Colustrum Supplements Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 4.01 Billion |

| Market Size (2031) | USD 5.51 Billion |

| Growth Rate (2026 - 2031) | 6.58% CAGR |

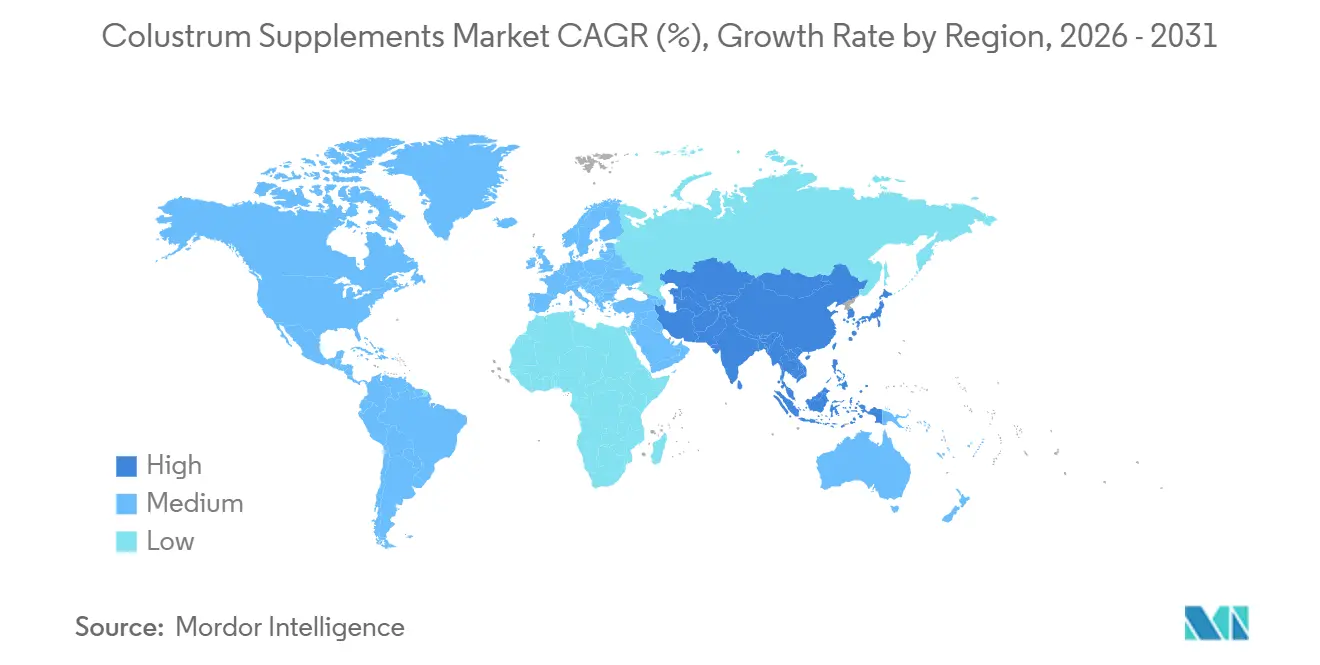

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

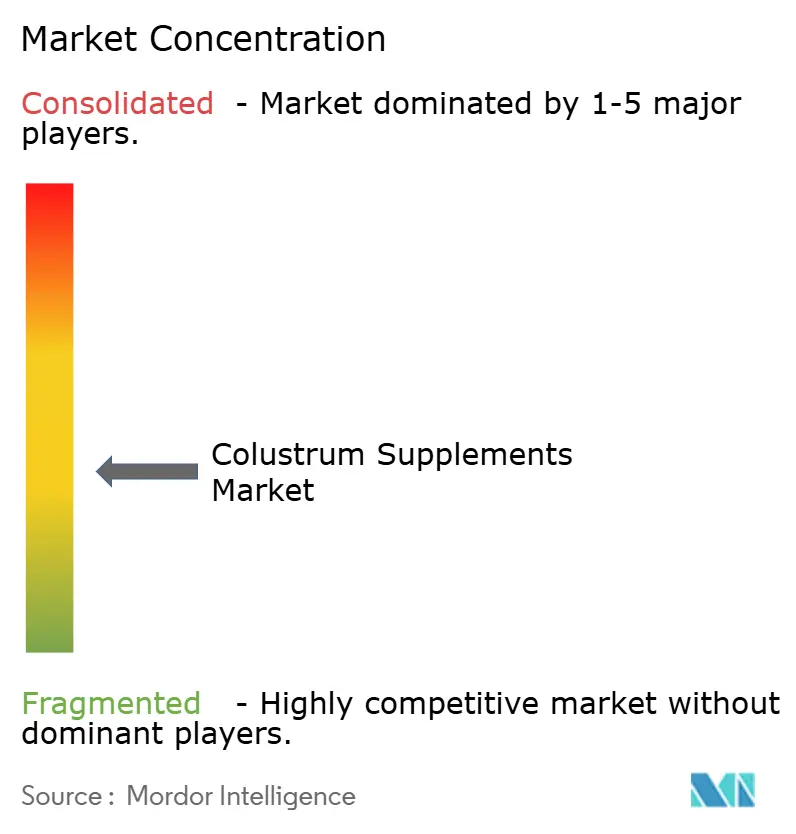

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Colustrum Supplements Market Analysis by Mordor Intelligence

The global colostrum supplements market was valued at USD 3.80 billion in 2025 and is estimated at USD 4.01 billion in 2026, projected to reach USD 5.51 billion by 2031, at a CAGR of 6.58% during the forecast period. Market growth is driven by rising consumer focus on preventive healthcare, immune system support, and gut health, along with increasing adoption of personalized nutrition and sports nutrition products. Additional growth factors include growing demand for clean-label, naturally derived bioactive ingredients, advancements in low-temperature processing technologies that preserve immunoglobulins and growth factors, and expanding product availability through online retail and specialty health stores.

Key Report Takeaways

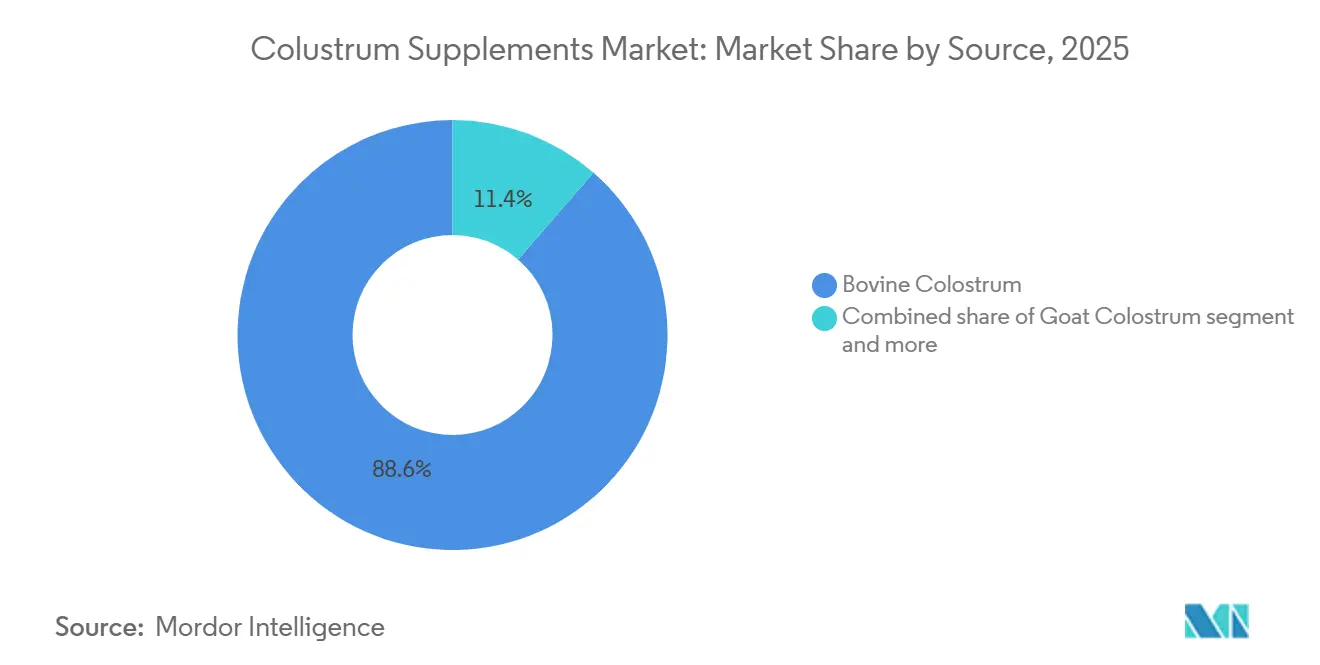

- By source, bovine colostrum held 88.61% share in 2025, while goat colostrum is projected to grow at a 7.32% CAGR from 2026 to 2031.

- By form, powder accounted for 47.82% share in 2025, while gummies are forecast to expand at an 8.03% CAGR from 2026 to 2031.

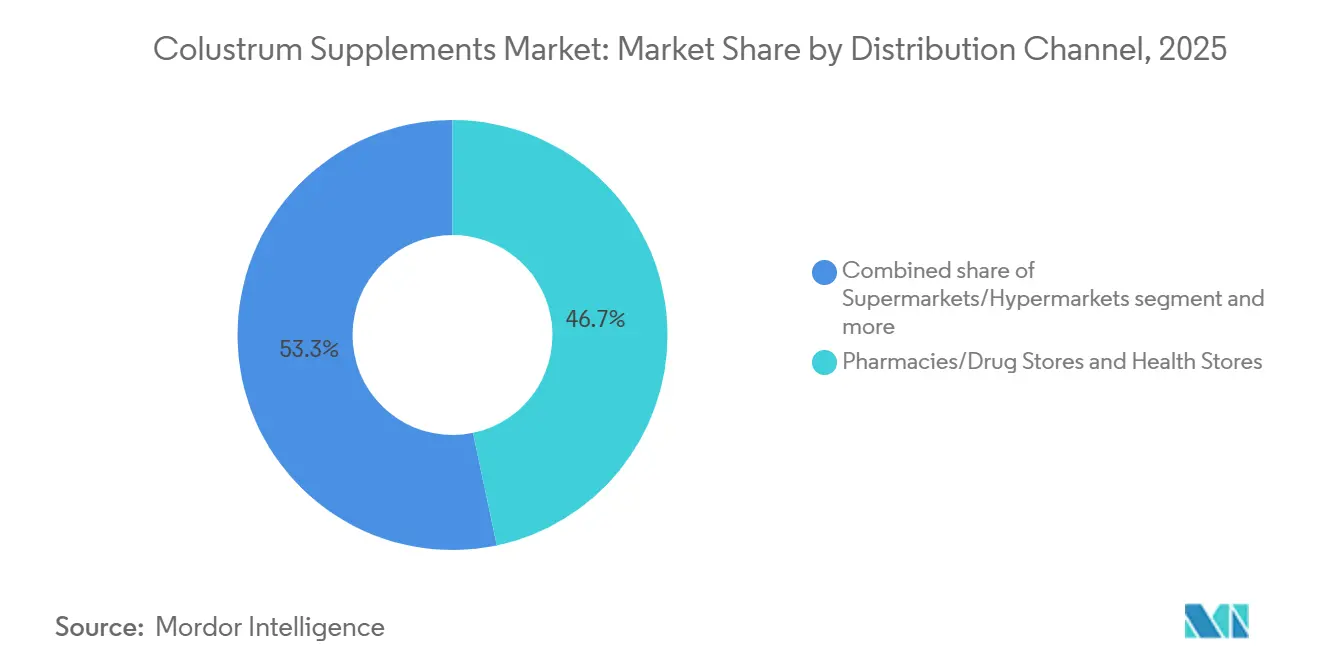

- By distribution channel, pharmacies, drug stores, and health stores captured 46.71% share in 2025, while online retail stores are expected to register the fastest growth at an 8.51% CAGR through 2031.

- By geography, North America represented 36.91% share in 2025, while Asia-Pacific is projected to grow at the highest 7.87% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Colustrum Supplements Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Consumer focus on immune health and disease prevention | +1.5% | Global | Short term (≤ 2 years) |

| Rising adoption of sports nutrition and muscle recovery supplements | +1.2% | North America, Europe and Asia-Pacific | Medium term (2–4 years) |

| Demand for clean-label and naturally derived nutritional supplements | +1.0% | North America and Europe | Medium term (2–4 years) |

| Growth of personalized nutrition and preventive healthcare trends | +0.8% | Global, with early gains in North America and China | Long term (≥ 4 years) |

| Advancements in low-temperature processing and bioactive ingredient preservation | +0.5% | Global | Medium term (2–4 years) |

| Expanding scientific research on bioactive compounds in colostrum | +0.7% | North America, Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Consumer focus on immune health and disease prevention

Growing consumer focus on immune health and disease prevention is a key driver of the global colostrum supplements market. Consumers are increasingly seeking naturally derived nutritional products that support immune resilience and overall wellness. Colostrum contains bioactive compounds such as immunoglobulins, lactoferrin, proline-rich polypeptides, and growth factors, which are widely recognized for their role in supporting immune function, making it an attractive ingredient in preventive health regimens. The increasing prevalence of immune-related disorders has further strengthened demand for supplements that help maintain immune balance. According to the Sjögren's Foundation, more than 50 million Americans, approximately 8% of the United States population, were affected by autoimmune diseases in 2025, highlighting the growing need for nutritional interventions that support immune health [1]Source: Sjögren's Foundation, "The Rise of Autoimmune Diseases", sjogrens.org. This increasing consumer emphasis on proactive wellness and long-term immune support continues to accelerate the adoption of colostrum supplements worldwide.

Rising adoption of sports nutrition and muscle recovery supplements

Rising adoption of sports nutrition and muscle recovery supplements is driving the global colostrum supplements market, as athletes, fitness enthusiasts, and physically active consumers increasingly seek natural ingredients that support recovery, muscle repair, and exercise performance. Colostrum is valued for its rich content of growth factors, immunoglobulins, amino acids, and bioactive proteins that help support post-exercise recovery, maintain muscle integrity, and promote gut health during periods of intense physical activity. The growing popularity of strength training, endurance sports, and recreational fitness has encouraged manufacturers to incorporate colostrum into sports nutrition formulations. According to the Health Fitness Association (HFA), 81 million Americans belonged to a gym, studio, or other fitness facility in 2025, reflecting the expanding base of consumers regularly participating in structured fitness activities [2]Source: Health Fitness Association (HFA), "81 Million Americans Were Members of a Fitness Facility in 2025, New HFA Report Finds", healthandfitness.org/. This sustained increase in fitness participation is driving demand for scientifically supported recovery supplements, reinforcing the growth of colostrum-based sports nutrition products.

Demand for clean-label and naturally derived nutritional supplements

Growing demand for clean-label and naturally derived nutritional supplements is driving the global colostrum supplements market. Consumers increasingly prefer products formulated with recognizable, minimally processed, and naturally sourced ingredients. Colostrum aligns with the clean-label movement as it is a naturally occurring dairy-derived ingredient rich in immunoglobulins, lactoferrin, growth factors, and bioactive proteins, without relying on synthetic additives for its core nutritional benefits. Manufacturers are responding by introducing formulations with transparent ingredient lists, free-from claims, and minimal processing techniques that preserve the natural bioactive profile of colostrum. This shift toward ingredient transparency and natural wellness has encouraged the development of premium colostrum supplements that meet consumer expectations for safe, traceable, and scientifically supported nutritional products, thereby supporting market growth.

Growth of personalized nutrition and preventive healthcare trends

The growth of personalized nutrition and preventive healthcare trends is a significant driver of the global colostrum supplements market, as consumers increasingly shift from reactive treatment to proactive health management through tailored nutritional solutions. Rather than adopting generic supplements, individuals are seeking ingredients that align with their specific health objectives, such as strengthening immune function, maintaining digestive health, supporting healthy aging, and enhancing overall wellness. Colostrum is well positioned within this trend due to its naturally occurring immunoglobulins, lactoferrin, growth factors, and bioactive peptides, which offer multiple physiological benefits in a single ingredient. The growing integration of digital health platforms, microbiome analysis, genetic testing, and biomarker-based wellness assessments is further encouraging consumers to select targeted nutritional products based on their personal health profiles.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory restrictions on health and therapeutic claims | -1.0% | United States, Europe, Canada | Short term (≤ 2 years) |

| Supply constraints due to limited colostrum collection window | -0.8% | Global | Long term (≥ 4 years) |

| Limited clinical evidence supporting certain health claims | -0.6% | North America and Europe | Medium term (2–4 years) |

| Ethical concerns regarding calf nutrition and animal welfare | -0.5% | Europe, North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Regulatory restrictions on health and therapeutic claims

Regulatory restrictions on health and therapeutic claims are a key restraint for colostrum supplement manufacturers. Although colostrum contains bioactive compounds associated with immune and gut health, companies are generally prohibited from making claims that their products diagnose, treat, cure, or prevent diseases without regulatory approval. Compliance with labeling regulations, claim substantiation requirements, and advertising standards lengthens product development timelines and raises compliance costs. In the United States, the Food and Drug Administration (FDA) regulates dietary supplement claims under 21 CFR 101.93, which permits only specific structure/function claims accompanied by the required disclaimer and prohibits unapproved disease claims for dietary supplements. These regulatory restrictions create marketing challenges for colostrum supplement manufacturers and can slow broader consumer adoption despite growing scientific interest in the ingredient.

Supply constraints due to limited colostrum collection window

Supply constraints arising from the limited colostrum collection window represent a significant restraint for the global colostrum supplements market. Colostrum is produced only during the first few milkings after calving, which naturally restricts the availability of raw material. Collection must be carefully managed to ensure newborn calves receive adequate colostrum for their nutritional and immune needs before any surplus can be directed toward commercial use. This narrow harvesting period limits production scalability and makes raw material availability highly dependent on herd management practices, calving schedules, and animal health. Additionally, manufacturers must adhere to strict quality controls during collection, processing, and storage to preserve the bioactivity of immunoglobulins, lactoferrin, growth factors, and other sensitive proteins, which further reduces usable yields.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source: Bovine Dominance Persists as Goat Colostrum Builds a Differentiated Niche

Bovine colostrum accounted for 88.61% of the colostrum supplements market in 2025, maintaining its dominant position due to its rich concentration of naturally occurring bioactive compounds and its well-established commercial production infrastructure. Its high levels of immunoglobulins, lactoferrin, growth factors, proline-rich polypeptides, and essential nutrients make it the most extensively utilized and scientifically recognized source of colostrum for nutritional formulations. Standardized collection during the initial post-calving period, combined with advanced low-temperature processing and freeze-drying technologies, enables manufacturers to preserve the biological activity of these sensitive compounds while ensuring consistent product quality. The availability of large-scale dairy supply chains, rigorous quality control protocols, and traceability systems further supports reliable sourcing and year-round production.

Goat colostrum is the fastest-growing source segment, projected to expand at a CAGR of 7.32% from 2026 to 2031, driven by increasing consumer preference for alternative dairy-derived bioactive ingredients with high nutritional value and perceived digestive compatibility. The segment is benefiting from growing interest in minimally processed, naturally sourced supplements that retain immunoglobulins, lactoferrin, growth factors, and other functional proteins. Advances in specialized collection, preservation, and low-temperature drying technologies are improving the stability and quality of goat colostrum while maintaining its bioactive profile. Manufacturers are also investing in standardized production methods and quality assurance practices to enhance consistency and strengthen consumer trust. The expanding availability of premium goat milk production systems and increasing research into the nutritional composition of goat colostrum are supporting the development of differentiated formulations.

By Form: Powder Anchors the Market as Gummies Redefine the Growth Frontier

Powder accounted for 47.82% of the colostrum supplements market in 2025, retaining its leading position due to its excellent stability, longer shelf life, and ability to preserve heat-sensitive bioactive compounds during processing. Powder formulations allow manufacturers to maintain high concentrations of immunoglobulins, lactoferrin, growth factors, and other functional proteins while offering flexibility in dosage and formulation. The format is also well suited for large-scale production, efficient storage, and convenient transportation due to its lower moisture content and reduced risk of microbial degradation. Advances in freeze-drying and low-temperature spray-drying technologies have further improved bioactive retention and product quality, while enhanced solubility and mixing characteristics have increased manufacturing efficiency.

Gummies represent the fastest-growing format, projected to expand at a CAGR of 8.03% from 2026 to 2031, driven by rising consumer preference for convenient and easy-to-consume supplement formats. Manufacturers are increasingly utilizing advanced formulation technologies to incorporate colostrum bioactives into gummies while preserving ingredient stability, taste, and texture. Continuous innovation in sugar-free formulations, natural flavors, clean-label ingredients, and plant-based gelling agents has broadened their appeal among health-conscious consumers. Improved packaging, portion-controlled servings, and enhanced product portability further support daily supplementation and consumer adherence. As brands continue to diversify their product portfolios with gummy formulations that combine convenience with premium nutritional value, this format is expected to experience the strongest growth in the colostrum supplements market.

By Distribution Channel: Pharmacies Anchor Trust While Online Channels Drive Acquisition

Pharmacies, drug stores, and health stores accounted for 46.71% of the colostrum supplements market in 2025. This dominance is rooted in the professional credibility these retail channels provide for scientifically formulated nutritional supplements. Consumers frequently rely on pharmacies and specialized health stores for products that emphasize ingredient quality, authenticity, and safety, making them preferred purchase points for colostrum supplements. These channels also provide guidance on dosage, ingredient composition, and product suitability, which supports purchasing decisions for bioactive nutritional products. Additionally, the extensive retail footprint of pharmacy chains and health stores ensures broad product availability and visibility. According to the United States Census Bureau, retail sales at pharmacy and drug stores in the United States reached approximately USD 33.6 billion in May 2025, highlighting the strong commercial importance of this distribution channel for health and wellness products [3]Source: United States Census Bureau, "Monthly retail sales of pharmacies and drug stores in the United States", census.gov.

Online retail stores are the fastest-growing distribution channel, projected to expand at a CAGR of 8.51% from 2026 to 2031. This growth is driven by increasing consumer preference for convenient purchasing, wider product selection, and direct access to premium nutritional brands. Digital platforms enable consumers to compare formulations, review ingredient transparency, access educational content, and evaluate customer feedback before making purchasing decisions. Subscription services, personalized product recommendations, and recurring delivery options are further improving customer retention and encouraging regular supplement use. Manufacturers are also strengthening their digital presence through direct-to-consumer websites and major e-commerce platforms, enabling faster product launches and more targeted consumer engagement. I

Geography Analysis

North America held 36.91% of the colostrum supplements market in 2025, maintaining its dominant position due to the region's well-established nutraceutical industry, high consumer awareness of preventive healthcare, and strong acceptance of scientifically formulated dietary supplements. The market benefits from advanced dairy ingredient processing technologies, rigorous quality assurance standards, and continuous innovation in bioactive nutritional products. A well-developed distribution network spanning pharmacies, health stores, specialty nutrition retailers, and e-commerce platforms ensures broad product accessibility. Increasing demand for clean-label, naturally sourced, and clinically supported supplements continues to drive premium product development, further strengthening North America's position in the global colostrum supplements market.

Asia-Pacific is the fastest-growing region in the global colostrum supplements market, projected to expand at a CAGR of 7.87% from 2026 to 2031. Growth is driven by the rapid expansion of the nutraceutical industry, increasing consumer awareness of preventive wellness, and growing demand for functional nutritional products. Manufacturers across the region are investing in advanced processing technologies, bioactive ingredient preservation, and premium supplement formulations to meet evolving consumer expectations. The expansion of organized retail, digital commerce platforms, and specialty nutrition stores has significantly improved product accessibility. Continuous innovation in clean-label formulations and high-quality dairy-derived ingredients is supporting broader market penetration, collectively positioning Asia-Pacific as the fastest-growing regional market during the forecast period.

Europe holds one of the largest regional positions in the global colostrum supplements market, supported by a strong preventive healthcare culture, stringent product quality standards, and widespread consumer acceptance of food supplements. According to the European Self-Care Industry Association (AESGP), 62% of Europeans used food supplements daily in 2025, reflecting the region's mature supplement consumption habits. South America is experiencing steady growth as awareness of functional nutrition and naturally derived wellness products continues to increase, supported by improving retail infrastructure and expanding availability of premium supplements. The Middle East and Africa is also emerging as a promising market, driven by rising demand for high-quality nutritional products, expanding pharmacy and specialty health store networks, and increasing consumer focus on immunity, preventive healthcare, and overall wellness.

Competitive Landscape

The global colostrum supplements market is moderately fragmented, with competition characterized by a mix of multinational nutrition companies, established nutraceutical manufacturers, and specialized colostrum-focused brands. Companies compete on product quality, bioactive ingredient concentration, processing technologies, clean-label positioning, and scientific validation rather than price alone. Manufacturers continue to invest in low-temperature processing, freeze-drying, and ingredient standardization technologies to preserve immunoglobulins, lactoferrin, and growth factors while ensuring consistent product quality. Major participants include PanTheryx, Inc., NOW Foods, Glanbia PLC, Nestlé S.A., and Sovereign Laboratories, each leveraging strong manufacturing capabilities, brand recognition, and distribution networks to expand their global presence.

Alongside established players, direct-to-consumer (DTC)-first brands are reshaping the competitive landscape by building subscriber communities through social media engagement, influencer collaborations, educational content, and digital wellness platforms before expanding into traditional retail channels. These brands increasingly utilize subscription-based purchasing models, personalized customer experiences, and transparent ingredient sourcing to improve customer retention and lifetime value. Digital-first marketing strategies also enable faster product launches, real-time consumer feedback, and efficient brand building, allowing emerging companies to compete effectively with larger incumbents despite having smaller retail footprints.

A notable emerging competitive trend is the rise of AI-driven proteomics and precision nutrition companies, which are utilizing artificial intelligence, advanced protein analytics, and bioinformatics to better characterize colostrum's bioactive compounds and optimize ingredient standardization. These companies are accelerating research into protein profiling, biomarker identification, and bioactive preservation to develop next-generation formulations with improved consistency and targeted nutritional benefits. The integration of AI into ingredient discovery, quality control, and formulation development is expected to enhance product differentiation, support scientific substantiation, and drive innovation across the global colostrum supplements market, creating new competitive dynamics alongside traditional nutraceutical manufacturers.

Colustrum Supplements Industry Leaders

-

Pantheryx, Inc.

-

NOW Foods

-

Glanbia PLC

-

Nestle S.A.

-

Sovereign Laboratories

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Caldic announced a new partnership with Maolac, a biotechnology company developing a class of clinically backed, colostrum-based ingredients inspired by the natural benefits of human breast milk. Under this collaboration, Caldic will market and distribute Maolac's portfolio across the North American nutrition market.

- November 2025: Lemme unveiled its latest products in gut health and beauty, formulated with colostrum, including Lemme Colostrum Gummies and Lemme Colostrum Liposomal Liquid.

- January 2025: Vital Proteins launched Vital Proteins Colostrum Capsules. Made from naturally sourced bovine colostrum derived from U.S. cows, this product is designed to support gut health and immune function.

Global Colustrum Supplements Market Report Scope

Colostrum supplements are concentrated, powdered or capsule versions of the first pre-milk fluid produced by mammals after birth. The colostrum supplements market is segmented by source, form, distribution channel, and geography. Based on source, the market is segmented into bovine colostrum, goat colostrum, buffalo colostrum, and others. Based on form, the market is segmented into capsules and tablets, powder, gummies, and others. Based on distribution channel, the market is segmented into supermarkets/hypermarkets, pharmacies/drug stores and health stores, online retail stores, and other distribution channels. Based on geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and Middle East and Africa. The report provides market size and forecasts in both value (USD) and volume (tons) for all the mentioned segments.

| Bovine Colostrum |

| Goat Colostrum |

| Buffalo Colostrum |

| Others |

| Capsules and Tablets |

| Powder |

| Gummies |

| Others |

| Supermarkets/Hypermarkets |

| Pharmacies/Drug Stores and Health Stores |

| Online Retail Stores |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | |

| Middle East and Africa |

| By Source | Bovine Colostrum | |

| Goat Colostrum | ||

| Buffalo Colostrum | ||

| Others | ||

| By Form | Capsules and Tablets | |

| Powder | ||

| Gummies | ||

| Others | ||

| By Distribution Channel | Supermarkets/Hypermarkets | |

| Pharmacies/Drug Stores and Health Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | ||

| Middle East and Africa | ||

Key Questions Answered in the Report

What is the current and projected size of the colostrum supplements market?

The colostrum supplements market was valued at USD 3.80 billion in 2025, stands at USD 4.01 billion in 2026, and is projected to reach USD 5.51 billion by 2031 at a 6.58% CAGR.

Which source segment leads the colostrum supplements market?

Bovine colostrum led the market with 88.61% share in 2025 because of its established supply chain, scale, and strong clinical positioning.

Which source segment is growing the fastest?

Goat colostrum is the fastest-growing source segment, with a projected 7.32% CAGR from 2026 to 2031.

Which product form holds the largest share?

Powder held the largest share at 47.82% in 2025 due to its formulation flexibility, dose delivery, and cost efficiency.

Page last updated on: