Connected Hardhats Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

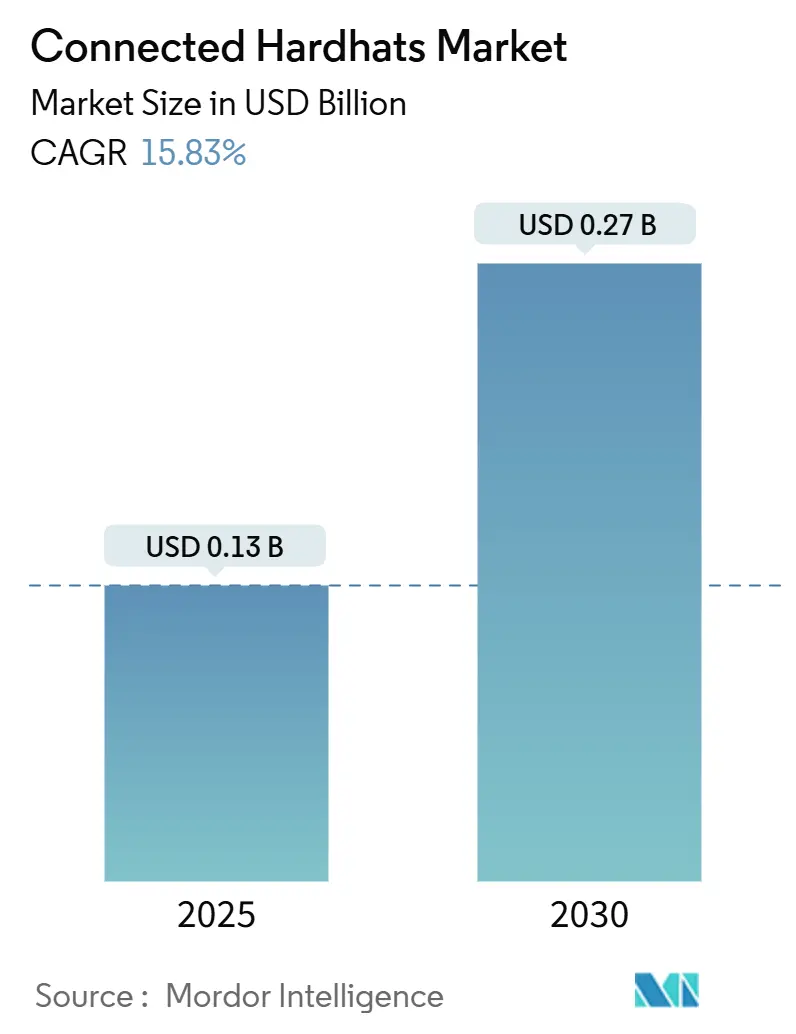

| Market Size (2025) | USD 0.13 Billion |

| Market Size (2030) | USD 0.27 Billion |

| Growth Rate (2025 - 2030) | 15.83% CAGR |

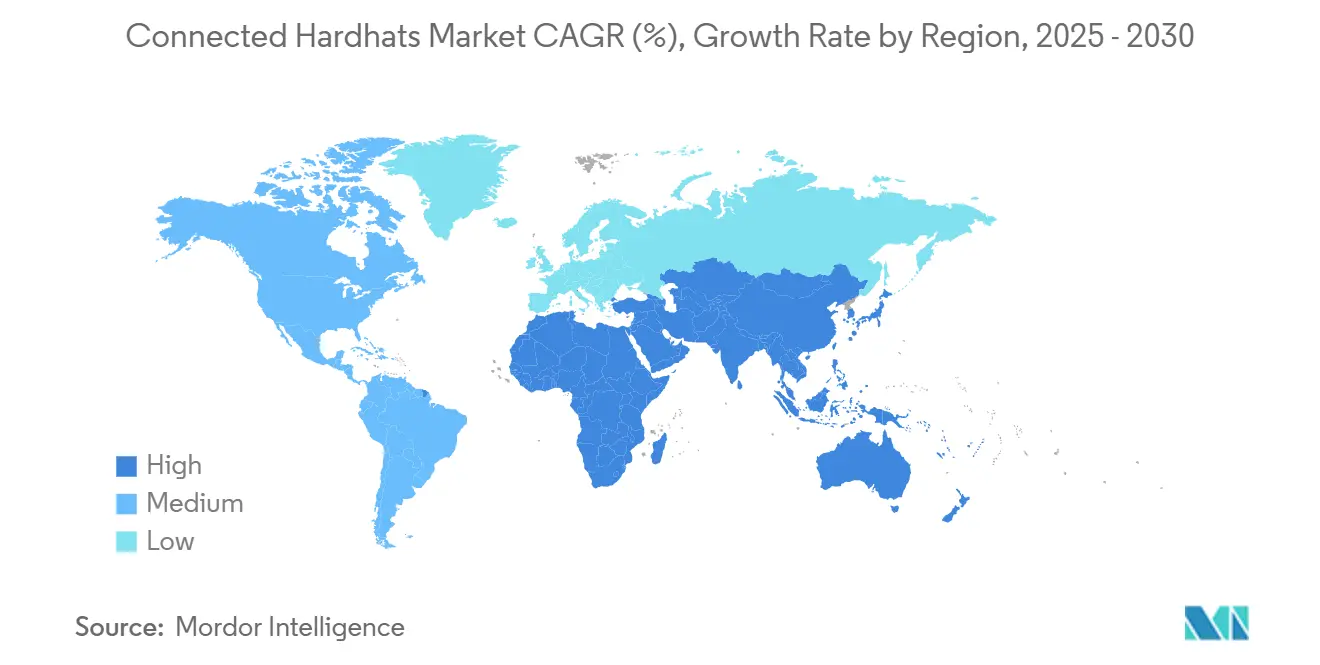

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

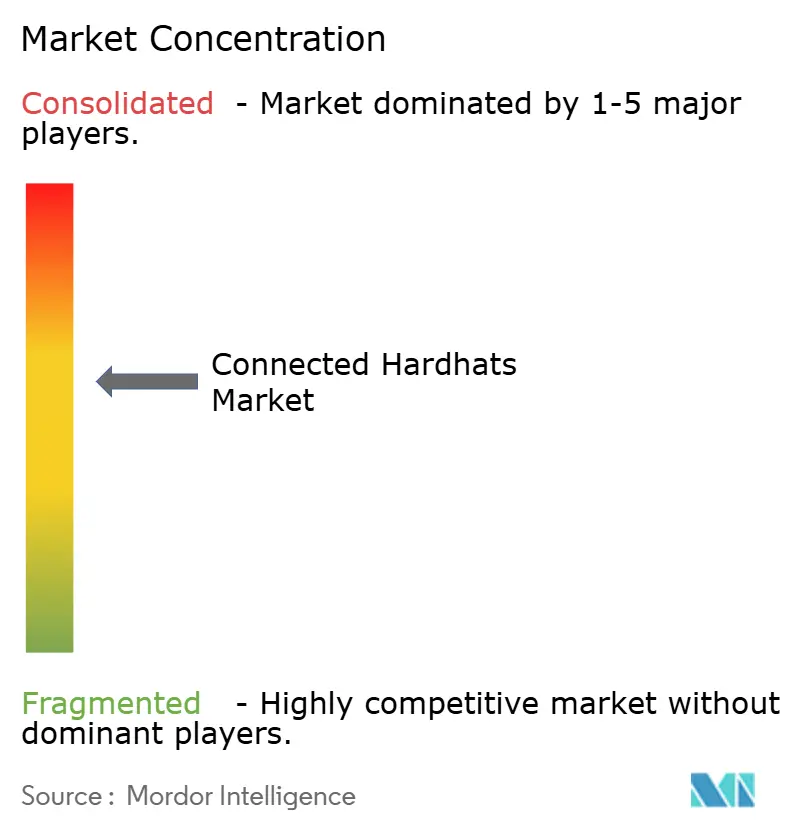

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Connected Hardhats Market Analysis by Mordor Intelligence

The connected hardhats market size is USD 0.13 billion in 2025 and is forecast to reach USD 0.27 billion by 2030, posting a 15.83% CAGR over the 2025-2030 period. This strong growth reflects the rapid convergence between industrial Internet of Things technologies and traditional personal protective equipment, intensifying regulatory pressure for continuous worker monitoring and the wider availability of edge-computing safety solutions. Enterprises are adopting connected hard hats to shorten incident response times, unlock predictive analytics, and secure insurance discounts tied to lower accident rates. Technology suppliers are leveraging declining sensor prices, longer-life batteries, and private 5G networks to introduce feature-rich models that address dynamic industrial hazards. Competitive differentiation is shifting from hardware durability to data-driven services as vendors roll out software-as-a-service platforms that monetize safety insights. At the same time, high upfront costs and cybersecurity concerns continue to delay rollouts at budget-constrained sites.

Key Report Takeaways

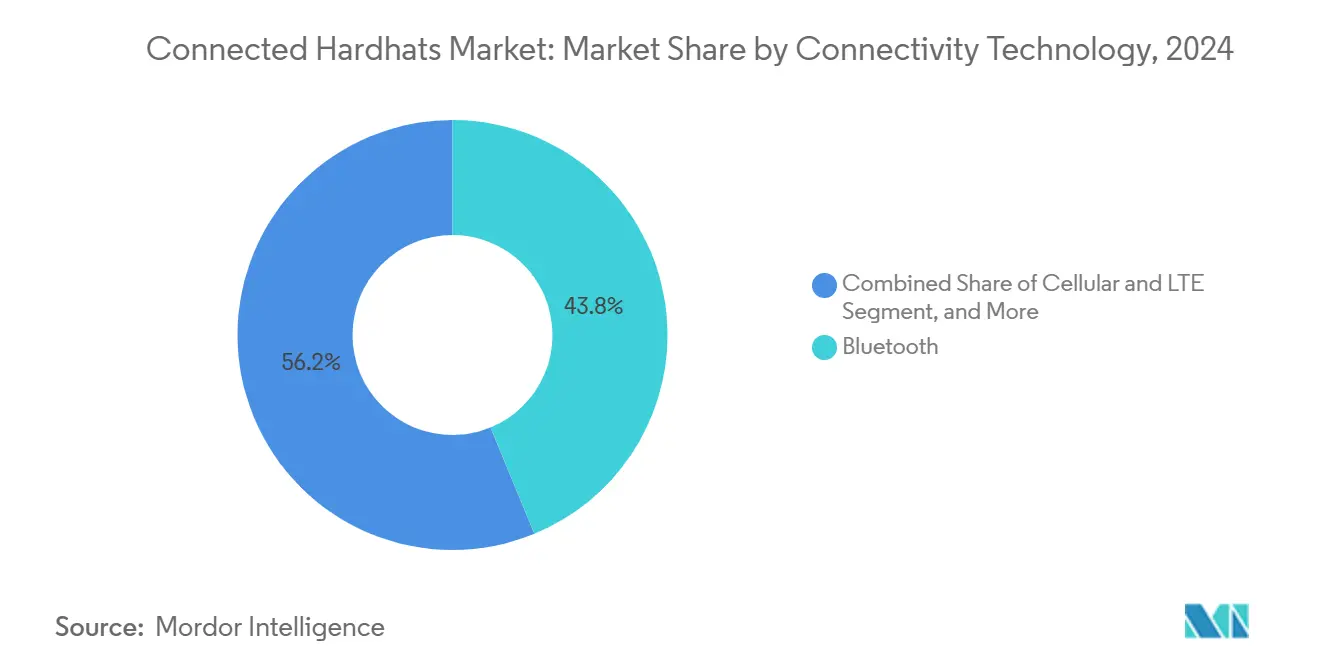

- By connectivity technology, Bluetooth led the connected hardhats market with a 43.78% revenue share in 2024, while cellular and LTE are forecast to expand at a 16.49% CAGR through 2030.

- By material, HDPE commanded a 39.67% market share of the connected hardhats market in 2024; polycarbonate is projected to advance at a 16.37% CAGR through 2030.

- By end-user industry, construction held a 47.91% share of the connected hardhats market size in 2024, and utilities are growing fastest at a 16.58% CAGR through 2030.

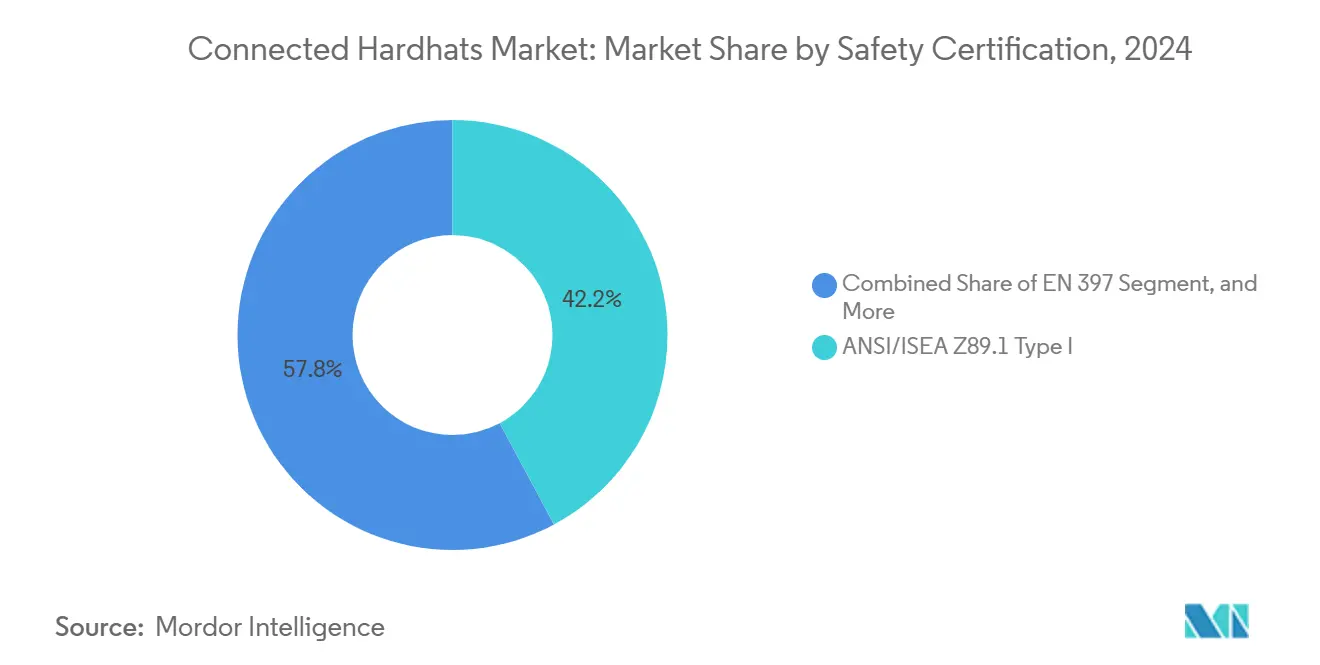

- By safety certification, ANSI/ISEA Z89.1 Type I accounted for 42.17% of the connected hardhats market share in 2024, while EN 397 is expected to increase at a 16.69% CAGR over the forecast period.

- By distribution channel, direct sales captured a 35.84% share of the connected hardhats market size in 2024, and online retail is registering the quickest uptake at a 16.21% CAGR through 2030.

- By geography, North America led with a 35.11% connected hardhats market share in 2024, whereas the Asia Pacific is on track for the fastest growth of 16.44% CAGR through 2030.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Connected Hardhats Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for real-time worker safety monitoring | +3.2% | Global, with early adoption in North America and Europe | Medium term (2-4 years) |

| Integration of IoT and edge-computing capabilities | +2.8% | Global, led by developed markets | Long term (≥ 4 years) |

| Rising occupational safety regulations in high-risk industries | +2.1% | North America and Europe primarily, expanding to Asia Pacific | Short term (≤ 2 years) |

| Expansion of smart construction initiatives globally | +1.9% | Global, with Asia Pacific showing rapid growth | Medium term (2-4 years) |

| Decreasing sensor costs and improved battery efficiency | +1.7% | Global manufacturing impact | Short term (≤ 2 years) |

| Emergence of private 5G networks at industrial sites | +1.4% | North America and Europe initially, spreading globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Real-Time Worker Safety Monitoring

Industrial sites are transitioning from periodic checks to continuous surveillance that identifies gas spikes, temperature fluctuations, or fall events in seconds, resulting in a 15% reduction in fatal incidents at early-adopter facilities in 2024.[1]IEEE, “Edge Computing for Industrial IoT Applications,” IEEE.ORG Continuous telemetry also helps insurers reassess premium structures in favor of companies proving lower claims frequency. Adoption is most pronounced in confined spaces, where atmospheric conditions can change without warning. Continuous monitoring data feeds machine-learning algorithms that flag risk patterns before incidents occur, pushing safety management from compliance toward prevention. Integration with location services further streamlines rescue operations, as supervisors can instantly identify workers in distress.

Integration of IoT and Edge Computing Capabilities

On-device microprocessors now execute safety algorithms locally, cutting latency to sub-millisecond response and eliminating reliance on cloud availability during critical events.[2]European Union, “Personal Protective Equipment Regulation,” EUR-LEX.EUROPA.EU Edge architectures also enable bandwidth-light deployments at remote mines and offshore rigs where backhaul is limited. Vendors combine edge analytics with AI to issue alerts for fatigue or heat stress that extend beyond hazard detection, linking worker wellness to productivity gains. Platform APIs expose deterministic data to enterprise resource planning systems, providing managers with a consolidated view of assets, personnel, and risk trends. Edge processing likewise protects sensitive operational data by limiting what leaves the site.

Rising Occupational Safety Regulations in High-Risk Industries

The European Union’s latest Personal Protective Equipment Regulation requires real-time monitoring in certain hazardous applications, triggering new procurement cycles among oil, gas, and mining operators.[3]Occupational Safety and Health Administration, “Commonly Used Statistics,” OSHA.GOV U.S. authorities emphasize the need for continuous exposure measurement, reinforcing the demand for sensor-enabled helmets and data records that prove compliance. Regulators now audit digital logs to verify that alarms were acknowledged and corrected, making manual forms obsolete. Non-compliance fines add financial pressure, while unions advocate for connected safety to safeguard members in volatile work sites. These mandates compress adoption timelines and reduce purchase hesitancy at regulated firms.

Expansion of Smart Construction Initiatives Globally

Project owners deploy connected hardhats that link to building information modeling systems, reducing recordable injuries by 25% at sensor-equipped sites in 2024. Automated geofencing pauses heavy equipment when workers enter danger zones, preventing costly stoppages and liability claims. Data captured across projects feeds continuous improvement cycles that refine scheduling, training, and sub-contractor safety audits. Technology adoption is highest in Asia Pacific mega-infrastructure projects, where developers value real-time dashboards for multilingual workforces. Insurers discount premiums when validated sensor data replaces subjective site inspections.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High initial procurement and deployment costs | -2.3% | Global, particularly affecting smaller enterprises | Short term (≤ 2 years) |

| Data privacy and cybersecurity concerns | -1.8% | Global, with varying regulatory responses by region | Medium term (2-4 years) |

| Integration complexity with legacy safety management systems | -1.6% | Global, greatest in heavily regulated process industries | Medium term (2-4 years) |

| Lengthy certification cycles in regulated industries | -1.4% | North America and Europe first, extending to Asia Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Initial Procurement and Deployment Costs

Enterprises often spend USD 500–1,200 per helmet, plus infrastructure, training, and recurring software subscriptions, which discourages small firms that operate on slim margins. Budget committees require complex return-on-investment models that weigh savings from fewer incidents against immediate cash outlay. The expense also includes integration with legacy safety databases and wireless upgrades in older facilities. Bulk purchasing pools and equipment leasing are emerging to reduce capital strain, but cost perception remains a hurdle at sites with infrequent incidents.

Data Privacy and Cybersecurity Concerns

Connected hard hats stream location, biometrics, and environmental readings, creating new attack surfaces identified as high priorities in the Industrial Internet Consortium's security framework. Companies fear liability if breaches expose worker health data or reveal production secrets. Workers also resist constant tracking that could be misused for performance monitoring beyond safety. Vendor diversity complicates risk assessments because certification schemes for wearable security are still evolving. Procurement teams now request end-to-end encryption, zero-trust architectures, and independent penetration tests before signing multiyear contracts.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Connectivity Technology: Bluetooth Leadership Faces Cellular Momentum

Bluetooth held 43.78% of the connected hardhats market share in 2024, underscoring its role as the default low-power solution that pairs seamlessly with smartphones. Enterprises favor Bluetooth because it reduces support overhead and works reliably in mesh topologies that keep helmets linked when line-of-sight is lost. Its dominance also stems from backward compatibility with existing mobile device fleets, allowing for rapid scaling across job sites. However, the connected hardhats market is shifting as private cellular networks mature, giving safety managers guaranteed bandwidth and extended range in vast mines or offshore rigs.

Cellular and LTE connectivity is advancing at a 16.49% CAGR through 2030, supported by the roll-out of industrial 5G that delivers sub-5 ms latency and secure, slice-based traffic segregation. Vendors now embed dual radios, allowing helmets to seamlessly transition from Bluetooth indoors to cellular outdoors without service gaps, thereby easing fleet management. Wi-Fi retains a foothold where high-resolution video or augmented-reality overlays demand more throughput, while RFID, Zigbee, and Thread satisfy the niches of proximity alerts and asset tracking. This multiprotocol reality is prompting platform providers to offer unified device orchestration dashboards that lower total cost of ownership.

By Material: HDPE Dominance Meets Polycarbonate Innovation

High-density polyethylene captured 39.67% of the connected hard hats market size in 2024, as it balances impact strength, chemical resistance, and cost. Its moldability allows manufacturers to integrate sensor housings, antennas, and battery channels directly into the shell, eliminating the need for extra fasteners and keeping the weight low for all-day wear. HDPE also maintains its structural integrity after repeated sterilization cycles, as demanded by food and pharmaceutical plants. These attributes preserve its lead even as buyers explore premium alternatives.

Polycarbonate is on track for a 16.37% annual growth rate thanks to its superior optical clarity, which supports visor-based heads-up displays that surface gas alerts or heat-stress warnings. The material’s higher impact rating exceeds energy-sector standards, opening doors to oil, gas, and utility sites that mandate additional drop protection. Fiberglass-reinforced blends are regaining interest where electromagnetic interference is a concern, shielding delicate sensor boards from high-voltage switchgear. Meanwhile, R&D into bio-based polymers aims to meet corporate sustainability targets without sacrificing ANSI impact performance.

By End-User Industry: Construction Leads While Utilities Accelerate

Construction accounted for 47.91% of connected hardhats market size in 2024, reflecting its high accident rates and the rapid digitalization of project management workflows. Contractors integrate helmets with access-control badges to ensure only certified personnel enter active zones, lowering insurance premiums tied to recordable incidents. Real-time location services also improve evacuation drills, reducing muster-point times during fire drills or gas leaks. As building information modeling platforms mature, supervisors overlay hazard zones on live worker maps, elevating situational awareness.

Utilities are expanding at the fastest rate, with a 16.58% CAGR, because aging grids require constant inspection and repair by dispersed field crews. Connected helmets equipped with arc-flash sensors and high-visibility LED strobes help linemen comply with live-line safety standards. Oil and gas operators prefer intrinsically safe models that monitor explosive atmospheres, while miners deploy mesh-networked units underground where GPS signals fail. In manufacturing, fatigue-detection algorithms notify supervisors before repetitive-stress injuries escalate, aligning with wider Industry 4.0 objectives.

By Safety Certification: ANSI Supremacy With European Standard Growth

ANSI/ISEA Z89.1 Type I products accounted for 42.17% of the connected hardhat market share in 2024, due to their long-established presence in North America. The standard’s clear guidance on electrical insulation and impact attenuation simplifies electronic integration tests, accelerating time-to-market. Enterprises appreciate the consistent labeling that streamlines audit paperwork during OSHA site inspections. Dual-rated Type I helmets also meet the requirements of many customers in Latin America, thereby extending their reach beyond the United States and Canada.

EN 397 approvals are growing at a 16.69% CAGR as European buyers demand products that align with stringent worker rights directives. Manufacturers now pursue simultaneous ANSI, CSA, and EN testing to serve multinational accounts with a single global SKU, thereby reducing tooling costs. CSA Z94.1 specifies battery chemistries rated for −30 °C, which is essential for Canadian oil sands and winter construction projects. In Australia and New Zealand, AS/NZS 1801 places an added focus on UV resistance, spurring the development of coatings that extend sensor lifespan under intense sunlight.

By Distribution Channel: Direct Engagement Leads While Online Scales

Direct sales captured 35.84% of the connected hardhat market size in 2024, as complex integrations require vendor engineers to map wireless coverage, install gateways, and train safety staff. Long implementation cycles make direct relationships ideal for tailoring analytics dashboards and meeting cybersecurity checklists. These engagements often culminate in multiyear service contracts that bundle firmware updates and analytics subscriptions, locking in predictable revenue.

Online retail is rising at a 16.21% CAGR as vendors release plug-and-play starter kits that small plants can self-deploy. E-commerce platforms now host configurators that enable buyers to select sensor suites, battery capacities, and connectivity options, thereby reducing procurement time from weeks to days. Industrial distributors remain vital where local inventory and rapid swap services minimize downtime when units fail. Specialist safety resellers carve out niches in hazardous industries, stocking intrinsically safe models and offering on-site recertification to ensure compliance with evolving regulations.

Geography Analysis

North America held a 35.11% connected hardhats market share in 2024, supported by stringent OSHA and Mine Safety and Health Administration enforcement, which drives the adoption of continuous monitoring. Early investment in 5G industrial campuses, combined with strong insurance incentives, further accelerates penetration. Large-scale utilities and oil majors set procurement benchmarks that ripple through their contractor ecosystems, anchoring vendor revenues in the region. Public sector infrastructure upgrades also specify connected PPE, bolstering demand across highways, bridges, and mass-transit projects.

The Asia Pacific is the fastest-growing region, advancing at a 16.44% CAGR, as China, India, and economies in Southeast Asia invest heavily in manufacturing, energy, and transportation. National digital-transformation plans in China reward factories that deploy real-time safety analytics, while Japan and South Korea integrate connected PPE with robotics to maintain global competitiveness. Mega-projects under Belt and Road initiatives require cross-border safety standardization, creating sizable addressable volumes for certified suppliers. Regional distributors partner with international brands to localize language interfaces and comply with various telecom regulations, thereby accelerating speed-to-market.

Europe combines stringent worker-rights legislation with sophisticated automation, resulting in high per-unit functionality and price points. Governments mandate real-time exposure tracking in chemical and tunneling projects, prompting rapid upgrades from passive helmets to sensor-enabled designs. Data-protection laws, such as GDPR, compel vendors to embed privacy-by-design principles, which differentiate European models in terms of encryption strength. Germany’s automotive manufacturing clusters deploy wearable analytics to predict ergonomic injuries, while the United Kingdom funds connected PPE pilots on high-rise construction sites. Eastern European mining sectors follow Western precedents, opening new customer segments.

Competitive Landscape

The connected hardhats market remains moderately fragmented, with the five largest suppliers controlling just over 50% of global revenue, allowing innovative entrants to secure niche positions alongside long-established personal protective equipment brands. Incumbent manufacturers leverage decades-old distribution channels and certification expertise to retrofit flagship shells with sensor suites, while pure-play technology firms differentiate through advanced analytics that convert episodic hardware sales into recurring software income. As a result, competitive advantage is shifting from simple product durability to integrated platforms that blend edge computing, cloud dashboards, and predictive algorithms, providing buyers with a single pane of glass for safety oversight. Hardware reliability still matters, yet procurement teams now rank data-security audits and firmware support commitments as highly as drop-test results, signaling a permanent reordering of vendor selection criteria. This evolution has prompted traditional suppliers to hire software engineers and cyber-risk specialists at a pace not seen in five years.

Recent moves underscore the industry’s pivot to data-centric offerings. In October 2024, MSA Safety committed USD 25 million to expand its Pennsylvania plant, adding laboratories for electromagnetic-compatibility and cybersecurity testing that align with enterprise procurement checklists. Honeywell followed in September 2024 with a cloud-native Industrial Internet of Things (IIoT) platform that links connected hard hats to facility controls, enabling supervisors to adjust work schedules based on live biometric and environmental data. 3M partnered with Microsoft in July 2024 to host safety analytics on Azure, promising faster updates to the artificial-intelligence model and seamless single sign-on for corporate customers. Start-up Guardhat closed a USD 15 million Series B round in August 2024 to accelerate edge-processing research that reduces network dependence at remote sites, widening the innovation gap between agile newcomers and hardware-centric incumbents. These actions illustrate a race to own the software layer that transforms raw sensor data into monetizable insights for insurance underwriting and operational efficiency.

Intellectual property filings corroborate the shift: connected safety patents increased by 45% in 2024, with a focus on battery chemistry, ultra-wideband ranging, and machine vision-based hazard detection. Strategic alliances are multiplying as helmet makers integrate radios from telecom vendors and analytics engines from cloud providers, creating de facto ecosystems that raise switching costs for customers. Supply-chain resilience has also emerged as a differentiator after recent semiconductor shortages, pushing top brands to dual-source critical sensor modules and lithium cells. Overall, the market’s medium concentration score of 5 reflects a balance between entrenched PPE leaders and nimble tech specialists, each using partnerships and intellectual property to defend or expand their foothold.

Connected Hardhats Industry Leaders

MSA Safety Incorporated

Honeywell International Inc.

3M Company

Daqri Inc.

KASK S.p.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Guardhat Inc. rolled out an AI driven safety platform that links its connected hardhats to machine learning models capable of predicting potential on site accidents up to 30 minutes in advance. By comparing real time biometric signals, ambient readings, and worker movement patterns, the system sends automated alerts and recommends immediate preventive steps, shifting safety programs from reactive responses to forward looking risk avoidance.

- August 2025: MSA Safety Incorporated invested USD 40 million to acquire a European IoT sensor maker, adding advanced gas detection features to its connected hardhat line and deepening its reach in the region’s utilities sector. The deal brings proprietary sensor fusion technology that can track several atmospheric hazards at once while remaining certified for use in explosive settings.

- June 2025: Honeywell International Inc. unveiled its latest connected hardhat equipped with built in 5G radios and edge processors, making live video streams and augmented reality support practical during complex field repairs. Designed for oil, gas, and mining operations where on site specialists are scarce, the helmet aims to trim downtime and raise safety standards.

- March 2025: 3M Company formed a broad partnership with top construction management software vendors to feed connected hardhat data straight into project scheduling tools. The integration lets managers adjust tasks in real time based on worker fatigue and environmental factors, setting an industry precedent for embedding safety insights into day to day construction workflows.

Global Connected Hardhats Market Report Scope

| Bluetooth |

| Wi-Fi |

| Cellular and LTE |

| RFID and NFC |

| Zigbee And Thread |

| Other Connectivity Technology |

| High-Density Polyethylene (HDPE) |

| Acrylonitrile Butadiene Styrene (ABS) |

| Polycarbonate |

| Fiberglass |

| Other Material |

| Construction |

| Oil And Gas |

| Mining |

| Manufacturing |

| Utilities |

| Other End User Industry |

| ANSI/ISEA Z89.1 Type I |

| ANSI/ISEA Z89.1 Type II |

| CSA Z94.1 |

| EN 397 |

| AS/NZS 1801 |

| Other Safety Certification |

| Direct Sales |

| Industrial Distributors |

| Online Retail |

| Safety Equipment Specialists |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Connectivity Technology | Bluetooth | ||

| Wi-Fi | |||

| Cellular and LTE | |||

| RFID and NFC | |||

| Zigbee And Thread | |||

| Other Connectivity Technology | |||

| By Material | High-Density Polyethylene (HDPE) | ||

| Acrylonitrile Butadiene Styrene (ABS) | |||

| Polycarbonate | |||

| Fiberglass | |||

| Other Material | |||

| By End User Industry | Construction | ||

| Oil And Gas | |||

| Mining | |||

| Manufacturing | |||

| Utilities | |||

| Other End User Industry | |||

| By Safety Certification | ANSI/ISEA Z89.1 Type I | ||

| ANSI/ISEA Z89.1 Type II | |||

| CSA Z94.1 | |||

| EN 397 | |||

| AS/NZS 1801 | |||

| Other Safety Certification | |||

| By Distribution Channel | Direct Sales | ||

| Industrial Distributors | |||

| Online Retail | |||

| Safety Equipment Specialists | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is the current size of the connected hardhats market?

The connected hardhats market size is USD 0.13 billion in 2025.

How fast is the market expected to grow over 2025-2030?

It is forecast to expand at a 15.83% CAGR, reaching USD 0.27 billion by 2030.

Which connectivity technology leads market adoption?

Bluetooth currently holds the largest 43.78% share due to low power needs and easy smartphone integration.

Which end-user sector adopts connected hardhats the most?

Construction accounts for 47.91% of market revenue, driven by high accident rates and digital project management systems.

Which region is growing quickest?

Asia Pacific is advancing at a 16.44% CAGR thanks to rapid industrialization and supportive digitalization policies.

What is the key restraint to broader deployment?

High initial procurement and deployment costs remain the biggest hurdle, particularly for small and medium-sized enterprises.

Page last updated on: