Commercial Aircraft Inflight Entertainment and Connectivity System Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Market Size (2026) | USD 7.60 Billion |

| Market Size (2031) | USD 11.09 Billion |

| Growth Rate (2026 - 2031) | 7.85% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Commercial Aircraft Inflight Entertainment and Connectivity System Market Analysis by Mordor Intelligence

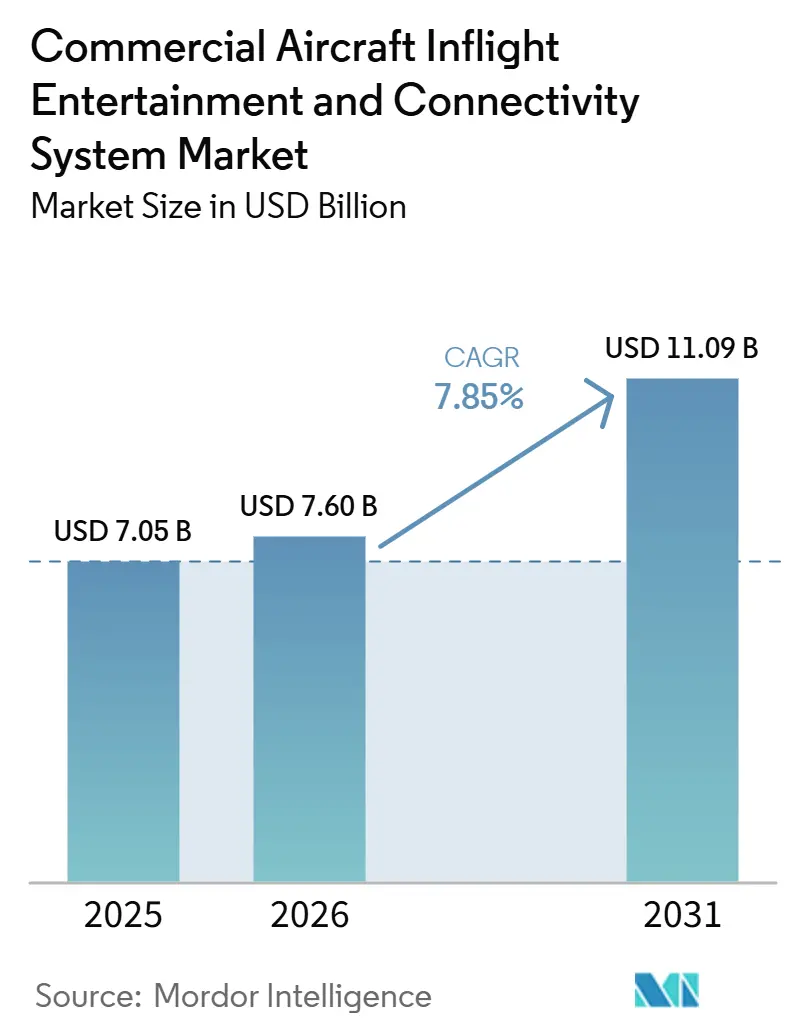

The commercial aircraft inflight entertainment and connectivity system market size was valued at USD 7.05 billion in 2025 and is forecast to grow from USD 7.6 billion in 2026 to reach USD 11.09 billion by 2031, at a CAGR of 7.85% during the forecast period (2026-2031). Airlines now treat cabin digital systems as a core part of product positioning, because onboard entertainment, connectivity, and digital retail increasingly shape passenger choice and loyalty. The commercial aircraft inflight entertainment and connectivity system market continues to benefit from seat-back demand among full-service carriers, while wireless and bring-your-own-device (BYOD) models are widening adoption among operators that need lower hardware intensity. Supplier strategy is also shifting, as modular platforms, lighter screens, and multi-orbit connectivity are being used to address lifecycle cost, weight, and upgrade concerns. The commercial aircraft inflight entertainment and connectivity system market is also gaining momentum from fleet expansion in Asia-Pacific and the Middle East, where new aircraft programs and retrofit plans are shifting demand toward suppliers capable of supporting linefit and upgrade cycles simultaneously. The competitive setting remains moderately concentrated in embedded system integration, but growth opportunities are broadening across software, connectivity management, content localization, in-seat power, and onboard commerce tools.

Key Report Takeaways

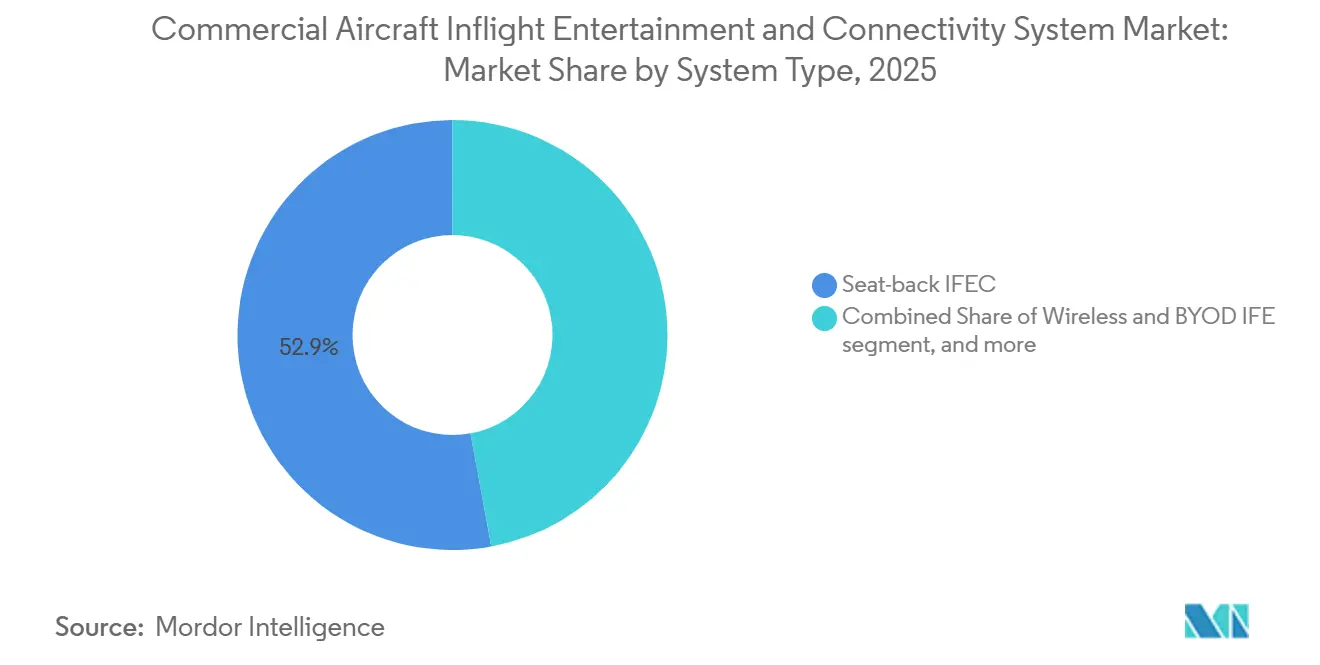

- By system type, seat-back IFEC led with a 52.88% revenue share in 2025, while wireless and BYOD IFE is projected to grow at a 10.41% CAGR through 2031.

- By aircraft type, narrowbody aircraft held a 49.35% revenue share in 2025, while regional jets are forecast to grow at a 10.92% CAGR through 2031.

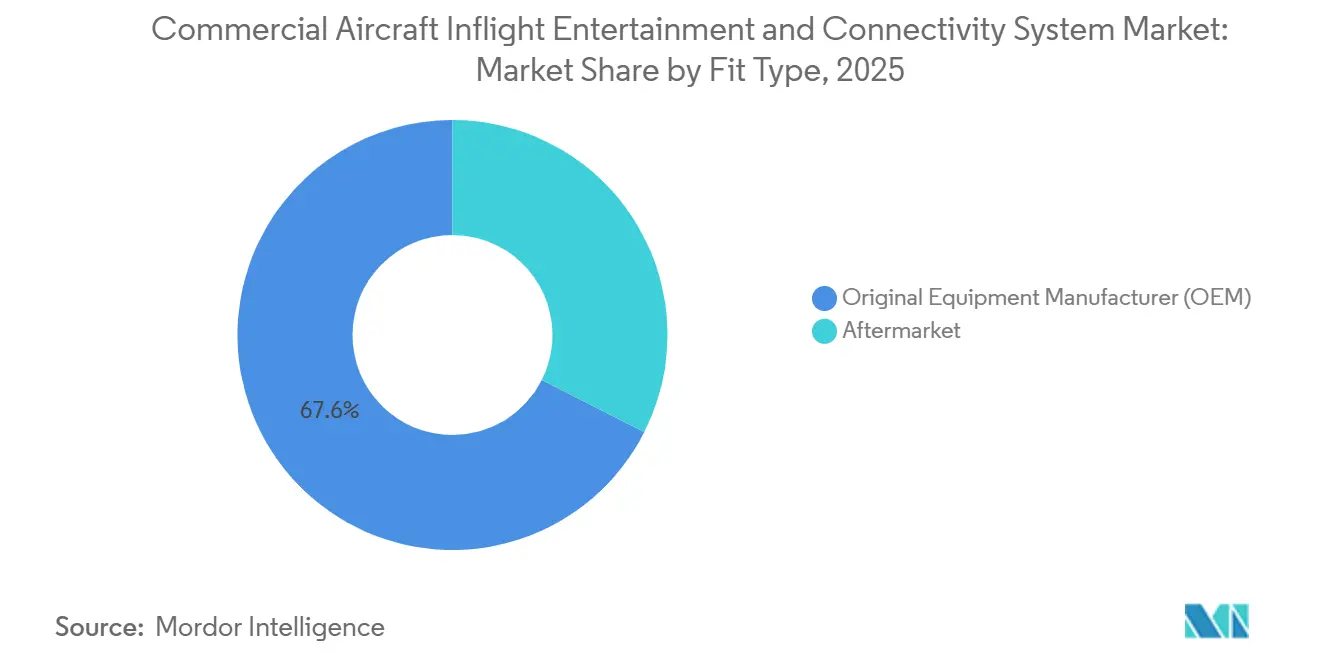

- By fit type, OEM installations accounted for 67.55% of the commercial aircraft inflight entertainment and connectivity system market in 2025, while aftermarket installations are forecast to grow at a 9.02% CAGR through 2031.

- By cabin class, economy class captured a 70.62% revenue share in 2025, while premium economy is forecast to grow at a 12.05% CAGR through 2031.

- By geography, North America accounted for a 30.88% share in the commercial aircraft inflight entertainment and connectivity system market in 2025, while Asia-Pacific is forecast to advance at a 10.34% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Commercial Aircraft Inflight Entertainment and Connectivity System Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Passenger-experience driven cabin differentiation | +2.20% | Global, concentrated spend in North America, Middle East, and Asia-Pacific | Medium term (2-4 years) |

| Asia-Pacific fleet and passenger boom | +1.80% | Asia-Pacific core, spill-over to Middle East and Africa | Long term (≥ 4 years) |

| High-speed SATCOM enabling streaming-grade bandwidth | +1.40% | Global | Medium term (2-4 years) |

| Low Earth Orbit (LEO) satellite bandwidth cost collapse | +1.00% | Global | Short term (≤ 2 years) to Medium term (2-4 years) |

| Bring Your Own Device (BYOD) retrofit cost advantage | +0.70% | Europe, Asia-Pacific, LCC-dominant markets globally | Short term (≤ 2 years) |

| IFE-enabled onboard e-commerce revenue | +0.50% | Global, early gains in North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Passenger-Experience Driven Cabin Differentiation

The commercial aircraft inflight entertainment and connectivity system market is being shaped by airline spending that now treats cabin digital equipment as a product decision rather than a maintenance choice. Singapore Airlines is committed to a multiyear A350 retrofit covering KrisWorld updates, new seating, premium economy upgrades, and revised first-class suites across 41 aircraft. Emirates also continued its USD 5 billion A380 retrofit program, adding premium economy with 13.3-inch inflight entertainment (IFE) displays across 219 aircraft, with the remaining two-class A380 retrofits expected to be completed by the end of 2026, subject to GCAA approval. This spending pattern shows that embedded entertainment is increasingly linked to airlines' efforts to defend premium positioning on long-haul and high-yield routes. It also suggests that carriers that reduce onboard digital quality without a credible substitute may face a weaker value proposition, especially when passengers compare entertainment and connectivity standards across competing airlines. The commercial aircraft inflight entertainment and connectivity system market, therefore, continues to gain support from airlines that use the cabin itself as a visible point of differentiation.

Asia-Pacific Fleet and Passenger Boom

The commercial aircraft inflight entertainment and connectivity system market is also advancing, as Asia-Pacific remains the strongest center of new aircraft demand. IATA forecasts Asia-Pacific passenger traffic growth of 7.30% in 2026, and the region already accounts for 34.50% of global RPK, keeping it at the center of future aircraft capacity expansion. AirAsia X placed a firm order for 150 A220 aircraft in May 2026, with the deal valued at USD 19 billion at list prices and deliveries set to begin from 2028. Vietnam Airlines also finalized an order for 50 B737 MAX-8 aircraft in February 2026, marking its first Boeing single-aisle order and linking future fleet growth to rising domestic passenger demand.[1]Boeing, “Vietnam Airlines Finalizes Order for 50 Boeing 737 MAX Airplanes,” Boeing Investor Relations, boeing.com These aircraft commitments matter because linefit decisions for IFEC are increasingly being locked in much earlier in the fleet planning cycle. The commercial aircraft inflight entertainment and connectivity system market is likely to see stronger supplier competition in Asia-Pacific as airlines seek earlier access to linefit slots and avoid waiting for retrofit queues after delivery.

High-Speed SATCOM Enabling Streaming-Grade Bandwidth

The commercial aircraft inflight entertainment and connectivity system market is being pushed forward by the shift from legacy connectivity to streaming-grade onboard bandwidth. The user-supplied content notes that LEO systems can reduce inflight latency to 20 to 40 milliseconds from the 600 to 800 millisecond range typical of geostationary systems, thereby changing connectivity from a convenience service into a functional productivity layer. American Airlines launched complimentary Wi-Fi across more than 2 million annual flights from January 2026, using Viasat and Intelsat systems across roughly 90% of its fleet, including nearly 500 regional jets with Intelsat multi-orbit electronically steered antennas. In 2025, Intelsat stated that its multi-orbit ESA solution had been installed on more than 100 jets, with Air Canada and Alaska Airlines joining American in deploying the platform on regional jets, with installation cycles of less than 2 days. This matters because faster installation and multi-orbit flexibility lower the operational barrier to upgrading smaller aircraft. The commercial aircraft inflight entertainment and connectivity system market is therefore moving toward an environment in which high-speed connectivity is expected across the network rather than limited to large long-haul aircraft.

IFE-Enabled Onboard E-Commerce Revenue

The commercial aircraft inflight entertainment and connectivity system market is also gaining support from the growing use of connected cabins as retail and service platforms. The user-supplied content states that global airline ancillary revenue exceeded USD 148 billion in 2024 and that digitally enabled onboard retail is among the fastest-growing categories for carriers with strong connectivity infrastructure. Anuvu signed an exclusive partnership with VidComply at AIX 2026 to automate content compliance, localization, and regional certification in the IFE supply chain, reducing catalog delays that can weaken passenger engagement on long-haul flights. Finnair also presented a personalized onboard retail approach at APEX FTE EMEA 2026, linking loyalty data to real-time cabin offers, which shows that connectivity is increasingly tied to merchandising rather than entertainment alone. This creates a reinforcing pattern in which better digital cabin systems help airlines improve ancillary yield, and stronger ancillary yield helps fund the next round of digital upgrades. The commercial aircraft inflight entertainment and connectivity system market is therefore expanding not only through hardware demand but also through revenue use cases that make connectivity more valuable over time.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Capex and weight penalty of seat-back systems | -0.90% | Global, most acute for narrowbody operators in Europe and North America | Medium term (2-4 years) |

| Certification hurdles for EMI/EMC | -0.60% | Global, with primary regulatory focus in FAA and EASA jurisdictions | Short term (≤ 2 years) |

| Cross-border content licensing complexity | -0.40% | Asia-Pacific and Middle East and Africa, where content regulatory fragmentation is highest | Medium term (2-4 years) |

| Cyber-security risks in open Wi-Fi architectures | -0.70% | Global | Short term (≤ 2 years) to Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Capex and Weight Penalty of Seat-Back Systems

The commercial aircraft inflight entertainment and connectivity system market still faces a structural cost challenge from embedded seat-back systems. The user-supplied content includes a per-seat installation cost of USD 10,000 for embedded seat-back hardware, before content licensing and maintenance are added over the aircraft lifecycle. That cost burden is amplified by weight, downtime, and the risk that onboard hardware becomes dated before the aircraft itself reaches midlife. Thales stated in 2026 that FlytEDGE Aura is more than 30% lighter than the prior generation, indicating that suppliers are directly targeting fuel burn and weight objections that have kept many narrowbody operators focused on BYOD alternatives. Panasonic also promoted Astrova as a modular platform with long-life infrastructure and upgradeable hardware elements, which addresses the same lifecycle cost problem from a different angle. Even with these improvements, the commercial aircraft inflight entertainment and connectivity system market remains constrained, where airlines prioritize fast aircraft utilization, minimal downtime, and lower retrofit complexity.

Cybersecurity Risks in Open Wi-Fi Architectures

The commercial aircraft inflight entertainment and connectivity system market also carries growing exposure to cybersecurity issues as open passenger networks support more devices, data exchanges, and onboard payment activity. The user-supplied content highlights risks such as data interception, man-in-the-middle attacks, and device-level intrusion across connected cabin environments. Patent US11991195B2 reflects active work on real-time monitoring of inflight entertainment systems linked to ground-based cybersecurity operations, indicating that security architecture is becoming a product layer in its own right.[2]United States Patent and Trademark Office, “Real-Time Cybersecurity Monitoring of Inflight Entertainment Systems,” Google Patents, google.com RTCA DO-160G remains a key airborne equipment standard for environmental and electromagnetic conditions. Still, the user-supplied content notes that network-layer cybersecurity for connected cabin systems is not yet addressed comprehensively in the same way. This creates a practical burden for airlines seeking to expand onboard connectivity while managing real-time threat detection across multiple aircraft. The commercial aircraft inflight entertainment and connectivity system market could therefore see slower rollout decisions among smaller carriers that lack dedicated cyber operations capacity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By System Type: Connected Seatback Redefines Premium IFE

Seat-back IFEC held 52.88% of the commercial aircraft inflight entertainment and connectivity system market share in 2025, making it the largest system type by revenue. The commercial aircraft inflight entertainment and connectivity system market still relies on embedded systems, where full-service carriers (FSCs) want a visible cabin standard that supports premium differentiation. Panasonic Avionics said Astrova reached 100 individual airline programs across 30 airlines by the end of 2025, with features including 4K OLED HDR10+ displays, Bluetooth spatial audio, and up to 67W USB-C power at each seat. Saudia then introduced Astrova on its A321XLR fleet in June 2026, which showed that embedded seat-back demand is expanding into narrowbody long-range aircraft that had often skipped heavier IFE systems in earlier cycles.

Wireless and BYOD IFE is projected to grow at a 10.41% CAGR through 2031, making it the fastest-growing system category in the commercial aircraft inflight entertainment and connectivity system industry. The commercial aircraft inflight entertainment and connectivity system market is seeing this shift because BYOD offers a lower hardware burden for carriers seeking connectivity and engagement without the full installation of embedded screens. Vueling deployed Viasat BYOD entertainment across more than half of its fleet, demonstrating that onboard content can be streamed to passenger devices even without a live external internet connection, according to the user-supplied content. Burrana also reported selections for its RISE Power platform on more than 880 aircraft globally at AIX 2026, more than double the footprint disclosed at AIX 2025, which highlights the importance of power infrastructure in BYOD and hybrid cabin setups. In practice, the commercial aircraft inflight entertainment and connectivity system market is moving toward a mixed model in which embedded systems dominate premium cabins, while power, portals, and device support expand across the rest of the cabin.

By Aircraft Type: Regional Jets Unlock New Connectivity Frontier

Narrowbody aircraft accounted for 49.35% of the commercial aircraft inflight entertainment and connectivity system market in 2025, reflecting their central role in the global fleet composition. The commercial aircraft inflight entertainment and connectivity system market has become increasingly dependent on narrowbody platforms as airlines increasingly use single-aisle aircraft on longer, more competitive routes. Air Canada’s Astrova program covers retrofits on 19 A321 aircraft and linefit on 30 A321XLRs, 23 A220-300s, and incoming B787-10 deliveries, which shows how narrowbody IFEC is moving from an optional upgrade to a standard specification on selected fleets. Widebody aircraft still attract the highest spending per unit because, first, business and premium economy cabins support more advanced displays, audio, and content hardware, according to the user-supplied content.

Regional jets are forecast to grow at a 10.92% CAGR through 2031, making them the fastest-growing aircraft type in the commercial aircraft inflight entertainment and connectivity system industry. The commercial aircraft inflight entertainment and connectivity system market is seeing this acceleration because regional fleets are finally becoming viable targets for faster, lower-downtime connectivity upgrades. Intelsat’s multi-orbit ESA had been installed on more than 100 regional jets by early 2025, and the deployment base included American Airlines, Air Canada, and Alaska Airlines, with installation timelines of under 2 days per aircraft. The user-supplied content also notes that Embraer began offering the Intelsat ESA as a linefit option on E2 twinjets, bringing connectivity decisions directly into the aircraft order process rather than leaving them for later retrofit. This means the commercial aircraft inflight entertainment and connectivity system market is extending its coverage to aircraft categories that previously operated with little or no comparable passenger digital capability.

By Fit Type: Aftermarket Programs Accelerate Behind OEM Foundation

OEM captured 67.55% of revenue in 2025, giving it the dominant position in the commercial aircraft inflight entertainment and connectivity system market. The commercial aircraft inflight entertainment and connectivity system market benefits from this structure because IFEC suppliers are increasingly tied to Airbus and Boeing delivery programs rather than relying solely on airline-led aftermarket spending. The user-supplied content states that newer linefit architectures can reduce power draw by 30% to 40% compared with earlier generations and can cut per-seat acquisition cost by a quarter when integrated during production. That advantage remains important because factory integration reduces certification friction and allows airlines to launch operations with connected cabins. At the same time, the commercial aircraft inflight entertainment and connectivity system market faces a timing problem when aircraft ordered years earlier arrive with specifications that are already behind the current technology curve.

Aftermarket installations are forecast to grow at a 9.02% CAGR through 2031, showing that the aftermarket is gaining weight even from a smaller base. The commercial aircraft inflight entertainment and connectivity system market is moving in this direction because aging widebody fleets need refresh cycles, and many aircraft that entered service without SATCOM now require connectivity upgrades. Emirates continued its USD 5 billion A380 retrofit program across 219 aircraft, adding premium economy and 13.3-inch IFE displays under GCAA oversight, which makes it one of the largest cabin retrofit commitments in commercial aviation. The user-supplied content also notes that Air India signed a 10-year FlytCARE agreement with Thales covering AVANT Up IFE on 57 aircraft, which shows how maintenance, support, and digital service continuity are becoming part of the retrofit business model. Even so, the commercial aircraft inflight entertainment and connectivity system market still faces slower retrofit velocity, where antenna approvals and supplemental type certificate processes extend implementation schedules.

By Cabin Class: Economy Volume Meets Premium Economy Momentum

Economy class held a 70.62% share in 2025, which made it the largest cabin class in the commercial aircraft inflight entertainment and connectivity system market. The commercial aircraft inflight entertainment and connectivity system market depends on economic demand, as this cabin carries the largest seat count and sets the scale for power, portal, and connectivity deployment across airline fleets. The user-supplied content shows a split strategy for this cabin, with FSCs continuing to install embedded screens. At the same time, low-cost operators remove them and strengthen BYOD portals, device holders, power outlets, and high-speed Wi-Fi. Panasonic launched eXneo as a lower-cost legacy upgrade option targeting this installed base, showing that economy cabin refresh is becoming a larger retrofit opportunity even when airlines stop short of a full next-generation platform replacement. In this sense, the commercial aircraft inflight entertainment and connectivity system market is not driven by a single hardware model in economy, but by different ways of meeting digital service expectations at scale.

Premium economy is forecast to rise at a 12.05% CAGR through 2031, making it the fastest-growing cabin class in the commercial aircraft inflight entertainment and connectivity system market. This part of the market is expanding because airlines are using premium economy to capture higher fares without moving passengers into full business class pricing. Singapore Airlines is committed to an A350 retrofit program that includes premium economy and an updated KrisWorld system, underscoring the strategic importance of this cabin on long-haul routes. The user-supplied content also notes that China Airlines introduced a B787 premium economy cabin with Bluetooth IFE connectivity in June 2026, showing that airlines are using this class as a technology showcase rather than treating it as a light upgrade over economy. As a result, the commercial aircraft inflight entertainment and connectivity system market is finding one of its strongest growth pockets in a cabin class that balances volume, fare uplift, and product visibility.

Geography Analysis

North America held 30.88% of the commercial aircraft inflight entertainment and connectivity system market share in 2025, maintaining its position as the largest regional contributor. It is driven by airline investment cycles, satellite infrastructure, and passenger expectations, which are already aligned around gate-to-gate connectivity. American Airlines launched complimentary Wi-Fi across more than 2 million annual flights from January 2026, using Viasat and Intelsat systems across roughly 90% of the fleet, including nearly 500 regional jets. The user-supplied content also points to activity by Delta and United as evidence that free, high-speed connectivity is becoming a baseline expectation in the US. Astronics reported record Q4 2025 revenue of USD 240.10 million, up 15.10% from the prior-year quarter, which reflects sustained demand for in-seat power hardware and IFEC components tied to this installed base.[3]Astronics Corporation, “Aerospace Drives Robust 4Q Sales and 2026 Outlook at Astronics,” Runway Girl Network, runwaygirlnetwork.com

Asia-Pacific is projected to grow at a 10.34% CAGR through 2031, making it the fastest-growing region in the commercial aircraft inflight entertainment and connectivity system market. IATA’s forecast of 7.30% year-on-year RPK growth in 2026 supports this view, as rising passenger traffic is driving aircraft deliveries and tighter installation timelines. AirAsia X ordered 150 A220 aircraft in May 2026, while Air India announced 30 additional Boeing single-aisle jets at Wings India 2026, according to user-supplied content, suggesting a widening future IFEC linefit pipeline. The user-supplied content also states that China’s major carriers have achieved IFE streaming coverage above 85% across widebody fleets, and that the C919 is adding momentum to localization discussions. India stands out because parallel commitments to Panasonic for widebody IFE and to Thales for long-term support show that catch-up investment is being compressed into a much shorter period than earlier airline upgrade cycles.

Europe held a stable position in 2025 in the commercial aircraft inflight entertainment and connectivity system market, with investment focused on retrofit, connectivity upgrades, and sustainability-linked platform choices rather than large greenfield programs. The user-supplied content notes that Lufthansa, SAS, and Virgin Atlantic confirmed satellite connectivity partnerships in 2024 and 2025, which shows that European FSCs are responding to rising onboard Wi-Fi expectations. The Middle East and Africa segment is expanding quickly through programs such as Emirates’ A380 retrofit, Etihad’s connectivity commitment, and Saudia’s Astrova deployment on the A321XLR, which are raising regional cabin specifications. Eutelsat and Anuvu signed a multiyear Ku-band capacity agreement on EUTELSAT 10B in May 2026 to strengthen IFC across the Middle East and European aviation corridors for a major global airline. South America remains smaller, but user-supplied content notes that operators such as Aerolíneas Argentinas are adopting multi-orbit connectivity, suggesting that regional IFC demand is broadening beyond the largest established aviation markets.

Competitive Landscape

The commercial aircraft inflight entertainment and connectivity system market is moderately consolidated at the system integration layer, with Panasonic Avionics and Thales holding the strongest positions in embedded IFE programs for FSCs. This does not make the entire competitive field tight because connectivity, content, power systems, antennas, and service software remain more fragmented across the commercial aircraft inflight entertainment and connectivity system market. Panasonic strengthened its position through Astrova, which reached 100 airline programs across 30 airlines by the end of 2025 and was then introduced on Air Canada and Saudia aircraft in 2026. Thales responded with FlytEDGE Aura, which it presented as the lightest IFE system in its portfolio, weighing more than 30% less than the prior generation, with planned retrofit availability from late 2028. These moves show that leading companies are competing on upgrade economics, cabin weight, modularity, and multi-orbit readiness rather than on screen hardware alone.

A second group of suppliers is building relevance in focused parts of the commercial aircraft inflight entertainment and connectivity system market rather than across full-stack integration. Anuvu is developing a position in content operations, AI-supported localization, and dedicated bandwidth management, while Burrana is expanding through in-seat power and cabin engagement products, and Astronics remains important in power hardware and IFC-related components. Burrana’s RISE Power selections exceeded 880 aircraft globally by AIX 2026, indicating that power architecture has become a strategic element in both embedded and BYOD cabin models. ThinKom also holds a differentiated place through phased-array antenna systems that fit the multi-orbit transition described in the user-supplied content. The commercial aircraft inflight entertainment and connectivity system market, therefore, combines concentration at the top of embedded integration with room for specialist suppliers to gain share in adjacent layers.

The commercial aircraft inflight entertainment and connectivity system market also has open space in AI-driven personalization, onboard retail integration, and cybersecurity services. Viasat’s SEC filing outlined a multi-orbit roadmap that combines LEO with its existing geostationary Ka-band platform, illustrating how established connectivity providers are reshaping their aviation offerings amid new competitive pressures. Burrana’s RISE Engage concept introduced a seatback e-paper display format for digital advertising, which points to a monetization layer that large incumbents have not fully addressed in a coordinated way, according to the user-supplied content. At the same time, certification requirements such as RTCA DO-160G continue to raise hardware entry barriers, helping protect incumbent positions in airborne equipment even as software-led services remain more open. The result is a competitive structure in which the core hardware layer is relatively protected, while value creation is spreading to service and software functions around the cabin.

Commercial Aircraft Inflight Entertainment and Connectivity System Industry Leaders

RTX Corporation

Burrana Pty Ltd.

Safran SA

Thales Group

Panasonic Holdings Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Panasonic Avionics Corporation announced that its next-generation Astrova IFE platform has entered commercial service with Air Canada, debuting on one of the airline's A321 aircraft. Air Canada is retrofitting the system across 19 A321 aircraft and will also linefit Astrova on 67 new aircraft, including A220-300, A321XLR, and B787-10 models, expanding deployment across its fleet.

- May 2026: Anuvu signed a multi-year agreement with Eutelsat to utilize high-throughput Ku-band capacity on the EUTELSAT 10B satellite to strengthen its IFC services, including support for a major global airline. Operational since July 2023, EUTELSAT 10B provides coverage from the Americas to Asia and features digital processing capabilities that enable flexible capacity allocation and efficient spectrum utilization.

Global Commercial Aircraft Inflight Entertainment and Connectivity System Market Report Scope

Commercial aircraft inflight entertainment and connectivity (IFEC) systems encompass the hardware, software, and communication technologies that deliver entertainment content, internet access, voice and messaging services, and digital passenger engagement during flight operations. These systems drive measurable improvements in passenger experience while enabling airlines to enhance operational efficiency, generate ancillary revenue, and maintain real-time aircraft communication through advanced connectivity solutions.

The commercial aircraft inflight entertainment and connectivity system market is segmented by system type, aircraft type, fit type, cabin class, end user, and geography. By system type, the market is segmented into seat-back IFEC, wireless and BYOD IFE, and in-seat power and peripherals. By aircraft type, the market is segmented into narrowbody, widebody, and regional jets. By fit type, the market is segmented into original equipment manufacturer (OEM) and aftermarket. By cabin class, the market is segmented into first class, business class, premium economy class, and economy class. The report also covers market sizes and forecasts for the commercial aircraft inflight entertainment and connectivity system market across major countries in different regions. For each segment, the market size is provided in terms of value (USD).

| Seat-back IFEC |

| Wireless and BYOD IFE |

| In-seat Power and Peripherals |

| Narrowbody Aircraft |

| Widebody Aircraft |

| Regional Jets |

| Original Equipment Manufacturer (OEM) |

| Aftermarket |

| First Class |

| Business Class |

| Premium Economy Class |

| Economy Class |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Indonesia | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Qatar | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By System Type | Seat-back IFEC | ||

| Wireless and BYOD IFE | |||

| In-seat Power and Peripherals | |||

| By Aircraft Type | Narrowbody Aircraft | ||

| Widebody Aircraft | |||

| Regional Jets | |||

| By Fit Type | Original Equipment Manufacturer (OEM) | ||

| Aftermarket | |||

| By Cabin Class | First Class | ||

| Business Class | |||

| Premium Economy Class | |||

| Economy Class | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Spain | |||

| Italy | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Indonesia | |||

| Singapore | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Qatar | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the 2026 value of the commercial aircraft inflight entertainment and connectivity system market?

The commercial aircraft inflight entertainment and connectivity system market is valued at USD 7.60 billion in 2026 and is forecast to reach USD 11.09 billion by 2031 at a 7.85% CAGR.

Which system type leads revenue in commercial aircraft IFEC?

Seat-back IFEC leads the market with a 52.88% revenue share in 2025, supported by FSCs and premium cabin product standards.

Which aircraft category is growing the fastest for inflight connectivity and entertainment system?

Regional jets are growing the fastest, with a projected 10.92% CAGR through 2031, driven by faster retrofit cycles and new linefit connectivity options.

Why is premium economy important for airline cabin technology investment?

Premium economy is the fastest-growing cabin class at a 12.05% CAGR through 2031, giving airlines a way to add fare upside with visible product upgrades at lower cost than full business class reconfiguration.

Which region shows the strongest growth outlook through 2031?

Asia-Pacific is expected to post the highest regional CAGR at 10.34% through 2031, supported by stronger passenger growth and a large future aircraft delivery pipeline.

What are the main risks affecting airline IFEC deployment?

The main risks are the capital and weight burden of seat-back systems, certification delays, content licensing complexity, and cybersecurity exposure in open Wi-Fi environments.

Page last updated on: