Connected Health and Wellness Solutions Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 94.24 Billion |

| Market Size (2031) | USD 244.74 Billion |

| Growth Rate (2026 - 2031) | 21.03% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Connected Health and Wellness Solutions Market Analysis by Mordor Intelligence

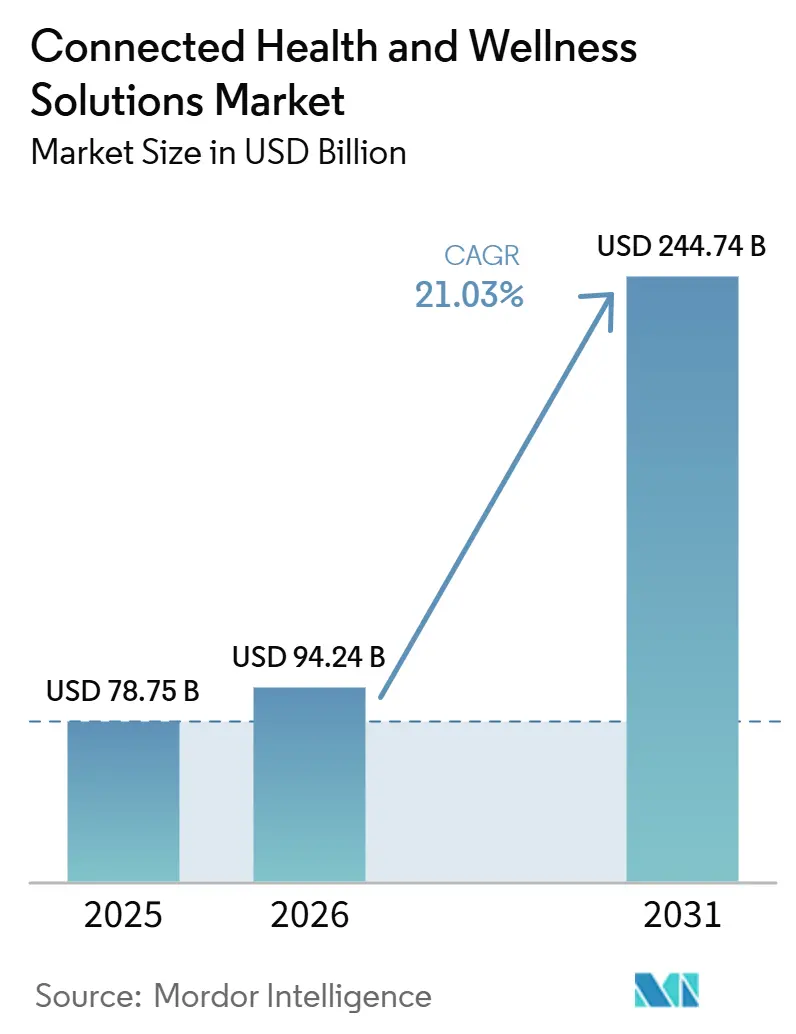

The connected health and wellness solutions market is projected to expand from USD 78.75 billion in 2025, USD 94.24 billion in 2026, and reach USD 244.74 billion by 2031, growing at a CAGR of 21.03% from 2026 to 2031. The growth base remains strong because chronic disease already absorbs 90% of U.S. healthcare spending, and that keeps long term demand for continuous monitoring, remote care, and digital engagement tools elevated. As providers and payers look for ways to shift care away from high-cost acute settings, connected platforms are being used less as optional technology and more as operating infrastructure for ongoing care delivery. The 2026 Medicare Physician Fee Schedule gives telehealth a more durable reimbursement base, which supports broader deployment decisions across the connected health and wellness solutions market. Consumer hardware and clinical monitoring are also moving closer together as FDA-cleared health functions enter mass retail devices, which increases pressure on legacy device distribution models and expands patient familiarity with connected care workflows. Competition remains moderate, but vendors that combine regulated devices, software analytics, and interoperability capabilities are better placed to defend their position in the connected health and wellness solutions market as adoption broadens across care settings.

Key Report Takeaways

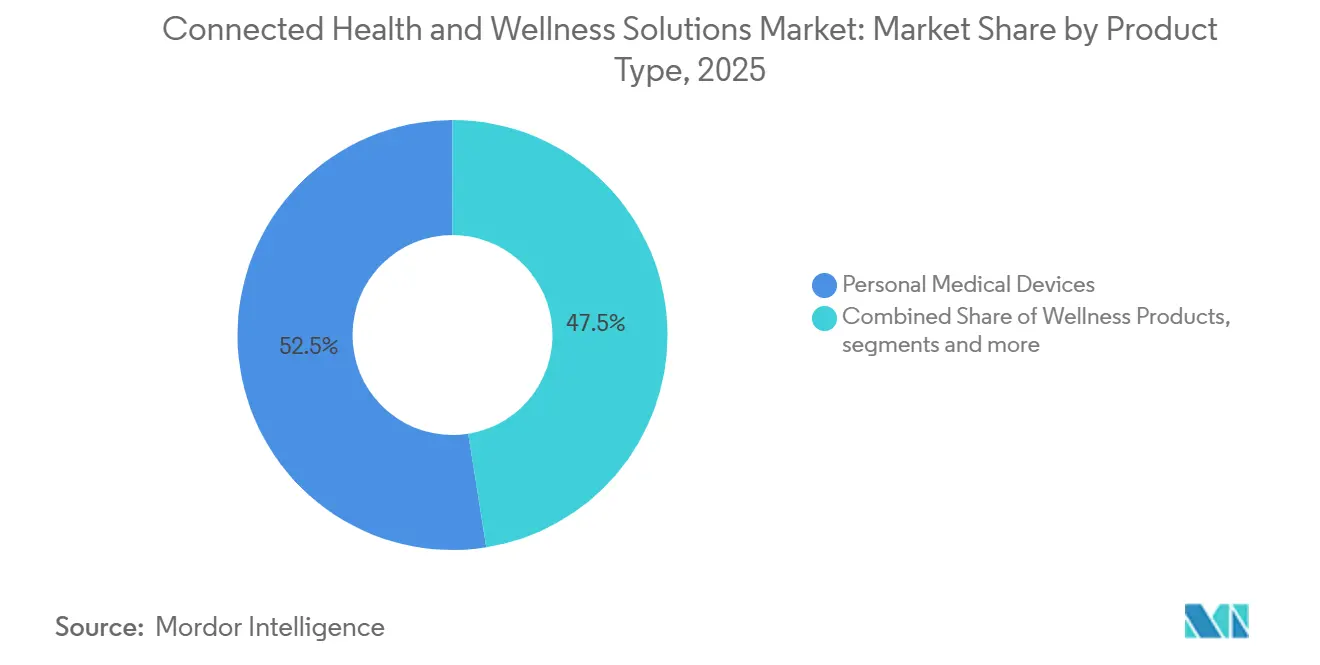

- By product type, personal medical devices led with 52.46% revenue share in 2025, while wellness products are forecasted to expand at a 23.85% CAGR through 2031.

- By function, remote patient monitoring held 48.92% share in 2025, while telehealth is expected to have the highest CAGR at 24.71% through 2031.

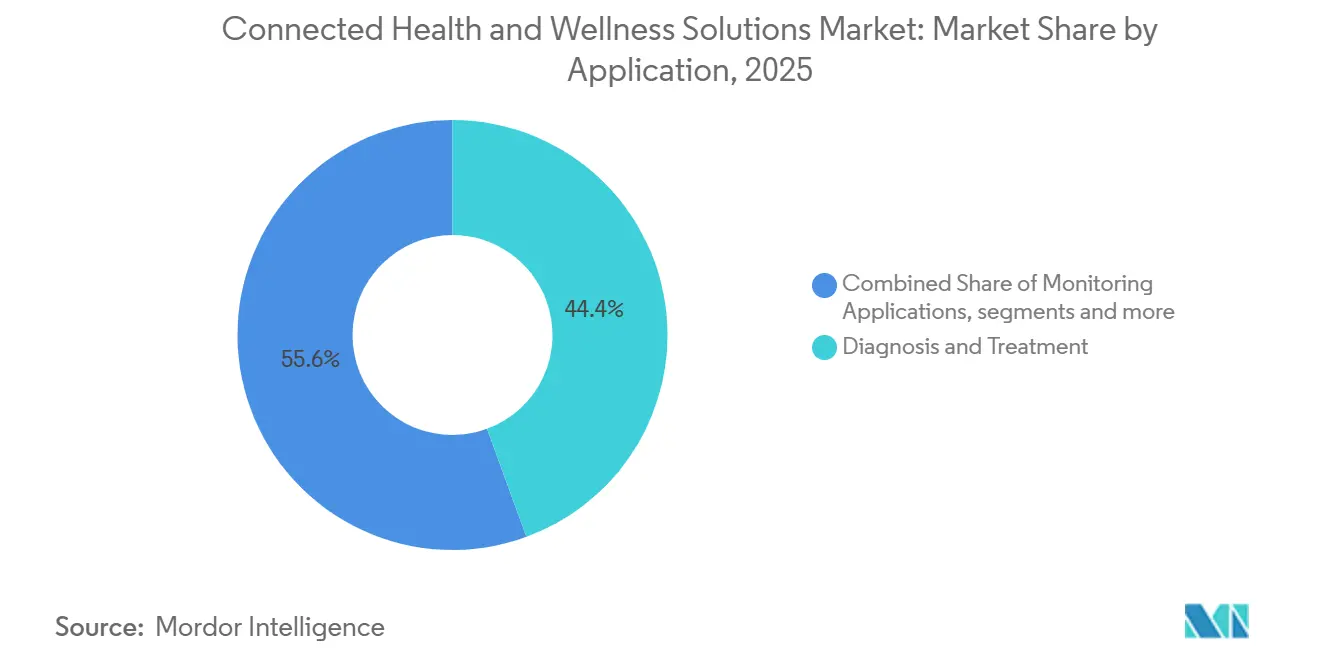

- By application, diagnosis and treatment accounted for 44.37% of revenue in 2025, while monitoring applications are expected to advance at a 25.28% CAGR through 2031.

- By end-user, hospitals and clinics captured 46.18% share in 2025, while homecare settings are forecasted to grow at a 26.12% CAGR through 2031.

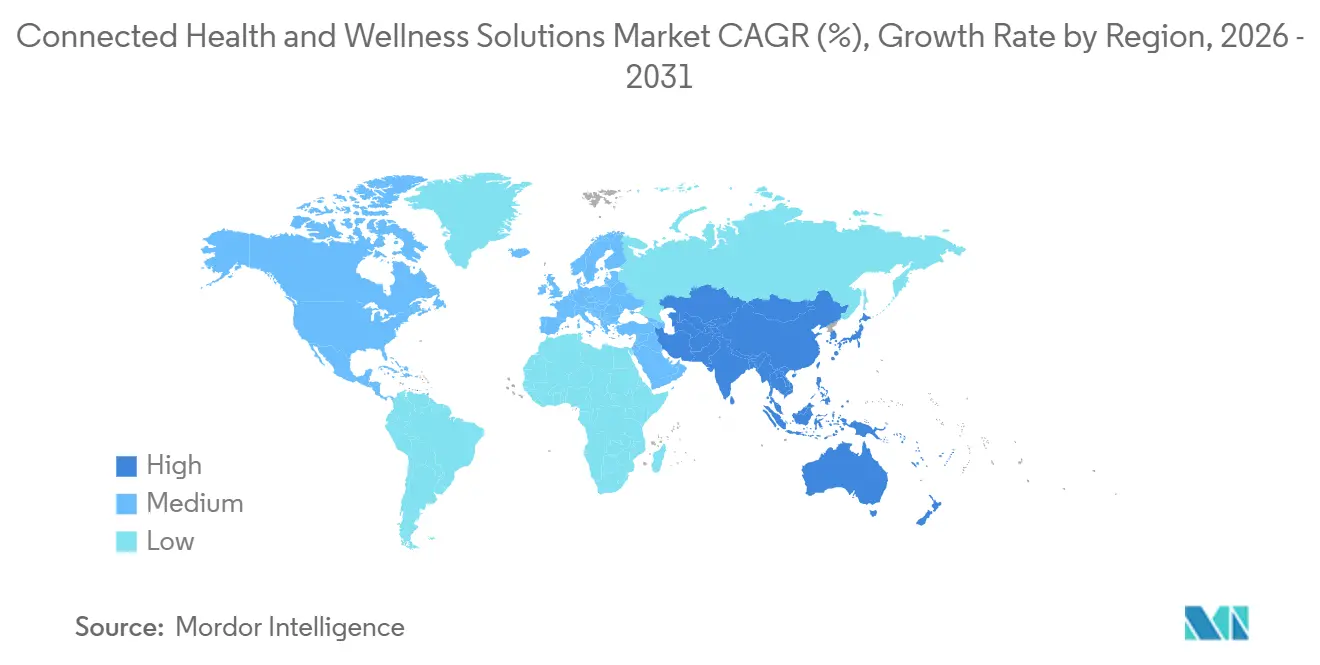

- By geography, North America held 42.84% share in 2025, while the Asia-Pacific is projected to expand at a 27.46% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Connected Health and Wellness Solutions Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Chronic Disease Monitoring Demand | +5.2% | Global | Long term (≥ 4 years) |

| Expansion of Remote Patient Monitoring Reimbursement | +4.1% | North America and EU, expanding to APAC | Medium term (2-4 years) |

| Shift from Episodic Care to Continuous Wellness Management | +3.5% | Global | Medium term (2-4 years) |

| Consumer Adoption of Wearables and Health Apps | +3.2% | North America, APAC, Western Europe | Short term (≤ 2 years) |

| Edge AI and Sensor Miniaturization Improve Clinical Utility | +2.8% | Global, early gains in the U.S., China, and South Korea | Medium term (2-4 years) |

| Interoperable Telehealth and Consumer Tech Ecosystems | +2.4% | North America and EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Chronic Disease Monitoring Demand

The connected health and wellness solutions market is being shaped by a disease burden that is persistent across both mature and developing healthcare systems. Noncommunicable diseases accounted for 74% of global annual mortality, and the WHO reported in 2025 that most countries were still off track on their reduction commitments. In the United States, CDC data published in 2025 showed that 74% of adults reported at least 1 chronic condition in 2023, while 51% reported multiple conditions, which reinforces demand for long-duration monitoring tools across the connected health and wellness solutions market.[1]Centers for Disease Control and Prevention, “Fast Facts, Health and Economic Costs of Chronic Conditions,” CDC, cdc.govA 2026 systematic review in JMIR also pointed back to the CDC finding that chronic disease spending consumes 90% of U.S. healthcare expenditure, which means the cost case for prevention and monitoring remains intact.[2]William David Strain et al., “Wearable Devices for Remote Monitoring of Chronic Diseases, Systematic Review,” JMIR mHealth and uHealth, jmir.org This keeps demand in the connected health and wellness solutions market tied to a structural healthcare need rather than a short-cycle technology purchase, which supports more predictable revenue planning for platform operators.

Shift from Episodic Care to Continuous Wellness Management

The connected health and wellness solutions market is moving with a broader care model shift from reactive visits toward continuous patient management. Traditional visits only capture a short point in time, while connected devices can generate longitudinal data that helps teams identify deterioration earlier and follow patients between encounters. The FDA’s TEMPO pilot, launched in January 2026, shows that regulators now recognize the importance of digital tools that can demonstrate meaningful patient outcomes in routine care.[3].S. Food and Drug Administration, “510(k) Premarket Notification K250507, Hypertension Notification Feature, Apple Inc.,” FDA, accessdata.fda.gov That policy signal favors the connected health and wellness market segments that already combine monitoring, virtual touchpoints, and evidence generation inside a single workflow. It also means that vendors collecting deeper longitudinal datasets can build a stronger position for future regulatory submissions and payer discussions than vendors that only provide isolated device readings.

Consumer Adoption of Wearables and Health Apps

The connected health and wellness solutions market is also benefiting from the way consumer devices are taking on clearer clinical roles. Apple received FDA 510(k) clearance in September 2025 for a hypertension notification feature on Apple Watch Series 11, which shows that large consumer platforms can now place regulated health functions inside mass market hardware. Dexcom also received FDA clearance in April 2025 for the G7 15 Day continuous glucose monitoring system, which expands the practical use case for connected monitoring in everyday disease management. As these products move closer to retail and over the counter access models, the connected health and wellness solutions market gains a wider front door for patient onboarding and recurring engagement. The next phase of growth in the connected health and wellness market will depend less on simple device ownership and more on how well these tools connect with clinical workflows, medication management, and personalized care plans.

Edge AI and Sensor Miniaturization Improve Clinical Utility

The connected health and wellness solutions market is gaining utility as edge AI reduces dependence on uninterrupted cloud connectivity. Local processing allows wearable devices to analyze signals on the device, shorten alert time, and reduce the amount of raw data that must move across networks. HL7 International then launched the Caliper FHIR Accelerator in 2026 to improve exchange standards for medical and personal health device data, which helps turn device output into something more actionable inside healthcare systems. As sensors become smaller and cheaper, the connected health and wellness solutions market will be able to extend monitoring functions into a wider range of devices and everyday settings.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data Privacy, Cybersecurity, and Consent Friction | -1.8% | Global | Short term (≤ 2 years) |

| High Integration Cost with Provider Workflows and Legacy IT | -1.4% | Global, most acute in MEA and South America | Long term (≥ 4 years) |

| Clinical Alert Fatigue and Low Signal to Noise Ratios | -0.9% | North America and EU | Medium term (2-4 years) |

| Uneven Reimbursement and Device Validation Across Markets | -1.2% | North America and EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Data Privacy, Cybersecurity, and Consent Friction

The connected health and wellness solutions market depends on continuous flows of biometric and behavioral data, and that makes trust a core adoption requirement. As more devices collect data outside hospitals and clinics, vendors must manage consent, identity, storage, and sharing expectations across multiple care settings. This slows deployment because providers do not only evaluate clinical performance, they also examine how a platform handles connected sensor data through the full care process. The same issue affects patients because long term adoption is harder when data use terms are unclear or when monitoring feels more intrusive than supportive. In the connected health and wellness solutions market, weak security design can therefore delay contracts, reduce utilization, and increase pressure on vendors to prove end to end governance before scale deployment.

Uneven Reimbursement and Device Validation Across Markets

The connected health and wellness solutions market still faces uneven reimbursement and validation pathways across countries, payer types, and care settings. CMS permanently embedded a simplified telehealth services framework in the 2026 Physician Fee Schedule, but Medicare’s broader telehealth flexibilities are only extended through December 31, 2027, after which many non-behavioral health services will again face geographic restrictions. That timeline is already pushing commercial strategies in the connected health and wellness solutions market toward value-based and employer-sponsored models that can hold up if fee-for-service access narrows. Outside the United States, many APAC and MEA markets still lack standardized reimbursement codes for wearable-generated data, which keeps revenue models more dependent on direct pay, employer benefits, or government programs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Clinical Devices Hold Share as Wellness Hardware Scales Fast

Personal medical devices held 52.46% of connected health and wellness solutions market share in 2025, which kept this category in the lead because clinically validated hardware still moves through reimbursement backed procurement channels with more predictable pricing. This part of the connected health and wellness solutions market includes continuous glucose monitors, ambulatory cardiac monitors, and remote vital sign patches that already fit into established care pathways.

Wellness products are forecasted to grow at a 23.85% CAGR, and the connected health and wellness solutions market size for this segment is rising as sensor costs fall and access widens beyond tightly defined clinical use cases. Software and services still represent a smaller revenue base, but this is where the connected health and wellness solutions industry is building stronger moats as hardware becomes easier to compare across vendors. Providers and payers are placing more value on analytics, decision support, and integration features because those layers shape long term stickiness after the device sale.

By Function: Remote Patient Monitoring Anchors the Market as Telehealth Reshapes Care Delivery

Remote patient monitoring held 48.92% share in 2025, which reflects its established role in discharge protocols, chronic care management, and value-based programs that encourage care at home. The connected health and wellness solutions market has given RPM a strong commercial base because cardiology, pulmonology, and diabetes already have years of clinical validation behind continuous monitoring models. This makes RPM easier for providers to justify in budget cycles because the link to readmission reduction and follow-up adherence is clearer than in newer digital categories. It also keeps RPM closely tied to the parts of healthcare where cost avoidance can be measured more directly.

Telehealth is projected to expand at a 24.71% CAGR, and the connected health and wellness solutions market size tied to virtual care functions should keep rising as billing rules become easier to navigate. Clinical monitoring remains important in institutional settings, but alarm fatigue documented in ICU settings increases the need for better prioritization and signal filtering rather than more alerts alone.

By Application: Diagnosis Leads in Volume as Monitoring Applications Set the Growth Pace

Diagnosis and treatment accounted for 44.37% of revenue in 2025, which kept this application group ahead because cleared diagnostic devices command stronger pricing and reimbursement than broader wellness tools. In the connected health and wellness solutions market, this category benefits from a steady stream of new clinical indications that expand use without requiring an entirely new commercial logic. That kind of launch deepens the addressable patient pool while keeping regulated monitoring at the center of value creation.

Monitoring applications are forecasted to grow at a 25.28% CAGR, and the connected health and wellness solutions market size attached to this group is rising because continuous biometric collection fits population health and chronic care programs more closely than point-in-time testing. Platforms that gather long-duration data also gain an advantage in regulatory and coverage discussions because they can show outcomes over longer periods and across larger patient cohorts. Wellness and prevention and healthcare management remain smaller in current revenue, but they are strategically relevant entry points into employer benefits and cardiometabolic care.

By End User: Institutional Procurement Anchors Revenues as Homecare Grows Fastest

Hospitals and clinics held 46.18% share in 2025, which reflects the concentration of procurement budgets, evidence requirements, and multiyear contracting within acute care institutions. The connected health and wellness solutions market still relies on these settings for revenue leadership because regulated deployment, post-discharge monitoring, and clinical decision support carry higher per-patient value. Institutional buyers also prefer platforms that can show interoperability, security controls, and workflow fit before large rollouts. That combination keeps hospitals and clinics central even as growth gradually broadens into other settings.

Homecare settings are forecasted to expand at a 26.12% CAGR, and the connected health and wellness solutions market size linked to home use is increasing as aging-in-place preferences, workforce shortages, and hospital-at-home models gain more policy and operational support. The case for homecare is stronger when connected monitoring can keep patients out of high-cost settings without reducing follow-up quality or continuity. Ambulatory and specialty care are also expanding with outpatient chronic care trends, while Research and Diagnostics remain important because they help convert connected datasets into evidence that can widen adoption across the connected health and wellness solutions industry.

Geography Analysis

North America held 42.84% of connected health and wellness solutions market share in 2025, which kept the region in front because it combines a high concentration of FDA cleared devices with a more mature telehealth reimbursement base and a faster moving interoperability agenda. The Office of the National Coordinator’s Draft USCDI Version 7, released in January 2026, advances data standardization for wearable and device generated health data, and that will continue shaping platform design choices in the connected health and wellness solutions market. The United States remains the regional anchor because regulatory clarity, payer alignment, and enterprise health IT spending are all stronger than in most other markets.

The connected health and wellness solutions market in Europe is moving on a different path, with reimbursement design and cross border data governance playing a larger role in adoption. Germany’s DiGA framework remains one of the clearest prescription digital health reimbursement models for software led care in the region. The United Kingdom is continuing to use remote patient monitoring more actively in post acute cardiovascular and respiratory pathways as workforce pressure pushes care outside traditional settings. France, Italy, and Spain are still following rather than leading these platform adoption patterns, and investment remains linked to national health IT budget cycles. Across the region, the European Health Data Space and the EU Medical Device Regulation should gradually reduce fragmentation and support wider deployment, while recent device approvals.

Asia-Pacific is forecasted to grow at a 27.46% CAGR, and the connected health and wellness solutions market size in the region is being lifted by strong demographic demand, public digital health investment, and a deep consumer electronics manufacturing base. Government backed infrastructure and broader familiarity with mobile first services create a favorable environment for remote monitoring and virtual care expansion across the connected health and wellness solutions market. The Middle East and Africa and South America remain earlier stage, but GCC countries and Brazil stand out for near term potential even as legacy health IT systems continue to raise integration costs and slow rollout speed.

Competitive Landscape

The connected health and wellness solutions market remains moderately concentrated at the top, with diversified medtech companies, consumer technology firms, and digital health native operators all competing for the same chronic care and monitoring budgets. Competition in the connected health and wellness solutions market is shifting away from pure device specifications and toward ecosystem control, clinician engagement, and workflow integration. Apple’s FDA cleared hypertension notification feature also shows how consumer electronics firms can place clinical style functions into retail products and pressure the traditional medical device route to market.

A clear white space remains in the connected health and wellness solutions market because very few platforms span diagnosis, continuous monitoring, wellness management, and care navigation in a seamless clinical workflow. Hinge Health’s 2025 IPO launch and Omada Health’s 2026 GLP 1 connected care expansion show that digital health focused firms are still targeting employer benefits and population health areas that legacy medtech has not fully addressed. Teladoc’s Q1 2026 results also showed restructuring costs and a continued move from subscription models to visit based arrangements, which reflects the profitability pressure that can emerge when payer pricing changes faster than platform cost structures. This keeps the connected health and wellness solutions market open to share shifts because scale alone does not guarantee durable margins or clinical workflow control.

HL7’s Caliper FHIR Accelerator is important for the connected health and wellness solutions market because it can lower interoperability barriers for smaller vendors while also raising the compliance floor for everyone. Vendors that can show secure data handling, clean integration, and useful evidence generation should have an advantage in institutional procurement. The connected health and wellness solutions market is therefore competitive, but it is not yet locked into a winner take most structure. Market position will keep shifting toward companies that combine regulated hardware, software depth, and day to day care integration more effectively than peers.

Connected Health and Wellness Solutions Industry Leaders

Apple Inc.

Koninklijke Philips N.V.

Medtronic plc

OMRON Corporation

GE HealthCare

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Dexcom presented results from the CONNECT randomized controlled trial at the 2026 ADA Scientific Sessions, demonstrating statistically significant A1C reductions in Type 2 diabetes patients not using insulin. The company simultaneously announced the acquisition of Nutrisense and an early access launch of a reimagined Stelo app, expanding its CGM platform into preventive metabolic health for the first time.

- June 2026: MiniMed announced an expanded agreement with Abbott to develop dual glucose-ketone sensors designed to integrate exclusively with MiniMed smart dosing systems, following Abbott's May 2026 CE Mark for Libre Duo, the world's first dual glucose-ketone continuous sensing technology, and marking a significant extension of the connected diabetes management ecosystem.

- May 2026: Abbott secured CE Mark for Libre Duo and Libre Duo 10 Day, the world's first systems to simultaneously measure glucose and ketone levels every minute, providing real-time visibility into both parameters from a single wearable sensor and opening a new category in continuous metabolic monitoring.

Global Connected Health and Wellness Solutions Market Report Scope

According to the report’s scope, the connected health and wellness solutions market refers to the ecosystem of digital platforms, devices, and services that integrate healthcare delivery with consumer wellness. It covers remote patient monitoring, telehealth, IoT medical devices, digital wellness apps, wearables, and preventive health platforms, enabling continuous, personalized, and data‑driven care across clinical and lifestyle domains.

The connected health and wellness solutions market is segmented into product type, function, application, end-user, and geography. By product type, the market is segmented into personal medical devices, wellness products, and software and services. By function, the market is segmented into remote patient monitoring, clinical monitoring, and telehealth. By application, the market is segmented into diagnosis and treatment, monitoring applications, wellness and prevention, and healthcare management. By end-user, the market is segmented into hospitals and clinics, homecare settings, ambulatory and specialty clinics, and research and diagnostic laboratories. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers values (USD) for all the above segments.

| Personal Medical Devices |

| Wellness Products |

| Software and Services |

| Remote Patient Monitoring |

| Clinical Monitoring |

| Telehealth |

| Diagnosis and Treatment |

| Monitoring Applications |

| Wellness and Prevention |

| Healthcare Management |

| Hospitals and Clinics |

| Homecare Settings |

| Ambulatory and Specialty Clinics |

| Other End-Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Personal Medical Devices | |

| Wellness Products | ||

| Software and Services | ||

| By Function | Remote Patient Monitoring | |

| Clinical Monitoring | ||

| Telehealth | ||

| By Application | Diagnosis and Treatment | |

| Monitoring Applications | ||

| Wellness and Prevention | ||

| Healthcare Management | ||

| By End-User | Hospitals and Clinics | |

| Homecare Settings | ||

| Ambulatory and Specialty Clinics | ||

| Other End-Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the expected value of connected health and wellness solutions by 2031?

The connected health and wellness solutions market is forecasted to reach USD 244.74 billion by 2031, rising from USD 78.75 billion in 2025 to USD 94.24 billion in 2026.

How fast is connected health and wellness solutions expected to grow through 2031?

Market growth is projected at a 21.03% CAGR from 2026 to 2031, supported by chronic disease management demand, telehealth reimbursement support, and wider monitoring use.

Which product category leads current revenue in connected health and wellness solutions?

Personal medical devices led in 2025 with 52.46% share, reflecting the strength of clinically validated hardware in reimbursement-backed procurement.

Which region offers the strongest near-term growth outlook?

Asia-Pacific is the fastest-growing region with a projected 27.46% CAGR through 2031, supported by digital health infrastructure investment and large-scale device manufacturing.

Page last updated on: