South America Coworking Office Spaces Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

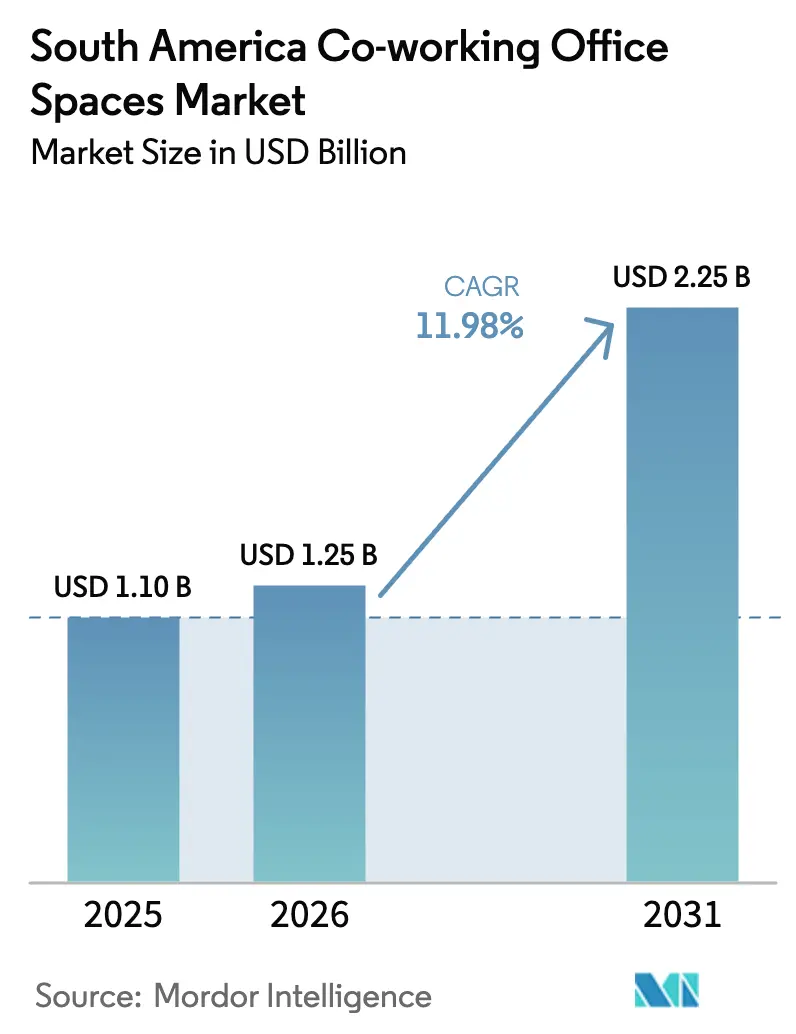

| Base Year Market Size (2025) | USD 1.10 Billion |

| Market Size (2026) | USD 1.25 Billion |

| Market Size (2031) | USD 2.25 Billion |

| Growth Rate (2026 - 2031) | 11.98% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South America Coworking Office Spaces Market Analysis by Mordor Intelligence

South America Coworking Office Spaces Market size was valued at USD 1.10 billion in 2025 and is estimated to grow from USD 1.25 billion in 2026 to USD 2.25 billion by 2031, at a CAGR of 12% during the forecast period (2026-2031). Momentum stems from enterprises tightening capital allocation, start-ups conserving runway, and professionals relocating to secondary hubs where premium inventory is scarce[1]fDi Intelligence, “Emerging Tech Hubs in Latin America Close Gap With Major Cities,” fdiintelligence.com. Distributed venture investment, firmer four-day office mandates, and Grade-A supply clustered in a handful of corridors are reshaping where and how flexible space is consumed. Brazil remains the revenue anchor, yet demand is dispersing toward Peru, Chile, and Colombia as public incentives and lifestyle migration redirect talent. Operators that blend capital-light franchising with neighborhood-focused footprints are well-positioned to capture this structural real estate reset.

Key Report Takeaways

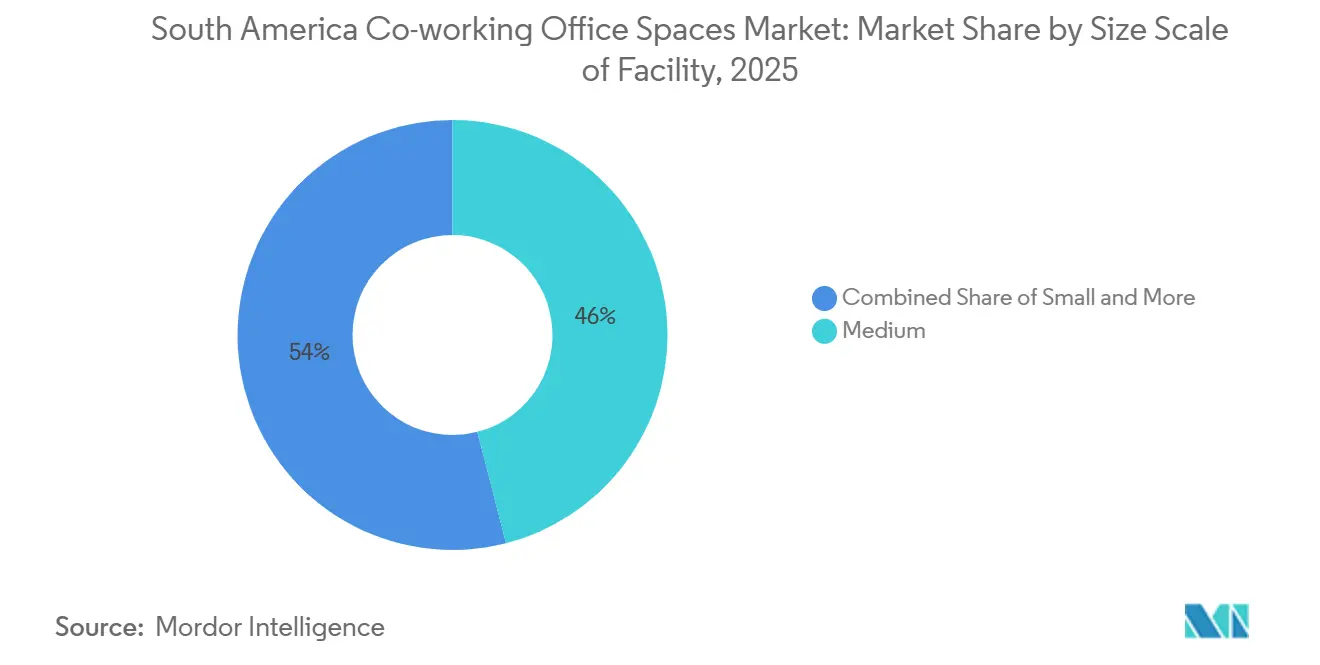

- By facility size, medium-sized centers led with 46% of the South American co-working office space market share in 2025, while large formats are projected to expand at a 12.7% CAGR through 2031.

- By sector, information technology and IT-enabled services commanded 42.7% of 2025 revenue; banking, financial services, and insurance is expected to accelerate the fastest at 12.9% CAGR to 2031.

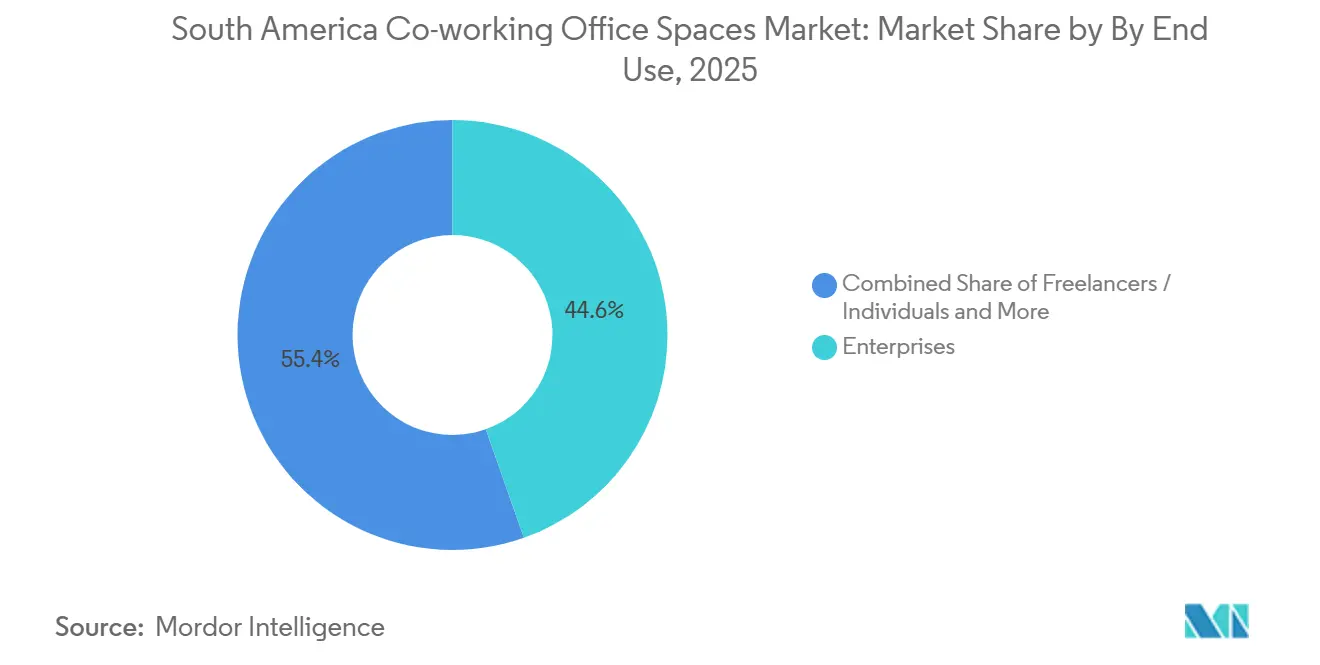

- By end use, enterprises accounted for 44.6% of 2025 revenue, whereas the start-ups and others segment is forecast to grow at 12.2% during 2026-2031.

- By geography, Brazil accounted for 35.6% of regional turnover in 2025, but Peru is forecast to register the fastest expansion at 13.2% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South America Coworking Office Spaces Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid growth of start-ups and SMEs in Brazil | +2.8% | Brazil with spillover to Argentina and Chile | Medium term (2-4 years) |

| Hybrid work models boosting demand for flexible leases | +3.1% | Brazil, Chile, Colombia | Short term (≤ 2 years) |

| Investor-developer alliances adding Grade-A supply | +2.2% | São Paulo, Santiago, Buenos Aires, Bogotá | Medium term (2-4 years) |

| Government-funded creative-economy districts | +1.5% | Chile (Santiago, Valparaíso, Concepción), Colombia (Bogotá, Medellín) | Long term (≥ 4 years) |

| 15-minute-city zoning pilots fostering micro-hubs | +1.2% | São Paulo downtown, Santiago, Buenos Aires | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Growth of Start-ups and SMEs in Brazil

Brazil’s technology scene generated more than 1.7 million IT and BPO positions by 2025, creating a steady pipeline of small teams that prefer pay-as-you-go desks to multi-year leases. SEBRAE subsidies and municipal incubators have nudged informal ventures toward formal space equipped with business services. Early-stage funding has contracted, yet the share flowing to Florianópolis, Belo Horizonte, and other secondary hubs has risen, forcing operators to seed locations outside São Paulo’s core. Residential developers are now pre-leasing common areas as co-working zones, ensuring residents have professional offices within walking distance. Together, these forces expand the South American co-working office space market by absorbing latent suburban demand while stabilizing operator revenue during Brazil’s volatile credit cycle.

Hybrid Work Models Boosting Demand for Flexible Short-term Leases

Global attendance norms have settled around 4 days a week, giving occupiers clarity to right-size headquarters and outsource overflow to flexible centers. São Paulo posted 250,000 m² of leasing in 2024, the highest since 2019, led by tech and services tenants. Enterprises are splitting portfolios: core teams stay in owned towers, while agile squads rotate through co-working memberships that can be tweaked quarterly. IWG captured this shift by signing 899 mostly suburban centers in 2024 under franchise deals that avoid lease liabilities. Operators that package reserved desks, on-demand rooms, and digital mail handling are now harvesting multi-threaded revenue streams from the same client, fortifying the South America Coworking Office Spaces Market against economic swings.

Investor-Developer Partnerships Expanding Grade-A Supply in Tier-1 Metros

Joint ventures completed 84,132 m² of Class A stock in São Paulo during 2024, headlined by JK Square, Corporativo Faria Lima, and Estaiada Corporate. Another 261,706 m² remains under construction, yet prime vacancies in Pinheiros and Paulista sit below 3%, revealing a split market where quality still prices at a premium. Flexible operators that pre-lease entire floors secure landlord-funded fit-outs and below-market rents during the lease-up phase. Chile’s CORFO and similar Colombian grants mirror this model, co-financing space for exporters and easing entry for co-working brands. Such alliances lower capital intensity, extend geographic reach, and collectively lift the South America Coworking Office Spaces Market size as new supply comes online with embedded flexible footprints.

Government-funded Creative-economy Districts Catalyzing Boutique Hubs in Chile and Colombia

Colombia’s Orange Economy zones in Bogotá and Medellín bundle tax breaks, infrastructure upgrades, and cultural programming that naturally feed co-working tenants into nearby hubs. Impact Hub Medellín’s 2,200 m² facility supports 3,000 participants, who report an average 77% increase in sales since 2018[2]Impact Hub Network, “Impact Hub Medellín,” impacthub.net. In Chile, municipal innovation hubs link entrepreneurs with universities, funneling start-ups into commercial centers as they scale. Operators that embed within these districts gain subsidized tenants and smoother permitting, trimming six to twelve months off expansion timelines. Over time, the resulting network of boutique locations diversifies the South America Coworking Office Spaces Market beyond its reliance on tier-1 CBD towers.

Restraints Impact Analysis*

| Restraint | ( ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High competition and oversupply in São Paulo CBDs | −1.8% | São Paulo (Chácara Santo Antônio, Itaim, Marginal Pinheiros) | Short term (≤ 2 years) |

| Limited penetration in secondary and interior cities | −1.2% | Interior Brazil, Argentine provinces, Peruvian regions beyond Lima | Medium term (2-4 years) |

| Complex title and zoning processes | −0.9% | Brazil, Argentina, Colombia | Medium term (2-4 years) |

| Security and insurance cost spikes | −0.7% | São Paulo, Rio de Janeiro, Buenos Aires, Bogotá | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Competition and Oversupply Risk in São Paulo CBDs

Vacancy rates reached 48.16% in Chácara Santo Antônio and 43.64% in Itaim during Q4 2024, prompting landlords to offer rent-free months and improvement allowances. WeWork’s September 2024 evictions highlighted how overstretching into soft districts erodes margins when dues cannot keep pace with lease obligations[3]Reuters, “WeWork Brazil Eviction,” reuters.com. With 250,000 m² of fresh stock arriving in 2025, pressure on weak nodes will persist. Operators must avoid the siren song of low headline rents in distressed corridors and instead pivot to high-occupancy zones such as Faria Lima, where asking rents average BRL 283.85/m² (USD 56.8) per month and vacancy is only 10.4%. Disciplined site selection shields the broader South America Coworking Office Spaces Market from destabilizing price wars in Brazil’s largest city.

Limited Penetration in Secondary and Interior Cities Despite Latent Demand

Florianópolis, Belo Horizonte, Lima, and Montevideo hosted 25.5% of new VC-backed firms in 2023, yet flexible space in these cities remains fragmented and undercapitalized. Interior landlords rarely release contiguous blocks, and fiber connectivity outside capitals lags, forcing operators to fund private links and generators. Broadband penetration across Latin America averaged only 12% in recent years, leaving performance gaps that discourage enterprise tenants. The capital outlay to harden space against power cuts and bandwidth drops extends payback periods beyond the tolerance of many investors. Until infrastructure gaps close or public partners co-invest, the South American coworking office space market will under-index in promising interior locales.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Size and Scale of Facility: Large-Format Centers Anchor Enterprise Demand

The medium category captured 46% of the South America Coworking Office Spaces Market share in 2025, reflecting its sweet spot for 20- to 100-person teams. Large formats, however, are projected to log a 12.7% CAGR between 2026 and 2031, the quickest of any size class. In practice, corporations now outsource entire floors as managed campuses, bundling reception, IT, cleaning, and security into a predictable monthly invoice. IWG’s capital-light signings and Selina’s Remote Year acquisition illustrate how franchising and hospitality hybrids can stretch this model across suburban belts. Operators that tier portfolios—micro hubs for freelancers, mid-size suites for scale-ups, and campus floors for corporates—keep customers within the South American co-working office space ecosystem as it matures.

Large facilities generally exceed 5,000 m² and combine private suites with communal cafes and event terraces. During 2024-2025, new deliveries such as JK Square offered co-working tenants early-move-in incentives, effectively subsidizing fit-outs while towers leased up. Medium centers, often 2,000-5,000 m², remain the workhorse, balancing cost and amenity depth. Small hubs under 2,000 m² proliferate in 15-minute-city districts, converting retail shells into 10- to 30-desk lofts that capture local freelancers. This tiered spectrum underpins the enduring breadth of the South American coworking office space market.

By Sector: IT/ITES Dominates While BFSI Surges on Resilience Mandates

Information technology and IT-enabled services accounted for 42.7% of 2025 revenue, cementing their role as the anchor tenant pool. Banking, financial services, and insurance is on track to post the fastest 12.9% CAGR through 2031 as regulators demand geographically dispersed recovery sites. Financial institutions now weigh ISO 27001 certification and compliant data rooms before signing, enabling premium pricing for operators that invest in audit-ready infrastructure. Professional services firms follow closely, using flexible centers to plant client-facing teams in secondary cities without long leases. Meanwhile, energy, life sciences, and legal practices are trickling into the South American co-working office space market as project-based assignments multiply.

The steady IT/ITES base shields occupancy when capital markets tighten, while BFSI contracts provide multiyear revenue and push footprint diversification across Brazil, Peru, and Chile. Operators securing data-sovereign cloud connectivity and biometric entry can monetize this compliance premium, lifting the overall market share of South American co-working office spaces captured by high-spec centers.

By End Use: Enterprises Provide Stability, Start-ups Propel Growth

Enterprises accounted for 44.6% of revenue in 2025, signing master leases for hybrid campuses that de-risk corporate real estate lines by shifting capex to opex. Start-ups and others will record a 12.2% CAGR to 2031, fueled by early-stage companies conserving cash during lean fundraising windows. Flexible memberships—hot desks for founders, private pods as teams expand—let operators upsell workspace alongside events and cloud credits. Freelancers buy day passes and meeting rooms, delivering high-margin ancillary income, though churn remains brisk.

Balanced tenant mixes cap start-up exposure at roughly one-third of revenue, insulating operators when venture funding cycles cool. Partnerships with residential developers, such as Magik LZ retrofits, bundle co-working fees into condo dues, hardwire occupancy, and extend the reach of the South American co-working office space market into purely residential blocks.

Geography Analysis

Brazil generated 35.6% of regional turnover in 2025, buoyed by 150,182 m² of net absorption in the São Paulo Class A segment, the strongest uptake in seven years. While total CBD vacancy slipped to 17.35%, disparities are stark: Pinheiros sits near full occupancy at premium monthly rents of USD 35.4/m² (BRL 176.85), whereas Chácara Santo Antônio lingers above 48%, confirming a bifurcated market where micro-location trumps headline supply. Government initiatives relocating state offices downtown boost weekday footfall, feeding demand for micro-hubs within ten minutes of transit. Yet oversupply pockets warn operators to champion disciplined site selection, preserving returns and reinforcing confidence in the South America Coworking Office Spaces Market.

Peru is emerging as the fastest-growing market in the region through 2031, supported by Lima’s rising position as a nearshore outsourcing hub. Local operator Comunal serves a broad base of corporate clients across key locations such as Santa Cruz, Panorama, and El Polo. Meanwhile, global brands Regus and Spaces have expanded their footprint across Lima, offering flexible formats including hourly desks and day passes. Further expansion into secondary cities such as Arequipa and Cusco is positioning operators ahead of large multinational landlords. As broadband infrastructure and business activity continue to strengthen in these cities, early entrants are likely to benefit from first-mover advantages.

Chile and Colombia benefit from public co-funding and ADN designations that pull creative entrepreneurs into subsidized districts. Impact Hub’s Medellín campus demonstrates the job-creation halo these schemes deliver, drawing mission-driven ventures that later graduate into commercial centers. Argentina, recovering from macro turbulence, presents opportunistic upside; Regus and Spaces maintain Buenos Aires footprints ready to capitalize once currency and policy volatility abates. Smaller nations—Uruguay and Ecuador foremost—leverage lifestyle migration, with Montevideo emerging on the digital-nomad circuit and attracting hospitality-co-working hybrids. Collectively, these divergent trajectories affirm that the South America Coworking Office Spaces Market will rely on country-specific playbooks rather than a one-size-fits-all roll-out.

Competitive Landscape

The leading providers, WeWork, IWG (Regus, Spaces), and Selina, continue to dominate the formal flexible workspace landscape, while still leaving room for regional operators and single-site independents to expand.WeWork reduced its Brazilian footprint in 2025 and shifted toward a lease-matching model that aligns rental obligations more closely with occupancy levels. However, the evictions reported in September 2024 highlighted the structural risks that arise when fixed liabilities outpace revenue performance.IWG pursued an asset-light growth strategy, executing numerous capital-light signings in 2024, with a strong focus on suburban locations. This demonstrates how franchise and management agreement models can enable expansion without significant balance-sheet exposure.

Second-tier challengers exploit local knowledge. Communal in Peru, Impact Hub in Colombia, and HQ in mixed Brazilian-Peruvian corridors leverage community ties and SDG-aligned programming to differentiate from transactional desks. Meanwhile, landlords dabbling in self-operated flexible floors add a quasi-competitor layer, yet many pivot to partnerships once occupancy analytics reveal expertise gaps. Technology is the new battleground: global chains invest in proprietary apps and IoT sensors for dynamic pricing, whereas independents deploy lighter SaaS stacks, constraining data-driven revenue optimization.

Consolidation rumblings persist. Institutional investors scour fragmented holdings for roll-up plays, especially operators with two to five sites and positive EBITDA yet limited scale capital. A merger wave could raise the concentration of the South American co-working office space market, but regulatory hurdles and cultural fit may temper the pace. For now, competitive dynamics reward asset-light franchisors and mission-driven boutiques alike, provided each remains disciplined on lease terms and location economics.

South America Coworking Office Spaces Industry Leaders

WeWork Inc.

IWG plc (Regus, Spaces)

Selina Hospitality

Co-Work LatAm

IOS OFFICES

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: WeWork has expanded its Coworking Partner Network to nearly 2,000 locations globally, with a strategic focus on international markets, notably Mexico in Latin America. By collaborating with local coworking operators, WeWork seeks to enhance the accessibility of flexible workspace solutions and streamline space bookings via its digital platform. This expansion holds significant importance for the Latin American market, as the presence of global players like WeWork bolsters demand and lends credibility to local coworking ecosystems.

- August 2025: In a significant stride for the Latin American coworking scene, Woba, a Brazil-based operator of coworking and flexible offices (previously known as BeerOrCoffee), clinched around USD 13.5 million in funding in 2025. This capital injection is earmarked for broadening its network of flexible workspaces throughout Brazil.

South America Coworking Office Spaces Market Report Scope

| Small |

| Medium |

| Large |

| Information Technology & ITES |

| BFSI (Banking, Financial Services and Insurance) |

| Business Consulting & Professional Services |

| Other Services (Retail, Life-sciences, Energy, Legal, etc.) |

| Freelancers / Individuals |

| Enterprises |

| Start-ups & Others |

| Brazil |

| Argentina |

| Chile |

| Colombia |

| Peru |

| Rest of South America |

| By Size & Scale of Facility | Small |

| Medium | |

| Large | |

| By Sector | Information Technology & ITES |

| BFSI (Banking, Financial Services and Insurance) | |

| Business Consulting & Professional Services | |

| Other Services (Retail, Life-sciences, Energy, Legal, etc.) | |

| By End Use | Freelancers / Individuals |

| Enterprises | |

| Start-ups & Others | |

| By Country | Brazil |

| Argentina | |

| Chile | |

| Colombia | |

| Peru | |

| Rest of South America |

Key Questions Answered in the Report

What is the forecast CAGR for flexible workspaces in South America through 2031?

The South America Coworking Office Spaces Market is projected to register a 12% CAGR between 2026 and 2031, rising from USD 1.25 billion in 2026 to USD 2.25 billion by the end of the period.

Which country currently contributes the largest revenue?

Brazil generated 35.6% of regional turnover in 2025, driven by São Paulo’s strong absorption of premium inventory.

Which country is expected to expand the fastest?

Peru is forecast to grow at 13.2% during 2026-2031 as Lima strengthens its near-shore outsourcing role and secondary cities open new centers.

Which facility size segment is set for the highest growth?

Large-format centers are projected to post the quickest 12.7% CAGR, reflecting enterprise appetite for campus-style environments with bundled services.

Why is BFSI demand accelerating?

Banking and insurance firms must meet stricter operational-resilience rules, prompting them to lease distributed, ISO-certified space, driving a 12.9% CAGR in the segment through 2031.

Page last updated on: