Cricket OTT Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 8.81 Billion |

| Market Size (2031) | USD 18.58 Billion |

| Growth Rate (2026 - 2031) | 16.10% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cricket OTT Market Analysis by Mordor Intelligence

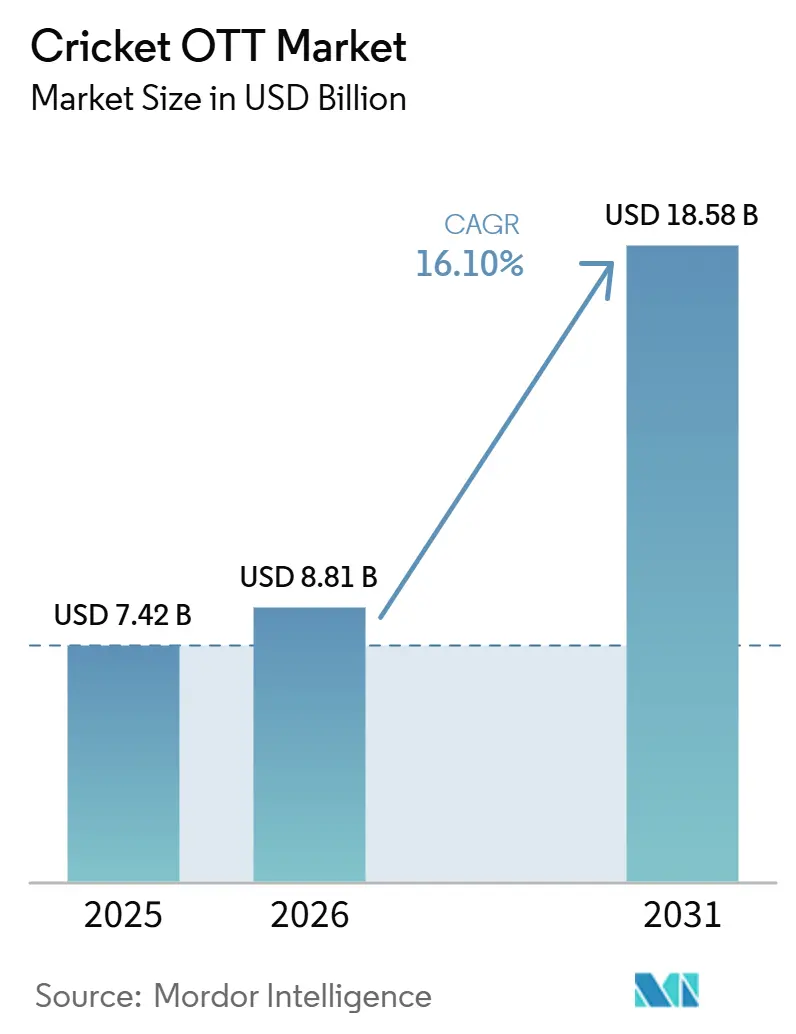

The Cricket OTT market size is projected to be USD 7.42 billion in 2025, USD 8.81 billion in 2026, and reach USD 18.58 billion by 2031, growing at a CAGR of 16.10% from 2026 to 2031. The Cricket OTT market is expanding because premium cricket rights now sit at the center of live sports streaming economics across several high-growth digital media markets. Hybrid access models, where low-cost paid plans sit beside ad-supported reach, are helping platforms convert event-driven audiences into more stable recurring revenue streams. Connected TV adoption is also improving monetization because large-screen sports viewers usually carry higher-value subscriptions and attract stronger advertising rates. Competition in the Cricket OTT market is increasingly shaped by regional rights concentration, sub-licensing partnerships, and technology-led viewing upgrades such as rapid highlights, multi-language feeds, and interactive match coverage. The main pressure point remains the gap between rising rights costs and slower growth in monetization, which is pushing platforms to balance scale, pricing discipline, and yield management more carefully.

Key Report Takeaways

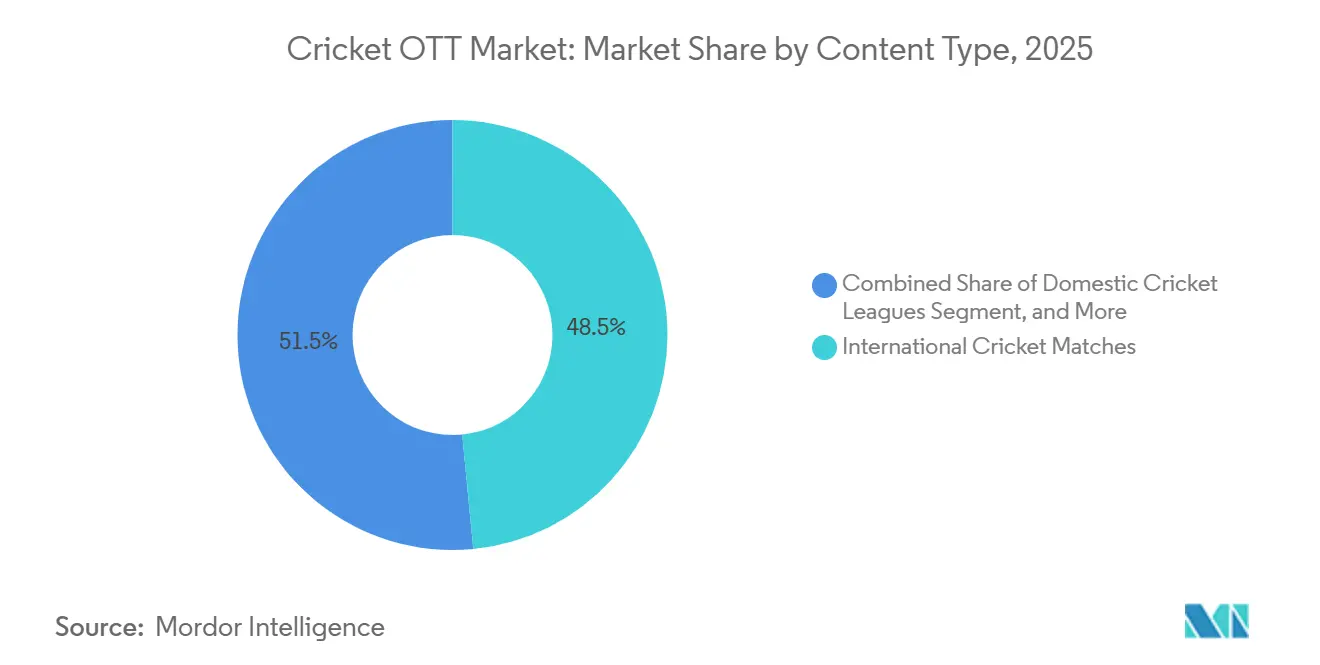

- By content type, international matches held 48.46% of the Cricket OTT market share in 2025, while domestic cricket leagues are projected to expand at a 16.42% CAGR through 2031.

- By device type, smartphones and tablets accounted for 60.23% share of the Cricket OTT market size in 2025, while smart TVs are projected to grow at a 16.36% CAGR through 2031.

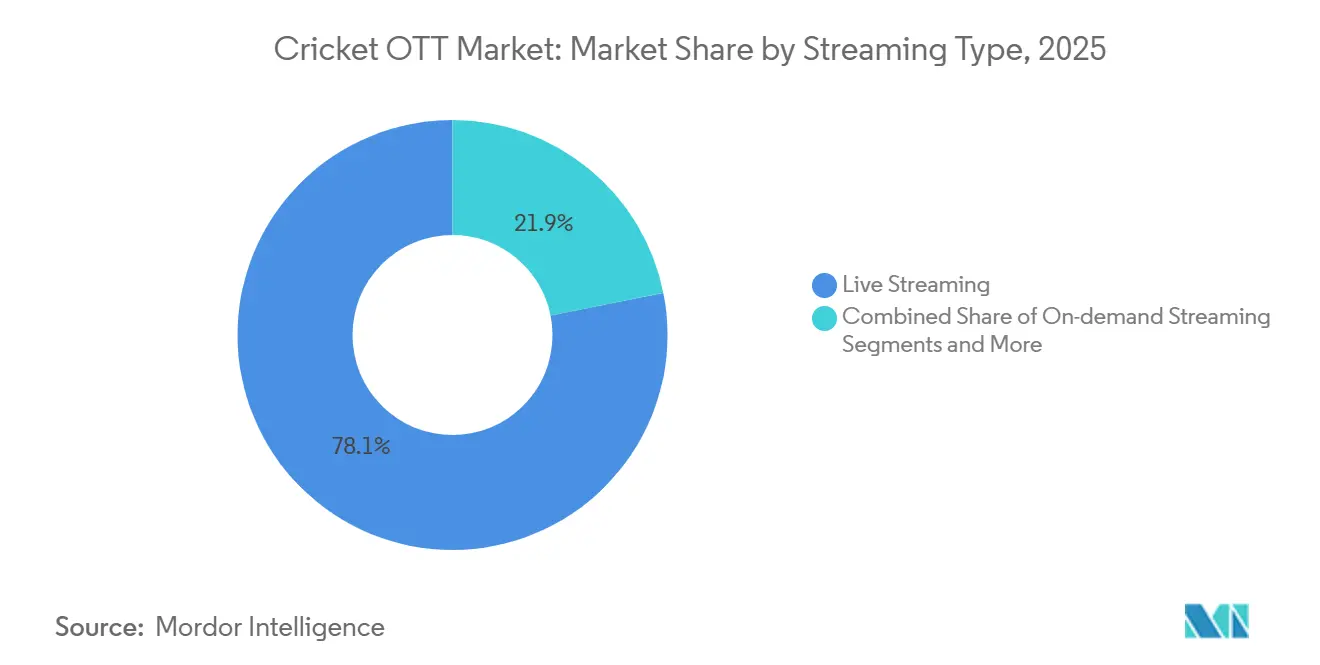

- By streaming type, live streaming held 78.13% of segment revenue in 2025, while on-demand streaming is projected to advance at a 16.58% CAGR through 2031.

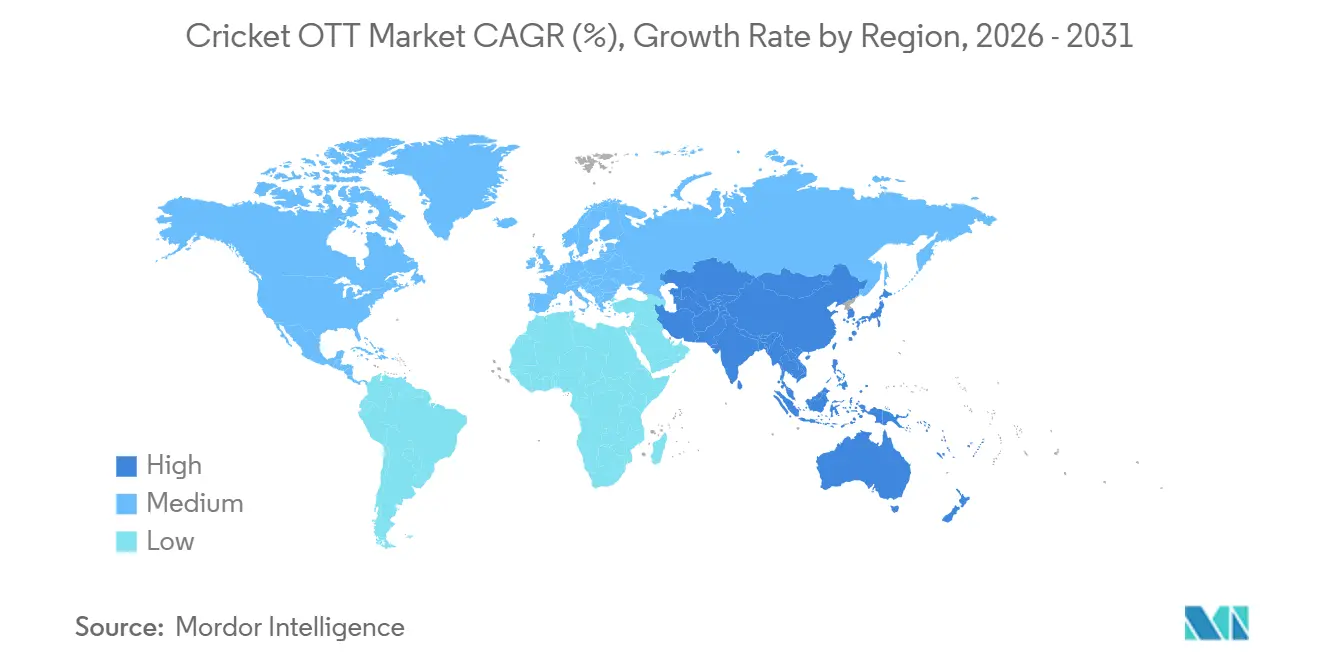

- By geography, Asia-Pacific accounted for 58.22% of revenue in 2025, while the Middle East is projected to record the fastest regional CAGR at 16.72% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Cricket OTT Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Monetization Through Digital Sports Rights Bundles | +3.5% | Global, led by Asia-Pacific and Europe | Short term (≤ 2 years) |

| Growth Of Hybrid Free And Premium Cricket Access Models | +2.8% | Asia-Pacific, spillover to MENA and North America | Medium term (2-4 years) |

| Rising Mobile-First Consumption During Live Match Windows | +2.5% | Asia-Pacific, MENA, Africa | Medium term (2-4 years) |

| Expansion Of Personalized Highlights, Replays, And Interactive Viewing | +2.0% | Global, with early gains in India and the UK | Long term (≥ 4 years) |

| Expansion Of Connected TV Adoption For Premium Cricket Streaming | 1.70% | Global, strongest in India, Australia, the UK, and North America | Medium term (2-4 years) |

| Increasing Demand For Multi-Language Commentary And Regionalized Content Experiences | 1.50% | Asia-Pacific, particularly India and multilingual cricket markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Monetization Through Digital Sports Rights Bundles

Sub-licensing and bundled rights deals are changing how the Cricket OTT market turns premium match inventory into revenue. JioStar and Sony Pictures Networks India split India’s 2025 and 2026 England tour rights between digital and linear delivery, which shows how platforms can create new value without displacing existing television distribution.[1]JioStar Team, “TATA IPL 2025: A Year of Firsts,” JioStar, jiostar.com The same pattern appeared in the UK, where DAZN secured IPL streaming rights and ITV retained a free-to-air window, preserving reach while building a premium digital layer. Bundled rights also generate shared audience data across screens, and that gives sellers better visibility into who watched, when they watched, and how to price targeted advertising. In the Cricket OTT market, that cross-platform data is becoming as important as the rights themselves because it raises monetization efficiency beyond what one isolated platform could achieve.

Growth Of Hybrid Free And Premium Cricket Access Models

Hybrid access is becoming a central growth lever in the Cricket OTT market because it widens reach without giving up the path to paid conversion. JioHotstar launched a cricket paywall in February 2025 with entry pricing from INR 149 per 3 months, which equals USD 1.8, and telecom bundles through Jio and Airtel lowered the practical access cost further for many users. This model helps platforms convert mass audiences into a structured subscriber base and then upsell premium plans with fewer swings in revenue from one tournament to the next. Free streaming is also being used as an entry strategy outside India, as Cricbuzz’s IPL 2026 MENA offering drew more than 300,000 daily unique viewers before any wider premium activation. As a result, the Cricket OTT market is moving toward blended revenue models where advertising still matters, but subscription depth is becoming more important for long-term stability.

Rising Mobile-First Consumption During Live Match Windows

Mobile viewing remains the largest access route in the Cricket OTT market, and platforms are designing products around this behavior rather than treating mobile as a reduced version of television. JioHotstar’s MaxView vertical format is gaining traction among mobile viewers during TATA IPL, indicating that mobile cricket viewing is becoming format-specific, not just screen-specific. In MENA, Cricbuzz users are spending considerable time per match on live streaming, suggesting that mobile engagement can remain strong enough to support targeted in-match ad placements. Regional language feeds are also widening the addressable audience, with digital regional-language watch time and regional-language connected TV watch time showing strong growth during IPL. In the Cricket OTT market, rights holders that combine low-cost access with mobile-native production are capturing viewers who may not watch a full broadcast but still generate meaningful season-long ad inventory.

Expansion Of Personalized Highlights, Replays, And Interactive Viewing

Personalized and rapid post-match content is extending the Cricket OTT market beyond the live event window. JioHotstar reduced the delay for match highlights to minutes after the final delivery, which narrowed the gap between live action and replay consumption and improved the value of on-demand content. FanCode also deployed AI-generated Hindi commentary during the 2025 Caribbean Premier League and signaled plans to scale that approach across more languages and competitions. That matters because smaller platforms can localize more leagues without carrying the full cost of traditional broadcast production. In the Cricket OTT market, short-form highlights and replay libraries are also working as a low-cost acquisition funnel because repeat engagement with quick content increases the chance that viewers later buy access to live matches.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Sports Rights Inflation Versus Monetization Lag | -2.80% | Global, with highest exposure in Asia-Pacific | Long term (≥ 4 years) |

| Advertising Concentration Around Peak Tournament Windows | -1.80% | Asia-Pacific, Europe, MENA | Medium term (2-4 years) |

| Regulatory Limits On High-Value Ad Categories | -1.20% | Asia-Pacific, with spillover to MENA | Short term (≤ 2 years) |

| Network Congestion and Streaming Quality Issues During High-Profile Cricket Matches | -1.60% | Global, particularly in high-concurrency mobile-first markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Sports Rights Inflation Versus Monetization Lag

The biggest structural pressure on the Cricket OTT market is the widening gap between rights pricing and realized monetization. The 2023-2027 IPL package reached INR 48,390 crore, or USD 5.7 billion, and later projections suggested that the next cycle may stay near USD 5.4 billion even as per-match values decline with a larger schedule.[2]Variety Staff, “IPL Media Rights Set to Plateau at USD 5.4 Billion in Next Cycle,” Variety, variety.com That shift shows that the market has moved from aggressive bidding toward rights-cost discipline, not because demand disappeared, but because monetization has not kept pace. JioStar’s provisions for onerous sports contracts are expected to peak in FY25 before declining in FY26. This trend indicates that even scaled operators continue to manage rights-related cost pressures carefully. For the Cricket OTT market, long-term winners will need stronger subscription ARPU, tighter control over production spending, and broader revenue streams beyond live match advertising.

Advertising Concentration Around Peak Tournament Windows

Advertising demand in the Cricket OTT market still depends too heavily on a small number of marquee fixtures. The ICC World Test Championship Final saw ad volumes decline significantly despite strong viewership because India did not participate, which exposed how much commercial demand is tied to a narrow set of team combinations. Industry estimates also suggested that the absence of an India-Pakistan group match could materially reduce tournament ad revenue from a single fixture. Concentration among advertisers adds another layer of risk, as a small group of leading advertisers accounted for the majority of total ad volumes in the ICC Champions Trophy. In the Cricket OTT market, platforms that cannot repackage unsold tournament inventory into broader season-long or on-demand products remain the most exposed to sudden revenue compression.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Content Type: International Matches Drive Revenue, Domestic Leagues Lead Growth

International matches accounted for 48.46% of content-type revenue in 2025, while domestic cricket leagues are projected to expand at a 16.42% CAGR through 2031, which shows that the Cricket OTT market still relies on premium national fixtures even as franchise formats gain ground. India bilateral series and ICC events remain the strongest pricing anchors because they gather the widest audience concentration and the highest advertiser urgency during short windows. Domestic leagues are building a different kind of value because they deliver longer seasons and more repeat viewing, which lowers dependence on a few isolated peak events. SA20 Season 3 recorded a 37% rise in global viewership, which supports the case for franchise cricket as a year-round streaming property rather than a secondary add-on. The European T20 Premier League also entered the calendar with distribution across JioStar, TNT Sports, HBO Max, Willow TV, and Cricbuzz, which extends the franchise model into new viewing markets.

That mix is changing the internal balance of the Cricket OTT market because longer domestic seasons can smooth revenue more effectively than short international windows. Regional and continental leagues occupy a middle layer where digital reach is improving, but rights structures remain more fragmented and per-match monetization still trails elite events. Other formats, including women’s cricket, short-form programming, and non-live cricket content, remain smaller today but are drawing more direct rights attention as platforms look for year-round engagement. The spread of archival and shoulder content is also widening the content base because platforms no longer need to rely only on live inventory to keep users active between major tournaments.

By Device Type: Mobile Scale Holds, Connected TV Improves Monetization

Smartphones and tablets held 60.23% of device-type revenue in 2025, while smart TVs are forecast to grow at a 16.36% CAGR through 2031, which means the Cricket OTT market remains mobile-led in scale but increasingly television-led in revenue quality. Affordable telecom bundles keep mobile access broad across South Asia and MENA, so that position is unlikely to weaken in absolute viewing terms during the forecast period. At the same time, connected TV has become a more important monetization surface because it attracts viewers with greater willingness to pay and stronger appeal for premium advertisers. IPL 2026 data showed connected TV reach rising 22-27% year over year and connected TV watch time increasing 20%, with season reach by game 45 already matching the whole prior season. That pattern suggests the Cricket OTT market is not moving from one device to another in a simple substitution cycle, but is layering usage across devices according to context.

Laptops and desktops still serve a stable base, especially among older viewers and work-adjacent consumption in developed markets. Other devices, including gaming consoles and voice-enabled screens, remain early-stage and have not yet changed the revenue profile of the Cricket OTT market in a major way. The more important shift is the rise of a dual-screen habit, where mobile handles alerts, social engagement, and statistics while smart TVs become the main match-viewing screen. Platforms that make movement between screens seamless are likely to capture more of the premium upside because session continuity strengthens both viewing time and ad delivery.

By Streaming Type: Live Leads Revenue, On-Demand Builds The Next Layer

Live streaming held 78.13% of streaming-type revenue in 2025, while on-demand streaming is projected to grow at a 16.58% CAGR through 2031, which keeps live action at the center of the Cricket OTT market while opening a faster-growing replay and highlights layer. Live streaming still commands the largest revenue base because cricket is most valuable when uncertainty, social conversation, and ad demand all peak at the same time. That economic logic remains hard to replicate with recorded content, even when replay quality is improving. JioHotstar’s AI-generated highlights, available within minutes after play ended, have started to reduce the historic gap between live and catch-up consumption.[3]JioStar Team, “TATA IPL 2025: A Year of Firsts,” JioStar, jiostar.com FanCode’s AI-led Hindi commentary during the 2025 Caribbean Premier League also showed that on-demand and localized production can scale more efficiently than full traditional broadcast workflows.

The result is that the Cricket OTT market is starting to extract more value from the same rights across a longer time window. FAST channels, replay libraries, and interactive feeds are widening the gap between a platform that only shows a live match and one that keeps the audience active before and after the match. Multi-cam feeds and immersive viewing options are also creating room for premium ad formats that sit outside the standard live stream. Over time, the strongest platforms in the Cricket OTT market are likely to be those that connect live and on-demand behavior into one viewing journey instead of treating them as separate products.

Geography Analysis

Asia-Pacific held 58.22% of revenue in 2025, which gave the region the largest share of the Cricket OTT market and kept it at the center of global demand through the current period. India remained the main engine because it combines unmatched audience scale, premium cricket rights, and expanding digital viewing depth. JioHotstar reached 503 million monthly active users in March 2025, which underlined how concentrated cricket streaming scale has become in the Indian market. JioHotstar also recorded a global peak concurrency of 72.5 million during the ICC Men’s T20 World Cup 2026 final, which reset the benchmark for live-streaming infrastructure at scale. TATA IPL 2026 later posted cumulative reach above 1.2 billion across TV and digital, with digital reach rising 15% year over year and connected TV reach increasing 22-27%, which showed that India is adding both depth and device diversity at the same time.

The Middle East is projected to record the fastest regional growth at 16.72% through 2031, which makes it the quickest expanding geography in the Cricket OTT market. That momentum is being supported by a large South Asian diaspora base and a rights environment that is becoming more consolidated around fewer streaming operators. STARZPLAY secured exclusive ICC cricket streaming rights across MENA through 2027 under its partnership with evision, which gave the platform a strong regional moat in premium tournament distribution. It also secured exclusive MENA streaming rights for the ICC Men’s T20 World Cup 2026 and the ACC Men’s T20 Asia Cup 2025, reinforcing the concentration of major rights in one regional service. Cricbuzz’s free IPL 2026 MENA stream drew more than 300,000 daily unique viewers and 26 million watch-time minutes in one weekend, which showed that ad-supported access can widen the audience beyond the premium subscription core.

Europe and North America formed the third major revenue cluster in the Cricket OTT market, driven mainly by Indian and Pakistani diaspora audiences and a gradual rise in mainstream T20 interest. The UK remained the leading European node, where TNT Sports secured a 5-year rights deal for international cricket played in India and DAZN paired with ITV to build a mixed paid and free-to-air IPL pathway. In North America, Willow by Cricbuzz and TrillerTV formalized a streaming partnership aimed at the United States and Canadian diaspora, while franchise cricket in the United States is helping create a local viewing base over time. South America and continental Europe remain early-stage parts of the Cricket OTT market, but the launch of the European T20 Premier League marked the first structured attempt to build OTT-first cricket demand in those geographies.

Competitive Landscape

The Cricket OTT market is moderately concentrated, but that concentration is organized by region rather than by one global leader. JioStar operated at the largest visible scale in 2026 because it combined IPL, ICC, and India bilateral rights on one platform and turned that portfolio into unmatched reach in its home market. JioHotstar delivered 300 million subscribers and 840 billion minutes of watch time during TATA IPL 2025, which showed how strong rights concentration can translate into both scale and retention when the product is built around cricket. The company also cut onerous sports contract provisions by 31% in FY26, which suggested that monetization discipline had started to improve after a period of heavy rights pressure. JioStar’s 2025 and 2026 England tour arrangement with Sony also showed that sub-licensing is becoming a normal commercial tool in the Cricket OTT market rather than a one-off exception.

DAZN followed a different strategy in the Cricket OTT market by building a cross-country sports portfolio instead of relying on one single cricket home base. Its USD 2.14 billion Foxtel acquisition in April 2025 expanded its position in Australia and gave it stronger control over premium sports distribution through Kayo Sports and Fox Cricket. STARZPLAY strengthened its position by concentrating on MENA, where exclusive ICC rights through 2027 created a defensible regional franchise in premium cricket streaming. These moves show that the strongest platforms are not chasing every right everywhere, but are instead assembling dominant clusters where distribution, pricing, and audience data reinforce each other. The Cricket OTT market therefore rewards platforms that can control premium rights in one region and then deepen monetization through subscriptions, targeted advertising, and distribution partnerships.

Specialists are also shaping the Cricket OTT market by filling gaps that larger rights holders do not always prioritize. FanCode reported a user base of 160 million and used AI-generated commentary, personalization, and selective league acquisition to serve a broader set of emerging competitions and adjacent cricket geographies. Its expansion into Bangladesh, Sri Lanka, and Nepal signaled that regional scaling can be built through focused cricket properties rather than only blockbuster global tournaments. White-space opportunities remain strongest in women’s cricket OTT and AI-powered multilingual streaming, where rights are becoming more separable and production automation can improve economics. In the Cricket OTT market, that leaves room for both major integrated platforms and more specialized services, which is why competition remains active even though premium rights are concentrated in a limited number of hands.

Cricket OTT Industry Leaders

Disney+ Hotstar Pvt. Ltd.

JioStar India Pvt. Ltd.

Amazon.com, Inc.

DAZN Group Limited

YouTube LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2026: The European T20 Premier League (ETPL), Europe's first ICC-sanctioned T20 franchise league, signed broadcast agreements with JioStar (India), TNT Sports and HBO Max (UK and digital), and Willow TV and Cricbuzz (US, MENA, and Southeast Asia) for its inaugural season from August 26 to September 20, 2026.

- July 2026: FanCode exclusively livestreamed the India vs. Zimbabwe 2026 T20I series in India in partnership with Zee Entertainment's Unite8 Sports channels, extending its position as a key aggregator of bilateral cricket digital rights.

- March 2026: JioHotstar introduced new immersive viewing capabilities for the ICC Men's T20 World Cup 2026, including vertical live streaming, 360-degree viewing, multi-camera feeds, and enhanced interactive features, strengthening its premium cricket OTT offering.

- March 2026: For IPL 2026, JioStar secured 27 advertising partners across sectors including technology, FMCG, and consumer electronics, reflecting growing advertiser confidence in cricket-centric OTT platforms and hybrid monetization models.

Global Cricket OTT Market Report Scope

Cricket OTT Market refers to the ecosystem of over-the-top digital platforms that stream live and on-demand cricket content directly to viewers over the internet. It includes subscription apps, ad-supported platforms, broadcaster-owned streaming services, and sports aggregators that deliver matches, highlights, and related programming across devices.

The Cricket OTT Market Report is Segmented by Content Type (International Cricket Matches, Regional / Continental Cricket Leagues, and Domestic Cricket Leagues), Device Type (Smartphones and Tablets, Smart TVs, and Laptops and Desktops), Streaming Type (Live Streaming, and On-Demand Streaming), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| International Cricket Matches |

| Regional / Continental Cricket Leagues |

| Domestic Cricket Leagues |

| Other Content Type |

| Smartphones and Tablets |

| Smart TVs |

| Laptops and Desktops |

| Other Device Type |

| Live Streaming |

| On-demand Streaming |

| Other Streaming Type |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Nigeria | |

| Rest of Africa |

| By Content Type | International Cricket Matches | |

| Regional / Continental Cricket Leagues | ||

| Domestic Cricket Leagues | ||

| Other Content Type | ||

| By Device Type | Smartphones and Tablets | |

| Smart TVs | ||

| Laptops and Desktops | ||

| Other Device Type | ||

| By Streaming Type | Live Streaming | |

| On-demand Streaming | ||

| Other Streaming Type | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current and forecast value of the Cricket OTT market?

The Cricket OTT market size is projected at USD 8.81 billion in 2026 and is expected to reach USD 18.58 billion by 2031, growing at a CAGR of 16.10% from 2026 to 2031.

Which content category generates the most revenue in cricket streaming?

International matches lead revenue generation, with a 48.46% share in 2025, because India bilateral series and ICC events still attract the highest premium audience concentration.

Which device is growing fastest for cricket OTT viewing?

Smart TVs are the fastest-growing device type, with a 16.36% CAGR through 2031, even though smartphones and tablets still held the largest 60.23% revenue share in 2025.

Why does live streaming remain the largest revenue stream in cricket OTT?

Live streaming held 78.13% of streaming-type revenue in 2025 because real-time viewing, social urgency, and premium ad demand remain strongest during live matches.

Which region is expanding fastest in cricket OTT services?

The Middle East is projected to grow at a 16.72% CAGR through 2031, supported by diaspora demand, rising OTT adoption, and concentrated premium rights ownership.

What is shaping competition among cricket streaming platforms?

Competition is being driven by control of premium rights, regional exclusivity, telecom and broadcast partnerships, and platform features such as AI-generated highlights, multi-language commentary, and connected TV optimization.

Page last updated on: