Congenital Hyperinsulinism Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

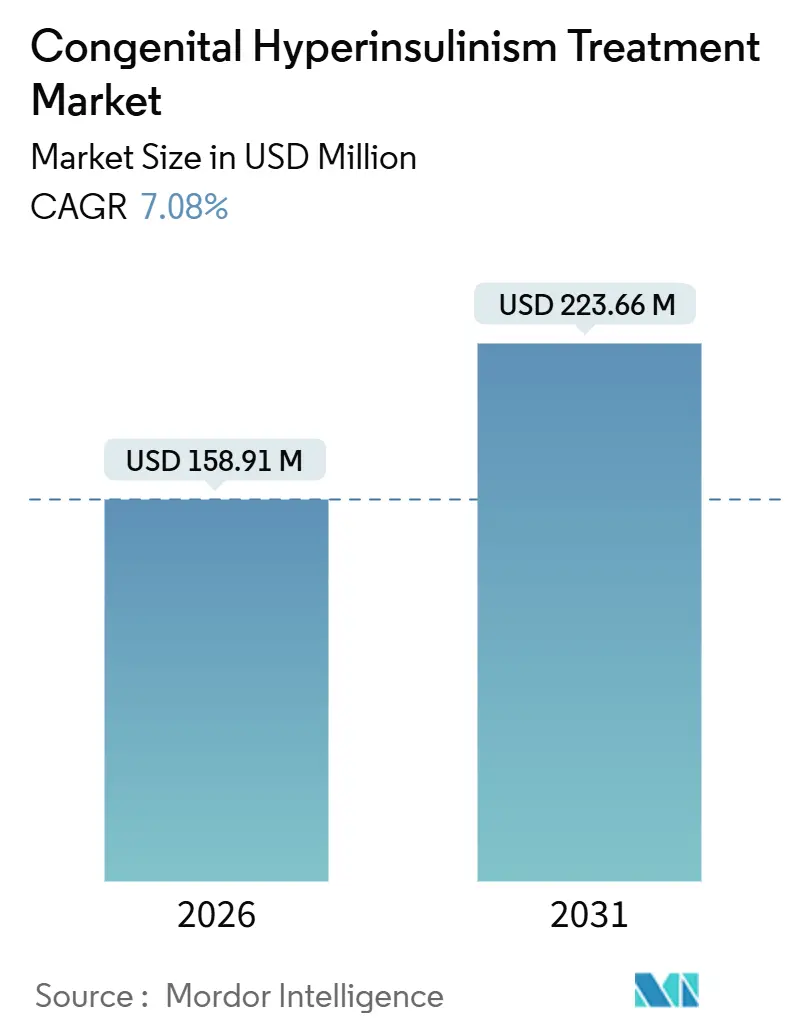

| Market Size (2026) | USD 158.91 Million |

| Market Size (2031) | USD 223.66 Million |

| Growth Rate (2026 - 2031) | 7.08% CAGR |

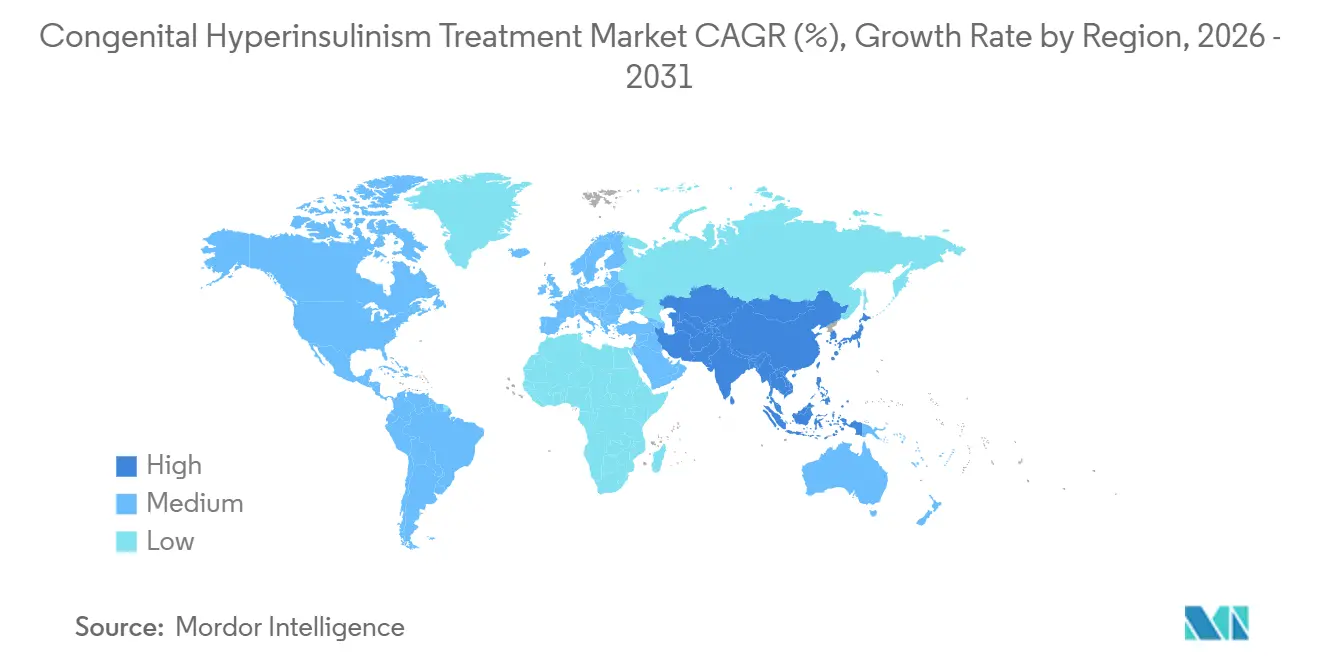

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Congenital Hyperinsulinism Treatment Market Analysis by Mordor Intelligence

The Congenital Hyperinsulinism Treatment Market size is estimated at USD 158.91 million in 2026, and is expected to reach USD 223.66 million by 2031, at a CAGR of 7.08% during the forecast period (2026-2031).

This progression reflects earlier case detection through newborn screening, the maturation of a diversified pipeline that includes β-cell–selective KATP channel openers and long-acting glucagon analogs, and steady improvements in 18F-DOPA PET–guided pancreatectomy that push focal cure rates above 95%. Medication remained the dominant treatment type in 2025, yet surgical intervention is poised for faster growth as imaging precision reduces the need for near-total resections and families pursue definitive focal surgery. Regionally, North America sustained leadership thanks to concentrated surgical expertise and an active investigational-drug environment, while Asia-Pacific emerged as the fastest-expanding territory on the back of newborn screening rollouts and growing access to genetic testing. Competitive intensity is moderate: generic suppliers control first-line pharmacotherapy, several venture-backed firms pursue orphan-drug approvals, and a handful of hospital-based surgical programs act as quasi-providers of last resort, collectively shaping a fragmented yet rapidly evolving competitive landscape for the congenital hyperinsulinism treatment market.

Key Report Takeaways

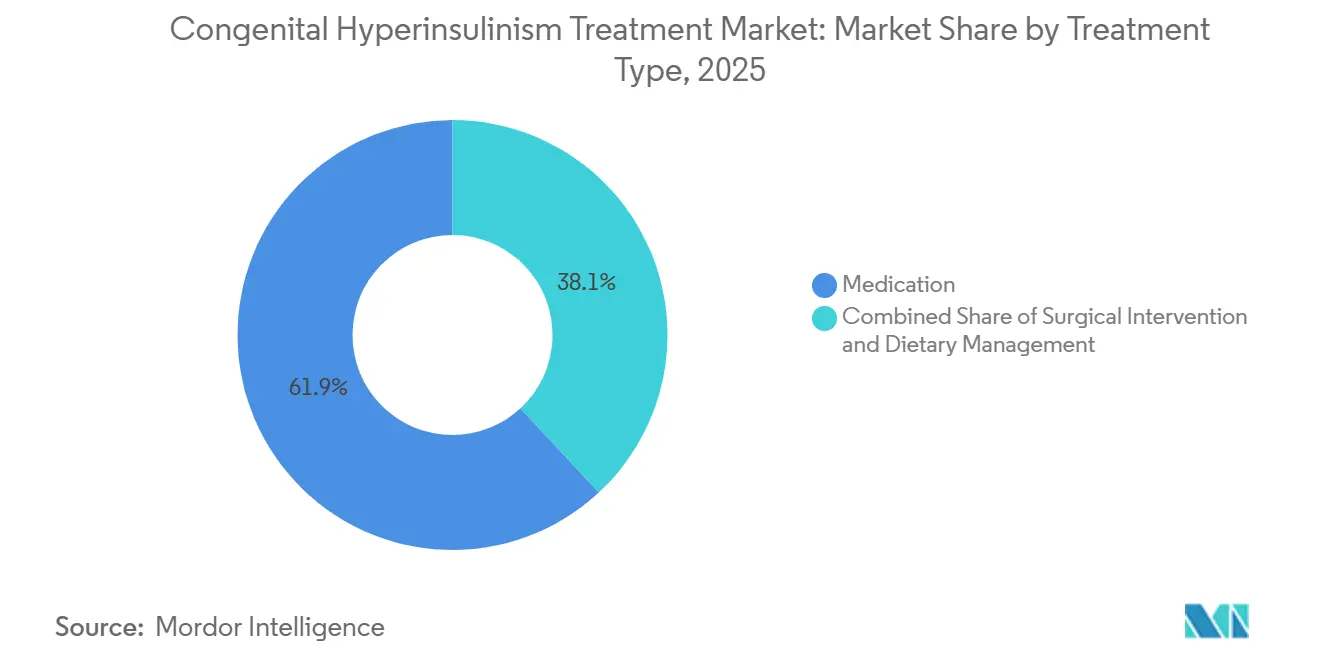

- By treatment type, medication accounted for 61.91% of revenue share in 2025, whereas surgical intervention is expected to grow at an 8.03% CAGR through 2031.

- By disease type, diffuse congenital hyperinsulinism accounted for 71.07% of the congenital hyperinsulinism treatment market share in 2025, while atypical and mosaic forms are forecast to expand at an 8.82% CAGR to 2031.

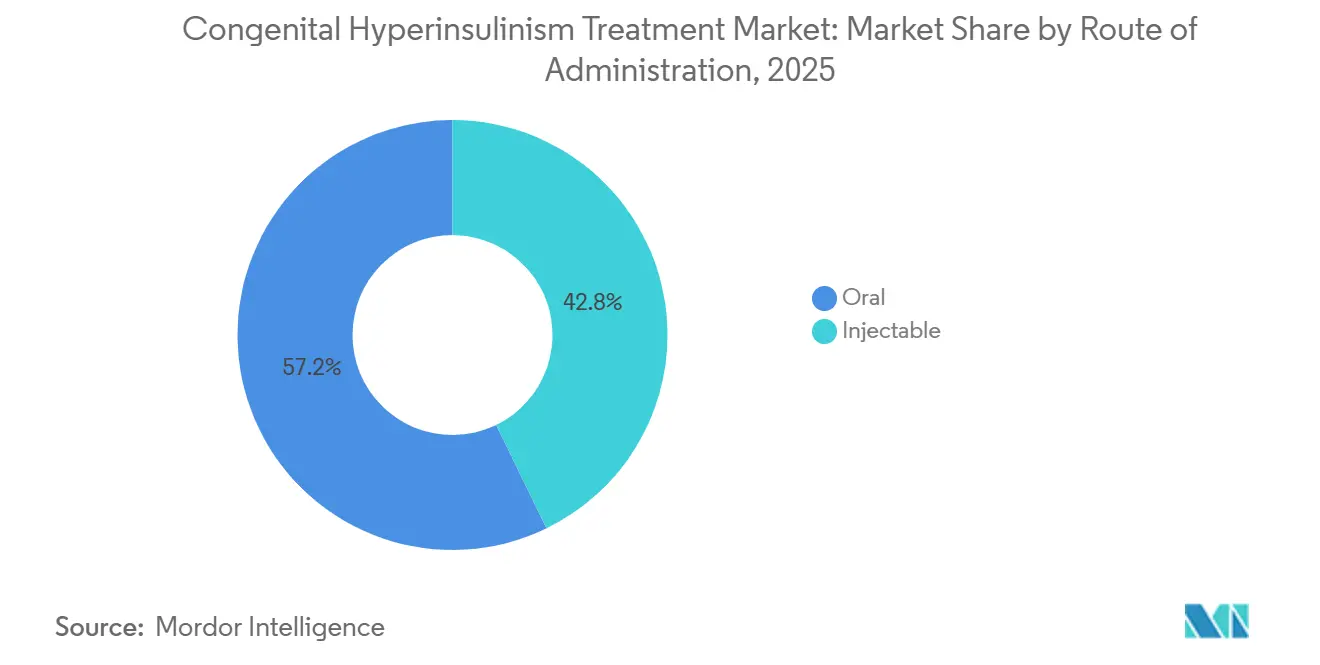

- By route of administration, oral formulations accounted for 57.22% of 2025 sales, and injectables are projected to register a 10.98% CAGR through 2031.

- By end user, hospitals accounted for 48.93% of the 2025 value, while specialty clinics recorded the highest projected CAGR of 9.37% over 2026-2031.

- By geography, North America led with a 41.63% revenue share in 2025, while Asia-Pacific is set to grow at a 11.63% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Congenital Hyperinsulinism Treatment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising diagnosis rates owing to expanded newborn screening panels | +1.8% | Global, early adoption in North America, EU, Japan, South Korea | Medium term (2-4 years) |

| Wider availability of diazoxide and octreotide generics | +1.2% | Global, strongest in India, Brazil, Eastern Europe | Short term (≤ 2 years) |

| Rapid adoption of next-generation genetic tests enabling early intervention | +1.5% | North America, EU, China, India, Japan | Medium term (2-4 years) |

| Growing orphan-drug designations attracting venture funding | +1.0% | North America, EU | Long term (≥ 4 years) |

| Development of long-acting somatostatin analogs tailored to CHI | +0.9% | North America, EU | Long term (≥ 4 years) |

| Pipeline of β-cell–selective KATP channel openers | +1.3% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Diagnosis Rates Owing to Expanded Newborn Screening Panels

Large-scale pilots that combine point-of-care glucose, beta-hydroxybutyrate, and tandem mass spectrometry metabolic markers at 48 hours of life now uncover persistent hypoglycemia before neurologic injury occurs.[1]J.R. Kaiser et al., “Newborn Screening for Congenital Hyperinsulinism Using Glucose and Beta-Hydroxybutyrate,” Journal of Clinical Endocrinology & Metabolism, academic.oup.com North American programs modeled on the Kaiser Permanente protocol are surfacing milder phenotypes that once escaped detection, increasing the diagnosed-prevalence pool feeding the congenital hyperinsulinism treatment market. Japan and South Korea deploy mass spectrometry panels, while tier-1 Chinese hospitals have integrated bedside glucose screens in maternity wards. Early identification channels infants toward timely diazoxide initiation, an intervention that costs a fraction of neurodevelopmental rehabilitation, strengthening payer support for universal screening. As adoption scales beyond high-income economies, medication volumes expand because newly diagnosed neonates that previously received only frequent feeding now enter pharmacotherapy earlier.

Wider Availability of Diazoxide and Octreotide Generics, Driving First-Line Use

Since 2020, multiple Indian and Brazilian manufacturers have introduced low-priced diazoxide and octreotide, undercutting originator brands by 60-70% and eliminating intermittent back-orders reported as recently as 2023.[2]American Society of Health-System Pharmacists, “Drug Shortages Statistics,” ASHP.org Broader availability permits tertiary hospitals in price-sensitive regions to stock first-line agents, reducing the historical reliance on expedited surgical referral for diffuse disease. The democratization of access is particularly salient in Latin America and sub-Saharan Africa, where earlier uptake was cost-constrained. Nevertheless, diazoxide’s hypertrichosis and edema prompt discontinuation in 15-20% of pediatric cases, sustaining appetite for better-tolerated second-line injectables and pipeline entrants, thereby diversifying revenue sources in the congenital hyperinsulinism treatment market.

Rapid Adoption of Next-Generation Genetic Tests Enabling Early Intervention

Turnaround times for six-gene next-generation sequencing panels now sit at under two weeks at many academic laboratories, and single-patient pricing has dropped below USD 1,500.[3]American College of Medical Genetics and Genomics, “Genetic Testing Standards and Guidelines,” ACMG.net Confirming biallelic ABCC8 or KCNJ11 mutations within days rules out diazoxide responsiveness, fast-tracking candidates to 18F-DOPA PET and potential focal surgery. Deep-coverage sequencing additionally detects somatic variants that classic Sanger approaches miss, fueling an 8.82% CAGR for atypical or mosaic case identification. Enhanced molecular precision reduces unnecessary near-total pancreatectomies, limits long-term diabetes risk, and channels payers toward reimbursing high-cost imaging, all of which bolster procedural and pharmaceutical revenues across the congenital hyperinsulinism treatment market.

Development of Long-Acting Somatostatin Analogs Tailored to CHI

Immediate-release octreotide demands 3-4 daily injections, creating adherence challenges for caregivers who already administer frequent feeds and glucose checks. Recordati is advancing a once-weekly pediatric depot that aims to maintain steady octreotide levels in infants weighing under 10 kg, an engineering hurdle given accelerated clearance in neonates. If pharmacokinetic hurdles are resolved, long-acting formulations could accelerate injectable uptake beyond the current 10.98% CAGR forecast, particularly among families discontinuing diazoxide for cosmetic or cardiorespiratory side effects. Longer dosing intervals would also enable specialty clinics to shift octreotide titration from inpatient to outpatient settings, broadening ambulatory throughput and expanding the congenital hyperinsulinism treatment market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited number of surgical centers of excellence worldwide | -1.1% | Most acute in Asia-Pacific, Middle East & Africa, Latin America | Long term (≥ 4 years) |

| Adverse-event profile and periodic shortages of diazoxide API | -0.7% | Global, API sourcing concentrated in China and India | Short term (≤ 2 years) |

| High cost and complexity of near-total pancreatectomy | -0.5% | Markets with limited pediatric surgical infrastructure | Medium term (2-4 years) |

| Regulatory ambiguity around compassionate-use access to investigational drugs | -0.4% | North America, EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Limited Number of Surgical Centers of Excellence Worldwide

Fewer than 20 institutions possess the integrated endocrinology, nuclear medicine, and pediatric surgery capabilities required for safe focal pancreatectomy, with the Children’s Hospital of Philadelphia alone having performed more than 635 procedures and reporting a 97% focal cure rate. Families in India, Brazil, or Nigeria often face prohibitive travel costs or must accept near-total pancreatectomy at local centers with limited case volumes, elevating complication rates and diabetes risk. Although a multicenter U.S. trial launched in 2024 aims to decentralize 18F-DOPA PET protocols, workforce development for pediatric pancreatic surgery remains a decade-long endeavor. Until regional centers reach critical mass, surgical growth lags behind medical therapy, capping the total achievable market size for congenital hyperinsulinism treatment through curative intervention.

Adverse-Event Profile and Periodic Shortages of Diazoxide API

Diazoxide cessation because of hypertrichosis, fluid retention, or rare pulmonary hypertension affects up to one in five treated neonates. Supply chains are fragile: a single API plant in Gujarat and another in Jiangsu Province collectively meet the bulk of global demand, and FDA inspection findings in 2024 forced temporary capacity curtailment. Even short disruptions leave hospitals scrambling for octreotide or emergency surgical referral, unsettling standard-of-care algorithms. Persistent perceptions of risk around both safety and supply temper formulary confidence and narrow diazoxide’s competitive moat in the congenital hyperinsulinism treatment market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Treatment Type: Medication Leads, Surgery Gains Ground

Medication captured 61.91% of the 2025 value, reflecting the widespread availability of generic diazoxide suspensions and octreotide ampoules stocked in tertiary pediatric centers. This dominance positions pharmacotherapy as the economic backbone of the congenital hyperinsulinism treatment market. Surgery, however, is slated for an 8.03% CAGR through 2031 as 18F-DOPA PET raises pre-operative localization sensitivity above 90%, enabling focal resection that eliminates lifelong drug costs in responsive patients.

Beyond 2026, injectables such as long-acting somatostatin analogs and investigational monoclonal antibodies are expected to erode diazoxide’s unit volumes, yet absolute drug spending should still climb because biologics command premium pricing. Near-total pancreatectomy remains a last-resort option given a 90% post-operative diabetes incidence by adolescence, but focal cure success stories resonate with caregivers. Dietary management, consisting of staggered feeds and cornstarch supplementation, provides an adjunct, not curative, modality, leaving the congenital hyperinsulinism treatment market highly reliant on ongoing innovation in both the pharmacologic and surgical arenas.

By Disease Type: Diffuse Dominates, Atypical Momentum Builds

Diffuse disease accounted for 71.07% of 2025 cases, anchoring the current congenital hyperinsulinism treatment market share thanks to its correlation with biallelic KATP mutations that resist diazoxide and demand chronic octreotide or eventual near-total pancreatectomy. Focal CHI remains surgically curable but accounts for only a minority of cases, while atypical and mosaic phenotypes are growing at an 8.82% CAGR because deeper sequencing detects somatic variants previously invisible to Sanger panels.

Growth in atypical diagnoses is clinically significant: some mosaic lesions respond to limited resection, others behave like diffuse disease but at lower insulin-secretion intensity, mandating bespoke management. For payers, variable resource use from short-focal surgery to multi-year octreotide complicates budgeting but also expands opportunities for tailored therapeutics in the congenital hyperinsulinism treatment market. Molecular stratification is therefore shifting R&D pipelines toward genotype-specific agents and diagnostic-linked reimbursement packages.

By Route of Administration: Oral Convenience Confronts Injectable Innovation

Oral formulations held 57.22% of 2025 revenues, a position underpinned by diazoxide’s twice-daily dosing and the simplicity of spoon-fed suspensions in home settings. Injectables are projected to grow at a 10.98% CAGR, driven by octreotide’s entrenched second-line status and emerging subcutaneous or pump-delivered analogs such as dasiglucagon that aim to provide glucose-responsive dosing.

Adoption dynamics rest on caregiver burden versus glycemic reliability. Oral therapies are suitable for outpatient management but face efficacy limitations and cosmetic side effects. Injectables offer potent, predictable control yet demand needle proficiency or pump maintenance. Longer-acting depots under development promise to mitigate injection frequency, potentially shifting the congenital hyperinsulinism treatment market size balance toward injectables by the late forecast window.

By End User: Hospitals Anchor Acute Care, Specialty Clinics Scale Follow-Up

Hospitals accounted for 48.93% of the 2025 spend, justified by intensive care requirements during diagnostic stabilization, when neonates may need continuous intravenous glucose and hourly monitoring. Specialty clinics, forecast to post a 9.37% CAGR, capitalize on the maturation of outpatient octreotide titration protocols, telemedicine follow-up, and integrated genetic counseling that collectively shorten inpatient stays.

As remote continuous glucose monitoring gains regulatory traction, home care adoption is rising among families managing mild phenotypes or post-operative follow-through. Device accuracy improvements and payer coverage for CGM supplies are critical catalysts. Collectively, this shift from hospital to ambulatory care reallocates service-mix revenue yet enlarges the overall congenital hyperinsulinism treatment market by enhancing access and compliance.

Geography Analysis

North America generated 41.63% of 2025 revenue, supported by a dense cluster of surgical centers and the FDA’s expedited-review ecosystem that pulled multiple CHI assets into Phase 3 between 2024 and 2026. The Children’s Hospital of Philadelphia’s cumulative total of 635 pancreatectomies serves as a magnet for cross-border referrals, reinforcing U.S. dominance. Canada contributes via Toronto’s Hospital for Sick Children, but lower birth volumes moderate absolute spending. Mexico has improved diagnosis rates through the National Institute of Pediatrics outreach, yet reimbursement gaps persist outside private insurance.

Asia-Pacific is the fastest-growing region, with a 11.63% CAGR to 2031. China’s National Health Commission initiated tier-1 hospital glucose screening in 2024, and Shenzhen-based BGI now markets a six-gene CHI panel at sub-USD 800, slicing genetic-testing barriers. India’s Newborn Screening Initiative enrolled 160,000 infants across nine states in 2025, doubling CHI case confirmations year-on-year. Japan and South Korea offer mature genetic infrastructure but fewer surgical centers, so medical management retains a higher relative share. Australia enjoys comprehensive coverage through the National Disability Insurance Scheme, underpinning stable but modest market expansion relative to population size.

Europe remains a mature yet innovative ecosystem. Germany, France, and the United Kingdom participate in the European Reference Network for rare endocrine disorders, which harmonizes protocols and accelerates data sharing. Recordati leverages EU-wide orphan-drug exclusivity to sustain octreotide revenues, while University College London’s Great Ormond Street Hospital leads continental 18F-DOPA PET volumes. Growth is steady but slower because screening and genetics were already widely adopted by 2025.

South America and the Middle East & Africa trail in both diagnosis and therapy adoption. Brazil spearheads regional progress: São Paulo’s Instituto da Criança implemented continuous glucose monitoring in public hospitals in 2025, and a partnership with Hyperion ensures uninterrupted diazoxide supply. The Gulf Cooperation Council invests in pediatric endocrine clinics in Dubai and Riyadh, while sub-Saharan Africa relies on medical tourism and charitable supply programs. Persistent gaps in imaging, surgical training, and drug reimbursement temper growth but also represent latent demand for the congenital hyperinsulinism treatment market.

Competitive Landscape

The congenital hyperinsulinism treatment market is moderately fragmented, with no clear market leader. Recordati Rare Diseases commands immediate-release octreotide across most of Europe under orphan-drug protections and invests in a pediatric-friendly depot formulation slated for mid-phase trials by 2027. Hyperion Therapeutics controls the North American diazoxide supply after acquiring intellectual property rights in 2020, but margin pressure from low-cost Asian generics narrows its strategic flexibility.

On the investigational front, Rezolute secured FDA breakthrough designation for monoclonal antibody RZ358 and raised USD 15 million in 2024 to complete the Phase 3 RIZE program, targeting a 2026 biologics license application filing. Amylyx Pharmaceutical’s 2024 acquisition of avexitide for USD 35.1 million underscores confidence in GLP-1 receptor antagonism as a differentiated mechanism. Zealand Pharma, in partnership with DEKA Research, continues to refine a wearable dasiglucagon pump; contract-manufacturing setbacks triggered two complete-response letters in 2024, pushing commercial timelines beyond 202.

Surgical expertise functions as an oligopolistic “provider” segment: five U.S. programs, two European centers, and single nodes in Japan and Australia perform the bulk of focal resections. Their open-source dissemination of standardized protocols has begun to diffuse know-how, but capacity expansion is slow. Device makers such as Dexcom and Medtronic pursue sensor-accuracy claims in neonatal hypoglycemia, but interoperability with pediatric pumps remains a work in progress.

Emerging white space spans three vectors: gene therapy aimed at ABCC8, β-cell–selective KATP openers without cardiovascular off-target effects, and closed-loop bihormonal pumps. Each faces formidable scientific and regulatory hurdles, yet orphan-drug economics and modest clinical-trial sizes continue to attract venture capital, sustaining a pipeline that could reshape the congenital hyperinsulinism treatment market over the long term.

Congenital Hyperinsulinism Treatment Industry Leaders

Boston Scientific Corporation

Johnson & Johnson

Rezolute Inc.

Eli Lilly and Company

Novartis AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Rezolute released topline Phase 3 sunRIZE results showing that ersodetug achieved statistically significant reductions in intravenous glucose infusion rates in patients with congenital hyperinsulinism.

- July 2024: Amylyx Pharmaceuticals acquired avexitide, a GLP-1 receptor antagonist with FDA breakthrough designation, from Eiger BioPharmaceuticals for USD 35.1 million and announced plans for a Phase 3 trial in Q1 2025.

Global Congenital Hyperinsulinism Treatment Market Report Scope

The Congenital Hyperinsulinism (CHI) Treatment Market is defined as the global healthcare segment focused on therapies, diagnostics, and management solutions for congenital hyperinsulinism, a rare genetic disorder characterized by excessive insulin secretion that leads to recurrent hypoglycemia. It includes pharmaceutical drugs, surgical interventions, dietary management, and emerging gene therapies.

The Congenital Hyperinsulinism Treatment Market Report is Segmented by Treatment Type (Medication, Surgical Intervention, Dietary Management), Disease Type (Diffuse CHI, Focal CHI, Atypical/Mosaic Forms), Route of Administration (Oral, Injectable), End User (Hospitals, Specialty Clinics, Homecare Settings), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, South America). Market Forecasts are Provided in Terms of Value (USD).

| Medication | Diazoxide |

| Octreotide | |

| Other Somatostatin Analogues | |

| Investigational KATP Channel Openers | |

| Surgical Intervention | Focal Pancreatectomy |

| Near-total Pancreatectomy | |

| Dietary Management |

| Diffuse CHI |

| Focal CHI |

| Atypical / Mosaic Forms |

| Oral |

| Injectable |

| Hospitals |

| Specialty Clinics |

| Homecare Settings |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Treatment Type | Medication | Diazoxide |

| Octreotide | ||

| Other Somatostatin Analogues | ||

| Investigational KATP Channel Openers | ||

| Surgical Intervention | Focal Pancreatectomy | |

| Near-total Pancreatectomy | ||

| Dietary Management | ||

| By Disease Type | Diffuse CHI | |

| Focal CHI | ||

| Atypical / Mosaic Forms | ||

| By Route of Administration | Oral | |

| Injectable | ||

| By End User | Hospitals | |

| Specialty Clinics | ||

| Homecare Settings | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the congenital hyperinsulinism treatment market?

The congenital hyperinsulinism treatment market size stood at USD 158.91 million in 2026 and is projected to reach USD 223.66 million by 2031.

Which treatment type is growing fastest?

Surgical intervention is forecast to lead growth with an 8.03% CAGR through 2031, supported by expanding 18F-DOPA PET imaging and high focal cure rates.

Which region offers the highest growth potential?

Asia-Pacific shows the highest growth, with a 11.63% CAGR, driven by the expansion of newborn screening and broader access to genetic testing.

How do generics influence overall treatment costs?

Increased availability of generic diazoxide and octreotide has cut acquisition costs by up to 70%, enabling broader first-line pharmacotherapy, especially in price-sensitive markets.

Are long-acting somatostatin analogs expected soon?

Recordati is developing a pediatric depot formulation that could reduce injection frequency to once weekly, with mid-phase trials anticipated around 2027.

Page last updated on: