Copper Clad Laminate Printed Circuit Board Substrate Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

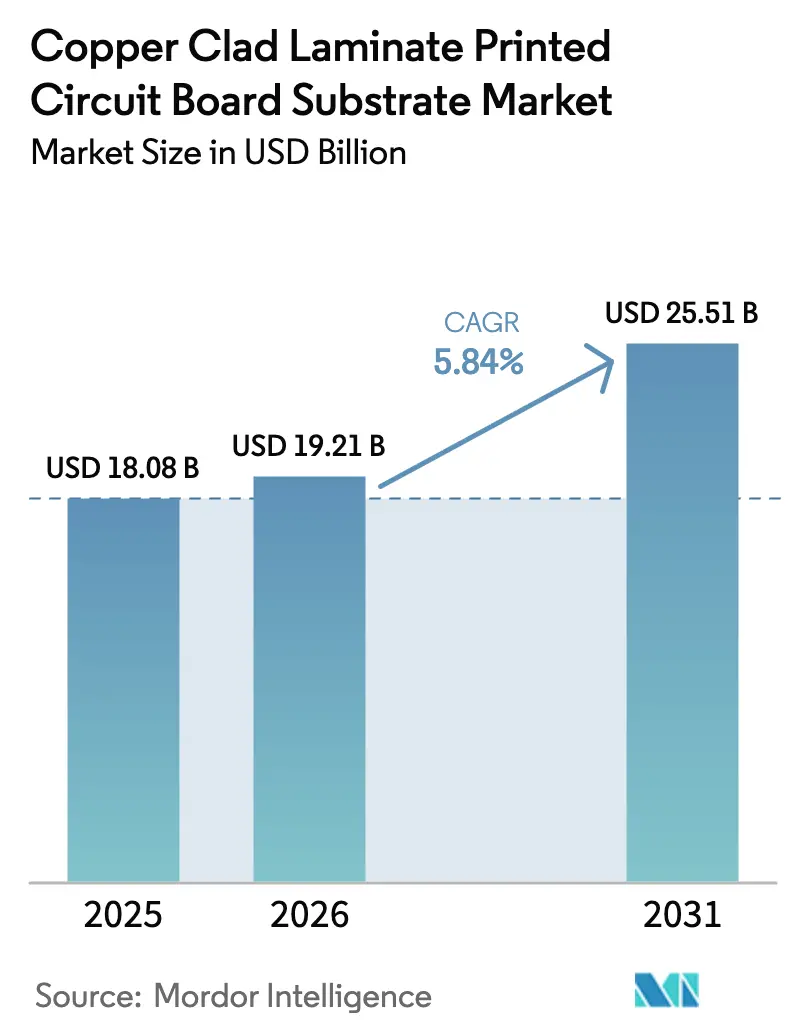

| Market Size (2026) | USD 19.21 Billion |

| Market Size (2031) | USD 25.51 Billion |

| Growth Rate (2026 - 2031) | 5.84% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Copper Clad Laminate Printed Circuit Board Substrate Market Analysis by Mordor Intelligence

The copper clad laminate printed circuit board substrate market size in 2026 is estimated at USD 19.21 billion, growing from 2025 value of USD 18.08 billion with projections showing USD 25.51 billion, growing at 5.84% CAGR over 2026-2031. Demand is shifting from commoditized, rigid boards toward premium, ultra-low-loss substrates that command 30-50% price premiums, reflecting the broader pivot to artificial-intelligence servers, electric vehicles, and high-frequency telecommunications gear. Service providers and OEMs are recalibrating procurement toward materials with dielectric constants below 3.5 and dissipation factors under 0.004 at 10 GHz, specifications that only a few vertically integrated suppliers can deliver at scale. The supply chain is under structural pressure from copper price volatility and tight availability of high-performance fiberglass cloth and HVLP copper foil, forcing producers to forward-integrate into raw materials and hedge commodity exposure. Asia Pacific retains manufacturing gravity due to its dense printed-circuit-board cluster, but rising energy costs and evolving European hazardous-substance rules are accelerating the qualification of halogen-free and low-formaldehyde resins. Competitive strategies now revolve around synchronized capacity expansions, captive copper foil, and quick-turn development of low-loss resin systems that win socket positions in data-center, EV, and radar platforms.

Key Report Takeaways

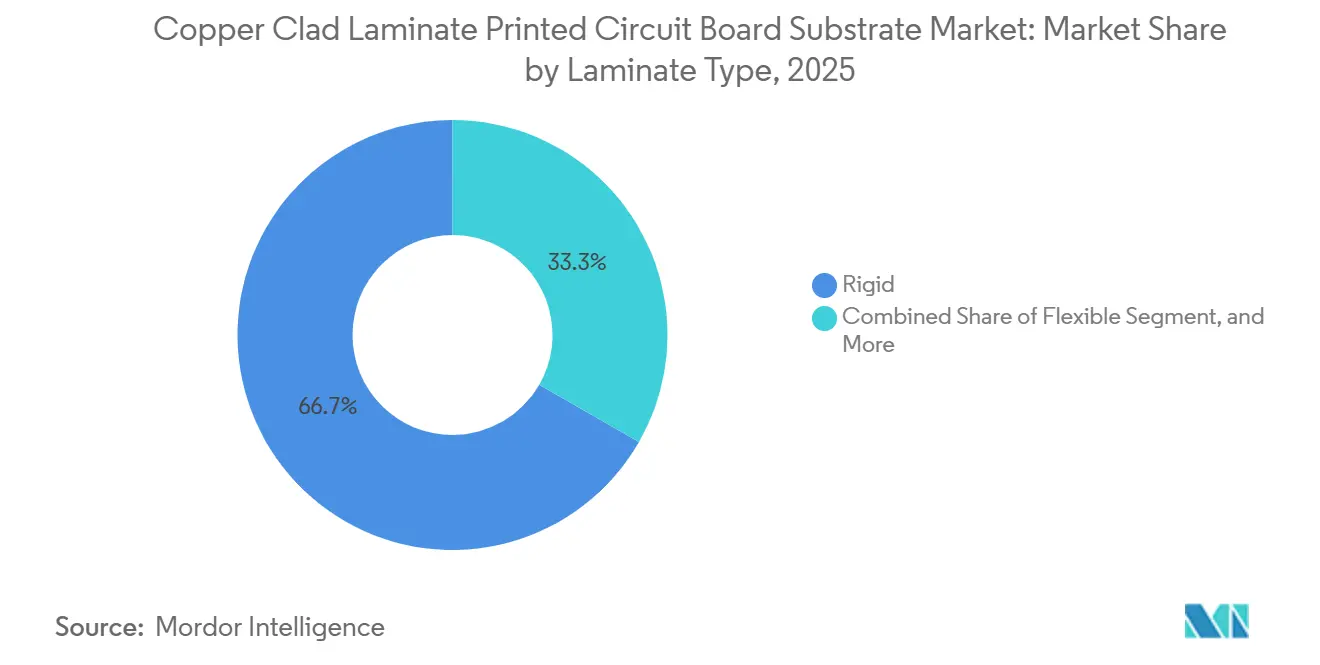

- By laminate type, rigid laminates led with a 66.71% of the copper clad laminate printed circuit board substrate market size in 2025, while flexible laminates are projected to expand at a 6.29% CAGR through 2031.

- By reinforcement material, glass fiber accounted for 62.33% of the copper clad laminate printed circuit board (PCB) substrate market size in 2025, and hybrid or composite fabrics are poised to grow at a 6.51% CAGR through 2031.

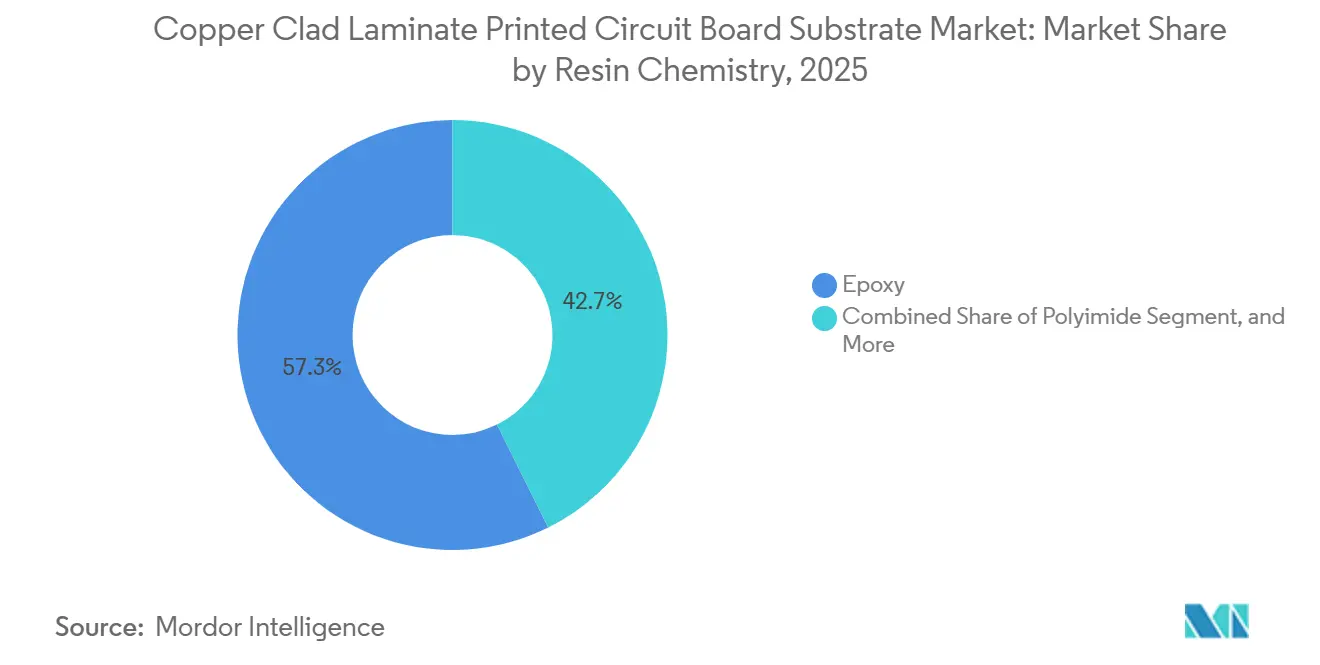

- By resin chemistry, epoxy commanded 57.34% of the copper clad laminate PCB substrate market in 2025; polyimide is the fastest-growing chemistry at a 6.68% CAGR through 2031.

- By application, consumer electronics and computing accounted for 44.89% of revenue in 2025, whereas automotive electronics is forecast to post a 7.24% CAGR between 2026-2031.

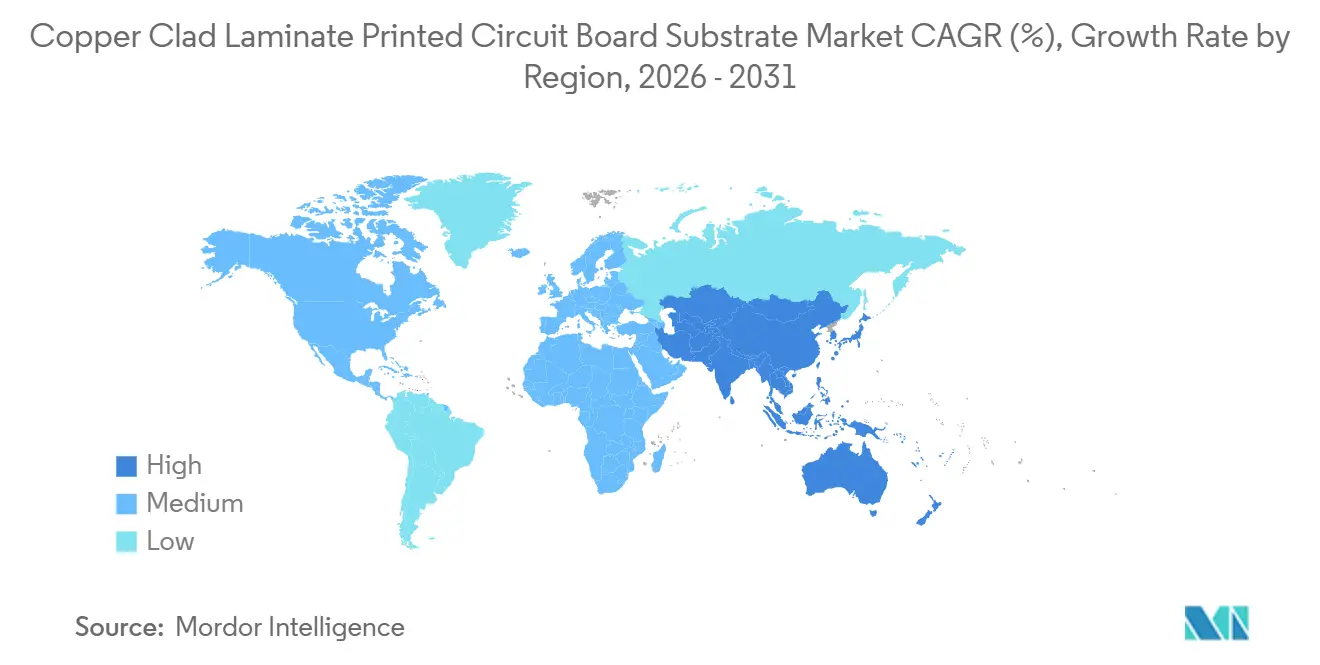

- By geography, the Asia Pacific held 53.28% of the copper clad laminate (CCL) PCB substrate market share in 2025 and is projected to expand at a 6.89% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Copper Clad Laminate Printed Circuit Board Substrate Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in 5G base station rollouts | +0.9% | China, North America, Europe | Medium term (2-4 years) |

| Expanding consumer electronics capacities | +0.8% | China, Vietnam, India, Southeast Asia | Short term (≤ 2 years) |

| Rapid growth in automotive ADAS and EVs | +1.2% | China, Europe, North America | Long term (≥ 4 years) |

| Demand for high-frequency high-speed PCBs | +1.0% | North America, Asia Pacific data-center hubs | Medium term (2-4 years) |

| Adoption of power electronics in renewables | +0.6% | China, Europe, India | Long term (≥ 4 years) |

| Push for halogen-free low-Dk/Df laminates | +0.5% | Europe, North America, Japan | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in 5G Base Station Rollouts

Operators are adding mid-band and millimeter-wave radios that use substrates with dielectric constants below 3.2 and dissipation factors below 0.002 to keep antenna gain within design limits.[1]Rogers Technical Team, “RO3000 Series Circuit Materials Data Sheet,” Rogers Corporation, rogerscorp.com Rogers RO3003 laminates meet these values and, when paired with reverse-treated LoPro copper foils featuring sub-1 µm roughness, reduce conductor loss by nearly 30% at 28 GHz compared with standard electrodeposited foils. China alone had deployed more than 1.8 million 5G macro cells by late 2025, and each massive-MIMO antenna module integrates multiple low-loss boards, multiplying laminate demand. North American and European carriers are following with densification programs that push premium sheet suppliers toward just-in-time deliveries on multiple continents. The rapid shift from sub-6 GHz to frequencies above 24 GHz amplifies skin-effect losses, cementing the need for ultra-smooth copper and stable resin systems over the medium term.

Expanding Consumer Electronics Production Capacities in the Asia Pacific

China-plus-one relocation is redirecting smartphone and notebook assembly to Thailand, Vietnam, and Malaysia, regions where Taiwanese PCB firms have committed USD 1.9 billion to new factories that are set to start mass production in 2026. Thailand’s PCB revenue is projected to climb from USD 2.07 billion in 2023 to USD 3.98 billion in 2028, forcing laminate vendors to build local prepreg and copper-foil inventories to win business from contract manufacturers. Taiwan still supplies high-frequency and high-speed sheets for AI notebooks, logging NTD 195.9 billion (USD 6.4 billion) in CCL and prepreg output in the first half of 2025, up 6.8% year on year.[2]I-Connect007 Editors, “Taiwan PCB Industry Projects NTD 915.7 Billion Output in 2025,” iconnect007.com Suppliers that combine China-based scale with Southeast-Asian logistics avoid tariff penalties and shorten lead times, giving them share gains in handset refresh cycles. The region’s shift toward foldable displays and wearable devices also increases demand for polyimide-based flex laminates that withstand repeated bending without micro-cracking.

Rapid Growth in Automotive ADAS and EV Electronics

Advanced driver-assistance systems and electrified powertrains push electronics content toward USD 10,000 per vehicle, tripling copper use compared with internal-combustion cars.[3]CME Group Analysts, “Copper: Major Factors That Offer Two Opposing Price Scenarios,” CME Group, cmegroup.com Substrates for 77-81 GHz radar and 800 V inverters must withstand ambient temperatures near 80 °C and repeated thermal cycling, prompting OEMs to specify laminates such as RO4350B that have a Z-axis CTE of 32 ppm/°C and a Tg above 280 °C. Kingboard gained Tier-1 approvals after adding 1,500 tons per month of dedicated thick copper foil for EV busbars in 2025. Europe’s tighter carbon-emission targets and the United States Inflation Reduction Act are accelerating EV model launches, reinforcing the long-term demand signal. As radar moves toward 120-140 GHz, dielectric-constant tolerance must narrow to ±0.05, opening white-space for hybrid fiberglass-ceramic reinforcements.

Demand for High-Frequency High-Speed PCB Materials

GPU-dense AI servers require 24-plus-layer boards that carry 56 Gbps signals across backplanes with loss budgets below 1.5 dB, necessitating dielectric constants under 3.5 and loss tangents below 0.004 at 40 GHz. Taiwan’s computer-related PCB shipments rose 25.2% year on year in Q3 2025, while AI server volumes climbed 82.8% for the full year, outstripping the supply of low-CTE copper foil and specialty fiberglass. Spread-glass fabrics and HVLP4 foils are in short supply, pushing laminate prices higher even in a soft consumer cycle. Rogers RO4835 materials, with a dissipation factor of 0.0037 at 10 GHz and Td of 390 °C, have become reference substrates for accelerator motherboards. The mix shift toward these ultra-low-loss sheets underpins steady mid-single-digit growth even if total server shipments plateau.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fluctuating copper and resin prices | −1.1% | Asia Pacific, Europe | Short term (≤ 2 years) |

| Environmental compliance costs | −0.4% | Europe, North America | Medium term (2-4 years) |

| Limited domestic manufacturing in EMs | −0.3% | Latin America, Middle East and Africa, South Asia | Long term (≥ 4 years) |

| Bottlenecks for ultra-low-loss glass fabrics | −0.5% | Supply concentrated in Japan | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fluctuating Copper and Resin Prices

Copper reached USD 11,200 per metric ton in October 2025, and J.P. Morgan projects USD 12,075 for 2026 on a 330,000-ton refined deficit, eroding laminate gross margins when pass-through clauses lag spot spikes. Kingboard and major Taiwanese peers responded with three sheet-price hikes in four months in 2025, yet each 10% sustained copper increase still trims 1-2.5 percentage points of margin, depending on the resin mix. Epoxy and phenolic resin markets track benzene and formaldehyde feedstock, adding another volatile layer as environmental levies rise. Spot shortages of bisphenol-A in early 2026 forced some producers to prioritize high-margin AI server materials at the expense of commodity FR-4, creating delivery gaps for consumer boards. Volatility, therefore, incentivizes deeper vertical integration into copper foil and captive phenolic reactors.

Environmental Compliance Costs for Hazardous Substances

The European Commission extended the RoHS exemption permitting up to 4% lead in copper alloys only until 31 December 2026, obliging laminate makers to validate substitution roadmaps or face a de facto lead ban in connectors and vias. Simultaneous REACH reviews target brominated flame retardants, accelerating the shift toward halogen-free phosphorus-nitrogen systems that demand new curing profiles and requalification with OEMs. Compliance adds laboratory testing, documentation, and audit costs that can exceed USD 800,000 for a full material family, squeezing smaller sheet producers. Export-oriented Asian suppliers must maintain dual product lines, one for strict EU and North American markets and another for domestic demand, raising inventory complexity. Early movers with certified halogen-free, low-formaldehyde resins gain preferred-supplier status and avoid costly redesign cycles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Laminate Type: Flexible Substrates Gain Amid AI Server Rigidity

Rigid laminates anchored 66.71% of 2025 demand, buoyed by multilayer PCBs in servers, telecom switches, and industrial controllers. Kingboard brought 1,500 tons per month of thick copper foil online at its Lianzhou site to feed this spike. Flexible films, however, exhibit the steeper 6.29% trajectory as wearables, foldable phones, and automotive interior displays prioritize bend radii below 1 mm. Taiwan’s flexible-PCB output did fall 10.9% year-on-year in Q3 2025, yet pipeline programs in medical implantables and cockpit electronics underpin the structural shift. Manufacturers emphasizing polyimide flex laminates with glass transition points above 280 °C now court Tier-1 automotive approvals.

Demand for rigid sheets is tilting toward high-layer and HDI constructions, adding press cycles and stressing dimensional control. Taiwan’s high-layer boards grew 20.1% year-on-year in 2025, while HDI volumes gained 8%. The copper clad laminate printed circuit board substrate market for rigid base materials is therefore expanding in absolute terms, even as the share moderates. Meanwhile, rigid-flex hybrids, down 14.9% year-on-year, remain cyclical proxies tied to handset refresh rhythms. Suppliers that integrate reverse-treated copper and laser-drillable prepregs are best positioned to regain momentum once handset volumes normalize.

By Reinforcement Material: Hybrid Composites Address Radar Tolerances

Glass fabrics remain the workhorse, accounting for 62.33% of 2025 volume, yet local dielectric variations hamper millimeter-wave circuits. Kingboard began construction of its first low-Dk fiberglass kiln in Qingyuan during H1 2025 and plans to add six specialty kilns by 2026 to mitigate bottlenecks. Hybrid or composite fabrics combining spread-glass with ceramic fillers improve phase stability, driving their 6.51% CAGR outlook. Rogers RO4360G2, a glass-reinforced ceramic thermoset laminate with a dielectric constant of 6.15 ±0.15, illustrates the balance of manufacturability and RF performance.

The copper clad laminate printed circuit board substrate market share allocated to hybrid reinforcement is growing fastest in automotive radar and high-speed backplanes, where dielectric constant tolerances must remain within ±0.05. Spread-glass weaves also enable 25 µm lines, critical for substrate-like PCB packaging. Capacity investment in specialty fiberglass, therefore, doubles as a hedge against Japanese material dominance and shipping delays for AI server boards.

By Resin Chemistry: Polyimide Captures Automotive Thermal Demands

Epoxy continues to underpin 57.34% of 2025 shipments thanks to cost and process familiarity, while polyimide is the clear growth frontier with a 6.68% CAGR. Polyimide flex films withstand solder-reflow peaks above 260 °C and ambient automotive temperatures of 80 °C, meeting OEM lifetime criteria. Hydrogenated bisphenol-A epoxies with low dielectric variance are also emerging, especially for compute-intensive boards requiring sub-0.004 loss tangents. The copper clad laminate printed circuit board substrate market size linked to epoxy will therefore expand in low-layer consumer and industrial boards, while polyimide and modified-epoxy platforms will win share in EV traction inverters and AI accelerators.

Phenolic curing agents account for more than half of the phenolic resin pool and provide flame retardancy, but formaldehyde classifications are tightening environmental scrutiny. European buyers are already specifying halogen-free V-0 systems, encouraging investment in phosphorus-nitrogen flame-retardant systems that keep dielectric loss minimal. Producers that commercialize bio-based phenolics with comparable mechanical strength can tap regulatory goodwill and brand sustainability goals, increasing pricing latitude.

By Application: Automotive Electronics Outpaces Consumer Demand

Consumer electronics and computing held 44.89% in 2025, yet their growth rate moderates as smartphones mature and cloud providers optimize refresh cycles. In contrast, automotive electronics are expected to grow at a 7.24% CAGR, driven by EVs' tripling of copper content per vehicle and radar, lidar, and zonal controllers multiplying board counts. Kingboard’s premium laminates have cleared Tier-1 qualification for these modules. The copper clad laminate printed circuit board substrate market's expansion in cars also absorbs specialty copper foil capacities redeployed from lithium-battery foil producers pivoting into PCB foil.

Telecom and networking remain critical secondary engines as hyperscale data centers consume another 110,000 tons of copper in 2026 alone. Industrial IoT, medical wearables, and defense avionics round out smaller but margin-rich niches that require low-outgassing, radiation-resistant laminates. Suppliers that tailor resin formulations for biocompatibility and moisture uptake below 0.05% gain an early design-in advantage in these regulated markets.

Geography Analysis

Asia Pacific commanded 53.28% of 2025 revenue and is projected to log a 6.89% CAGR to 2031 as China, Taiwan, and Southeast Asia deepen vertical integration into copper foil, fiberglass yarn, and specialty resins. China’s PCB output climbed to USD 27.95 billion in 2024 and is forecast at USD 34.18 billion in 2025, translating into a 37.6% global share. Taiwan added NTD 915.7 billion (USD 30.1 billion) of PCB revenue in 2025, a 12.1% jump, powered by AI server demand. Japan maintains specialty strength with Ibiden supplying 70% of AI-GPU substrates, while South Korea concentrates 45% of its PCB value in semiconductor packages.

Southeast Asia is the fastest-growing subregion, forecast to expand the CCL printed circuit board substrate market for local PCB makers at a 12.8% CAGR to 2028, as Thailand alone absorbs 72% of outbound Taiwanese investment. This China-plus-one redistribution spreads geopolitical risk and diversifies energy sourcing amid higher mainland electricity tariffs. Local laminate sheet presses in Thailand and Vietnam shorten lead times for consumer and automotive boards, improving working-capital efficiency for EMS players.

North America and Europe trail in fabrication output but wield regulatory and design influence. U.S. data-center electricity share could reach 12% by 2028, driving domestic preference for high-reliability, low-loss boards. Europe’s RoHS and REACH frameworks accelerate the adoption of halogen-free laminates and penalize high-lead alloys, nudging global suppliers toward compliant chemistries. Latin America, the Middle East, and Africa contribute single-digit percentages, limited by weak upstream ecosystems and skills gaps, yet present emerging demand for industrial automation and telecom backhaul, where cost-optimized FR-4 variants still suffice.

Competitive Landscape

High-performance tiers are consolidating, while commodity segments are fragmenting. The top five mainland producers controlled roughly 68% of rigid and premium sheet volume in 2014; the share has since risen as Kingboard, Shengyi, and ITEQ extended scale. Kingboard ships about 9 million sheets monthly and operates 20+ factories across China and Southeast Asia. The firm commissioned three low-Dk fiberglass kilns in 2025 and plans six more by 2026, cementing upstream self-sufficiency.

Shengyi Technology launched a CNY 1.9 billion high-layer PCB plant targeting AI and server clients, adding 700,000 m² annual output with trial runs slated for 2026. Its integrated chain spans 45 million m² of rigid boards and 9.6 million m² of flex sheets, supported by more than 40 state-level R&D programs. Rogers Corporation and niche U.S. and Japanese specialists dominate PTFE-ceramic and hydrocarbon-ceramic laminates, leveraging proprietary chemistries and reverse-treated copper foil to win data-center and radar sockets.

New entrants from the battery, copper foil, and specialty resin segments are entering the PCB laminate market, driven by overlapping purity and thickness specifications. Defu Technology expanded foil capacity to 175,000 tons in 2025 and signed offtake with CATL and Gotion, signaling a pivot into board-grade foil. Mergers between foil mills and sheet pressers could reshape bargaining power over the next cycle. Regulatory shifts, especially the 2026 RoHS lead exemption sunset, add uncertainty that favors incumbents with large compliance staffs and diversified resin portfolios in the CCL PCB substrate market.

Copper Clad Laminate Printed Circuit Board Substrate Industry Leaders

Kingboard Laminates Holdings Ltd.

Shengyi Technology Co., Ltd.

Nanya Plastics Corporation

ITEQ Corporation

Panasonic Holdings Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: China-based Kingboard Laminates implemented its third price increase in four months to offset copper and fiberglass surges.

- August 2025: Kingboard’s Lianzhou plant reached 1,500 tons per month thick-foil capacity, while three low-Dk fiberglass kilns in Qingyuan started commissioning.

- August 2025: Shengyi Electronics approved a CNY 1.9 billion intelligent manufacturing project for high-layer computing-power boards, with trial output in 2026.

- July 2025: Kingboard expanded Thailand sheet capacity to 1 million sheets per month, targeting 1.8 million by 2027.

Global Copper Clad Laminate Printed Circuit Board Substrate Market Report Scope

The Copper Clad Laminate Printed Circuit Board Substrate Market Report is Segmented by Laminate Type (Rigid, Flexible), Reinforcement Material (Glass Fiber, Paper Base, Hybrid/Composite and Other Reinforcement Materials), Resin Chemistry (Epoxy, Phenolic, Polyimide, Other Resin Chemistries), Application (Consumer Electronics and Computing, Telecom and Networking, Automotive Electronics, Industrial and Commercial Electronics, Medical and Healthcare Devices, Aerospace and Defense, Other Applications), and Geography (North America, South America, Europe, Asia Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Rigid |

| Flexible |

| Glass Fiber |

| Paper Base |

| Hybrid / Composite and Other Reinforcement Materials |

| Epoxy |

| Phenolic |

| Polyimide |

| Other Resin Chemistries |

| Consumer Electronics and Computing |

| Telecom and Networking |

| Automotive Electronics |

| Industrial and Commercial Electronics |

| Medical and Healthcare Devices |

| Aerospace and Defense |

| Other Applications |

| North America | United States |

| Canada | |

| South America | Brazil |

| Mexico | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| South Korea | |

| Taiwan | |

| Southeast Asia | |

| India | |

| Rest of Asia Pacific | |

| Middle East and Africa |

| By Laminate Type | Rigid | |

| Flexible | ||

| By Reinforcement Material | Glass Fiber | |

| Paper Base | ||

| Hybrid / Composite and Other Reinforcement Materials | ||

| By Resin Chemistry | Epoxy | |

| Phenolic | ||

| Polyimide | ||

| Other Resin Chemistries | ||

| By Application | Consumer Electronics and Computing | |

| Telecom and Networking | ||

| Automotive Electronics | ||

| Industrial and Commercial Electronics | ||

| Medical and Healthcare Devices | ||

| Aerospace and Defense | ||

| Other Applications | ||

| By Geography | North America | United States |

| Canada | ||

| South America | Brazil | |

| Mexico | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| South Korea | ||

| Taiwan | ||

| Southeast Asia | ||

| India | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | ||

Key Questions Answered in the Report

How fast will the copper clad laminate printed circuit board substrate market grow through 2031?

It is projected to expand from USD 19.21 billion in 2026 to USD 25.51 billion by 2031, reflecting a 5.84% CAGR.

Which end-use sector will add the most incremental revenue?

Automotive electronics is expected to post the steepest 7.24% CAGR as EVs and ADAS content multiply board demand.

Why is Asia Pacific so dominant in production?

The region concentrates PCB fabrication, controls upstream materials like copper foil and fiberglass, and benefits from large hyperscale data-center builds.

What resin system is gaining share fastest?

Polyimide laminates, valued for glass-transition temperatures above 280 °C, are the fastest growing at 6.68% CAGR.

How are suppliers mitigating copper price risk?

Leading producers forward-integrate into foil production, adjust contract pass-through clauses, and diversify into higher-margin low-loss substrates that better absorb raw-material swings.

Page last updated on: