CT/NG Testing Products Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.97 Billion |

| Market Size (2031) | USD 2.82 Billion |

| Growth Rate (2026 - 2031) | 7.41% CAGR |

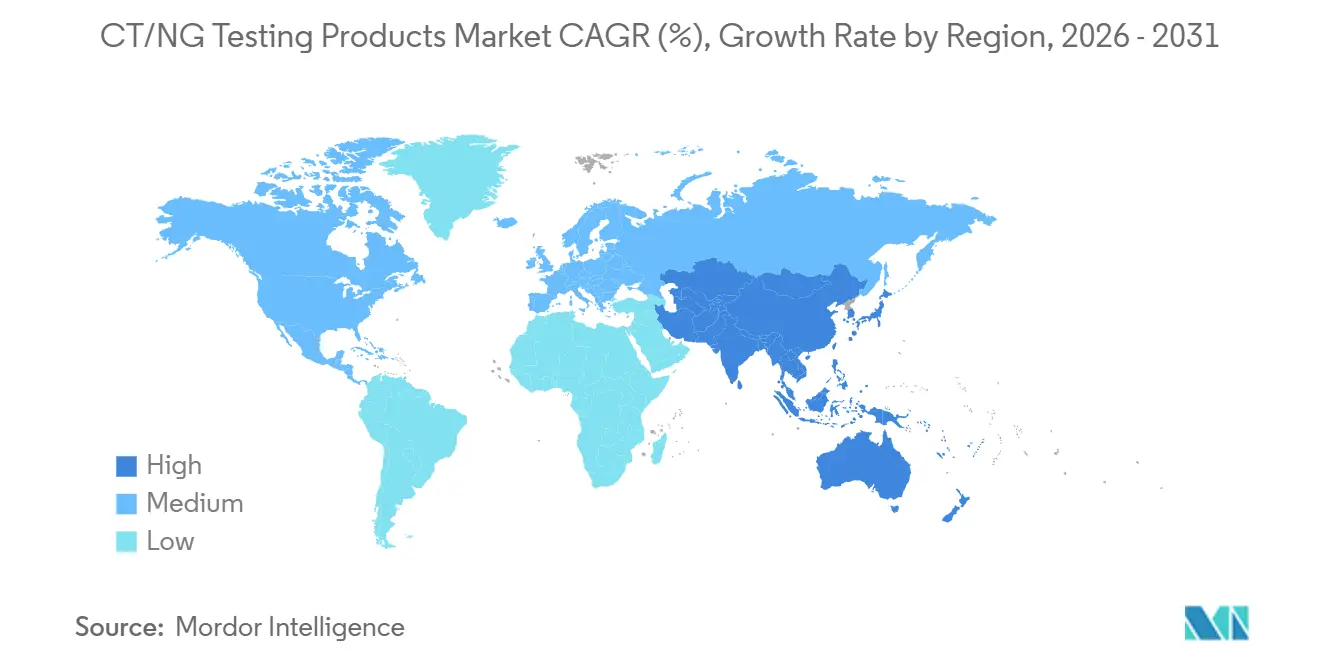

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

CT/NG Testing Products Market Analysis by Mordor Intelligence

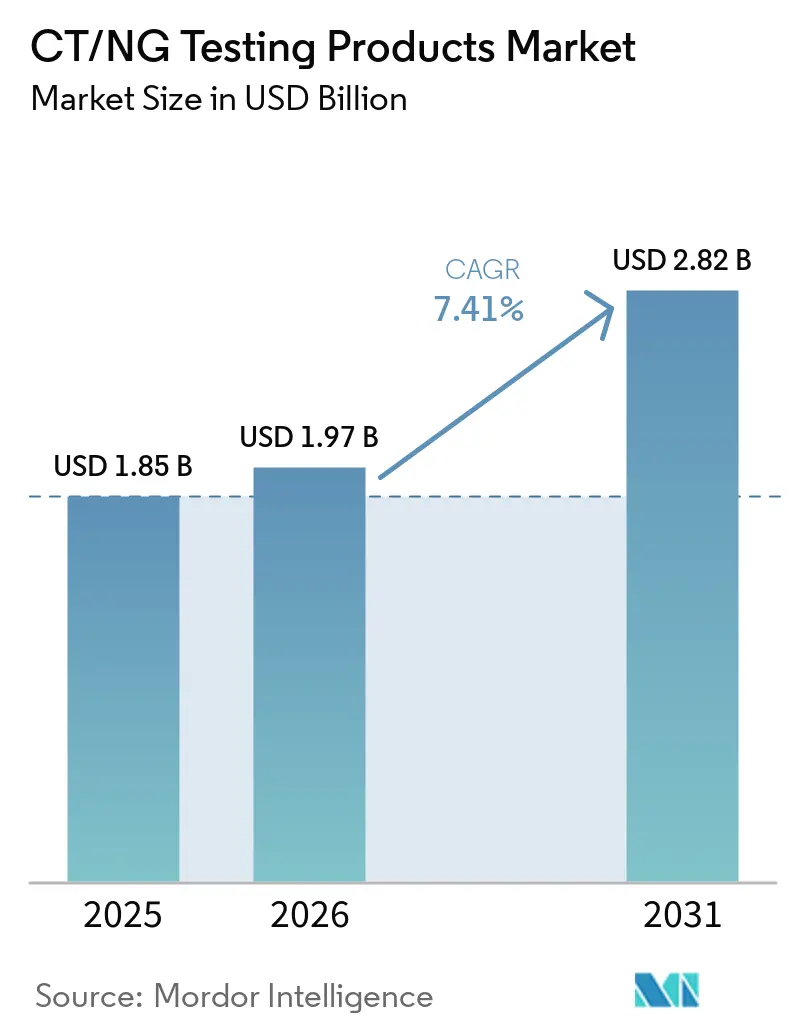

The CT/NG Testing Products Market size is expected to increase from USD 1.85 billion in 2025 to USD 1.97 billion in 2026 and reach USD 2.82 billion by 2031, growing at a CAGR of 7.41% over 2026-2031.

The CT/NG testing products market is being supported by stronger antimicrobial resistance surveillance, with the WHO Enhanced Gonococcal Antimicrobial Surveillance Programme reporting in November 2025 that 13 countries were contributing resistance data and showing rising ceftriaxone and azithromycin resistance across multiple regions. The CT/NG testing products market is also benefiting from faster decentralized testing after Roche received FDA clearance and a CLIA waiver in January 2025 for cobas liat CT/NG and CT/NG/MG assays that deliver results in 20 minutes with under 1 minute of hands-on time. The CT/NG testing products market continues to gain from laboratory automation, wider use of single-swab workflows, and reagent-rental models that reduce upfront instrument costs for laboratories and urgent care sites. The CT/NG testing products market is also seeing stronger expansion in Asia-Pacific as manufacturers add research and manufacturing capacity and use faster approval pathways such as the China-Malaysia in vitro diagnostic mutual recognition framework that took effect on July 30, 2025. The CT/NG testing products market remains moderately concentrated, with large diagnostics groups maintaining broad installed bases while specialized molecular players compete through automation, analytics, menu breadth, and resistance-focused capabilities.

Key Report Takeaways

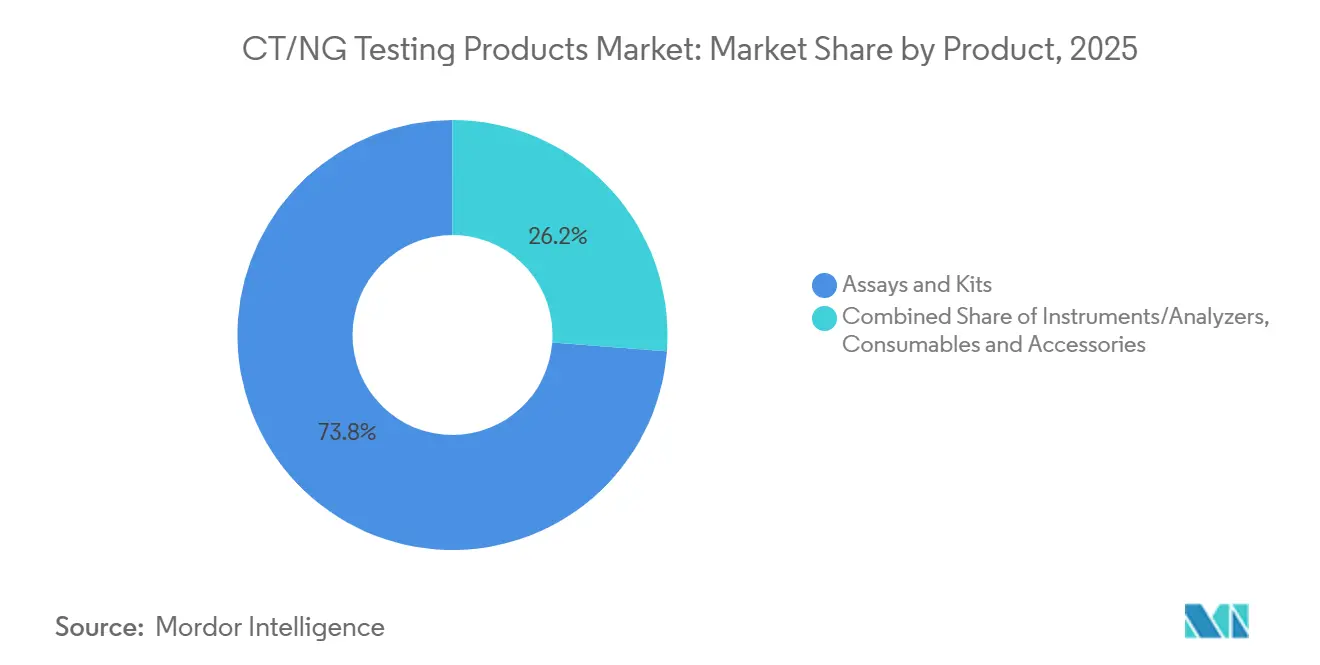

- By product, assays and kits led with 73.8% share in 2025, and the same segment is projected to grow at 7.67% through 2031.

- By technology, NAAT held 47.54% share in 2025, while immunoassays are expected to expand at 7.75% through 2031.

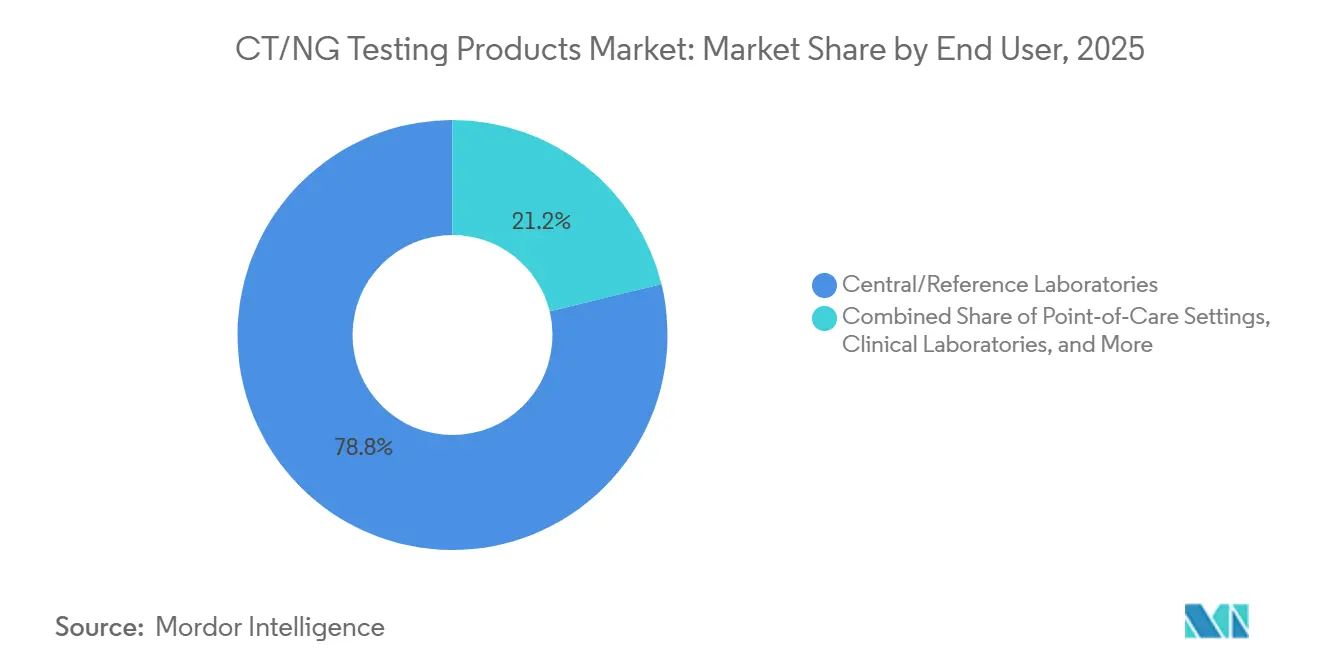

- By end user, central and reference laboratories accounted for 78.8% of revenue in 2025, while point-of-care settings are forecast to grow at 7.98% through 2031.

- By geography, North America held 38.47% share in 2025, while Asia-Pacific is expected to record the fastest growth at 8.13% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global CT/NG Testing Products Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Routine Screening Mandates in Women Under 25 and High-Risk Groups | +1.2% | Global, strongest in North America and Europe | Medium term (2-4 years) |

| Rapid NAAT and CLIA-Waived Point-of-Care Expansion | +1.5% | North America, Europe, with spillover to urban Asia-Pacific and Latin America | Short term (≤ 2 years) |

| OTC At-Home CT/NG Testing Approvals Expand Access | +0.8% | Primarily the United States and Europe, with pathways under review in Canada and Australia | Long term (≥ 4 years) |

| Lab Automation and High-Throughput Platforms Lower Turnaround Time and Cost per Test | +1.4% | Global, with heavier investment in Asia-Pacific and North America | Medium term (2-4 years) |

| Extragenital Screening Adoption Increases Tests per Patient | +1.0% | North America, Europe, Australia, and urban Asia-Pacific | Short term (≤ 2 years) |

| AMR Surveillance Needs for NG Favor Precise Molecular Diagnostics | +0.9% | Global, led by WHO, Euro-GASP, China, the United Kingdom, and Australia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Routine Screening Mandates in Women Under 25 and High-Risk Groups

The CT/NG testing products market is supported by public health screening guidance that continues to widen testing among younger women and people with defined risk factors. Canada’s Public Health Agency revised its guidance in April 2025 and reaffirmed annual universal CT/NG screening for individuals under 25, while also supporting repeat testing based on risk among those aged 25 and older. The Canadian Task Force on Preventive Health Care also recommends opportunistic screening up to age 30 for people who are not in high-risk groups, which broadens the addressable pool beyond the narrowest clinical risk definitions[1]Housne Begum, Dominique Basque, Michelle Haavaldsrud, Holly Sullivan, and Stephan Gadient, “Environmental Scan of Available Guidelines for Chlamydia and or Gonorrhea Screening Recommendations,” Canada Communicable Disease Report, canada.ca.

Kaiser Permanente Washington updated its approach through June 2025 and used opt-out extragenital screening questions in routine visits so providers can capture asymptomatic infections that standard discussions may miss. This makes testing less dependent on patient disclosure and increases the clinical value of broader specimen menus within the CT/NG testing products market. Quality frameworks such as CLIA in the United States and ISO 15189 in accredited laboratories also make these recommendations more practical to implement at scale because they support consistent workflows and result reliability.

Rapid NAAT and CLIA-Waived Point-of-Care Expansion

The CT/NG testing products market is gaining from rapid molecular platforms that reduce turnaround time from days to minutes and support treatment during the same visit. Roche received FDA 510(k) clearance and a CLIA waiver on January 21, 2025, for cobas liat CT/NG and CT/NG/MG assays that deliver PCR-quality results in 20 minutes with under 1 minute of hands-on time. These systems are being positioned for urgent care centers, retail clinics, and community health venues where same-visit diagnosis can reduce loss to follow-up.

A WHO-supported evaluation of Cepheid’s GeneXpert Xpert CT/NG assay across Italy, Malta, and Peru enrolled 1,702 men who have sex with men and showed pooled sensitivity of 91.4% for NG in urine, specificity above 98% for CT and NG across all tested sites, and willingness among 96% of participants to wait for point-of-care results. Providers in the same study rated the instructions very clear or excellent in 79% of cases and reported optimal training times of 30 to 60 minutes, which shows that the CT/NG testing products market can expand beyond specialized laboratory staff. This combination of short hands-on time, acceptable workflow, and high willingness to wait supports continued movement of testing volumes toward decentralized care settings in the CT/NG testing products market.

Lab Automation and High-Throughput Platforms Lower Turnaround Time and Cost per Test

The CT/NG testing products market is also moving toward more automated and higher-throughput laboratory systems that reduce manual steps and improve specimen flow. Seegene announced CURECA in August 2025 as a fully unattended PCR automation system that can manage pre-treatment for blood, stool, sputum, and urine, and it paired that launch with STAgora, a real-time infectious-disease analytics platform with more than 40 statistical modules. Hitachi High-Tech stated that its LABOSPECT TS total laboratory automation system went live at Seegene Medical Foundation Seoul in October 2025 with six high-speed pre-processing sets and six analyzers, reducing overtime and supporting larger test volumes.

Sansure Biotech markets the Natch CS3 Automatic Nucleic Acid Extractor, which processes 96 samples through extraction and PCR setup within 80 minutes and allows 1 technician to handle up to 1,700 samples per day. These investments improve cost per test not only through labor savings but also through multiplexing, because a single reaction can cover CT, NG, and additional targets without duplicate runs. As a result, the CT/NG testing products market is seeing stronger demand from central and reference laboratories that need to absorb higher specimen volumes without proportionate staffing growth.

AMR Surveillance Needs for NG Favor Precise Molecular Diagnostics

The CT/NG testing products market is being reinforced by the need to monitor resistant Neisseria gonorrhoeae strains with faster and more precise molecular tools. The WHO Enhanced Gonococcal Antimicrobial Surveillance Programme reported in November 2025 that 13 countries were contributing resistance data, which reflects a broader shift toward coordinated surveillance. Australia’s 2024 surveillance data showed that 0.5% of 10,702 isolates met the WHO criterion for decreased ceftriaxone susceptibility, more than double the prior year, and 76.4% of those isolates carried the mosaic penA 60.001 allele.

A study published in February 2025 found that Seegene’s Allplex NG & DR assay achieved 100% sensitivity and 98.3% specificity for predicting ciprofloxacin resistance through detection of the gyrA S91F mutation, although azithromycin resistance prediction remained weaker. Another study published in January 2026 identified 33 novel mutations linked to decreased ceftriaxone susceptibility and showed that 49-site mutation-based sequence typing outperformed penA typing alone for identifying resistant strains. These developments raise the strategic value of assays that can do more than detect infection, because surveillance, stewardship, and therapy selection are becoming more closely linked across the CT/NG testing products market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU IVDR Compliance Costs and Notified Body Bottlenecks | -1.1% | Europe, with indirect spillover to companies targeting Europe first | Medium term (2-4 years) |

| Insufficient Evidence for Routine Screening in Men | -0.7% | United States | Long term (≥ 4 years) |

| Stigma and Privacy Barriers Still Limit Testing Uptake in Some Groups | -0.5% | Global, especially in conservative and rural settings | Long term (≥ 4 years) |

| LDT Restrictions and Migration to CE-IVD Reduce Menu Flexibility | -0.4% | North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

EU IVDR Compliance Costs and Notified Body Bottlenecks

The CT/NG testing products market faces a clear drag in Europe from the In Vitro Diagnostic Regulation and the burden it creates for certification, recertification, and portfolio maintenance. Transition deadlines now run through December 2027 for Class D devices, December 2028 for Class C devices, and December 2029 for Class B and A-Sterile devices, which keeps compliance pressure elevated for several more years.

MedTech Europe reported in March 2025 that the administrative load under IVDR and MDR is heavy enough to redirect company resources away from innovation and toward regulatory upkeep. This matters for the CT/NG testing products market because sexual health menus often depend on multiplex claims, specimen-specific validation, and regular updates as guidelines change. When certification paths slow down, companies are less willing to expand panels or localize launches for Europe, especially if those products already have better commercial timing in the United States or Asia. The result is slower menu renewal, higher compliance cost per assay, and a tougher environment for smaller developers that do not have the same regulatory infrastructure as global incumbents in the CT/NG testing products market[2]MedTech Europe, “Report on Administrative Burden under IVDR and MDR, MedTech Europe’s Proposal for IVDR and MDR Targeted Evaluation,” MedTech Europe, medtecheurope.org.

Insufficient Evidence for Routine Screening in Men

The CT/NG testing products market also faces a longer-term restraint in the United States because routine screening in asymptomatic men still lacks a broad preventive recommendation. The U.S. Preventive Services Task Force position continues to influence payer behavior, and that keeps reimbursement less certain for testing programs aimed at low-risk or undefined male populations. Kaiser Permanente Washington addressed this limitation through targeted guidance, recommending annual screening for men who have sex with men at sites of contact and screening every 3 to 6 months for those on PrEP, living with HIV, or reporting multiple partners.

Canada’s 2025 environmental scan also highlighted that international guidance remains inconsistent for asymptomatic men, which shows why manufacturers in the CT/NG testing products market cannot rely on one global screening model. This uncertainty tends to limit payer enthusiasm for broader urogenital screening and makes reimbursement for rectal and pharyngeal testing harder to expand outside clearly defined high-risk groups. Until clinical and economic evidence becomes more uniform, adoption in this part of the CT/NG testing products market is likely to remain selective rather than universal.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Reagent-Rental Models Shift Capital Risk

Assays and kits accounted for 73.8% of the CT/NG testing products market size in 2025 and are expected to expand at a 7.67% CAGR through 2031. This leadership reflects the way laboratories prefer reagent-rental arrangements that avoid upfront instrument purchases and shift capital risk to the supplier. BD’s COR MX approach fits this pattern because hospitals commit to reagent volumes for CTGCTV2 assays in exchange for instrument placement, training, and service bundled into per-test pricing[3]Becton, Dickinson and Company, “BD Onclarity HPV Assay for BD COR and BD Viper LT Systems Receive WHO Prequalification,” BD, bd.com. Roche followed a similar model in decentralized settings, where cobas liat CT/NG and CT/NG/MG assays use closed single-use cartridges and allow molecular testing without dedicated batch preparation. That combination keeps assays and kits at the center of revenue generation in the CT/NG testing products market even when placement growth starts with instruments rather than consumables.

Instruments and analyzers are growing from a smaller base, but expansion in the CT/NG testing products industry still depends on rising menu breadth and automation intensity. Hitachi High-Tech’s October 2025 installation at Seegene Medical Foundation Seoul showed how larger laboratories are scaling pre-processing and retesting capacity to absorb more complex molecular workloads. Consumables and accessories also benefit as self-collection becomes more accepted, because transport media, swabs, and specimen-handling materials gain volume when home or clinic self-swab workflows expand. The 2025 European guideline on chlamydia management stated that self-collected vulvo-vaginal, pharyngeal, and rectal specimens have similar diagnostic accuracy to clinician-collected samples for NAATs, which supports broader packaging of collection devices with simplified instructions. Across the CT/NG testing products market, this keeps product demand tied not only to instrument placements but also to how often patients are screened and how many anatomical sites are tested in the same episode.

By Technology: Dual-Target NAATs Remain Core While Immunoassays Gain from Broader Women’s Health Workflows

NAAT held 47.54% of the CT/NG testing products market share in 2025, while immunoassays are projected to grow at 7.75% through 2031. NAAT remains the core technology because laboratories value analytical sensitivity, specimen flexibility, and the ability to handle multi-site screening in the same workflow. BD’s dual-target design for CT and GC addresses the known risk that single-target assays can miss plasmid-lacking variants, which helps explain why molecular formats remain central in the CT/NG testing products market. Hologic’s TMA-based approach also remains competitive because some laboratories prefer ribosomal RNA detection and see operational value in faster processing of urine samples. Within this segment, the CT/NG testing products market continues to reward platforms that can balance sensitivity, throughput, and resistance to common workflow interruptions.

Immunoassays are growing faster because women’s health laboratories increasingly want broader testing from the same patient interaction rather than isolated STI workflows. Roche received a CE Mark in December 2025 for cobas BV/CV, which lets laboratories use the same vaginal swab for bacterial vaginosis, candida vaginitis, CT, NG, Trichomonas vaginalis, and Mycoplasma genitalium workflows on cobas systems. This reduces separate sample handling and improves the case for consolidated laboratory operations, especially in high-volume reference settings. Culture and other methods still matter for antimicrobial susceptibility work and some legal or confirmatory use cases, but they represent a small part of routine diagnostic demand in the CT/NG testing products industry. The practical direction of the CT/NG testing products market remains clear, with technologies that support multiplexing, workflow consolidation, and specimen versatility gaining the strongest commercial traction.

By End User: Central Labs Lead Revenue While Point-of-Care Gains from Same-Visit Testing

Central and reference laboratories represented 78.8% of the CT/NG testing products market size in 2025 because they combine economies of scale, batch processing, broad menus, and established quality systems. These facilities are also the main buyers of high-throughput automation, which lets them support large catchment areas without matching staff growth one-for-one with specimen growth. Hospital and clinical laboratories remain important for moderate volumes and for same-day inpatient and emergency decision-making, but they usually do not match the scale economics of reference networks. This volume concentration keeps central sites dominant across the CT/NG testing products market, especially where extragenital and multiplex testing are expanding together. It also explains why automation, analytics, and menu breadth remain strong differentiators for vendors competing in the CT/NG testing products market.

Point-of-care settings are forecast to expand at 7.98% through 2031, the fastest rate among end users, because CLIA-waived molecular platforms now allow same-visit diagnosis and treatment. Roche’s cobas liat CT/NG and CT/NG/MG assays deliver results in 20 minutes with under 1 minute of hands-on time, which makes them practical for urgent care centers, retail clinics, and community health settings. The WHO-supported GeneXpert evaluation also showed that 96% of participants were willing to wait for point-of-care results, confirming that patients see value in immediate answers when the workflow is simple enough. At-home and remote collection models are still early, but self-collection is becoming more credible because the 2025 European guideline reported equivalent accuracy to clinician collection for several NAAT specimen types.

Geography Analysis

North America held 38.47% of the CT/NG testing products market share in 2025, making it the largest regional contributor. The United States anchors this position because CDC guidance supports extragenital screening for men who have sex with men at 3 to 6 month intervals when they are on PrEP, living with HIV, or have multiple partners. Kaiser Permanente Washington reinforced that direction through its June 2025 opt-out screening workflow that asks patients whether any exposure sites should be excluded from routine STI testing. This kind of operational change lifts specimen volumes per patient and supports broader uptake across the CT/NG testing products market in North America. Canada also adds demand through updated 2025 guidance that reaffirmed annual universal CT/NG screening for people under 25 and targeted repeat screening in older groups based on risk.

Asia-Pacific is the fastest-growing regional block in the CT/NG testing products market, with an expected 8.13% CAGR through 2031. The China-Malaysia IVD mutual recognition arrangement became effective on July 30, 2025, and shortened approval timelines for qualifying Chinese products in Malaysia to 30 working days and for Malaysian products in China to 60 working days. Sansure also added a 6,100-square-meter research center and a 7,900-square-meter manufacturing base, which shows how regional suppliers are preparing for larger diagnostic demand. Australia strengthens the regional case from a surveillance standpoint, because 2024 data showed ceftriaxone decreased susceptibility in 0.5% of 10,702 isolates and supported the need for resistance-aware molecular diagnostics. Europe remains an important revenue base for the CT/NG testing products market, but it is operating under heavier regulatory pressure as MedTech Europe continues to report high administrative burden under IVDR and MDR.

The United Kingdom also remains clinically important because GRASP data to September 2025 showed rising resistance pressure, including 15 confirmed ceftriaxone-resistant cases in the first 8 months of 2025 and multiple extensively drug-resistant cases linked mainly to Asia-Pacific travel. Across continental Europe, Euro-GASP tested 3,579 isolates across 22 countries in 2024 and found tetracycline resistance of 62.3%, which keeps surveillance needs elevated. Middle East and Africa remain more fragmented, with stronger uptake in Gulf states that rely on centralized laboratory infrastructure and standardized procurement. South America is also growing from a smaller base, with adoption centered in larger urban systems and private clinic networks rather than broad nationwide testing saturation. Across both regions, the CT/NG testing products market still depends heavily on public procurement consistency, import conditions, and the ability of vendors to support decentralized testing where central laboratory access is uneven.

Competitive Landscape

The CT/NG testing products market shows moderate to high competitive intensity, with Roche, Danaher through Cepheid, Hologic, Abbott, and BD maintaining a large installed base across laboratory and decentralized settings. The leading companies benefit from reagent-rental models, broad assay menus, and long customer relationships that make switching less frequent once a workflow is established. Specialized firms such as Seegene, bioMérieux, and QIAGEN still hold meaningful positions because they offer automation, analytics, and broader infectious-disease coverage that appeals to reference laboratories with complex testing needs. This structure leaves the CT/NG testing products market concentrated enough for scale to matter, but still open enough for specialized capabilities to win share. The main competitive divide is no longer only sensitivity or throughput, because customers increasingly judge platforms by workflow fit, menu integration, and resistance-related value across the CT/NG testing products market.

Roche used its January 2025 FDA clearance and CLIA waiver for cobas liat CT/NG and CT/NG/MG assays to extend beyond central laboratories and address urgent care, retail clinics, and community settings that want same-visit answers. bioMérieux made a different move when it acquired Day Zero Diagnostics on June 16, 2025, for under USD 25 million and added next-generation sequencing workflows that can identify bacterial species and antibiotic resistance profiles within hours instead of 2 to 5 days. Seegene pushed further on automation and analytics in August 2025 with CURECA and STAgora, showing that vendors are now competing on unattended processing and real-time data interpretation rather than only assay chemistry. These moves show that the CT/NG testing products market is rewarding 3 different strategies at once, faster decentralized testing, stronger resistance-linked capability, and lower-touch laboratory automation. Vendors that cannot align with at least 1 of these routes are more exposed to pricing pressure and slower placement growth in the CT/NG testing products market.

Another clear divide is specimen scope, because companies that lack strong claims for rectal and pharyngeal testing lose relevance as screening protocols extend beyond urogenital sampling. CDC guidance, Kaiser Permanente workflows, and the 2025 European guideline all support broader multi-site testing in populations at elevated risk. BD’s dual-target molecular design also shows how intellectual property and assay architecture still matter because they help protect performance against evolving variants and reduce the risk of false negatives. In that setting, the CT/NG testing products market remains competitive, but leadership is increasingly tied to full workflow coverage rather than a single instrument or assay advantage.

CT/NG Testing Products Industry Leaders

Roche Diagnostics

Danaher Corporation

Hologic, Inc.

Abbott Laboratories

Becton, Dickinson and Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: A Chinese genomics study published January 20, 2026, identified 33 novel mutations associated with ceftriaxone decreased susceptibility in Neisseria gonorrhoeae and demonstrated that 88.4% of resistant strains belonged to 34 high-frequency MLST types (ST7363, ST1901, ST1903, ST7365, ST7360), enabling continuous molecular surveillance of at-risk lineages; the 49-site mutation-based sequence typing achieved 68.4% sensitivity and 77.3% specificity for identifying ceftriaxone-resistant strains, outperforming penA typing alone (36.7% sensitivity).

- December 2025: Roche announced CE Mark for its cobas BV/CV assay on December 9, 2025, a PCR test detecting bacteria associated with bacterial vaginosis and yeast linked to candida vaginitis from the same vaginal swab used for CT, NG, Trichomonas vaginalis, and Mycoplasma genitalium testing on cobas 5800/6800/8800 systems, consolidating vaginitis and STI workflows.

Global CT/NG Testing Products Market Report Scope

As per the scope of the report, CT/NG testing refers to diagnostic tests used to detect Chlamydia trachomatis (CT) and Neisseria gonorrhoeae (NG), the bacteria responsible for chlamydia and gonorrhea infections.

The CT/NG testing products market is segmented by product into assays & kits, instruments/analyzers, and consumables & accessories. By technology, the market is categorized into NAAT (PCR, transcription-mediated amplification, and isothermal amplification), immunoassays, and culture/other methods. By end user, the segmentation includes central/reference laboratories, hospital/clinical laboratories, point-of-care settings, and at-home/remote collection. Geographically, the market is divided into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Assays & Kits |

| Instruments/Analyzers |

| Consumables & Accessories |

| NAAT | PCR |

| Transcription-Mediated Amplification | |

| Isothermal amplification | |

| Immunoassays | |

| Culture / Other Methods |

| Central/Reference Laboratories |

| Hospital/Clinical Laboratories |

| Point-of-Care Settings |

| At-Home / Remote Collection |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product | Assays & Kits | |

| Instruments/Analyzers | ||

| Consumables & Accessories | ||

| By Technology | NAAT | PCR |

| Transcription-Mediated Amplification | ||

| Isothermal amplification | ||

| Immunoassays | ||

| Culture / Other Methods | ||

| By End User | Central/Reference Laboratories | |

| Hospital/Clinical Laboratories | ||

| Point-of-Care Settings | ||

| At-Home / Remote Collection | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of CT/NG testing products?

The CT/NG testing products market reached USD 1.85 billion in 2025 and is projected to reach USD 2.82 billion by 2031 at a 7.41% CAGR.

Which product category leads revenue generation?

Assays and kits led with 73.8% share in 2025 because reagent-rental models and recurring consumable demand keep them central to laboratory purchasing.

Which technology is growing fastest for CT and NG diagnostics?

NAAT remained the largest technology segment in 2025 with 47.54% share, while immunoassays are expected to grow fastest at 7.75% through 2031 as women's health workflows become more integrated.

Why are point-of-care settings gaining traction?

Point-of-care settings are forecast to grow at 7.98% through 2031 because CLIA-waived molecular tests can deliver results in 20 minutes and enable diagnosis and treatment in the same visit.

Which region is expanding the fastest?

Asia-Pacific is expected to grow the fastest at 8.13% through 2031, supported by faster approval pathways, local manufacturing expansion, and stronger surveillance-driven demand.

What is the main competitive advantage in this space now?

Vendors with strong multi-site specimen claims, automation, decentralized workflows, and resistance-linked capabilities are in a better position than suppliers competing only on basic assay throughput.

Page last updated on: