Market Overview

| Study Period | 2020 - 2030 |

|---|---|

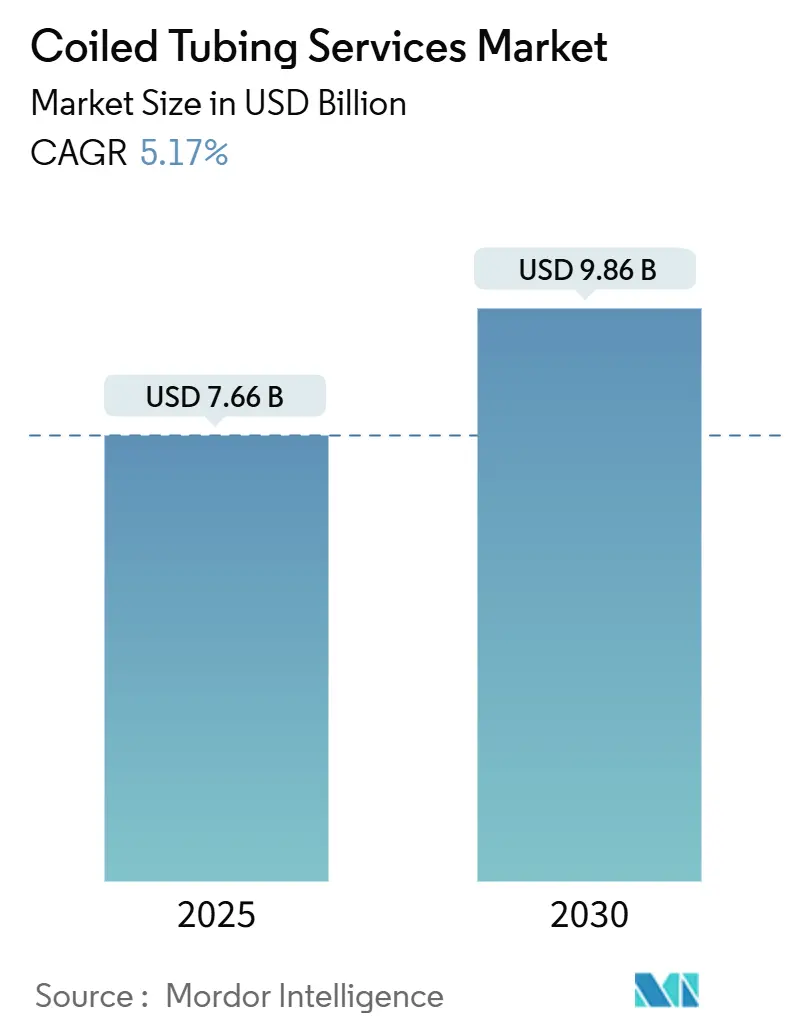

| Market Size (2025) | USD 7.66 Billion |

| Market Size (2030) | USD 9.86 Billion |

| Growth Rate (2025 - 2030) | 5.17% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Coiled Tubing Services Market Analysis by Mordor Intelligence

The Coiled Tubing Services Market size is estimated at USD 7.66 billion in 2025, and is expected to reach USD 9.86 billion by 2030, at a CAGR of 5.17% during the forecast period (2025-2030).

Robust demand for live-well interventions, rising unconventional resource development, and expanding deployment of intelligent downhole systems continue to anchor growth even as crude-price swings affect operator budgets. Operators are favoring coiled tubing for its ability to enter extended-reach laterals without requiring rig mobilization, thereby reducing nonproductive time and associated costs. Real-time telemetry, fiber-optic sensing, and AI-driven control packages now enable crews to adjust pumping rates, weight on bit, and tool orientation continuously, thereby improving treatment placement accuracy while minimizing the need for remedial runs. The shift toward geothermal retrofits and carbon-capture storage wells presents additional use cases, keeping the coiled tubing services market expanding beyond traditional oil and gas projects.

Key Report Takeaways

- By service type, well cleaning and stimulation accounted for 54.7% of the coiled tubing services market share in 2024 and is expected to advance at a 6.1% CAGR through 2030.

- By pipe diameter, the 2–2.5-inch segment accounted for 46.3% of the coiled tubing services market size in 2024, while leading projected growth at a 5.9% CAGR through 2030.

- By application, well intervention accounted for 68.5% of 2024 revenue and is expected to expand at a 5.7% CAGR through 2030.

- By deployment location, onshore operations held 79.1% share in 2024; in contrast, offshore activity is forecast to post the fastest 6.5% CAGR owing to deeper-water subsea projects that now rely on riserless coiled tubing systems.

- By geography, North America accounted for 43.8% of the market share in 2024, while the Middle East and Africa is projected to grow at the fastest rate of 7% CAGR through 2030.

Global Coiled Tubing Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for well intervention in maturing fields | 1.80% | Global, with concentration in North America and North Sea | Medium term (2-4 years) |

| Expansion of shale plays in North America | 1.50% | North America, with spillover to Argentina and Australia | Short term (≤ 2 years) |

| Cost-efficiency versus conventional work-over rigs | 1.20% | Global, particularly onshore operations | Short term (≤ 2 years) |

| Adoption of intelligent CT with real-time downhole data | 0.90% | North America and Europe, expanding to Middle East | Medium term (2-4 years) |

| Geothermal & CCUS well retrofits using CT | 0.60% | North America and Europe, early adoption in Asia-Pacific | Long term (≥ 4 years) |

| Remote deep-water subsea intervention capability | 0.70% | Global offshore regions, led by Gulf of Mexico and North Sea | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Well Intervention in Maturing Fields

Operators focused on maximizing recovery from aging reservoirs are accelerating the use of coiled tubing as a cost-effective substitute for workover rigs. Live-well capability enables crews to circulate, clean, and stimulate without killing the well, thereby protecting reservoir pressure and avoiding costly re-perforation.[1]Baker Hughes, “Well Intervention in Mature Fields,” bakerhughes.com In shale basins, refracturing and production enhancement programs rely on coiled tubing to navigate tight radii and deliver sand plugs or diverters precisely, thereby lifting incremental production with minimal capital expenditure. Bottom-hole assemblies equipped with vibration and torque sensors transmit data in real-time, enabling engineers to detect bridge plugs or scale buildup early and adjust parameters on the fly. Such efficiency gains explain why the coiled tubing services market continues to outpace rig-based workovers in mature oil and gas plays. With more than 60% of global crude now produced from fields that are older than 15 years, intervention intensity is set to intensify throughout the decade.

Expansion of Shale Plays in North America

Horizontal laterals exceeding 20,000 feet are now commonplace in the Permian and Bakken, driving uptake of larger-diameter, often 2-inch and above, strings that can deliver higher fluid volumes while maintaining fatigue life.[2]OnePetro, “Operational Advances in Large-Diameter Coiled Tubing,” onepetro.org New hybrid strings combine coiled tubing with flush-joint pipe to improve reach, and automated fracturing services leverage downhole pressure sensors to close the loop between surface pumps and reservoir response. Emerging unconventional prospects in Argentina’s Vaca Muerta and Australia’s Canning Basin are replicating these practices, underscoring how the North American learning curve is propagating globally. As export capacity for liquefied natural gas grows, operators are expected to prioritize completion acceleration, which will further stimulate the coiled tubing services market.

Cost-Efficiency Versus Conventional Work-over Rigs

A modern coiled tubing unit arrives on location with a smaller crew, a lighter footprint, and no pipe-handling crane, cutting mobilization costs by 30–40% compared to a double-derrick workover rig in many basins. Continuous circulation eliminates connection breaks, reducing pump stoppages and surface emissions while shortening job duration. Automated injector heads and computerized rate-control panels permit a single supervisor to oversee multiple tasks, shrinking labor exposure and insurance costs simultaneously.[3]Halliburton, “OCTIV Intelligent Fracturing,” halliburton.com Offshore, riserless coiled tubing deployed from monohull vessels can reduce intervention budgets by up to 50% compared to semi-submersible rigs in water depths exceeding 6,000 feet. These savings are particularly appealing as capital discipline remains paramount across public E&P companies.

Adoption of Intelligent CT with Real-Time Downhole Data

Fiber-optic-enabled strings, such as SLB’s ACTive X trail, continuously distribute temperature and acoustic profiles, allowing engineers to confirm diversion efficiency during acidizing without halting pumping. Baker Hughes’ CoilTrak platform integrates measurement-while-drilling sensors that report inclination, tool face, and gamma counts, turning coiled tubing into a drilling conduit for reentries and sidetracks. Combined with cloud analytics, these data streams feed AI algorithms that predict fatigue life and recommend optimal pull speeds, elevating equipment reliability. As more operators adopt digital oilfield principles, intelligent coiled tubing is evolving from an intervention tool into a real-time reservoir management system, reinforcing long-term demand across the coiled tubing services market.[4]SLB, “ACTive Annular Intervention Services,” slb.com

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Crude-oil price volatility curbing E&P capex | -2.10% | North America shale, global deepwater projects | Short term (≤ 2 years) |

| Technical limits in ultra-HPHT & sour environments | -0.80% | Deepwater Gulf of Mexico, Middle East sour gas | Medium term (2-4 years) |

| Emission regulations on diesel CT units | -0.60% | North America, Europe | Long term (≥ 4 years) |

| Alloy supply shortages for large-diameter strings | -0.40% | Global manufacturing centers in Asia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Crude-Oil Price Volatility Curbing E&P Capex

Lower and more unpredictable crude benchmarks frequently prompt operators to defer discretionary clean-out and stimulation programs. Capital budgets for tight-oil producers in the United States have already shifted toward dividend payments and debt reduction, thereby squeezing service procurement cycles. When WTI falls below the breakeven range for high-pressure gas zones, coiled tubing jobs, often priced on a per-hour basis, are among the first to be rescheduled. Service companies thus experience swings in fleet utilization that complicate forward staffing and maintenance planning. Although long-term well-intervention demand remains intact, yearly volatility subtracts tangible growth from the coiled tubing services market.

Technical Limits in Ultra-HPHT & Sour Environments

Pressures above 20,000 psi and temperatures exceeding 400 °F test the collapse rating and yield strength of even high-chromium strings. Hydrogen-induced cracking can initiate when sour gas contacts weld seams, forcing operators to specify specialty 25Cr35Ni alloys and impose stringent inspection intervals. Such materials command premiums of 50% or more over standard grades, elevating project costs and narrowing economics in deepwater plays. Specialized surface equipment, including blowout preventers, injector heads, and umbilicals, must undergo additional certification, which elongates project lead times. Until metallurgical advances push the operational envelope further, ultra-HPHT and sour settings will continue to limit the rapid penetration of the coiled tubing services market in certain frontier basins.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Well Cleaning and Stimulation Extend Leadership

Well cleaning and stimulation operations represented 54.7% of 2024 revenue, confirming their status as the cornerstone of the coiled tubing services market. The category is forecast to grow at a 6.1% CAGR through 2030 as unconventional reservoirs require periodic sand plug removal, scale dissolution, and post-frac acid washes to sustain flow. Mature offshore fields in the North Sea and Asia rely on solvent-based treatments delivered via coiled tubing to mitigate asphaltene deposition and water coning, demonstrating the segment’s utility across geologies.

Revenue momentum also benefits from integrated service packages that combine fluid design, real-time downhole sensing, and post-job production monitoring in one mobilization. Major providers now market “single-trip efficiency bundles” that log, perforate, stimulate, and clean with sequential tool changes at surface, preserving injector fatigue life. As operators increasingly outsource multi-disciplinary workflows, well cleaning is likely to maintain the largest contribution to the coiled tubing services market size over the forecast horizon.

By Pipe Diameter: 2–2.5 Inch Strings Balance Reach and Strength

The 2–2.5 inch category secured 46.3% of 2024 sales and is on track for a 5.9% CAGR, making it the most influential diameter class within the coiled tubing services market share. Engineers routinely specify this range for long-reach horizontals where flow capacity must support high-rate nitrogen lifts or abrasive slurry transports without sacrificing bend fatigue performance.

Manufacturers have responded with proprietary micro-alloy steels and orbital-welded continuous lengths exceeding 30,000 feet that reduce spool-on-rig joints. Alleima’s recent rollout of 1,000-meter weld-free sections illustrates how materials science is expanding service windows while reducing failure risk. As deepwater prospects migrate beyond 10,000-foot water depths, demand for larger outside diameters may grow, yet mid-range pipe remains the workhorse for most onshore and shelf operations, safeguarding its dominance in the coiled tubing services market.

By Application: Well Intervention Underpins Market Scale

Intervention services accounted for 68.5% of global turnover in 2024, confirming their status as the primary revenue engine for the coiled tubing services market. Operators favor coiled tubing for scale removal, refracturing, and water-shutoff jobs that restore declining wells at a fraction of the cost of new drilling. Extended-reach laterals with multiple depletion profiles demand zonal isolation, and real-time distributed temperature sensing aids diversion accuracy during acid stimulation.

The forecasted growth of 5.7% CAGR through 2030 reflects the rising population of onshore horizontal wells worldwide. Additionally, automated well-intervention platforms integrating pressure-controlled deployment of electric submersible pumps or gas-lift mandrels are expanding the breadth of operations achievable without a workover rig. These trends ensure that well intervention remains the anchor tenant within the coiled tubing services market size for the foreseeable future.

By Location of Deployment: Onshore Remains Commanding Yet Offshore Accelerates

Onshore projects accounted for 79.1% of the 2024 turnover, buoyed by the prolific shale patch and shorter cycle times that coiled tubing enables. Land fleets benefit from lower mobilization costs and easier logistics, ensuring a broad geographic spread from West Texas to western Siberia.

Offshore, however, is projected to log a 6.5% CAGR through 2030, as deepwater asset owners turn to riserless coiled tubing for scale squeeze, barium sulfate removal, and electrical submersible pump change-outs without the need for a rig. Halliburton’s catenary offshore spread demonstrated economic viability in 7,200-foot water depth, cutting intervention spend by nearly half compared with rig-based alternatives. Successful trials in the Gulf of Mexico and the North Sea are prompting national oil companies in Brazil and Malaysia to pilot similar concepts, driving volume growth from a small but expanding base.

Geography Analysis

North America retained leadership in 2024, leveraging its vast unconventional portfolio and deep service-provider ecosystem. Intensifying refracture campaigns in the Permian and record-length laterals, such as Tenaris’s 24,166-foot run in West Virginia, exhibit the region’s appetite for advanced coiled-tubing deployments. Mid-continent producers are increasingly embedding AI-driven geosteering and fatigue-prediction models, turning every run into a learning loop that enhances development planning efficiency. Although spending discipline tempers short-term activity, aggregate intervention intensity keeps the coiled tubing services market well-supported across the United States and Canada.

The Middle East and Africa are poised for the fastest compound growth over the next five years, as NOCs expand enhanced-oil-recovery schemes and adopt coiled tubing for gas-storage developments, such as Dubai Petroleum’s Margham project. High-temperature sour environments in Kuwait and Saudi Arabia incentivize premium metallurgy, pushing operators toward intelligent downhole safety valves installed via coiled tubing, which boosts the average revenue per job. Offshore West Africa’s deepwater fields offer additional headroom, particularly where riserless access reduces the dependency on semisubmersibles.

Europe and the Asia-Pacific collectively represent a solid second-tier opportunity base. North Sea operators utilize coiled tubing to clean barium sulfate and install chemical-injection lines in mature subsea wells, thereby extending field life beyond platform cessation targets. In Asia, China’s Sichuan tight-gas and India’s Cambay shale pilots employ 2-inch hybrids to execute multi-stage fracture stimulations where rig availability is constrained. Stringent European environmental directives are driving the rapid uptake of electric pump powerpacks and low-toxicity fluids, differentiating service offerings and elevating compliance-driven margins within the regional coiled tubing services market.

Competitive Landscape

Global market competition remains moderate, with integrated majors such as SLB, Baker Hughes, and Halliburton leading technology investments and cross-basin coverage. Each has unveiled electric well-control packages that replace hydraulics with digitally controlled actuators, reducing leak risk and providing instantaneous tool feedback. Mid-tier specialists continue to thrive by focusing on niche diameter ranges, geothermal wells, or regional exclusivity. Consolidation is gathering pace, as evidenced by SLB’s USD 7.7 billion purchase of ChampionX, which combines production chemicals with intervention hardware, foreshadowing broader solutions bundling.

Technology differentiation is overtaking price as the key tender criterion. AI-powered fatigue tracking, digital twins, and integrated stimulation-while-logging workflows enable operators to verify treatment quality in real-time, thereby mitigating rework costs. Equipment manufacturers such as NOV supply Arctic-rated mast units and extra-heavy injectors that expand operational envelopes to 150,000-pound pull capacity, ensuring service companies can accept ultra-deep HPHT assignments. Collaborations between pipe makers, tool vendors, and data analytics firms are shortening development cycles for new alloys and sensor suites, knitting a tighter value chain around the coiled tubing services market.

Regional champions are also merging to reach a critical scale. The recent combination of Axis and Brigade in the United States created the country’s largest dedicated well-service fleet, positioning the new entity to negotiate multiyear contracts with supermajors. Similar aggregation moves are unfolding in Latin America and Southeast Asia, where incumbents seek nationwide coverage. With procurement teams favoring providers that can mobilize anywhere within 24 hours, such scale gains are likely to intensify competitive pressure at the bottom end of the pricing curve while leaving premium, technology-rich service tiers relatively protected.

Coiled Tubing Services Industry Leaders

Schlumberger Limited

Schlumberger Limited

Halliburton Company

Weatherford International PLC

Calfrac Well Services Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: SLB completed its acquisition of ChampionX Corporation, integrating production chemicals with intervention hardware and targeting USD 400 million in annual pretax synergies within three years.

- April 2025: Baker Hughes introduced the Hummingbird all-electric land cementing unit, alongside SureCONTROL Plus interval control valves, broadening its line of low-emission equipment.

- March 2025: Baker Hughes secured a multi-year integrated coiled-tubing drilling contract from Dubai Petroleum Establishment for the Margham Gas storage project, deploying CoilTrak systems for horizontal connectivity.

- February 2025: NOV booked orders for three bespoke Arctic Mast coiled-tubing units for Alaskan deployment and delivered five high-spec spreads to an international service firm.

Global Coiled Tubing Services Market Report Scope

Coiled tubing services employ a flexible steel pipe, continuously spooled on a reel, to conduct operations in oil, gas, and geothermal wells. These services facilitate wellbore cleanouts, hydraulic fracturing, and well interventions. A primary advantage is the capability to operate on live wells without necessitating a shutdown, leading to substantial time and cost savings. Additionally, these services enable operators to inject fluids or pump chemicals through the tubing during operations.

The coiled tubing services market is segmented by service type, pipe diameter, application, location of deployment, and geography. By service type, the market is segmented into well cleaning and stimulation, logging and perforation, and fishing and milling. By pipe diameter, the market is segmented into up to 2 in, 2 to 2 5 in, and above 2 5 in. By application, the market is segmented into drilling, completion, and well intervention. By location of deployment, the market is segmented into onshore and offshore. The report also covers the market sizes and forecasts for the global coiled tubing services market across major countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

By Service Type

| Well Cleaning and Stimulation |

| Logging and Perforation |

| Fishing and Milling |

By Pipe Diameter

| Up to 2 in |

| 2 to 2.5 in |

| Above 2.5 in |

By Application

| Drilling |

| Completion |

| Well Intervention |

By Location of Deployment

| Onshore |

| Offshore |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| NORDIC Countries | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Service Type | Well Cleaning and Stimulation | |

| Logging and Perforation | ||

| Fishing and Milling | ||

| By Pipe Diameter | Up to 2 in | |

| 2 to 2.5 in | ||

| Above 2.5 in | ||

| By Application | Drilling | |

| Completion | ||

| Well Intervention | ||

| By Location of Deployment | Onshore | |

| Offshore | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| NORDIC Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the coiled tubing services market in 2025?

The coiled tubing services market size stands at USD 7.66 billion for 2025 and is on course to reach USD 9.86 billion by 2030, reflecting a 5.17% CAGR.

Which service type holds the largest share of revenue?

Well cleaning and stimulation services dominate, accounting for 54.7% of 2024 revenue and registering the fastest 6.1% CAGR going forward.

Why is the 2–2.5-inch diameter segment gaining prevalence?

It balances flow capacity and flexibility, enabling long-reach interventions while withstanding high pumping rates, giving the segment 46.3% share in 2024.

What is driving offshore coiled tubing demand?

Riserless intervention systems that cut costs and novel deepwater developments are pushing offshore activity to the highest 6.5% CAGR through 2030.

How are intelligent coiled tubing systems changing operations?

Fiber-optic sensing and AI control enable live monitoring and automated adjustments, reducing nonproductive time and enhancing treatment precision.

Which regions are expected to grow fastest?

The Middle East and Africa are projected to expand quickest as NOCs intensify enhanced-oil-recovery projects and adopt advanced intervention technologies.

Page last updated on: