Contactless Connector Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 0.36 Billion |

| Market Size (2030) | USD 0.66 Billion |

| Growth Rate (2025 - 2030) | 12.82% CAGR |

| Fastest Growing Market | Middle East |

| Largest Market | Asia Pacific |

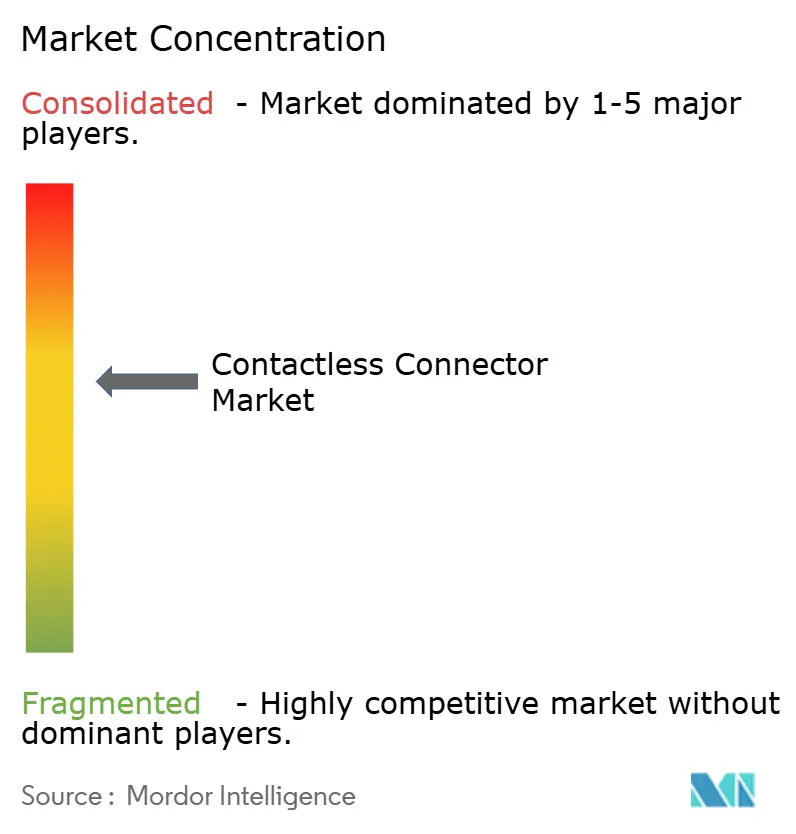

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Contactless Connector Market Analysis by Mordor Intelligence

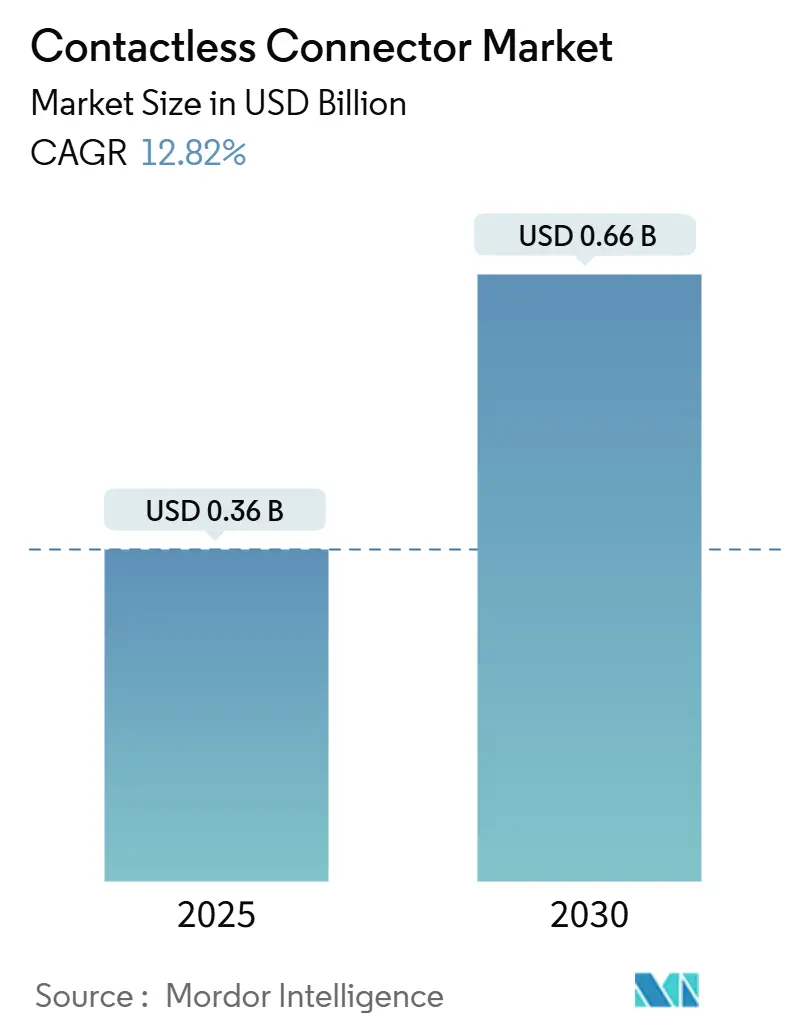

The contactless connector market size is estimated at USD 0.36 billion in 2025 and is projected to reach USD 0.66 billion by 2030, growing at a 12.82% CAGR. Adoption accelerates as design teams replace wear-prone mechanical interfaces with sealed, galvanically isolated power and data links that operate across air gaps measuring up to 150 mm, a capability now validated in commercial couplers and wireless charging pads. Manufacturers emphasize ingress-protection, ease of maintenance, and EMI mitigation, which together underpin robust demand across industrial automation, automotive electrification, and high-density consumer electronics. Major suppliers expand their hybrid portfolios by blending legacy wired products with proprietary inductive, RF, and optical solutions, while venture-backed specialists focus on long-range infrared and multi-kilowatt inductive charging technologies. Regional capacity additions in the Asia Pacific, along with strategic alliances among chipset vendors, connector houses, and OEMs, shorten the time-to-market for new reference designs, further supporting the growth of the contactless connector market. Heightened regulatory activity, especially around electric-vehicle (EV) charging safety and medical device hygiene, creates a policy tailwind that favors contactless architectures.

Key Report Takeaways

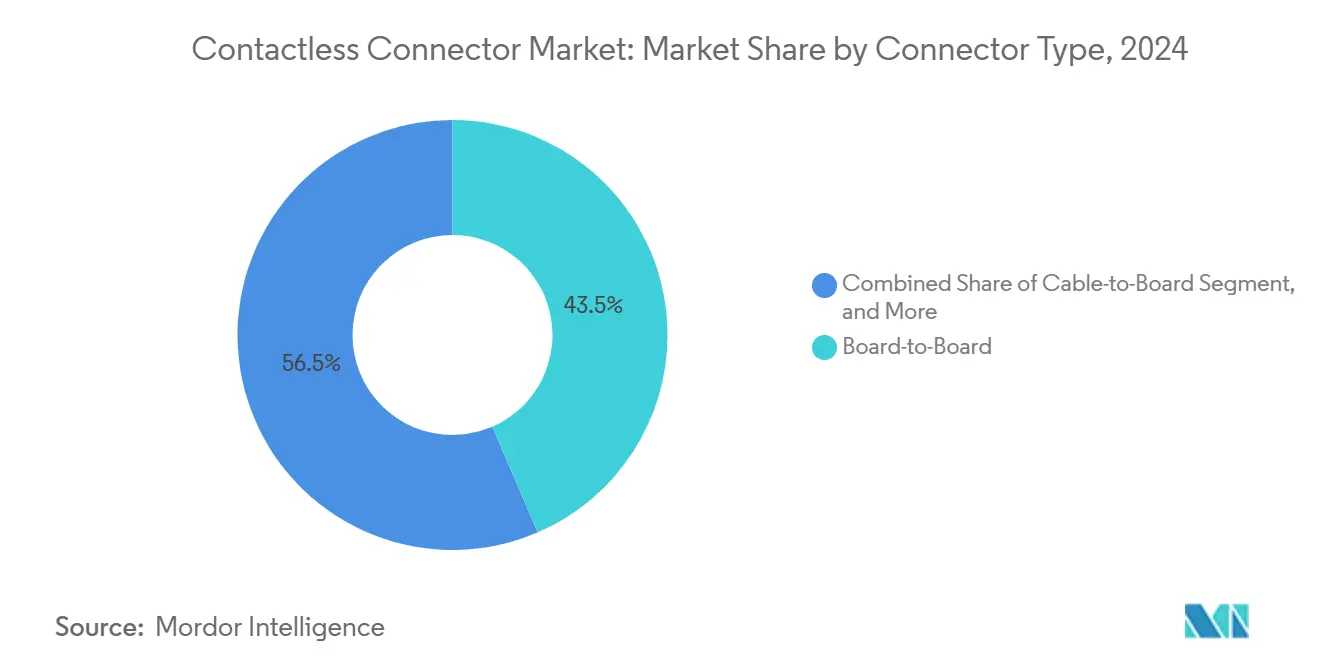

- By connector type, board-to-board units captured 43.51% of the contactless connector market share in 2024, whereas chip-to-chip variants are projected to log the fastest growth rate of 13.78% through 2030.

- By technology, radio-frequency solutions accounted for a 39.87% share of the contactless connector market size in 2024, while magnetic inductive approaches are projected to lead growth at a 13.64% CAGR.

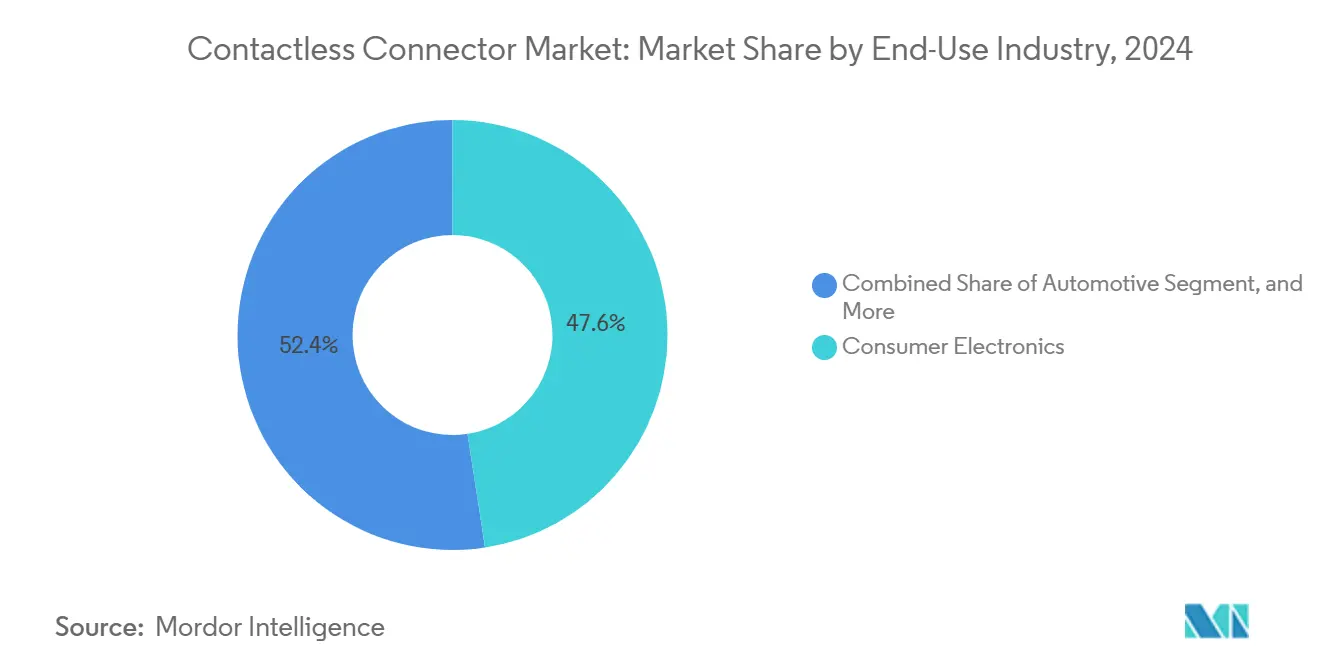

- By end-use industry, consumer electronics led with 47.59% share in 2024; automotive applications are expected to expand at a 13.48% CAGR to 2030.

- By application, data transfer held a 41.23% share of the contactless connector market size in 2024; however, charging solutions are advancing at a 13.39% CAGR.

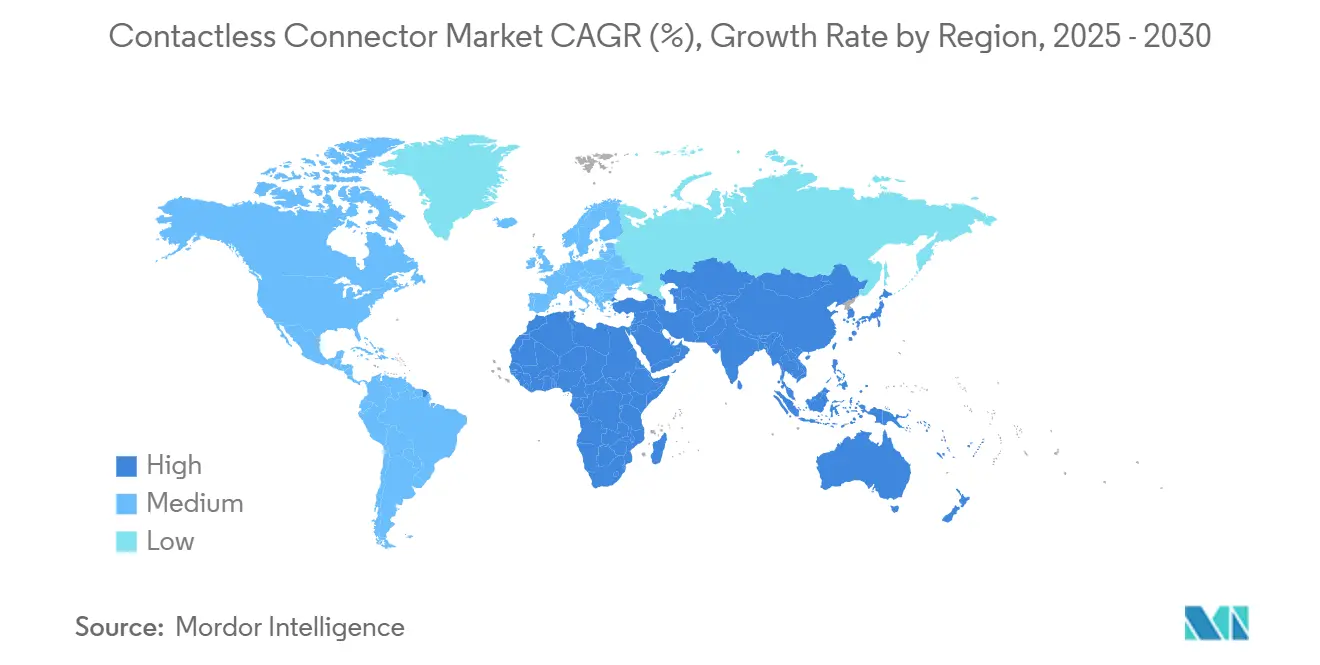

- By geography, the Asia Pacific region dominated with 49.71% revenue in 2024, whereas the Middle East is forecast to post the highest CAGR of 13.64%.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Contactless Connector Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for waterproof and dustproof designs | +2.1% | Global, led by Asia Pacific production hubs | Medium term (2-4 years) |

| Rapid proliferation of 5G-enabled electronics | +2.8% | North America and Asia Pacific, spillover to Europe | Short term (≤ 2 years) |

| Increasing adoption of autonomous driving architectures | +2.3% | North America and Europe, expanding in Asia Pacific | Long term (≥ 4 years) |

| Miniaturization in medical wearables | +1.9% | Global, concentration in North America and Europe | Medium term (2-4 years) |

| Growth of Industry 4.0 wireless lines | +2.4% | Europe and Asia Pacific manufacturing regions | Medium term (2-4 years) |

| Regulatory push for connector-free EV charging | +1.7% | Global, led by European and California frameworks | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Waterproof and Dustproof Device Designs

Sealed electronics used in industrial robotics, outdoor telecom, and home-appliance platforms increasingly specify contactless couplers that eliminate mating surfaces vulnerable to moisture ingress. Phoenix Contact’s NearFi system, for example, transfers 100 Mbps Ethernet and 50 W of power across a 40 mm gap while sustaining IP65 and IK06 ratings, thereby extending service life in wash-down and high-shock settings. By removing mechanical contacts, design teams simplify gasket architectures, reduce maintenance cycles, and mitigate vibration-induced failures. These reliability gains reduce the total cost of ownership, an argument that resonates strongly in Industry 4.0 conversions of brownfield factories. As purchasing departments normalize lifetime cost analyses over upfront component price, the driver exerts an increasingly positive influence on the contactless connector market.

Rapid Proliferation of 5G-Enabled Consumer Electronics

Higher radio frequencies and denser antenna arrays require interconnects with minimal parasitic effects and superior shielding. Contactless RF couplers meet these demands by leveraging tuned cavity structures that maintain impedance control without the dimensional restrictions of pogo-pin or spring-probe interfaces. Component suppliers such as Smiths Interconnect now specify contactless Mini-Lock terminations up to 110 GHz, illustrating scalability toward future 6G bands.[1]Smiths Interconnect, “Mini-Lock High-Density RF Connector,” smithsinterconnect.com OEMs also value the form-factor flexibility: eliminating a physical port enables slimmer handset edges and uninterrupted cosmetic surfaces. Regulatory agencies, including the United States Federal Communications Commission (FCC), continue to tighten radiated-emission limits, indirectly reinforcing the adoption of air-gap solutions that reduce ground-loop noise. The resultant design pull drives incremental unit volume and price-premium capture throughout the forecast period.

Increasing Adoption of Autonomous Driving Architectures

Advanced driver-assistance and fully autonomous platforms require hundreds of sensor inputs and distributed computing modules, which escalates connector cycle counts and increases exposure to vibration. TE Connectivity’s floating charge coupler for automated guided vehicles (AGVs) demonstrates how contactless power links tolerate 0.5 mm positional misalignment while guaranteeing 30,000 cycles.[2]TE Connectivity, “HDC Floating Charge Connector Portfolio,” te.com Automotive OEMs deploy similar inductive interfaces to bridge high-voltage battery packs and low-voltage control domains, achieving galvanic isolation that simplifies ISO 26262 functional safety compliance. As zonal architectures consolidate wiring harnesses, contactless links further reduce mass and assembly time. The lengthy design cycles of vehicle programs mean that sockets awarded in 2025 will impact series production well into the 2030s, imparting a durable upside to the contactless connector market.

Miniaturization in Medical Wearables

Patient-worn monitors, hearing aids, and implant programmers shift toward sealed housings that can be disinfected without removing batteries or cables. Wi-Charge’s infrared platform transmits multiple watts over room-scale distances, allowing device enclosures rated IPX7 or higher to remain closed throughout service life.[3]Wi-Charge, “Infrared Wireless Power Platform,” wi-charge.com Combined with inductive chip-to-chip links that remove fragile board jumpers, these technologies address the medical community’s infection-control and reliability objectives. Compliance with IEC 60601-1 and FDA biocompatibility mandates serves as an additional catalyst, as contactless power blocks circumvent the corrosion risks inherent to exposed metal contacts. Suppliers active in medical wearables, therefore, expect multi-year, design-win-driven revenue expansion.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High initial cost of proprietary interface IP | -1.8% | Global, higher sensitivity in cost-conscious Asia Pacific markets | Short term (≤ 2 years) |

| Interoperability challenges in multi-vendor systems | -1.4% | Global, acute in North American and European integration projects | Medium term (2-4 years) |

| Efficiency decline at larger transfer distances | -1.6% | Global, most evident in spacious warehouse and outdoor infrastructure sites | Medium term (2-4 years) |

| EMC and safety compliance hurdles in high-power RF links | -1.3% | Global, with stricter enforcement in Europe and Japan | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Initial Cost of Proprietary Contactless Interface IP

Licensing fees tied to patented coil geometries, resonant control ASICs, and secure protocol stacks add appreciable non-recurring engineering (NRE) overhead. Wi-Charge fields a portfolio exceeding 200 patents, while Energous invests heavily in FCC Part 18 and Part 15 certifications, reinforcing high barriers to entry. Start-ups must amortize the expenses of compliance testing, custom ferrite tooling, and EMC chamber testing-often three times those of equivalently rated wired connectors-before entering volume production. In price-sensitive consumer segments, this premium constrains addressable demand and slows supplier switching, limiting near-term upside for the contactless connector market.

Interoperability Challenges Across Multi-Vendor Ecosystems

Industrial automation projects often integrate components from multiple suppliers; however, contactless interfaces lack a unifying standard equivalent to USB-C or RJ-45. AirFuel RF and inductive specifications cover selected wireless-charging use cases, but they do not extend to hybrid power-plus-Gigabit-Ethernet couplers or chip-level data bridges. System integrators, therefore, confront bespoke firmware and calibration steps whenever they mix brands, which inflates commissioning time and raises warranty risk. The additional engineering burden discourages adoption in distributed control and automotive infotainment networks, tempering the growth of the contactless connector market until broader standardization emerges.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Connector Type: Chip-to-Chip Drives the Miniaturization Revolution

Chip-to-chip configurations recorded the highest 13.78% CAGR outlook, reflecting semiconductor roadmaps that integrate inductive micro-coils and ferrite layers directly within advanced packages. Although board-to-board formats commanded the largest 43.51% revenue share during 2024, chipset-embedded contactless links are now displacing traditional wire bonds in multi-die modules that handle AI inference and mmWave transceivers. The shift compresses z-height, removes fragile solder joints, and offers galvanic isolation among disparate voltage domains—critical for functional safety in EV powertrains. Flex-to-board and cable-to-board variants serve niche needs where mechanical deflection or harsh environmental sealing is paramount, but neither matches the anticipated volume trajectory of ultrathin chip-level sockets. In several pilot programs, the contactless connector market size for chip-to-chip couplers is projected to double between 2025 and 2028 as mainstream smartphones and wearables adopt advanced substrates.

Design services increasingly adopt reference designs that pre-tune resonant frequencies, thereby reducing field-failure rates. Specialist suppliers collaborate with package houses in Japan and South Korea to validate thermal models, ensuring that inductive losses remain below 1 °C rise at 4 W power budgets. These efforts shorten qualification cycles and cultivate ecosystem trust, further reinforcing the growth advantage of chip-integrated solutions. While board-to-board links will persist in industrial control cabinets and retrofit robotics, the strategic narrative now centers on silicon-embedded interfaces that unlock next-generation form factors.

By Technology: Magnetic Inductive Gains Share Against RF Dominance

Radio-frequency coupling retained 39.87% of 2024 revenue because it supports centimeter-scale gaps and multi-hundred-megabit signaling, traits exploited in factory floor contactless Ethernet hubs. Yet magnetic inductive circuits post the leading 13.64% CAGR through 2030 owing to their superior 85-95% transfer efficiencies and reduced EMC footprints. Delta’s M∞V system, for instance, delivers up to 30 kW at 95% efficiency across 150 mm, a benchmark that resonates with logistics-robot OEMs seeking to minimize battery downtime. Optical couplers and capacitive plates occupy specialized terrain, ranging from space-borne radar front ends to ultra-thin smartcards, but their penetration remains bounded by alignment tolerances and susceptibility to foreign objects.

The R&D direction illustrates a pivot toward integrated control silicon that actively tunes coil impedance in real-time, thereby mitigating coil-to-coil misalignment losses. Suppliers are also experimenting with composite ferrite polymers to reduce mass and accommodate curved surfaces. Such material advances, combined with regulatory clarity from IEC 61980 on EV inductive power transfer, underpin the magnetic inductive segment’s ascent. Nevertheless, RF technology will continue to hold a substantial share of the contactless connector market, where long reach, high data throughput, and multi-device point-to-multipoint topologies remain design priorities.

By End-Use Industry: Automotive Electrification Accelerates Adoption

Automotive platforms represent the fastest-growing vertical at a 13.48% CAGR, thanks to EV charging paddles, in-cabin sensor hubs, and zonal-architecture gateways that benefit from maintenance-free designs. Major Tier-1 suppliers incorporate contactless signal and power blocks within 48 V wiring harnesses, enabling modular sub-assemblies that workers can snap together without the need for torque tools, thereby reducing labor costs on high-volume assembly lines. Consumer electronics, however, retained top billing with a 47.59% revenue share in 2024, reflecting the entrenched adoption of smartphone wireless charging pads and smartwatch docking cradles. The industrial automation, medical devices, and aerospace sectors follow, each valuing the reliability and ingress-protection advantages inherent in air-gap connections.

Automotive design authorities anticipate that contactless power couplers will underpin hands-free robotic charging depots, avoiding contamination and vandalism issues at public facilities. Standards bodies such as SAE codify test procedures for coil-to-coil alignment and stray-field exposure, actions that de-risk large-scale rollouts. Conversely, consumer-electronics BOM costs continue to exert downward pressure, signaling price-sensitive suppliers to streamline coil production and leverage system-in-package integration to sustain margins.

By Application: Charging Solutions Accelerate, Data Transfer Retains Scale

Data transfer still constitutes the largest 41.23% slice, as high-speed couplers service Ethernet, USB, and custom SerDes protocols in autonomous robots and panel PCs. The contactless connector market share for charging applications, however, logs the highest 13.39% CAGR, buoyed by fleet investments in AGVs and last-mile delivery drones that require rapid, unattended energy top-ups. Energous set a milestone by shipping record volumes of 1 W and 2 W PowerBridge transmitters during late-2024 corporate deployments inside retail supply-chain tracking systems. Identification and sensing use cases-ranging from tool presence detection to seat-belt buckle confirmation-advance steadily as Melexis and others roll out ASICs that integrate both sensor coil and control logic on a single die, minimizing BoM and PCB complexity.

In the longer term, analysts expect application boundaries to blur, with hybrid modules simultaneously providing 60W power and multi-gigabit signaling over a single contactless link. Such convergence raises average selling prices and embeds the technology deeper into mission-critical workflows.

Geography Analysis

The Asia Pacific, encompassing China, Japan, South Korea, and Taiwan, generated 49.71% of 2024 revenue, driven by dense consumer electronics manufacturing clusters and a local supply of ferrite cores, high-frequency laminates, and assembly automation services. Government incentives for smart-factory upgrades channel capital toward maintenance-free connectors that mitigate unplanned downtime. Japanese regulators have already approved 1 W RF power bridges for unlimited distance operation, demonstrating a pragmatic approach to spectrum allocation that accelerates commercialization. South Korea’s semiconductor ecosystem further catalyzes the adoption of chip-to-chip contactless technology, leveraging fan-out wafer-level packaging lines to integrate inductive loops directly into redistribution layers.

North America benefits from investments in automotive electrification and a vibrant logistics and robotics market. Tier-1 suppliers collaborate with EV-charging start-ups to prototype hands-free inductive pads compatible with SAE J2954 alignment protocols. Aerospace and defense contractors also specify optical and inductive links to satisfy shock, vibration, and out-gassing requirements. Europe mirrors these trends but adds a strong Industry 4.0 dimension: German and Italian machine builders embed contactless Ethernet couplers in modular production cells to simplify cleaning and quick-change tooling. Phoenix Contact, HARTING, and Rosenberger maintain regional design centers, allowing rapid customization for IEC-63171-6 and EN-45545-2 compliance.

The Middle East is projected to post the highest 13.64% CAGR forecast as energy companies retrofit desert pipelines and solar farms with hermetically sealed sensors. Industrial conglomerates in the Gulf States sponsor pilot programs for wireless power pads that service cleaning robots in airports and smart-city installations. Africa and South America present nascent yet adjacent opportunities in mining and remote microgrid infrastructure, where eliminating exposed contacts enhances asset uptime in abrasive or humid environments.

Competitive Landscape

The contactless connector sector features a balance of global interconnect incumbents and specialized wireless-power pure-plays. TE Connectivity, Amphenol, and Phoenix Contact utilize extensive sales channels to cross-sell inductive or RF add-ons to their existing wired customers. At the same time, dedicated innovators such as Wi-Charge, Energous, and Keyssa emphasize patented long-range or high-bandwidth technologies, often partnering with module assemblers to reach mass markets. Molex’s 2024 acquisition of Keyssa’s IP portfolio exemplifies a convergence strategy, allowing the company to weave ultra-short-range 6 Gbps links into automotive infotainment harnesses without retooling legacy factories.

Strategic collaborations dominate go-to-market plays: Delta pairs its 30 kW M∞V pads with AGV integrators, while Smiths Interconnect co-designs mmWave contactless links with radar chipset vendors. Distributors such as Mouser accelerate engineering adoption by stocking reference evaluation kits and publishing cross-vertical application notes. Pricing pressure persists in mature consumer electronics, but mission-critical aerospace, medical, and factory automation applications sustain margin premiums, thereby mitigating the risk of commoditization. Overall, no single vendor commands an outsized portion of global revenue, although brand recognition and certification track records create durable entry barriers.

Contactless Connector Industry Leaders

TE Connectivity Ltd.

Amphenol Corporation

Molex LLC

Japan Aviation Electronics Industry, Ltd.

Rosenberger Hochfrequenztechnik GmbH and Co. KG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Phoenix Contact introduced NearFi contactless couplers that transmit 50 W of power and 100 Mbps Ethernet across 40 mm air gaps, achieving IP65 and IK06 protection for harsh industrial settings.

- May 2025: Wi-Charge secured USD 20 million in Series C funding led by Standard Investments to scale manufacturing of its infrared wireless-power platform and broaden OEM integrations.

- February 2025: Molex completed the acquisition of Keyssa’s wireless-connector technology, integrating the contactless IP into its automotive and consumer-electronics portfolios.

- January 2025: TE Connectivity expanded its HDC floating charge connector line for AGV and AMR applications, boosting ratings to 250 V / 80 A and durability to 30,000 mating cycles.

Global Contactless Connector Market Report Scope

| Board-to-Board |

| Cable-to-Board |

| Flex-to-Board |

| Chip-to-Chip |

| Radio Frequency (RF) |

| Magnetic Inductive |

| Optical |

| Capacitive |

| Consumer Electronics |

| Automotive |

| Industrial Automation |

| Medical Devices |

| Aerospace and Defense |

| Charging |

| Data Transfer |

| Identification and Authentication |

| Sensing |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Connector Type | Board-to-Board | ||

| Cable-to-Board | |||

| Flex-to-Board | |||

| Chip-to-Chip | |||

| By Technology | Radio Frequency (RF) | ||

| Magnetic Inductive | |||

| Optical | |||

| Capacitive | |||

| By End Use Industry | Consumer Electronics | ||

| Automotive | |||

| Industrial Automation | |||

| Medical Devices | |||

| Aerospace and Defense | |||

| By Application | Charging | ||

| Data Transfer | |||

| Identification and Authentication | |||

| Sensing | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is the projected value of the contactless connector market in 2030?

The market is expected to reach USD 0.66 billion by 2030, expanding at a 12.82% CAGR.

Which connector type is growing the fastest?

Chip-to-chip contactless links lead with a forecast 13.78% CAGR, driven by advanced semiconductor packaging.

Which application is projected to add the most incremental revenue?

Charging solutions, particularly in AGVs and EVs, show the highest 13.39% CAGR through 2030.

Which region commands the largest market share?

Asia Pacific held 49.71% of 2024 revenue owing to its concentrated electronics manufacturing base.

What is the key restraint hampering faster adoption?

High upfront licensing and certification costs of proprietary technologies remain the primary barrier.

Which industry vertical is forecast to grow the quickest?

Automotive electrification is set to advance at 13.48% CAGR as OEMs pursue maintenance-free charging and sensor links.

Page last updated on: