Coated Glass Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 47.06 Billion |

| Market Size (2031) | USD 68.12 Billion |

| Growth Rate (2026 - 2031) | 7.68% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Coated Glass Market Analysis by Mordor Intelligence

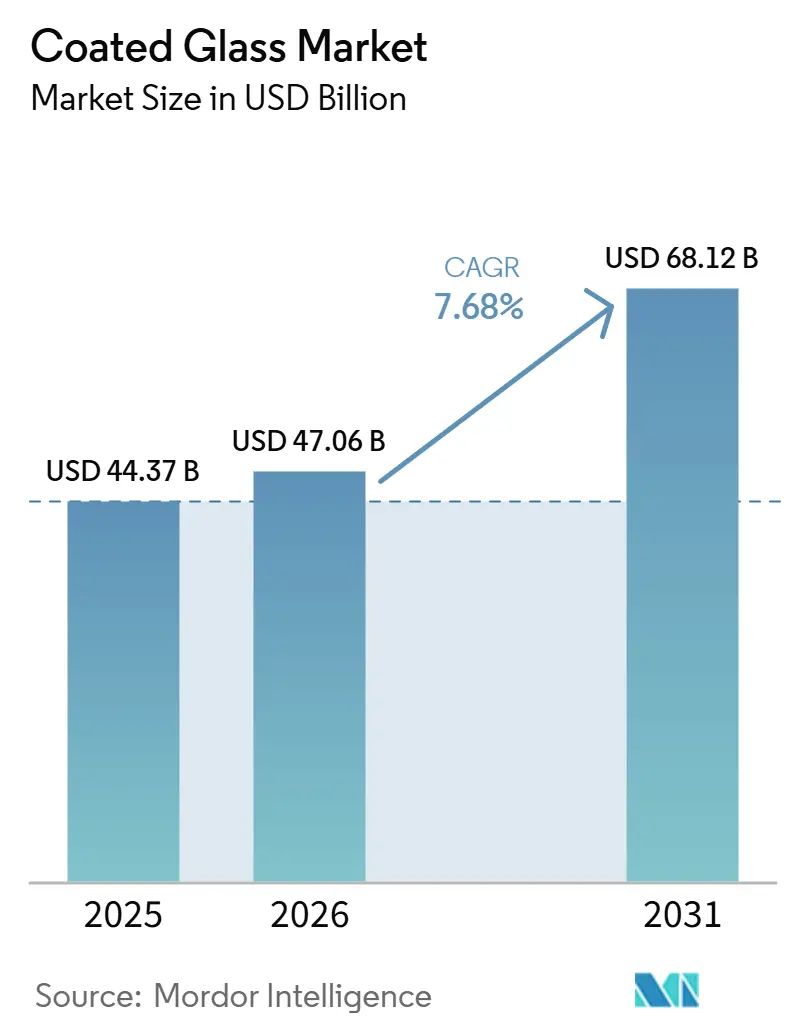

The Coated Glass Market size was valued at USD 44.37 billion in 2025 and is estimated to grow from USD 47.06 billion in 2026 to reach USD 68.12 billion by 2031, at a CAGR of 7.68% during the forecast period (2026-2031). Demand in the coated glass market remains linked to stricter building efficiency regulations, particularly in Europe and China, where new standards are shifting coated products from optional upgrades to core project requirements. This trend supports the market’s base, as renovation demand, commercial energy compliance, and improved envelope performance continue to drive volumes, even as new construction slows in some regions. At the same time, the coated glass market is developing an additional growth avenue through automotive and solar applications, where heat control, optical clarity, and anti-reflective performance influence product value and system efficiency. Competitive activity indicates that producers are expanding capacity in regions with regulatory demand while securing higher-value product lines ahead of the next round of project specifications. However, margin pressure remains relevant, as silver price volatility and new embodied-carbon disclosure requirements are increasing raw material risks and compliance costs across the coated glass market.

Key Report Takeaways

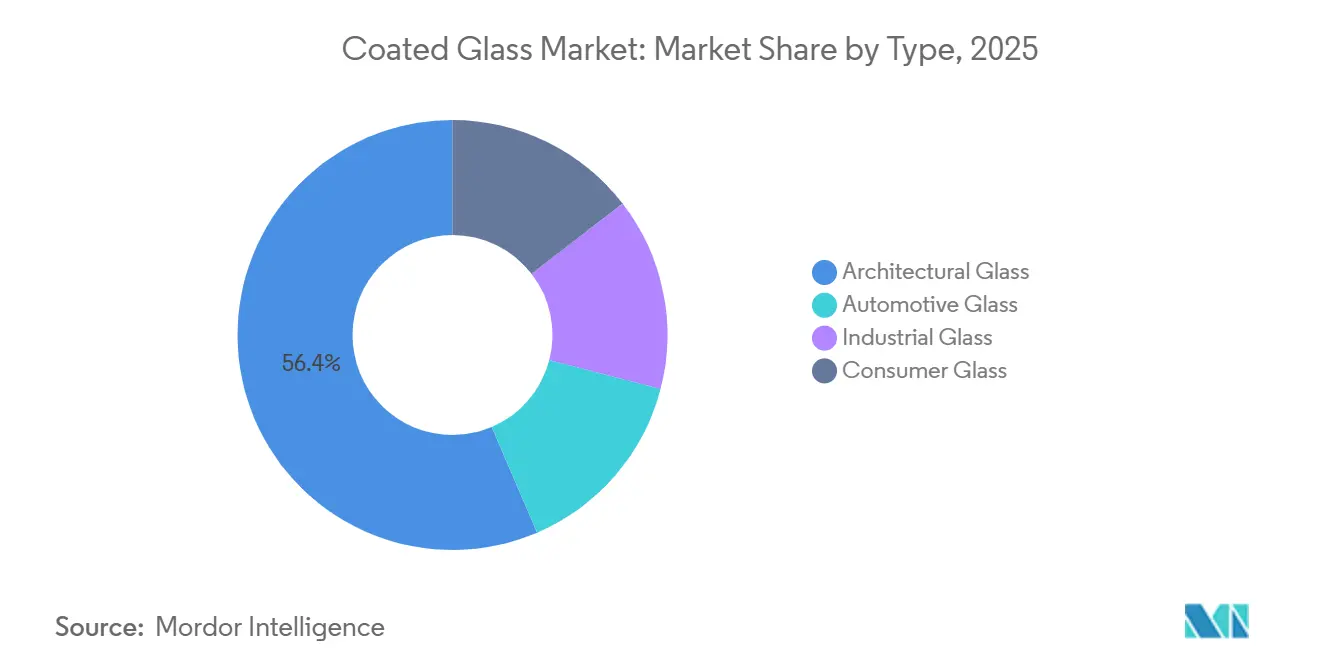

- By type, architectural glass accounted for 56.44% of the coated glass market size in 2025, while automotive glass is forecast to expand at a 7.80% CAGR through 2031.

- By coating type, Low-E coatings accounted for 42.70% of revenue in 2025, while anti-reflective coatings are projected to grow at a 8.12% CAGR through 2031.

- By substrate, float glass led with a 62.35% share in 2025, while laminated glass is expected to record the fastest growth at an 8.33% CAGR through 2031.

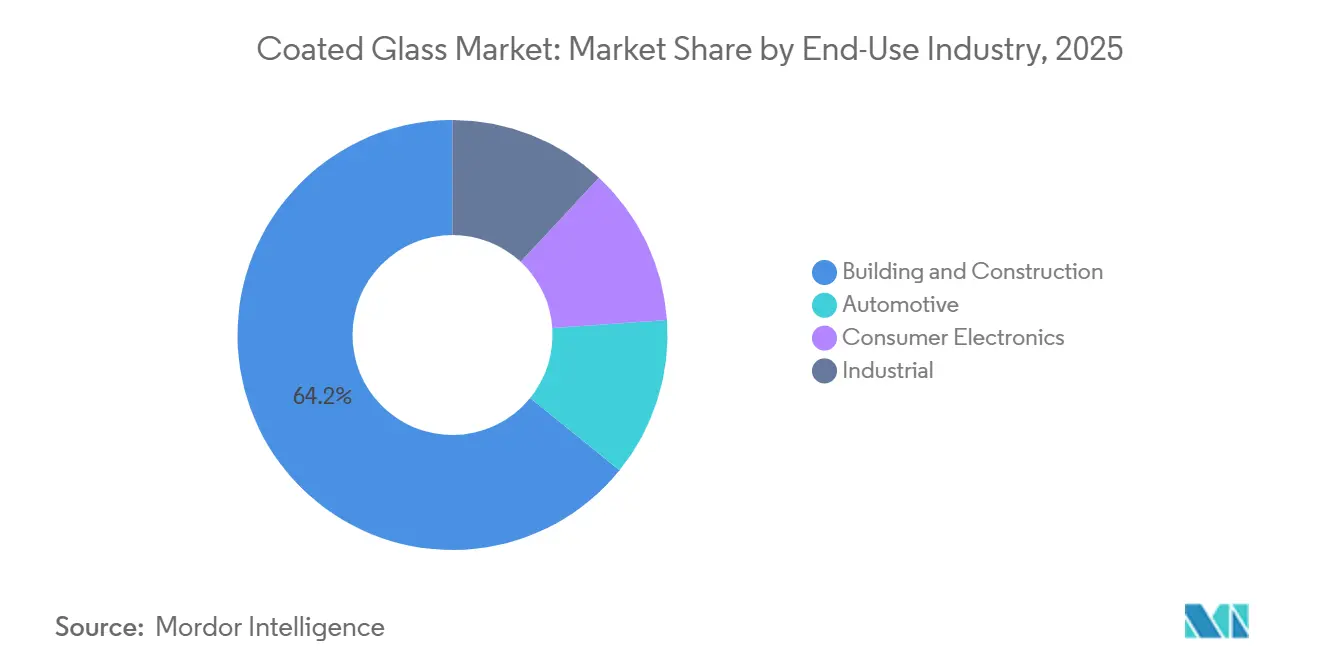

- By end-use industry, building and construction commanded 64.17% of revenue in 2025, while automotive is set to advance at an 8.25% CAGR through 2031.

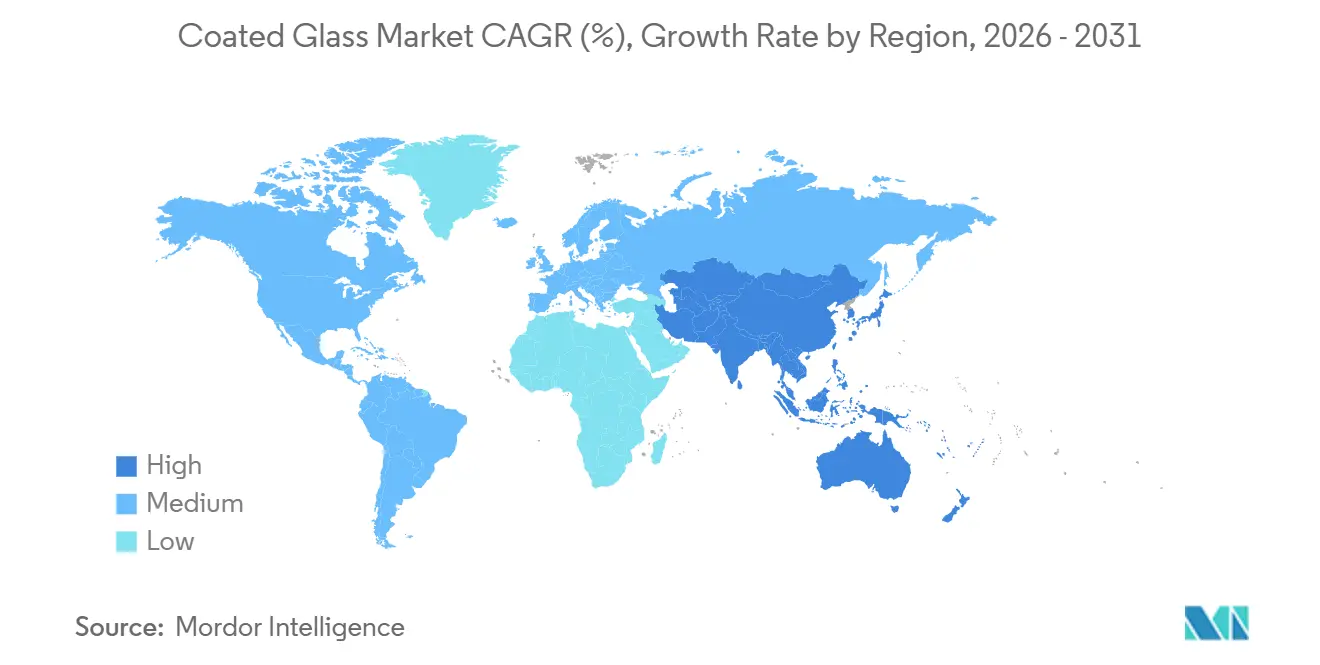

- By geography, Asia-Pacific held 47.52% of the global coated glass market share in 2025 and is also expected to post the highest regional CAGR at 8.41% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Coated Glass Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lower Building Envelope Energy Consumption | +2.1% | Global, with a stronger effect in the EU, China, and North America | Short term (≤ 2 years) |

| Rising Solar-Control Demand from Automotive and Solar Photovoltaic (PV) | +1.5% | Global, with core demand in Asia-Pacific and North America | Medium term (2-4 years) |

| Growth in Electrochromic and Dynamic Coated Glass | +1.0% | North America, Europe, and East Asia | Medium term (2-4 years) |

| Stricter Embodied-Carbon Regulations for Building Materials | +0.7% | Europe and North America, with spillover into the Asia-Pacific | Long term (≥ 4 years) |

| Need for Scratch-Resistant Multifunctional Coatings | +0.5% | Global, with a concentration in Asia-Pacific electronics hubs | Medium term (2-4 years) |

| Expansion of Multifunctional Coatings Combining Thermal, Acoustic, and Self-Cleaning Properties | +0.4% | Europe and North America commercial construction | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Lower Building Envelope Energy Consumption Lifts Low-Emissivity (Low-E) Specification Rates

Building envelope performance is becoming a direct purchasing factor in the coated glass market, as glazing now plays a central role in energy compliance for commercial and residential buildings. The revised Energy Performance of Buildings Directive entered into force in May 2024 and requires member states to incorporate it into national law by May 2026, turning renovation targets and zero-emission building standards into near-term demand indicators for project developers and fabricators[1]European Commission, “Energy Performance of Buildings Directive,” European Commission, energy.ec.europa.eu. China’s GB/T 47553-2026 standard, released in April 2026 and effective from November 2026, is also expected to support the coated glass market by linking building glass selection more closely to measurable energy balance calculations. As efficiency rules become stricter, standard clear glass is losing scope in large commercial tenders, increasing the practical value of certified Low-E products in the coated glass market even before the new supply fully comes online. NSG Group’s decision to invest PLN 160 million (USD 40 million) in a new sputtering coating line in Poland shows how suppliers are placing capacity close to the next wave of regulated renovation demand.

Rising Solar-Control Demand Links EV Range Economics to Coated Glass Specification

The coated glass market is also benefiting as vehicle design and solar generation increase the value of optical and thermal control performance within a single product. In electric vehicles, solar-control and heatable glass can improve cabin temperature management, which is becoming more important as manufacturers aim to protect driving range and increase the feature content of each platform. Fuyao Glass reported that the share of its high-value-added products increased by 5.4 percentage points in 2025, while net profit rose by 24.2%, indicating that coated and function-rich glazing is growing faster than standard vehicle glass lines. On the solar side, anti-reflective coated glass remains important because project developers continue to value improvements that enhance module performance and long-term project economics, helping the coated glass market maintain a broader application base beyond construction. Guardian Glass’s investment in a new high-performance coater in Egypt also shows that suppliers are positioning for solar-control and Low-E demand from both regional construction and nearby export corridors.

Growth in Electrochromic Glass Converts Glazing from Passive to Active Infrastructure

Dynamic coatings are changing the premium segment of the coated glass market by turning glazing from a static envelope material into a responsive control surface. This shift reflects both product performance and early-stage specification, as these systems are typically selected during the building design phase, giving early partners a stronger position than suppliers that compete later on price alone. The Netherlands Organisation for Applied Scientific Research (TNO) reported in June 2026 that its SunSmart thermochromic coating was applied in real buildings and homes for the first time, indicating that smart coatings are moving from test settings into actual use. This development matters for the coated glass market because smart coatings can support thermal control without relying on the same design logic as standard static Low-E stacks, widening the product ladder for premium projects. It also means facade engineers, system integrators, and coating producers are likely to collaborate more closely at earlier project stages, which can reshape competition for specification-led business in high-performance urban buildings.

Stricter Embodied-Carbon Regulations Redefine Procurement Criteria for Coated Glass

Embodied carbon rules are adding a documentation layer to the coated glass market that is becoming nearly as important as thermal and optical performance in major building projects. The delegated regulation adopted in December 2025 requires life-cycle global warming potential disclosure for new buildings above 1,000 m² from January 2028 and for all new buildings from January 2030, giving suppliers a fixed schedule for compliance investment. Leadership in Energy and Environmental Design (LEED) v5 is also raising the bar, as product-specific Environmental Product Declarations (EPDs) are becoming more central to project qualification and reducing the usefulness of broad average data in specification decisions. Cardinal Glass responded by publishing a product-specific Type III EPD for its coated glass range in January 2026, demonstrating that documentation itself is becoming a competitive asset in the coated glass market. Smaller fabricators and converters face greater pressure because coating reformulation, environmental reporting, and customer requalification can restrict time and commercial access at the same time.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capex Requirements and Yield Challenges in Coating Line Investment | -0.6% | Global, with the strongest effect on emerging markets and new entrants | Medium term (2-4 years) |

| Silver and Specialty Oxide Cost Volatility in Sputtering Processes | -0.5% | Global, with margin pressure concentrated in Europe and East Asia | Short term (≤ 2 years) |

| Requalification Burden Following Coating Stack Reformulation | -0.3% | Europe and North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capex Requirements Create a Structural Barrier for Market Entrants

The coated glass market has a high entry barrier, as advanced sputtering lines require large capital outlays, long commissioning periods, and strict yield control once production begins. NSG Group’s Poland project illustrates this factor: a single advanced coating line requires an investment of PLN 160 million (USD 40 million)[2]NSG Group, “Investing in the Future, Advanced Glass Coating Line in Poland,” NSG Group, nsg.com. Şişecam’s continued investments in coated glass lines further indicate that meaningful capacity expansion in this market remains largely limited to companies with strong balance sheets and stable downstream access. In the coated glass market, regional demand can outpace local coated glass supply in emerging economies because many potential entrants lack the time, process expertise, or capital structure needed to build competitive lines quickly. As a result, large incumbents can expand into new regions faster than smaller firms can establish viable domestic capacity, particularly during periods of strong demand when equipment lead times increase.

Silver And Specialty Oxide Price Volatility Undermines Cost Predictability

Silver price volatility remains a key operating risk in the coated glass market because silver-based sputtering targets are essential for high-performance Low-E and solar-control stacks. The input indicates that silver spot prices may move sharply through 2025. The broader volatility pattern is already evident in the London Bullion Market Association’s 2024 survey, which reported a 78% swing between the floor and ceiling of the 2024 trading range. This volatility affects producers because many commercial supply contracts are based on delivery commitments and product performance, while raw material cost shocks can affect margins faster than companies can reprice products. The issue extends beyond silver, as other specialty oxide targets also face supply concentration risks. These risks make cost planning more difficult for companies that lack long-term agreements or clear pass-through terms.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Architectural Glass Holds the Core Volume Base, While Automotive Glass Raises The Technology Value Mix

Architectural glass accounted for 56.44% of revenue in 2025, making it the largest type in the coated glass market. Large-scale commercial and residential building activity supported this position, while energy-efficiency regulations also contributed, as coated architectural glazing has become a common specification in many large projects. The coated glass market continues to rely on this type for its volume base, as office buildings, commercial corridors, public projects, and higher-performance residential developments require a broad mix of Low-E and solar-control products. This base remains important when individual end markets become uneven, as building-related demand spans renovations, new construction, and code-driven upgrades rather than depending on a single product cycle. The same broad demand base also helps leading producers improve plant utilization, supporting investment in newer coating stacks and downstream processing.

Architectural glass leads because of its scale and its alignment with the coated glass industry's key demand drivers: regulation, energy savings, and specification-led procurement. Automotive glass, however, is the fastest-growing type, with a 7.80% CAGR through 2031, indicating that higher-value functionality is expanding faster than traditional construction-led categories. In automotive applications, glass now supports heat management, optical performance, display integration, and sensor compatibility, allowing each new vehicle platform to carry more coating content than before. Fuyao Glass’s 2025 results, including the increase in the share of high-value-added products, support this shift, as they indicate stronger demand for coated and function-rich products rather than growth driven only by higher vehicle output. This dynamic keeps the coated glass market balanced between a large architectural volume base and a faster-moving automotive value stream that is expected to continue reshaping the product mix.

By Coating Type: Low-E Coatings Lead Current Revenue, While Anti-Reflective Coatings Gain the Fastest Momentum

Low-emissivity (Low-E) coatings led the coated glass market with a 42.70% share in 2025, reflecting their central role in energy-efficient windows, facades, and insulated glazing units. Their position comes from their ability to address the coated glass market’s primary regulatory requirement: reducing heat transfer through building envelopes without compromising daylight performance. This makes Low-E products the main revenue anchor for coating producers serving Europe, China, North America, and other regions tightening building performance rules. Reflective and solar-control coatings remain important alongside Low-E products, as they address hot-climate building requirements, glare control, and facade aesthetics in markets where solar gain is a major design concern. Together, these coatings keep the coated glass market linked to compliance and climate-specific performance needs, helping maintain broad demand across different building types.

Anti-reflective coatings are projected to grow at an 8.12% CAGR through 2031, showing how the coated glass market is expanding beyond traditional window applications. Applications where optical clarity directly affects performance, such as automotive sensors, heads-up display systems, camera covers, and photovoltaic glass, provide the strongest support for this growth. As glass surfaces take on more electronic and visual functions, anti-reflective performance becomes more embedded in product requirements. Corning’s January 2025 launch of Gorilla Armor 2, described as the first scratch-resistant anti-reflective glass ceramic for mobile devices, also supports the shift toward coatings that combine visibility, durability, and premium positioning in a single layer stack. As a result, the coated glass market is no longer defined only by thermal efficiency, as optical performance is becoming important in faster-growing product niches.

By Substrate: Float Glass Supports Scale Economics While Laminated Glass Expands on Safety and Performance

Float glass accounted for 62.35% of revenue in 2025, making it the leading substrate across the coated glass market. Its position reflects the basic economics of the value chain, as float glass provides the flatness, clarity, and production scale that coating lines require for large architectural and many automotive applications. This role also makes float glass the operational base for most leading producers, as stable float supply remains closely linked to coating quality, line efficiency, and delivery reliability. In practical terms, much of the coated glass market still depends on float-based output, even when final applications vary by performance level, design, or end use. Tempered glass continues to occupy a middle position where strength and safety requirements matter, but its processing route limits some coating choices compared with float-first production.

Laminated glass is expected to record the highest substrate CAGR at 8.33% through 2031, pointing to the rising importance of safety, acoustic control, and integrated functionality across the coated glass market. Growth is strongest where windshields, roof lights, and advanced vehicle glazing require both optical quality and the ability to carry added features without losing structural performance. NSG Group’s annual results for the fiscal year ended March 2026 highlighted laminated glass expansion for high-precision windshields and roof lights in North American automotive platforms, supporting the view that premium vehicle programs are pulling more volume toward this substrate. Laminated formats also suit commercial buildings that require sound control, impact resistance, or stronger safety performance, giving them a broader demand base than a single end market alone. As a result, the coated glass market is likely to retain float glass as its scale platform, while laminated glass captures more of the premium and higher-growth layer of demand.

By End-Use Industry: Building And Construction Drive Revenue While Automotive Delivers Faster Expansion

Building and construction accounted for 64.17% of revenue in 2025, keeping it ahead of every other end-use category in the coated glass market size. This position reflects the scale of the built environment and the role of coated glass as a core performance material in commercial facades, insulated windows, and higher-standard residential projects. In many markets, permit-stage requirements now focus more closely on U-value, solar heat gain, and visible light performance, which means stakeholders make coating choices earlier and more formally than before. This keeps the coated glass market connected to project design, tender specifications, and compliance documentation rather than only to price-led product selection. It also explains why architectural demand remains the main revenue anchor, even as other end uses grow faster.

Automotive is projected to grow at an 8.25% CAGR through 2031, making it the fastest-growing end use in the coated glass market. This growth differs from older vehicle glass cycles because it depends not only on unit production but also on the amount of electronic, thermal, and optical content built into each vehicle. As vehicles increasingly feature panoramic roofs, display systems, sensor suites, camera modules, and advanced windshield functions, coated glass becomes more valuable per vehicle. Fuyao Glass’s increase in the share of high-value-added products in 2025 supports this direction, as it shows that higher-function products are taking a larger place in the sales mix. Consumer electronics and industrial uses remain smaller, but they still matter because they reward precision coatings and specialized performance, helping the coated glass market build a broader technology profile over time.

Geography Analysis

Asia-Pacific is expected to hold 47.52% of the global coated glass market share in 2025 and is forecast to record the fastest regional CAGR, at 8.41%, through 2031. This positions Asia-Pacific as a key demand region for the coated glass market, supported by large-scale construction activity, manufacturing networks, and rising performance requirements across buildings and vehicles. China remains the region’s largest-volume base, driven by its vast built environment and flat-glass and downstream-processing ecosystem. Although new housing growth may moderate compared with previous years, renovation demand and compliance-led upgrades continue to support demand for coated products. China’s updated green product assessment standard, GB/T 35604-2025, which is set to take effect in November 2025, will add another formal layer to building glass selection in the country’s largest construction applications.

India is emerging as a key growth market within the coated glass market, as commercial corridors and demand for higher-performance buildings drive greater adoption of Low-E and solar-control glass. The region also benefits from a manufacturing model that favors local supply for coated products, especially where transportation, breakage risk, and delivery timelines are critical. In vehicle and electronics-linked applications, Asia-Pacific retains an advantage because producers, component suppliers, and end-use customers are concentrated across the same broader industrial zones. This combination of scale and adjacency continues to support the coated glass market in Asia-Pacific and remains difficult for other regions to match in the near term.

North America and Europe remain regulatory and technology reference points for the coated glass market, although the input does not assign them specific regional shares. In Europe, the May 2026 national transposition timeline under the revised Energy Performance of Buildings Directive (EPBD) is expected to support steady procurement of high-performance architectural products across the region. NSG Group’s new coating line in Poland and Şişecam’s coated glass investments in Europe indicate that suppliers are placing capacity in markets where policy support and renovation demand are likely to remain firm. In North America, demand for higher-performing architectural products and increased focus on product documentation, including Environmental Product Declaration (EPD)-backed materials for commercial projects, support the coated glass market.

South America, the Middle East and Africa, and the rest of Europe remain smaller parts of the coated glass market, but their outlook remains positive. South America benefits from improving construction activity, although currency volatility and energy costs can limit the pace of coated glass demand growth. In the Middle East and Africa, Guardian Glass’s investment in a high-performance coater in Egypt indicates a gradual shift from higher import dependence toward more local or regional supply options. This shift can reduce supply delays and improve the availability of higher-performance coated products across nearby building markets.

Competitive Landscape

The coated glass market is moderately consolidated. A limited group of vertically integrated producers competes for the largest building and automotive contracts, while many smaller regional processors and converters serve local demand. This creates a layered market structure. Scale plays a major role in float supply, sputtering technology, and multinational customer relationships, while fragmentation remains visible at the downstream level. Large suppliers are positioned to combine substrate access, coating expertise, certification support, and multinational delivery coverage in a single offering. This capability is important when customers require the same coated glass product family to qualify across multiple countries or project sites. It also explains why capacity additions, documentation quality, and product mix upgrades are as important as price in competitive positioning.

One competitive pattern in the coated glass market is the addition of capacity in regions where regulated architectural demand is strongest. Şişecam is expected to commission three coated glass lines within the first six months of 2026 and increase its total global coated glass capacity to 48.1 million square meters. This move indicates an effort to strengthen supply reach in a market where timing and proximity influence project wins. Another pattern is the use of product documentation as a market access tool, as demonstrated by Cardinal Glass’s planned January 2026 publication of a product-specific Type III EPD for its coated glass range. A third pattern is the growth of higher-value automotive glazing, supported by Fuyao Glass’s expected increase in high-value-added products during 2025.

Ownership and capital strategy are also becoming more important in the coated glass market, as companies need long-term funding for plant upgrades, premium product lines, and cleaner production systems. Apollo Funds is expected to announce a USD 3.7 billion strategic investment in NSG Group in March 2026, with completion expected around March 2027. This investment could give NSG additional flexibility to accelerate high-value architectural, automotive, and solar glass programs. This development matters because the next stage of competition is likely to depend on which companies can scale energy-efficient, compliance-ready, and application-specific coated products while maintaining cost discipline. The coated glass market still offers opportunities in dynamic coatings, documented low-carbon products, and advanced automotive glazing. However, companies that move first on qualification and customer integration are likely to hold a stronger competitive position.

Coated Glass Industry Leaders

Saint-Gobain

AGC Inc.

Guardian Industries

Nippon Sheet Glass Co., Ltd.

Fuyao Glass Industry Group Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Şişecam commissioned a coated glass production line at its Tarsus, Turkey, complex, with an annual capacity of 7 million square meters and an investment of USD 26 million. The company plans to export products from the line to the Middle East, North Africa, Eastern Europe, and South Asia. The addition increased Şişecam’s global coating capacity to 48.1 million square meters across seven lines.

- May 2026: Gujarat Guardian Limited (GGL), a joint venture between Guardian Industries and Modi Rubber Limited, broke ground on its second float glass line and a wet coating facility with a capacity of 72,000 metric tons per year at Ankleshwar, India. The facility, expected to be completed by mid-2028, will produce mirror glass, Low-E glass, and value-added coated glass for the Indian architectural market.

Global Coated Glass Market Report Scope

Coated glass has thin metallic or chemical layers applied to its surface to improve properties such as thermal insulation, solar control, and durability. It is used in architectural design and scientific research to manage light, block UV rays, and improve energy efficiency.

The coated glass market is segmented by type, coating type, substrate, end-use industry, and geography. By type, the market is segmented into architectural glass, automotive glass, industrial glass, and consumer glass. By coating type, the market is segmented into reflective coatings, low-E coatings, solar control coatings, and anti-reflective coatings. By substrate, the market is segmented into float glass, tempered glass, and laminated glass. By end-use industry, the market is segmented into building and construction, automotive, consumer electronics, and industrial. The report also covers market size and forecasts for coated glass across 16 countries in major regions. The market sizes and forecasts are provided in terms of value (USD).

| Architectural Glass |

| Automotive Glass |

| Industrial Glass |

| Consumer Glass |

| Reflective Coatings |

| Low-E Coatings |

| Solar Control Coatings |

| Anti-Reflective Coatings |

| Float Glass |

| Tempered Glass |

| Laminated Glass |

| Building and Construction |

| Automotive |

| Consumer Electronics |

| Industrial |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Type | Architectural Glass | |

| Automotive Glass | ||

| Industrial Glass | ||

| Consumer Glass | ||

| By Coating Type | Reflective Coatings | |

| Low-E Coatings | ||

| Solar Control Coatings | ||

| Anti-Reflective Coatings | ||

| By Substrate | Float Glass | |

| Tempered Glass | ||

| Laminated Glass | ||

| By End-Use Industry | Building and Construction | |

| Automotive | ||

| Consumer Electronics | ||

| Industrial | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is current market size of Coated Glass Market?

The Coated Glass Market size was valued at USD 44.37 billion in 2025 and is estimated to grow from USD 47.06 billion in 2026 to reach USD 68.12 billion by 2031, at a CAGR of 7.68% during the forecast period (2026-2031).

Which product type contributes the most revenue?

Architectural glass led with a 56.44% share in 2025, driven by building efficiency rules and large construction volumes, which kept it as the core demand base.

Which category is growing the fastest?

Anti-reflective coatings are projected to grow at an 8.12% CAGR through 2031, supported by automotive optics, display uses, and solar glass demand.

Why is Asia-Pacific the leading region?

Asia-Pacific accounted for 47.52% of global revenue in 2025 and posted the fastest regional growth, driven by large construction demand, manufacturing scale, and tighter performance standards.

Page last updated on: