Common-Mode Chokes Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

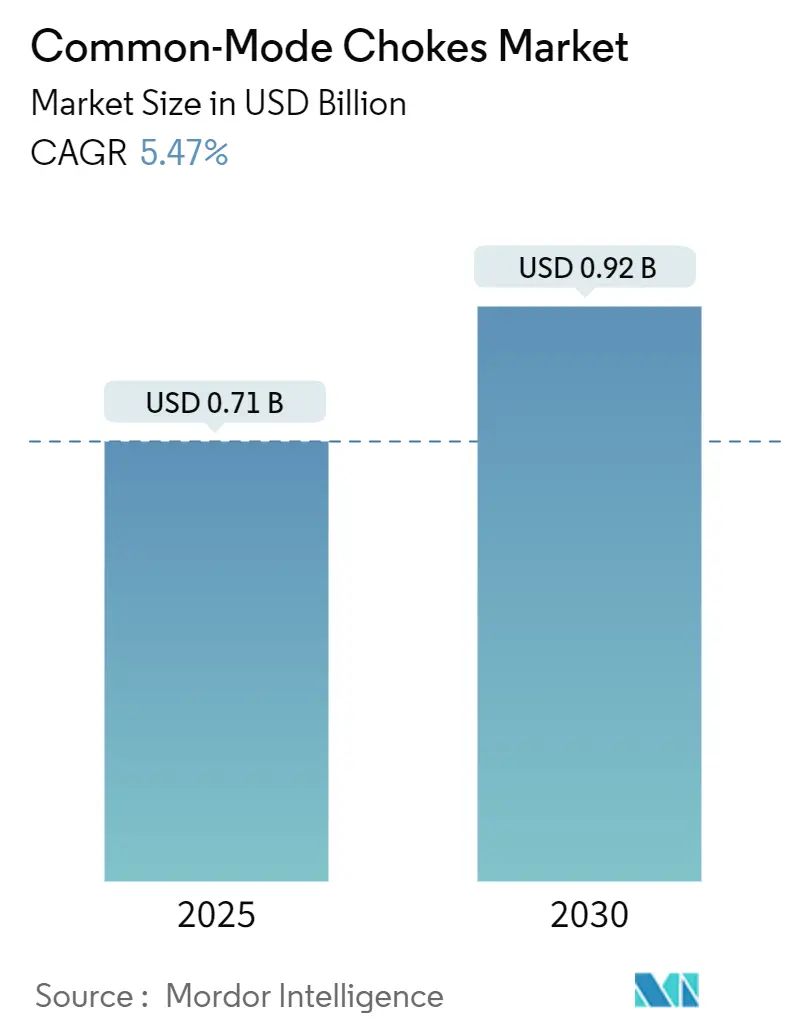

| Market Size (2025) | USD 0.71 Billion |

| Market Size (2030) | USD 0.92 Billion |

| Growth Rate (2025 - 2030) | 5.47% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Common-Mode Chokes Market Analysis by Mordor Intelligence

The Common-Mode Chokes market size stood at USD 0.71 billion in 2025 and is forecast to reach USD 0.92 billion by 2030, advancing at a 5.47% CAGR. This pace reflects regulatory pressure for electromagnetic compatibility in every major electronics category, the electrification of powertrains, and the spread of multi-gigabit data links that elevate common-mode noise. Equipment makers focus on smaller footprints, wider temperature envelopes, and higher current ratings, which pushes demand toward nanocrystalline cores and surface-mount formats. Competitive strategies revolve around vertical integration of magnetic materials, qualification to AEC-Q200 standards, and partnerships that secure alloy supply. Opportunities emerge in connector-integrated filtering for industrial Ethernet, miniaturized chokes for USB4 devices, and high-current parts for 800 V traction inverters.

Key Report Takeaways

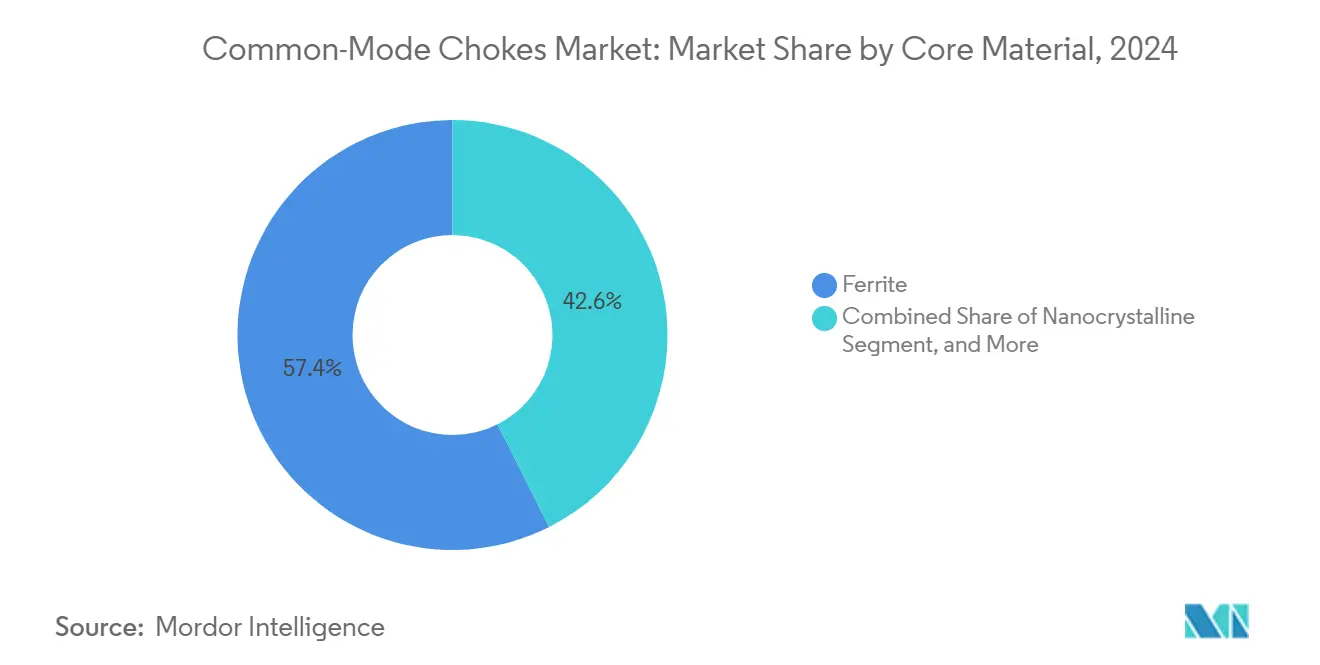

- By core material, ferrite retained 57.43% of the Common-Mode Chokes market share in 2024, whereas nanocrystalline cores are expanding at a 6.12% CAGR through 2030.

- By mounting type, through-hole components led with 45.72% revenue share in 2024; surface-mount designs are projected to post a 6.87% CAGR to 2030.

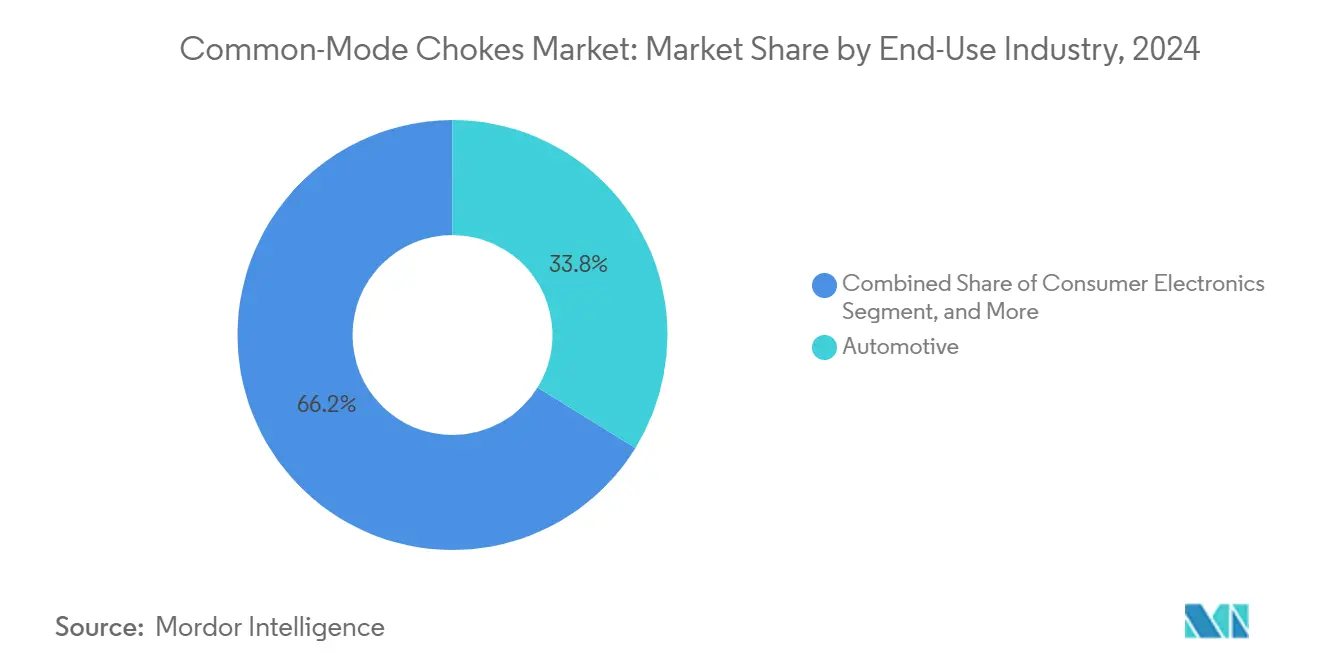

- By end-use industry, automotive captured 33.81% of the Common-Mode Chokes market size in 2024, while renewable energy and power is tracking a 5.76% CAGR to 2030.

- By application, power-line EMI suppression commanded 39.74% share of the Common-Mode Chokes market size in 2024 and high-speed interface filtering is advancing at a 6.23% CAGR through 2030.

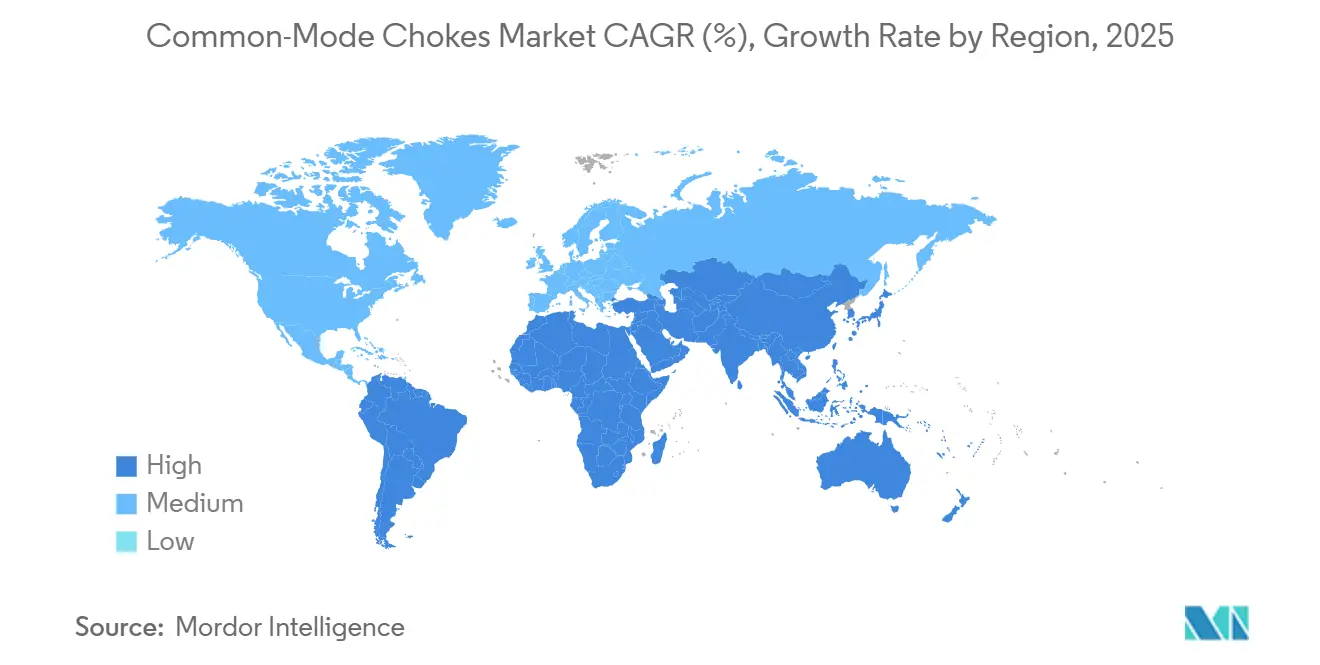

- By geography, Asia-Pacific accounted for 48.63% revenue share in 2024; the Middle East and Africa is forecast to register the fastest 6.34% CAGR to 2030.

Global Common-Mode Chokes Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent EMC regulations worldwide | +1.2% | Global with emphasis on EU, North America, Japan | Medium term (2-4 years) |

| EV power-electronics boom | +1.8% | Asia-Pacific core, spill-over to North America and EU | Long term (≥ 4 years) |

| High-speed consumer interfaces | +0.9% | Global, led by Asia-Pacific manufacturing hubs | Short term (≤ 2 years) |

| Shift to nanocrystalline cores | +0.7% | North America, EU, China automotive corridors | Long term (≥ 4 years) |

| Connector-integrated CMCs | +0.6% | North America, EU industrial automation centers | Medium term (2-4 years) |

| Residential PV + battery inverters | +0.4% | MEA, South America, India | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent EMC Regulations Worldwide

Global directives such as the EU EMC Directive 2014/30/EU and FCC Part 15 obligate manufacturers to prove radiated and conducted emissions compliance, prompting systematic incorporation of common-mode chokes in consumer, industrial, and automotive electronics. UNECE R.10 further extends the mandate to 800 V electric vehicles, compelling high-current choke adoption for traction inverters. Industrial sites fall under IEC 61000 rules that demand low noise floors for motor drives and Ethernet-based control networks, reinforcing use in factory automation. Regulatory audits penalize non-conformity, so compliance budgets are increasingly allocated to filtering components. As more jurisdictions harmonize to CISPR, the Common-Mode Chokes market gains a predictable, regulation-anchored pull.

EV Power-Electronics Boom (High-Current Demand)

The migration to 800 V battery packs and SiC MOSFET inverters raises switching edge rates and common-mode currents that often exceed 50 A, a stress level that standard ferrite chokes cannot manage. Nanocrystalline cores keep permeability stable up to 1 MHz, letting designers shrink size while sustaining impedance, as demonstrated in Tesla’s high-power converters. Each electric vehicle now carries 15-25 chokes across the inverter, on-board charger, and DC-DC stages, multiplying volume demand as global EV output targets 30 million units by 2030. Automotive OEMs tie sourcing contracts to AEC-Q200 grading, which favors vertically-integrated suppliers.

Proliferation of High-Speed Consumer Interfaces

USB4 at 40 Gbps and HDMI 2.1 at 48 Gbps introduce aggressive common-mode noise spectra above 10 GHz, where insertion-loss budgets are tight. Miniaturized surface-mount chokes from Murata are embedded in Mac Studio Thunderbolt boards to preserve eye-diagrams over long cables.[1]Murata Manufacturing Co., Ltd., “Murata Unveils World’s Highest Capacitance 0603-inch size MLCC,” murata.com Similar filters are specified in industrial vision networks and medical imaging consoles that rely on deterministic Ethernet links. The cadence of interface upgrades-USB5, DisplayPort 2.1, 25 GigE-keeps design cycles brisk, supporting recurrent revenues for vendors that refresh choke geometries and materials.

Shift to Nanocrystalline Cores for 800 V Architectures

Iron-based nanocrystalline alloys deliver saturation flux densities above 1.2 T, triple that of ferrite, and lower core losses across the -40 °C to +150 °C vehicle range. Porsche’s Taycan inverter adopts nanocrystalline chokes and reports a 50% footprint cut with lower winding temperature rise.[2]TDK Corporation, “TDK sets the course for the age of artificial intelligence at electronica 2024,” tdk.com Manufacturing, however, depends on ribbon annealing lines concentrated in Japan and Germany, and automakers now lock multi-year offtake deals to secure supply. As 800 V platforms proliferate, nanocrystalline volumes outpace ferrite growth, lifting the premium segment of the Common-Mode Chokes market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Commodity price pressure from Asian over-capacity | -0.8% | Global, originating from China and Southeast Asia | Short term (≤ 2 years) |

| Thermal and saturation limits of ferrite cores | -0.5% | Global, affecting high-power applications | Medium term (2-4 years) |

| Supply-chain risk for nanocrystalline ribbon alloys | -0.4% | North America, EU automotive markets | Medium term (2-4 years) |

| On-chip EMI filters in mobiles | -0.3% | Global consumer electronics markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Commodity Price Pressure from Asian Over-Capacity

A 40% capacity build-out in Chinese ferrite plants during 2023-2024 sent ex-works prices down 15-20%, compressing margins for global brands. Export incentives sustain the oversupply, forcing incumbents to cut costs or redirect investment to high-value automotive parts. While the situation benefits low-end buyers, it discourages R&D in entry-level chokes and raises the break-even hurdle for new entrants. The price war is expected to persist until at least 2026, shaving points off the overall Common-Mode Chokes market CAGR.

Thermal and Saturation Limits of Ferrite Cores

Ferrite permeability drops steeply above 125 °C and flux saturates near 0.4 T, hindering effectiveness in 11 kW on-board chargers where core temperatures routinely spike. Vishay highlighted the need for de-rating or active cooling in recent automotive reference designs.[3]Vishay Intertechnology, “Automotive Reference Design Notes on Thermal Performance,” vishay.com The work-arounds-oversized cores or heat-sink clamps-add weight and cost, driving designers toward nanocrystalline or amorphous alternatives. Until ferrite formulations improve, its physical ceiling will cap performance in emerging 800 V powertrains.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Core Material: Nanocrystalline Gains, Ferrite Holds Mass Volume

Ferrite dominated at 57.43% revenue in 2024, buoyed by mature tooling and low unit prices. Yet nanocrystalline parts are pacing a 6.12% CAGR and drawing share whenever high current, high temperature, or space savings outweigh price premiums. The Common-Mode Chokes market size for nanocrystalline designs reached USD 0.17 billion in 2025 and is projected to hit USD 0.23 billion by 2030, underscoring the shift toward performance-driven applications. Automotive traction and industrial servo drives now specify nanocrystalline rings with permeability above 100 k, eclipsing ferrite’s 10 k ceiling. Amorphous, iron-powder, and sendust grades serve niche medical or aerospace builds that prioritize low loss at MHz ranges.

Cost and supply remain decisive. Only four ribbon suppliers worldwide can anneal nanocrystalline tape at the volume automotive OEMs require, exposing buyers to spot shortages. TDK and other vertically-integrated vendors mitigate risk through captive alloys and long-term offtake agreements. Conversely, ferrite enjoys abundant feedstock and hundreds of sintering lines in East Asia, which secures availability for commodity IT and home-appliance boards. As EV production exceeds 30 million units, nanocrystalline will erode ferrite’s lead but ferrite will still anchor consumer-grade and low-power nodes.

By Mounting Type: Surface-Mount Catches Up With Through-Hole

Through-hole parts led with 45.72% revenue in 2024 because automotive and industrial inverters favor the mechanical strength of pin-mounted toroids. The Common-Mode Chokes market size attributable to surface-mount designs is, however, posting the faster 6.87% CAGR to 2030. Surface-mount chokes underpin USB4 hubs, laptop motherboards, and 25 Gbps optical modules where pick-and-place efficiency and low profile matter. Infineon’s power stages now co-package surface-mount EMI filters with MOSFETs to trim loop inductance.

Automotive electronics increasingly adopt press-fit or hybrid SMT formats that survive vibration while fitting onto insulated metal substrates. Through-hole remains essential above 20 A; climatic stresses and potting compounds complicate reflow. Clamp-on rings target field retrofits in industrial gear, and cable-mount variants secure compliance without PCB redesign. Adoption curves indicate parity between surface-mount and through-hole revenue by 2029 as consumer, telecom, and renewable inverters pursue automated assembly.

By End-Use Industry: Renewable Energy Accelerates Behind Automotive

Automotive applications accounted for 33.81% revenue in 2024 and remain the anchor customer for high-current, AEC-Q200-graded chokes. The segment’s Common-Mode Chokes market share benefits from rising EV penetration and the multiplication of power electronic subsystems per vehicle. Renewable energy, though smaller, is expanding at 5.76% CAGR thanks to residential PV in India, Brazil, and Saudi Arabia where 5-10 kW string inverters rely on grid-code compliant filtering.

Industrial automation, consumer electronics, and telecom together account for over 40% of unit volumes but skew to lower ASPs. Data centers and 5G antennas adopt high-frequency chokes for DC bus and PoE rails, adding incremental value. Medical and aerospace segments purchase highly specialized, traceable parts that fetch the highest margins but minimal volume. As nations step up inverter-based solar and storage, renewable energy could challenge automotive for growth leadership during 2028-2030.

By Application: High-Speed Interface Filters Surging From Low Base

Power-line EMI suppression held 39.74% of turnover in 2024 because every AC-DC supply integrates a C-MC at the input. The Common-Mode Chokes market size tied to high-speed interface filtering is climbing at a 6.23% CAGR, fueled by USB4 docks, HDMI 2.1 projectors, and deterministic Ethernet drives in factories. Signal-line filters must juggle low differential insertion loss with high CM impedance, driving vendors to tweak winding symmetry and bead geometry.

Hybrid filters that combine DM and CM suppression in a single footprint are gaining in IoT gateways and drones, trimming BOM line-items. Industrial 10 GbE upgrades and time-sensitive networking keep designers hunting for parts with flat impedance through 100 MHz-3 GHz, where ferrite starts to waste heat. Military radars and avionics also specify extreme-temperature chokes that maintain impedance at -55 °C to +175 °C. These premium use-cases bolster ASPs even as commodity phone chargers commoditize the lower end.

Geography Analysis

Asia-Pacific dominated the Common-Mode Chokes market with a 48.63% revenue share in 2024 thanks to the electronics manufacturing bases of China, Japan, South Korea, and Taiwan. Government incentives in China continue to enlarge ferrite output, while Japanese and Korean firms concentrate on high-end nanocrystalline strips. The regional Common-Mode Chokes market size is projected to climb from USD 0.34 billion in 2025 to USD 0.45 billion by 2030 on the back of EV exports and gigabit consumer devices.

North America ranks second on revenue, propelled by the electrification roadmaps of Ford, GM, and Tesla and by data-center build-outs that demand stringent EMI control. Federal clean-energy credits accelerate domestic inverter factories, and suppliers respond with local assembly lines to capture sourcing preferences tied to the Inflation Reduction Act. Europe twins regulatory pull with sustainability goals, embedding chokes in smart-grid converters, heat pumps, and 22 kW fast chargers that must pass CISPR 11 limits.

The Middle East and Africa logged the quickest 6.34% CAGR outlook as Saudi Arabia’s NEOM project, UAE PV farms, and South African mining automation drive sizable inverter deployments. Nidec’s supply deal with Noveon Magnets underscores intent to localize magnetic supply for the region’s renewables. South America follows, spearheaded by Brazil’s solar homes and Argentina’s electric-bus fleets. These emerging territories lean on turnkey European and Asian inverter OEMs, importing high-spec chokes until domestic foundries scale.

Competitive Landscape

The Common-Mode Chokes market tilts moderately concentrated, with the top five vendors-TDK, Murata, Vishay, Delta Electronics, and Premo—controlling roughly 62% of global revenue. TDK leverages captive nanocrystalline alloy lines and an AEC-Q200 catalog that grants pole position in EV and industrial drives. Murata’s forte in multilayer chip geometry strengthens its grip on mobile and notebook sockets. Vishay covers the power server niche with rugged toroids rated beyond 60 A. Delta’s 2024 pick-up of Alps Alpine’s inductor unit added machining know-how for datacenter converters.

Rivals from China and South Korea chase the low-cost tier by marrying abundant ferrite supply with scale PCB assembly, an approach that unsettles ASPs in commodity SKUs. To blunt price erosion, incumbents lengthen service contracts, bundle simulation tools, and co-design modules with SiC device makers. Patent filings center on amorphous metal blends, orthogonal windings, and resin systems that push temperature endurance above 175 °C. Connector-integrated chokes for SPE and industrial Ethernet represent a whitespace where smaller design houses can differentiate.

Strategic moves in 2025 lean toward verticalization and regional redundancy. Murata broke ground on a USD 20.1 million plant in Vietnam to double coil output and sidestep geopolitical risk. Premo teamed with Delta to open a ferrite plant in India, aligning with the government’s Make-in-India thrust. Siemens’ USD 10 billion pick-up of Altair augments electromagnetic simulation capability, giving OEMs a one-stop design-verify path that embeds choke selection early. As EV volumes swell, tier-1 suppliers are negotiating multi-year offtakes for nanocrystalline ribbon, locking in both price and continuity.

Common-Mode Chokes Industry Leaders

TDK Corporation

Murata Manufacturing Co., Ltd.

Vishay Intertechnology, Inc.

Würth Elektronik eiSos GmbH & Co. KG

Bourns, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Murata Manufacturing Vietnam began construction of a new production building at its Ho Chi Minh plant, investing JPY 3 billion (USD 20.1 million) to expand inductor coil capacity for automotive customers.

- July 2025: TDK Corporation launched the world’s first spin photo detector supporting 20 ps response times, a platform that underpins ultra-fast optical interconnects.

- June 2025: Premo and Delta formed a joint venture for soft ferrite production in India that will serve regional electronics makers.

- May 2025: REalloys Inc. signed a memorandum with Saskatchewan Research Council to scale rare-earth magnet output to 1,000 t by 2028.

Global Common-Mode Chokes Market Report Scope

| Ferrite |

| Nanocrystalline |

| Amorphous |

| Iron Powder |

| Other Core Materials |

| Through-Hole |

| Surface-Mount (SMD) |

| Clamp-On / Ring-Core (Cable) |

| Other Mounting Types |

| Automotive |

| Consumer Electronics |

| Industrial Equipment and Machinery |

| Renewable Energy and Power |

| Telecom and Datacom |

| Medical and Aerospace |

| Other End-Use Industries |

| Power-Line EMI Suppression |

| Signal/Data-Line Filtering |

| High-Speed Interface (USB/HDMI/Ethernet) |

| Hybrid Differential + Common-Mode Filtering |

| Other Applications |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Core Material | Ferrite | ||

| Nanocrystalline | |||

| Amorphous | |||

| Iron Powder | |||

| Other Core Materials | |||

| By Mounting Type | Through-Hole | ||

| Surface-Mount (SMD) | |||

| Clamp-On / Ring-Core (Cable) | |||

| Other Mounting Types | |||

| By End-Use Industry | Automotive | ||

| Consumer Electronics | |||

| Industrial Equipment and Machinery | |||

| Renewable Energy and Power | |||

| Telecom and Datacom | |||

| Medical and Aerospace | |||

| Other End-Use Industries | |||

| By Application | Power-Line EMI Suppression | ||

| Signal/Data-Line Filtering | |||

| High-Speed Interface (USB/HDMI/Ethernet) | |||

| Hybrid Differential + Common-Mode Filtering | |||

| Other Applications | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

How large is the Common-Mode Chokes market in 2025?

The market stands at USD 0.71 billion in 2025 and is projected to climb to USD 0.92 billion by 2030.

Which region leads sales of common-mode chokes?

Asia-Pacific holds 48.63% of 2024 revenue, driven by electronics production hubs in China, Japan, and South Korea.

Why are nanocrystalline cores gaining traction?

Nanocrystalline alloys offer higher saturation flux and lower losses, enabling smaller, higher-current chokes needed in 800 V EV systems.

What mounting style is growing fastest?

Surface-mount common-mode chokes are expanding at a 6.87% CAGR as miniaturization and automated assembly spread across devices.

Which application segment offers the most growth?

High-speed interface filtering, linked to USB4 and HDMI 2.1 adoption, is advancing at a 6.23% CAGR through 2030.

How intense is competition in this market?

The top five suppliers control about 62% of revenue, indicating moderate consolidation that still leaves space for specialist entrants.

Page last updated on: