Confectionery Packaging Machine Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 5.18 Billion |

| Market Size (2030) | USD 6.72 Billion |

| Growth Rate (2025 - 2030) | 5.33% CAGR |

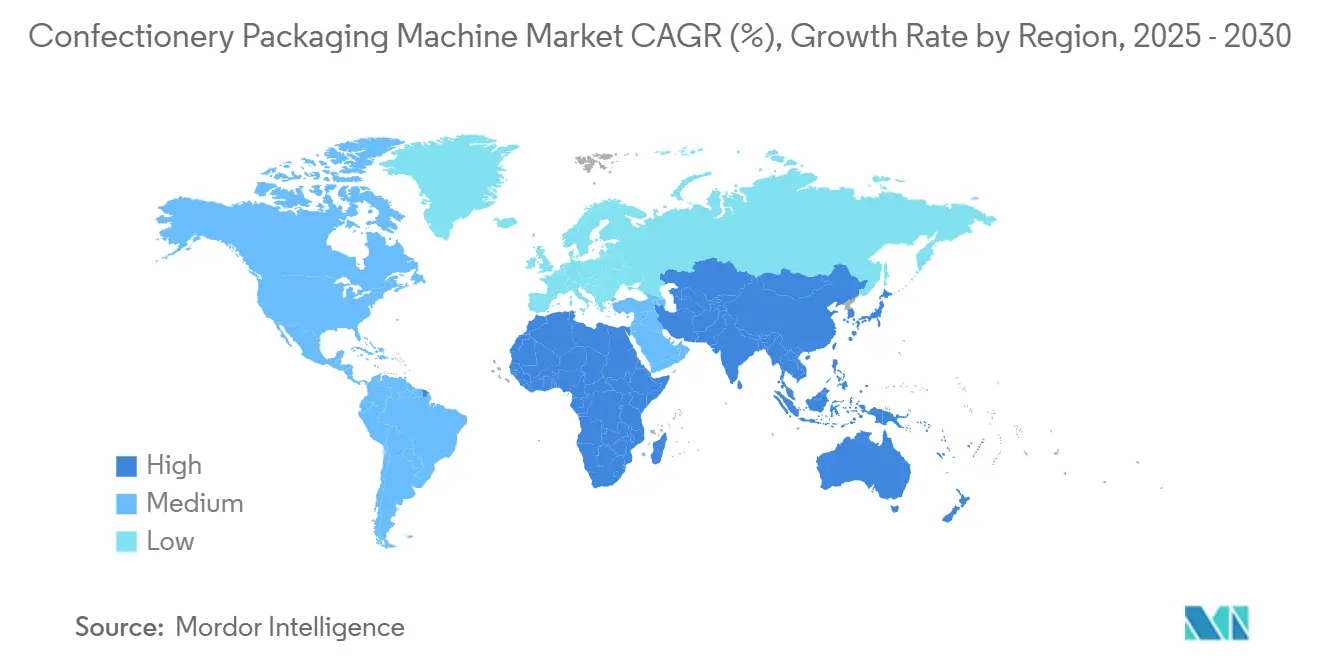

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Confectionery Packaging Machine Market Analysis by Mordor Intelligence

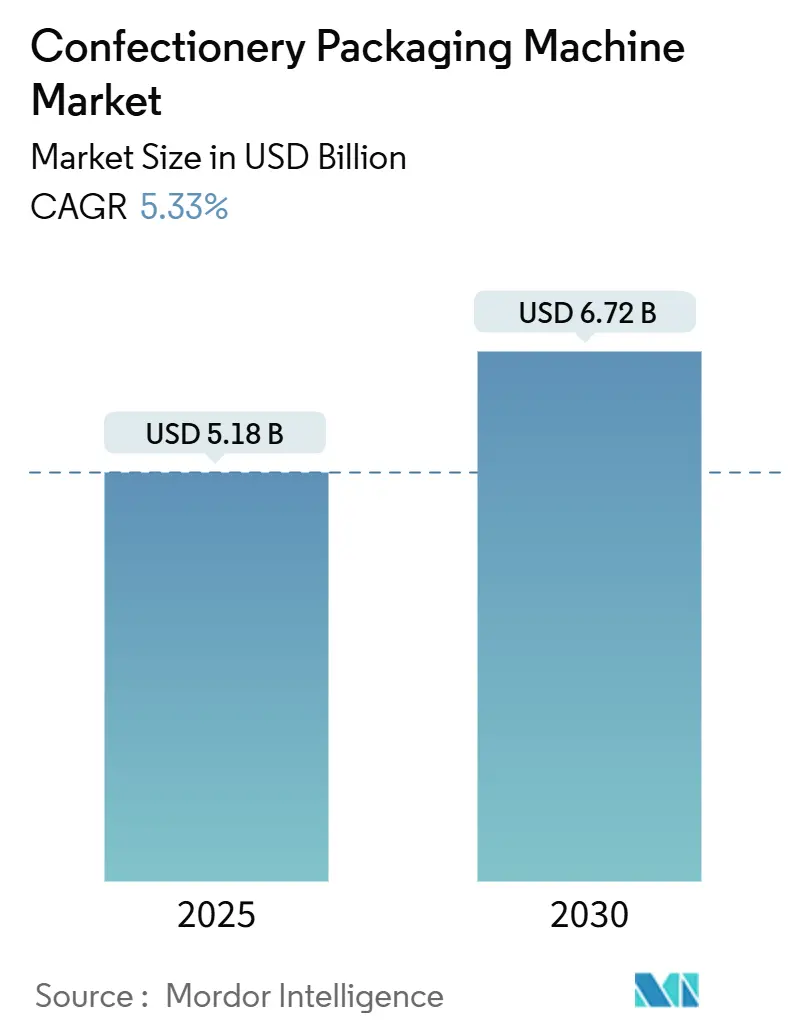

The confectionery packaging machine market size was USD 5.18 billion in 2025 and is projected to reach USD 6.72 billion by 2030, growing at a 5.33% CAGR over the forecast period. Current spending is anchored in large brand owners retrofitting lines for bio-based films, while small and medium-sized enterprises (SMEs) invest in compact automation to pursue premiumization and e-commerce formats. Ferrero allocated EUR 958 million (USD 1.082 billion) across four plants during fiscal 2024 to increase throughput and transition to sustainable substrates. Mondelez India has earmarked INR 4,000 crore (USD 480 million) for the Sri City expansion through 2028, confirming long-term demand in the Asia-Pacific region despite raw material volatility. Nestlé’s first Saudi factory aligns with regional momentum in Jeddah, a SAR 270 million (USD 72 million) greenfield project that will feature fully automated flow-wrap and cartoning lines.

Key Report Takeaways

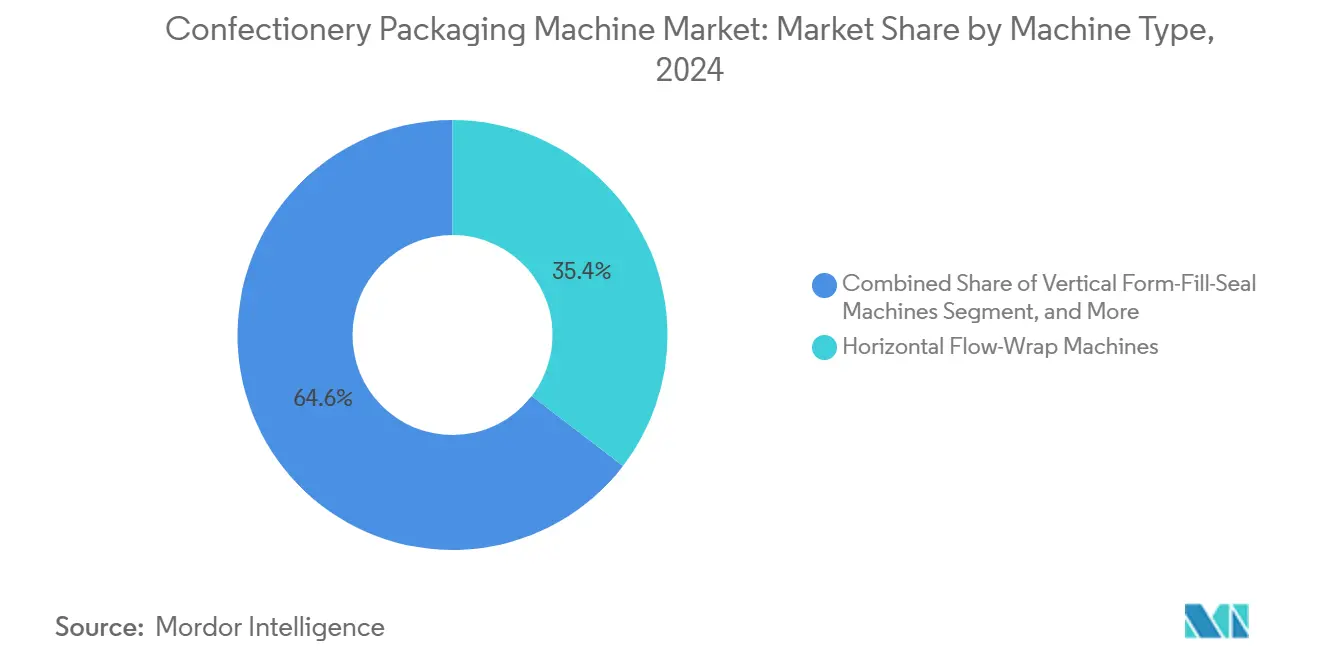

- By machine type, the horizontal flow-wrap segment captured 35.42% of the confectionery packaging machine market share in 2024.

- By automation level, the confectionery packaging machine market for fully automatic systems is projected to grow at a 6.43% CAGR between 2025-2030.

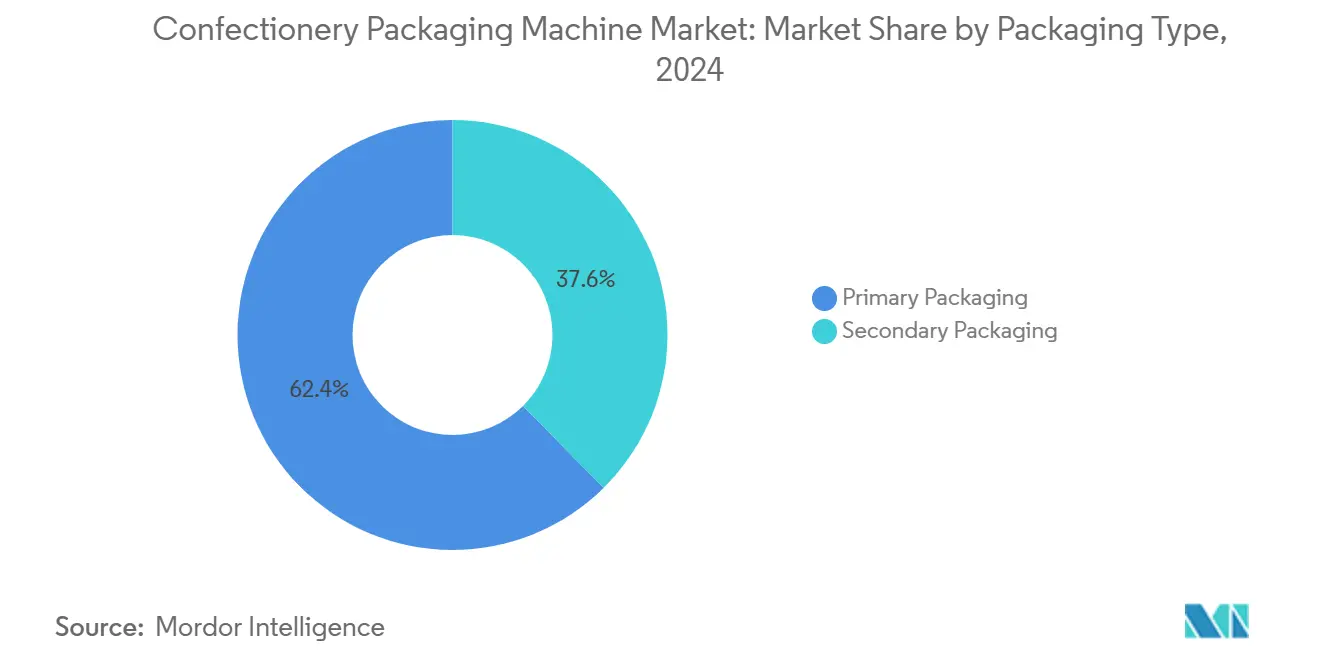

- By packaging type, primary packaging captured 62.43% of the confectionery packaging machine market share in 2024.

- By application, the confectionery packaging machine market for snack and energy bars is set to grow at a 6.87% CAGR between 2025–2030.

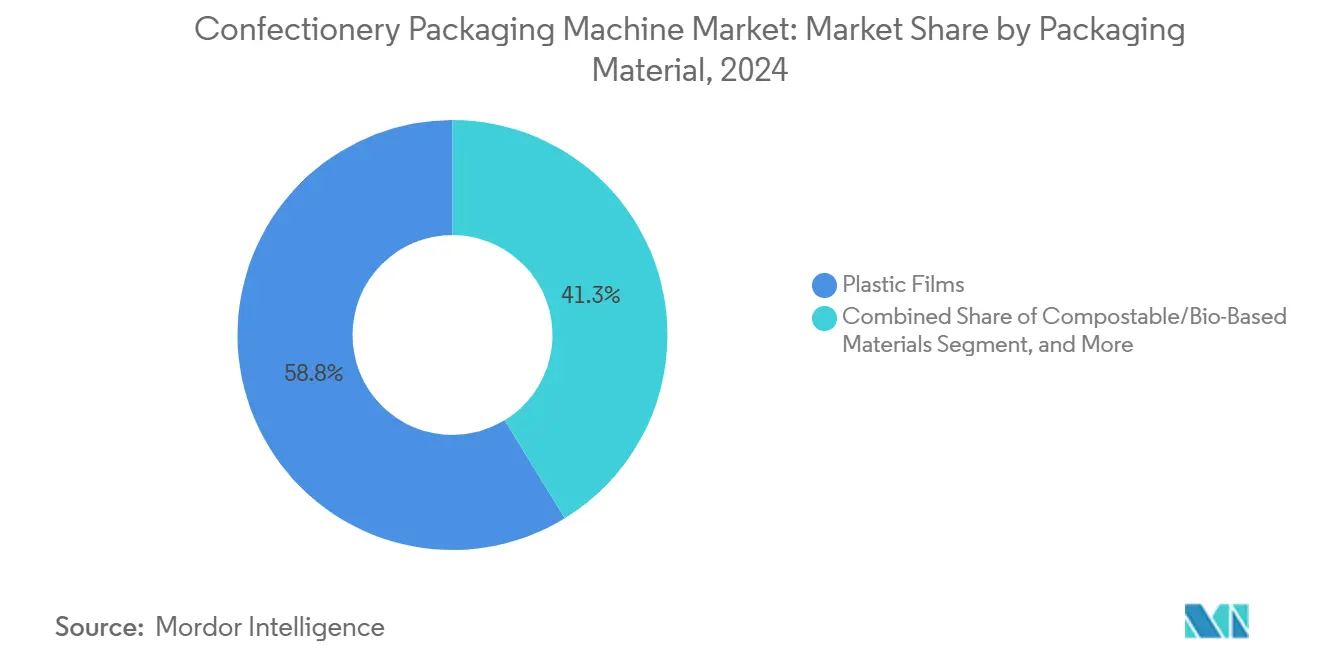

- By packaging material, plastic films captured 58.75% of the confectionery packaging machine market share in 2024.

- By end user, the confectionery packaging machine market for SMEs is forecast to expand at an 8.12% CAGR between 2025–2030.

- By geography, Asia-Pacific captured 40.21% of the confectionery packaging machine market in 2024.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Confectionery Packaging Machine Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Disposable Income in Developing Countries | +1.2% | Asia-Pacific core, spillover to the Middle East and Africa | Medium term (2-4 years) |

| Automation Push for Higher Line Throughputs | +1.0% | Global, early gains in North America and Europe | Short term (≤ 2 years) |

| Sustainability Mandates Shifting to Paper and Bio-Film Compatibility | +0.9% | Europe and North America lead, Asia-Pacific following | Medium term (2-4 years) |

| Rapid Expansion of E-Commerce Friendly Packaging Formats | +0.7% | Global, concentrated in urban centers | Short term (≤ 2 years) |

| Digitization and Predictive Maintenance Adoption | +0.6% | North America and Europe, with gradual Asia-Pacific uptake | Long term (≥ 4 years) |

| Niche Premiumization Requiring Small-Batch Flexible Machines | +0.5% | Europe and North America artisan markets, select Asia-Pacific cities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Disposable Income in Developing Countries

Per-capita confectionery consumption in India and Southeast Asia remains below Western levels, yet a fast-growing middle class is boosting volumes. Mondelez India’s incremental INR 1,600 crore (USD 192 million) outlay aims to double Sri City capacity to serve a domestic confectionery market valued at INR 25,000 crore (USD 3 billion). Lotte Wellfood is investing USD 300 million in local chocolate and ice cream plants, including a USD 60 million (INR 500 crore) biscuit-stick unit launched in 2025. Barry Callebaut added CHF 50 million (USD 54.5 million) for twin Indian factories to supply gourmet and industrial customers. Each expansion triggers the use of multi-lane flow-wrap machines and VFFS cells, which are designed to operate in humid climates and accommodate a wide range of pack sizes. Meanwhile, premium formats, such as resealable praline pouches, drive demand for rapid changeovers that legacy semi-automatic lines cannot match.

Automation Push for Higher Line Throughputs

Persistent labor shortages and wage inflation squeeze operating margins, encouraging the substitution of manual packing with robotic pick-and-place modules. PMMI valued the United States packaging machinery market at USD 11.3 billion in 2024, forecasting 2.2% growth for 2025 as food manufacturers prioritize automation.[1]PMMI, “2024 State of the Industry Report,” pmmi.org Theegarten-Pactec’s CHS wrapper handles 1,600 products per minute, illustrating how high-speed units cut unit costs by consolidating multiple legacy lines. SACMI’s H-SM and ACMA’s CW 1400 achieve 160 and 1,400 packs per minute, respectively, catering to producers aiming for single-shift payback windows. Predictive maintenance now covers 43% of food plants, reducing unplanned downtime that can cost thousands of dollars per hour and strengthening the business case for fully automatic configurations.

Sustainability Mandates Shifting to Paper and Bio-Film Compatibility

The European Union’s Packaging and Packaging Waste Regulation requires 25% rPET content by 2025 and 30% by 2030, while banning per- and polyfluoroalkyl substances in food-contact packaging. Ferrero’s new Bloomington, Illinois, chocolate plant was specified for both conventional and bio-based films, ensuring compliance without costly retrofits. Rovema notes that paper films’ higher friction demands power unwinds and recalibrated sealing bars to prevent tearing, prompting OEMs to redesign hardware for multi-material handling. Compostable and bio-based substrates are growing at a rate of 7.82% per year, the fastest pace among materials.

Rapid Expansion of E-Commerce Friendly Packaging Formats

Direct-to-consumer (D2C) channels are reshaping package geometry and durability. DHL projects that next-generation packaging will reach USD 24 billion by 2033, with a 6.43% CAGR, underpinned by tamper-evident seals and unboxing features. Mars invested USD 70 million in a Hackettstown innovation lab to prototype packs optimized for parcel networks. Smurfit highlights how tactile unboxing boosts repeat purchases, spurring the development of flow-wrap and VFFS lines equipped with resealable zippers and QR codes for enhanced traceability. Pillow packs and stand-up pouches lower cube weight in shipping cartons, reducing freight costs and accelerating the adoption of vertical form-fill-seal systems.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Initial Capital Outlay for Advanced Equipment | -0.8% | Global, acute in emerging markets | Short term (≤ 2 years) |

| Volatility in Plastic Film and Aluminum Foil Prices | -0.6% | Global, sharper swings in Asia-Pacific | Short term (≤ 2 years) |

| Shortage of Skilled Technicians for Smart Machines | -0.5% | North America and Europe, and emerging in the Asia-Pacific | Medium term (2-4 years) |

| Sustainability Regulations Outpacing Material Readiness | -0.4% | Europe leads, North America follows | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Initial Capital Outlay for Advanced Equipment

Fully automatic confectionery packaging cells with integrated vision and robotic case packing often exceed USD 500,000 per line, a steep hurdle for SMEs. The United States producer price index for packaging machinery climbed from 309.161 in April 2025 to 314.976 by August 2025, reflecting cost inflation in steel and electronics. Lenders remain cautious about financing highly customized assets with limited secondary markets, which can lengthen project payback periods beyond three years. Equipment-as-a-service models are emerging, but adoption is slow because many regional banks view performance-based leasing as a risk. For contract packers operating on thin margins, the capital burden restricts their participation in premium SKUs that require sophisticated packaging lines.

Volatility in Plastic Film and Aluminum Foil Prices

Substrates account for the single largest variable cost in confectionery packaging. The Flexible Packaging Association recorded Q2 2024 price jumps of 6% for low-density polyethylene, 5% for high-density polyethylene, and 5% for aluminum foil. The International Monetary Fund reported that aluminum averaged USD 2,525.95 per metric ton in June 2025, which remains elevated compared to 2023. Brands facing cost spikes either renegotiate supply contracts or absorb margin erosion, forcing some to defer machinery upgrades. OEMs now design platforms that can switch among substrates, but such flexibility adds to capital costs, creating a circular challenge for smaller producers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Machine Type: Flow-Wrap Dominance Meets VFFS Versatility

Horizontal flow-wrap units accounted for 35.42% of the confectionery packaging machine market share in 2024, a position earned through their reliable hermetic seals for chocolate bars and biscuit sticks. The confectionery packaging machine market size for flow-wrap solutions benefits from incremental upgrades such as servo-driven crimpers and integrated metal detection. Growing consumer preference for gummies, pouches, and single-serve snack bars is driving manufacturers toward vertical form-fill-seal platforms, which are forecast to post a 7.43% CAGR through 2030.

The demand for VFFS lines is intensified by e-commerce, as pillow packs and stand-up pouches optimize cube utilization during parcel shipments. Matrix Packaging emphasizes that intuitive human-machine interfaces and remote diagnostics minimize VFFS downtime, raising overall equipment effectiveness. Ancillary segments, such as cartoning and stick-pack machinery, continue to serve niche formats, while robotic case packers increasingly anchor end-of-line automation.[2]Matrix Packaging, “VFFS Changeover and OEE Optimization,” matrixpackaging.com IMA Group’s 2024 acquisition of a 70% stake in Mespic expands its turnkey capabilities from primary wrapping to palletizing.

By Automation Level: Fully Automatic Systems Command Premium

Fully automatic machines held 68.32% of installations in 2024, reflecting their capacity to integrate forming, filling, sealing, and inspection in a single footprint. This penetration underpins a 6.43% CAGR to 2030 as labor scarcity and rising wages accelerate automation. Semi-automatic lines still attract artisan chocolatiers, but their throughput of 200–400 units per minute cannot match the over 1,000 units per minute of top-tier automatic cells.

Syntegon’s 2024 revenue rose 7% to EUR 1.6 billion (USD 1.8 billion), driven largely by confectionery projects that require PackML recipe management and OPC Unified Architecture connectivity. Augmented-reality headsets now reduce operator training time, while predictive algorithms minimize unplanned stoppages. As payback periods become tighter, SMEs are increasingly adopting modular designs that upgrade from semi- to fully automatic by adding servo modules rather than replacing entire lines.

By Packaging Type: Primary Packaging Anchors Revenue

Primary formats represented 62.43% of the confectionery packaging machine market in 2024, and this share is expected to expand at a 6.12% CAGR, highlighting the link between shelf-life protection and consumer appeal. The confectionery packaging machine market size for primary equipment grows as metallized films, holographic designs, and resealable closures become standard in premium lines. Secondary packaging, although slower at the checkout lane, gains relevance in e-commerce where protective mailers and tamper-evident seals are indispensable.

ACMA’s CW 1400, capable of 1,400 products per minute, epitomizes high-speed primary wrapping solutions that preserve flavor integrity. Minimalist club-store trends temper secondary demand, yet smart carton coding for traceability remains a regulatory requirement. OEMs now offer hybrid stations that combine primary wrapping with immediate insertion into display cartons, allowing brands to reduce floor space needs and simplify maintenance.

By Application: Chocolate Leads, Snack Bars Surge

Chocolate lines controlled 38.23% of the confectionery packaging machine market in 2024 and continue to command investment, as temperature-sensitive bars demand precise enrobing and cooling. Snack and energy bars, however, exhibit the fastest 6.87% CAGR, spurred by high-protein, low-sugar formulations. The confectionery packaging machine market size for bar applications is buoyed by consumers seeking portion control and on-the-go convenience.

Bühler’s SmartChoc platform, ranging from 90 kg/h to 400 kg/h, offers small-batch flexibility that aligns with artisanal bean-to-bar makers. Lotte Wellfood’s 2025 launch of Pepero biscuit sticks in India required wrapping machinery capable of handling biscuit-confectionery hybrids and humidity challenges. Soft candies and gummies still rely on twist-wrap and flat-fold formats, but new gel-based nutraceuticals push equipment suppliers to refine dosing accuracy and gentle handling.

By Packaging Material: Bio-Based Films Gain Momentum

Plastic films retained a 58.75% share in 2024; however, compostable and bio-based options are expanding at an annual rate of 7.82%, the swiftest pace across materials, as retailers impose sustainable sourcing requirements. The confectionery packaging machine market share for recycled or renewable substrates is expected to rise further once rPET supply chains stabilize. Rovema’s upgraded sealing jaws manage the higher coefficients of friction of paper films, ensuring hermetic integrity without scorched edges.

Aluminum foil remains relevant for premium chocolate bars that require light and oxygen barriers, but its 5% price increase in Q2 2024 encourages brands to consider metallized biaxially oriented polypropylene as an alternative. Ferrero’s EUR 958 million program added multi-material capability to plants in the United States, Italy, Germany, and Chile. OEMs increasingly provide modular unwinds and tool-less changeovers to switch between conventional and biodegradable films on demand.

By End User: SMEs Outpace Large Manufacturers

Large confectionery groups controlled 65.32% of the market demand in 2024, leveraging their scale to operate fully integrated, high-speed production lines. Yet SMEs, including contract packers and artisan chocolatiers, will deliver an 8.12% CAGR to 2030, making them the fastest-growing customer group. The confectionery packaging machine market size allocated to SMEs is increasing because retailers and online marketplaces are encouraging niche products with premium positioning.

ULMA Packaging’s 40% stake in RAMA broadens its presence among Latin American co-packers seeking flexible lines with production rates under 200 units per minute. Modular platforms enable small operators to purchase a semi-automatic base today and upgrade to automatic motion controllers as volumes increase, thereby minimizing initial capital outlay and de-risking expansion. Large manufacturers respond by carving out flexible pilot cells within megaplants to incubate limited-edition SKUs without disrupting high-volume staples.

Geography Analysis

The Asia-Pacific generated 40.21% of the confectionery packaging machine market in 2024 and is forecast to log an 8.75% CAGR from 2024 to 2030, the fastest regional pace. Investments such as Mondelez India’s INR 4,000 crore (USD 480 million) program and Nestlé India’s INR 6,500 crore (USD 780 million) multi-site outlay underscore confidence in sustained volume gains. China anchors regional demand, yet regulatory scrutiny of food safety pushes OEMs to integrate serialization. Japan’s aging demographic drives the demand for portion-controlled packs, while South Korea’s export-oriented bar makers invest in flow-wrap lines to service Western retailers.

Europe ranks second by value, propelled by Germany, Italy, France, Spain, and the United Kingdom. The European Union’s rPET mandate accelerates retrofit activity, and Ferrero’s modernization of its Stadtallendorf plant demonstrates how leading brands prepare for 2026 compliance. Germany’s concentration of OEMs, including Syntegon and Theegarten-Pactec, enables rapid prototyping and service support. Italy maintains a powerful cluster of suppliers, such as ACMA and SACMI, that co-develop specialty chocolate and nougat lines with local brands.

North America exhibits steady demand, driven by high automation and e-commerce penetration. Ferrero’s USD 75 million Bloomington plant and Mars’s USD 70 million Hackettstown upgrade exemplify the drive to localize production and test direct-to-consumer (D2C) packs. Charms committed USD 97.7 million to expand its Covington, Tennessee, site, while Spangler Candy increased sugar-house throughput to 300,000 pounds per day to meet seasonal peaks.

Competitive Landscape

European specialists, including Syntegon, Theegarten-Pactec, ACMA, IMA Group, Loesch, SACMI, PFM, Cama Group, and ULMA Packaging, collectively hold a commanding position by offering modular, digital-twin-enabled lines and extensive service coverage. Syntegon exited its Food Liquid unit and divested a facility in Waiblingen in 2024 to sharpen its focus, later acquiring Telstar for its expertise in sterile processing. IMA Group acquired 70% of Mespic, integrating end-of-line robotics into the IMA FLX HUB platform that provides artificial-intelligence diagnostics and digital sandboxes. ULMA Packaging acquired a 40% stake in RAMA in 2025 to expand its Latin American presence.

Asian suppliers, notably Hopak and JOIEPACK, compete on cost and delivery speed, targeting SMEs in Southeast Asia and Latin America. Disruptors utilize additive manufacturing to produce custom tooling on demand, thereby reducing the time required for changeovers. Technology adoption revolves around predictive maintenance sensors; 43% of food plants deployed them in 2024, and another 45% plan to follow, creating aftermarket opportunities for software vendors.

White-space innovation includes sealing stations optimized for compostable films and compact cells with throughput rates below 200 units per minute for premium artisan lines. Players who strengthen rPET and paper compatibility are likely to secure long-term contracts with retailers, as they move aggressively toward circular-economy targets.

Confectionery Packaging Machine Industry Leaders

Syntegon Technology GmbH

Loesch Verpackungstechnik GmbH & Co. KG

ACMA S.p.A.

Theegarten-Pactec GmbH & Co. KG

Gerhard Schubert GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Charms, a Tootsie Roll arm, announced a USD 97.7 million expansion of its Covington, Tennessee, plant to grow hard-candy output.

- February 2025: ULMA Packaging acquired a 40% stake in RAMA, expanding its Latin American footprint and complementing the earlier IPS Dairypack purchase.

- January 2025: KKR invested in CMC Machinery to accelerate sustainable end-of-line packaging and 3D on-demand e-commerce formats.

- January 2025: ANDRITZ acquired 70% of Diatec S.R.L., expanding its nonwoven line-up with converting machines for hygiene and food packaging.

Global Confectionery Packaging Machine Market Report Scope

The Confectionery Packaging Machine Market refers to the global industry focused on the design, manufacturing, and sale of machinery used for packaging confectionery products such as chocolates, candies, gums, and other sweets. These machines are essential for ensuring product safety, maintaining hygiene, extending shelf life, and enhancing visual appeal through attractive packaging.

The Confectionery Packaging Machine Market Report is Segmented by Machine Type (Horizontal Flow-Wrap, Vertical Form-Fill-Seal, Cartoning, Wrapping, Sachet and Stick-Pack, Case Packing and End-of-Line), Automation Level (Fully Automatic, Semi-Automatic), Packaging Types (Primary, Secondary), Application (Chocolate, Hard Candies, Soft Confectionery, Chewing Gum, Snack and Energy Bars, Gummies and Jellies, Other Applications), Packaging Material (Plastic Films, Paper, Compostable Bio-Based Materials, Aluminium Foil), End-User (Large Confectionery Manufacturers, Small and Medium-Sized Manufacturers, Contract Private-Label Manufacturers) and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Horizontal Flow-Wrap Machines |

| Vertical Form-Fill-Seal Machines |

| Cartoning Machines |

| Wrapping Machines |

| Sachet and Stick-Pack Machines |

| Case Packing and End-of-Line Machines |

| Fully Automatic Systems |

| Semi-Automatic Systems |

| Primary Packaging |

| Secondary Packaging |

| Chocolate |

| Hard Candies |

| Soft Confectionery |

| Chewing Gum |

| Snack and Energy Bars |

| Gummies and Jellies |

| Other Applications |

| Plastic Films |

| Paper |

| Compostable/Bio-Based Materials |

| Aluminium Foil |

| Large Confectionery Manufacturers |

| Small and Medium-Sized Manufacturers |

| Contract/Private-Label Manufacturers |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

| By Machine Type | Horizontal Flow-Wrap Machines | ||

| Vertical Form-Fill-Seal Machines | |||

| Cartoning Machines | |||

| Wrapping Machines | |||

| Sachet and Stick-Pack Machines | |||

| Case Packing and End-of-Line Machines | |||

| By Automation Level | Fully Automatic Systems | ||

| Semi-Automatic Systems | |||

| By Packaging Types | Primary Packaging | ||

| Secondary Packaging | |||

| By Application | Chocolate | ||

| Hard Candies | |||

| Soft Confectionery | |||

| Chewing Gum | |||

| Snack and Energy Bars | |||

| Gummies and Jellies | |||

| Other Applications | |||

| By Packaging Material | Plastic Films | ||

| Paper | |||

| Compostable/Bio-Based Materials | |||

| Aluminium Foil | |||

| By End-User | Large Confectionery Manufacturers | ||

| Small and Medium-Sized Manufacturers | |||

| Contract/Private-Label Manufacturers | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current global value of confectionery packaging machines?

The market is valued at USD 5.18 billion in 2025 and is projected to reach USD 6.72 billion by 2030.

Which region grows fastest for confectionery packaging machinery?

The Asia-Pacific region records the highest 8.75% CAGR through 2030, driven by rising incomes and significant capacity additions in India and China.

Which machine type is gaining share quickest?

Vertical form-fill-seal systems are growing at a rate of 7.43% per year, as brands favor pillow packs and stand-up pouches for gummies and snack bars.

How are sustainability rules affecting equipment demand?

EU rPET mandates and retail sourcing policies are driving investment in lines compatible with recycled and bio-based films, thereby pushing the adoption of material-flexible sealing stations.

Why are SMEs important in future sales?

SMEs grow at an 8.12% CAGR because artisan and contract packers need compact, changeover-friendly machines to serve premium and D2C brands.

What is the biggest cost barrier for small producers?

Advanced fully automatic packaging cells can exceed USD 500,000 each, making capital expenditure the main restraint for smaller firms.

Page last updated on: