Construction Enterprise Resource Planning Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

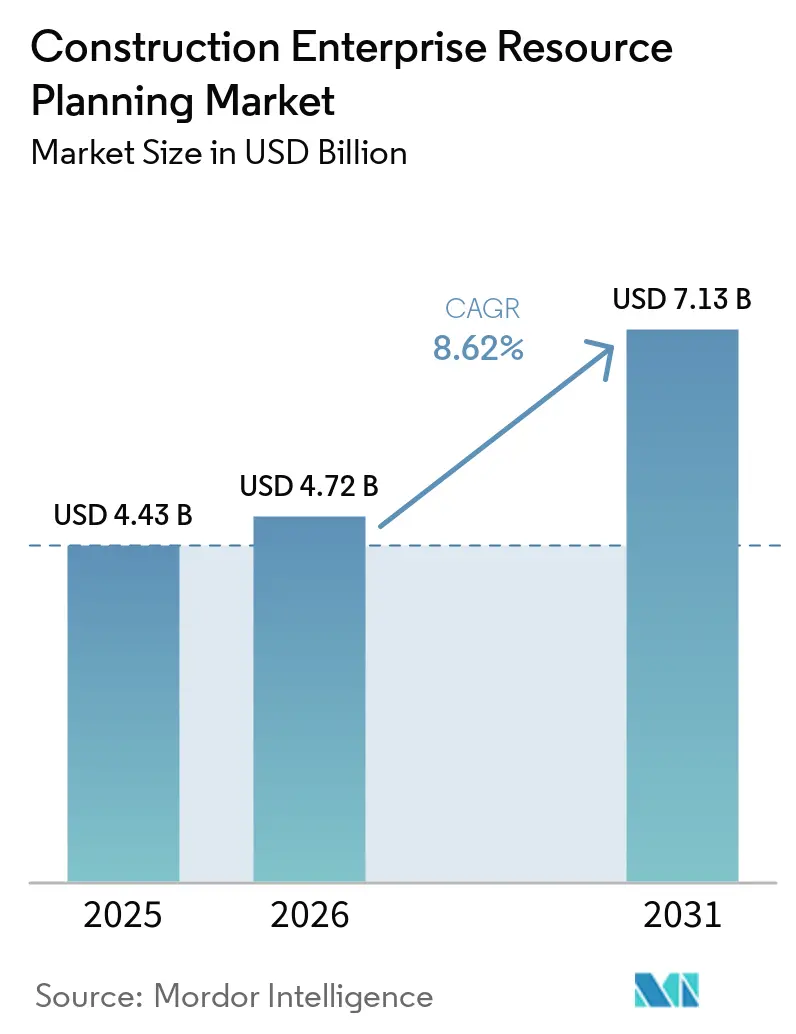

| Market Size (2026) | USD 4.72 Billion |

| Market Size (2031) | USD 7.13 Billion |

| Growth Rate (2026 - 2031) | 8.62% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Construction Enterprise Resource Planning Market Analysis by Mordor Intelligence

The Construction ERP market size is projected to expand from USD 4.43 billion in 2025 and USD 4.72 billion in 2026 to USD 7.13 billion by 2031, registering an 8.62% CAGR between 2026 and 2031. Robust public-sector capital programs, accelerating cloud adoption, and heightened compliance demands are reshaping purchasing priorities and sustaining multi-year software spending. The Construction ERP market is also benefiting from mounting pressure to improve thin margins, which run at 2%–4% for many general contractors, by automating project controls and financial workflows. Vendors that combine multi-tenant cloud architectures with low-code configuration tools are shortening deployment cycles, thereby lowering total cost of ownership and expanding the addressable market for small and mid-size firms. At the same time, agentic artificial intelligence is moving from proof-of-concept to mainstream deployment, allowing project teams to spot cost overruns, forecast cash requirements, and flag safety risks before they materialize. Finally, cybersecurity readiness has become a decisive factor in competitive bids as owners and public agencies insist on SOC 2 Type II attestations and zero-trust frameworks.

Key Report Takeaways

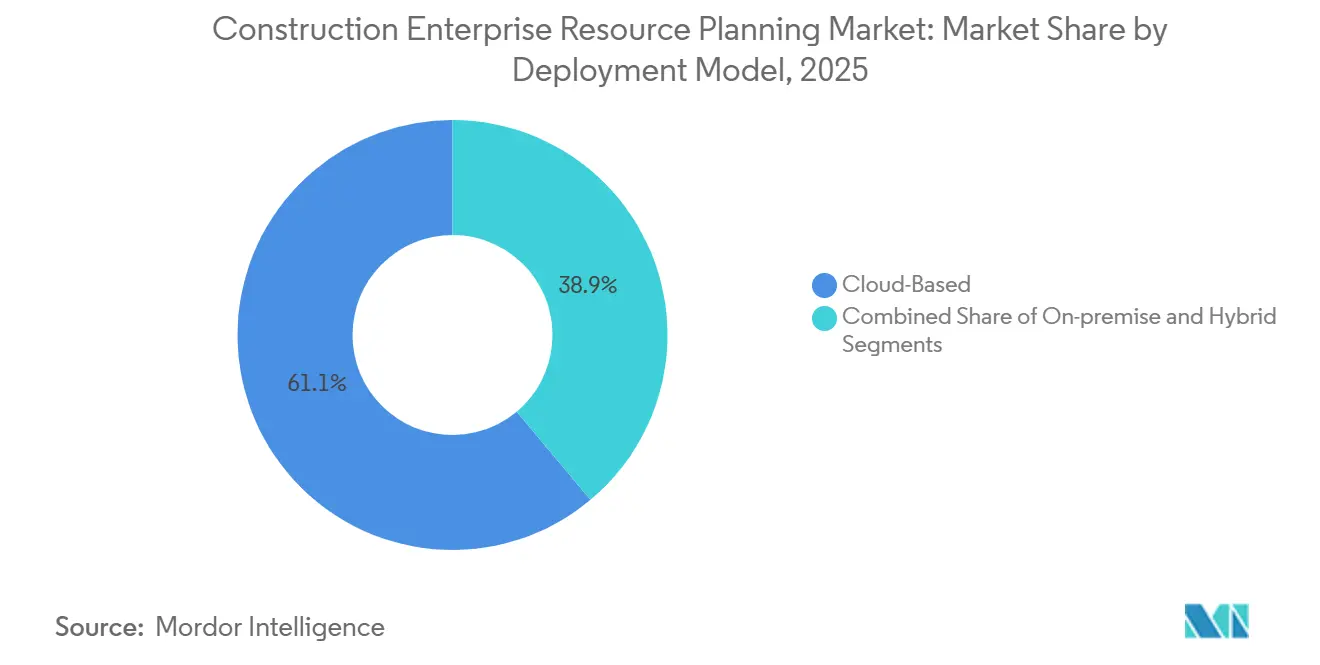

- By deployment mode, cloud-based solutions accounted for 61.10% of revenue in 2025 and expanded at a 11.20% CAGR through 2031.

- By enterprise size, large enterprises led with 58.20% of the Construction ERP market share in 2025; small and medium enterprises are advancing at a 10.40% CAGR to 2031.

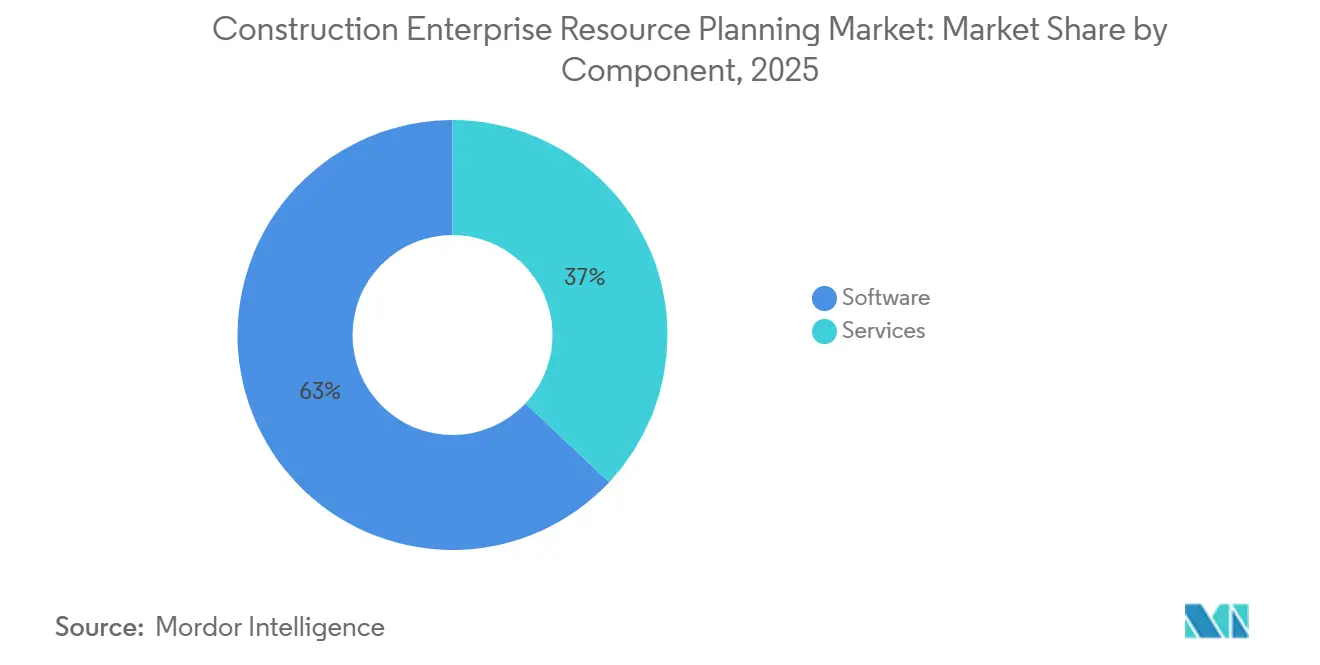

- By solution, software accounted for 63.00% of the Construction ERP market size in 2025, whereas services revenue is growing at a 10.90% CAGR through 2031.

- By end use, commercial construction captured 35.40% of the revenue share in 2025; infrastructure and civil engineering is the fastest-growing segment, with a 12.30% CAGR to 2031.

- By geography, North America dominated with 43.70% revenue share in 2025, while Asia-Pacific is forecast to post a 9.60% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Construction Enterprise Resource Planning Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Adoption of Cloud-Based ERP Solutions | +2.1% | Global, strongest in North America and Europe | Medium term (2-4 years) |

| Increasing Government Infrastructure Spending on Construction | +1.8% | Asia-Pacific, Middle East, North America | Long term (≥4 years) |

| Rising Demand for Mobile-First and Remote Collaboration Capabilities | +1.3% | Global, accelerated in North America and Europe | Short term (≤2 years) |

| Stricter Regulatory Compliance for Construction Accounting and Reporting | +1.0% | North America and Europe, emerging in Middle East and Asia-Pacific | Medium term (2-4 years) |

| Emergence of AI-Powered Predictive Modules Reducing Rework | +0.9% | Early adopters in North America and Europe, expanding into Asia-Pacific | Medium term (2-4 years) |

| Integration of BIM Digital Twin Data with ERP Workflows | +0.7% | Europe and Asia-Pacific | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Growing Adoption of Cloud-Based ERP Solutions

Cloud deployment accounted for 61.10% of revenue in 2025 and is growing at a 11.20% CAGR, nearly 300 basis points above the Construction ERP market. Subscription pricing converts capital expenditures into operating expenses, freeing cash for equipment and labor. Public agencies validate cloud reliability, as seen when the United States Department of Veterans Affairs migrated 171 medical centers to a unified cloud platform in 2025. Vendors now package multi-tenancy and role-based portals so subcontractors can be onboarded in minutes, reducing email back-and-forth. The Federal Risk and Authorization Management Program (FedRAMP) certification, secured by Procore in 2025, has become mandatory for U.S. federal projects.[1]Procore Technologies, “FedRAMP Authorization,” PROCORE.COM European small firms are also entering the fold: Eurostat shows a 48-percentage-point adoption gap between small and large companies, which vendors are narrowing through pay-per-project tiers.[2]Eurostat, “Enterprise ERP Adoption Statistics,” EC.EUROPA.EU

Increasing Government Infrastructure Spending on Construction

Spending momentum is pronounced. The United States Infrastructure Investment and Jobs Act channels USD 1.2 trillion over five years, while the United Kingdom’s 2025 Budget added GBP 1.7 billion (USD 2.15 billion) for major transport corridors.[3]UK Government, “Autumn Budget 2025,” GOV.UK In the Middle East and North Africa, USD 157 billion in contracts were let during the first three quarters of 2025, with Saudi Arabia alone accounting for 31%. India’s National Infrastructure Pipeline and Smart Cities Mission underpin a rise from USD 190.7 billion in 2025 to USD 280.6 billion by 2030. These mega-projects demand joint-venture accounting, earned-value analysis, and multicurrency consolidation modules that generic suites cannot supply.

Rising Demand for Mobile-First and Remote Collaboration Capabilities

Field crews form 80%–90% of construction labor, so mobile access is no longer optional. CMiC’s CrewView app syncs timecards and photos in under a minute, while Procore reported that over half of all interactions were mobile in 2025. Offline capability has become a competitive differentiator for remote sites with spotty connectivity. Younger superintendents expect chat and video tools to be embedded natively rather than grafted on via third-party plug-ins, pressuring lagging vendors.

Stricter Regulatory Compliance for Construction Accounting and Reporting

ASC 606 requires contractors to allocate transaction prices to performance obligations and then recognize revenue over time, adding complexity that spreadsheets cannot handle. On U.S. federal jobs, the Davis-Bacon Act compels weekly certified payrolls, with USD 10,000 fines per infraction. Saudi Arabia’s e-invoicing Phase 2, launched in 2025, mandates real-time submissions to ZATCA. Contractors bidding on defense or infrastructure work are also grappling with Cybersecurity Maturity Model Certification thresholds. ERP platforms that automate these specialized reports are winning share in both mature and emerging regions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Implementation and Customization Costs | -1.4% | Global, acute for SMEs in North America and Europe | Short term (≤2 years) |

| Cybersecurity and Data-Privacy Concerns | -1.1% | Global, heightened in North America and Europe | Medium term (2-4 years) |

| Legacy Data Migration Complexity | -0.8% | North America and Europe | Short term (≤2 years) |

| Shortage of Skilled Construction-Specific ERP Talent | -0.6% | Asia-Pacific and Middle East emerging markets | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

High Upfront Implementation and Customization Costs

Benchmarking shows a 50-person firm spent USD 140,000–210,000 on first-year deployment in 2025, excluding opportunity cost. With net margins at 2%–4%, six-figure outlays deter many bidders. Entry-level subscriptions from Buildertrend and Projul lower sticker shock but omit advanced consolidation and API features, often forcing a costly re-platform within three years.

Cybersecurity and Data-Privacy Concerns

Ransomware incidents surged 70% in 2025. High-profile breaches at Aegis Project Controls and Clark Sullivan Construction exposed gigabytes of sensitive schedules and payroll data. Fines under GDPR and California’s CCPA can reach 4% of global revenue. Owners now demand SOC 2 Type II, ISO 27001, and zero-trust designs before signing long-term contracts, raising vendor compliance costs by USD 50,000–150,000 per year.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Mode: Cloud Platforms Reshape Total Cost of Ownership

Cloud solutions accounted for 61.10% of revenue in 2025 and are growing at a 11.20% CAGR. This strength is anchored in subscription models that shift servers and backups to the vendor's responsibility, thereby reducing capital outlays. The Construction ERP market size for cloud deployments is forecast to climb sharply as public bodies adopt FedRAMP-authorized tools for federal highways and healthcare facilities. Hybrid configurations are growing rapidly because contractors in low-bandwidth regions keep financial cores on-premises while shifting field collaboration to the cloud. On-premise is contracting as vendors phase out perpetual licenses, yet it persists among defense contractors bound by strict data-sovereignty rules.

The Construction ERP market now rewards suppliers that embed rapid provisioning. Procore’s FedRAMP authority has opened lucrative federal channels, forcing rivals to invest 12–18 months to earn similar clearance. Multi-tenant architectures allow general contractors to spin up subcontractor portals immediately, eliminating email-based RFIs. Low-code workflow engines further compress implementation timelines for standard cost-plus or unit-price projects.

By Enterprise Size: Small and Medium Contractors Close the Adoption Gap

Large enterprises held 58.20% of revenue share in 2025, buoyed by multi-year enterprise agreements covering hundreds of active projects. However, SMEs are advancing at a 10.40% CAGR to 2031, narrowing historical adoption gaps. The Construction ERP market share commanded by SMEs is expected to climb as governments launch digitalization grants. Malaysia now subsidizes 50% of software costs. Yet financing constraints linger: 44% of European SMEs reported credit difficulties in 2025. Tiered pricing from Buildertrend and Projul brings entry-level annual fees below USD 10,000, although missing consolidation and fleet modules can create hidden upgrade costs.

Implementation fatigue remains real. A 50-person company allocates 10%–20% of key staff hours during a six-month rollout, disrupting billable work. To compete, vendors are bundling pre-configured templates for residential remodeling, tenant improvement, or heavy civil so SMEs can go live in under eight weeks, thus protecting cash flow and improving time-to-value.

By Solution: Services Revenue Accelerates as Integration Complexity Deepens

Software represented 63.00% of 2025 revenue, yet services are expanding faster, at a 10.90% CAGR, as owners demand bespoke integrations and AI-led analytics. The Construction ERP market size attributable to services is climbing because typical contractors run 5–15 disconnected systems. Procore’s 2026 purchase of Datagrid highlights escalating demand to automate data flows among cost, schedule, and payroll tools. CMiC’s NEXUS platform ships with 25 AI agents but still requires three to six months of workflow tuning.

Training is equally lucrative. Role-based curricula covering revenue recognition, equipment cost allocation, and certified payroll reporting now command 20%–30% of annual license fees for premium support tiers with four-hour response guarantees. The Construction ERP industry has thus shifted from a license‐centric to a lifecycle-value model, where integration roadmaps, managed security, and AI adoption are monetized as recurring service streams.

By End Use: Infrastructure Projects Drive Unit-Price and Equipment-Centric Modules

Commercial construction led with a 35.40% revenue share in 2025, driven by office towers and mixed-use complexes operating under fixed-price contracts. Infrastructure and civil engineering, however, is growing at 12.30% CAGR, the strongest of any end-use, riding Saudi Arabia’s Vision 2030 and India’s railway and highway expansions. The Construction ERP market size tied to infrastructure is ramping because unit-price billing requires granular tracking of cubic meters moved or linear meters installed, features missing in many horizontal software suites.

Heavy civil contractors also need real-time equipment utilization; iron assets can consume 30%–50% of project budgets, yet native fleet modules remain scarce. These facilities comply with OSHA 1926 and 1910 mandates that must be reflected in ERP safety registers.

Geography Analysis

North America generated 43.70% of global revenue in 2025, energized by USD 147.1 billion in the United States Department of Transportation’s 2026 budget and stringent Davis-Bacon certified payroll rules. Canada contributes roughly 8%–10% of regional sales through its Investing in Canada Plan, totaling CAD 180 billion (USD 133 billion) over 12 years. Mexico’s nearshoring-driven factory boom is sparking ERP pilots among tier-one contractors, although smaller firms still favor spreadsheets. U.S. interest-rate hikes temper residential starts, but the Construction ERP market continues to bank on steady maintenance income from renewals and module add-ons.

Asia-Pacific is the fastest-growing region, with a 9.60% CAGR through 2031. India targets USD 280.6 billion in construction outlay by 2030, and Saudi Arabia’s pipeline is slated to reach USD 174.4 billion at 8.7% CAGR by 2030, catalyzing demand for Arabic-language, VAT-ready systems. China’s ERP adoption remains fragmented due to integration hurdles with Golden Tax and data-residency laws. Japan’s Big Five contractors have standardized on enterprise suites and now pilot digital twins to drive predictive maintenance. Southeast Asia enjoys SME-friendly grants and is seeing Construction ERP market penetration grow as connectivity improves.

Europe captured significant percentage of global sales in 2025. The United Kingdom added GBP 1.7 billion (USD 2.15 billion) for projects such as the Lower Thames Crossing, spurring demand for subcontractor compliance automation. Germany and France automate invoicing under national commercial codes, while ISO 19650-4 drives BIM-to-ERP data exchange mandates. In the Middle East, Saudi Arabia and the United Arab Emirates together represented a notable percentage of global Construction ERP market revenue in 2025, with mega-projects that favor platforms embedding Arabic language packs and multicurrency ledgers. South America and Africa remain early-stage, but localized vendors such as EVOP and SYNEco are carving niches with e-invoicing connectors to regional tax portals.

Competitive Landscape

The Construction ERP market is moderately fragmented: the top five suppliers, Procore Technologies, Trimble’s Viewpoint unit, Oracle’s Aconex and Primavera duo, Autodesk Construction Cloud, and CMiC, collectively holding a significant percentage of the share in 2025. Regional firms such as COINS Global, RIB Software, and Buildertrend excel in country-specific payroll and VAT handling. Competitive thrusts revolve around three axes: artificial intelligence, ecosystem integrations, and geographic localization.

Procore’s January 2026 purchase of Datagrid accelerates event-driven data automation, slashing manual reconciliations and anchoring the firm in enterprise accounts.[4]Procore Technologies, “Datagrid Acquisition Announcement,” PROCORE.COM CMiC’s November 2025 launch of NEXUS packs 25 AI agents, illustrating a shift where predictive analytics is now basic hygiene.[5]CMiC, “NEXUS AI Platform Launch,” CMIC.CA

White-space persists in equipment-centric workflows, compliance automation for cross-border bids, and sustainability tracking, the latter motivated by owners who increasingly demand carbon balance sheets on new builds. Smaller challengers are rolling out no-code workflow designers, cutting implementation timelines from a year to under two months and lowering lifetime ownership costs by up to 40%. Standards bodies are steering future roadmaps: ISO/IEC 30186:2025 sets a digital-twin maturity ladder, and vendors implementing it first will gain an edge in public procurements that tie payment milestones to model-based progress verification.

Construction Enterprise Resource Planning Industry Leaders

Procore Technologies, Inc.

Trimble Inc. (Viewpoint Division)

CMiC Global Inc.

Sage Group plc

Buildertrend Solutions, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Bauwise released Tender Management to trim subcontractor procurement cycles by up to 30%.

- February 2026: Aegis Project Controls disclosed a DragonForce ransomware breach exposing schedules and cost data.

- January 2026: Procore acquired Datagrid to embed agentic AI for cross-platform integrations.

- December 2025: Clark Sullivan Construction confirmed a PLAY ransomware attack that halted operations for three days.

Global Construction Enterprise Resource Planning Market Report Scope

The Construction ERP market encompasses specialized software solutions and associated services that manage, integrate, and optimize end-to-end operations across construction and engineering organizations.

The Construction ERP Report is Segmented by Deployment Mode (Cloud-Based, On-Premise, Hybrid), Enterprise Size (Small and Medium Enterprises, Large Enterprises), Solution (Software, Services), End Use (Residential Construction, Commercial Construction, Infrastructure and Civil Engineering, Industrial Construction), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, Africa).

| Cloud-Based |

| On-Premise |

| Hybrid |

| Small and Medium Enterprises |

| Large Enterprises |

| Software |

| Services |

| Residential Construction |

| Commercial Construction |

| Infrastructure and Civil Engineering |

| Industrial Construction |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Deployment Mode | Cloud-Based | |

| On-Premise | ||

| Hybrid | ||

| By Enterprise Size | Small and Medium Enterprises | |

| Large Enterprises | ||

| By Solution | Software | |

| Services | ||

| By End Use | Residential Construction | |

| Commercial Construction | ||

| Infrastructure and Civil Engineering | ||

| Industrial Construction | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What will the Construction ERP market be worth by 2031?

It is forecast to reach USD 7.13 billion by 2031 at an 8.62% CAGR between 2026 and 2031.

Which deployment mode is growing fastest?

Cloud-based solutions are expanding at an 11.20% CAGR, almost 300 basis points ahead of the overall market.

Why are small and medium contractors adopting Construction ERP platforms more quickly?

Subscription pricing, government digitalization grants, and low-code templates shorten payback periods, driving a 10.40% CAGR for SMEs.

Which end-use segment is expected to post the highest growth?

Infrastructure and civil engineering projects are projected to expand at 12.30% CAGR, outpacing commercial, residential, and industrial builds.

How are cybersecurity concerns influencing software selection?

Owners now require SOC 2 Type II, ISO 27001, and zero-trust architectures, favoring vendors with mature security postures and penalizing those without documented controls.

Who are the leading vendors in the Construction ERP space?

Procore Technologies, Trimbles Viewpoint division, Oracle Aconex and Primavera, Autodesk Construction Cloud, and CMiC collectively hold roughly 30%35% share.

Page last updated on: