Compartment Syndrome Monitoring Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 273.70 Million |

| Market Size (2031) | USD 398.45 Million |

| Growth Rate (2026 - 2031) | 7.80% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

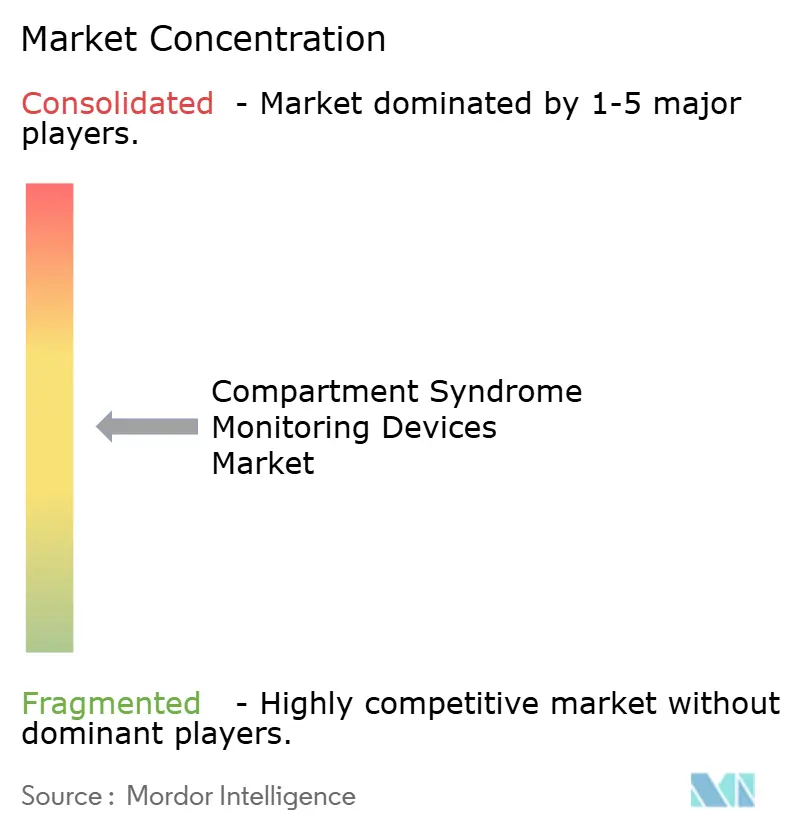

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Compartment Syndrome Monitoring Devices Market Analysis by Mordor Intelligence

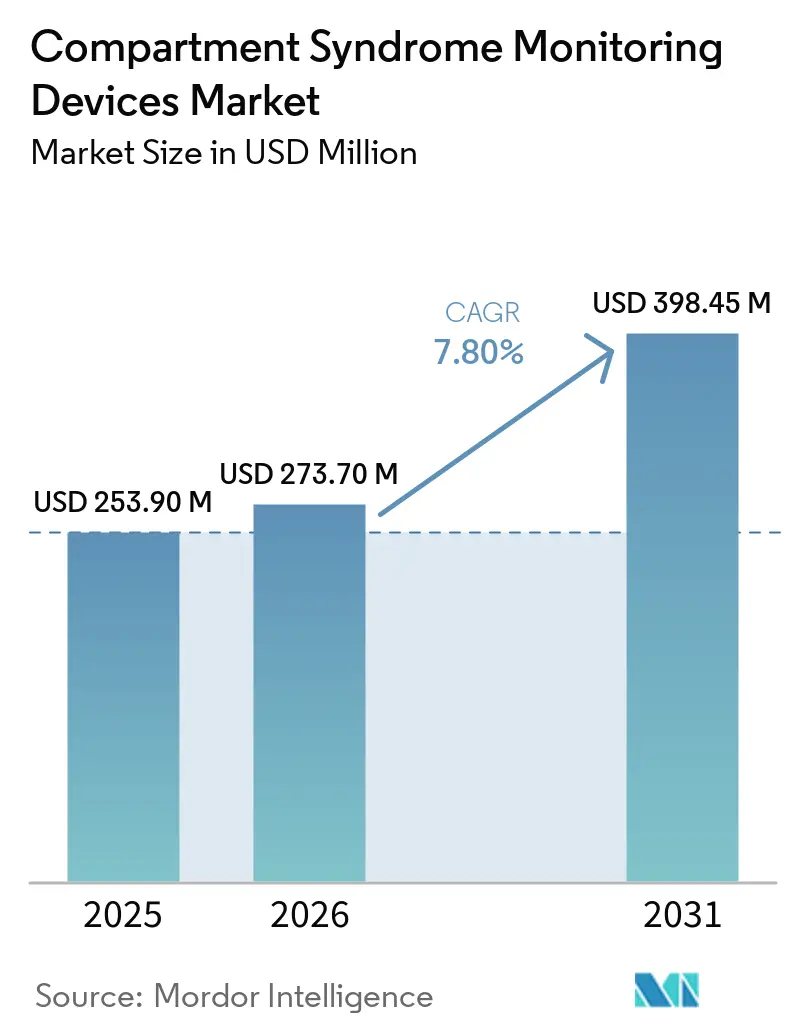

The Compartment Syndrome Monitoring Devices Market size is projected to be USD 253.90 million in 2025, USD 273.70 million in 2026, and reach USD 398.45 million by 2031, growing at a CAGR of 7.80% from 2026 to 2031.

Increasing trauma caseloads, clearer reimbursement codes, and a decisive move toward continuous wireless systems are catalyzing adoption. Hospitals value the technology’s ability to avert unnecessary fasciotomies, and device makers are aligning portfolios to recurring disposable revenue. Non-invasive sensors that remove infection risk are accelerating interest among ambulatory surgical centers, while AI-enabled analytics promise earlier alerts that preserve tissue viability. Asia-Pacific trauma-center expansions and localization incentives further sustain a robust demand outlook.

Key Report Takeaways

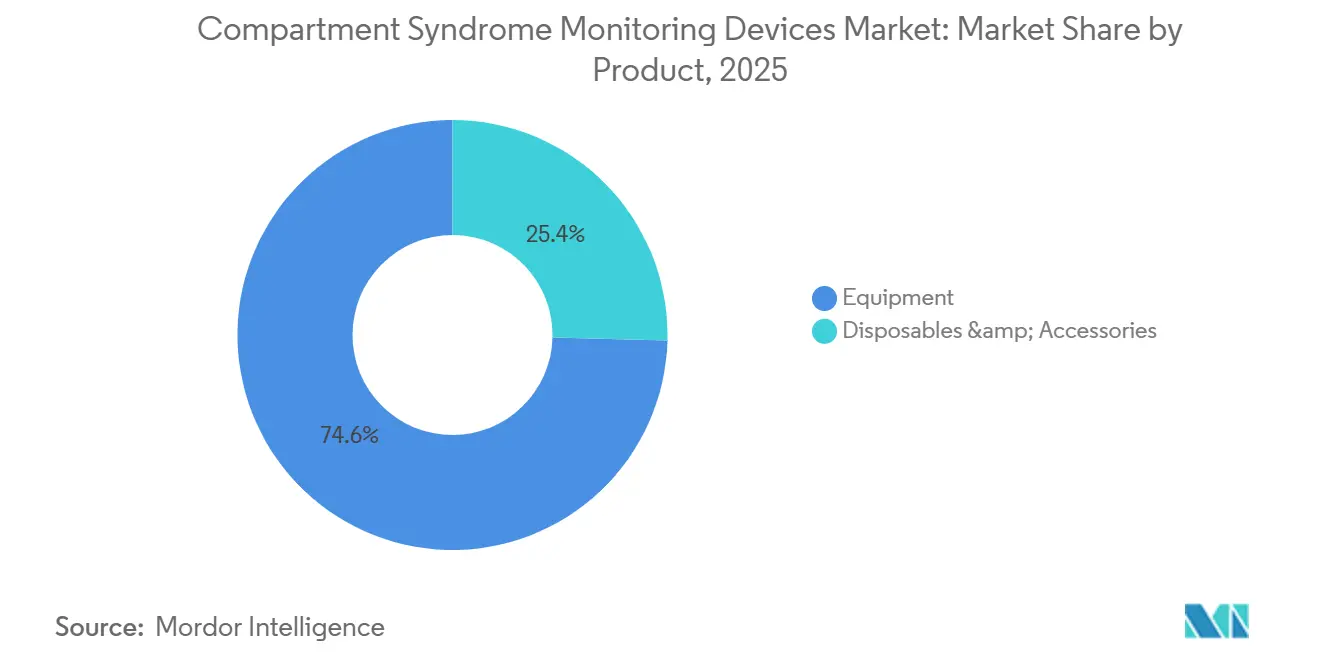

- By product, equipment led with 74.60% of the compartment syndrome monitoring devices market share in 2025, while disposables and accessories are expected to grow at a 9.08% CAGR through 2031.

- By technology, invasive monitoring devices commanded 54.06% share of the compartment syndrome monitoring devices market size in 2025, but non-invasive or minimally invasive devices will be projected to record the highest 9.55% CAGR to 2031.

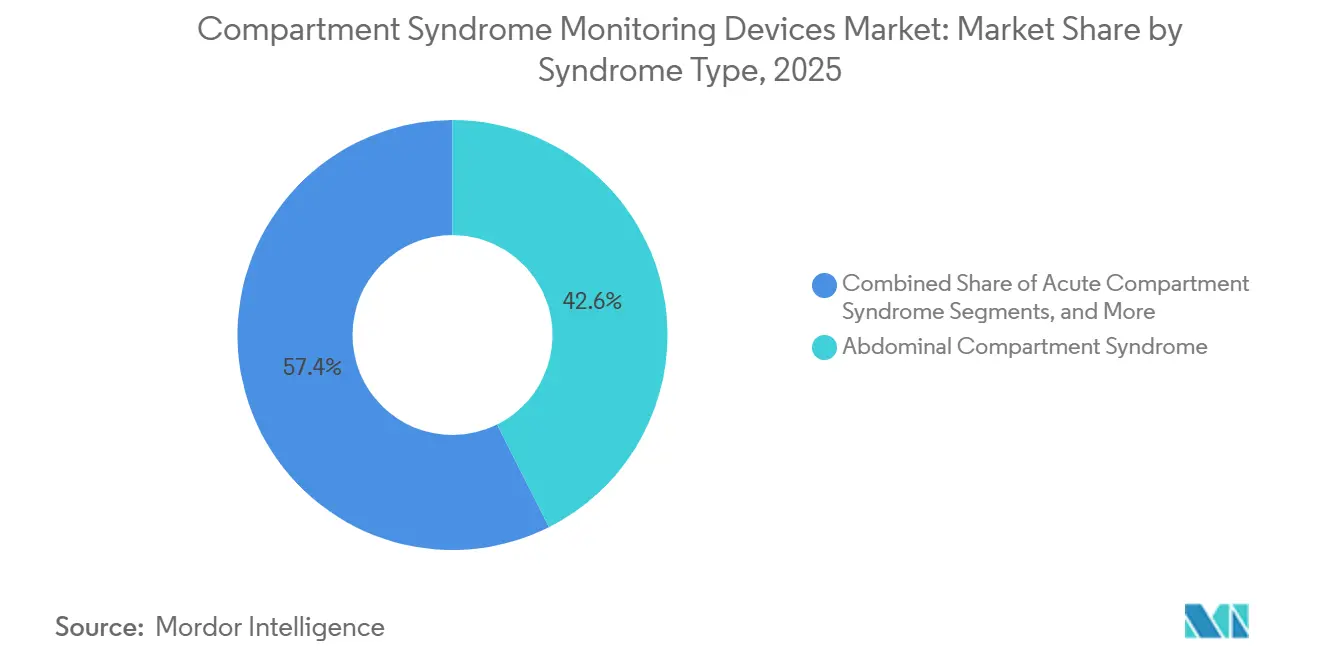

- By syndrome type, abdominal compartment syndrome captured 42.60% revenue in 2025 and is projected to expand at an 8.96% CAGR during 2026-2031.

- By end user, hospitals (Level I/II) accounted for 46.89% share in 2025, whereas ambulatory surgical centers will be the fastest-growing segment at an 8.40% CAGR through 2031.

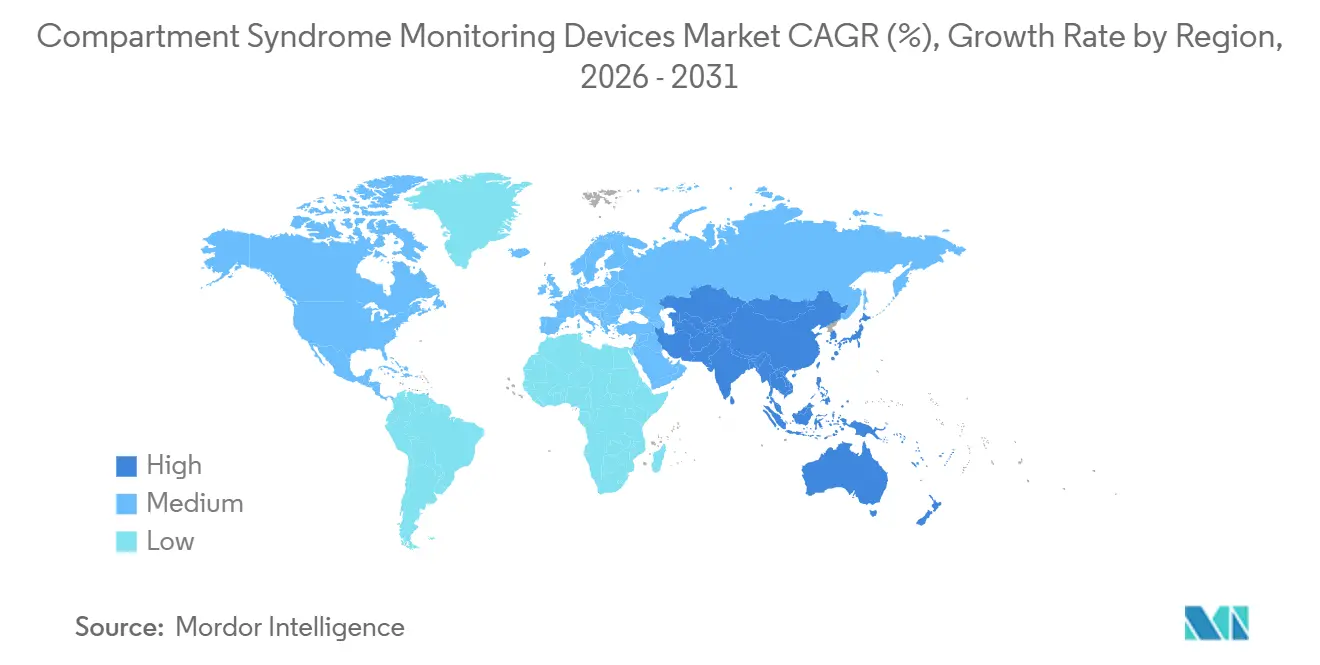

- By geography, North America led with 43.13% share of the compartment syndrome monitoring devices market in 2025, while Asia-Pacific will grow at a 8.80% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Compartment Syndrome Monitoring Devices Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising incidence of trauma-related injuries | +1.8% | Global, highest absolute volumes in APAC and North America | Medium term (2-4 years) |

| Growing clinician awareness of early diagnosis | +1.2% | North America & EU, spill-over to APAC tertiary centers | Short term (≤ 2 years) |

| Advances in continuous & wireless monitoring | +1.5% | Global, led by North America and Western Europe | Medium term (2-4 years) |

| Ai-driven predictive alert systems | +1.0% | North America & EU, early pilots in APAC | Long term (≥ 4 years) |

| Reimbursement code updates in key markets | +1.6% | United States; gradual EU adoption | Short term (≤ 2 years) |

| Military field-care procurement surge | +0.7% | United States and NATO allies | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Incidence of Trauma-Related Injuries

Global road-traffic collisions, sports fractures, and military casualties are driving an increase in acute compartment syndrome (ACS) cases, requiring prompt diagnosis. The U.S. Department of Defense has invested significant funds in its Advanced Medical Monitor program, emphasizing the importance of continuous pressure sensors for battlefield triage. Civilian trauma centers are also addressing this need, with a 2024 multicenter study involving 100 patients showing that continuous monitoring reduced amputation odds to 0.23 compared to intermittent checks. As traffic injury volumes rise in the Asia-Pacific, the demand for reliable monitoring in regional centers is growing.[2]JAMA Network, M. Rodriguez et al., “Continuous Pressure Monitoring in Polytrauma,” jamanetwork.com

Growing Clinician Awareness of Early Diagnosis

Professional societies are recommending protocolized monitoring for high-risk fractures. Research shows that performing a fasciotomy within six hours of symptom onset can reduce amputations by two-thirds, but subjective signs often delay surgery. Clinicians are increasingly relying on objective thresholds, such as maintaining a delta pressure below 30 mmHg. In the United States, malpractice insurers consider documented pressure trends as a risk mitigation measure, encouraging hospitals to invest in necessary capital purchases. Simulation training in academic centers is enhancing proficiency, establishing continuous monitoring systems as the emerging standard of care.

Advances in Continuous & Wireless Monitorin

Bluetooth-enabled devices are transmitting real-time data to mobile dashboards, reducing nurse workloads and improving visibility during staffing shortages. The MY01 platform, approved by regulatory authorities, enables alerts to be sent to surgeons even when they are off-site. MEMS transducers, originally developed for automotive applications, are now effectively measuring compartment pressure through 18-gauge catheters. Bioimpedance spectroscopy, which detects tissue edema by monitoring conductivity shifts, is progressing toward regulatory approval for acute trauma applications following its success in chronic exertional compartment syndrome (CECS) trials.

AI-Driven Predictive Alert Systems

Machine-learning algorithms are combining compartment pressure data with heart-rate variability, tissue oxygenation, and limb temperature metrics to predict potential deterioration well before traditional thresholds. BD’s HemoSphere Alta demonstrates the feasibility of embedding predictive analytics into bedside devices. Stryker has allocated substantial funds for research and development in 2025, aiming to integrate AI-driven decision support into surgical workflows. Although regulatory guidelines for software as a medical device have introduced stricter validation requirements, successful approvals could transform clinical practices, shifting the focus from reactive measures to preventive interventions.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| High device & disposable costs | -1.3% | Global, most acute in emerging markets | Short term (≤ 2 years) |

| Mixed clinical-outcome evidence | -0.9% | Global, especially EU academic centers | Medium term (2-4 years) |

| EU MDR sterilization validation delays | -0.6% | Europe | Short term (≤ 2 years) |

| Tariff-driven component cost volatility | -0.8% | Global, highest impact on U.S. importers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Device & Disposable Costs

Capital units can cost up to USD 25,000, and single-use catheters cost USD 400, putting financial pressure on smaller hospitals.[1]AHRQ Healthcare Cost and Utilization Project, “Cost-Effectiveness of Continuous Monitoring,” hcup-us.ahrq.gov A 2024 analysis identified net 60-day savings of USD 2,789 per patient due to fewer fasciotomies and shorter hospital stays. However, these savings benefit hospital finance teams rather than the departments responsible for funding the equipment, leading to budget misalignment. India’s 2024 production linked incentive scheme aims to localize manufacturing, but the benefits are not expected to materialize before 2027.

Mixed Clinical-Outcome Evidence

Continuous monitoring significantly reduces unnecessary fasciotomies, but randomized evidence demonstrating improved long-term function remains limited. A 2024 meta-analysis on CECS reported postoperative pain reduction, though 15% of patients experienced residual symptoms. This has fueled skepticism among European surgeons, who often prioritize clinical judgment over numerical thresholds. In the absence of large-scale randomized controlled trials, payers remain hesitant to reimburse expensive systems, and hospital committees delay their adoption.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Disposables Gain as Hospitals Shift to Recurring Revenue

Disposables are expected to surpass equipment as hospitals focus on infection-control compliance and predictable cost structures. The preference for single-use catheters aligns with the razor-and-blade model, enhancing profitability for suppliers. Equipment manufacturers are introducing modular consoles that activate premium software through licenses, combining capital affordability with long-term annuity streams. This strategic approach is likely to sustain the growth of the compartment syndrome monitoring devices market even after core capital placements reach saturation.

The shift towards disposables is particularly evident in ambulatory surgical centers, where lower upfront costs outweigh resistance to higher per-case fees. These facilities transfer catheter expenses to payers under fee-for-service rules, supporting a 9.08% compound annual growth rate through 2031 for consumables. Leading orthopedic companies are already reporting double-digit growth in single-use monitoring portfolios, indicating that consumables will play a key role in margin expansion across the compartment syndrome monitoring devices market.

By Technology: Non-Invasive Devices Accelerate as Infection Risk Drives Innovation

Non-invasive and minimally invasive systems are poised to gain market share as clinicians aim to reduce catheter-related complications. While invasive devices maintained a 54.06% lead in 2025, emerging bioimpedance and near-infrared platforms are growing rapidly at a 9.55% rate, outpacing the overall compartment syndrome monitoring devices market growth. Early-adopter trauma centers are validating the accuracy of these platforms, and regulatory pathways are becoming clearer following positive pilot data linking bioimpedance readings to invasive gold standards.

For community hospitals and sports clinics, non-invasive probes offer faster learning curves and simplified credentialing. Eliminating puncture risks also expands their use in anticoagulated or coagulopathic patients. As manufacturing volumes increase, component costs are expected to decline, narrowing price differences. Combined with AI analytics, contactless monitoring could eventually become the primary approach, relegating catheters to niche high-acuity scenarios.

By Syndrome Type: Abdominal Compartment Syndrome Dominates Critical Care Protocols

The abdominal subsegment benefits from established WSACS guidelines that integrate bladder pressure checks into ICU workflows. Defined thresholds for intra-abdominal hypertension and compartment syndrome simplify decision-making, providing manufacturers with a strong value proposition for pressure transducers. Bladder-based systems require only minor modifications to existing Foley catheters, supporting a 42.60% revenue share and an 8.96% growth outlook.

Limb-related ACS remains clinically significant but is primarily limited to high-energy fractures in trauma centers, while chronic or exertional cases are mostly seen in sports clinics. This fragmentation reduces purchasing power, making abdominal monitoring the higher-volume, protocol-driven segment within the compartment syndrome monitoring devices market. However, hybrid consoles that address both abdominal and limb indications offer opportunities for cross-selling.

By End User: Ambulatory Surgical Centers Emerge as Growth Frontier

The U.S. Centers for Medicare & Medicaid Services has expanded ASC reimbursements, enabling same-day fracture repairs that previously required inpatient stays. ASCs prioritize rapid turnover and low complication risks, driving demand for wireless and non-invasive systems that support immediate discharge. Vendors are developing portable kits that integrate with existing anesthetic monitors, reducing installation challenges and supporting the projected 8.40% compound annual growth rate.

Hospitals remain the primary market segment with a 46.89% share, driven by their dominance in multi-system trauma care and larger capital budgets. However, even hospitals are transitioning to hybrid models where disposables contribute to recurring revenue streams. As health systems acquire ASCs, procurement standards are aligning, ensuring technology consistency across inpatient and outpatient settings and expanding the reach of the compartment syndrome monitoring devices market.

Geography Analysis

In 2025, North America secured 41.13% of the revenue share, supported by its extensive network of Level I and II trauma centers and the FDA's predictable 510(k) pathway, which expedites market entry. The introduction of the October 2025 Transitional Pass-Through and New Technology Add-on Payments for MY01 established a dedicated reimbursement channel, accelerating hospital adoption and validating premium device pricing. US quality programs have now integrated compartment pressure monitoring into their benchmarks, aligning financial incentives with its adoption.

Asia-Pacific emerges as the fastest-growing region, achieving an 8.80% CAGR, driven by road-traffic injuries and government incentives for local device assembly. MedTech clusters in India have reduced manufacturing costs by up to 40%, promoting domestic production that competes with imports. China's expansion of trauma centers, along with Japan's premium market catering to its aging population, ensures consistent demand. However, US tariffs on Japanese sensors have prompted a shift in some assembly operations to Southeast Asia. While Australia's trauma network is relatively smaller, it serves as a crucial English-language regulatory platform, with many multinationals leveraging it for pilot deployments.

Europe grapples with EU MDR bottlenecks, causing delays in sterilization validations and extending launch cycles compared to North America. Germany is considering a distinct DRG code that could transform the economic landscape, but its implementation is unlikely before 2027. The UK's NICE evaluation of non-invasive devices will play a pivotal role in shaping procurement decisions amidst tight NHS budgets. Southern Europe lags in trauma-center density, resulting in a fragmented adoption curve, where northern markets lead and their southern counterparts trail by three to five years.

Competitive Landscape

The compartment syndrome monitoring devices market is moderately fragmented, with pure-play innovators and orthopedic giants coexisting. Smith+Nephew utilizes its Leaf Patient Monitoring System to expand into trauma wards, leveraging its expertise in continuous tissue-status monitoring, a capability developed in pressure-injury prevention. Stryker, with a USD 1.6 billion R&D budget, demonstrates its strong focus on sensor-enabled surgical ecosystems. Meanwhile, Zimmer Biomet's acquisition of Paragon 28 reflects a strategic move by implant players toward perioperative analytics to protect their market share.

Start-ups differentiate themselves through advantages in wireless technology, AI, and cost-effective disposables. However, challenges such as FDA clearances, biocompatibility testing, and seamless hospital IT integrations create significant barriers, favoring established players with extensive service networks. Procurement committees prefer vendors offering EMR interfaces, predictive dashboards, and reliable catheter supplies. As a result, while new entrants can capture specialized niches, scaling up often requires partnerships with major distributors or acquisition by established orthopedic firms, maintaining a competitive yet balanced market for compartment syndrome monitoring devices.

Compartment Syndrome Monitoring Devices Industry Leaders

MY01, Inc.

Critical Care Diagnostics (C2DX), Inc.

Millar, Inc.

Medline Industries, Inc.

Potrero Medical

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: OrthoPediatrics partnered with MY01 to extend continuous perfusion monitoring into pediatric trauma, easing early ACS detection challenges in children.

- October 2025: CMS granted Transitional Pass-Through and New Technology Add-on Payments for MY01, unbundling device costs from surgical packages and accelerating U.S. adoption.

Global Compartment Syndrome Monitoring Devices Market Report Scope

As per the scope of the report, compartment syndrome monitoring devices are medical instruments, such as portable handheld manometers or catheter systems, designed to measure interstitial pressure within muscle compartments. By inserting a needle or sensor into the tissue, they provide real-time data to help clinicians diagnose increased pressure over 30mmHg, preventing tissue necrosis and facilitating timely decompressive fasciotomy.

The compartment syndrome monitoring devices market is segmented by product, technology, syndrome type, end-user, and geography. By product, the market includes equipment and disposables & accessories. By technology, the market is segmented into invasive monitoring devices and non-invasive/minimally invasive devices. By syndrome type, the market is categorized into acute compartment syndrome, chronic/exertional compartment syndrome, and abdominal compartment syndrome. By end-user, the market is segmented into hospitals (level I/II trauma), ambulatory surgical centers, orthopedic & sports medicine clinics, and military & emergency medical services. By geography, the market is analyzed across North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Equipment |

| Disposables & Accessories |

| Invasive Monitoring Devices |

| Non-Invasive / Minimally Invasive Devices |

| Acute Compartment Syndrome |

| Chronic/Exertional Compartment Syndrome |

| Abdominal Compartment Syndrome |

| Hospitals (Level I/II Trauma) |

| Ambulatory Surgical Centers |

| Orthopaedic & Sports Medicine Clinics |

| Military & Emergency Medical Services |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of MEA | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product | Equipment | |

| Disposables & Accessories | ||

| By Technology | Invasive Monitoring Devices | |

| Non-Invasive / Minimally Invasive Devices | ||

| By Syndrome Type | Acute Compartment Syndrome | |

| Chronic/Exertional Compartment Syndrome | ||

| Abdominal Compartment Syndrome | ||

| By End User | Hospitals (Level I/II Trauma) | |

| Ambulatory Surgical Centers | ||

| Orthopaedic & Sports Medicine Clinics | ||

| Military & Emergency Medical Services | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of MEA | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How fast is the compartment syndrome monitoring devices market expected to grow through 2031?

The compartment syndrome monitoring devices market size is projected to rise from USD 253.90 million in 2026 to USD 398.45 million by 2031, registering a 7.80% CAGR over 2026-2031.

Which product category is set to outpace the rest?

Disposables and accessories are forecast to post a 9.08% CAGR, ahead of reusable equipment, as hospitals shift toward single-use catheters that simplify infection control.

Why are non-invasive technologies gaining traction?

Bioimpedance and optical sensors avoid catheter-related infections and integrate easily into ambulatory settings, helping non-invasive devices capture the fastest 9.55% growth path.

Which syndrome type currently leads device utilization?

Abdominal compartment syndrome accounted for 42.60% of 2025 revenue and maintains the highest 8.96% CAGR thanks to ICU protocols that mandate serial intra-abdominal pressure checks.

What region shows the strongest growth potential?

Asia-Pacific posts the highest 8.80% CAGR through 2031 as China and India build trauma centers and incentivize localized device manufacturing.

Page last updated on: