Co-Packaged Memory Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 0.56 Billion |

| Market Size (2031) | USD 1.77 Billion |

| Growth Rate (2026 - 2031) | 25.88% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Co-Packaged Memory Market Analysis by Mordor Intelligence

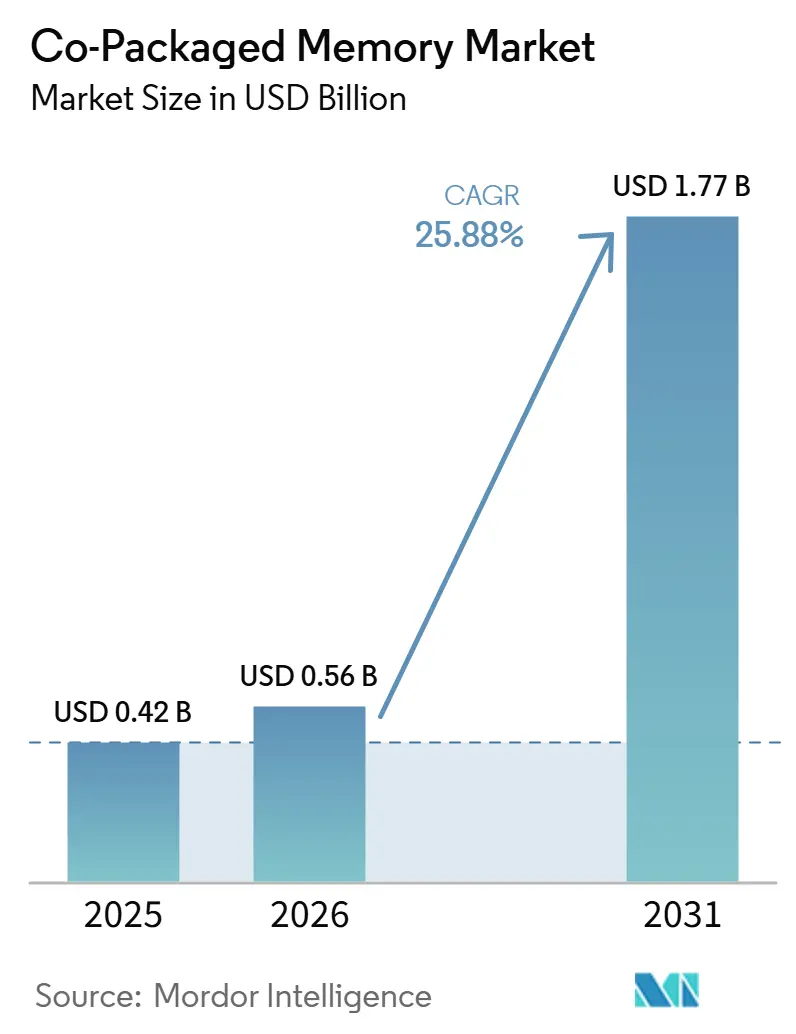

The co-packaged memory market size is projected to be USD 0.42 billion in 2025, USD 0.56 billion in 2026, and reach USD 1.77 billion by 2031, growing at a CAGR of 25.88% from 2026 to 2031. The growth pattern reflects a deeper change in accelerator design, because AI systems now need far more memory bandwidth and far shorter data paths than conventional off-package memory links can deliver at scale. Commercial HBM4 production in 2026 shows that the co-packaged memory market is moving on a product cycle that is tied to AI server buildouts, not to the older demand swings that shaped prior memory expansions. Supply remains tight because advanced packaging lines, TSV-heavy stack assembly, and multi-die qualification still limit how quickly manufacturers can convert announced spending into usable output. Competition is also changing, because leadership now depends on the ability to combine memory design, base-die logic, packaging integration, and customer-specific qualification under one roadmap. That leaves the strongest opening in the co-packaged memory market with suppliers that can secure packaging capacity, support custom accelerator programs, and serve both the highest-bandwidth AI workloads and the broader wave of cloud inference deployments.

Key Report Takeaways

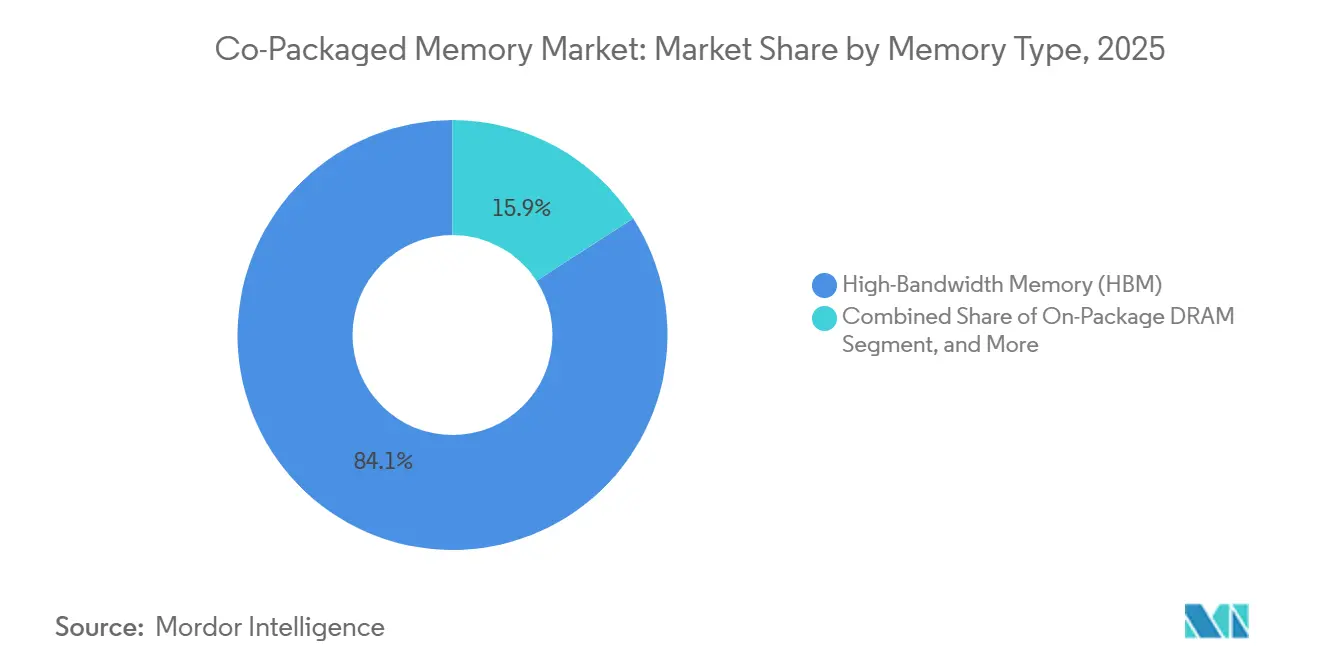

- By memory type, HBM held 84.11% of the co-packaged memory market share in 2025, while on-package DRAM is projected to expand at a 25.91% CAGR through 2031.

- By packaging architecture, 2.5D interposer-based packaging accounted for 70.34% share of the co-packaged memory market size in 2025, while 3D stacked packaging is expected to grow at a 26.13% CAGR through 2031.

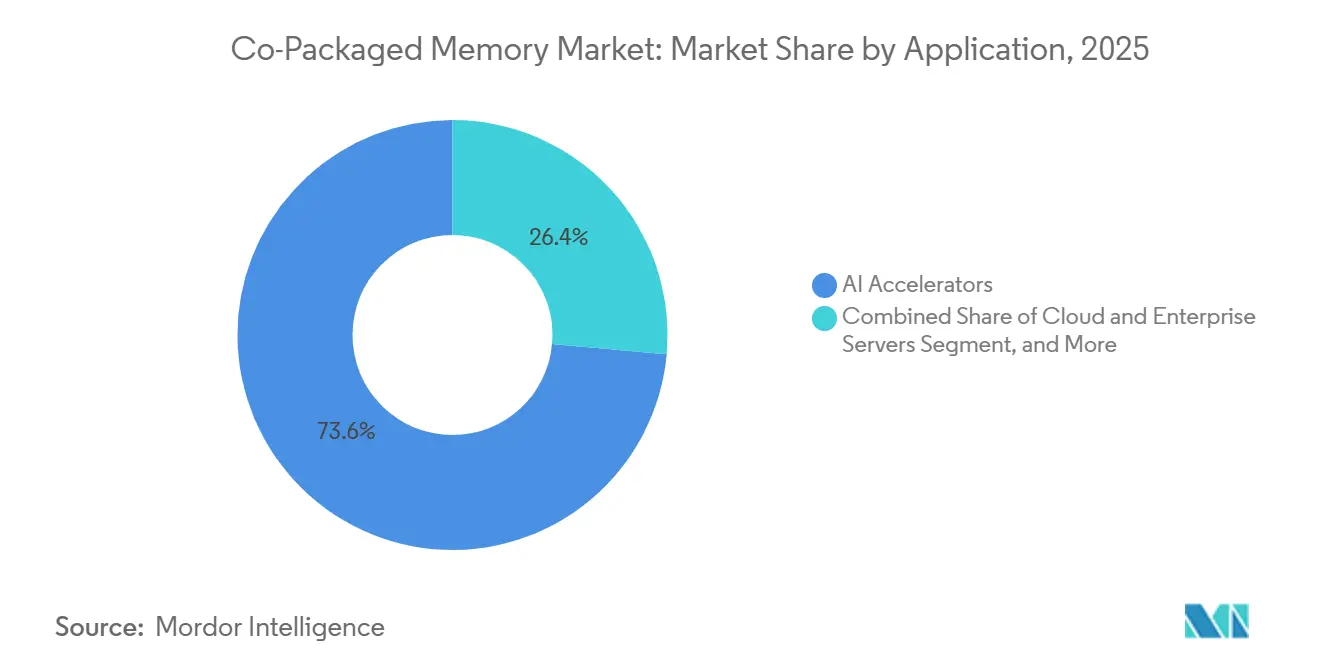

- By application, AI accelerators captured 73.57% of revenue in 2025, while cloud and enterprise server deployments are forecast to expand at a 26.11% CAGR through 2031.

- By customer type, semiconductor and AI chip vendors held 55.12% of revenue in 2025, while hyperscalers and cloud service providers recorded the highest projected CAGR at 26.32% through 2031.

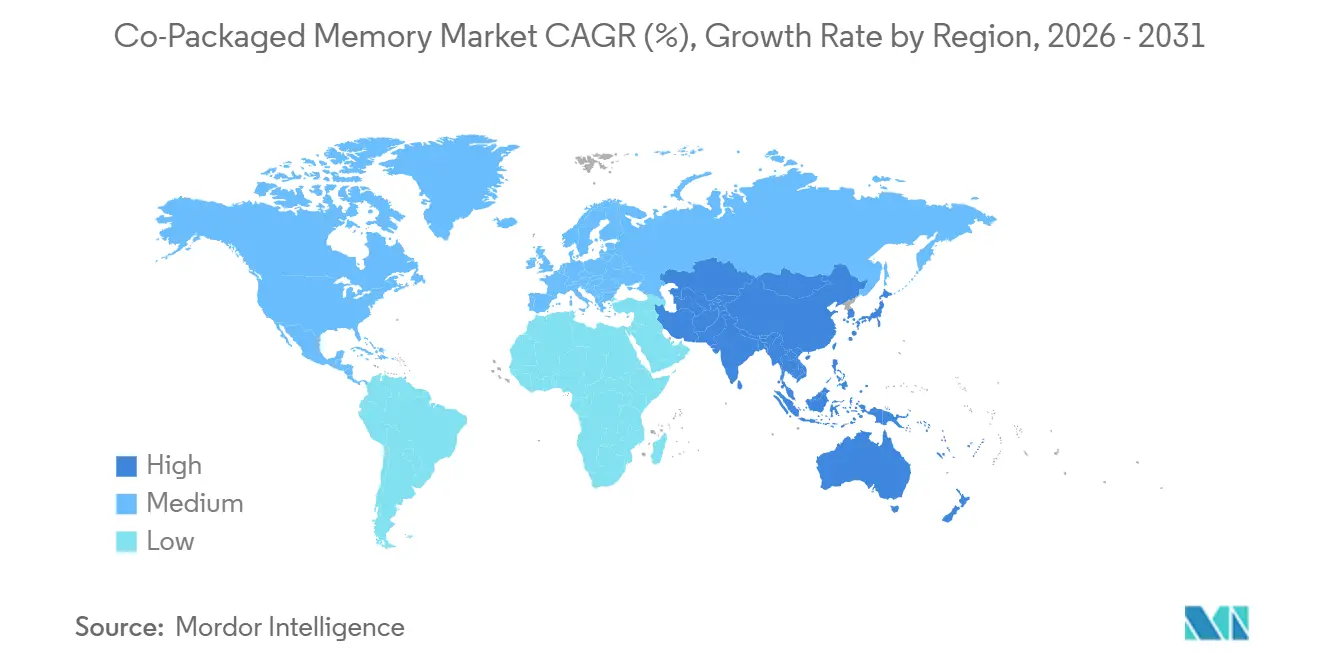

- By geography, Asia-Pacific represented 56.58% of revenue in 2025 and is also projected to advance at the fastest regional CAGR of 26.27% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Co-Packaged Memory Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AI Server Memory Density Requirements | +8.5% | Global, with highest intensity in North America and Asia-Pacific | Short term (≤ 2 years) |

| Shift Toward HBM-Centric Package Architectures | +6.5% | Asia-Pacific core, with spill-over to North America | Medium term (2-4 years) |

| Co-Integration of Logic and Memory in Chiplet Designs | +5.0% | Global, with R&D concentrated in Asia-Pacific and North America | Medium term (2-4 years) |

| Hyperscaler Preference for Lower Latency and Higher Bandwidth Stacks | +3.5% | North America, with procurement impact across Asia-Pacific supply chain | Short term (≤ 2 years) |

| Government Subsidies for Advanced Packaging Ecosystems | +2.0% | North America, Asia-Pacific, and Europe | Long term (≥ 4 years) |

| Memory-Adjacent Power Efficiency Gains in Accelerated Computing | +1.5% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

AI Server Memory Density Requirements

AI training and inference systems no longer scale mainly through raw compute, because memory bandwidth now limits how effectively accelerator cores can stay utilized across large model workloads. NVIDIA’s Blackwell architecture carries 192 GB of HBM3e and delivers 8 TB/s of memory bandwidth, which shows how close memory and compute must sit in current high-end server designs.[1]NVIDIA Corporation, “Blackwell Architecture Technical Overview and Product Disclosures,” NVIDIA Investor Relations / Product Pages, nvidia.com Samsung stated in 2026 that its commercial HBM4 can deliver up to 3.3 TB/s per stack and improve power efficiency by 40% versus HBM3E, which supports the move toward denser memory attached directly to compute logic.[2]Samsung Electronics, “Samsung Ships Industry-First Commercial HBM4 With Ultimate Performance for AI Computing,” Samsung Global Newsroom, news.samsung.com That shift matters because each new accelerator generation consumes more HBM capacity per chip, which turns every server refresh into a larger memory event rather than a simple processor upgrade. As a result, the co-packaged memory market is expanding not only because AI server volumes are rising, but also because each installed unit now carries a much heavier memory content load than earlier platforms. This keeps demand firm even when buyers become selective on broader server spending, since memory proximity now affects model throughput, latency, and power draw at the system level.

Shift Toward HBM-Centric Package Architectures

HBM-centered packaging has moved from a premium design choice into the default layout for the highest-bandwidth AI platforms, because conventional board-level memory cannot deliver comparable throughput without far larger power and signal penalties. NVIDIA product disclosures and package-level technical documentation show that multi-stack HBM designs already provide bandwidth far above conventional DDR-based approaches, which explains why HBM now dominates the co-packaged memory market by memory technology. The co-packaged memory market also benefits from the fact that packaging standards and process flows are still evolving in ways that protect near-term manufacturability, not just peak performance. Samsung noted that HBM4 entered commercial production in 2026 with meaningful performance gains over HBM3E, which indicates that suppliers are still extracting major value from current stack designs before the next bonding transition becomes unavoidable. That matters for buyers because it allows near-term platform growth to stay anchored in proven HBM integration paths while keeping the next step toward more complex bonding methods tied to later generations. It also reinforces why the co-packaged memory market is seeing demand concentrate around suppliers that can align memory, packaging, and accelerator roadmaps without forcing abrupt design changes on customers.

Co-Integration of Logic and Memory in Chiplet Designs

The co-integration of logic into memory structures changes the role of memory from a passive bandwidth source into an active part of the system design, especially in high-density accelerator packages. Samsung stated that its HBM4 uses a 4 nm logic base die, which means more control and interface functionality now sits inside the HBM stack itself rather than outside the memory package. UCIe 3.0, released in August 2025, doubled the maximum die-to-die data rate to 64 GT/s and added runtime power-state improvements, which broaden the ways memory and logic chiplets can work together inside the same package.[3]UCIe Consortium, “UCIe 3.0 Specification Release,” UCIe Industry Consortium, uciexpress.org This matters because the co-packaged memory market is no longer defined only by how many DRAM dies can be stacked, but also by how much control logic, interoperability, and system tuning can be embedded in each design. That lifts the bar for participation because memory suppliers now need access to strong logic process technology, package integration capability, and reusable interface IP at the same time. It also supports durable concentration at the top of the co-packaged memory market, since incumbents can spread these development costs across larger customer programs and longer roadmap commitments.

Hyperscaler Preference for Lower Latency and Higher Bandwidth Stacks

Hyperscalers are now shaping memory package requirements directly, because their custom accelerator programs demand bandwidth and latency profiles that standard catalog parts do not always match. NVIDIA’s March 2026 investment in Marvell showed how compute, networking, and memory roadmaps are being tied together more tightly across AI server racks, not handled as separate hardware layers. That matters because once a supplier co-develops a memory-based die or package design around a large customer’s accelerator plan, the commercial relationship becomes harder to replace than a normal component contract. The co-packaged memory market, therefore, gains momentum from a form of customer lock-in that is based on joint qualification, package tuning, and software-aligned infrastructure planning. This pushes suppliers to reserve capacity, deepen engineering support, and build longer planning cycles around a small group of very large buyers. It also widens the difference between vendors that can support custom high-bandwidth programs and those that remain limited to standard memory supply.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Yield Losses in TSV and Multi-Die Integration | -4.5% | Global, most acute in Asia-Pacific HBM production lines | Short term (≤ 2 years) |

| Limited Advanced Packaging Capacity for Memory Integration | -3.0% | Asia-Pacific, with ripple effects globally | Medium term (2-4 years) |

| Thermal Dissipation and Reliability Constraints | -2.0% | Global, with the greatest pressure in dense AI data center deployments | Medium term (2-4 years) |

| High Capital Intensity and Qualification Cycles | -1.5% | Global, with disproportionate burden on new entrants | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Yield Losses in TSV and Multi-Die Integration

Yield loss remains one of the strongest checks on near-term expansion, because co-packaged memory stacks accumulate risk across thousands of vertical connections and multiple bonded dies. Research from the IMAPS Device Packaging Conference showed that a single HBM layer may require 5,000 to 10,000 TSVs, and that a 12-layer stack at a 95% per-layer success rate can fall to a total stack yield near 54%. That math matters because scrap not only removes finished output, but it also consumes silicon, assembly time, materials, and scarce packaging tools that could have gone to usable product. The challenge becomes harder as interface widths rise and stack heights move from 12 layers toward 16 layers, because more density usually brings more defect sensitivity and more process tuning. Hybrid bonding will likely improve long-term scaling, but peer-reviewed work shows that bonding pressure, surface condition, and interface quality remain central to thermal and reliability outcomes. This means the co-packaged memory market can attract strong demand and still face slower usable supply growth when yields on next-generation packages take time to stabilize.

Limited Advanced Packaging Capacity for Memory Integration

Advanced packaging capacity remains a structural bottleneck, because wafer output alone does not create sellable co-packaged memory products without enough 2.5D and 3D integration lines behind it. The U.S. Department of Commerce and NIST said in January 2025 that USD 1.4 billion in final NAPMP awards would support the next generation of U.S. semiconductor advanced packaging, which underscores how serious the capacity gap had become. ASE also stated that its advanced packaging revenue is expected to double to USD 3.2 billion in 2026, which shows that outsourced providers see strong and immediate demand for HBM-related integration capacity. Amkor’s 2026 investor materials pointed to USD 2.5 billion to USD 3 billion in capital expenditure focused mainly on 2.5D and high-density fan-out capacity in South Korea and Taiwan, with the Arizona campus moving toward later installation and production milestones. Even with that spending, the bottleneck matters because major AI chip programs still compete for the same limited pool of advanced package assembly, testing, and interposer-related capacity. This keeps pricing firm, slows some rollout schedules, and gives packaging access a larger role in the co-packaged memory market than chip design strength alone would suggest.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Memory Type: HBM Dominance Sustains as On-Package DRAM Scales Outward

HBM held 84.11% of the co-packaged memory market share in 2025, which reflects its central role in systems where bandwidth is the main performance constraint rather than simple memory capacity. The co-packaged memory market keeps leaning toward HBM because current AI accelerators demand short interconnect paths and far higher throughput than off-package DRAM can supply at comparable power efficiency. NVIDIA’s Blackwell platform illustrates that point, because its HBM-rich design reaches 8 TB/s of memory bandwidth and depends on close package-level integration between compute and memory. Samsung also stated that commercial HBM4 delivers up to 3.3 TB/s per stack with 40% better power efficiency than HBM3E, which reinforces why HBM remains the default path for high-end AI infrastructure in the co-packaged memory market. The current lead is therefore not only a reflection of product availability, but it is also tied to the fact that no other memory format in the 2025 to 2026 window matches HBM’s blend of bandwidth density, package proximity, and accelerator compatibility.

On-package DRAM is projected to grow at a 25.91% CAGR from 2026 to 2031, which makes it the fastest-rising memory category inside the co-packaged memory market even though it starts from a much smaller base. AMD’s Versal Premium Gen 2 Memory on Package design shows why, because it integrates up to 32 GB of LPDDR5X memory on package, delivers 288 GB/s bandwidth, and uses 60% less board area for customers that need a longer product life and a different cost profile than HBM. This opens room in the co-packaged memory industry for deployments in adaptive compute, edge AI, automotive, and long-lifecycle embedded systems where HBM supply, refresh cadence, and cost remain harder to justify. Emerging memory technologies still sit earlier in the adoption curve, because packaging ecosystems, interoperability, and process flows are not yet aligned to absorb them at volume across mainstream accelerator programs. UCIe 3.0 provides an important technical anchor by increasing die-to-die data rates and adding runtime power controls, which helps define how future memory forms may plug into package-level designs. The result is a two-track co-packaged memory market where HBM remains the clear revenue engine while on-package DRAM broadens the addressable base without displacing HBM at the top end.

By Packaging Architecture: 2.5D Interposer Dominates as 3D Stacking Sets the Pace

2.5D interposer-based packaging accounted for 70.34% share of the co-packaged memory market size in 2025, which shows that the leading commercial path still favors a layout that places compute dies and multiple memory stacks on a shared interposer. The co-packaged memory market benefits from this architecture because it balances very high bandwidth with a manufacturing base that is more mature than full 3D alternatives in current production programs. Interposer-based designs also fit the way most present accelerator platforms are qualified, since they allow dense memory placement without yet forcing the most demanding thermal and bonding conditions seen in deeper vertical stacks. That is why competing approaches such as embedded bridge and fan-out or RDL packaging remain more relevant in networking, telecom, and cost-sensitive compute applications than in the top tier of AI training infrastructure. The present dominance of 2.5D is therefore closely tied to practical manufacturability, packaging line availability, and customer comfort with known process windows across the co-packaged memory market.

3D stacked packaging is projected to expand at a 26.13% CAGR from 2026 to 2031, because it offers a path to even tighter integration when hybrid bonding, thermal control, and yield management improve enough for broader use. Research presented at IEEE ECTC 2025 showed that TSMC’s SoIC Cool-Stacking approach reduced thermal resistance by 77% versus micro-bump schemes, which points to a stronger long-term case for high-density 3D package designs. At the same time, imec showed in late 2025 that a 3D HBM-on-GPU layout can drive far higher peak temperatures than a comparable 2.5D package unless system and technology co-optimization is applied, which explains why adoption still depends on cooling and design refinement rather than on package density alone. This means the co-packaged memory market will likely move into 3D in stages, with the earliest traction centered on applications that can justify the engineering effort, thermal management cost, and slower yield ramp. Equipment lead times and learning curves for hybrid bonding also keep 2.5D firmly in front for now, even as 3D stacked formats set the growth pace. The co-packaged memory market, therefore, shows a split between today’s dominant production standard and tomorrow’s most aggressive performance path.

By Application: AI Accelerators Anchor Revenue as Cloud Server Demand Broadens

AI accelerators held 73.57% of application revenue in 2025, which makes them the main demand center for the co-packaged memory market in the current cycle. This concentration exists because the most advanced training systems and many high-end inference platforms need HBM placed close to compute dies to sustain the throughput required by large models and heavy parallel workloads. NVIDIA’s Blackwell platform and other high-bandwidth accelerator programs show that package-level memory design is now inseparable from processor performance, not an optional supporting feature. High-performance computing and supercomputing remain smaller in revenue terms, yet they still matter because they reward the same bandwidth-per-watt and latency characteristics that pushed co-packaged memory into mainstream AI hardware. Data center networking and telecom are also becoming more relevant as switch and interconnect silicon absorb larger data flows, while automotive and edge deployments remain earlier-stage users that value footprint efficiency and controlled bandwidth in more specialized systems.

Cloud and enterprise server deployments are projected to expand at a 26.11% CAGR through 2031, which marks them as the fastest-growing application path in the co-packaged memory market. That growth is important because it shows demand spreading beyond the narrow core of training accelerators and into a broader installed base of inference, custom silicon, and mixed-workload server systems. AMD’s 2026 Memory on Package announcement supports this direction, since it highlights a package-level memory approach that fits applications needing strong bandwidth in a smaller footprint without always requiring full HBM economics. As hyperscalers design more inference hardware around their own workload mix, the co-packaged memory market is likely to serve a wider spread of memory types and performance bands within the same cloud environment. This broadening makes application demand less dependent on one hardware category while still leaving AI accelerators as the immediate center of revenue. It also rewards suppliers that can support both HBM-heavy systems and lighter on-package DRAM deployments across the co-packaged memory industry.

By Customer Type: Semiconductor and AI Chip Vendors Lead but Hyperscalers Drive Growth

Semiconductor and AI chip vendors represented 55.12% of revenue in 2025, which confirms that the main buying power in the co-packaged memory market still sits with the companies that define accelerator package architecture from the start. These firms decide stack height, interface targets, power budgets, and package layout, and those choices then shape demand for memory fabrication, advanced packaging, and outsourced testing across the rest of the value chain. Their leadership also reflects the fact that many system customers still rely on chip vendors to bring fully qualified designs to market before committing to large deployment cycles. In that sense, the co-packaged memory market remains supply-led at the design stage even when end demand is ultimately driven by AI service providers and data center operators. The revenue base, therefore, stays concentrated among customers that have both large silicon programs and the engineering ability to influence package-level memory standards.

Hyperscalers and cloud service providers are projected to expand at a 26.32% CAGR through 2031, which makes them the fastest-growing customer group in the co-packaged memory market. Their rise matters because large cloud operators now influence memory design more directly through custom accelerator programs, qualification requirements, and platform-level planning around inference and training infrastructure. NVIDIA’s investment in Marvell in 2026 highlights that server-scale AI systems are being built through deeper ties among compute, networking, and memory ecosystems, which increases the strategic value of customers that control large infrastructure roadmaps. Once these buyers co-develop package and memory features with suppliers, switching costs rise because the value sits in validated integration rather than in a simple component order. Server, storage, and networking OEMs remain important channels for enterprise deployment, while automotive and industrial electronics companies represent a smaller but meaningful group where lifecycle, reliability, and thermal requirements matter as much as headline bandwidth. This shift gives the co-packaged memory market a stronger custom-design character, where winning future revenue depends on fitting tightly into a few large customer roadmaps.

Geography Analysis

Asia-Pacific held 56.58% of the co-packaged memory market share in 2025 and is projected to record the fastest CAGR at 26.27% through 2031, which reflects the region’s deep concentration in HBM production, foundry capability, and advanced package assembly. The co-packaged memory market remains heavily anchored in South Korea and Taiwan because Samsung Electronics and SK Hynix lead memory supply, while Taiwan stays central to interposer-led packaging and outsourced semiconductor assembly. This regional structure matters because it brings design execution, memory fabrication, and package-level integration into close physical proximity, which shortens iteration cycles for high-bandwidth AI platforms. China is evolving in a different way, with JCET planning a CNY 7.8 billion (USD 1.15 billion) advanced packaging facility in Shanghai Lingang to serve computing and automotive electronics customers as local packaging ambition rises. The co-packaged memory market, therefore, draws much of its scale from Asia-Pacific not only because factories are located there, but also because the region has the most complete operating chain for HBM-linked packaging today.

North America represents a smaller production base in the co-packaged memory market, yet it holds rising strategic weight because many hyperscalers, AI chip designers, and advanced packaging policy programs are concentrated there. NIST stated in January 2025 that the U.S. Department of Commerce finalized USD 1.4 billion in NAPMP awards, including support for the Advanced Packaging Piloting Facility in Arizona and several substrate and fan-out processing programs. Amkor’s investor materials showed that its Arizona advanced packaging campus remained on track for tool installation in 2027 and production start in 2028, which gives North America a clearer route toward domestic 2.5D packaging and HBM integration capacity. That means the region’s role in the co-packaged memory market is still stronger on demand, design, and policy than on immediate supply, but the effort to change that balance is now clearly underway.

Europe remains smaller in direct production terms, though it carries strategic value through process research and package-level thermal work that can influence later commercial adoption. imec’s published 2025 work on 3D HBM-on-GPU thermal mitigation shows why Europe matters to the co-packaged memory market even without equivalent scale in HBM manufacturing capacity. Japan, while counted within Asia-Pacific, has become more notable through Micron’s HBM-related ramp activity, which adds another production node to the broader regional supply base. Middle East and Africa remain early in adoption and largely demand-led, while South America has no meaningful production presence in the current forecast window. This leaves the co-packaged memory market geographically concentrated, with diversification efforts growing but not yet strong enough to alter the center of gravity away from Asia-Pacific.

Competitive Landscape

The co-packaged memory market has a dual competitive structure, with extreme concentration in qualified HBM supply and wider but still tightening competition in advanced packaging services. Samsung Electronics, SK Hynix, and Micron collectively define the top memory tier because they are the only commercially qualified HBM suppliers serving the leading AI accelerator build cycle described in the report. Samsung’s 2026 HBM4 launch is strategically important because it combines commercial output, higher bandwidth per stack, stronger power efficiency, and a logic base die approach that supports tighter integration at the package level. That gives the co-packaged memory market a leadership pattern where memory suppliers compete not only on wafer output, but also on how much of the surrounding design and packaging stack they can control. The result is a market where supply qualification, package integration, and customer-specific development create stronger barriers than simple bit production alone.

Competition becomes broader at the packaging services layer, where ASE, Amkor, JCET, and other advanced providers are trying to capture more of the value created by AI-related package complexity. ASE said its advanced packaging revenue is expected to double to USD 3.2 billion in 2026, which shows that outsourced packaging specialists see room to expand as HBM integration and multi-die assembly needs rise. Amkor’s 2026 capital plan of USD 2.5 billion to USD 3 billion, centered on 2.5D and high-density fan-out expansion, points to the same competitive push in South Korea, Taiwan, and later the United States. JCET’s Shanghai Lingang plan adds another layer of competition by strengthening domestic Chinese packaging capacity for high-growth computing and automotive electronics programs.

The next competitive edge in the co-packaged memory market will likely come from who can shorten the gap between advanced memory supply and usable package output while meeting tighter thermal and reliability demands. IEEE ECTC 2025 results on SoIC Cool-Stacking and imec’s thermal work both show that package design quality is now a direct performance variable rather than a back-end manufacturing detail. NVIDIA’s investment in Marvell also shows that ecosystem control is widening beyond memory and packaging into the networking layer that links AI racks together. This leaves the co-packaged memory market concentrated at the top, but still open to meaningful strategic gains in packaging capacity, thermal engineering, interface IP, and customer-specific integration support.

Co-Packaged Memory Industry Leaders

SK hynix Inc.

Samsung Electronics Co., Ltd.

Micron Technology, Inc.

Taiwan Semiconductor Manufacturing Company Limited

Intel Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Samsung Electronics delivered the industry’s first 12-layer HBM4E samples, 48 GB and up to 3.6 TB/s per stack at 16 Gbps, to major global customers, with SK Hynix following in June 2026 with its own HBM4E 12-layer samples incorporating TSMC 3 nm process base dies.

- May 2026: Amkor Technology secured an additional 67 acres adjacent to its Arizona advanced packaging campus, expanding the site’s long-term capacity footprint, while remaining the only scaled OSAT constructing full-turnkey advanced packaging facilities in the United States.

- April 2026: SK Hynix broke ground on a large-scale advanced packaging facility in Cheongju Technopolis, South Korea, establishing a dedicated HBM back-end processing hub that will accelerate its capacity ramp for HBM4 packaging operations.

- February 2026: Micron Technology finalized its USD 2 billion acquisition of PSMC’s P5 fab in Tongluo, Taiwan, converting the brownfield facility into a dedicated HBM4 capacity addition and securing critical advanced packaging floor space ahead of U.S. capacity coming online in 2027.

Global Co-Packaged Memory Market Report Scope

The co-packaged memory market refers to advanced semiconductor packaging solutions that integrate memory chips more closely with processors, accelerators, or other logic components within the same package. This architecture reduces data transfer distance, lowers latency, and improves bandwidth efficiency compared to traditional separate-chip designs.

The Co-Packaged Memory Market Report is Segmented by Memory Type (HBM, On-Package DRAM, Emerging Memory Technologies), Packaging Architecture (2.5D Interposer-Based Packaging, Embedded Bridge-Based Packaging, Fan-Out / RDL-Based Packaging, and 3D Stacked Packaging), Application (AI Accelerators, High-Performance Computing and Supercomputing, Cloud and Enterprise Servers, Data Center Networking and Telecom Infrastructure, and Automotive and Edge Compute Platforms), Customer Type (Semiconductor and AI Chip Vendors, Hyperscalers and Cloud Service Providers, Server, Storage, and Networking OEMs, and Automotive and Industrial Electronics Companies), and Geography (North America, Europe, Asia-Pacific, South America, MEA). The Market Forecasts are Provided in Terms of Value (USD)

| High-Bandwidth Memory (HBM) |

| On-Package DRAM |

| Emerging Memory Technologies |

| 2.5D Interposer-Based Packaging |

| Embedded Bridge-Based Packaging |

| Fan-Out / RDL-Based Packaging |

| 3D Stacked Packaging |

| AI Accelerators |

| High-Performance Computing and Supercomputing |

| Cloud and Enterprise Servers |

| Data Center Networking and Telecom Infrastructure |

| Automotive and Edge Compute Platforms |

| Semiconductor and AI Chip Vendors |

| Hyperscalers and Cloud Service Providers |

| Server, Storage, and Networking OEMs |

| Automotive and Industrial Electronics Companies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Southeast Asia | |

| Rest of Asia-Pacific | |

| South America | |

| Middle East and Africa |

| By Memory Type | High-Bandwidth Memory (HBM) | |

| On-Package DRAM | ||

| Emerging Memory Technologies | ||

| By Packaging Architecture | 2.5D Interposer-Based Packaging | |

| Embedded Bridge-Based Packaging | ||

| Fan-Out / RDL-Based Packaging | ||

| 3D Stacked Packaging | ||

| By Application | AI Accelerators | |

| High-Performance Computing and Supercomputing | ||

| Cloud and Enterprise Servers | ||

| Data Center Networking and Telecom Infrastructure | ||

| Automotive and Edge Compute Platforms | ||

| By Customer Type | Semiconductor and AI Chip Vendors | |

| Hyperscalers and Cloud Service Providers | ||

| Server, Storage, and Networking OEMs | ||

| Automotive and Industrial Electronics Companies | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Southeast Asia | ||

| Rest of Asia-Pacific | ||

| South America | ||

| Middle East and Africa | ||

Key Questions Answered in the Report

What is the current and forecast size of the co-packaged memory market?

The co-packaged memory market was valued at USD 0.42 billion in 2025, stands at USD 0.56 billion in 2026, and is forecast to reach USD 1.77 billion by 2031 at a 25.88% CAGR.

Why is HBM so important in co-packaged memory deployments?

HBM is central because it supports the bandwidth and proximity requirements of large AI accelerators. It held 84.11% of revenue by memory type in 2025, which shows how dominant it remains in current high-performance systems.

Which application is driving the most revenue today?

AI accelerators lead current demand, accounting for 73.57% of application revenue in 2025. Their dominance comes from the need to place high-bandwidth memory close to compute dies in training and advanced inference hardware.

Which area is growing fastest within applications?

Cloud and enterprise server deployments are the fastest-growing application group, with a projected 26.11% CAGR through 2031. This reflects the wider rollout of custom inference silicon and broader use of package-level memory in cloud infrastructure.

Why does Asia-Pacific dominate this space?

Asia-Pacific held 56.58% of revenue in 2025 and is projected to post the fastest regional CAGR at 26.27%. The region leads because it combines memory production, foundry capacity, and advanced packaging capability in the same supply chain cluster.

What is the biggest supply-side risk for co-packaged memory?

Yield loss and packaging capacity remain the main constraints. High TSV counts in multi-die HBM stacks lower usable output, while limited 2.5D and 3D packaging lines slow how quickly announced investment can turn into commercial supply.

Page last updated on: