Coronary Scoring Balloons Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 169.79 Million |

| Market Size (2031) | USD 247.17 Million |

| Growth Rate (2026 - 2031) | 7.80% CAGR |

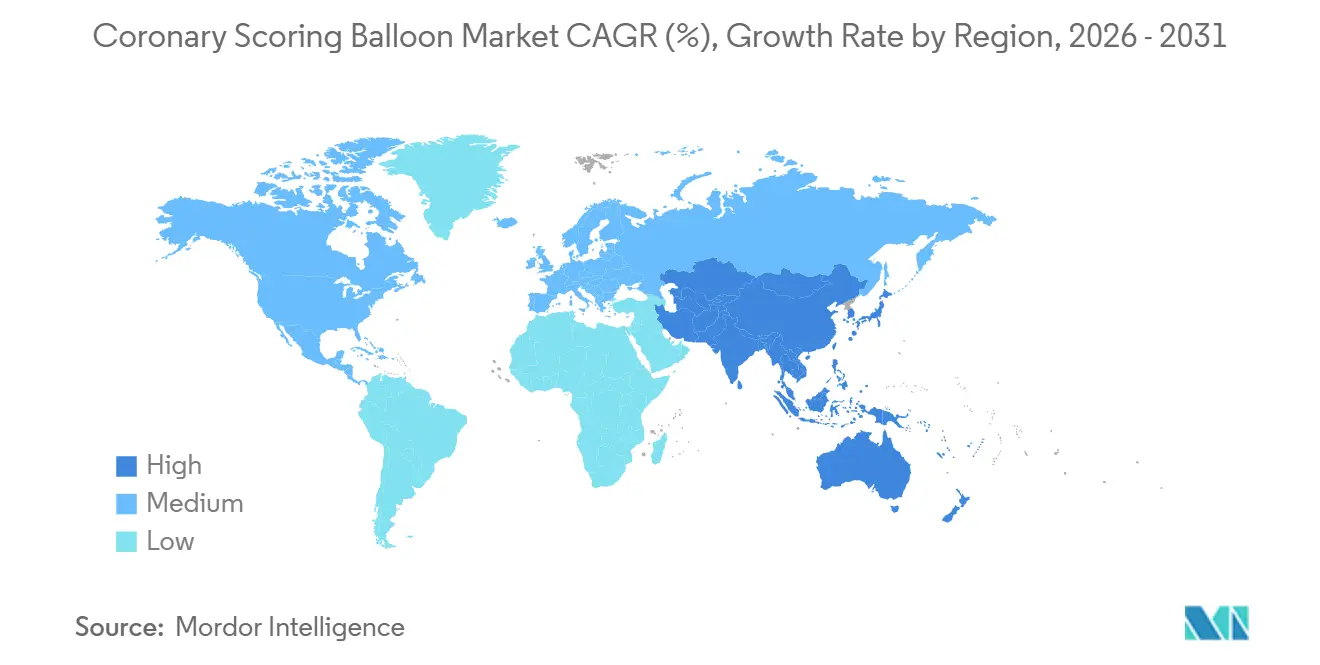

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

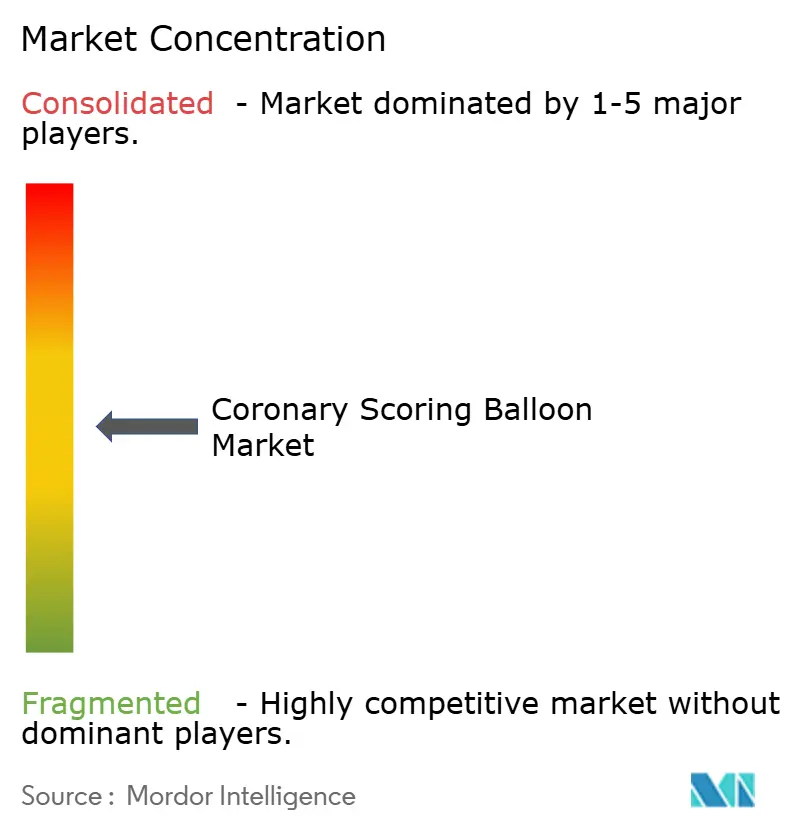

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Coronary Scoring Balloons Market Analysis by Mordor Intelligence

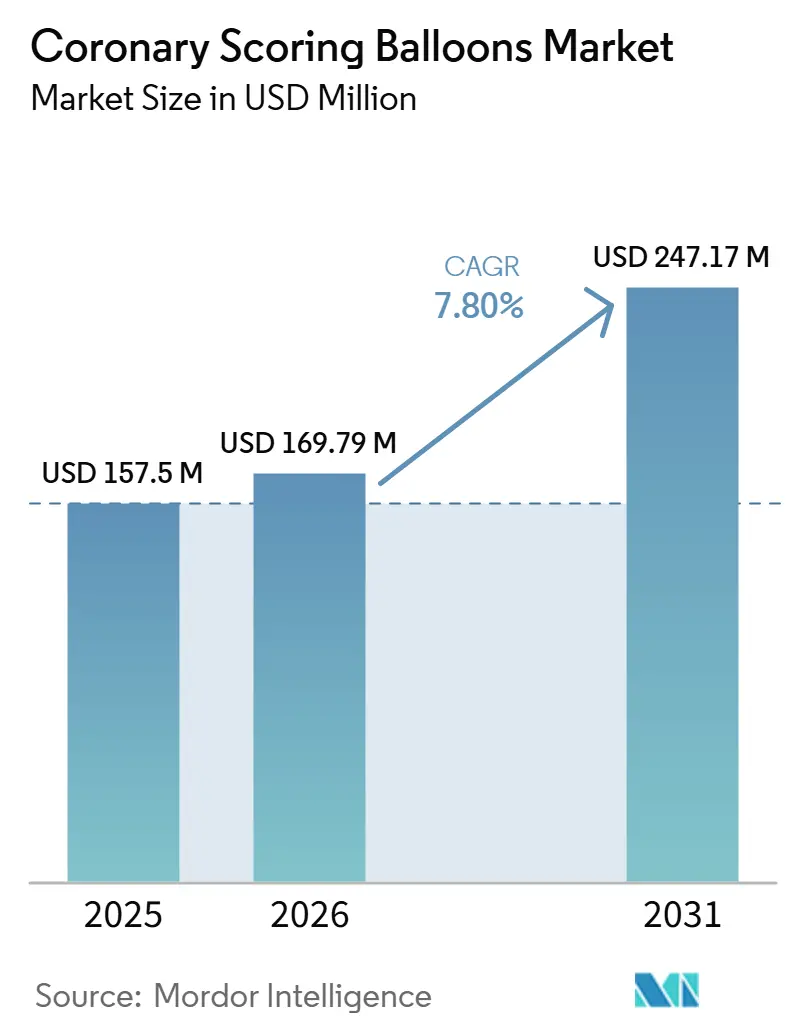

The Coronary Scoring Balloons Market size is projected to be USD 157.5 million in 2025, USD 169.79 million in 2026, and reach USD 247.17 million by 2031, growing at a CAGR of 7.80% from 2026 to 2031.

The coronary scoring balloons market is supported by the rising burden of calcified coronary lesions, since contemporary evidence shows coronary artery calcification in more than 90% of men and more than 67% of women above 70 years of age, and moderate to severe calcification in 18% to 26% of patients undergoing PCI. The addressable patient pool is also widening because aging, chronic kidney disease, and type 2 diabetes continue to raise lesion complexity across PCI practice, and a large 2025 cohort study showed a steep rise in calcified plaque prevalence with age in China. In the coronary scoring balloons market, adoption is shaped more by the need for dependable lesion preparation and stent expansion than by price competition alone, because clinical use is tied to complex coronary anatomy and operator control. The coronary scoring balloons market also faces a more segmented treatment pathway, since imaging-guided PCI is improving device selection while intravascular lithotripsy is drawing severe calcification cases into a separate therapy track. The coronary scoring balloons market will continue to find opportunity in outpatient PCI expansion, imaging-led precision workflows, and product designs that improve deliverability in tortuous anatomy.

Key Report Takeaways

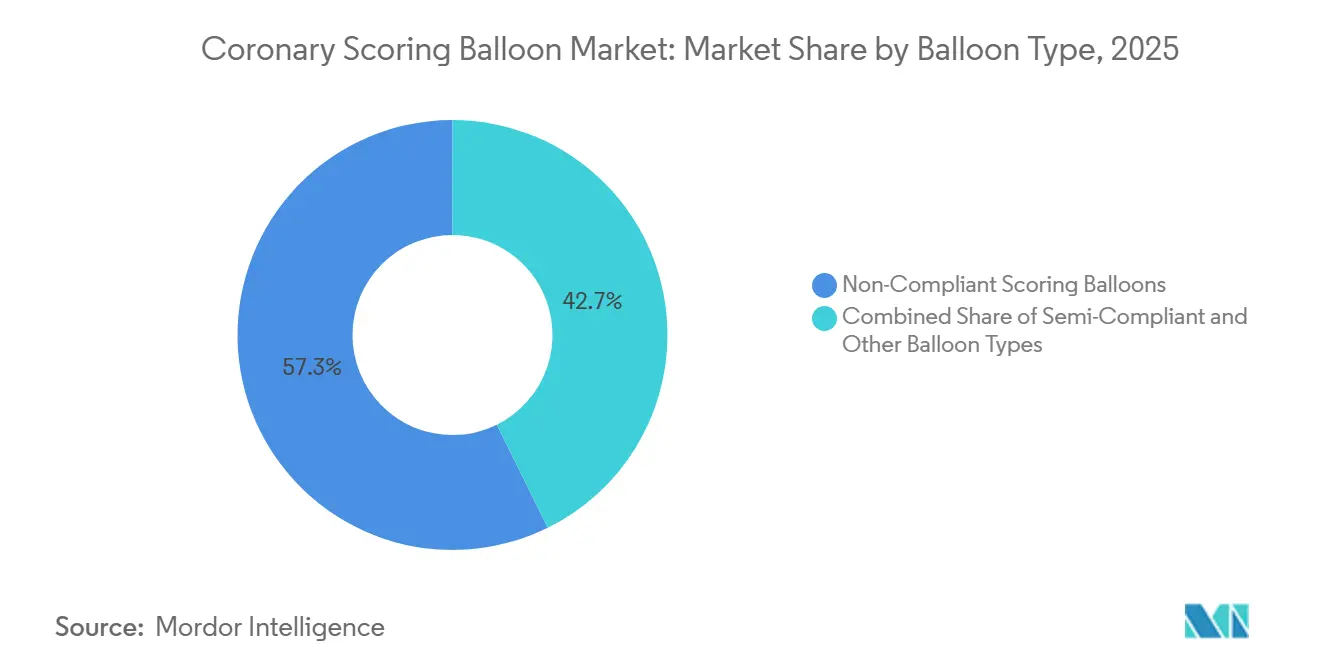

- By balloon type, non-compliant scoring balloons held 57.31% of the coronary scoring balloons market share in 2025, and the same segment is projected to record the fastest growth at 8.82% CAGR through 2031.

- By material, nylon accounted for 46.20% share of the coronary scoring balloons market size in 2025, while polyurethane is forecast to expand at a 9.21% CAGR through 2031.

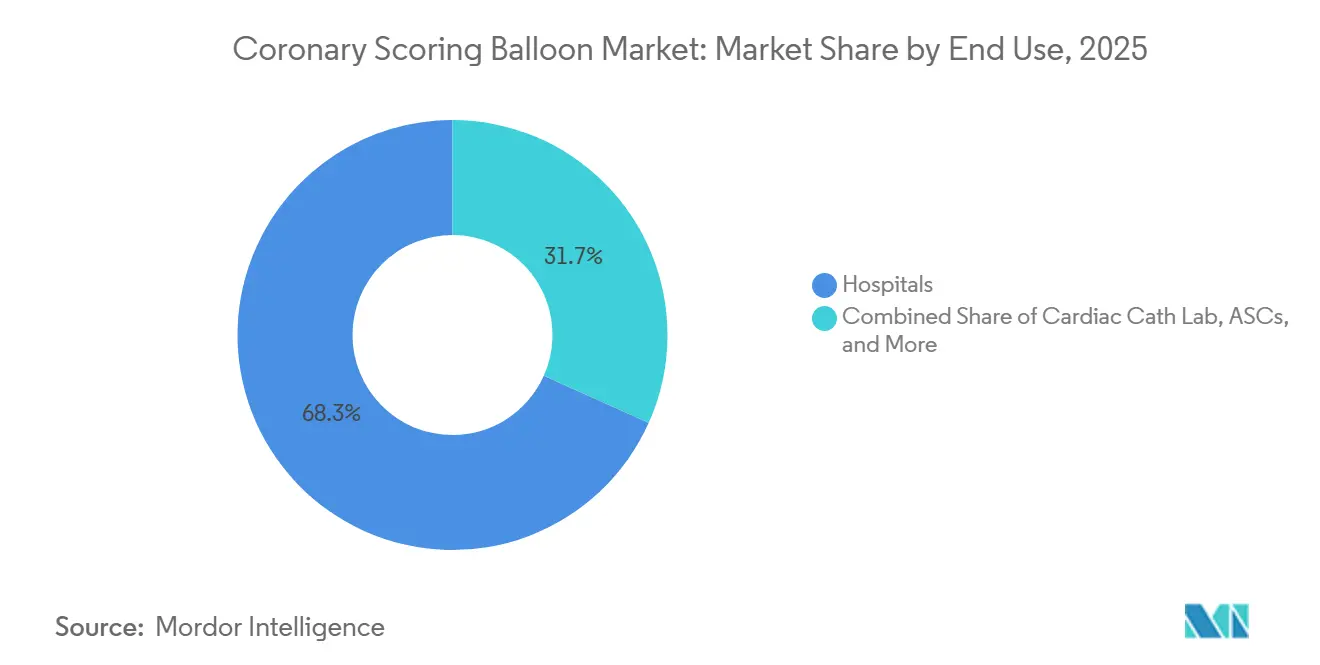

- By end use, hospitals captured 68.30% revenue share in 2025, while cardiac catheterization laboratories are projected to advance at an 11.42% CAGR through 2031.

- By geography, North America held 38.10% share of the coronary scoring balloons market size in 2025, while Asia-Pacific is forecast to grow at a 10.12% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Coronary Scoring Balloons Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Burden of Calcified Coronary Lesions | +1.8% | Global | Long term (≥ 4 years) |

| Shift Toward Predictable Lesion Preparation Before Stenting | +1.4% | North America and Europe, Japan | Medium term (2-4 years) |

| Expansion of PCI-Capable Cath Labs and Ambulatory Settings | +0.9% | North America, APAC | Medium term (2-4 years) |

| Clinical Preference for Lower Dissection and Better Stent Expansion Outcomes | +0.8% | North America, Europe | Medium term (2-4 years) |

| Underused Intravascular Imaging Creates Upside for Precision Scoring Use | +0.7% | APAC, North America | Long term (≥ 4 years) |

| Reimbursement Favoring Device-Based Lesion Preparation Over Reintervention | +0.5% | North America, Western Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Burden of Calcified Coronary Lesions

The coronary scoring balloons market is closely tied to the growing burden of calcified coronary disease, because lesion calcification is no longer treated as a minor procedural issue in PCI practice[1]Source: PubMed Central, “Contemporary Management of Calcified Coronary Artery Disease,” PubMed Central, pmc.ncbi.nlm.nih.gov. Contemporary reviews showed moderate to severe calcification in 18% to 26% of PCI patients, which keeps demand centered on devices that can modify plaque in a controlled manner. Chronic kidney disease adds another layer of demand because it accelerates medial calcification through a pathway that differs from standard atherosclerosis, which broadens the target population beyond older age groups alone. A 2025 study in China found calcified plaque prevalence rose from 11.7% in patients younger than 45 to 36.0% in those older than 75, which suggests lesion complexity in Asia-Pacific will rise with volume growth. For the coronary scoring balloons market, this demand pattern is structural because it follows patient mix and lesion severity rather than a short-term purchasing cycle.

Shift Toward More Predictable Lesion Preparation Before Stenting

The coronary scoring balloons market is benefiting from a wider preference for predictable lesion preparation before stenting, especially in cases where uncontrolled balloon expansion can compromise final results. A 2024 systematic review and meta-analysis reported that cutting or scoring balloons used before stenting were linked to a 33% reduction in target lesion revascularization compared with conventional balloons, without increasing perforation, myocardial infarction, or all-cause mortality. This matters because operators are placing more value on lesion-level control than on simple predilation success. The same shift is creating added demand from drug-coated balloon workflows, since better lesion preparation is being tested as a way to improve outcomes in in-stent restenosis and related use cases. In the coronary scoring balloons market, this trend lifts unit demand by converting cases that once relied on plain non-compliant balloons into scoring balloon procedures.

Expansion of PCI-Capable Cath Labs and Ambulatory Settings

The coronary scoring balloons market is also gaining from the steady move of elective PCI into catheterization laboratories and ambulatory settings, where procedure planning is becoming more standardized. This shift is not only a cost issue, because it changes which devices become routine choices in moderate complexity coronary work. When outpatient cath lab capacity expands, device demand becomes linked to installed procedural infrastructure rather than only to physician preference. That pattern supports durable growth in cardiac catheterization laboratories, which are projected to grow faster than other end-use settings through 2031. For the coronary scoring balloons market, the result is a broader site-of-care base that can support recurring demand for lesion preparation devices as outpatient PCI activity rises.

Underused Intravascular Imaging Creates Upside for Precision Scoring Use

The coronary scoring balloons market has further upside from intravascular imaging adoption, because imaging makes calcium distribution and thickness more visible during PCI planning. A Michigan registry initiative showed intracoronary imaging use increased from 7.3% in the first year to 44.0% in the fifth year, which indicates that structured quality programs can change routine practice in complex lesions. Outside Japan, intravascular imaging still accounts for only 5% to 15% of PCI in most developed markets, while Japan guides more than 75% of PCI cases with imaging. A 2026 Japanese study found that OCT-assessed calcium arcs above 218° and calcium thickness above 655 µm were optimal cutoffs for predicting calcium fracture with scoring balloons. In the coronary scoring balloons market, greater imaging use will likely raise co-utilization because it helps operators select scoring balloons more confidently in calcified lesions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Higher Unit Cost Than Plain Balloons Limits Routine Substitution | -1.2% | APAC, Latin America, MEA | Long term (≥ 4 years) |

| Operator Learning Curve Slows Penetration in Smaller Centers | -0.7% | Rest of World, Tier-2 centers globally | Medium term (2-4 years) |

| Competition From Atherectomy and Intravascular Lithotripsy Caps Share Gains | -1.0% | North America, Europe | Short term (≤ 2 years) |

| Regulatory Evidence Burden Delays New Product Introductions | -0.5% | Global, EU MDR and US FDA PMA pathway | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Competition From Atherectomy and Intravascular Lithotripsy Caps Share Gains

The coronary scoring balloons market is facing tighter competition from atherectomy and intravascular lithotripsy in calcified lesion preparation, especially in cases at the severe end of the complexity spectrum. A 2026 observational study reported lower in-hospital mortality with IVL compared with cutting or scoring balloon angioplasty in patients with different risk profiles, while also noting that the finding was hypothesis generating and not based on randomized evidence. Reimbursement support is also strengthening IVL adoption because the 2026 CMS Final Rule confirmed separate payment for coronary IVL through HCPCS code C1761 and CPT add-on code +92972. This does not remove the role of scoring balloons, since cost, guidewire compatibility, and procedural simplicity still support their use in moderate calcification. For the coronary scoring balloons market, the practical effect is a narrower pool of borderline lesions that once defaulted to scoring balloons but may now move to IVL when payment and clinical confidence align.

Higher Unit Cost Than Plain Balloons Limits Routine Substitution

The coronary scoring balloons market also remains constrained by the price gap between scoring balloons and plain balloon catheters in cost-sensitive settings. Published Japanese pricing placed anti-slipping scoring balloons at JPY 95,000 per unit, which was equivalent to USD 630, compared with JPY 29,000, or USD 193, for a standard compliant balloon catheter in 2025. That 3.3x premium makes full substitution difficult in emerging markets where imaging use is limited and lesion complexity is not always documented with precision. Procurement pressure is stronger in lower-middle-income Asia-Pacific and Latin American markets, where imported premium devices face tighter budget scrutiny. In the coronary scoring balloons market, this pricing barrier will likely keep adoption selective until lower-cost local manufacturers and volume purchasing models improve affordability.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Balloon Type: Non-Compliant Designs Remain the Core Choice

Non-compliant scoring balloons held 57.31% of the coronary scoring balloons market share in 2025, and they are also projected to post the fastest growth at 8.82% CAGR through 2031. This combination shows that the leading design is still gaining strength rather than entering a late maturity phase. In the coronary scoring balloons market, non-compliant devices are favored because they deliver focal scoring force at controlled inflation pressures without substantial vessel oversizing[2]Source: Abbott Laboratories, “Abbott Cardiovascular, Scoreflex NC Scoring PTCA Catheter,” Abbott Laboratories, cardiovascular.abbott. Abbott’s Scoreflex NC is positioned around that need, with a rated burst pressure of 20 atm and a 0.034-inch crossing profile that supports both deliverability and scoring reliability in calcified lesions.

Semi-compliant scoring balloons still hold a relevant role in the coronary scoring balloons market because they remain useful in moderate calcification and in vessels where trackability matters more than maximum focal force. Their lower crossing profile can make lesion access easier in tortuous anatomy, which keeps them in first-line use for selected procedures. Other balloon types, including hybrid scoring-cutting designs, serve a narrower part of the coronary scoring balloons market where severe calcification or difficult crossing reduces the effectiveness of standard designs. A 2025 first-in-man registry for iVascular’s Naviscore reported 94% procedural success in 85 patients with moderate or severe de novo calcified lesions, which shows that innovation within balloon design is still expanding the usable range of the category.

By Material: Nylon Leads While Polyurethane Gains Ground

Nylon accounted for 46.20% of the coronary scoring balloons market size in 2025, which kept it as the leading material platform in this category. The coronary scoring balloons market continues to rely on nylon because of its known burst resistance, stable compliance behavior, and compatibility with established production methods. That record also lowers the validation burden for manufacturers that want to introduce new products without taking on the full risk of a novel polymer path. DK Medtech’s DK Score, which received CE MDR certification in 2025, uses a nylon balloon with nitinol scoring elements and shows that companies are still improving the nylon platform rather than moving away from it.

Polyurethane is projected to record the fastest growth in the coronary scoring balloons market size at 9.21% CAGR from 2026 to 2031. Manufacturers are giving more attention to polyurethane because it offers flexibility and thinner wall sections that can reduce crossing profiles in complex anatomy. PET remains relevant in non-compliant applications, especially in specialist European settings where operators have long experience with PET-based balloon behavior. Across the coronary scoring balloons market, this material shift suggests that product development is moving toward better deliverability as severe calcification cases increasingly split off toward IVL and other advanced calcium modification options.

By End Use: Hospitals Hold the Base While Cath Labs Drive Growth

Hospitals captured 68.30% of revenue in 2025, which kept them as the dominant end-use setting in the coronary scoring balloons market. This position reflects the concentration of complex calcified lesion cases in tertiary care environments with cardiac surgery backup, perfusion support, and advanced imaging access. Hospitals also continue to manage the most challenging PCI cases, which supports demand for devices that provide controlled plaque modification. In the coronary scoring balloons market, this makes the hospital channel stable even as care delivery models change.

Cardiac catheterization laboratories are projected to expand at 11.42% CAGR from 2026 to 2031, making them the fastest-growing end-use segment. The shift toward elective PCI in cath labs and outpatient settings is broadening the procedural base for lesion preparation devices and creating more standardized device stocking patterns. Ambulatory surgical centers remain smaller, but they are gaining relevance as reimbursement policies and operational readiness improve for coronary interventions. For the coronary scoring balloons market, this means future growth will come from a wider mix of sites of care rather than from hospitals alone.

Geography Analysis

North America held 38.10% of the coronary scoring balloons market share in 2025, which made it the largest regional contributor. The coronary scoring balloons market in North America is supported by deep PCI infrastructure, high clinical research activity, and established reimbursement pathways for complex coronary devices. The United States anchors most of the regional demand because imaging-guided PCI and specialized lesion preparation are more embedded in routine practice there than in many other markets. Structured quality initiatives have also helped drive imaging use higher, and that raises the probability that calcified lesions are treated with scoring balloons instead of plain non-compliant balloons[3]Source: BMC2 Registry, “Statewide Initiative to Increase Intracoronary Imaging Optimization in PCI, A Report From the BMC2 Registry,” PubMed, pubmed.ncbi.nlm.nih.gov. This regional base remains important because it supports premium device adoption and faster uptake of new workflow standards.

Europe remains the second-largest regional cluster in the coronary scoring balloons market, but adoption patterns vary widely across countries. Germany stands out as one of the strongest PCI markets in the region because of higher use of imaging guidance and plaque modification techniques. The 2024 Spanish cardiac catheterization registry also showed continuing use of plaque modification approaches and a 10.6% rate of intracoronary imaging guidance across PCI procedures. EU MDR compliance continues to shape launch timing in the coronary scoring balloons market because a CE MDR decision can open access to 27 EU countries at once, which is why certifications such as DK Medtech’s 2025 approval matter strategically.

Asia-Pacific is the fastest-growing region in the coronary scoring balloons market, with a projected CAGR of 10.12% from 2026 to 2031. Japan remains a key reference market because imaging guides more than 75% of PCI procedures there, which strongly supports scoring balloon co-use. OrbusNeich’s Scoreflex product family is approved and marketed in Japan, which shows how product depth and operator familiarity reinforce adoption in that country. China is also important because procedure volume is expanding and domestic manufacturers such as DK Medtech, Kossel Medtech, and MicroPort Scientific are pairing local regulatory progress with overseas expansion plans. India, South Korea, Australia, and the rest of Asia-Pacific add to the regional opportunity because interventional cardiology capacity is still broadening and unmet need in complex PCI remains meaningful.

Competitive Landscape

The coronary scoring balloons market has a concentrated upper tier and a fragmented second tier. Abbott Laboratories, Boston Scientific, Medtronic, Terumo, and Philips hold the strongest portfolio breadth and have the widest cath lab relationships. Their advantage in the coronary scoring balloons market comes from integrated cardiovascular selling rather than from one product alone. That gives large companies room to position scoring balloons alongside imaging, guidewires, and broader PCI systems.

Product differentiation still matters in the coronary scoring balloons market because device design affects focal force, deliverability, and ease of use in calcified anatomy. Philips markets the AngioSculpt Evo with helical nitinol scoring elements and positions it around a premium performance profile, including a claim of up to 25 times the focal force of a standard non-compliant balloon. Abbott’s Scoreflex NC remains relevant through a design that combines high burst pressure with a slim crossing profile, which supports use in complex lesion preparation.

A 2026 review in Frontiers in Cardiovascular Medicine also noted that Terumo NaviScore, Philips AngioSculpt, and Nipro Aperta NSE occupy different clinical niches, which suggests differentiation in the coronary scoring balloons market is still meaningful rather than cosmetic.

Several recent moves show how competition in the coronary scoring balloons market is evolving. In January 2026, Kossel Medtech and Medtronic signed a strategic cooperation agreement around the Seledora coronary scoring balloon catheter, pairing Kossel’s local product base with Medtronic’s global commercial reach. In 2025, MicroPort Scientific received FDA 510(k) clearance for the Firefighter Pro PTCA balloon catheter, which advanced its broader coronary device portfolio in the United States. DK Medtech also secured CE MDR certification for DK Score in 2025, which strengthened the path for Asian challengers to enter European markets through a recognized regulatory route. The coronary scoring balloons market therefore remains moderately concentrated, but it still leaves space for specialized firms that can combine lower profiles, hybrid designs, or stronger imaging compatibility with faster regional execution.

Coronary Scoring Balloons Industry Leaders

Boston Scientific Corporation

Abbott Laboratories

Medtronic plc

Terumo Corporation

Philips

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Kossel Medtech and Medtronic signed a strategic cooperation agreement centered on the Seledora Coronary Scoring Balloon Catheter, combining Kossel's NMPA-approved scoring technology with Medtronic's global commercial infrastructure; the partnership signals accelerating Chinese-Western co-development in the segment

- March 2025: Kossel Medtech and Medtronic signed a strategic cooperation agreement centered on the Seledora Coronary Scoring Balloon Catheter, combining Kossel's NMPA-approved scoring technology with Medtronic's global commercial infrastructure; the partnership signals accelerating Chinese-Western co-development in the segment

Global Coronary Scoring Balloons Market Report Scope

As per the scope of the report, coronary scoring balloons are specialized percutaneous coronary intervention (PCI) devices designed to facilitate controlled plaque modification and lesion preparation in coronary arteries before stent implantation or other interventional procedures. These balloons incorporate scoring elements, such as nitinol or polymer-based structures, on the balloon surface that create controlled micro-incisions in atherosclerotic plaques during inflation. Coronary scoring balloons aim to improve lesion dilatation, enhance stent expansion, reduce balloon slippage, and minimize vessel trauma, thereby improving procedural outcomes in patients with coronary artery disease.

The coronary scoring balloon market is segmented by balloon type into semi-compliant scoring balloons, non-compliant scoring balloons, and other balloon types; by material into nylon, polyethylene terephthalate (PET), polyurethane, and other materials; by end use into hospitals, cardiac catheterization laboratories, ambulatory surgical centers, and other end users; and by geography into North America, Europe, Asia-Pacific, and Rest of the World. For each segment, the market size and forecast are provided in terms of value (USD).

| Semi-Compliant Scoring Balloons |

| Non-Compliant Scoring Balloons |

| Other Baloon Types |

| Nylon |

| Polyethylene Terephthalate |

| Polyurethane |

| Other Material |

| Hospitals |

| Cardiac Catheterization Laboratories |

| Ambulatory Surgical Centers |

| Other End Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Rest of the World |

| By Balloon Type | Semi-Compliant Scoring Balloons | |

| Non-Compliant Scoring Balloons | ||

| Other Baloon Types | ||

| By Material | Nylon | |

| Polyethylene Terephthalate | ||

| Polyurethane | ||

| Other Material | ||

| By End Use | Hospitals | |

| Cardiac Catheterization Laboratories | ||

| Ambulatory Surgical Centers | ||

| Other End Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Rest of the World | ||

Key Questions Answered in the Report

How large is the coronary scoring balloons space through 2031?

The coronary scoring balloons market size was USD 157.50 million in 2025, reaches USD 169.79 million in 2026, and is forecast to reach USD 247.17 million by 2031 at a 7.80% CAGR.

Why are non-compliant scoring balloons leading adoption?

Non-compliant scoring balloons led with 57.31% share in 2025 and are also the fastest-growing balloon type at 8.8% CAGR, because operators value controlled focal force and reliable lesion preparation in calcified anatomy.

Which region is growing the fastest?

Asia-Pacific is the fastest-growing region at 10.12% CAGR through 2031, supported by high imaging use in Japan and ongoing expansion by Chinese device manufacturers.

How does intravascular imaging affect product use?

Imaging supports more precise calcium assessment and improves device selection, and a structured registry program increased intracoronary imaging use from 7.3% to 44.0% over 5 years.

What is the main competitive threat to scoring balloons?

The main competitive pressure comes from intravascular lithotripsy, especially in severe calcification, as separate reimbursement in 2026 strengthened its clinical and commercial position.

What is the main competitive challenge for device makers in this space?

The main challenge is pressure from adjacent technologies such as drug-coated balloons, atherectomy systems, and IVL, along with pricing pressure in cost-sensitive markets.

Page last updated on: