocols | +0.7% | North America, Europe, and early gains in Australia | Medium term (2-4 years) |

| Reimbursement Support for Preventive STI Screening | +0.6% | North America, with expansion in Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Asymptomatic Infection Burden Expands the Screened Population

A large share of CT and NG infections remains silent, which keeps the clinical burden higher than routine case reporting suggests. The CT/NG testing services market benefits from this gap because public health systems need screening programs to identify infections before complications appear.[1]“Global, Regional, and National Burden of Chlamydial Infection, A Systematic Analysis of Incidence, Prevalence, Deaths, and DALYs With Projections to 2046,” A 2025 study in Frontiers in Public Health estimated global chlamydial incidence at 235.7 million cases in 2021, with an age-standardized incidence rate of 2,902 per 100,000 population. A 2025 study in BMC Infectious Diseases from Hangzhou found no significant change in CT or NG prevalence between 2018 and 2024 at the study site, which shows how persistent the reservoir remains even after years of control efforts.[2]“Prevalence of Ureaplasma Urealyticum, Chlamydia Trachomatis, Neisseria Gonorrhoeae and Herpes Simplex Virus in Hangzhou, China,” This sustained reservoir supports recurring outreach, repeat testing, and broader screening pathways, which keep the CT/NG testing services market tied to hidden prevalence rather than only to reported case counts.

Broader Screening for Sexually Active Under-25 Populations Institutionalizes Demand

The CT/NG testing services market gains stability when screening moves from physician discretion to formal quality and coverage frameworks. In the United States, the NCQA chlamydia screening measure keeps health plans focused on testing performance for eligible populations, which supports recurring demand at the payer level.[3]“Chlamydia Screening (CHL),” NCQA State of Health Care Quality Report CMS preventive services coverage also supports routine sexually transmitted infection screening for eligible beneficiaries, which reduces direct payment barriers in covered settings.[4]Centers for Medicare & Medicaid Services, “Preventive Services Coverage" Once screening becomes part of plan performance and covered preventive care, volumes are less sensitive to short-term swings in reported prevalence. This creates a predictable floor for the CT/NG testing services market and supports lab investment in capacity, automation, and provider network expansion.

Multiplex CT/NG Panels Reducing Repeat Sample Collection Increase Revenue per Encounter

Multiplex panels raise the value of a single sample by testing for multiple pathogens at once. The CT/NG testing services market benefits because providers can deliver broader diagnostic coverage without asking patients to return for new collection visits. A 2025 clinical study of the Cobas Liat CT/NG/MG assay across 4,800 participants reported specificity above 97% and sensitivity above 92% for CT and NG across specimen types, supporting the case for decentralized multiplex testing. Altona Diagnostics also launched its FlexStar STI panel under full IVDR compliance in 2025, showing that multiplex menu expansion is moving forward in Europe as well. Higher-value panels improve revenue per encounter in the CT/NG testing services market and make single-sample workflows more attractive for clinics and laboratories.

Home Collection and Telehealth-Fulfilled Testing Adoption Opens Non-Clinical Demand

Home-linked testing expands access beyond the clinic visit and reaches people who may delay or avoid in-person care. The CT/NG testing services market has started to benefit from this shift as self-collection and direct-to-consumer pathways become more credible. The FDA authorized Visby Medical’s Women’s Sexual Health Test in March 2025 as the first home test for chlamydia, gonorrhea, and trichomoniasis that can be bought without a prescription and completed entirely at home. Visby stated that the product delivers results in around 30 minutes and connects positive users to telehealth support, which turns a test into a fuller care pathway. Labcorp also introduced STI self-collection options through patient service centers and participating physician offices, which supports broader use of lower-friction collection models. These steps bring incremental volume into the CT/NG testing services market from people who previously sat outside normal testing pathways.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Social Stigma and Privacy Concerns Limit Test-Seeking Behavior | -0.9% | Global, strongest in APAC, MEA, and South America | Long term (≥ 4 years) |

| Cost Pressure on Multiplex Molecular Assays | -0.8% | APAC core markets, MEA, and South America | Medium term (2-4 years) |

| Reimbursement Gaps for Asymptomatic and Panel Testing | -0.6% | APAC core markets, MEA, and spillover to South America | Medium term (2-4 years) |

| Regulatory Complexity for Home-Use and Point-Of-Care Assays | -0.5% | Global, especially the United States and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Social Stigma and Privacy Concerns Constrain Test-Seeking Behavior

Social stigma still keeps a meaningful share of infected people away from testing, even where diagnostic tools are available. The CT/NG testing services market, therefore, faces a demand ceiling that cannot be solved by equipment expansion alone. A 2026 multicenter study in southern China found that more than 75% of patients with gonorrhea at Shenzhen clinics were not tested during their most recent visit, and only 37.7% had confirmed positive results, which shows how behavior and care processes still leave major detection gaps. Home testing addresses part of the privacy problem, but the current over-the-counter option cited in the input is limited to female users, which narrows the full reach of private testing pathways. Until routine wellness visits, opt-out screening, and broader private testing formats become more common, stigma will continue to slow the CT/NG testing services market in several high-burden populations.

Cost Pressure on Multiplex Molecular Assays Slows Market Penetration in Price-Sensitive Settings

NAAT and multiplex molecular formats deliver better sensitivity, but they still carry higher per-test costs than simpler methods. The CT/NG testing services market, therefore, grows unevenly across countries with different funding models and laboratory budgets. WHO’s 2024 guidance on asymptomatic sexually transmitted infections recognized NAAT as the recommended option for CT and NG detection, while also noting that its cost can limit sustainable use in lower-resource settings without stronger funding support. The cost challenge is reinforced by reagent expenses, instrument investment, and staffing needs for molecular workflows. Reimbursement gaps for asymptomatic and panel testing add another limit in the CT/NG testing services market because providers may not be paid for the broader test menu that public health goals increasingly require.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Test Type: Combined Testing Leads Current Revenue While Standalone CT Testing Expands Faster

Combined CT/NG testing services held 58.24% share in 2025, which made it the largest test-type segment in the CT/NG testing services market. This position reflects the clinical preference for co-testing when either infection is suspected and the operational ease of using one encounter to rule in or rule out both pathogens. The segment also benefits from the fact that co-infection is clinically meaningful, so combined ordering is often seen as standard care rather than as an optional add-on. Billing support has also improved the case for combined panels in the United States. EmblemHealth added CPT code 0455U to chlamydia and gonorrhea screening coverage effective July 1, 2024, which supports clearer reimbursement pathways for panel-based ordering.

Chlamydia testing services are projected to grow at an 8.12% CAGR from 2026 to 2031, making it the fastest-growing test-type segment in the CT/NG testing services market. Growth is linked to wider screening in primary care, family planning clinics, and urgent care settings where CT screening is more routinely emphasized, especially for younger women. The CDC’s enhanced Gonococcal Isolate Surveillance Project keeps gonorrhea testing strategically important, but CT screening reaches a broader preventive care base and supports more repeat testing cycles CDC.GOV. Updated guidelines in China and India published in 2024 also support the spread of evidence-based CT testing into routine STI workflows, which broadens the standalone opportunity outside mature Western markets. As these protocols move into more clinics, standalone CT testing captures incremental demand that combined testing does not yet fully absorb across all settings in the CT/NG testing services market.

By Technology: NAAT Remains the Core Modality While Culture Gains Importance in Resistance Surveillance

NAAT services held 73.67% share in 2025, which confirmed their structural lead across the CT/NG testing services market. This dominance rests on higher sensitivity, faster reporting, and broad clinical acceptance across centralized and decentralized settings. The performance data for newer molecular platforms continues to support this position. A 2025 Journal of Clinical Microbiology study found strong sensitivity and specificity for a rapid multiplex CT/NG/MG assay across specimen types, which reinforces confidence in advanced molecular testing models. NAAT also aligns well with self-collection, automated high-throughput labs, and multiplex menu expansion, which keeps it at the center of both public health and commercial testing workflows in the CT/NG testing services market.

Culture-based testing services are projected to grow at an 8.94% CAGR through 2031, even though it remains smaller than molecular testing in the CT/NG testing services market. This growth is tied less to first-line diagnosis and more to gonorrhea resistance surveillance, where viable organisms are still needed for susceptibility work. Australia’s Public Health Laboratory Network updated its national NAAT guidelines in 2025 and supported supplemental culture use for certain non-urogenital gonorrhea specimens to strengthen antimicrobial surveillance. A 2025 Eurosurveillance study screened 54,837 gonococcal genomes and identified 17 diagnostic-escape variants linked to the Xpert CT/NG assay across 5 countries, which showed that NAAT-only systems can develop blind spots. That risk does not reduce NAAT’s lead, but it creates a durable secondary role for culture in reference settings across the CT/NG testing services market.

By Sample Type: Urine Holds the Largest Base While Vaginal and Cervical Swabs Gain Momentum

Urine samples held 42.78% share in 2025, making them the largest sample-type segment in the CT/NG testing services market. Their lead reflects patient preference for non-invasive collection, broad clinical familiarity, and long-standing NAAT validation on urine specimens. Urine also fits well with high-volume testing programs because it simplifies collection logistics and lowers collection discomfort in many settings. These advantages help preserve strong routine use in screening programs, urgent care, and general outpatient pathways. For many providers, urine remains the most practical starting point when broad testing access matters more than maximizing sensitivity in every female case.

Vaginal and cervical swabs are projected to expand at a 9.37% CAGR from 2026 to 2031, which makes them the fastest-growing sample-type segment in the CT/NG testing services market. The main reason is clinical performance in women, where swab-based collection often detects infection more effectively than first-catch urine. A 2024 Journal of Women’s Health review confirmed that vaginal swabs show better sensitivity than urine for detecting chlamydia and gonorrhea in women. Self-collected vaginal swabs are also central to emerging self-collection models, including Labcorp’s STI self-collection rollout and home-oriented testing workflows. Extragenital sites remain clinically important as well, and a 2024 BMC Infectious Diseases study supported strong GeneXpert performance at pharyngeal and rectal sites for MSM screening. As more guidelines adopt multi-site and self-collected approaches, swab use should continue to rise across the CT/NG testing services market.

By Testing Mode: Centralized Labs Keep the Largest Base While At-Home Pathways Grow Fastest

Centralized laboratory testing held 63.19% share in 2025 and remained the largest testing-mode segment in the CT/NG testing services market. Large networks maintain this lead through high-throughput systems, broad compliance infrastructure, and durable provider relationships built over many years. Centralized labs also support complex confirmatory work, broad payer integration, and efficient logistics for specimen movement from clinics and collection points. These features matter when programs need scale, menu breadth, and consistent quality controls. The model, therefore, remains the commercial backbone of the CT/NG testing services market even as new access routes emerge.

At-home collection and laboratory testing services are projected to grow at a 10.65% CAGR through 2031, which makes it the most dynamic mode in the CT/NG testing services market. The FDA’s 2025 authorization of Visby’s home test gave the segment a strong commercial signal and helped legitimize consumer-led molecular STI testing. Visby’s launch also linked home testing to app-based guidance and telehealth follow-up, which reduces friction between diagnosis and treatment. Labcorp’s self-collection expansion shows that the line between home use and lab-backed testing is becoming more flexible rather than fully separate. This means growth in consumer-led testing can still support established processing networks instead of fully replacing them in the CT/NG testing services market.

By End User: Reference Laboratories Hold the Lead While Hospital and Clinical Labs Expand More Quickly

Reference laboratories held 46.52% share in 2025 and kept the largest end-user position in the CT/NG testing services market. Their advantage comes from batch processing scale, lower per-test economics, broad courier systems, and established relationships with outpatient collection sites. Reference labs also tend to carry broader STI test menus and stronger automation, which supports both routine screening and higher-value multiplex work. These strengths fit well with preventive screening programs that generate recurring volume across dispersed patient populations. As a result, reference laboratories remain central to how the CT/NG testing services market converts screening activity into processed revenue.

Hospital and clinical laboratories are projected to grow at an 11.76% CAGR through 2031, the fastest rate among end users in the CT/NG testing services market. Growth is linked to tighter integration of STI testing into hospital-affiliated outpatient care and digital ordering workflows that support routine screening at the point of care. This segment also benefits when public systems face budget pressure and routine commercial testing shifts toward better-capitalized hospital and private lab networks. Public health laboratories will remain essential for outbreak response and resistance surveillance, especially in gonorrhea. However, day-to-day commercial volume is increasingly moving toward providers that can combine clinical access, rapid processing, and modern molecular capacity within the CT/NG testing services market.

Geography Analysis

North America held 39.55% of global revenue in 2025, which gave the region the largest share in the CT/NG testing services market. The region benefits from formal screening measures, broad private insurance participation, and preventive coverage frameworks that support repeat testing cycles. NCQA’s chlamydia screening measure keeps payer attention on testing performance, while CMS preventive services coverage helps support access for eligible beneficiaries. North America also has a stronger commercial base for self-collection and consumer-led testing than most other regions. Quest Diagnostics completed its Corewell Health laboratory joint venture in Michigan in January 2026, which shows that major operators are still investing in added processing infrastructure as the CT/NG testing services market expands.

Europe remained the second-largest regional revenue base in the CT/NG testing services market. The region includes several large diagnostic networks and operates across diverse reimbursement systems, which creates uneven testing intensity across countries. At the same time, the IVDR framework raises compliance demands and tends to favor larger organizations with stronger regulatory resources. Altona Diagnostics launched its FlexStar STI panel under full IVDR compliance in 2025, which reflects how larger and better-prepared suppliers are adapting to the new environment. The United Kingdom remains notable because its population screening framework gives Europe one of its more organized testing pathways outside the United States.

Asia-Pacific is projected to grow at a 12.38% CAGR from 2026 to 2031, making it the fastest-growing regional block in the CT/NG testing services market. The region combines structural underdiagnosis with updated national guidelines, which creates a large runway for expansion. A 2025 Hangzhou study reported no significant reduction in CT or NG prevalence between 2018 and 2024, which points to ongoing diagnostic gaps in care pathways. China updated its CT urogenital infection guideline in 2024, and India issued new national technical guidance on STIs in 2024, both of which support wider evidence-based molecular testing. Middle East and Africa presents longer-term potential as private healthcare investment rises in selected markets, and the WHO’s STI prevalence database launched in July 2026 adds a stronger epidemiological basis for future testing expansion. South America still faces reimbursement fragmentation and public lab funding pressure, but urban laboratory networks are beginning to adopt broader molecular workflows in the CT/NG testing services market.

Competitive Landscape

The CT/NG testing services market is moderately concentrated at the top tier, with a limited group of large diagnostic networks such as Quest Diagnostics, Labcorp, Eurofins Scientific, Sonic Healthcare, and SYNLAB holding the strongest positions across scale, menu breadth, and geographic reach. Below that tier, the CT/NG testing services market remains fragmented because regional reference labs, hospital laboratories, and specialty sexual health clinics still control important local relationships. This creates a structure where national or multinational scale matters, but local access channels still shape a large share of routine volume. Leading players are responding by expanding direct access, deepening processing capacity, and improving alignment between collection models and molecular testing workflows. That pattern shows a market where scale helps, but breadth of access still matters just as much as brand visibility.

One clear strategic move has been the push into home-linked testing. Visby Medical received FDA authorization for its Women’s Sexual Health Test in March 2025 and then launched the product nationally, which helped define a new direct-to-consumer molecular testing lane in the CT/NG testing services market. Another move has been infrastructure expansion through partnerships and network buildout. Quest Diagnostics completed its Corewell Health joint venture in January 2026 after signing the agreement in August 2025, which shows how major labs are using partnerships to secure specimen flow and local scale. A third move is regulatory readiness, where companies with strong compliance capability can launch and defend more advanced testing menus.

CT/NG Testing Services Industry Leaders

ARUP Laboratories

Eurofins Scientific SE

Labcorp

PathCare.AI

Unilabs

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Quest Diagnostics and Corewell Health completed their previously announced laboratory joint venture, establishing Diagnostic Lab of Michigan, LLC, with 51% Quest ownership and 49% Corewell Health ownership. Plans include a 100,000 sq ft state-of-the-art laboratory facility in Southfield, Michigan, expected to be operational in Q1 2027.

- November 2025: Visby Medical launched its Women's Sexual Health Test nationally in the United States, the first PCR-based OTC diagnostic for any indication, delivering results for chlamydia, gonorrhea, and trichomoniasis in approximately 30 minutes at home via Bluetooth-connected app, and enabling same-day treatment access through integrated telehealth.

- August 2025: Quest Diagnostics and Corewell Health signed a definitive agreement to form their Michigan laboratory services joint venture, expected to generate cost efficiencies and expand access across Corewell's 22-hospital network. Supply chain and reference agreements began transitioning in late 2025.

Global CT/NG Testing Services Market Report Scope

As per the scope of the report, CT/NG testing services are clinical laboratory and digital‑health services that perform Chlamydia trachomatis (CT) and Neisseria gonorrhoeae (NG) detection using NAAT/TMA assays on patient samples. These services include specimen collection, transport, laboratory processing, result reporting, and clinical follow‑up across hospital labs, commercial reference labs, sexual‑health clinics, and at‑home testing providers. They represent the service component of the CT/NG Testing Market, distinct from diagnostic products or instruments.

The CT/NG testing services market is segmented by test type, technology, sample type, testing mode, end user, and geography. By test type, the market is segmented into chlamydia (CT) testing services, gonorrhea (NG) testing services, and combined CT/NG testing services. By technology, the market is segmented into nucleic acid amplification testing (NAAT) services, culture-based testing services, immunoassay-based testing services, and others. By sample type, the market is segmented into urine samples, vaginal and cervical swabs, urethral swabs, rectal and pharyngeal swabs, and others. By testing mode, the market is segmented into centralized laboratory testing, point-of-care testing services, and at-home collection and laboratory testing services. By end user, the market is segmented into reference laboratories, hospital and clinical laboratories, public health laboratories, and others. The geography segment is further divided into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market size and forecasts in value (USD) for the above segments.

| Chlamydia (CT) Testing Services |

| Gonorrhea (NG) Testing Services |

| Combined CT/NG Testing Services |

| Nucleic Acid Amplification Testing (NAAT) Services |

| Culture-Based Testing Services |

| Immunoassay-Based Testing Services |

| Others |

| Urine Samples |

| Vaginal and Cervical Swabs |

| Urethral Swabs |

| Rectal and Pharyngeal Swabs |

| Others |

| Centralized Laboratory Testing |

| Point-of-Care Testing Services |

| At-Home Collection and Laboratory Testing Services |

| Reference Laboratories |

| Hospital and Clinical Laboratories |

| Public Health Laboratories |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Test Type | Chlamydia (CT) Testing Services | |

| Gonorrhea (NG) Testing Services | ||

| Combined CT/NG Testing Services | ||

| By Technology | Nucleic Acid Amplification Testing (NAAT) Services | |

| Culture-Based Testing Services | ||

| Immunoassay-Based Testing Services | ||

| Others | ||

| By Sample Type | Urine Samples | |

| Vaginal and Cervical Swabs | ||

| Urethral Swabs | ||

| Rectal and Pharyngeal Swabs | ||

| Others | ||

| By Testing Mode | Centralized Laboratory Testing | |

| Point-of-Care Testing Services | ||

| At-Home Collection and Laboratory Testing Services | ||

| By End User | Reference Laboratories | |

| Hospital and Clinical Laboratories | ||

| Public Health Laboratories | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is driving growth in CT/NG testing services through 2031?

Growth is being supported by routine screening mandates, rising testing frequency, wider use of multiplex molecular panels, and the expansion of home-linked testing pathways. The CT/NG testing services market is projected to grow from USD 2.73 billion in 2026 to USD 3.93 billion by 2031 at a 7.53% CAGR.

Which test type generates the most revenue today?

Combined CT/NG testing services leads current revenue, with 58.24% share in 2025. The segment benefits from co-testing becoming standard practice when either infection is suspected.

Why is standalone chlamydia testing growing faster than combined testing?

Standalone CT testing is expanding faster because screening programs for younger women and routine preventive visits often emphasize chlamydia testing first. That helped make chlamydia testing services the fastest-growing test-type segment at an 8.12% CAGR through 2031.

Why does NAAT remain the leading technology despite higher costs?

NAAT remains dominant because it offers better sensitivity, faster turnaround, and broad compatibility with multiplex workflows and self-collection models. It held 73.67% share in 2025, even as cost pressure still limits adoption in some lower-resource settings.

Which region offers the strongest growth outlook?

Asia-Pacific has the strongest growth outlook, with a projected 12.38% CAGR from 2026 to 2031. Updated guidelines in China and India and persistent underdiagnosis are expanding the need for more structured testing pathways.

How are competitive strategies changing in this space?

Leading companies are building direct-access channels, investing in laboratory partnerships, and launching compliant multiplex or self-collection solutions. Recent examples include Visby’s home test authorization and launch, along with Quest’s laboratory joint venture with Corewell Health.

Page last updated on: