Cough Assist Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

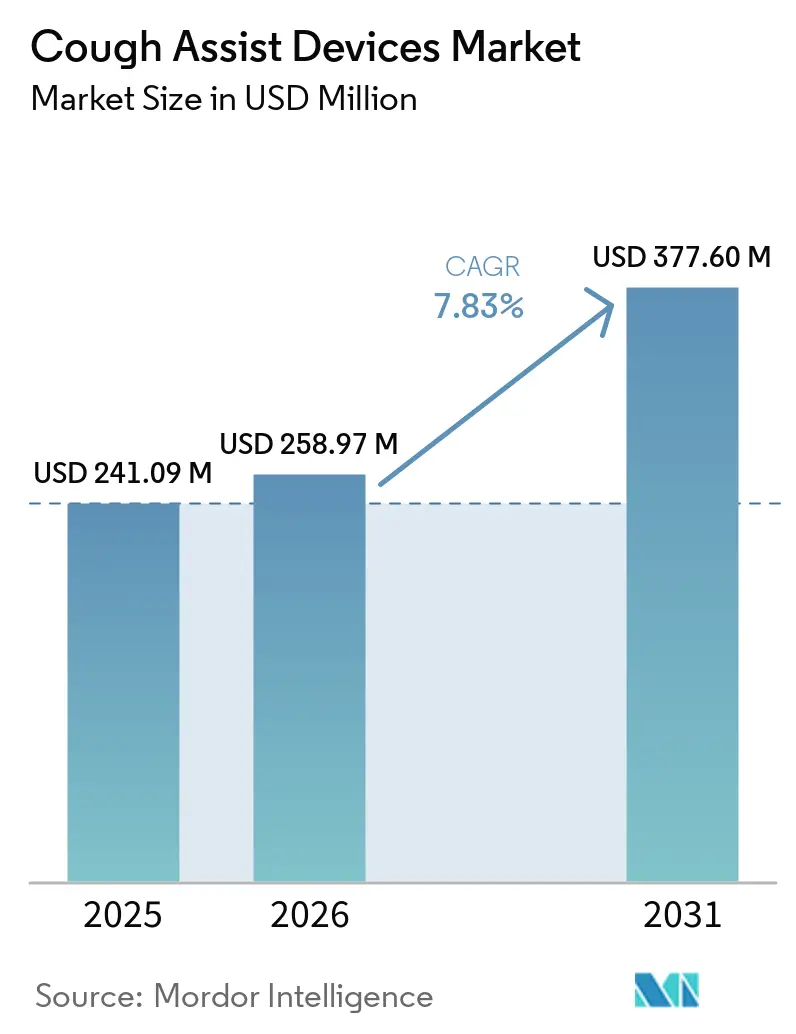

| Market Size (2026) | USD 258.97 Million |

| Market Size (2031) | USD 377.60 Million |

| Growth Rate (2026 - 2031) | 7.83% CAGR |

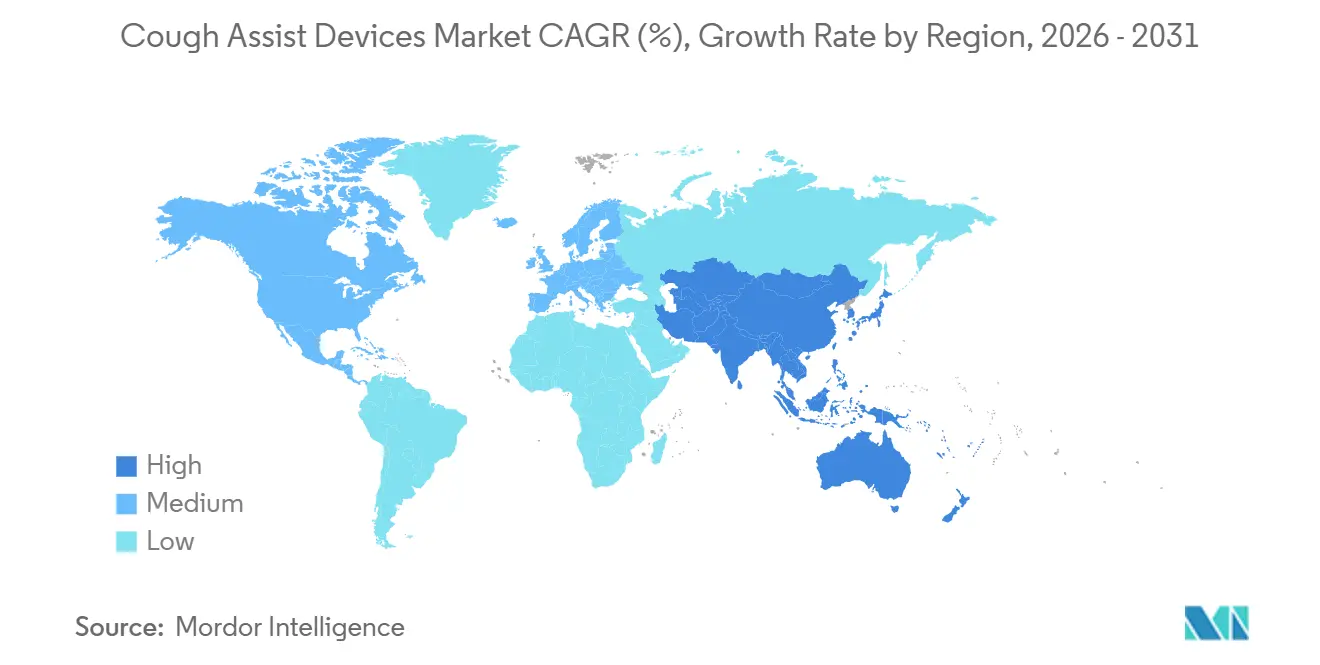

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cough Assist Devices Market Analysis by Mordor Intelligence

The Cough Assist Devices Market size is projected to be USD 241.09 million in 2025, USD 258.97 million in 2026, and reach USD 377.60 million by 2031, growing at a CAGR of 7.83% from 2026 to 2031.

Demand reflects a structural shift from episodic inpatient use to continuous home management as remote device adjustments become standard clinical practice and enable broader discharge eligibility to home settings. Expanding coverage criteria from public and private payers, including clarified coding for integrated ventilators, is lowering administrative friction and favoring single-platform solutions that bundle mechanical insufflation-exsufflation with ventilation and airway care. The cough assist devices market benefits from rising survival among neuromuscular disease populations that continue to need airway-clearance support after initial stabilization, which sustains recurring device utilization over longer care journeys. Clinical pathways and pediatric guidelines embed mechanical insufflation-exsufflation across acute care and home care, which strengthens institutional adoption and standardizes practice patterns across regions. Competitive dynamics are influenced in 2026 by the aftermath of Philips Respironics’ 2024 U.S. consent decree, which created near-term white space for rivals while quality remediation continues.

Key Report Takeaways

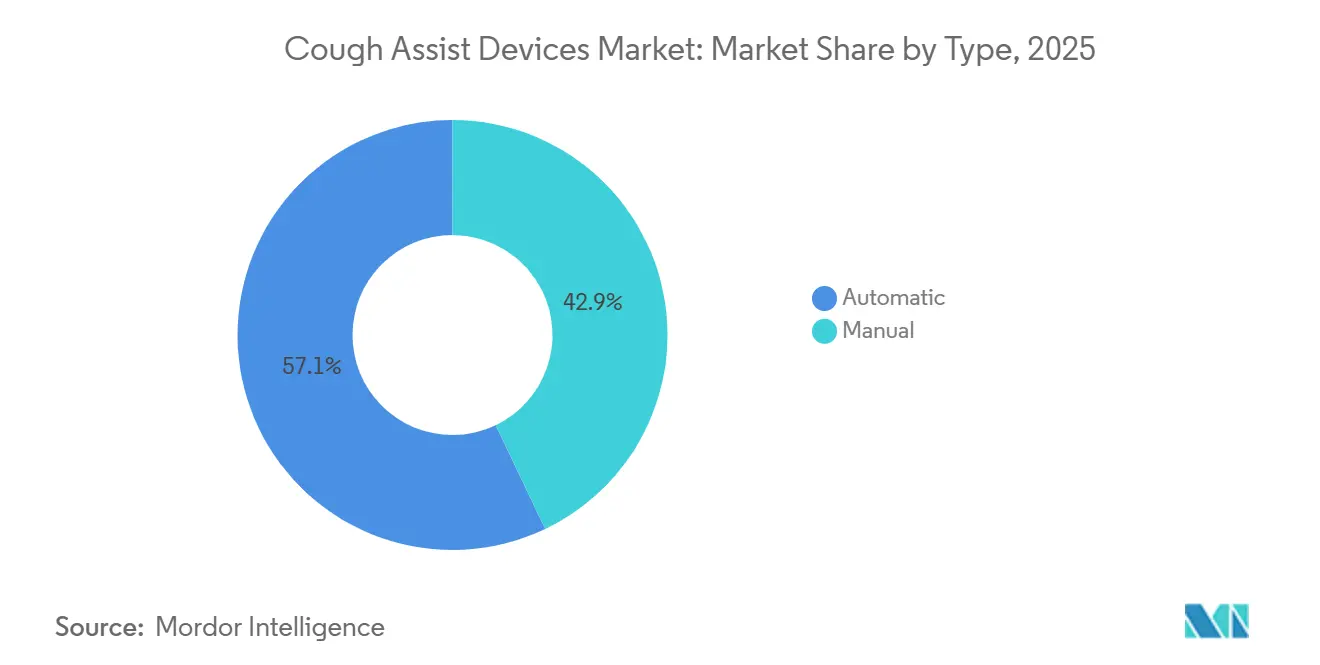

- By type, automatic cough assist systems led with 57.10% revenue share in 2025 and are projected to grow at a 9.01% CAGR through 2031.

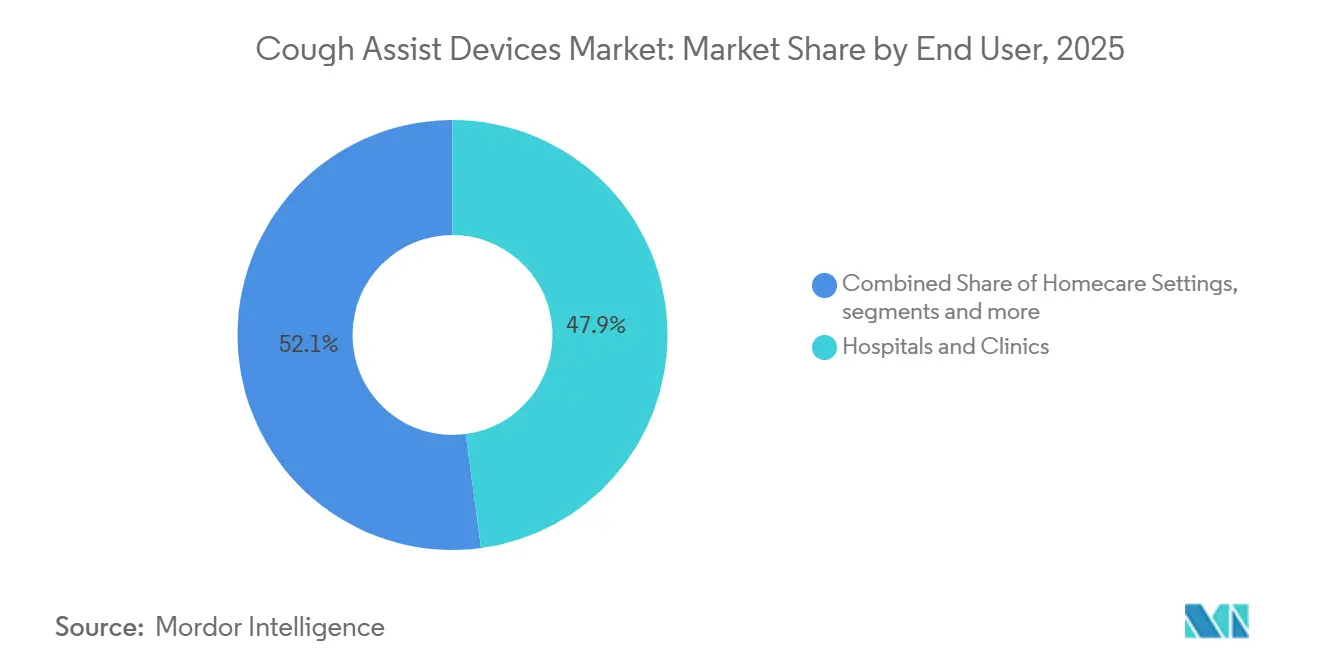

- By end user, hospitals and clinics accounted for 47.89% of 2025 revenue while homecare settings are projected to expand at an 8.67% CAGR through 2031.

- By product type, face mask interfaces held 51.23 of 2025 revenue while tracheostomy or endotracheal adapters are forecast to grow at a 9.13% CAGR through 2031.

- By geography, North America held 43.07% of 2025 revenue while Asia-Pacific is projected to grow at a 9.06% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Cough Assist Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing neuromuscular disease prevalence and survival driving cough augmentation demand | +1.2% | Global, pronounced in North America, EU | Medium term (2-4 years) |

| Shift to home-based respiratory care and telehealth-enabled MI-E support | +1.8% | North America, Asia-Pacific, EU | Short term (≤ 2 years) |

| Expanding reimbursement and coding pathways for MI-E and integrated ventilators | +1.6% | North America (CMS), select EU markets | Medium term (2-4 years) |

| Clinical guideline endorsements across acute and pediatric care | +1.0% | Global, with North America leadership | Long term (≥ 4 years) |

| Integration of MI-E with ventilators and digital platforms enabling care bundling | +1.4% | Global | Medium term (2-4 years) |

| Pediatric complex care programs formalizing MI-E in home ventilation | +0.8% | North America, EU, spill-over to APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Neuromuscular Disease Prevalence and Survival Driving Cough Augmentation Demand

Improving survival in spinal muscular atrophy, amyotrophic lateral sclerosis, and Duchenne muscular dystrophy is expanding the pool of patients who live long enough to require chronic cough augmentation. A narrative review reported invasive ventilation use in ALS cohorts of 5% to 10% in the United States and Europe, which signals enduring respiratory support needs as disease-modifying care advances. Pediatric findings align with this pattern, where MI-E is often initiated when peak cough flow falls below 160 L per minute in multidisciplinary programs that integrate home-based therapy. After adoption of daily home MI-E, one center reported a 75% reduction in respiratory infection-related hospitalizations, which underscores the role of consistent airway-clearance routines outside hospital settings. Sydney Children’s Hospitals Network now endorses MI-E use from six months of age in relevant neuromuscular conditions, which sets a clear precedent for early initiation in pediatric care. As these standards diffuse, the cough assist devices market captures recurring demand tied to chronic management rather than short-term episodic use[1]Sydney Children’s Hospitals Network, “Mechanical Insufflation-Exsufflation (MI-E) use in Physiotherapy,” SCHN Guideline 2020-130 v2.0, health.nsw.gov.au.

Shift to Home-Based Respiratory Care and Telehealth-Enabled MI-E Support

The migration of respiratory care to home environments accelerated and remote supervision has become central to effective MI-E support. U.S. Medicare now permits clinicians to adjust respiratory assist and ventilatory parameters remotely, which expands home eligibility by lowering the need for in-person titration visits. Integrated homecare programs such as those rolled out by Air Liquide combine telemonitoring, video consultations, and multidisciplinary follow-up that streamline adherence and intervention timing across large patient panels. China’s home oxygen therapy policy discourse has emphasized remote monitoring and leasing models that raise treatment compliance and support continuity of care beyond hospitals. In Japan, 2024 fee schedule changes increased guidance and device-related points for home high-flow therapy, which signaled a broader policy shift toward reimbursed home-based respiratory interventions. As these operational frameworks mature, the cough assist devices market benefits from higher discharge confidence and fewer administrative barriers to home initiation.

Expanding Reimbursement and Coding Pathways for MI-E and Integrated Ventilators

Coverage evolution is aligning mechanical insufflation-exsufflation with multi-function ventilator bundles, which changes prescribing incentives and device selection. CMS coding adds E0468 for dual-function devices and recognizes E0467 for multi-function platforms that combine oxygen, nebulization, suction, and cough assist, both under all-inclusive monthly servicing structures. Documentation rules updated for 2026 require modifiers that attest to medical necessity or notify expected denials, which reduces ambiguity for providers using integrated platforms in complex cases. Private insurers mirror this trajectory with explicit MI-E criteria such as peak cough flows below 300 liters per minute paired with qualifying neuromuscular diagnoses that help reduce avoidable denials when prescriptions match policy language. Cigna’s coverage policy lists qualifying ICD codes and references device 510(k) clearances such as Breas Clearo, which tightens diagnostic targeting while offering a clear path to coverage where criteria are met. Internationally, Japan’s 2024 revisions on home high-flow therapy reinforce global convergence toward funded home respiratory solutions that complement MI-E in integrated care plans.

Clinical Guideline Endorsements Across Acute and Pediatric Care

Institutional guidance is elevating MI-E from a last-resort measure to a standard airway-clearance option across inpatient and chronic care. The Children’s Hospital of Philadelphia pathway includes cough assist alongside suction and chest physiotherapy in respiratory compromise management for neuromuscular patients, which normalizes MI-E across acute and transitional care. Sydney Children’s Hospitals Network details pediatric pressure ranges and practical setup considerations that help standardize care in younger cohorts with varied diagnoses and clinical severities. Germany’s S3 guideline on non-invasive ventilation addresses cough assist in neuromuscular conditions, which signals that MI-E is embedded in broader European respiratory standards of care. These endorsements influence purchasing committees and training agendas, which in turn lower start-up barriers for new service lines around home-based and post-acute care. As pathways mature, the cough assist devices market benefits from consistent algorithms that guide initiation thresholds, titration steps, and follow-up intervals across care settings.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Uneven reimbursement/funding and out-of-pocket burden across markets | -1.1% | Global, acute in Asia-Pacific, Latin America | Short term (≤ 2 years) |

| Mixed evidence and clinician variability limiting adoption | -0.7% | Global, pronounced in markets lacking local guidelines | Medium term (2-4 years) |

| Interface tolerance and bulbar airway collapse challenges in subgroups | -0.5% | Global, particularly severe NMD populations | Long term (≥ 4 years) |

| Documentation/coding complexity and accessory denials under bundled ventilator codes | -0.6% | North America, select EU markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Uneven Reimbursement/Funding and Out-of-Pocket Burden Across Markets

Coverage disparities slow adoption where explicit national policies or benefit designs are not in place. U.S. LCDs define MI-E criteria that reduce ambiguity for qualifying diagnoses, yet many markets operate under case-by-case approvals that lengthen lead times and elevate financial exposure for families and providers. Chinese policy commentary on home oxygen care has flagged quality and oversight concerns while still promoting remote-monitored home models to raise adherence, which shows uneven regulatory maturity across sub-segments of home respiratory care. In Germany, patient guidance documented access constraints for a cough-treatment drug even after EU approval, which illustrates administrative frictions that can spill over into respiratory care pathways. The net effect is slower ramp-up outside mature funding environments and a tendency to defer MI-E starts despite clinical eligibility. As payers update codes and documentation policies, the cough assist devices market can recover some of this demand through clearer eligibility rules and integrated equipment bundles.

Mixed Evidence and Clinician Variability Limiting Adoption

Practice variation is common because device settings and patient tolerance differ across populations and care settings. A European review reported variability in inspiratory times and pressure targets used for MI-E in children, which reflected the lack of standardized pediatric protocols and uneven training resources. In Japan, policy support for home high-flow therapy coexists with staff shortages and low awareness that restrict uptake, which indicates implementation gaps even when reimbursement pathways are present. Patients with bulbar dysfunction may struggle with mask or mouthpiece tolerance due to airway collapse during exsufflation, which can lead to underuse unless tracheostomy adapters are considered. Randomized trials remain limited for head-to-head comparisons with other airway-clearance modalities, which preserves debate in settings with conservative formulary norms. Bridging education and standard operating procedures improves consistency and supports a more predictable adoption curve in the cough assist devices market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Automatic Devices Propelled by Algorithmic Precision

Automatic systems accounted for 57.10% of 2025 revenue and are projected to grow at a 9.01% CAGR through 2031, which outpaces manual variants as synchronized triggering and adaptive control refine therapy delivery. Evidence shows adaptive control can eliminate pressure overshoot and sharply damp oscillations compared with conventional PID strategies, which supports higher peak cough flows with more consistent cycles[2]Liangsong Lu et al., “Adaptive control of airway pressure during the expectoration process in a cough assist system,” Frontiers in Bioengineering and Biotechnology, frontiersin.org. Algorithmic synchronization such as Cough-Trak aligns insufflation and exsufflation with patient efforts, which reduces clinician workload and standardizes session quality across variable breathing patterns. Recent 510(k) activity such as Breas Clearo reflects growing investment in automation coupled with connected workflows that support home titration and follow-up without clinic visits. These features help the cough assist devices market as integrated ventilator platforms bundle cough assist into standard respiratory care packages favored by payers.

Manual devices retain a role in cost-constrained environments and during acute exacerbations where hands-on coordination is preferred by bedside teams. Usage is stabilizing in facilities that emphasize tactile cues and direct control over trigger timing during complex airway management. Even in these settings, data logging and remote monitoring are becoming common requirements for discharge planning, which shifts preference toward automatic systems with connectivity. The cough assist devices industry is responding with patient-friendly workflows that flatten training curves for caregivers while supporting remote oversight protocols mandated by payers. As cloud portals and telemonitoring expand, the relative advantage of automatic devices grows, which reinforces their position at the center of the cough assist devices market in both inpatient transitions and long-term home care.

By End User: Homecare Settings Gaining Traction via Bundled Payment Models

Hospitals and clinics held 47.89% of 2025 revenue due to the concentration of acute respiratory failure episodes and post-extubation care in monitored environments. Homecare settings are projected to expand at an 8.67% CAGR as coding updates allow remote parameter adjustments and integrated ventilator bundles cover accessories and servicing within a single rental construct. This alignment with telehealth reduces travel burdens and enables timely adaptations, which helps sustain regular therapy and lower exacerbation risk. Large-scale homecare contracts such as Air Liquide’s in Madrid demonstrate how multidisciplinary teams can integrate telemonitoring and coaching to maintain adherence at scale. The cough assist devices market size for homecare settings is projected to expand significantly through 2031 as payers seek to avoid preventable readmissions with platform-based device bundles.

Transitions from inpatient to home are smoother when care teams rely on standardized pathways and connected devices. The Children’s Hospital of Philadelphia pathway embeds MI-E in routine respiratory management for neuromuscular compromise, which normalizes discharge planning that includes home instruction and follow-up. Baxter’s airway clearance portfolio and point-of-care programs support continuity by combining equipment, training assets, and integration with clinical systems that streamline ordering and oversight. As remote portals capture adherence signals, therapy plans can be adjusted between visits, which helps stabilize outcomes. The cough assist devices market reflects these operational gains as home-based delivery becomes the preferred destination for chronic management that requires recurring adjustments and coaching. Over time, this pushes more volume to integrated platforms that simplify supply chains for providers and payers while improving patient experience.

By Product Type: Tracheostomy Adapters Surge on Invasive Ventilation Integration

Face mask interfaces commanded 51.23% of 2025 revenue due to ease of use across age groups and compatibility with non-invasive care pathways. Tracheostomy and endotracheal adapters are projected to grow at a 9.13% CAGR, which aligns with higher pressure requirements and more consistent flows in patients who cannot tolerate masks or mouthpieces. These adapters integrate naturally with life-support ventilators that now include cough assist functions under bundled payment models recognized by CMS. As plans consolidate equipment into multi-function devices, invasive interfaces gain relevance because circuits and accessories are packaged with platform rentals. This visibility supports a stronger position for invasive accessories within the cough assist devices market where ventilator-dependent patients require robust secretion management.

Mouthpieces and dedicated circuits serve stable outpatients and bridge transitions between hospital and home. Mouthpiece delivery is common in volume-assured protocols for progressive neuromuscular disease where patients can coordinate sessions with caregiver support. Dedicated circuits help reduce contamination risk in facilities with strict infection control, which improves operational consistency in long-term care. The cough assist devices market size for invasive adapters is supported by rising deployment on multi-function platforms and clearer coverage rules for integrated solutions. As clinical guidelines continue to standardize pressure ranges and session structures, product selection will track institutional preferences shaped by outcomes and usability in complex patient groups.

Geography Analysis

North America accounted for 43.07% of 2025 revenue, supported by defined LCD criteria for MI-E and coding structures for integrated ventilators that clarify documentation and payment. Pediatric pathways such as CHOP’s embed cough assist in acute and chronic management, which improves referral consistency across specialties and strengthens standard operating procedures. Private payer policies including Univera specify peak cough expiratory flow thresholds and qualifying neuromuscular diagnoses, which reduce uncertainty for prescribing clinicians in outpatient settings. Philips’ 2024 U.S. consent decree reoriented near-term competitive dynamics, which created opportunities for peers to expand while compliance and remediation proceed. As integrated platforms scale and remote adjustments become routine, the cough assist devices market continues to rely on unified coding and coverage that support multi-year home use cycles.

Asia-Pacific is projected to grow at a 9.06% CAGR supported by policy updates and evolving care models around home respiratory support. Japan’s 2024 medical fee changes increased guidance and device-related points for home high-flow therapy, which signals official support for home-based care that complements MI-E in suitable patients. Chinese policy discourse on home oxygen therapy has emphasized remote monitoring and compliance improvement, which reflects the region’s focus on sustaining therapy outside hospitals. Disaster preparedness guidance in Japan highlights oxygen backup readiness across major events, which keeps continuity planning central to respiratory support programs. As remote models normalize and clinical protocols spread, the cough assist devices market benefits from wider eligibility and growing acceptance of home-based regimens in large urban centers.

Europe’s landscape is anchored by Germany’s S3 guideline that addresses cough assist within non-invasive ventilation care pathways for chronic respiratory insufficiency in neuromuscular patients. Regional expansion of integrated homecare services, exemplified by Air Liquide’s multi-year Spain program, pairs predictive analytics with multidisciplinary interventions that reduce secondary-care use[3]Air Liquide, “Air Liquide awarded large contract in Spain for home respiratory care,” Air Liquide, airliquide.com. The ecosystem includes ventilator platforms with native cough assist functions and telemedical connectivity that align with European preferences for portable life-support solutions. Country-level reimbursement frameworks support neuromuscular cohorts through public insurance or national health systems, which sustains regular utilization across outpatient care. With institutional guidance broadening and homecare programs scaling, the cough assist devices market size in Europe is poised to expand with standardized pathways and connected device portfolios.

Competitive Landscape

The cough assist devices market shows moderate fragmentation with share redistribution following events that reshaped competitive positioning in key regions. Philips Respironics remains a reference brand with a broad respiratory portfolio, while the 2024 U.S. consent decree created near-term constraints and encouraged purchasers to evaluate alternatives. Philips has outlined fresh investments in U.S. manufacturing and R&D to reinforce quality systems and scale advanced health technology production, which can improve supply resilience when fully implemented. Competitors leveraged the opening to position integrated platforms that bundle airway care with ventilation and digital supervision. This bundling model aligns with coding and payer preferences that prioritize simplified equipment fleets and predictable servicing arrangements.

Baxter advanced airway clearance capabilities with the 2024 launch of the Vest APX System, which reduced device bulk and updated interface design for usability and adherence support. Baxter’s tools can complement cough assist by addressing mucus mobilization through high-frequency chest wall oscillation as part of multi-modality care plans in complex patients. The company’s care programs integrate ordering, training, and digital touchpoints that support longitudinal adherence and therapy optimization for home-based users. As connected platforms document session quality, clinicians can react to usage patterns in near real time. These practices strengthen outcomes and reduce administrative friction while reinforcing the position of bundled solutions in the cough assist devices market.

Breas and Löwenstein drive competition through compact life-support ventilators that integrate cough assist functions and telemedical connectivity suited for home and travel. Breas Clearo received 510(k) clearance and supports synchronized therapy that shortens titration and helps maintain comfortable cycles in variable breathing patterns. Löwenstein’s prisma VENT50-C features integrated cough support and cloud connectivity that align with payer expectations for remote adjustments and serviceability across large homecare fleets. Regional homecare leaders such as Air Liquide extend differentiation by embedding telemonitoring and multidisciplinary interventions into routine workflows, which produce earlier interventions and fewer avoidable escalations. Across these moves, strategy converges on platform integration, device connectivity, and data-driven case management that together reinforce adoption in the cough assist devices market.

Cough Assist Devices Industry Leaders

Baxter (Hillrom)

Breas Medical AB

Koninklijke Philips N.V. (Respironics)

ABM Respiratory Care

Air Liquide Medical Systems (EOVE)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Breas Medical Inc – Americas highlighted its Clearo Cough Assist device, aiming to transition respiratory care into home environments. The company underscored features like TreatRepeat and Synchrony Beep technologies, touting their benefits in easing therapy initiation, minimizing laryngeal closure and patient guarding, and enhancing progressive lung inflation.

- September 2025: Air Liquide secured a five-year contract with the Community of Madrid to deliver home healthcare services for 70,000 respiratory patients, deploying multidisciplinary teams (nurses, physiotherapists, pulmonologists, clinical psychologists) alongside telemonitoring, video consultations, and AI-driven predictive algorithms integrated into healthcare professionals' portals, aiming to improve patient outcomes while reducing secondary-care admissions.

- September 2024: Baxter International launched The Vest Advanced Pulmonary Experience (APX) System at the North American Cystic Fibrosis Conference, receiving FDA 510(k) clearance earlier in 2024. The next-generation airway clearance system features a 19% smaller and 30% lighter control unit than its predecessor, streamlined garment design with wicking fabric and Velcro closure, and an intuitive touch screen, demonstrating a 43% reduction in disease-specific hospitalizations in prior clinical evaluations of the underlying Vest System (Model 105) HFCWO technology.

Global Cough Assist Devices Market Report Scope

As per the scope of the report, a cough assist device, referred to as a mechanical insufflation-exsufflation (MI-E) machine, facilitates the removal of lung secretions in patients with compromised cough strength. By alternating between positive air pressure for inhalation and rapid negative pressure for exhalation, the device effectively replicates a natural, deep cough. It is predominantly utilized in managing neuromuscular conditions such as ALS or in post-injury scenarios, with patient interface options including a mask, mouthpiece, or tracheostomy tube.

The cough assist devices market is segmented by type, end user, product type, and geography. By type, the market is segmented as automatic and manual. By end user, the market is segmented as hospitals & clinics, homecare settings, ambulatory care settings, long-term care/rehabilitation centers, and others. By product type, the market is segmented as mouthpiece, face mask, tracheostomy / endotracheal adapter, and cough assist circuits. By geography, the market is segmented as North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD) for the above segments.

| Automatic |

| Manual |

| Hospitals & Clinics |

| Homecare Settings |

| Ambulatory Care Settings |

| Long-term Care / Rehabilitation Centers |

| Others |

| Mouthpiece |

| Face Mask |

| Tracheostomy / Endotracheal Adapter |

| Cough Assist Circuits |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Type | Automatic | |

| Manual | ||

| By End User | Hospitals & Clinics | |

| Homecare Settings | ||

| Ambulatory Care Settings | ||

| Long-term Care / Rehabilitation Centers | ||

| Others | ||

| By Product Type | Mouthpiece | |

| Face Mask | ||

| Tracheostomy / Endotracheal Adapter | ||

| Cough Assist Circuits | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected size and growth of the cough assist devices market by 2031?

The cough assist devices market size is projected at USD 377.60 million by 2031, with a 2026-2031 CAGR of 7.83%.

Which product type is growing fastest within cough assist solutions?

Tracheostomy and endotracheal adapters are forecast to grow at 9.01% due to integration with invasive ventilation and consistent delivery needs.

How are reimbursement changes influencing adoption of cough assist devices?

CMS coding for integrated ventilators and clearer private-payer criteria reduce denials and favor bundled platforms with remote adjustments and single-rental economics.

What segments lead demand across care settings for these devices?

Hospitals and clinics lead revenue today while homecare settings are the fastest growing as telehealth and integrated bundles expand remote management.

Which regions are expected to contribute the most to future growth of cough assist devices?

Asia-Pacific shows the highest projected growth rate as policy updates and home respiratory models scale, while North America remains the largest revenue base.

How are clinical guidelines shaping usage of mechanical insufflation-exsufflation?

Pathways from CHOP, SCHN, and Germany’s S3 NIV guideline embed MI-E into acute and chronic care plans, which standardizes initiation and follow-up across age groups.

Page last updated on: