Cognitive Assessment and Training In Healthcare Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

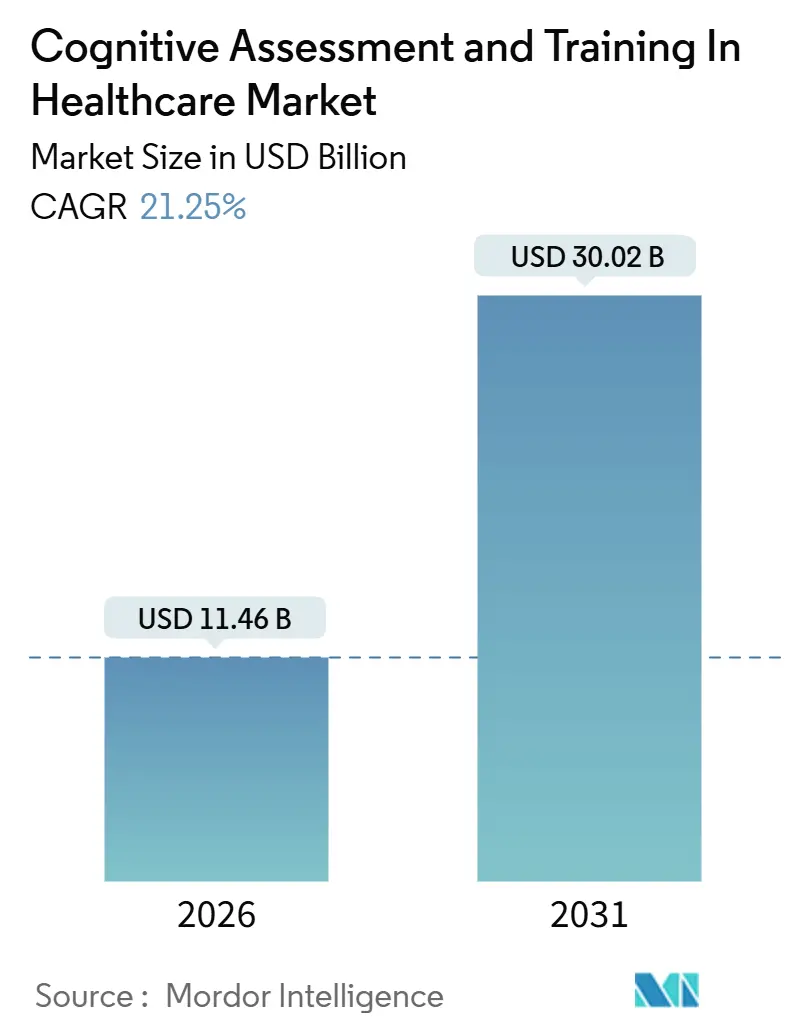

| Market Size (2026) | USD 11.46 Billion |

| Market Size (2031) | USD 30.02 Billion |

| Growth Rate (2026 - 2031) | 21.25% CAGR |

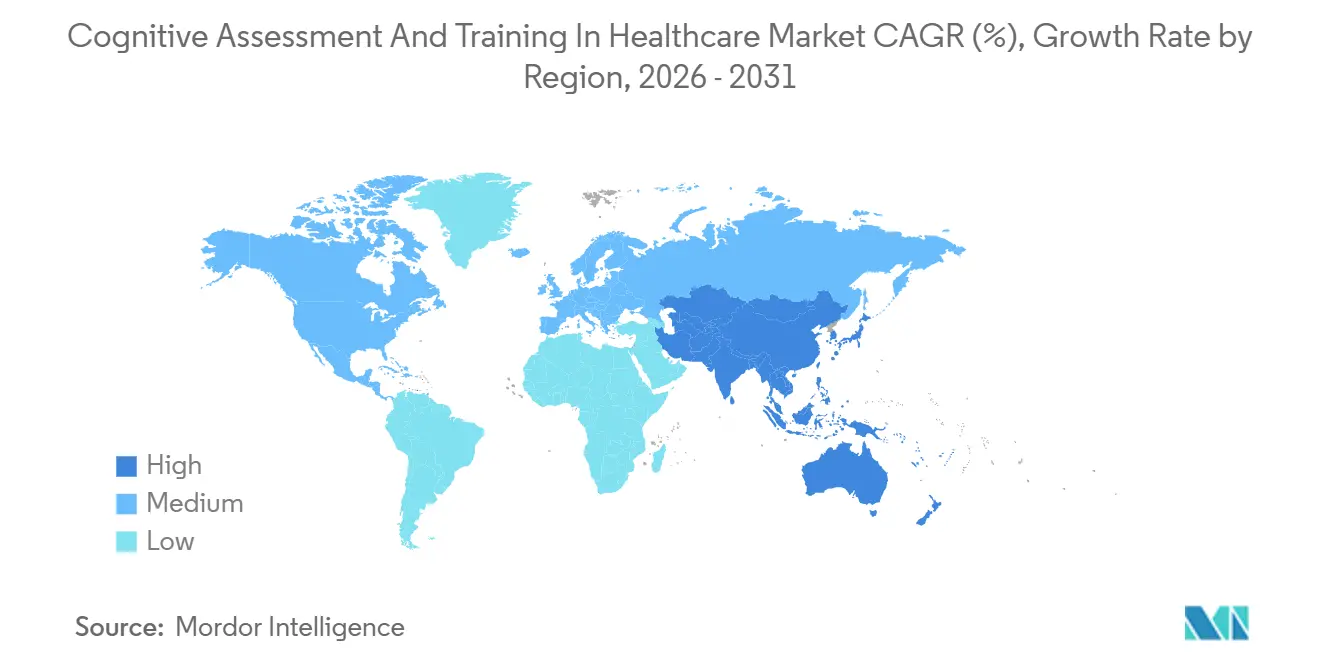

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cognitive Assessment and Training In Healthcare Market Analysis by Mordor Intelligence

The Cognitive Assessment And Training In Healthcare Market size is estimated at USD 11.46 billion in 2026, and is expected to reach USD 30.02 billion by 2031, at a CAGR of 21.25% during the forecast period (2026-2031).

The surge is propelled by validated digital endpoints in pharmaceutical research, employer-funded brain-wellness benefits, and national dementia initiatives that treat cognitive testing as preventive care rather than discretionary diagnostics. Regulatory clearances issued between 2024 and 2026 have accelerated platform adoption, while the expansion of CPT 96132 coverage to telehealth has removed a major U.S. reimbursement barrier. Capital continues to flow toward vendors that link cognitive scores with multimodal biomarkers, creating new revenue streams in longitudinal disease management. Meanwhile, algorithmic bias and fragmented payer policies remain headwinds that vendors must mitigate through stratified validation studies and advocacy for harmonized reimbursement codes.

Key Report Takeaways

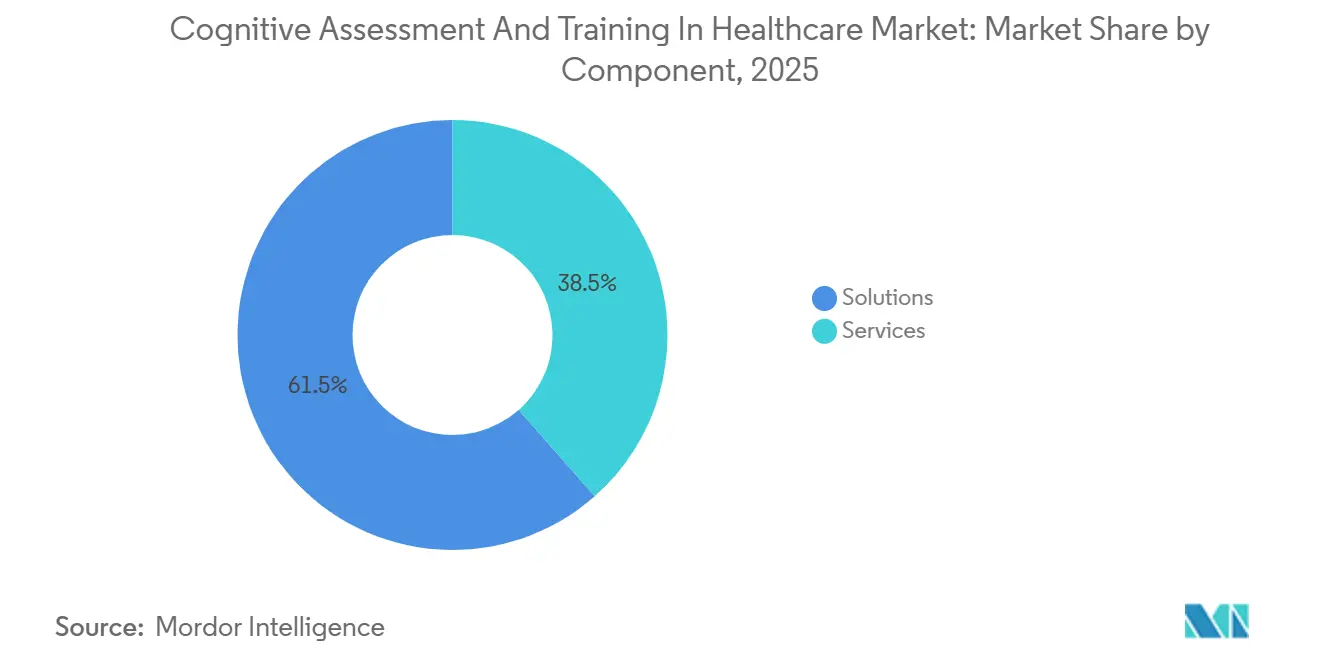

- By component, Solutions captured 61.55% revenue in 2025, whereas Services are forecast to advance at a 22.25% CAGR through 2031 and will narrow the gap rapidly.

- By assessment type, Screening & Diagnostics commanded 45.23% of revenue in 2025, but Clinical Trials are set to post the highest 22.15% CAGR to 2031, reflecting sponsors’ shift to digital cognitive endpoints.

- By delivery mode, Computer-based Testing held 49.15% revenue in 2025, yet Mobile / App-based Testing is projected to expand at 23.51% CAGR, underpinned by smartphone penetration in emerging regions.

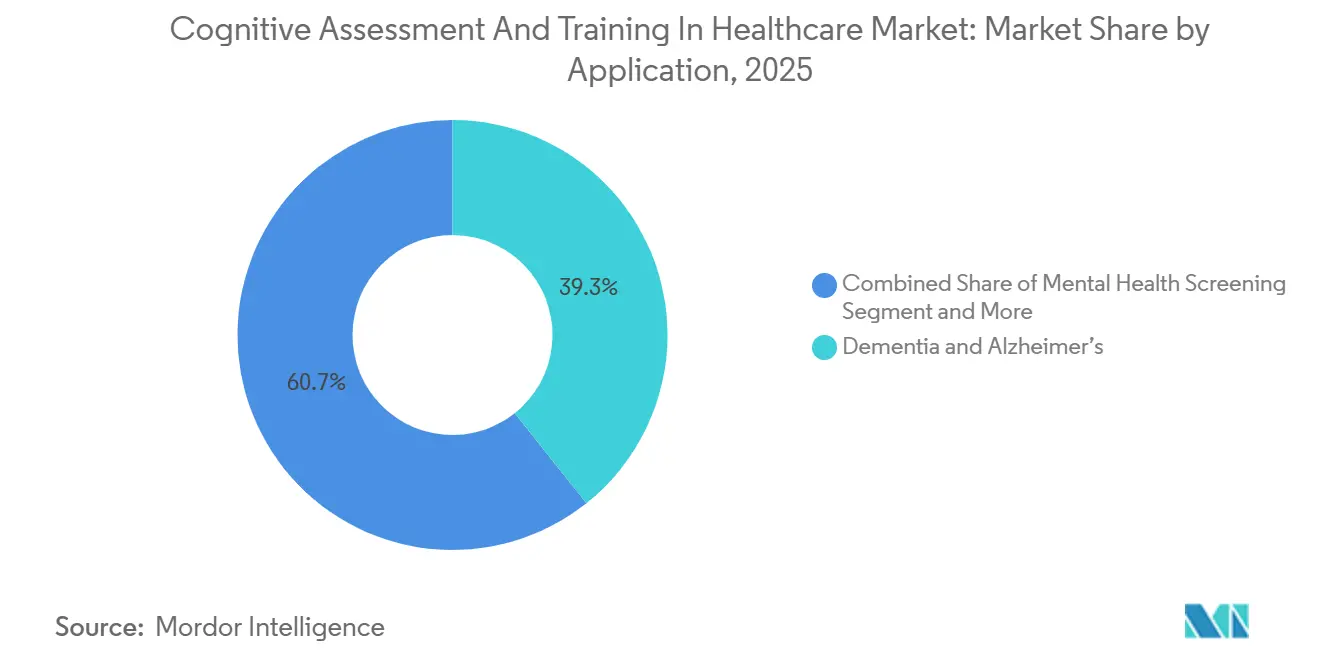

- By application, Dementia & Alzheimer’s led with 39.35% share in 2025, while Mental Health Screening will record a 22.11% CAGR through 2031 on the back of corporate wellness programs.

- By end user, Healthcare Providers generated 54.25% revenue in 2025; however, Home-care & Patients will be the fastest growing group at 24.02% CAGR as direct-to-consumer platforms gain traction.

- By geography, North America accounted for 38.45% revenue in 2025, whereas Asia-Pacific is poised for the fastest 22.22% CAGR to 2031, led by China and India.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Cognitive Assessment and Training In Healthcare Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing prevalence of neuro-degenerative disorders | +4.2% | Global | Long term (≥ 4 years) |

| Rapid adoption of digital health platforms | +5.1% | Global | Short term (≤ 2 years) |

| Regulatory endorsement of computerized tools | +3.8% | North America, Europe | Medium term (2-4 years) |

| Increased CNS clinical-trial spend | +2.9% | Global | Medium term (2-4 years) |

| Wearable biomarker integration | +2.6% | North America, Europe | Medium term (2-4 years) |

| Employer-sponsored brain-wellness benefits | +2.1% | North America, Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Prevalence of Neuro-Degenerative Disorders

Fifty-five million people were living with dementia in 2024, and the global tally is expected to climb to 78 million by 2030 and 139 million by 2050. Health systems are therefore shifting toward proactive cognitive screening at primary-care touchpoints. Early detection through digital tests slowed progression to moderate dementia by 18 months on average in 2025, saving USD 50,000 per patient in long-term care outlays. Pharmaceutical sponsors embed these tools in Phase II Alzheimer’s trials to capture subtle efficacy signals and shorten timelines by up to nine months. The economic burden of dementia exceeded USD 1.3 trillion in 2024, galvanizing payer support for large-scale assessment programs that can defer costly institutional care. As a result, the Cognitive Assessment and Training in Healthcare market continues to benefit from both clinical urgency and economic incentives.

Rapid Adoption of Digital Health & mHealth Platforms

Twelve digital devices for cognitive testing cleared the FDA between January 2024 and December 2025, five of which run entirely on smartphones[1]U.S. Food and Drug Administration, “Digital Health Center of Excellence,” FDA, fda.gov. Tele-neuropsychology sessions are reimbursed under CPT 96132 following Medicare’s 2025 rule change, removing travel friction for patients in rural areas. The United Kingdom’s MHRA now permits software-as-a-medical-device cognitive tools to rely on algorithmic equivalence rather than full clinical trials when predicates exist. Weekly at-home tests capture intra-individual variability that one-off clinic visits miss, enabling real-time therapy adjustments. This capability was pivotal in Biogen’s 2024 lecanemab filing, where digital endpoints revealed treatment effects four months earlier than paper scales.

Regulatory Endorsement of Computerized Cognitive Tools

The FDA granted three De Novo clearances for AI-powered platforms in 2024, setting a precedent for Class II approval without a predicate device. Europe followed suit in June 2025 with EMA guidance that formalized digital cognitive endpoints for Alzheimer’s studies, while Japan approved its first computerized tool in September 2024. Draft FDA guidance published in late 2025 now requires subgroup-specific validation to mitigate algorithmic bias. Although the new rules raise the bar for entrants, they strengthen payer confidence and accelerate provider adoption.

Rising CNS Clinical-Trial Spend for Cognitive End-Points

Industry R&D on CNS disorders hit USD 28 billion in 2024, with 78% of Alzheimer’s and Parkinson’s studies specifying cognitive endpoints. Eli Lilly cut screen-failure rates by 22% and saved USD 15 million by replacing paper scales with digital batteries in its 2024 donanemab program. Roche extended tablet-based testing to 40 trial sites in 2025 to automate scoring and anomaly detection. Contract research organizations now sell turnkey cognitive-endpoint packages, anchoring a high-margin growth vertical within the Cognitive Assessment and Training in Healthcare market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-privacy & HIPAA / GDPR compliance | -2.8% | North America, Europe | Short term (≤ 2 years) |

| Limited reimbursement pathways | -3.4% | Global | Medium term (2-4 years) |

| Cultural / linguistic bias in AI | -1.7% | APAC, Latin America | Long term (≥ 4 years) |

| Fragmented validation standards | -2.3% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Data-Privacy & HIPAA / GDPR Compliance Burden

Average breach costs in healthcare reached USD 10.9 million in 2024, making longitudinal cognitive datasets an attractive ransomware target[2]U.S. Department of Health and Human Services, “HIPAA Enforcement Actions,” HHS, hhs.gov. GDPR treats cognitive data as special-category information, forcing vendors to adopt encryption and third-party audits. A vendor paid USD 4.8 million in HIPAA fines in 2024 after investigators uncovered lax access controls, damping venture funding for startups without mature compliance infrastructures. Smaller direct-to-consumer platforms often exit the European Union rather than absorb the 40–60% premium for GDPR-compliant hosting.

Limited Reimbursement Pathways

CMS pays USD 45–65 per computerized test, barely covering licensing and clinician time. Commercial payers deny 42% of initial claims and often require prior authorization, adding weeks of delay. India’s national plan excludes cognitive screening, forcing patients to pay USD 30–50 out of pocket—more than many monthly healthcare budgets. The reimbursement gap restricts uptake in primary care, where early detection could yield the highest return on investment for the Cognitive Assessment and Training in Healthcare market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Gain as Complexity Rises

Services revenue is projected to climb at 22.25% CAGR through 2031, closing the gap with Solutions, which held 61.55% share in 2025. Hospital networks cite shortages of neuropsychologists and data scientists, prompting outsourced contracts that bundle software, interpretation, and EHR integration. Solutions face margin compression from open-source alternatives, while Services command premium rates for actionable insights. The Cognitive Assessment and Training in Healthcare market size captured by Services is expected to surpass USD 14 billion by 2031 as value-based care models reward longitudinal tracking.

Managed-service leaders employ quality-assurance dashboards that flag anomalous scores in real time, a feature pharmaceutical sponsors now list as a top-three procurement criterion. Accountable care organizations integrate weekly cognitive updates into dementia pathways, triggering personalized interventions without clinician bottlenecks. As payer quality metrics evolve, hybrid vendors that combine platforms with expert interpretation will outpace pure-play software providers in the Cognitive Assessment and Training in Healthcare market.

By Assessment Type: Clinical Trials Accelerate

Clinical Trials are on pace for a 22.15% CAGR, reflecting regulators’ acceptance of smartphone-based cognitive endpoints. Screening & Diagnostics still commands the largest slice, yet reimbursement constraints will slow growth relative to trial demand. Sponsors budget generous per-test fees to cut enrollment timelines, allowing vendors to sustain margins above 65%. The Cognitive Assessment and Training in Healthcare market share attached to Clinical Trials could approach 25% by 2031.

Standardization delivers network effects: as more sponsors adopt the same digital battery, regulators become familiar with its psychometrics, further boosting credibility. CROs embed cognitive testing modules into turnkey offerings, making digital endpoints a default rather than an add-on. Academic consortia also adopt these tools for population studies, reinforcing the market flywheel.

By Delivery Mode: Mobile Apps Disrupt Infrastructure

Mobile / App-based Testing is forecast to post 23.51% CAGR, surpassing computer-based kiosks by 2029. Rural India achieved 84% sensitivity and 78% specificity using smartphone tests, at one-tenth the cost of clinic batteries. Smartphone ubiquity in Asia-Pacific lowers acquisition costs, while built-in cameras and touchscreens support eye-tracking and reaction-time metrics that rival dedicated hardware. Continuous monitoring shifts revenue from per-test to subscription fees, stabilizing cash flows for vendors across the Cognitive Assessment and Training in Healthcare market.

Hospitals are reluctant to purchase new kiosks amid capital budget freezes, further tilting demand toward apps that run on consumer devices. Apple and Google have released cognitive assessment APIs, expanding the developer ecosystem and accelerating feature innovation. Pen-and-paper methods will persist only in ultra-low-resource settings or among clinicians nearing retirement who are unwilling to retool.

By Application: Mental Health Screening Emerges

Mental Health Screening is poised for 22.11% CAGR as employers bundle cognitive wellness with mood assessments. Digital cognitive scores help psychiatrists tailor therapy, boosting treatment efficacy by 23% in a 2025 JAMA Psychiatry study. Dementia & Alzheimer’s will remain the largest revenue source, yet its growth moderates as installed infrastructure matures. The Cognitive Assessment and Training in Healthcare market size tied to Mental Health Screening could top USD 6 billion by 2031.

Sports leagues and militaries represent ancillary growth pools for traumatic brain injury modules, while learning disability batteries target pediatric clinics despite fragmented school funding. Integrated platforms that score cognition, mood, and functional capacity in a single session will hold competitive advantage.

By End-User: Home-Care Disrupts Traditional Channels

Home-care & Patients will expand at 24.02% CAGR, fastest among end-users, as direct-to-consumer models undercut clinic prices by 40–60%. A 2024 McKinsey survey revealed that 58% of adults aged 50–70 prefer at-home tests for convenience and privacy. The FDA clarified in 2025 that over-the-counter cognitive apps delivering educational insights can avoid premarket clearance, triggering rapid product launches. Consequently, the Cognitive Assessment and Training in Healthcare market share for Home-care solutions could double by 2031.

Caregivers use these tools to monitor relatives and inform decisions about assisted living, creating a secondary demand channel. Healthcare Providers will still dominate absolute revenue, but their share slips as administrative friction and low reimbursement push testing out of clinical workflows. Payer segments move slowly due to multi-year validation studies, and pharmaceutical demand remains cyclical with trial pipelines.

Geography Analysis

North America accounted for 38.45% of 2025 revenue, anchored by Medicare’s remote-testing coverage and the Veterans Health Administration’s compulsory baseline screening for 9 million beneficiaries. Canada’s Ontario province budgeted CAD 150 million through 2027 to digitize dementia testing, yet slower regulatory clearance tempers short-term gains. Mexico’s 2025 dementia plan prioritizes screening, but limited smartphone penetration in rural districts curbs early uptake. Incumbents leverage payer networks and decades of validation data, presenting high entry barriers for newcomers in the North American Cognitive Assessment and Training in Healthcare market.

Asia-Pacific will deliver the fastest 22.22% CAGR to 2031. China mandates annual cognitive tests for adults aged 65+, a cohort of 190 million. India targets 50 million screenings by 2028 via primary-care health centers[3]Ministry of Health & Family Welfare, India, “National Dementia Strategy 2025,” MOHFW, mohfw.gov.in. Japan’s aging demographics and JPY 30 billion digital health fund fuel home-based monitoring adoption. Australia boasts 42% penetration among memory clinics, but absolute volumes remain modest. South Korea’s national dementia plan aims for 80% coverage by 2030, creating demand for platforms that handle 15 million annual assessments.

Europe, the Middle East, Africa, and South America form a heterogeneous landscape. Germany’s low reimbursement and prior-authorization hurdles deter primary-care adoption. The U.K. has piloted digital testing across 50 clinics, yet budget constraints delay national rollout. France allocates EUR 400 million through 2029 for early detection infrastructure, including computerized tools. The UAE and Saudi Arabia include cognitive testing in digital health roadmaps, but limited population bases cap revenue potential. Brazil’s public-sector rollout is stalled by fiscal austerity, while South Africa’s private hospitals mirror European adoption rates. These disparities will keep EMEA and South America’s combined Cognitive Assessment and Training in Healthcare market growth below the global average.

Competitive Landscape

The top 10 vendors collectively command a sizeable slice of global revenue, yielding a moderately concentrated environment. Cambridge Cognition, Cogstate, and Pearson leverage extensive validation libraries and entrenched pharma relationships to secure high-value clinical-trial contracts. New entrants such as BrainCheck and Neurotrack target primary-care and employer channels with simplified user experiences and lower price points. Signant Health’s acquisition of MedAvante-ProPhase in 2024 exemplifies vertical integration that appeals to sponsors seeking one-stop shops for endpoint management.

White-space opportunities revolve around mobile disruption in low-resource settings, where pen-and-paper tests still dominate. Vendors integrating cognitive scores with wearable biosensor data stand to differentiate through superior predictive accuracy. Patent filings for AI-driven cognitive algorithms jumped 180% between 2022 and 2024, signaling intensifying intellectual-property competition. Smaller players such as Savonix focus on pediatric learning disabilities, while AnthroTronix tailors solutions for military traumatic brain injury, illustrating niche defense strategies within the broader Cognitive Assessment and Training in Healthcare market.

Incumbents respond with subscription pricing, outcome-based contracts, and regional language expansion to preempt startup encroachment. Nonetheless, algorithmic bias scrutiny and data-privacy compliance could tilt the playing field toward vendors able to finance extensive validation studies.

Cognitive Assessment and Training In Healthcare Industry Leaders

Cambridge Cognition

Cogstate

Pearson PLC

Signant Health

BrainCheck

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: QHSLab introduced Q-Cog, a cloud-based assessment aimed at early detection of mild cognitive impairment in primary care.

- July 2025: Linus Health launched Anywhere, an AI-enabled tool that facilitates remote cognitive evaluations and personalized interventions.

Global Cognitive Assessment and Training In Healthcare Market Report Scope

As per the scope of the report, cognitive assessment and training in healthcare refer to the processes of evaluating an individual's mental functions, such as memory, attention, and problem-solving, and then providing targeted activities or interventions to improve or maintain cognitive health. These practices are used to identify cognitive impairments, monitor changes over time, and enhance mental abilities to support overall well-being and quality of life.

The segmentation for the cognitive assessment and training in healthcare market is categorized as follows: by component, it includes solutions and services. By assessment type, it covers screening & diagnostics, clinical trials, and academic & research. By delivery mode, it comprises computer-based testing, mobile/app-based testing, and pen-and-paper. By application, it includes dementia & Alzheimer’s, traumatic brain injury, learning disabilities, and mental health screening. By end-user, it involves healthcare providers, payers, pharmaceutical & biotech, and home-care & patients. By geography, it is segmented into North America, Europe, Asia-Pacific, Middle East and Africa, and South America. The adoption of Cognitive Assessment And Training solutions across clinical evaluation, rehabilitation programs, and digital health platforms is accelerating the development of integrated cognitive care models within healthcare systems. The Market Forecasts are Provided in Terms of Value (USD).

| Solutions |

| Services |

| Screening & Diagnostics |

| Clinical Trials |

| Academic & Research |

| Computer-based Testing |

| Mobile / App-based Testing |

| Pen-and-Paper |

| Dementia & Alzheimer's |

| Traumatic Brain Injury |

| Learning Disabilities |

| Mental Health Screening |

| Healthcare Providers |

| Payers |

| Pharmaceutical & Biotech |

| Home-care & Patients |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Component | Solutions | |

| Services | ||

| By Assessment Type | Screening & Diagnostics | |

| Clinical Trials | ||

| Academic & Research | ||

| By Delivery Mode | Computer-based Testing | |

| Mobile / App-based Testing | ||

| Pen-and-Paper | ||

| By Application | Dementia & Alzheimer's | |

| Traumatic Brain Injury | ||

| Learning Disabilities | ||

| Mental Health Screening | ||

| By End-User | Healthcare Providers | |

| Payers | ||

| Pharmaceutical & Biotech | ||

| Home-care & Patients | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the Cognitive Assessment and Training in Healthcare market in 2026?

The market stands at USD 11.46 billion in 2026 and is projected to reach USD 30.02 billion by 2031 at a 21.25% CAGR.

Which segment grows fastest through 2031?

Home-care & Patients end-users expand at 24.02% CAGR as direct-to-consumer platforms gain popularity.

What drives adoption of mobile cognitive testing?

Smartphone ubiquity, reduced hardware costs, and CPT 96132 reimbursement for remote assessments accelerate Mobile / App-based Testing.

Why are Services outpacing Solutions?

Health systems outsource interpretation and longitudinal tracking to vendors, generating a higher 22.25% CAGR for Services.

Which region posts the highest growth?

Asia-Pacific leads with a 22.22% CAGR through 2031, fueled by national screening programs in China and India.

What is the main barrier to wider clinical uptake?

Fragmented reimbursement and stringent data-privacy requirements continue to limit routine deployment in primary-care settings.

Page last updated on: