Commercial Aircraft Cabin Lighting Market Size and Share

Market Overview

| Study Period | 2026 - 2031 |

|---|---|

| Market Size (2026) | USD 1.12 Billion |

| Market Size (2031) | USD 1.34 Billion |

| Growth Rate (2026 - 2031) | 3.70% CAGR |

| Fastest Growing Market | Narrowbody |

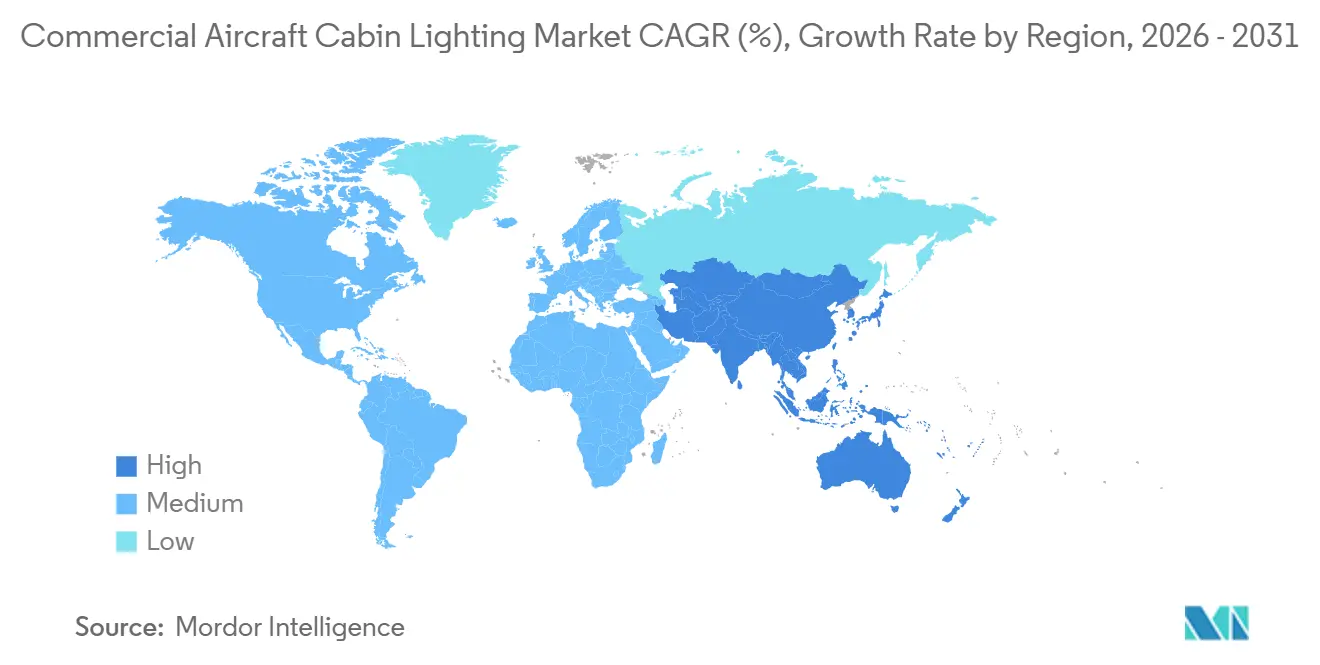

| Largest Market | Asia-Pacific |

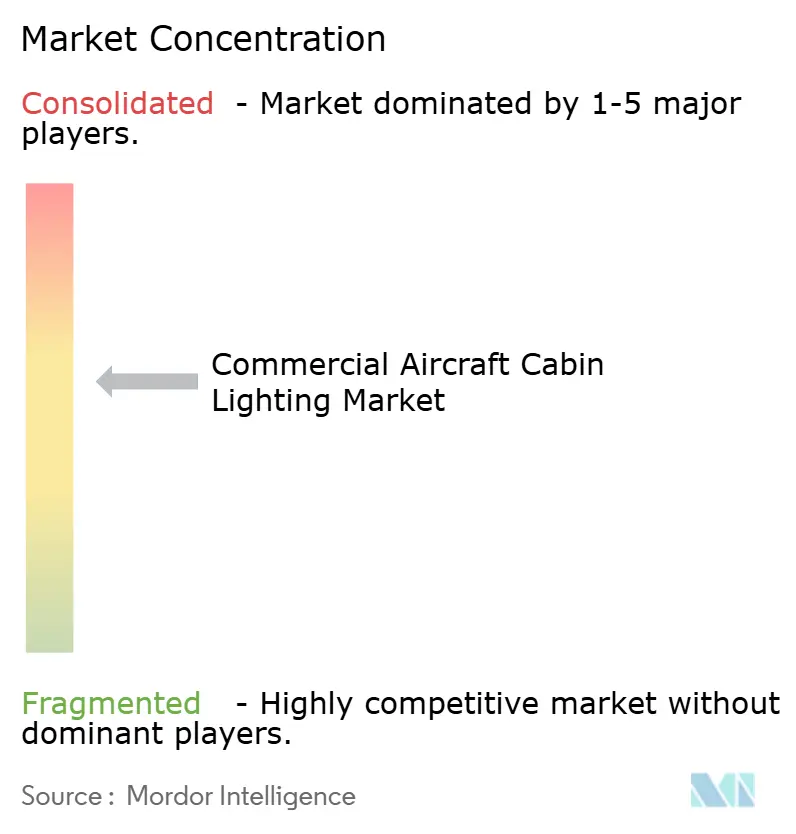

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Commercial Aircraft Cabin Lighting Market Analysis by Mordor Intelligence

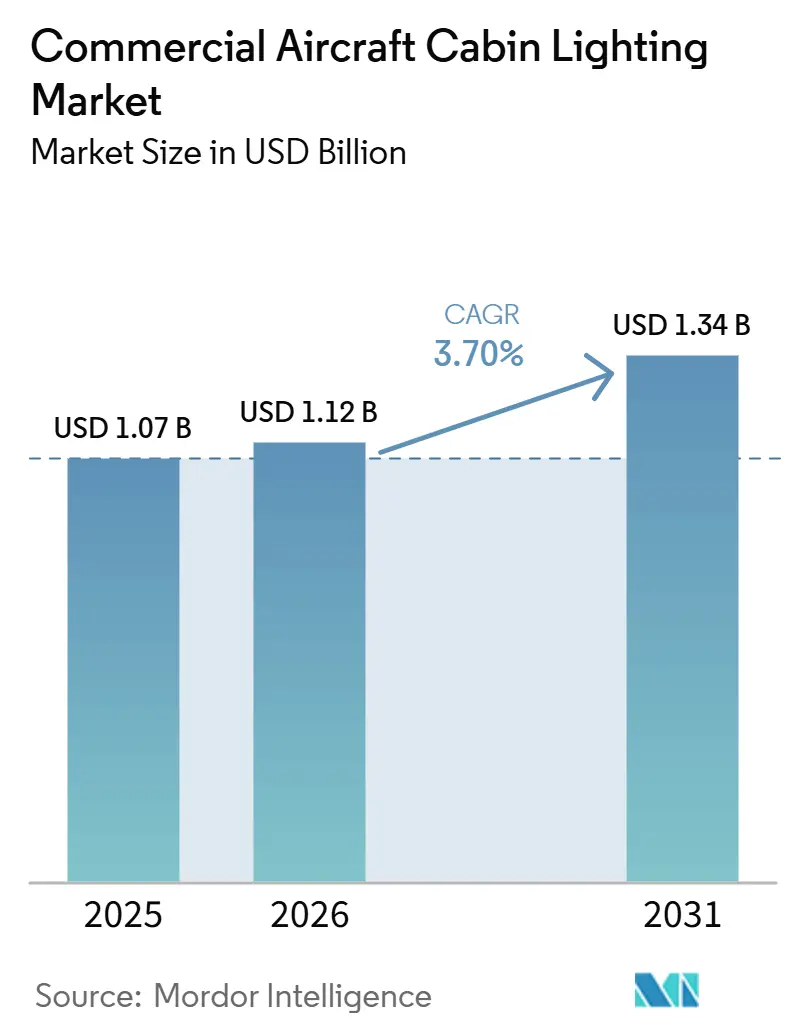

The commercial aircraft cabin lighting market size is expected to grow from USD 1.07 billion in 2025 to USD 1.12 billion in 2026, and is forecast to reach USD 1.34 billion by 2031, at a 3.70% CAGR over 2026-2031. Fleet expansion by low-cost carriers (LCCs), regulatory pressure to replace fluorescent tubes, and rising retrofit demand underpin steady growth even as widebody production delays temper linefit volumes. LED penetration has crossed the inflection point where retrofit economics eclipse incremental bulb swaps, collateral gains accrue from lighter wiring harnesses that help airlines meet ESG weight-reduction targets, and IoT-ready driver ICs unlock predictive-maintenance efficiencies. North America retains the largest regional position due to high aftermarket activity; Asia-Pacific records the fastest trajectory on the back of Indian and Chinese fleet programs; and Europe’s RoHS mandate sustains baseline demand even for cash-constrained carriers. Competitive intensity remains moderate because three incumbents, Collins Aerospace, Safran, and Diehl, command roughly 60% of linefit contracts through long-term Airbus and Boeing agreements. However, agile specialists such as STG Aerospace and Astronics are winning retrofit share with certified kits that trim aircraft downtime to under one week.

Key Report Takeaways

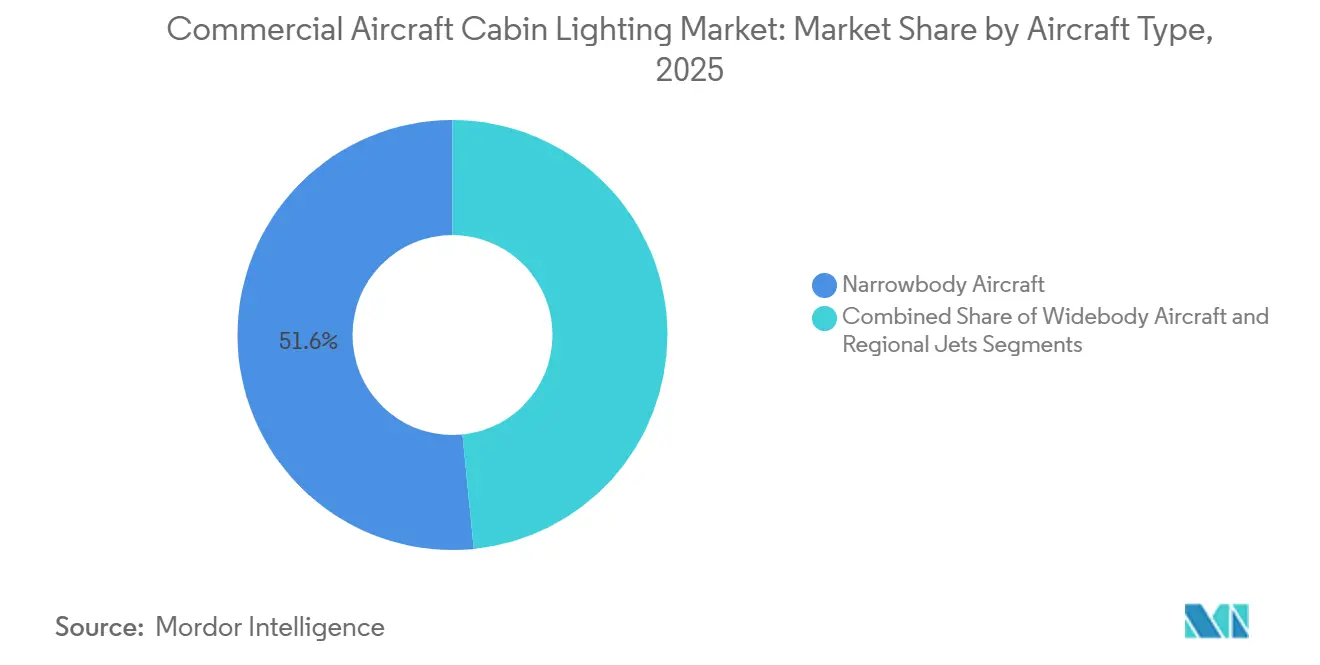

- By aircraft type, narrowbodies led with 51.58% of the commercial aircraft cabin lighting market share in 2025, while widebodies are forecast to expand at a 5.81% CAGR through 2031.

- By light type, ceiling and wall lights accounted for 44.15% share of the commercial aircraft cabin lighting market size in 2025. Reading lights are projected to grow at a 5.37% CAGR through 2031.

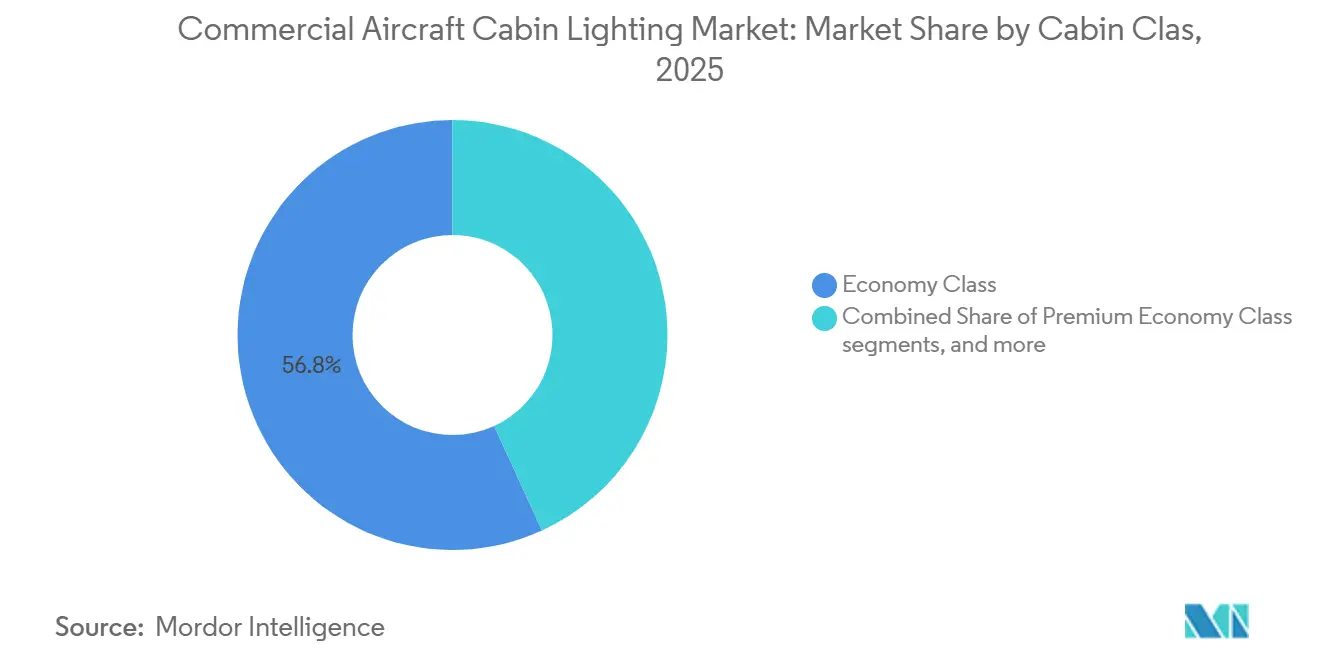

- By cabin class, economy installations accounted for 56.84% of 2025 revenue, whereas premium economy is forecast to grow at a 4.96% CAGR through 2031.

- By end user, OEM linefit held a 52.69% share in 2025, while aftermarket retrofits are projected to grow at a 5.48% CAGR through 2031.

- By geography, North America accounted for 39.45% of 2025 revenue; Asia-Pacific is forecast to grow at a 4.92% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Commercial Aircraft Cabin Lighting Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated narrowbody fleet expansion among LCCs | +0.8% | Asia-Pacific, Middle East, global spill-over | Medium term (2-4 years) |

| Retrofit wave toward LED mood-lighting for cabin refresh | +0.6% | North America, Europe, selective Middle East | Short term (≤ 2 years) |

| Shift from fluorescent to energy-efficient, RoHS-compliant LEDs | +0.5% | Europe, North America, Asia-Pacific | Long term (≥ 4 years) |

| IoT-enabled smart lights enabling predictive maintenance | +0.4% | North America, Europe, selective Asia-Pacific | Medium term (2-4 years) |

| Airline ESG targets favoring ultra-light photoluminescent floor paths | +0.3% | Europe, North America, global carriers with net-zero pledges | Long term (≥ 4 years) |

| Government stimulus for airport infrastructure upgrades post-COVID | +0.2% | US, European Union, select Asia-Pacific markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Accelerated Narrowbody Fleet Expansion Among LCCs

LCCs are purchasing narrowbodies at an unprecedented scale, as evidenced by flynas ordering 160 A320neo jets and IndiGo planning to reach a 400-aircraft fleet by 2027.[1]Airbus, “Aircraft Orders and Deliveries,” airbus.com Every new frame ships with linefit LED ceiling and wall arrays, cementing the commercial aircraft cabin lighting market as a beneficiary of the single-aisle boom. High-density seating magnifies weight-savings advantages because each kilogram trimmed compounds fuel burn over 25-year service lives. Suppliers face margin pressure when airlines bundle multiple cabin systems to secure volume discounts, yet volume stability offsets pricing stress. The resulting need for agile supply chains capable of synchronizing multiple final-assembly lines has become a decisive factor in vendor selection.

Retrofit Wave Toward LED Mood Lighting for Cabin Refresh

Airlines enhance cabin appeal through LED mood-lighting retrofits that cost 40% less than full refurbishments and can be completed within routine maintenance windows.[2]STG Aerospace, “Photoluminescent Emergency Lighting,” stgaerospace.com United’s B767-300ER Polaris program and Turkish Airlines’ fleet-wide liTeMood deployment showcase how RGB-tunable LEDs revitalize aging interiors without replacing seats or monuments. Retrofits also enable circadian-rhythm lighting on long-haul routes, elevating passenger comfort metrics to levels comparable to new widebody cabins. Concentrated in North America and Europe, the wave now spreads to the Gulf region, where Emirates couples LED kits with lie-flat seat upgrades. Intensifying retrofit activity raises aftermarket share, helping the commercial aircraft cabin lighting market withstand temporary OEM delivery shortfalls.

Shift from Fluorescent to Energy-Efficient, RoHS-Compliant LEDs

The European Union’s RoHS directive prohibits mercury-containing tubes after 2027, requiring complete LED conversions across the EU airspace.[3]European Commission, “RoHS Directive – Restriction of Hazardous Substances,” European Commission, ec.europa.eu LEDs consume roughly 50% less power and last five times longer than fluorescent strips, creating strong total-cost-of-ownership arguments beyond compliance. North American carriers, though not legally bound, voluntarily adopt RoHS-compliant products to cut maintenance expenses and avoid hazardous waste fees. China and other Asia-Pacific regulators mirror the policy on phased timelines, thereby unifying technical specifications and enabling vendors to scale standardized product lines. The sustainability halo bolsters airline ESG narratives, driving board-level budget approvals.

IoT-Enabled Smart Lights Enabling Predictive Maintenance

Embedding sensors in LED drivers transforms fixtures into data nodes that stream voltage, temperature, and lumen output, enabling maintenance planners to intervene before failures occur.[4]Collins Aerospace, “Cabin Interior Solutions,” collinsaerospace.com Airbus Skywise analytics shows unscheduled lighting events fall by 25% when IoT-ready PSUs populate the fleet. Diehl’s smart-cabin platform links lighting health to seat-occupancy sensors for granular fault isolation, reducing troubleshooting labor during A-checks. Airlines glean additional value by correlating lighting data with environmental variables such as humidity, enabling localized provisioning of spares and shaving 18% off inventory levels. Adoption concentrates in technologically mature markets where in-flight connectivity infrastructure already supports real-time data offload.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent widebody production backlog and delivery delays | -0.4% | North America, Europe, global spill-over | Medium term (2-4 years) |

| Lengthy STC certification cycles for novel lighting systems | -0.3% | Global, stricter in North America and Europe | Long term (≥ 4 years) |

| Supply-chain tightness for high-CRI LED chips and driver ICs | -0.3% | Asia-Pacific semiconductor hubs, global users | Short term (≤ 2 years) |

| Capital reallocation toward IFEC/connectivity over lighting | -0.2% | North America, Europe, selective Middle East carriers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Persistent Widebody Production Backlog and Delivery Delays

Spirit AeroSystems fuselage defects halted B787 output in 2024, extending average delivery delays by eight months and pushing linefit lighting revenue into later periods. Airbus likewise missed its A350 monthly target because Tier-2 suppliers struggled to supply pre-integrated lighting panels on time. OEM linefit accounted for 52.69% of 2025 revenue, so any disruption reverberates through vendor order books, eroding margins as fixed costs spread over fewer units. Delayed widebodies compel airlines to retain aging aircraft longer, partly offsetting the revenue gap through retrofit work but at lower per-aircraft prices. Narrowbody ramp-up moderately cushions the impact yet cannot fully neutralize deferred twin-aisle cash flows.

Lengthy STC Certification Cycles for Novel Lighting Systems

Securing a supplemental type certificate for new lighting solutions can take 12-24 months, with rigorous flammability and electromagnetic interference tests inflating R&D budgets. Smaller innovators struggle to fund repeated destruction of test articles, leading to a supply landscape dominated by incumbents who amortize certification costs across multiple programs. Parallel approval paths at the FAA and EASA remain partially harmonized, resulting in duplicate documentation for transatlantic fleets. While recent FAA guidance has shaved several weeks off specific photoluminescent approvals, complex RGB mood-lighting arrays still undergo the full compliance gauntlet. Protracted cycles slow innovation adoption and hinder rapid differentiation, mildly dragging the commercial aircraft cabin lighting market CAGR.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Aircraft Type: Widebody Growth Trails Narrowbody Dominance

Narrowbody aircraft accounted for 51.58% of the commercial aircraft cabin lighting market. Widebodies, though smaller today, are forecast to grow at a 5.81% CAGR through 2031, lifted by B787 backlog clearance and A350 production rises. Growth momentum also derives from retrofit campaigns on B777 and A330 platforms, where circadian-rhythm LEDs refresh passenger perception without costly structural changes. Regional jets secured a 12% share in 2025, aided by Embraer E2 deliveries featuring compact PSU modules tailor-made for tight cross-sections.

Standardized lighting packages dominate single-aisle linefit requests, keeping per-unit cost low and installation friction to a minimum. Nevertheless, airlines increasingly specify zonal brightness control to mimic widebody ambiance, a requirement that boosts driver-IC complexity and value-added revenue for vendors. Widebody retrofits in Gulf carriers illustrate how long-haul operators employ full RGB tunability as part of soft-product overhauls. Regional aircraft, conversely, require ultra-compact power supplies that meet the same electromagnetic criteria inside smaller overhead bins. This segment, therefore, favors niche suppliers capable of engineering miniature solutions, thereby diversifying the commercial aircraft cabin lighting market landscape.

By Light Type: Reading Lights Gain as Personalization Surges

Ceiling and wall fixtures accounted for 44.15% of the commercial aircraft cabin lighting market size. Reading lights will register the fastest CAGR at 5.37%, propelled by premium-economy expansion and passengers' desire for personal control. Each individually addressable LED spot reduces wiring mass by up to 30%, a tangible fuel-saving metric airlines can quantify in environmental disclosures. Signage lighting benefits from photoluminescent technology that eliminates electrical draw, while lavatory suites integrate micro-LED mirrors that double lumen output without enlarging the enclosure footprint.

The personalization wave is moving beyond business-class cabins into economy-plus cabins, prompting airlines to retrofit turnkey PSU units with three-axis reading-light adjustment. Growth in signage products remains steady because regulatory mandates fix installation counts, yet the switch to photoluminescent materials frees power budget for ambient effects elsewhere in the cabin. Floor-path strips, though a small revenue slice, offer strategic weight-reduction value and cross-sell opportunities for emergency signage packages. Altogether, light-type diversification enables suppliers to balance stable linefit volumes against higher-margin retrofit customizations.

By Cabin Class: Premium Economy Retrofit Surge Outpaces Economy Linefit

Economy accounted for 56.84% of revenue in 2025 due to dense single-aisle deliveries, yet premium-economy installations will grow at a 4.96% CAGR through 2031 as airlines monetize intermediate comfort tiers. Business class remains a technology sandbox where tunable white arrays replicate sunrise and dinner ambiance, but growth is decelerating because most widebodies already feature modern lie-flat seats. First-class suites occupy a niche 4% share, adopting OLED panels for indirect illumination only when ultra-long-haul branding justifies cost.

Retrofit economics favor premium economy because a seat-count boost comes bundled with new lighting to visually mark the zone. Airlines thereby unlock incremental ancillary revenue without compromising economy density. Business class retrofits focus on color-temperature modulation that synchronizes with meal-service timing. In the economy, price ceilings limit feature sets to basic dimmable LEDs, though modular PSUs keep upgrade pathways open. Across all cabins, ESG reporting pressures coax operators toward solutions that blend passenger comfort with power and weight savings, reinforcing the value proposition of advanced LED systems.

By End User: Aftermarket Gains as Fleet Age Extends Retrofit Windows

OEM linefit captured 52.69% of the 2025 value, anchored by robust A320neo and B737 MAX output, yet aftermarket demand is set to grow at a 5.48% CAGR because airlines now retain airframes beyond 20 years. Supplemental regulatory triggers, such as mandatory photoluminescent floor-path upgrades, often escalate to full cabin lighting refreshes during heavy checks. Retrofit kit suppliers differentiate through short installation times and STC portfolios spanning multiple airframe families, enabling operators to compress ground time to fewer than seven days.

Linefit negotiations yield volume-driven discounts but limit aesthetic customization, whereas aftermarket customers pay premium margins for branded color palettes and IoT capability. Life-cycle cost calculus often tips in favor of retrofitting because LED longevity reduces the need for subsequent maintenance, a feature airlines highlight in sustainability reports. As OEM backlogs persist, retrofit programs provide immediate cabin uplift, positioning the aftermarket as the growth engine of the commercial aircraft cabin lighting market over the medium term.

Geography Analysis

North America commanded a 39.45% share of the commercial aircraft cabin lighting market in 2025. United’s B767 Polaris and Delta’s A350 refresh anchor aftermarket momentum, and FAA stimulus grants indirectly spur component demand by scaling LED supply chains. A high average fleet age amplifies retrofit volumes as carriers stretch asset lifespans while waiting for newer narrowbodies. Canadian operators move cautiously, but WestJet’s B787 linefit orders sustain baseline growth. Mexican LCC fleets are taking delivery of A320neos equipped with factory LED cabins, reinforcing steady single-aisle throughput.

Asia-Pacific is forecast to post the swiftest 4.92% CAGR through 2031, powered by Air India’s USD 400 million dual-fleet retrofit and China’s C919 domestic-content policy that mandates indigenous LED supply. IndiGo’s record order book turns linefit deliveries into a multi-year tailwind, and Southeast Asian carriers like Vietjet and AirAsia bolster demand with high-utilization narrowbody fleets. Japanese full-service operators are integrating photoluminescent strips to meet national carbon-neutrality goals by 2030, tying sustainability to passenger-experience upgrades.

Europe maintained a 22% share in 2025, supported by Lufthansa’s Allegris B787-9 cabin, Air France’s A350 business-class revamp, and Iberia’s A321XLR deliveries carrying factory-installed PSU units. The RoHS mercury phase-out compels even cash-tight airlines to prioritize LED replacements before the 2027 deadline. Middle Eastern carriers collectively represented a 12% share; Emirates’ USD 3 billion B777 retrofit and Qatar Airways’ QSuite Next Gen program keep the region technologically advanced and supplier-diverse. South America and Africa contribute a modest 4% to the aggregate, with LATAM’s B787 upgrades and South African Airways’ A350 linefit serving as sporadic but valuable opportunities.

Competitive Landscape

Collins Aerospace (RTX Corporation), Safran SA, and Diehl Stiftung & Co. KG together held a majority of linefit contracts in 2025, leveraging integrated-cabin agreements with both Airbus and Boeing. Their regulatory credentials under the FAA and EASA Part 21 constitute formidable barriers to entry. Collins further entrenched its position by renewing a four-year Satair distribution pact that secures exclusive A320 family spare-parts channels. Safran is pursuing vertical integration into LED drivers to reduce dependence on a volatile semiconductor supply. Diehl continues to champion smart-cabin ecosystems that tie lighting to predictive-maintenance dashboards.

Niche players focus on retrofit agility. STG Aerospace’s saf-Tglo SSUL obtained dual approvals in 2024 and offers 70% weight savings, enabling carriers to report immediate fuel benefits in ESG disclosures. Astronics packages modular PSU kits that fit within C-check windows, while Luminator Technology Group enjoys a first-mover advantage in regional-jet installations. Emerging disruptors such as SCHOTT introduce fiber-optic solutions for ultra-luxury segments, though adoption remains narrow due to price. Competitive tactics, therefore, bifurcate: incumbents champion volume and breadth of compliance; challengers emphasize rapid customization, weight savings, and shorter certification cycles.

Strategic moves in 2025 illustrate divergent priorities. Collins unveiled a composite A320 Airspace PSU that slashes weight by 20% and adds USB-C charging, aligning with airlines’ sustainability and connectivity narratives. Safran rolled out an in-house driver IC line to buffer against chip shortages. STG’s blue-hued photoluminescent strip met customer requests for brand-aligned evacuation pathways. As connectivity budgets cannibalize traditional cabin-upgrade funds, lighting vendors increasingly tether proposals to measurable fuel savings and predictive-maintenance value-adds, ensuring enduring relevance.

Commercial Aircraft Cabin Lighting Industry Leaders

Safran SA

Collins Aerospace (RTX Corporation)

Diehl Stiftung & Co. KG

Astronics Corporation

SCHOTT AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Airbus announced plans to integrate the A350-1000 First Class Experience concept onboard the A350-1000. The concept features a 1-1-1 layout centered around a Master Suite for two passengers. The suite includes a double bed, a private lavatory and changing area, and a small bar. This offering is expected to create retrofit and linefit opportunities for airlines seeking to provide a premium experience to their First Class passengers.

- April 2025: Satair and Collins Aerospace announced a four-year extension of their distribution agreement for cabin interior components, which now also includes lighting solutions.

- March 2025: Diehl Aviation presented its advanced cabin illumination technologies at the AIX in Hamburg. These innovations, featuring accent lighting and high-quality materials, are designed to significantly enhance the passenger experience.

Global Commercial Aircraft Cabin Lighting Market Report Scope

Cabin lighting systems create a comfortable atmosphere for passengers and crew members. The study includes lighting solutions for aircraft cabins.

The commercial aircraft cabin lighting market is segmented based on aircraft type, light type, cabin class, end user, and geography. By aircraft type, the market is segmented into narrowbody, widebody, and regional jets. By light type, the market is segmented into reading lights, ceiling and wall lights, signage lights, lavatory lights, and floor-path lighting stripes. By cabin class, the market is segmented into first class, business class, premium economy class, and economy class. By end user, the market is segmented into OEM linefit and aftermarket/retrofit. The report also covers the market sizes and forecasts for the commercial aircraft cabin lighting market in major countries across different regions. For each segment, the market size is provided in terms of value (USD).

| Narrowbody Aircraft |

| Widebody Aircraft |

| Regional Jets |

| Reading Lights |

| Ceiling and Wall Lights |

| Signage Lights |

| Lavatory Lights |

| Floor-path Lighting Strips |

| First Class |

| Business Class |

| Premium Economy Class |

| Economy Class |

| OEM Linefit |

| Aftermarket/Retrofit |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| Qatar | ||

| United Arab Emirates | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Aircraft Type | Narrowbody Aircraft | ||

| Widebody Aircraft | |||

| Regional Jets | |||

| By Light Type | Reading Lights | ||

| Ceiling and Wall Lights | |||

| Signage Lights | |||

| Lavatory Lights | |||

| Floor-path Lighting Strips | |||

| By Cabin Class | First Class | ||

| Business Class | |||

| Premium Economy Class | |||

| Economy Class | |||

| By End User | OEM Linefit | ||

| Aftermarket/Retrofit | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Italy | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| Qatar | |||

| United Arab Emirates | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

How large will the commercial aircraft cabin lighting market be by 2031?

The commercial aircraft cabin lighting market size is expected to grow from USD 1.07 billion in 2025 to USD 1.12 billion in 2026, and is forecast to reach USD 1.34 billion by 2031, at a 3.70% CAGR over 2026-2031.

Which region shows the fastest growth in cabin lighting demand?

Asia-Pacific is expected to post a 4.92% CAGR through 2031, led by Indian and Chinese fleet programs.

What drives airlines to retrofit LED systems instead of full cabin overhauls?

LED mood-lighting retrofits cost 40% less, cut power draw by up to 60%, and can be installed during routine maintenance.

Why are photoluminescent floor-path strips gaining popularity?

They weigh 70% less than electroluminescent strips, need no power, and help airlines meet ESG weight-reduction targets.

How do IoT-enabled smart lights benefit maintenance operations?

Embedded sensors stream health data that reduce unscheduled lighting failures by about 25% when integrated with predictive-analytics platforms.

Which factor most constrains near-term deliveries?

Supply-chain and labor bottlenecks, including casting lead-times and skilled-worker shortages, currently delay all F-35 shipments and affect broader production schedules.

Page last updated on: