Continuous Peripheral Nerve Block Catheters Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

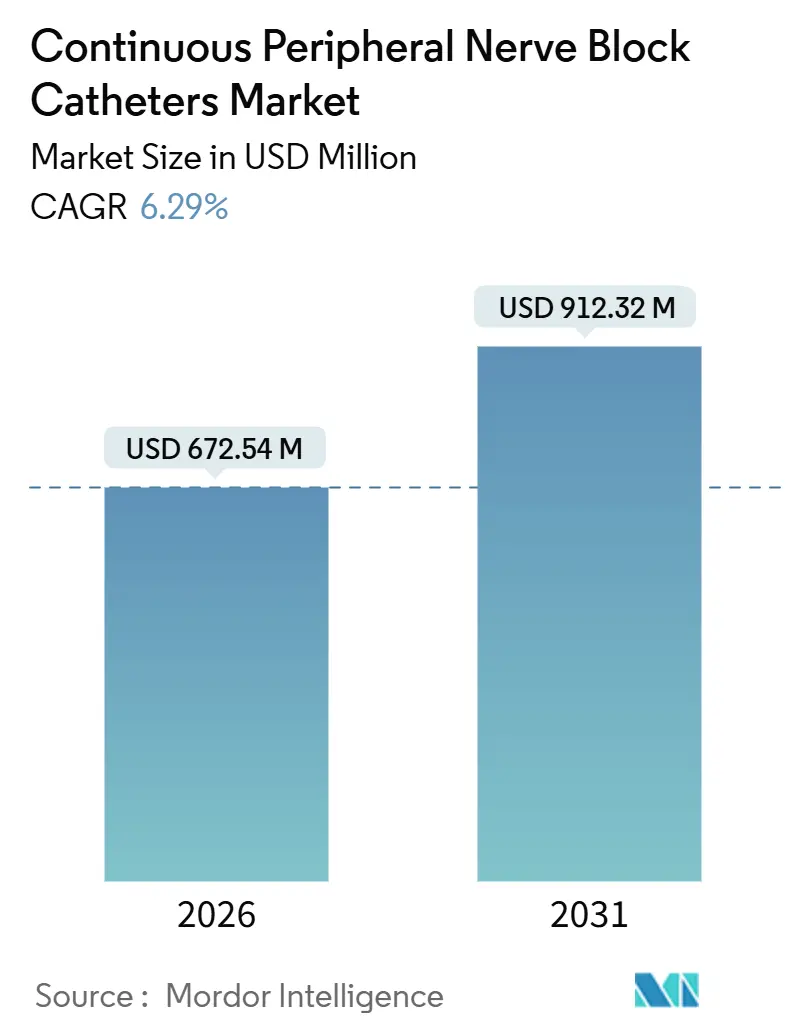

| Market Size (2026) | USD 672.54 Million |

| Market Size (2031) | USD 912.32 Million |

| Growth Rate (2026 - 2031) | 6.29% CAGR |

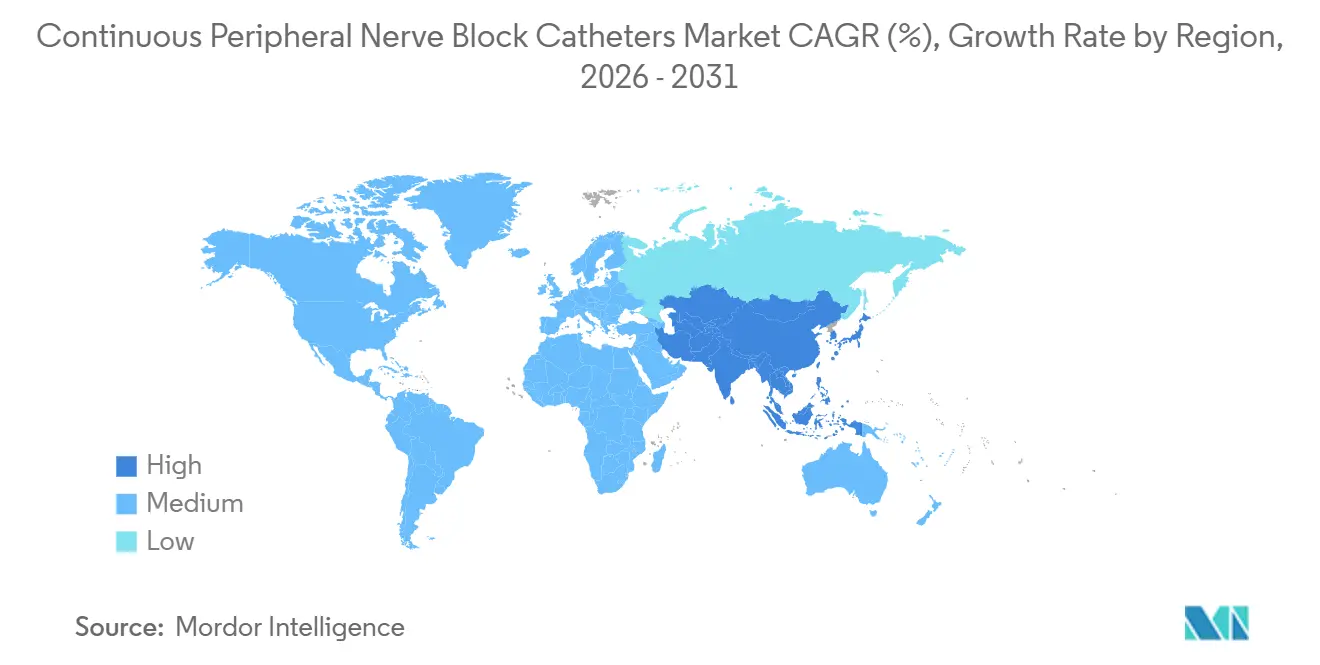

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

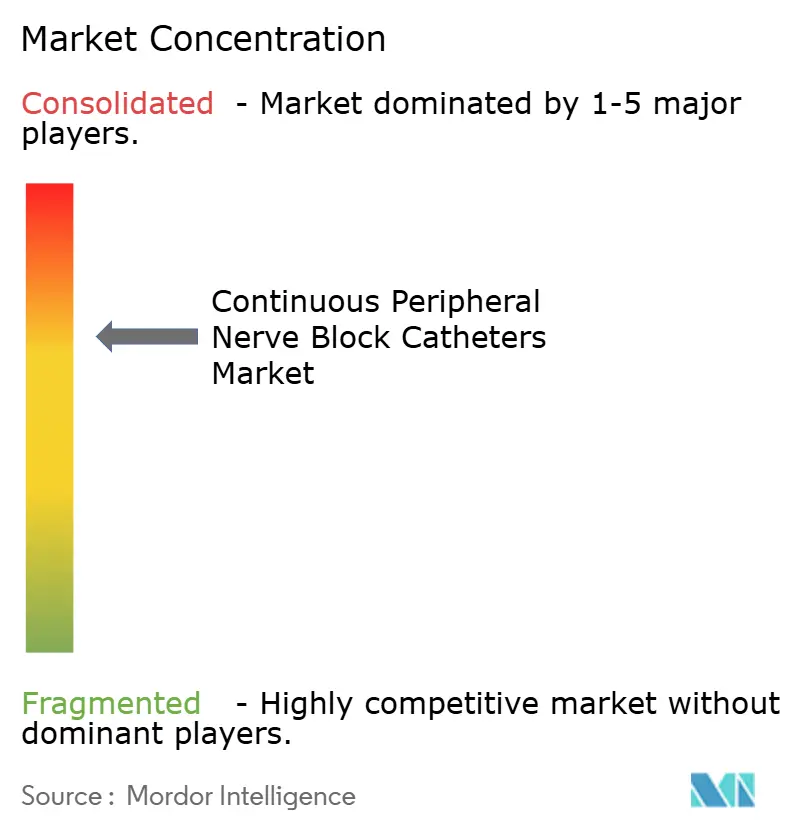

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Continuous Peripheral Nerve Block Catheters Market Analysis by Mordor Intelligence

The Continuous Peripheral Nerve Block Catheters Market size is estimated at USD 672.54 million in 2026, and is expected to reach USD 912.32 million by 2031, at a CAGR of 6.29% during the forecast period (2026-2031).

Rising orthopedic trauma volumes among aging populations, mandatory multimodal analgesia protocols, and the maturation of ultrasound-guided regional techniques are accelerating global demand. Payers are rewarding opioid-sparing approaches, ambulatory surgical centers are capturing same-day joint-replacement procedures, and manufacturers are integrating smart sensors to enable remote monitoring. Supply-side dynamics such as sterilization bottlenecks, regulatory scrutiny, and bundled tenders in emerging economies are reshaping production costs and pricing strategies. Competitive intensity remains moderate because the top five players control about 60% of revenue, yet regional distributors and start-ups continue to fragment share below the tier-1 level.

Key Report Takeaways

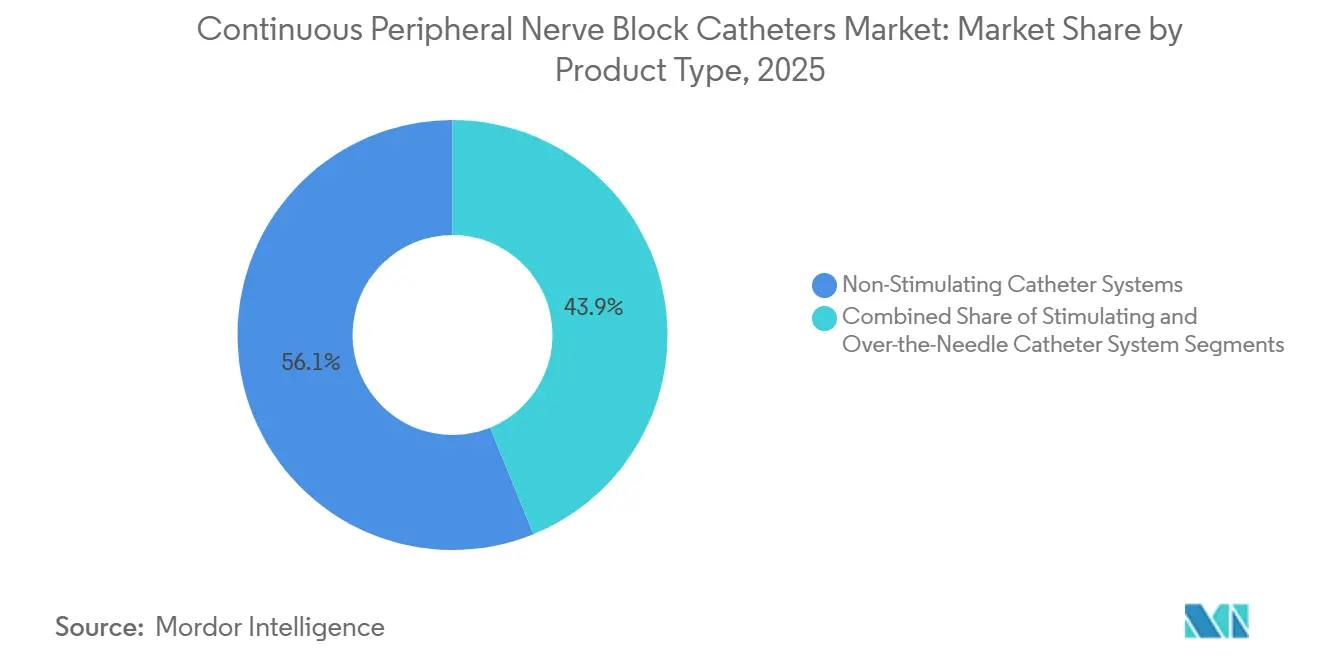

- By product type, non-stimulating systems led with 56.14% revenue share in 2025, while over-the-needle designs are set to record the fastest 8.13% CAGR through 2031.

- By insertion technique, nerve-stimulation guidance held 49.62% of revenue in 2025, whereas ultrasound-guided placement is advancing at a 9.21% CAGR toward 2031.

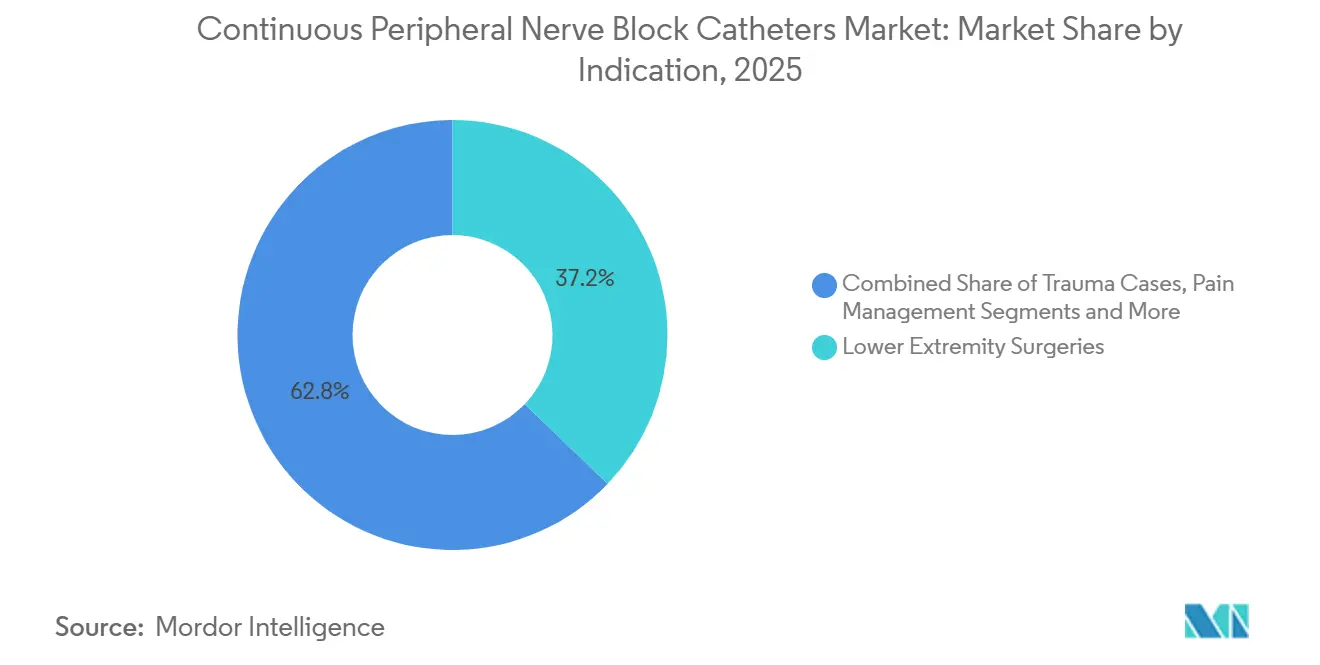

- By indication, lower extremity surgeries accounted for 37.16% of demand in 2025, yet trauma cases are accelerating at a 10.89% CAGR across the forecast window.

- By end user, hospitals captured 63.21% revenue in 2025, while ambulatory surgical centers exhibit the highest 9.58% CAGR to 2031.

- By geography, North America dominated with 44.55% share in 2025, whereas Asia-Pacific is poised to expand at an 8.26% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Continuous Peripheral Nerve Block Catheters Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Global Orthopedic & Trauma Surgery Volumes | +1.2% | North America, Europe, Asia-Pacific urban centers | Medium term (2-4 years) |

| ERAS & Opioid-Sparing Protocols Accelerating Adoption | +1.5% | North America, Europe, Australia, Middle East | Short term (≤ 2 years) |

| Advances in Ultrasound-Guided Placement Accuracy | +1.3% | North America, Western Europe, Tier-1 Asia-Pacific hospitals | Medium term (2-4 years) |

| Hospital-to-ASC Shift Demanding Longer Ambulatory Analgesia | +1.1% | North America core, Europe, select Asia-Pacific markets | Long term (≥ 4 years) |

| Integration of Smart Sensor-Enabled Catheters & Remote Monitoring | +0.8% | North America, Western Europe pilot sites | Long term (≥ 4 years) |

| Emerging Bundled Tender Contracts in Developing Regions | +0.4% | China, India, GCC, Brazil | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Global Orthopedic & Trauma Surgery Volumes

Worldwide orthopedic procedures climbed 7% year on year during 2025 as population aging and obesity hastened joint degeneration, leading to higher rates of hip, knee, and shoulder reconstructions.[1]OECD Staff, “OECD Health Statistics 2025,” Organisation for Economic Co-operation and Development, oecd.org Hip-fracture incidence among adults aged 65 and older reached 1.6 million cases, a figure projected to hit 2.1 million by 2030 as life expectancy rises and osteoporosis prevalence grows.[2]World Health Organization Team, “Ageing and Health Fact Sheet 2025,” World Health Organization, who.int Trauma admissions surged in low- and middle-income countries, where road-traffic injuries generate millions of operations requiring prolonged analgesia. In the United States, total knee arthroplasty volumes surpassed 1 million in 2025 after Medicare expanded outpatient coverage, incentivizing efficient pain control. Continuous peripheral nerve block catheters permit 24-hour discharge with analgesia equivalent to inpatient opioid regimens, trimming hospital stays by 1.2 days per case.

ERAS & Opioid-Sparing Protocols Accelerating Adoption

Enhanced recovery after surgery guidelines published in 2024 recommend continuous peripheral nerve blocks for major lower-extremity procedures, citing 60% opioid reductions compared with intravenous patient-controlled analgesia.[3]Thomas Wainwright, “Enhanced Recovery After Surgery Guidelines for Hip and Knee Arthroplasty,” ERAS Society, erassociety.org The CMS Comprehensive Care for Joint Replacement model began penalizing 90-day readmissions above 5% and rewarding facilities that keep pain scores under 3, intensifying interest in sustained regional analgesia. U.S. opioid-related overdose deaths declined 3% in 2025, the first sustained drop in ten years, partly due to surgical protocols that limit systemic opioids. European ministries earmarked EUR 200 million to train anesthesiologists in ultrasound-guided techniques, reporting EUR 1,500 savings per joint replacement. Collectively, these changes embed catheter-based analgesia into routine orthopedic care.

Advances in Ultrasound-Guided Placement Accuracy

Portable ultrasound units with linear transducers now deliver sub-0.3 millimeter resolution, letting clinicians visualize nerve bundles and adjacent vessels during placement. Needle-guidance overlays cut catheter misplacement rates below 5%, compared with 12% for nerve-stimulator methods. Artificial-intelligence algorithms identify key nerve anatomy with 94% accuracy, supporting novice providers. Community hospitals acquired systems priced under USD 8,000 in 2025, widening access to image-guided regional anesthesia. Hybrid ultrasound plus stimulation platforms shaved 4 minutes off insertion times, a meaningful gain in high-throughput ambulatory centers.

Hospital-to-ASC Shift Demanding Longer Ambulatory Analgesia

Ambulatory surgical centers performed 28% of U.S. total knee arthroplasties in 2025 after Medicare removed inpatient-only restrictions. Same-day discharge requires analgesia lasting 48-72 hours, a window single-shot blocks cannot meet. Catheters coupled with elastomeric pumps satisfy this duration, letting patients self-manage infusion at home with telephone support. Average outpatient knee-replacement reimbursement reached USD 18,000 versus USD 28,000 inpatient, boosting provider net margins. Readmission rates for ASC patients using catheters stayed below 2%, compared with 6% among those discharged on oral opioids alone.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Device & Procedure Costs in Low-Volume Centres | −0.6% | Rural North America, Eastern Europe, tier-2/3 Asia-Pacific | Medium term (2-4 years) |

| Stringent FDA/CE Evidence Requirements Slowing Launches | −0.5% | North America, Europe | Short term (≤ 2 years) |

| Sterilization Capacity Limits After EtO Emission Rules | −0.4% | North America, Europe, ripple effects Asia-Pacific | Medium term (2-4 years) |

| Limited Anesthetist Training in Tier-2 Hospitals | −0.7% | Asia-Pacific, Latin America, Middle East & Africa, rural U.S. | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Device & Procedure Costs in Low-Volume Centres

Catheter kits cost USD 150 to 300, an outlay that hospitals performing under 100 joint replacements yearly struggle to absorb. Portable ultrasound units range from USD 8,000 to USD 40,000, competing with other capital needs. Insertion takes roughly 15 minutes versus 5 minutes for single-shot blocks, adding USD 200 per case in operating-room expense. Rural U.S. hospitals operate on margins below 2%, limiting investment capacity. Medicare’s APC reimbursement remained flat at USD 180, failing to cover supply and labor costs.

Stringent FDA/CE Evidence Requirements Slowing Launches

The FDA now expects clinical data for antimicrobial-coated or design-modified catheters, extending clearance timelines by a year. European MDR demands post-market surveillance plans, adding EUR 500,000 per product line in compliance spending. Only nine of 18 catheter submissions cleared U.S. review in 2025, delaying revenue and compressing life cycles. Smaller firms devote 8% of sales to regulatory costs, spurring consolidation. Collectively, these hurdles slow next-generation rollouts.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Non-Stimulating Systems Dominate, Over-the-Needle Designs Gain Traction

Non-stimulating systems accounted for 56.14% of continuous peripheral nerve block catheters market share in 2025, buoyed by streamlined workflows and reduced setup time. This product class delivers strong visibility under ultrasound and costs USD 20–30 less than stimulating equivalents, advantages that resonate with cost-sensitive ambulatory centers. Over-the-needle designs supply the fastest growth, projected at 8.13% CAGR, helped by echogenic markers and kink-resistant polymers that stabilize placement during ambulation. Stimulating variants maintain traction in edema-laden trauma cases where ultrasound images blur, but their unit share is set to erode as younger anesthesiologists adopt image-first protocols.

Over-the-needle catheters now feature antimicrobial coatings that cut infection rates below 2%, opening prospects for indwelling periods of five or more days. Manufacturers position these products as single-operator solutions, critical as anesthesia technician shortages rise across North America and Europe. The continuous peripheral nerve block catheters market size for non-stimulating systems is expected to maintain the largest absolute revenue through 2031, while over-the-needle volumes will close the gap on the back of rapid ASC uptake. Suppliers investing in polyurethane blends and securement accessories stand to capture outsized gains.

By Insertion Technique: Ultrasound Guidance Overtakes Nerve Stimulation

Nerve-stimulation guidance still held 49.62% revenue in 2025, reflecting entrenched habits among clinicians trained before portable ultrasound became affordable. Nevertheless, ultrasound-guided insertion is pacing a 9.21% CAGR through 2031 on evidence of lower vascular puncture rates and shorter procedure times. Hybrid dual-guidance systems combine both modalities, catering to teaching hospitals that value multi-layer verification for residents. The continuous peripheral nerve block catheters market size for ultrasound-guided procedures is forecast to surpass USD 500 million by 2031 as portable devices priced under USD 10,000 penetrate community settings.

Nerve stimulation retains advantages in morbidly obese patients where ultrasound depth is constrained beyond six centimeters. Hybrid consumables add USD 50–80 per use, a premium high-volume centers accept to mitigate complications and operating-room delays. Training reforms reinforce the shift: 75% of U.S. residencies required ultrasound proficiency for 2025 graduates, ensuring future clinicians default to image guidance. As reimbursement models privilege safety and efficiency, ultrasound will cement its leadership.

By Indication: Trauma Cases Surge, Lower Extremity Surgeries Anchor Demand

Lower extremity surgeries, including total knee arthroplasty and hip fracture repair, represented 37.16% of 2025 demand, anchoring the continuous peripheral nerve block catheters market. These procedures favor femoral, sciatic, and popliteal blocks that easily accommodate 72-hour infusions. Trauma indications are expanding at a 10.89% CAGR, fueled by road-traffic injuries and battlefield wounds in emerging economies. Upper-extremity surgeries hold steady in the mid-20% range, leveraging interscalene blocks for shoulder reconstructions.

Trauma centers in low-income regions observe 30% intensive-care savings by adopting catheter-based analgesia over opioids. However, catheter-related infection stands at 5% in emergency insertions versus 2% in controlled operating-room settings, prompting development of securement devices and subcutaneous tunneling kits. Pain-management applications are niche but rising as palliative programs seek opioid-sparing options. The continuous peripheral nerve block catheters market size for trauma is projected to nearly double by 2031 if current growth persists.

By End User: Hospitals Retain Dominance, ASCs Accelerate

Hospitals generated 63.21% of revenue in 2025, reflecting their grip on high-acuity trauma and revision arthroplasty cases. Yet ambulatory surgical centers are pacing a 9.58% CAGR, benefiting from bundled payments that reimburse outpatient joint replacement at rates 35% lower than inpatient episodes. Specialty pain clinics occupy a smaller but stable slice, extending catheter infusions up to two weeks for chronic pain clients.

Hospitals counter ASC competition by setting up dedicated outpatient wings within their facilities, offering catheter-guided same-day discharge while retaining escalation capacity. ASC expansion is limited by state regulations governing home-based analgesia, keeping adoption to 28% of eligible joint replacements in 2025. The continuous peripheral nerve block catheters industry therefore sees parallel growth: hospitals sustain baseline volumes, while ASCs deliver accelerated incremental gains.

Geography Analysis

North America contributed 44.55% of 2025 revenue, powered by Medicare Advantage penetration above 50%, robust ASC infrastructure, and anesthesiologist density of 1 per 3,500 population. CMS penalty-and-reward frameworks promote catheter-based analgesia, cutting 90-day readmissions by 40% for joint replacements. Canada funded USD 60 million in 2025 to equip rural hospitals with ultrasound units, and Mexico’s private sector adopted catheters to attract medical tourists at 50% price discounts versus the United States.

Asia-Pacific is forecast to register an 8.26% CAGR through 2031 as China’s centralized procurement slashes prices and India’s private chains standardize ultrasound-guided protocols. Japan’s aging demographic produces 400,000 hip fractures annually, driving steady catheter demand. Australia boosted reimbursement by AUD 50 in 2025, cutting opioid prescriptions by 25% among post-surgical patients.

Europe mirrors North American adoption, with Germany reimbursing EUR 180 per catheter procedure and the United Kingdom investing in simulation-based training. The Middle East’s GCC allocated USD 2.7 billion for anesthesia capacity under Vision 2030, while Brazil secured 500,000 units annually for public hospitals yet struggles with anesthetist shortages. South Africa’s private sector turned to catheters to stem rising codeine misuse.

Competitive Landscape

The continuous peripheral nerve block catheters market displays moderate concentration, leaving room for regional players and niche innovators. Teleflex, B. Braun, and BD bundle catheters with infusion pumps and ultrasound systems, securing multi-year contracts with group purchasing organizations. Pajunk and Epimed lean on specialty features such as pediatric sizes and echogenic coatings to win share in underserved segments.

Patent filings for antimicrobial coatings rose 40% in 2025 as firms chase infection rates below 2%, a level that would open chronic-pain indications. Start-ups developing bioresorbable catheters completed Phase I human trials, reporting analgesia comparable to polyurethane devices and eliminating removal procedures. ICU Medical’s 2024 acquisition of a regional catheter maker underscores consolidation trends, while Chinese and Indian manufacturers captured 25% share in public tenders by pricing 40% below multinationals. Training programs remain a critical differentiator; B. Braun operates 25 simulation centers that build clinician loyalty and pipeline visibility.

Growing interest in smart catheters with telemetry adds a fresh competitive axis. No supplier owns more than 5% share in this sub-segment, but early adopters believe remote monitoring will become standard as reimbursement stabilizes. Suppliers able to integrate hardware, software, and education are likely to widen moats over pure-device competitors.

Continuous Peripheral Nerve Block Catheters Industry Leaders

B. Braun Melsungen

Avanos Medical Inc.

Teleflex Incorporated

Pajunk GmbH Medizintechnologie

Epimed International Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Boston Scientific agreed to acquire SoniVie Ltd. and its TIVUS intravascular ultrasound system, potentially broadening Boston Scientific’s pain-management pipeline.

- January 2025: B. Braun Medical introduced the Clik-FIX Epidural/Peripheral Nerve Block Catheter Securement Device, expanding its catheter-stabilization portfolio.

Global Continuous Peripheral Nerve Block Catheters Market Report Scope

Continuous Peripheral Nerve Block (CPNB) catheters are thin, flexible tubes inserted near specific nerves or plexuses to deliver a continuous infusion of local anesthetic, providing prolonged postoperative analgesia and reducing opioid use.

The Continuous Peripheral Nerve Block Catheters Market Report is segmented by Product Type, Insertion Technique, Indication, End User, and Geography. By Product Type, the market is segmented into Stimulating Catheter Systems, Non-Stimulating Catheter Systems, and Over-the-Needle Catheter Systems. By Insertion Technique, the market is segmented into Ultrasound Guided, Nerve Stimulation Guided, and Hybrid. By Indication, the market is segmented into Trauma Cases, Upper Extremity Surgeries, Lower Extremity Surgeries, Pain Management, and Others. By End User, the market is segmented into Hospitals, Ambulatory Surgical Centres, and Specialty Pain Clinics. By Geography, the market is segmented into North America, Europe, Asia-Pacific, Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. Market Forecasts are Provided in Terms of Value (USD).

| Stimulating Catheter Systems |

| Non-Stimulating Catheter Systems |

| Over-the-Needle Catheter Systems |

| Ultrasound Guided |

| Nerve Stimulation Guided |

| Hybrid (Dual Guidance) |

| Trauma Cases |

| Upper Extremity Surgeries |

| Lower Extremity Surgeries |

| Pain Management (Chronic & Acute) |

| Others |

| Hospitals |

| Ambulatory Surgical Centres |

| Specialty Pain Clinics |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Stimulating Catheter Systems | |

| Non-Stimulating Catheter Systems | ||

| Over-the-Needle Catheter Systems | ||

| By Insertion Technique | Ultrasound Guided | |

| Nerve Stimulation Guided | ||

| Hybrid (Dual Guidance) | ||

| By Indication | Trauma Cases | |

| Upper Extremity Surgeries | ||

| Lower Extremity Surgeries | ||

| Pain Management (Chronic & Acute) | ||

| Others | ||

| By End User | Hospitals | |

| Ambulatory Surgical Centres | ||

| Specialty Pain Clinics | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the continuous peripheral nerve block catheters market by 2031?

The market is expected to reach USD 912.32 million by 2031, reflecting a 6.29% CAGR.

Which product type leads current revenue in continuous peripheral nerve block catheters?

Non-stimulating systems held 56.14% share in 2025 and remain the dominant category.

Why are ambulatory surgical centers adopting continuous nerve block catheters rapidly?

ASCs benefit from bundled payments that favor outpatient joint replacement and require 48–72 hour analgesia, which catheters provide.

Which geographic region shows the fastest growth through 2031?

Asia-Pacific is forecast to expand at an 8.26% CAGR, driven by China’s procurement and India’s private-sector upgrades.

How are smart sensor-enabled catheters impacting clinical practice?

Early pilots show a 30% reduction in emergency visits thanks to remote monitoring, and CMS now reimburses USD 50 per patient monthly for data review.

Page last updated on: