Colombia Corrugated Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

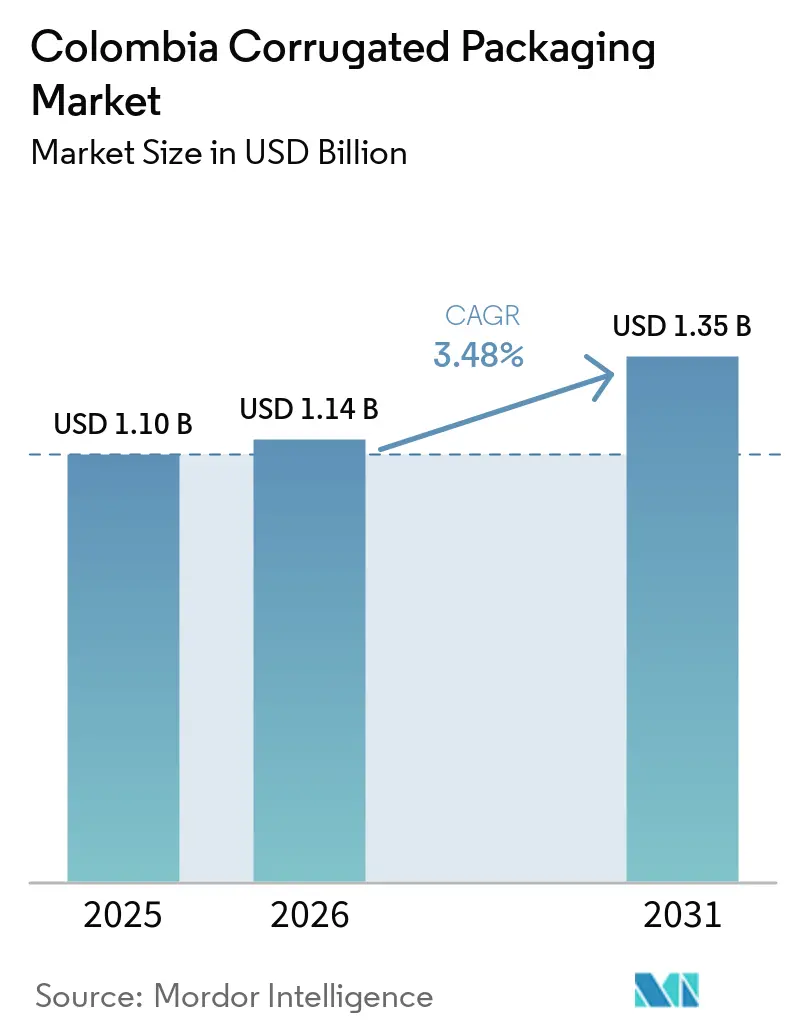

| Base Year Market Size (2025) | USD 1.10 Billion |

| Market Size (2026) | USD 1.14 Billion |

| Market Size (2031) | USD 1.35 Billion |

| Growth Rate (2026 - 2031) | 3.48% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Colombia Corrugated Packaging Market Analysis by Mordor Intelligence

The Colombia corrugated packaging market size is projected to be USD 1.10 billion in 2025, USD 1.14 billion in 2026, and reach USD 1.35 billion by 2031, growing at a CAGR of 3.48% from 2026 to 2031. Colombia’s gradual pivot from commodity grades to value-added formats is driven by e-commerce, export agriculture, and regulatory incentives that favor fiber-based substrates over single-use plastics. Recycled linerboard dominance anchors cost competitiveness, while semi-chemical fluting upgrades improve stacking strength without adding weight. Digital printing and die-cutting shorten lead times for custom shippers, enhancing brand presence in omnichannel retail. Investments in biomass boilers and bagasse-based medium highlight the race to decarbonize production and diversify fiber sources, cushioning the Colombia corrugated packaging market against recycled-paper volatility. Competitive intensity remains moderate as four integrated players hold a clear scale advantage yet face nimble digital-native converters in short-run niches.

Key Report Takeaways

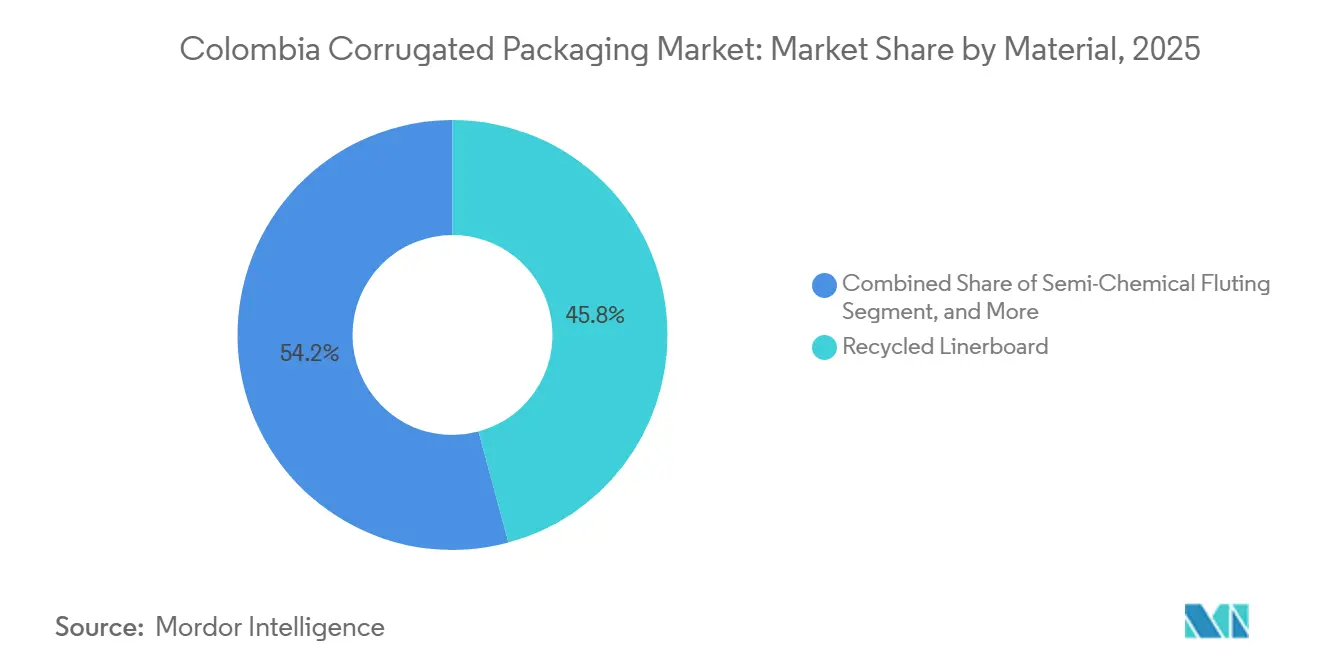

- By material, recycled linerboard captured 45.81% of the Colombia corrugated packaging market share in 2025.

- By flute type, the Colombia corrugated packaging market size for the E flute segment is forecast to advance at a 4.69% CAGR through 2031.

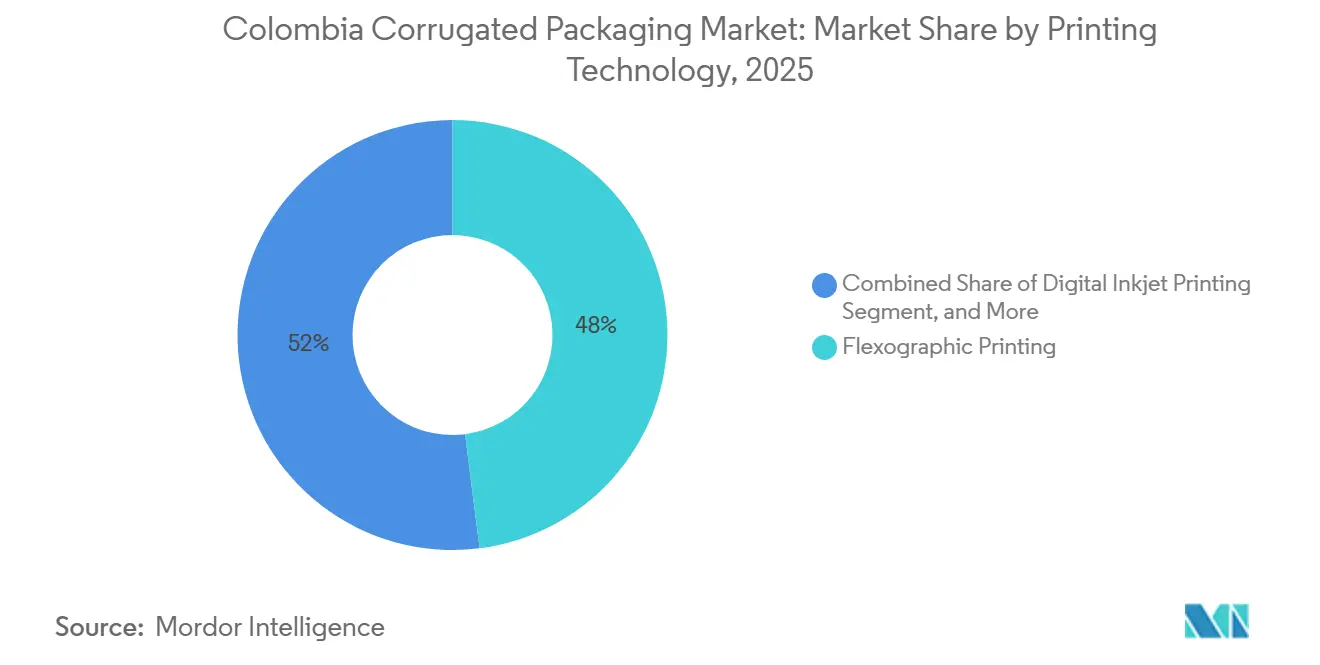

- By printing technology, flexographic printing captured 47.99% of the Colombia corrugated packaging market share in 2025.

- By packaging wall type, the Colombia corrugated packaging market size for the triple-wall formats segment is forecast to advance at a 4.32% CAGR through 2031.

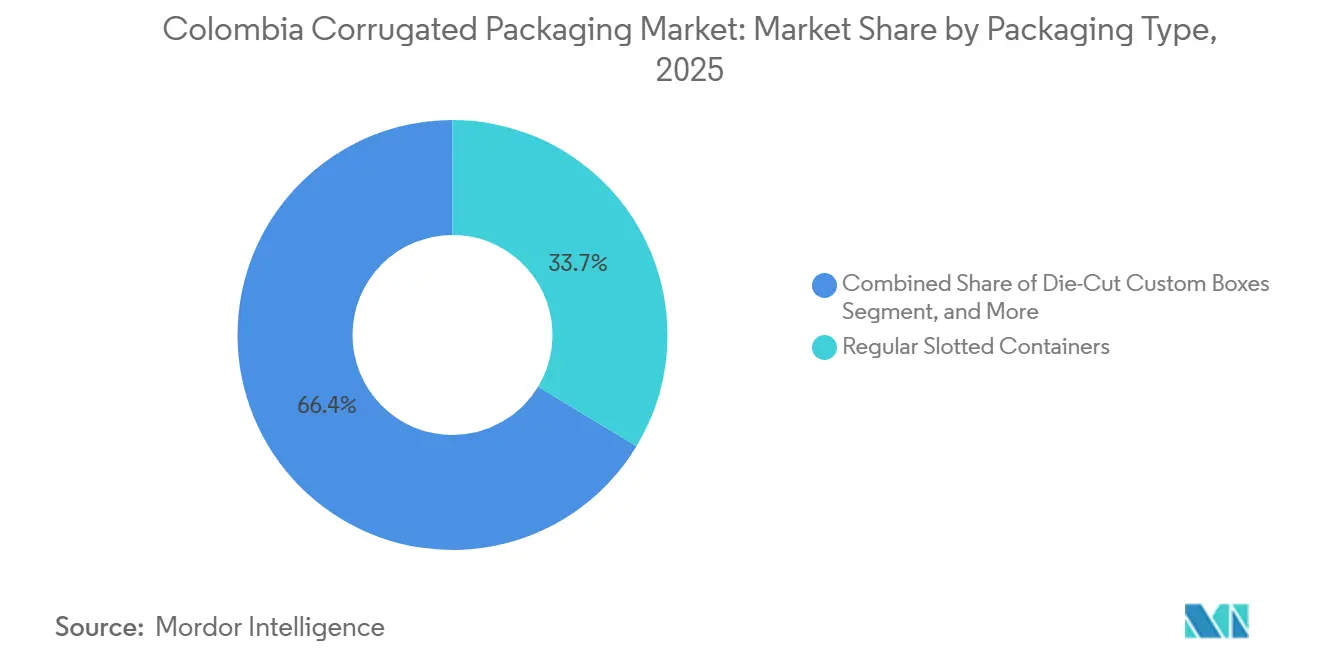

- By packaging type, regular slotted containers captured 33.65% of the Colombia corrugated packaging market share in 2025.

- By end-user, the Colombia corrugated packaging market size for the e-commerce fulfillment centers segment is forecast to advance at a 5.25% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Colombia Corrugated Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Boom in E-Commerce and Last-Mile Delivery | +1.20% | National, especially Bogotá, Medellín, Cali | Short term (≤ 2 years) |

| Expansion of Processed Food and Beverage Sectors | +0.90% | National, led by Sabana de Bogotá and Valle del Cauca | Medium term (2-4 years) |

| Government Tax on Single-Use Plastic Packaging | +0.70% | National, strongest in major municipalities | Medium term (2-4 years) |

| Demand for Lightweight Export-Grade Produce Boxes | +0.50% | Valle del Cauca, Antioquia, Cundinamarca | Long term (≥ 4 years) |

| Cold-Chain Growth in Floriculture Requiring Moisture-Resistant Boxes | +0.40% | Sabana de Bogotá, Rionegro | Medium term (2-4 years) |

| Near-Shoring of Electronics Assembly Driving Specialty Inserts | +0.30% | Bogotá free-trade zones, Barranquilla, Cartagena | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Boom in E-Commerce and Last-Mile Delivery

Rising urban internet adoption pushed Colombian digital commerce to COP 105.4 trillion (USD 0.0261 trillion) in 2024, a 26.7% jump that lifted parcel volumes in Bogotá, Medellín, and Cali.[1]Colombian Chamber of Electronic Commerce, “E-Commerce in Colombia 2024 Report,” ccec.org.co Couriers now demand right-sized shippers that fit delivery lockers, driving custom die-cut formats with pre-creased score lines that cut packing times by 30%. Fulfillment centers increasingly specify E flute liners that balance printability with cube efficiency. Smurfit WestRock opened a digital print service bureau in Bogotá in 2025, offering variable-data graphics that turn the shipper into a marketing asset. As omnichannel retailers ship from store inventory, smaller branded cartons gain traction, expanding the addressable pool for the Colombia corrugated packaging market.

Expansion of Processed Food and Beverage Sectors

Packaged-food retail sales reached USD 13.7 billion in 2023 amid lifestyle shifts toward ready-to-eat meals. Global brands consolidate suppliers and demand Forest Stewardship Council certification, pushing smaller box plants to invest in chain-of-custody audits. Beverage producers are moving from shrink-wrapped trays to fully enclosed corrugated cases that improve warehouse stacking and curb plastic use. Carvajal Empaques’ bagasse-based medium targets this shift, offering an 8%-12% raw-material saving compared with imported kraft pulp. These dynamics widen the opportunity for high-graphics litho-laminated cases that elevate shelf presence in modern trade, further energizing the Colombia corrugated packaging market.

Government Tax on Single-Use Plastic Packaging

Law 2232 of 2022 and Resolution 0803 of 2024 levy escalating taxes on single-use plastics, prompting quick-service chains to replace clamshells with corrugated take-out boxes.[2]Ministry of Environment and Sustainable Development, “Resolution 0803 of 2024,” minambiente.gov.co Demand surged by an estimated 18,000 metric tons in 2025 as enforcement tightened in major cities. Cartones America installed an aqueous-dispersion line that delivers grease-resistant coatings compliant with food-contact rules, gaining first-mover access to foodservice accounts. Although unit costs remain above flexible plastics, consumer perception of fiber-based sustainability strengthens brand loyalty, reinforcing long-term volume gains for the Colombia corrugated packaging market.

Demand for Lightweight Export-Grade Produce Boxes

Fresh fruit exports grew 37.5% in value during the first four months of 2025, with avocados and gooseberries requiring ventilated die-cut boxes that preserve cold-chain airflow.[3]Ministry of Agriculture and Rural Development, “Agricultural Export Statistics April 2025,” agricola.gov.co Converters swap C flute for B or E flute to minimize freight surcharges while maintaining edge-crush targets. Smurfit WestRock’s Guarne plant added precision rotary die-cutters with 1 millimeter registration, reducing spoilage by 8% during ocean transit. Higher box prices are offset by lower waste and enhanced phytosanitary compliance, stimulating specialty-grade demand within the Colombia corrugated packaging market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in Recycled Paper Prices | -0.60% | National, acute in Bogotá and Medellín | Short term (≤ 2 years) |

| Competition from Flexible Plastic Packaging | -0.40% | National, strongest in processed-food and personal-care segments | Medium term (2-4 years) |

| Scarcity of Domestic Virgin Fiber | -0.30% | National, affecting specialty-grade producers | Long term (≥ 4 years) |

| High Inter-Regional Logistics Costs | -0.20% | Andean and Pacific regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatility in Recycled Paper Prices

Antidumping tariffs of 18%-30% on Brazilian recycled linerboard tightened domestic supply and lifted prices 22% in 2024. Margins narrowed for non-integrated plants lacking long-term fiber contracts, forcing short shutdowns in Valle del Cauca. Smurfit Westrock’s USD 100 million biomass boiler, commissioned in 2024, trimmed energy bills by 15% and cushioned input cost swings.[4]Smurfit Kappa Group, “Guarne Plant Modernization,” smurfitkappa.com Price instability deters capital spending by smaller converters, slowing modernization across parts of the Colombia corrugated packaging market.

Competition from Flexible Plastic Packaging

Litoplas expanded rotogravure capacity 25% in 2025, promoting pouches that cost 30%-40% less per unit than paper-based shippers. While corrugated converters test hybrid film-lined boxes, added complexity limits adoption. Regulatory exemptions for food-contact films further shield polymers, especially in snacks and instant coffee. Unless barrier coatings become cost competitive, plastics will continue to siphon volumes from price-sensitive segments of the Colombia corrugated packaging market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Recycled Fiber Anchors Cost, Semi-Chemical Fluting Climbs

Recycled linerboard commanded 45.81% of the Colombia corrugated packaging market share in 2025, reflecting mature urban collection networks and tariff barriers that discourage virgin imports. Converters favor recycled grades for general-purpose boxes because the cost per ton trails virgin kraft by 12%, shielding margins when peso depreciation inflates imported pulp costs. Semi-chemical fluting, though pricier, is growing at a 4.19% CAGR by replacing recycled medium in export produce cartons that require superior edge crush in humid holds. Virgin Kraft linerboard stays confined to pharmaceutical and baby-food packs, where European migration limits require certified pulp. Corrugating-medium margins remain thin, so mills push light-weighting to 120 g while targeting additive packages that boost ring-crush thresholds.

Carvajal Empaques’ bagasse-fiber pilot, on-stream since mid-2025, promises feedstock diversification and an 8%-12% raw-material savings benchmarked to imported kraft, therefore appealing to multinational beverage clients chasing scope-3 reductions. Integrated mills explore enzymatic de-inking to upgrade recovered white ledger into top liner, potentially trimming chemical demand by 15%. The INVIMA guide issued in January 2026 raises analytical testing frequency for heavy metals, pushing uncertified imports out of food-contact channels. Specialty coatings using bio-resin barriers are gaining early adoption among dairy exporters seeking wax-free melon cartons acceptable in U.S. composting streams. Accelerated adoption of lower-basis-weight boards aligns with carrier incentives that penalize dimensional mass, cementing low-grammage dominance inside the Colombia corrugated packaging market.

By Flute Type: E Flute Extends Reach Into Premium Graphics

B flute held 38.21% of the Colombian corrugated packaging market size in 2025, underpinning canned-food, beverage, and general industrial runs where cushioning outranks graphics. E flute edges forward at a 4.69% CAGR, driven by cosmetics, personal care, and OTC pharma brands that appreciate its thin profile and litho-quality surface. Retail shelf facings shrink when suppliers switch from B to E, freeing space for line extensions and prompting retailers to prefer thinner carriers during range reviews. Hybrid B/E double-wall, pioneered by Smurfit Westrock’s technical center, merges B’s crush resistance with E’s print surface, expanding eligibility in e-commerce shippers.

A flute’s bulky cushioning retains appliance and chemical-drum niches, yet shares slips as triple-wall B/C/B surpasses required drop-test thresholds at lower tare. C flute, once the workhorse of export cartons, yields to B flute variants that cut freight weight by 8% on avocado shipments to Rotterdam. The flute, with a 0.8 millimeter caliper, gains luxury-goods traction, with foil and spot-UV embellishments headline the unboxing ritual. Adhesive formulators such as Henkel and H.B. Fuller released low-temperature starch blends in 2024 that shorten set times by 20%, mitigating warp on lightweight E and F liners. As premium graphics migrate beyond metropolitan malls into digital shopping baskets, thin-caliper flutes capture incremental orders, reinforcing upward mix progression in the Colombian corrugated packaging market.

By Packaging Type: Die-Cut Custom Boxes Outpace Commodity RSCs

Regular slotted containers accounted for 33.65% of the Colombia corrugated packaging market in 2025, owing to standardized footprints that are suited for conveyorized packing lines in beverage plants. Yet die-cut custom boxes advance at a 4.17% CAGR because e-commerce sellers value void-minimized dimensions that lower filler material and dimensional-weight penalties. Short-run digital layouts enable brand-specific graphics per promotion and even per consumer, driving higher perceived value with marginal ink cost. Folding cartons converge with micro flute corrugated when litho-laminated sheets bridge rigidity and shelf presence for consumer electronics.

Pallet boxes for mangoes and pineapples are upgraded to grower-specific die cuts with laser-etched QR codes that support phytosanitary traceability along the cold chain. Point-of-purchase displays, though sub-5% volume, deliver double-digit gross margins and ride supermarket expansion in Medellín suburbs. Tetra Pak’s mid-2025 alliance with local converters to co-supply aseptic carton outers illustrates a hybrid approach, with moisture-barrier inner walls preserving pack integrity on milk lines. Integrated mills have refined slitter-scorer automation so changeovers complete in under 7 minutes, underpinning profitable small orders that previously bypassed the Colombia corrugated packaging market.

By Wall Type: Single-Wall Dominates, Triple-Wall Finds Heavy-Duty Niches

Single-wall constructions captured 51.27% of the Colombia corrugated packaging market share in 2025 as 32-ECT offerings meet performance targets for most processed food, beverage, and apparel shipments. Converter focuses on adhesive spread optimization allowed down-gauging to 130 g m-2 facings without compromising compression. Double-wall boards remain a mid-strength staple for glass-jar and detergent bottle cases, while premium produce exporters are shifting to single-wall B flute with corner posts, saving 6% on box cost.

Triple-wall demand, set to climb 4.32% CAGR, aligns with near-shored PCB and appliance exports that need >55 psi edge-crush to survive sea freight stacking heights. Smurfit WestRock added a triple-wall corrugator in Guarne late 2024, advertising cycle-time parity with double-wall runs. Anti-static PE foams laminated to inner walls protect integrated circuits bound for Central American assembly plants. Single-face corrugated resurfaces in furniture plants that wrap scratch-prone lacquer panels, substituting for expanded polystyrene sheets now taxed under environmental levies. Regulatory foresight that positions corrugated as a recyclable void-fill accentuates single-wall cost-effectiveness and sustains hierarchy within the Colombia corrugated packaging market.

By Printing Technology: Flexo Holds Volume, Digital Inkjet Scales Fast

Flexographic presses delivered 47.99% share of the Colombia corrugated packaging market size in 2025 by supporting long-run trays for soda and beer clusters. Water-based ink formulation meets city VOC regulations, safeguarding access to urban factories. Digital inkjet gallops at 5.11% CAGR as fulfillment centers commission campaign-specific art in runs below 5,000 units. Variable data such as lottery codes and personalization feeds incremental brand engagement, with minimal plate-change delays.

Grafix Digital’s Highcon system, installed Q1-2025, lasers crease lines without metal tooling, compressing prototype lead time to eight hours and attracting beauty startups that iterate seasonal designs. Litho-laminated sheets carry metallic and holographic finishes onto B/E double walls for smartphone launches. Screen printing stays niche, accenting point-of-purchase displays with tactile varnish that triggers impulse buys. Food-grade regulatory limits on certain solvent pigments accelerate the retirement of legacy gravure in snack cans. As adoption widens, inkjet heads reach linear speeds of 90 meters-per-minute, shrinking the cost delta versus flexo and broadening addressability within the Colombia corrugated packaging market.

By End-User Industry: E-Commerce Takes Off, Food Remains Anchor

Processed foods led the Colombian corrugated packaging market with a 28.44% share in 2025, supplying rice, pasta, and canned vegetables sold through modern trade. Corrugated secondary packs replace wooden crates in chilled meat and cheese lines as hygiene rules tighten. E-commerce fulfillment centers show the market’s fastest 5.25% CAGR as fashion, electronics, and groceries migrate online, demanding right-sized, branded shippers that withstand reverse logistics.

Floriculture and fresh fruit exporters pivot to moisture-resistant die-cuts that raise average selling prices by 15% while slashing waste for growers near Rionegro and Guasca. Beverage bottlers switch to fully enclosed cases compatible with automated high-bay storage, cutting pallet collapse risk and plastic use. Electronics assemblers in Bogotá's free-trade zones request anti-static, triple-wall cartons to protect circuit boards en route to Miami distribution hubs. Cosmetics and personal-care brands transition away from blister plastics toward corrugated gift boxes shaped by influencer unboxings, while pharmaceutical clients demand ISO-audited, migration-tested secondary packs, extending premium pricing latitude throughout the Colombia corrugated packaging market.

Geography Analysis

Bogotá and the Sabana corridor accounted for roughly 40% of national demand in 2025, driven by processed-food plants, fulfillment hubs, and pharma pack-outs that reinforce the Colombia corrugated packaging market. The capital’s population density supports just-in-time deliveries, reducing converter lead times to 24-48 hours for repeat SKUs. Medellín’s Aburrá Valley accounted for 22% of the market as textile revivals and electric-bus assembly lines require transit packs, turning regional converters into strategic partners for just-launched factories.

Cali and the wider Valle del Cauca contributed close to 17%, thanks to fruit and floriculture exporters that need moisture-resistant ventilated cartons for refrigerated containers. April 2025 flower export volumes climbed 13.9%, intensifying overnight box demand during Mother’s Day and Valentine’s Day peaks. The Pacific port of Buenaventura allows same-day backhauls of empty pallets and sheets, shrinking inventory for produce shippers and boosting flexibility in the Colombia corrugated packaging market.

Barranquilla and Cartagena, while smaller, are the fastest-growing coastal nodes as near-shored consumer electronics and pharmaceutical contract manufacturers specify tamper-evident double-wall boxes. Road-freight costs to remote departments remain high, yet the 2024-2028 National Logistics Plan promises a 12%-15% cost drop by 2028, potentially unlocking demand in Chocó and Putumayo. Integrated players such as Smurfit Westrock and Carvajal Empaques position mills near major highways to cap inter-regional freight exposure, sustaining competitive delivery times.

Competitive Landscape

Four integrated firms, Smurfit Westrock, Cartones America, Carvajal Empaques, and Cartón de Colombia, held about 60% collective share in 2025, giving the Colombian corrugated packaging market a moderate concentration. Scale enables backward integration into recovered fiber and energy assets, as illustrated by Smurfit WestRock’s Barbosa biomass boiler, which now supplies 85% of onsite power. Cartones America’s dispersion-coated line secures first access to foodservice buyers seeking grease resistance, while Carvajal Empaques’ bagasse medium diversifies fiber risk and appeals to eco-labels.

Digital-native entrants such as Grafix Digital leverage Highcon technology to deliver same-day prototypes for e-commerce sellers. Their asset-light model bypasses tooling costs and competes on speed rather than volume, nibbling at the fringes of traditional long-run flexo. Integrated incumbents respond by adding digital presses and automated die-cutters, raising capital requirements for newcomers and reinforcing entry barriers in the Colombia corrugated packaging market.

Regulatory rigor further separates contenders. INVIMA’s January 2026 guide requires converters to document heavy-metal and volatile-organic migration for every lot that touches food or drugs. Plants lacking ISO 9001 systems risk product rejections, steering pharmaceutical and infant-nutrition brands toward certified suppliers. Sustainability credentials, including FSC chain-of-custody and life-cycle carbon data, increasingly feature in RFQs, giving integrated mills an edge that small regionals struggle to match.

Colombia Corrugated Packaging Industry Leaders

Smurfit Westrock plc

Cartones America S.A.

Carvajal Empaques S.A.S.

Cartón de Colombia S.A.

Empacor S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: INVIMA released the Application Guide for Resolutions 683 and 4143 of 2012, clarifying approval procedures for food-contact packaging and raising documentation standards for converters.

- December 2025: Smurfit Westrock began ramp-up of a digital-print line in Medellín, cutting lead times for personalized e-commerce cartons to 48 hours.

- June 2025: Carvajal Empaques launched a pilot sugarcane-bagasse medium line in Cali, targeting processed-food and beverage cases.

- April 2025: Highcon and Grafix Digital installed a digital cutting and creasing system in Bogotá, enabling same-day short runs for custom boxes.

Colombia Corrugated Packaging Market Report Scope

The Colombia Corrugated Packaging Market report encompasses a comprehensive analysis of fiber-based and polymer-based corrugated materials used for the containment, protection, and transport of goods across diverse industrial and retail sectors. The market refers to the industry that produces multi-layered boards, typically consisting of a fluted medium sandwiched between linerboards, designed to provide high strength-to-weight ratios and crush resistance for secondary and tertiary packaging.

The Colombia Corrugated Packaging Market Report is Segmented by Material (Virgin Kraft Linerboard, Recycled Linerboard, Corrugating Medium, Semi-Chemical Fluting, and Other Materials), Flute Type (A Flute, B Flute, C Flute, E Flute, and F Flute), Packaging Type (Regular Slotted Containers, Die-Cut Custom Boxes, Folding Cartons, Point-of-Purchase Displays, Pallet Boxes, and Other Packaging Types), Wall Type (Single-Wall, Double-Wall, Triple-Wall, and Single Face), Printing Technology (Flexographic Printing, Digital Inkjet Printing, Litho-Lamination, Screen Printing, and Other Printing Technologies), End-User Industry (Processed Foods, Fresh Food and Produce, Beverages, Electrical Products, Personal Care and Cosmetics, E-commerce Fulfillment Centers, Pharmaceuticals, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD

| Virgin Kraft Linerboard |

| Recycled Linerboard |

| Corrugating Medium |

| Semi-Chemical Fluting |

| Other Materials |

| A Flute |

| B Flute |

| C Flute |

| E Flute |

| F Flute |

| Regular Slotted Containers |

| Die-Cut Custom Boxes |

| Folding Cartons |

| Point-of-Purchase Displays |

| Pallet Boxes |

| Other Packaging Types |

| Single-Wall |

| Double-Wall |

| Triple-Wall |

| Single Face |

| Flexographic Printing |

| Digital Inkjet Printing |

| Litho-Lamination |

| Screen Printing |

| Other Printing Technologies |

| Processed Foods |

| Fresh Food and Produce |

| Beverages |

| Electrical Products |

| Personal Care and Cosmetics |

| E-Commerce Fulfillment Centers |

| Pharmaceuticals |

| Other End-User Industries |

| By Material | Virgin Kraft Linerboard |

| Recycled Linerboard | |

| Corrugating Medium | |

| Semi-Chemical Fluting | |

| Other Materials | |

| By Flute Type | A Flute |

| B Flute | |

| C Flute | |

| E Flute | |

| F Flute | |

| By Packaging Type | Regular Slotted Containers |

| Die-Cut Custom Boxes | |

| Folding Cartons | |

| Point-of-Purchase Displays | |

| Pallet Boxes | |

| Other Packaging Types | |

| By Wall Type | Single-Wall |

| Double-Wall | |

| Triple-Wall | |

| Single Face | |

| By Printing Technology | Flexographic Printing |

| Digital Inkjet Printing | |

| Litho-Lamination | |

| Screen Printing | |

| Other Printing Technologies | |

| By End-User Industry | Processed Foods |

| Fresh Food and Produce | |

| Beverages | |

| Electrical Products | |

| Personal Care and Cosmetics | |

| E-Commerce Fulfillment Centers | |

| Pharmaceuticals | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the current Colombia corrugated packaging market size and its growth outlook to 2031?

The market is projected at USD 1.14 billion in 2026 and is expected to reach USD 1.35 billion by 2031, reflecting a 3.48% CAGR over 2026-2031.

Which material segment is growing the fastest in Colombian corrugated packaging?

Semi-chemical fluting is expanding at a 4.19% CAGR as exporters seek lighter yet stronger board.

How is the single-use plastic tax influencing packaging choices in Colombia?

The escalating tax is pushing quick-service restaurants and retailers to shift toward grease-resistant corrugated boxes, adding around 18,000 metric tons of annual demand.

Why is digital printing gaining share in Colombia corrugated packaging?

E-commerce brands value variable graphics and low minimum orders, and digital presses eliminate plate costs, supporting a 5.11% CAGR through 2031.

Which regions generate the highest demand for corrugated boxes in Colombia?

Bogotá and the Sabana corridor contribute about 40% of national consumption, followed by Medellín and the Valle del Cauca region.

What is driving the adoption of triple-wall corrugated boxes?

Near-shored electronics assembly and heavy industrial exports require edge-crush strengths above 55 psi, fueling a 4.32% CAGR for triple-wall formats.

Page last updated on: