Consumer Electronics Printed Circuit Board Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 34.76 Billion |

| Market Size (2031) | USD 42.92 Billion |

| Growth Rate (2026 - 2031) | 4.30% CAGR |

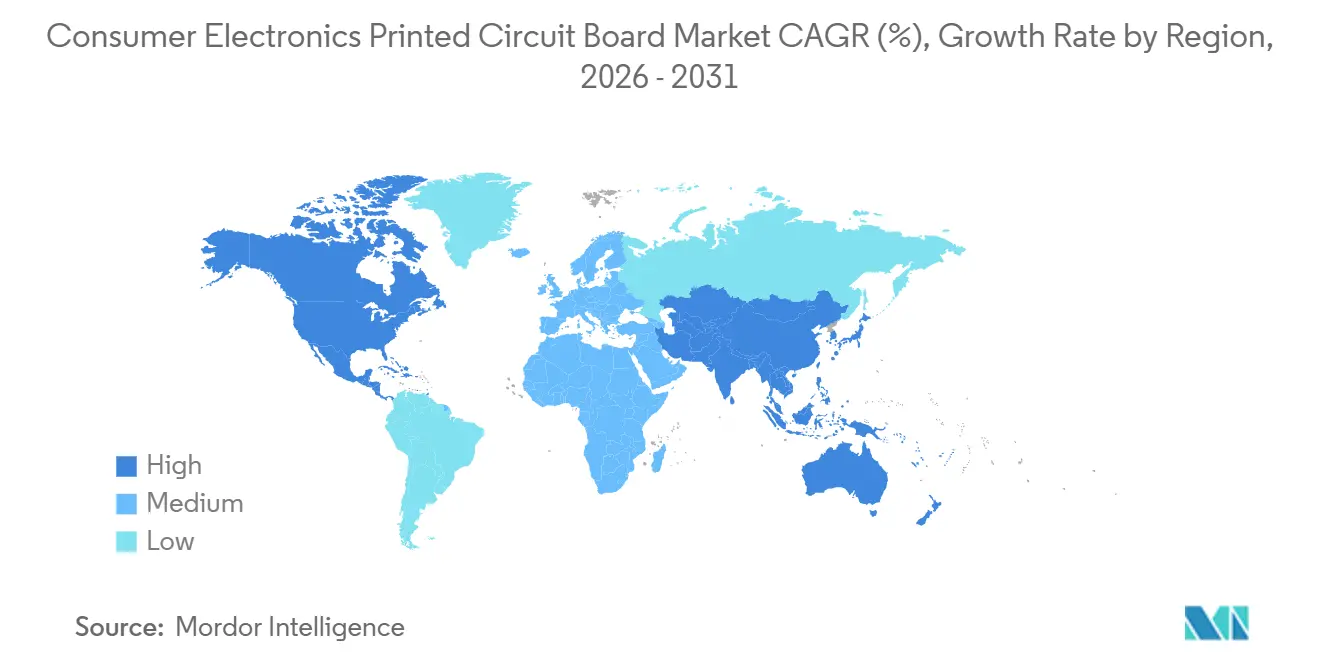

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Consumer Electronics Printed Circuit Board Market Analysis by Mordor Intelligence

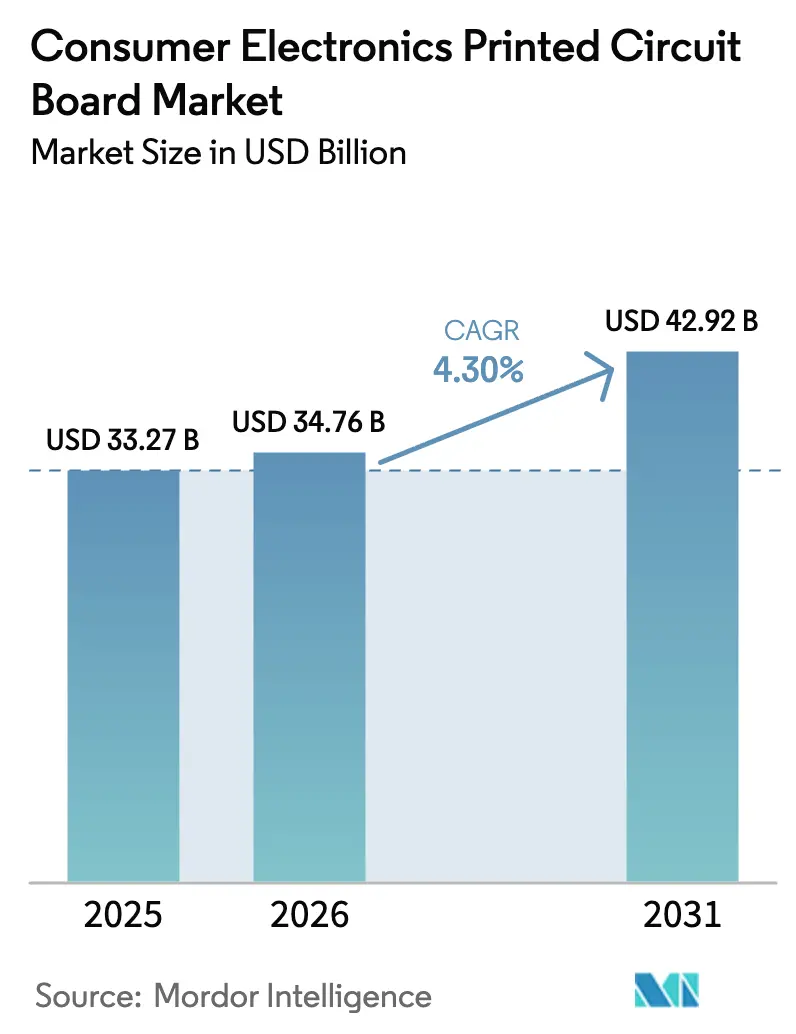

The Consumer Electronics Printed Circuit Board Market size is projected to be USD 33.27 billion in 2025, USD 34.76 billion in 2026, and reach USD 42.92 billion by 2031, growing at a CAGR of 4.30% from 2026 to 2031.

This steady trajectory hides a widening performance gap between commodity board fabricators and high-margin substrate specialists, a divide driven by constrained ABF film supply, rising copper costs, and accelerating demand for on-device artificial intelligence, high-density interconnects, and flexible form factors. Leading smartphone brands are locking in multi-year HDI capacity to secure launch schedules, while Western subsidies and Indian production-linked incentives reshape geographic supply patterns. Capital expenditure from Taiwanese, Japanese, and European leaders now exceeds historical norms, signaling that the next growth phase will reward process control, material innovation, and geographically diversified footprints. Simultaneously, regulatory pressures, from e-waste collection targets to export-control tightening, add compliance complexity that favors well-capitalized incumbents.

Key Report Takeaways

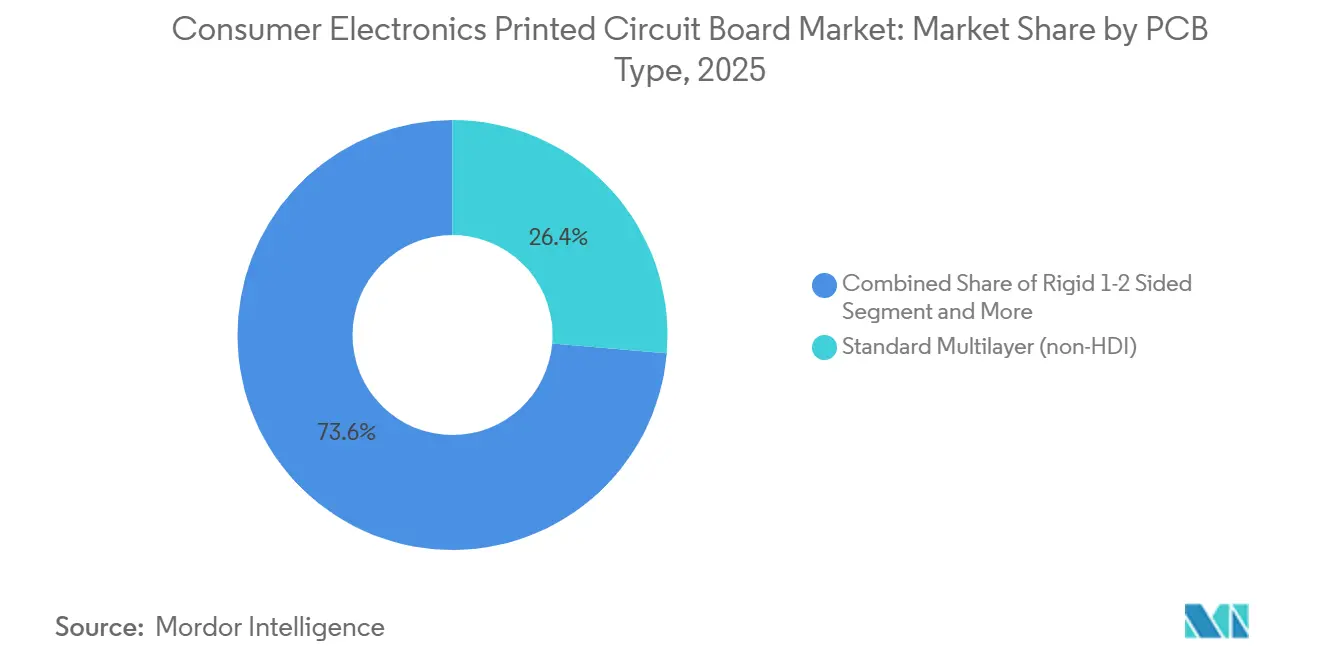

- By PCB type, Standard Multilayer held 26.36% of consumer electronics PCB market share in 2025, while Flexible Circuits are forecast to expand at a 6.21% CAGR through 2031.

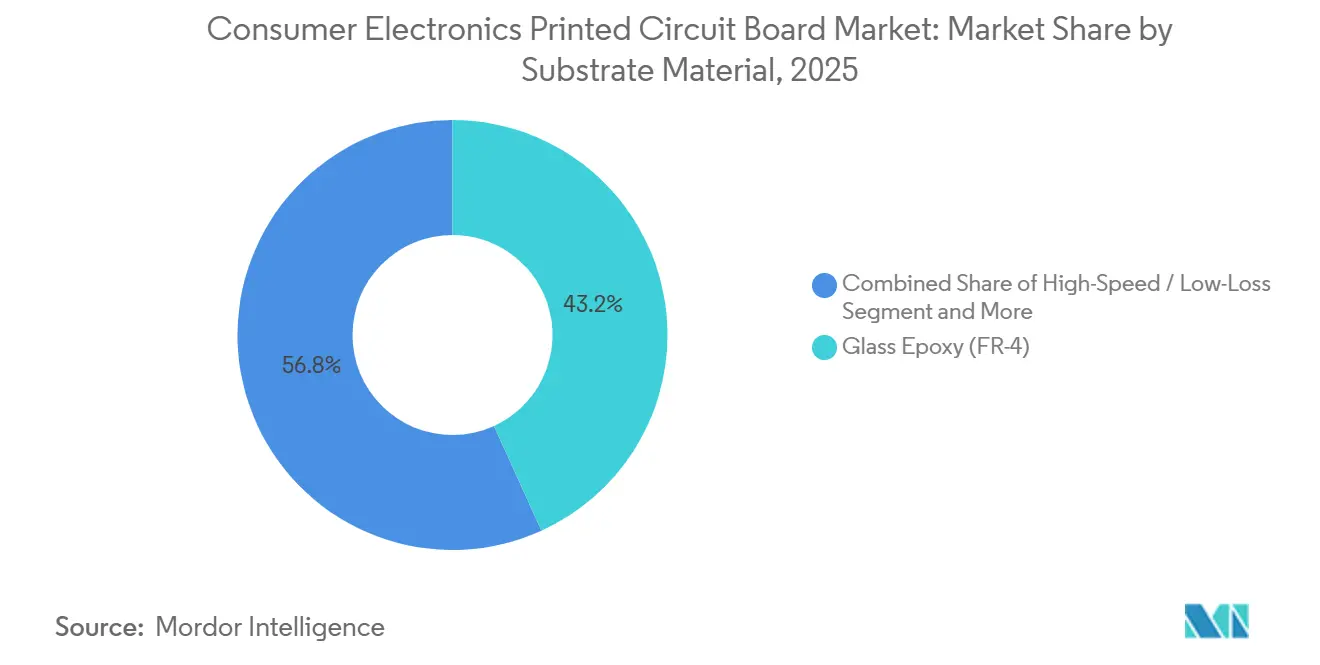

- By substrate material, Glass Epoxy accounted for 43.21% share of the consumer electronics PCB market size in 2025; Polyimide is advancing at a 5.70% CAGR to 2031.

- By geography, Asia Pacific commanded an 84.01% revenue share in 2025, and the region is progressing at a 4.85% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Consumer Electronics Printed Circuit Board Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of HDI Boards in Flagship Smartphones | +0.8% | Asia Pacific core, spillover to North America and Europe | Medium term (2-4 years) |

| Surging Wearables Shipments Driving Flexible PCB Demand | +0.7% | Global, concentrated in Asia Pacific manufacturing hubs | Short term (≤ 2 years) |

| Transition to Packaging Substrates for Advanced Chiplets | +0.9% | Global, led by North America design and Asia Pacific fabrication | Long term (≥ 4 years) |

| Mini-LED Backlighting Adoption in TVs and Tablets | +0.5% | Asia Pacific manufacturing, North America and Europe end-markets | Medium term (2-4 years) |

| On-Device AI Processing Requiring High-Speed Low-Loss Materials | +0.6% | Global, early adoption in North America and Asia Pacific | Long term (≥ 4 years) |

| Supply-Chain Localization Incentives in United States and India | +0.7% | North America and India, indirect effects in Asia Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Proliferation Of HDI Boards In Flagship Smartphones

Galaxy S26 and forthcoming iPhone 17 platforms employ any-layer boards with stacked microvias under 100 µm, forcing fabricators to maintain sub-50 µm registration accuracy[1]Source: Samsung Newsroom, “Samsung Galaxy S26 Series Technical Specifications,” news.samsung.com. Taiwanese suppliers invested more than USD 500 million in laser drilling and sequential lamination during 2025 to meet these tolerances. Only a handful of companies possess the necessary equipment, concentrating share with Zhen Ding Technology, Unimicron, and Compeq. As average smartphone layer counts exceed 10, program delays now run into quarters when a tier-one HDI line goes offline, amplifying supply-chain risk for handset makers.

Surging Wearables Shipments Driving Flexible PCB Demand

Global wearables shipments topped 500 million units in 2025, and the installed base is set to exceed 1 billion devices by 2028. Flex circuits wrap around curved housings and survive millions of bend cycles, traits essential for foldables and smartwatches. LG Innotek and Flexium added polyimide-based capacity in 2025 ahead of Apple’s anticipated foldable launch in late 2026. Polyimide costs remain elevated, yet device brands prioritize form factor and durability over bill-of-material cost. Rollable and stretchable circuits nearing pilot scale will widen the technology moat around material and equipment innovators.

Transition To Packaging Substrates For Advanced Chiplets

Chiplet architectures, supported by the UCIe 1.1 specification, require substrates with sub-40 µm line-and-space geometry and thousands of microvias per cm². Intel’s EMIB and AMD’s EPYC lines already rely on such substrates. Substrate demand is therefore decoupled from total PCB volumes because every new chiplet SKU needs a bespoke design. Ibiden, Kinsus, and Shinko are adopting modified semi-additive processes, but high capex and yield challenges limit the field of qualified vendors, keeping margins resilient despite commodity price inflation.

On-Device AI Processing Requiring High-Speed Low-Loss Materials

Edge AI accelerators generate higher heat and demand faster signaling between processor and memory. Designers now specify laminates with dielectric constants below 3.5 and dissipation factors under 0.005 at multi-gigahertz frequencies[2]Source: Glenn Zorpette, “On-Device AI Accelerators Drive Demand for Low-Loss PCB Materials,” IEEE Spectrum, spectrum.ieee.org. Rogers Corporation and Panasonic debuted hydrocarbon-ceramic materials in 2024 that carry 10 Gbps signals across thinner boards, enabling tighter component placement. Automotive advanced driver-assistance systems, which fuse radar, lidar, and camera data in real time, represent an early high-value use case where signal integrity carries safety implications.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tight ABF Substrate Capacity Constraining High-End Devices | -0.6% | Global, acute in Asia Pacific fabrication hubs | Short term (≤ 2 years) |

| Rising Copper and Resin Prices Squeezing OEM Margins | -0.5% | Global, most severe in Asia Pacific and Europe | Short term (≤ 2 years) |

| Geopolitical Export Controls on Advanced Packaging Technology | -0.4% | China primarily, indirect effects in Asia Pacific | Medium term (2-4 years) |

| Stringent E-Waste Regulations Increasing Compliance Costs | -0.3% | Europe and North America, expanding to Asia Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Tight ABF Substrate Capacity Constraining High-End Devices

Ajinomoto Fine-Techno supplies roughly 98% of global ABF film, and allocation for 2026 is fully booked. Kinsus reported lead times stretching to 26 weeks in late 2025, up from 16 weeks in 2024. Data-center server makers and AI accelerator vendors, which require 12-plus layer FC-BGA substrates, face launch delays unless capacity expansions in Japan come online in 2027.

Rising Copper And Resin Prices Squeezing OEM Margins

Copper spot prices rose from USD 9,173 per ton in Q4 2024 to USD 11,114 in Q4 2025 and are trending toward USD 12,000 in early 2026. Each 10% copper price increase lifts finished board costs by roughly 3%-4% absent contract renegotiation. Epoxy resins also climbed due to environmental curbs on Chinese and Indian petrochemical plants, compressing margins for Kingboard Laminates and Nan Ya Plastics. Smaller fabricators are already exiting low-margin segments, tightening supply for commodity boards.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By PCB Type: Flexible Circuits Gain Momentum Over Legacy Multilayer

Standard Multilayer boards held 26.36% of consumer electronics printed circuit board market revenue in 2025, reflecting their entrenched role in cost-sensitive applications. Flexible Circuits, however, are projected to register a 6.21% CAGR through 2031, outpacing every other category. Wearable devices and foldable smartphones fuel this surge, demanding circuits that bend repeatedly without failure[3]Source: Jack Farchy, “Global Wearables Shipments Exceed 500 Million Units,” Financial Times, ft.com. The consumer electronics PCB market size for Flexible Circuits is therefore forecast to climb faster than legacy multilayer volumes, even as commodity suppliers fight price erosion.

Rigid-Flex hybrids blend rigid sections with flex tails, winning share in medical and aerospace devices where space and weight remain critical. IC Substrates, though lower in unit volume, capture premium margins by serving high-performance processors. Capacity additions in Taiwan and Japan, valued at more than USD 3 billion between 2024 and 2026, underscore how substrate scarcity reshapes design roadmaps. HDI adoption in flagship smartphones remains another structural tailwind, with via diameters dipping below 100 µm and layer counts surpassing 10. Rigid 1–2-Sided boards persist in power supplies and LED lighting but face margin pressure from Chinese high-volume producers.

By Substrate Material: Polyimide Emerges As Fastest-Growing Category

Glass Epoxy (FR-4) captured 43.21% revenue in 2025 thanks to cost efficiency and mature supply chains. Polyimide’s superior thermal stability and flexibility, however, drive a 5.70% CAGR to 2031, the fastest in the material mix. The consumer electronics printed circuit board market share for Polyimide already expanded in 2025 as LG Innotek and Nippon Mektron scaled new lines in Southeast Asia[4]Source: Kana Inagaki, “Nippon Mektron and Fujikura Expand Flexible Circuit Capacity,” Nikkei Asia, asia.nikkei.com. High-Speed Low-Loss laminates, built on hydrocarbon or ceramic fillers, address data-center and automotive radar applications where signal integrity is paramount.

Packaging Resins, especially ABF film, remain tightly supplied, capping near-term growth despite robust demand from chiplet packages. Metal-core and liquid-crystal polymer substrates serve niche high-frequency or high-thermal-load markets, commanding heavy price premiums. DuPont and Kaneka capacity expansions are expected to narrow supply gaps by 2027, but elevated energy costs will keep Polyimide pricing firm in the medium term.

Geography Analysis

Asia Pacific generated 84.01% of 2025 revenue and is expected to record a 4.85% CAGR through 2031. Taiwan houses more than 60% of global IC substrate capacity, supplying Apple, Nvidia, and AMD. China added 15 million m² of new multilayer and flexible capacity in 2025, leveraging low-cost clusters in Guangdong and Jiangsu. South Korea focuses on flexible circuits for foldables, while Japan specializes in high-reliability boards for automotive and aerospace.

North America and Europe combined for 15.99% of 2025 sales, yet localization incentives are accelerating expansion. The United States awarded USD 75 million to Absolics and USD 85 million to TTM Technologies to build advanced substrate lines. AT&S is investing EUR 2 billion (USD 2.2 billion) in Malaysia to serve European customers. India’s production-linked incentives worth INR 22,919 crore (USD 2.8 billion) aim to reduce import dependence, with domestic production projected to reach USD 5 billion by 2028.

South America, the Middle East, and Africa remain below 2% of global volume. However, rising e-waste regulations in Europe and North America could redirect some final-assembly work to emerging regions with lower compliance costs. Geopolitical tension around Taiwan and export controls on advanced packaging tools reinforce the strategic weight of new capacity in North America, Europe, and South Asia.

Competitive Landscape

In 2025, the top 10 suppliers in the consumer electronics printed circuit board market secured approximately 45% of the global revenue, indicating a moderate concentration in the industry. Unimicron, Nan Ya PCB, Tripod Technology, and Kinsus have established dominance in the high-end substrate supply, a feat achieved through decades of process refinement and consistent innovation. These companies have leveraged their expertise to maintain a competitive edge in a market that demands precision and reliability. Meanwhile, Samsung Electro-Mechanics and LG Innotek have taken the lead in flexible circuits, capitalizing on their vertical integration with display and battery divisions. This integration allows them to streamline production processes and achieve cost efficiencies, further solidifying their market position. Japanese firms Ibiden, Kyocera, and Nippon Mektron are carving a niche by focusing on high-reliability boards tailored for the automotive and industrial sectors, where stringent qualification cycles and regulatory requirements pose significant challenges for new entrants. These companies benefit from their long-standing reputation for quality and reliability, which acts as a barrier to entry for competitors.

Investment intensity in the sector is on the rise, driven by the need to meet growing demand and technological advancements. By 2027, Samsung Electro-Mechanics plans to invest a substantial KRW 4.5 trillion (equivalent to USD 3.4 billion) to enhance its FC-BGA capacity, reflecting its commitment to scaling operations and addressing market needs. Highlighting the importance of technology as a competitive edge, AT&S secured 37 patents on embedded-component substrates between 2024 and 2025, showcasing its focus on innovation and intellectual property as key growth drivers. In a strategic move to diversify its portfolio, TTM Technologies broadened its horizons by acquiring Anaren in 2024, delving into radiofrequency and microwave applications.

This acquisition enables TTM Technologies to expand its capabilities and cater to emerging market demands. While startups are venturing into additive manufacturing for rapid prototyping, challenges like yield and unit cost confine them to niche volumes, limiting their scalability in the broader market. Quality standards IPC-6012 and IPC-6013 remain pivotal as industry benchmarks, ensuring that products meet the rigorous demands of end-users and regulatory bodies. These standards continue to act as quality gateways, fostering trust and reliability in the market.

Consumer Electronics Printed Circuit Board Industry Leaders

Zhen Ding Technology Holding Limited

Unimicron Technology Corp.

AT&S Austria Technologie & Systemtechnik AG

TTM Technologies Inc.

Samsung Electro-Mechanics Co. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Samsung Electro-Mechanics confirmed full FC-BGA allocation through 2026 and outlined a KRW 4.5 trillion (USD 3.4 billion) expansion.

- December 2025: Unimicron finished phase one of its Kunshan ABF substrate project, adding 200,000 m² annual capacity.

- November 2025: AT&S began equipment installation at its EUR 2 billion (USD 2.2 billion) Kulim facility, with production slated for Q3 2026.

- October 2025: Ibiden reached 70% completion of its JPY 150 billion (USD 1.0 billion) IC substrate build-out in Ogaki, Japan.

Global Consumer Electronics Printed Circuit Board Market Report Scope

The consumer electronics PCB Market Report is Segmented by PCB Type (Standard Multilayer, Rigid 1-2 Sided, High-Density Interconnect, Flexible Circuits, IC Substrates, Rigid-Flex, and Other PCB Types), Substrate Material (Glass Epoxy, High-Speed Low-Loss, Polyimide, Packaging Resins, and Other Substrate Materials), and Geography (North America, Europe, Asia Pacific, South America, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Standard Multilayer (Non-HDI) |

| Rigid 1-2 Sided |

| High-Density Interconnect (HDI) |

| Flexible Circuits (FPC) |

| IC Substrates (Package Substrates) |

| Rigid-Flex |

| Other PCB Types |

| Glass Epoxy (FR-4) |

| High-Speed / Low-Loss |

| Polyimide (PI) |

| Packaging Resins (BT / ABF) |

| Other Substrate Materials |

| North America | United States |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Taiwan | |

| Japan | |

| India | |

| South Korea | |

| Southeast Asia | |

| Rest of Asia-Pacific | |

| Rest of World |

| By PCB Type | Standard Multilayer (Non-HDI) | |

| Rigid 1-2 Sided | ||

| High-Density Interconnect (HDI) | ||

| Flexible Circuits (FPC) | ||

| IC Substrates (Package Substrates) | ||

| Rigid-Flex | ||

| Other PCB Types | ||

| By Substrate Material | Glass Epoxy (FR-4) | |

| High-Speed / Low-Loss | ||

| Polyimide (PI) | ||

| Packaging Resins (BT / ABF) | ||

| Other Substrate Materials | ||

| By Geography | North America | United States |

| Rest of North America | ||

| Europe | United Kingdom | |

| Germany | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Taiwan | ||

| Japan | ||

| India | ||

| South Korea | ||

| Southeast Asia | ||

| Rest of Asia-Pacific | ||

| Rest of World | ||

Key Questions Answered in the Report

How large is the consumer electronics PCB market in 2026?

It reached USD 34.76 billion in 2026 and is forecast to rise to USD 42.92 billion by 2031 with a 4.30% CAGR.

Which PCB type is growing the fastest through 2031?

Flexible Circuits are projected to expand at a 6.21% CAGR as wearables and foldable devices gain share.

Why is ABF substrate capacity a bottleneck?

Ajinomoto controls around 98% of ABF film, and allocation is booked through 2026, delaying high-end device launches.

What role do localization incentives play?

U.S. CHIPS Act and India’s PLI scheme subsidize domestic lines, aiming to diversify supply away from Asia Pacific dominance.

Page last updated on: