Combination Vaccines Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

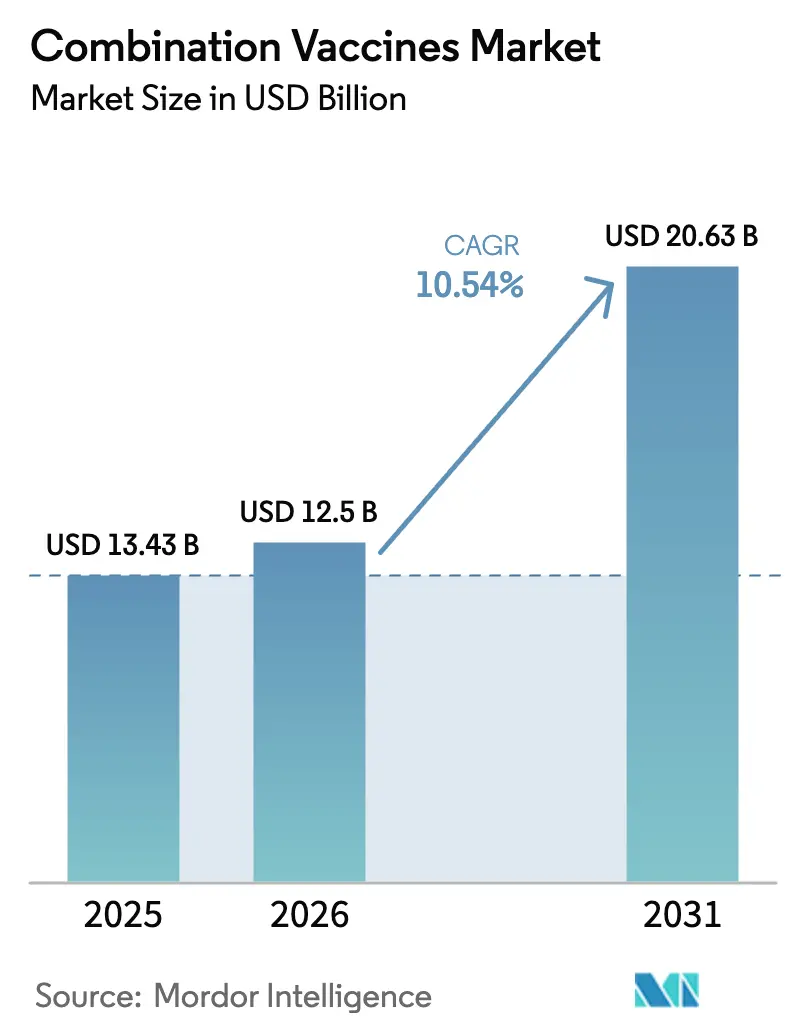

| Market Size (2026) | USD 12.5 Billion |

| Market Size (2031) | USD 20.63 Billion |

| Growth Rate (2026 - 2031) | 10.54% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Combination Vaccines Market Analysis by Mordor Intelligence

The Combination Vaccines Market is expected to grow from USD 13.43 billion in 2025 to USD 12.5 billion in 2026 and is forecasted to reach USD 20.63 billion by 2031 at 10.54% CAGR over 2026-2031.

Growing government focus on pandemic readiness, regulatory moves that privilege efficacy-proven multivalent products, and persisting gaps in routine immunization are steering the combination vaccines market toward double-digit growth. Manufacturers that master process scale-up for multi-antigen formulations now secure priority positions in national tenders, while payers view fewer clinic visits per patient as a direct cost-saver. Demand tailwinds include adult booster expansions, Asia-Pacific self-reliance programs, and new technologies, especially mRNA and protein-scaffold platforms that cut development timelines. Simultaneously, tightening U.S. and European trial requirements raises the capital threshold, limiting market entry to firms able to run large efficacy studies and maintain parallel quality-control streams for every component.

Key Report Takeaways

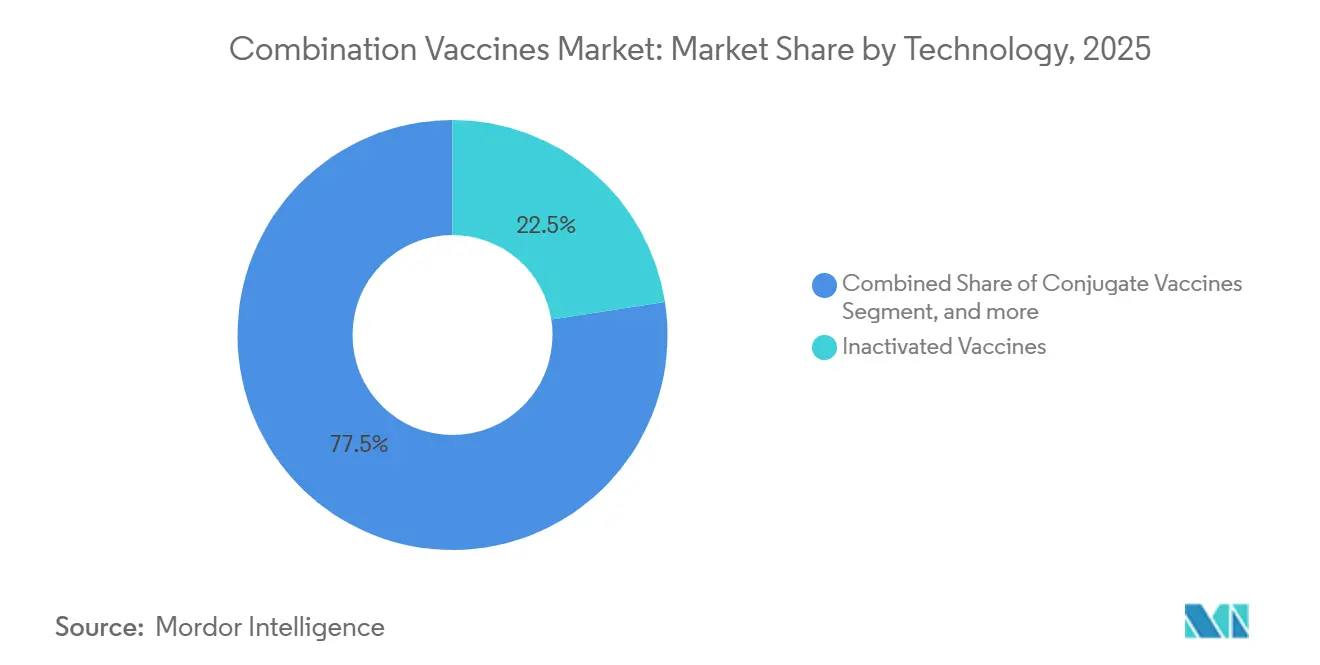

- By technology, inactivated vaccines led with 22.54% of the combination vaccines market share in 2025, whereas mRNA platforms are set to post the fastest 12.54% CAGR through 2031.

- By route of administration, parenteral products accounted for 42.54% of 2025 revenue, and oral vaccines are forecast to record a 12.77% CAGR through 2031.

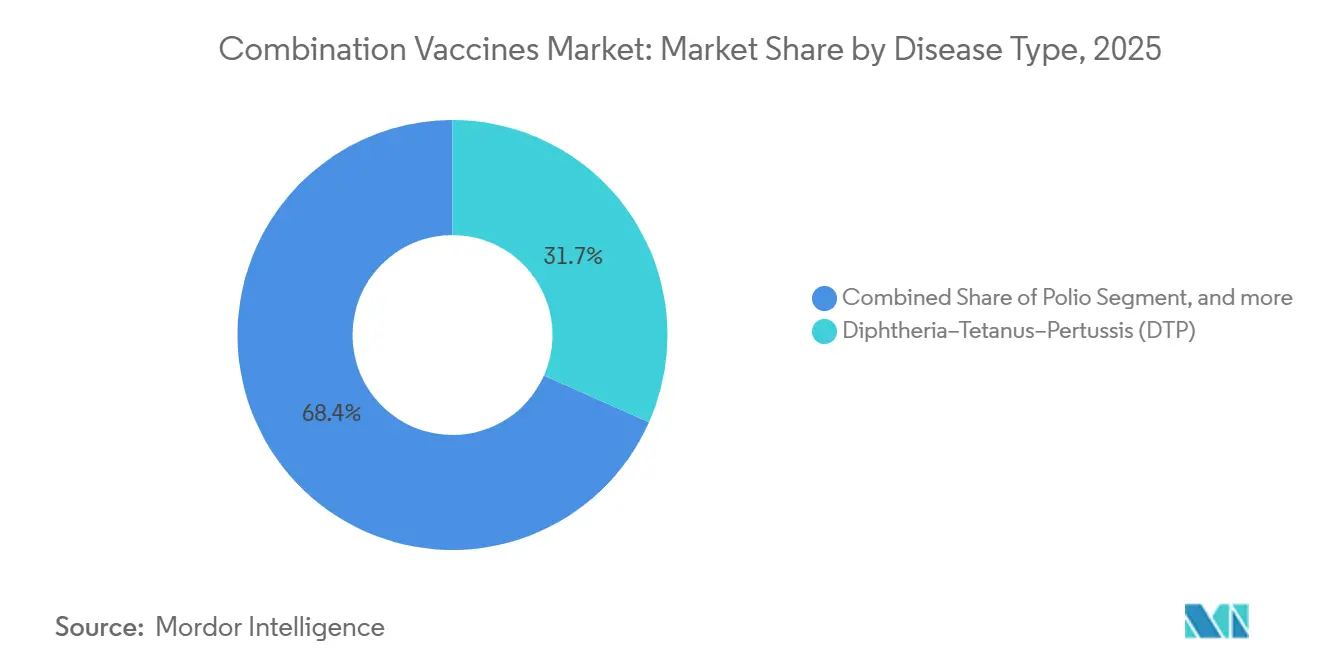

- By disease target, diphtheria-tetanus-pertussis combinations accounted for 31.65% of 2025 sales, while hepatitis B combinations are projected to grow at 13.67% CAGR through 2031.

- By end user, pediatric doses accounted for 51.43% of 2025 demand, while adult indications are poised for a 13.54% CAGR over the outlook period.

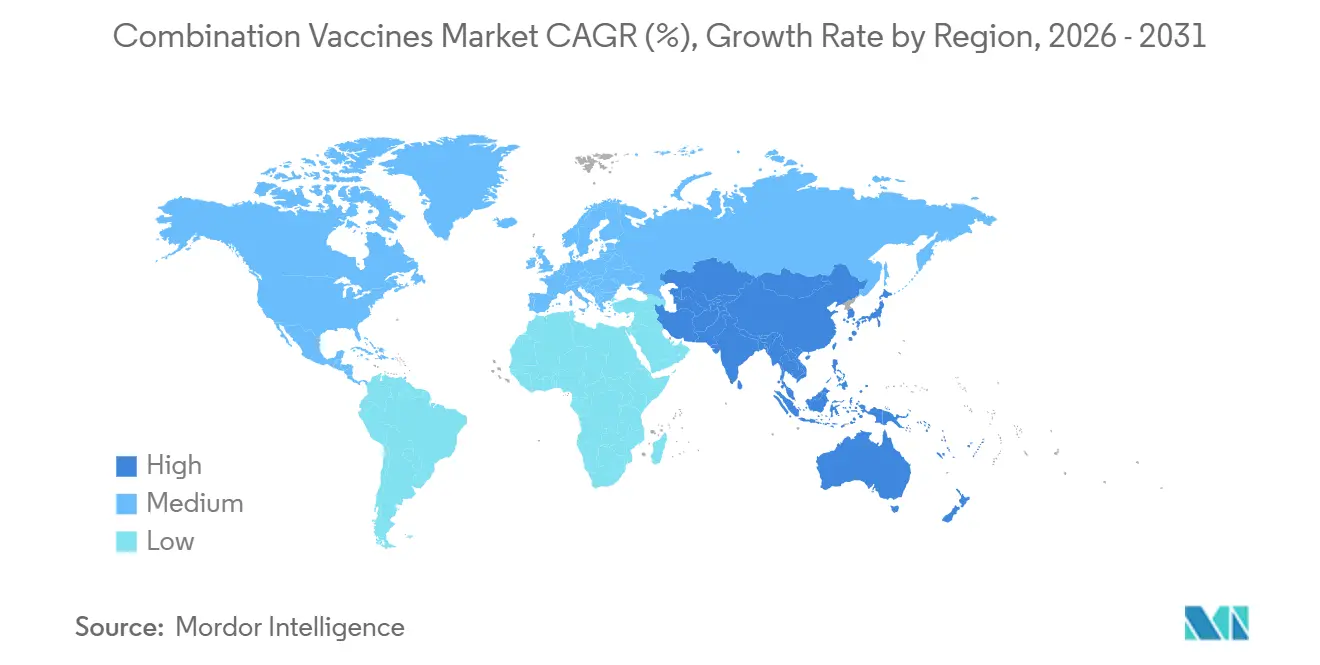

- By geography, North America captured 43.65% of 2025 revenue, and Asia-Pacific is expected to grow at a 11.54% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Combination Vaccines Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Burden of Vaccine-Preventable Diseases | +1.8% | Sub-Saharan Africa, South Asia, global spillover | Medium term (2-4 years) |

| Government-Sponsored Immunization Programs | +2.1% | North America, Europe, Gavi-eligible countries | Long term (≥4 years) |

| Advantages of Reduced Injection Burden | +1.3% | North America, Europe, urban Asia-Pacific | Short term (≤2 years) |

| Technological Advances in Multivalent Design | +1.9% | North America, Europe, Asia-Pacific production hubs | Medium term (2-4 years) |

| Adult Booster Schedule Expansion | +1.6% | North America, Europe, emerging Latin America | Medium term (2-4 years) |

| Stockpile Integration for Pandemic Response | +1.2% | Global, WHO and national security agencies | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Rising Burden of Vaccine-Preventable Diseases

Measles cases surged to 11 million in 2024 with 95,000 deaths, most in countries where DTP3 coverage dipped below 80%. The same surveillance confirmed 14.3 million zero-dose infants, a signal that complex multidose schedules strain fragile delivery systems. Multi-antigen vaccines consolidate up to six pathogens into a single vial, reducing cold-chain volume and clinic visits, thereby lowering dropout rates. Gavi has consequently shifted procurement toward pentavalent and hexavalent products, purchasing more than 2.5 billion combination doses between 2005 and 2024[1]WHO, “Measles and Rubella Surveillance Data,” who.int. China’s 2025 inclusion of a domestic 9-valent HPV shot in its program illustrates how high-burden settings are now adopting combination options to curb parallel disease threats while improving logistics.

Government-Sponsored Immunization Programs

The 2025 U.S. immunization schedule designates Vaxelis as the preferred hexavalent option for American Indian and Alaska Native infants, underpinning federal contracts worth USD 180 million per year. In Europe, the Health Emergency Preparedness and Response Authority (HERA) signed a 27.4 million-dose framework that obliges bidders to show modular combination capability for fast antigen swaps during outbreaks[2]European Commission, “HERA Vaccine Strategy,” europa.eu. India has approved 12 pentavalent and hexavalent products since 2009; yet only four secured state tenders, revealing that cost-effectiveness modeling, not licensure alone, unlocks public funding. Such policies increase the addressable volume for firms able to demonstrate both clinical value and per-dose savings.

Advantages of Reduced Injection Burden

GlaxoSmithKline’s PENMENVY, cleared by the FDA in February 2025, folds five meningococcal serogroups into one injection for adolescents, eliminating the previous two-shot regimen FDA. Advisory Committee modeling shows the single-visit approach saves USD 1.4 million per U.S. birth cohort in direct costs and averts additional invasive cases. Hexavalent pediatric vaccines approved in 2025 lowered infant needle sticks from 10 to 7 before age 2, and trial data linked the reduction to a 23% improvement in series completion rates. Lower injection counts also curb clinic congestion, an operational win for providers absorbing post-pandemic patient backlogs.

Technological Advances in Multivalent Design

GlaxoSmithKline’s Multiple Antigen Presenting System attaches polysaccharides to a protein scaffold via non-covalent bonds, allowing rapid addition or removal of serotypes without revalidating every conjugation chemistry step. The architecture halves cycle time—from 18 months to roughly 9—for next-generation pneumococcal candidates. Moderna’s mRNA-1010 delivered superior influenza A immunity in 2024 Phase III trials, yet its COVID-19–flu combo (mRNA-1083) missed influenza B targets and was withdrawn in May 2025, underscoring the immune-interference hurdle when stacking RNA transcripts. Regulatory agencies now insist on antigen-specific analytics for every component, raising costs and complexity while pushing the field toward platform-level innovation that streamlines future updates.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Development and Manufacturing Complexity | -1.4% | North America, Europe, global GMP-intensive facilities | Medium term (2-4 years) |

| Stringent and Differing Regulatory Requirements | -1.1% | Global, FDA-EMA-WHO pathway fragmentation | Long term (≥4 years) |

| Limited Antigen Compatibility in Novel Platforms | -0.8% | North America, Europe, mRNA and viral-vector pipelines | Medium term (2-4 years) |

| Supply Chain Strain From Multi-Antigen Testing | -0.9% | Asia-Pacific, Latin America bottlenecks | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

High Development and Manufacturing Complexity

Each pentavalent formula can require more than 40 validated release assays, compared with roughly 12 for a monovalent vaccine, magnifying labor and capital demands. Merck’s USD 1 billion Durham build-out added eight dedicated sterile lines for its U.S. hexavalent product, illustrating the scale needed to meet good-manufacturing-practice standards. GlaxoSmithKline’s 2024 expansion in Pennsylvania experienced an 18% yield loss during scale-up due to protein-scaffold aggregation, delaying the launch by 9 months. Even with the FDA’s Advanced Manufacturing Technologies designation, only three combination facilities qualified by late 2025, showing how steep the technical curve remains.

Stringent and Differing Regulatory Requirements

The FDA now calls for randomized placebo-controlled efficacy trials for healthy-population combination vaccines, adding up to two years and USD 200 million to development budgets. The EMA caps acceptable immune-titer reductions at 10%, versus 20% in the United States, forcing dual trial designs and inflating costs[3]European Medicines Agency, “Lessons Learned From COVID-19,” ema.europa.eu. WHO prequalification demands stability data for each antigen across multiple temperatures, creating dossiers that exceed 50,000 pages. India’s CDSCO timelines span 14-48 months depending on domestic bridging data, adding uncertainty for manufacturers targeting that high-volume market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: mRNA Platforms Disrupt Legacy Conjugate Dominance

In 2025, inactivated products accounted for 22.54% of the combination vaccine market, underpinned by decades-old DTP-IPV combinations adopted worldwide. Conjugate vaccines remain essential for pneumococcal and Hib protection, yet they face a valency ceiling near 20 serotypes because each polysaccharide requires a separate conjugation step. GlaxoSmithKline’s protein-scaffold approach breaks that barrier, enabling a 24-valent candidate already in Phase II trials. mRNA contenders, although accounting for a small base today, are forecast to post a 12.54% CAGR through 2031, reflecting investor confidence that process automation and antigen-swap speed outweigh immune-interference hurdles once dosing strategies mature.

Competitive signals suggest a future in which the combination vaccines market divides between high-volume pediatric conjugates and fast-iterating mRNA adult boosters. Live attenuated vaccines, constrained by cold-chain limits, retain niche roles in MMR and varicella regimens. Recombinant protein and toxoid technologies are being reformulated into lower-reactogenicity acellular DTaP blends. Viral-vector combinations remain in early development, partly because regulators require extensive vector-immunity data to mitigate risks of booster attenuation.

By Route of Administration: Oral Vaccines Gain Ground in Eradication Campaigns

Parenteral shots accounted for 42.54% of 2025 revenue; however, oral formulations are projected to expand at a 12.77% CAGR, buoyed by rotavirus and polio programs that require community-level reach without syringes. WHO prequalified four oral rotavirus vaccines by late 2024; injectable contenders fell behind after PATH’s subunit candidate missed Phase III futility thresholds. BARDA’s Beyond the Needle initiative is channeling funds into oral, intranasal, and patch delivery, positioning these routes as contingency tools for future outbreaks.

Oral polio vaccine still underpins eradication drives in Afghanistan and Pakistan, yet IPV-based hexavalent blends are the future standard once circulating vaccine-derived strains disappear. Intranasal influenza vaccines, while popular among children, currently struggle when combined with COVID-19 antigens because mucosal competition reduces neutralizing titers by one-third, dampening regulatory enthusiasm. Transdermal patches, though accounting for only about 1% of sales today, offer compelling cold-chain savings and may feed into emergency stockpiles once dose-stability hurdles are cleared.

By Disease Target: Hepatitis B Combinations Surge on Adult Mandates

Diphtheria-tetanus-pertussis formulations secured 31.65% of 2025 revenue, anchoring infant schedules on every continent. Hepatitis B blends, however, are forecast to grow at 13.67% CAGR, the fastest among disease clusters, after the CDC recommended universal adult hepatitis B vaccination in 2022. That guideline instantly expanded the eligible U.S. cohort by 110 million people, driving a run-up in Twinrix demand and prompting developers to explore hepatitis B pairing with pneumococcal or influenza antigens.

Polio combinations will accelerate once the Global Polio Eradication Initiative completes its oral-to-IPV transition, opening space for hexavalent constructs containing IPV. Measles-mumps-rubella-varicella volumes climbed in 2024 catch-up campaigns across 23 nations responding to measles resurgence. HPV combinations gained a policy tailwind when China offered free domestic 9-valent doses to 13-year-old girls in 2025, foreshadowing HPV-hepatitis pairings that cut clinic visits in adolescence.

By End-User: Adult Uptake Accelerates from a Smaller Base

Pediatric programs still accounted for 51.43% of 2025 doses, yet adult indications are set to grow faster at a 13.54% CAGR, propelled by booster schedule expansions and workplace mandates in healthcare, food handling, and eldercare. The adult combination vaccines market size remains modest today, but projected U.S. volumes could top 500 million doses annually by 2032 if current adherence trends continue. The gap between recommended injections and tolerated needle sticks makes multivalent solutions a practical necessity for seniors managing multiple chronic conditions.

Provider economics can occasionally hamper uptake; administering a combination product may reimburse less than billing separately for influenza, pneumococcal, and COVID-19 vaccines in a single visit. Stakeholders, therefore, advocate new payment codes that mirror pediatric administration fees. On the pediatric side, the CDC’s 2025 schedule listing Vaxelis as the preferred hexavalent option for certain Native American populations underscores how health equity goals steer procurement toward combination formats that reduce visit counts and injection-site reactions.

Geography Analysis

North America generated 43.65% of 2025 revenue, reflecting early adoption of pentavalent meningococcal and hexavalent pediatric products as well as high per-capita pricing. PENMENVY’s 2025 launch cut adolescent visits in half and saved USD 1.4 million per birth cohort, strengthening payer confidence in multivalent value propositions. U.S. manufacturers also benefit from priority review vouchers and large-scale federal contracts that de-risk capital investments in dedicated multi-antigen lines.

Asia-Pacific is positioned to be the fastest-growing region, advancing at 11.54% CAGR through 2031. Domestic suppliers in India and China who win WHO prequalification can underprice imports by 40%–50% in Gavi tenders, improving access while nurturing local industry. China’s free 9-valent HPV program, launched nationwide in October 2025, signals policy momentum toward combination formats that cut cold-chain burden and clinic congestion. India’s Serum Institute and Bharat Biotech, armed with IPV technology transfers, aim to export pentavalent offerings to 70-plus Gavi countries by leveraging low-cost stainless-steel fermenters and syrup-pack filling lines.

Europe maintains a steady share aided by HERA’s 27.4 million-dose pandemic framework that mandates combination-ready capacity. The region’s new Vaccine Hub, funded with EUR 102 million until 2029, views multivalent formulations as modular building blocks for surge production. Pricing dynamics vary: Germany caps cost-effectiveness at EUR 50,000 per QALY, whereas France allows EUR 80,000, prompting staggered launch tactics. Latin America and the Middle East rely heavily on PAHO revolving funds and Gavi support to secure pentavalent vaccine supplies, yet cold-chain gaps and lab backlogs lead to intermittent stock-outs that constrain uptake. Africa’s share remains demand-constrained but poised for upside if pledged donor funds materialize for adult hepatitis B and HPV rollouts.

Competitive Landscape

The top four producers—GlaxoSmithKline, Sanofi, Pfizer, and Merck—accounted for an estimated 60% of global revenue in 2025, indicating a moderately concentrated market. They defend pediatric franchises through heavy capital commitments: GlaxoSmithKline earmarked USD 30 billion over five years to scale its protein-scaffold pneumococcal line, while Merck invested USD 1 billion in Durham to secure hexavalent capacity. Pfizer channels mRNA know-how toward next-wave adult boosters after COVID-19 windfalls, and Sanofi leverages long-standing conjugate expertise to enter tender bids with bundled discount options.

India’s Serum Institute and Bharat Biotech, along with China’s Sinovac and Walvax, are eroding price points in Gavi markets by offering WHO-prequalified pentavalent vaccines at USD 0.90 per dose ex-works, roughly half multinational benchmarks. Modern disruptors center on platform flexibility: Valneva’s CEPI-funded chikungunya-dengue combo aims at endemic belts where dual-pathogen overlap justifies a single vial, and Takeda is co-developing dengue formulations with Biological E for South Asian deployment by 2027.

The adult combination space remains a white field: only Tdap currently enjoys mainstream use. Moderna’s 2025 setback with mRNA-1083 affirmed regulatory insistence on full efficacy evidence for every antigen; nevertheless, speed advantages continue to draw investor capital toward RNA platforms. Patent filings at the European Patent Office confirm a shift to scaffold-based conjugates that slash cycle times and promise 24-valent or higher constructs, potentially reshaping pneumococcal standards within five years.

Combination Vaccines Industry Leaders

GlaxoSmithKline (GSK)

Sanofi

Pfizer, Inc.

Merck & Co.

Serum Institute of India

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Moderna withdrew the mRNA-1083 COVID-19–influenza combo application after FDA requested placebo-controlled efficacy data.

- February 2025: GlaxoSmithKline secured FDA approval for PENMENVY, a five-serogroup meningococcal vaccine that replaces separate MenACWY and MenB shots for adolescents.

- December 2024: The US Food and Drug Administration granted Fast Track designation to two Sanofi combination vaccine candidates to prevent influenza and COVID-19 infections in individuals aged 50 and older. Both candidates combine two already licensed and authorized vaccines with proven efficacy through from randomized controlled studies and e tolerability.

Global Combination Vaccines Market Report Scope

As per the scope of the report, combination vaccines are vaccines that protect against multiple diseases with a single injection. They contain antigens for two or more pathogens, reducing the number of shots needed. This approach improves vaccination compliance and convenience.

The Combination Vaccines Market is Segmented by Technology (Conjugate, Inactivated, Live Attenuated, mRNA, Recombinant, Toxoid, and Viral-Vector), Route of Administration (Oral, Parenteral, and Other), Disease Target (DTP, Polio, Hib, Hepatitis B, MMR, Varicella, Influenza, HPV, COVID-19 & Influenza Combo, and Other), End-User (Adult and Paediatric), and Geography (North America, Europe, Asia-Pacific, MEA, and South America). The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Conjugate Vaccines |

| Inactivated Vaccines |

| Live Attenuated Vaccines |

| mRNA Vaccines |

| Recombinant Vaccines |

| Toxoid Vaccines |

| Viral-Vector Vaccines |

| Oral |

| Parenteral |

| Other Route of Administrations |

| Diphtheria–Tetanus–Pertussis (DTP) |

| Polio |

| Haemophilus Influenzae Type B |

| Hepatitis B |

| Measles–Mumps–Rubella (MMR) |

| Varicella |

| Influenza |

| Human Papillomavirus (HPV) |

| COVID-19 & Influenza Combo |

| Other Disease Combinations |

| Adult Vaccines |

| Paediatric Vaccines |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest Of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest Of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest Of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest Of South America |

| By Technology | Conjugate Vaccines | |

| Inactivated Vaccines | ||

| Live Attenuated Vaccines | ||

| mRNA Vaccines | ||

| Recombinant Vaccines | ||

| Toxoid Vaccines | ||

| Viral-Vector Vaccines | ||

| By Route Of Administration | Oral | |

| Parenteral | ||

| Other Route of Administrations | ||

| By Disease Target | Diphtheria–Tetanus–Pertussis (DTP) | |

| Polio | ||

| Haemophilus Influenzae Type B | ||

| Hepatitis B | ||

| Measles–Mumps–Rubella (MMR) | ||

| Varicella | ||

| Influenza | ||

| Human Papillomavirus (HPV) | ||

| COVID-19 & Influenza Combo | ||

| Other Disease Combinations | ||

| By End-User | Adult Vaccines | |

| Paediatric Vaccines | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest Of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest Of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest Of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest Of South America | ||

Key Questions Answered in the Report

How large is the combination vaccines market in 2026 and where is it heading by 2031?

It stands at USD 12.50 billion in 2026 and is expected to reach USD 20.63 billion by 2031, reflecting a 10.54% CAGR.

Which technology segment is growing fastest?

MRNA-based formulations are projected to rise at a 12.54% CAGR through 2031 as platform speed and modularity attract investment.

Why are oral combination vaccines gaining attention?

Oral delivery supports polio and rotavirus eradication campaigns by removing needle use, simplifying logistics, and improving uptake in low-resource settings.

What is driving adult demand for combination vaccines?

Expanded CDC booster schedules and workplace immunization mandates are lifting adult uptake, with a forecast 13.54% CAGR to 2031.

Which region offers the highest growth potential?

Asia-Pacific is set to grow at 11.54% CAGR, driven by domestic manufacturing, WHO prequalification wins, and national program expansions in China and India.

How are regulators influencing product development timelines?

FDA and EMA now require full efficacy trials and component-specific analytics for multivalent products, adding up to two years and significant cost to approval pathways.

Page last updated on: