Cloud EDA Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

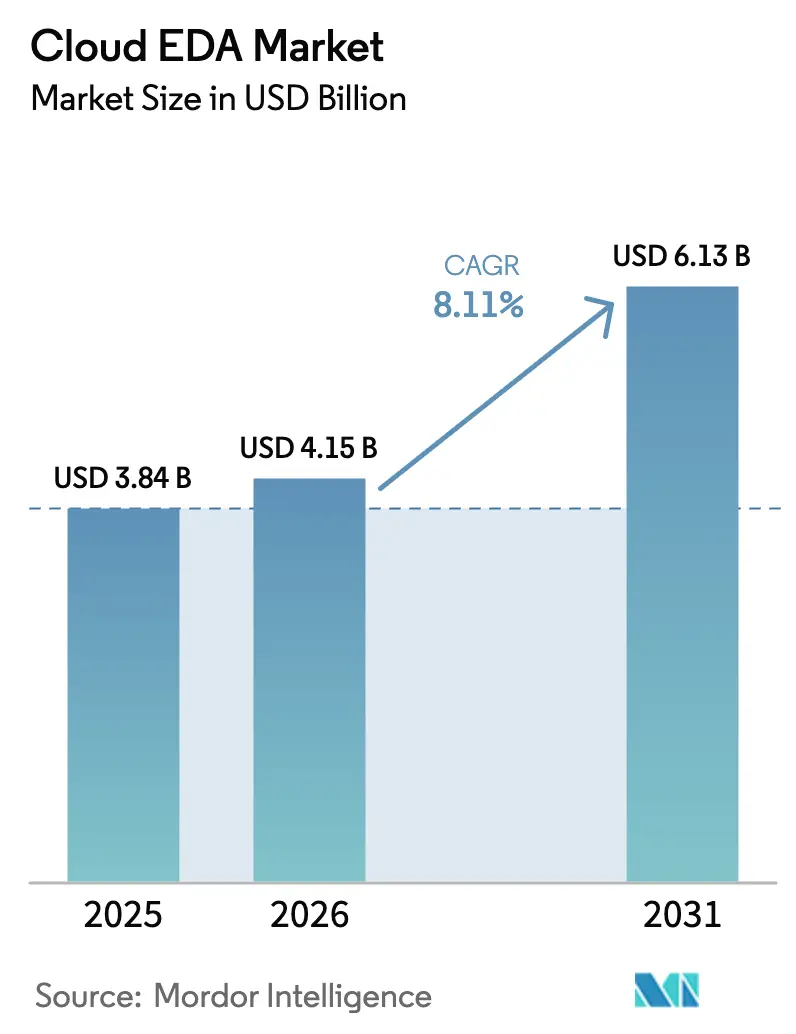

| Market Size (2026) | USD 4.15 Billion |

| Market Size (2031) | USD 6.13 Billion |

| Growth Rate (2026 - 2031) | 8.11% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cloud EDA Market Analysis by Mordor Intelligence

The cloud EDA market size in 2026 is estimated at USD 4.15 billion, growing from 2025 value of USD 3.84 billion with 2031 projections showing USD 6.13 billion, growing at 8.11% CAGR over 2026-2031. This expansion reflects an industry-wide shift toward elastic compute, which enables design teams to simulate 2-nanometer and smaller nodes without requiring additional on-premise capacity. Verification-heavy CAE use cases, early access to foundry design kits, and AI-driven design-space exploration together accelerate adoption. Incumbent vendors are embedding AI into cloud workflows to shrink simulation time, while hyperscalers subsidize new design starts to capture high-margin workloads. Regulatory incentives in the United States, the European Union, and China are funding sovereign cloud instances that preserve data residency and unlock demand from customers concerned about export controls.[1]U.S. Department of Commerce, “CHIPS and Science Act Implementation,” commerce.gov Competitive intensity is rising as Chinese and Indian start-ups enter the market with cloud-native toolchains that bypass legacy code and undercut pricing.

Key Report Takeaways

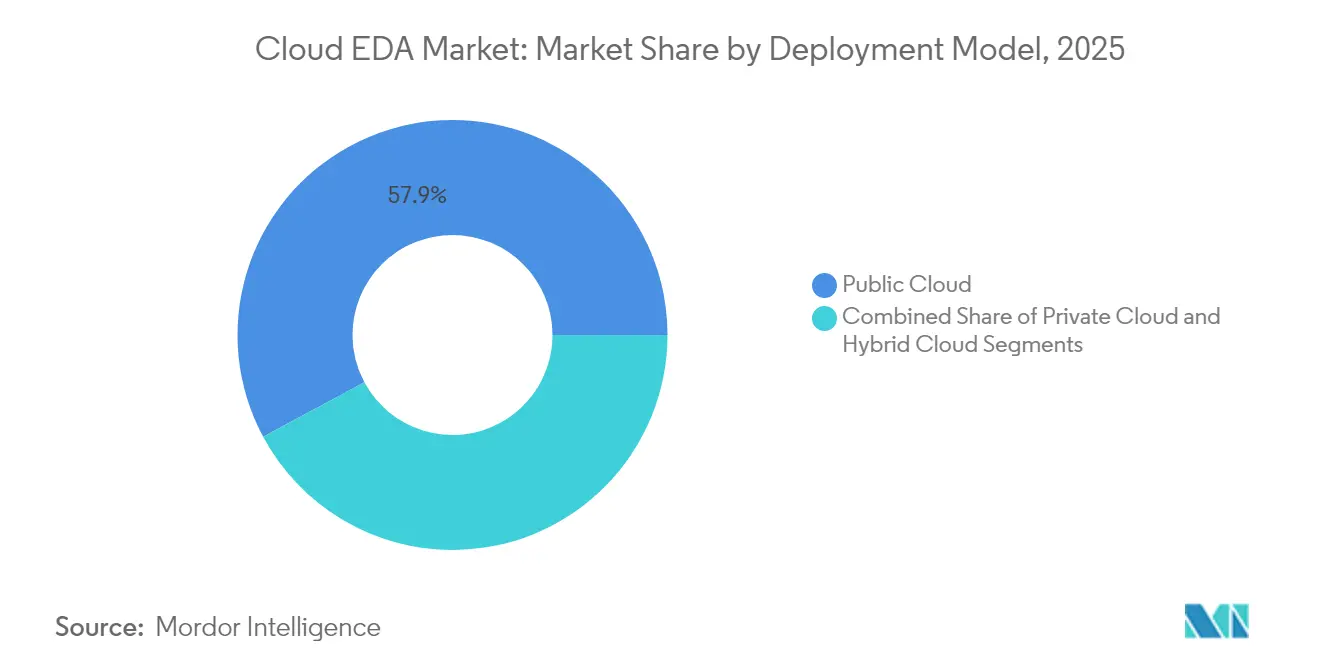

- By deployment model, public cloud commanded 57.85% revenue share of the cloud EDA market in 2025; the Hybrid cloud is forecast to grow at a 10.12% CAGR through 2031.

- By tool type, CAE verification accounted for 33.55% of the cloud EDA market size in 2025; PCB and MCM design tools are projected to expand at a 11.29% CAGR between 2026 and 2031.

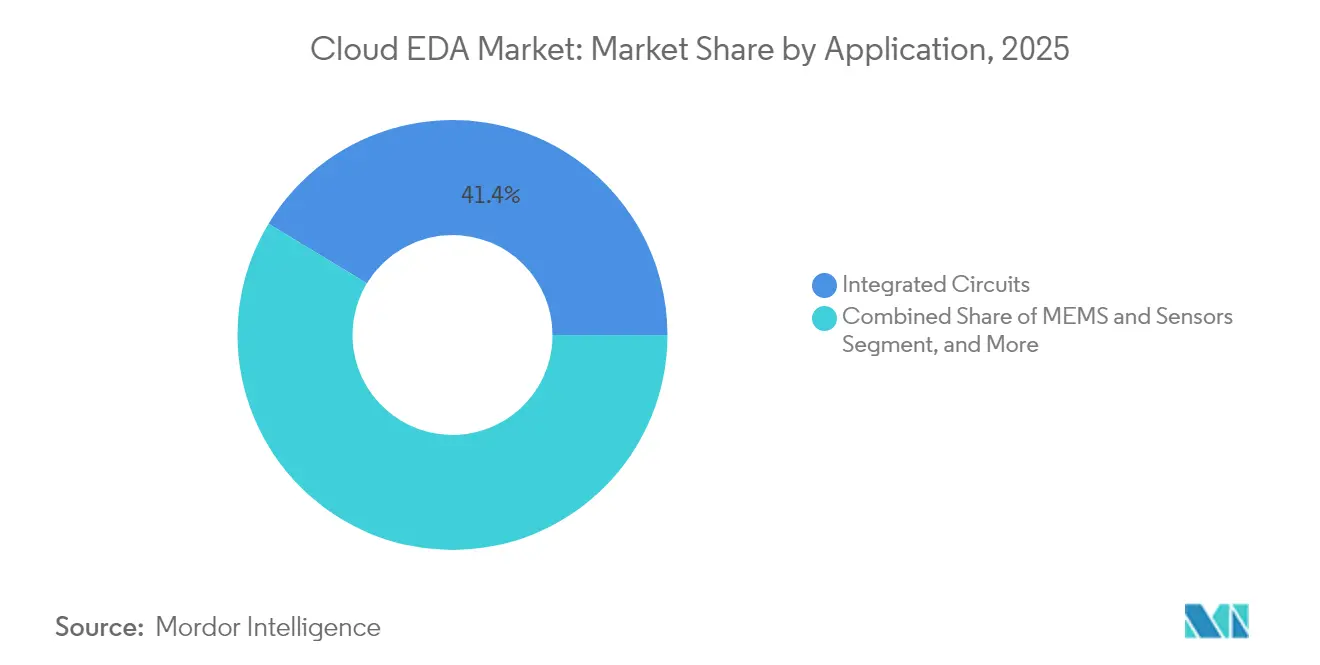

- By application, integrated circuits captured 41.35% of the cloud EDA market share in 2025; MEMS and sensors are set to record a 11.95% CAGR through 2031.

- By end user, fabless semiconductor companies accounted for 43.10% of the cloud EDA market revenue in 2025; foundries are expected to advance at a 11.52% CAGR through 2031.

- By industry vertical, consumer electronics led with a 30.25% demand share of the cloud EDA market in 2025; automotive applications are poised to grow at a 12.76% CAGR over the forecast period.

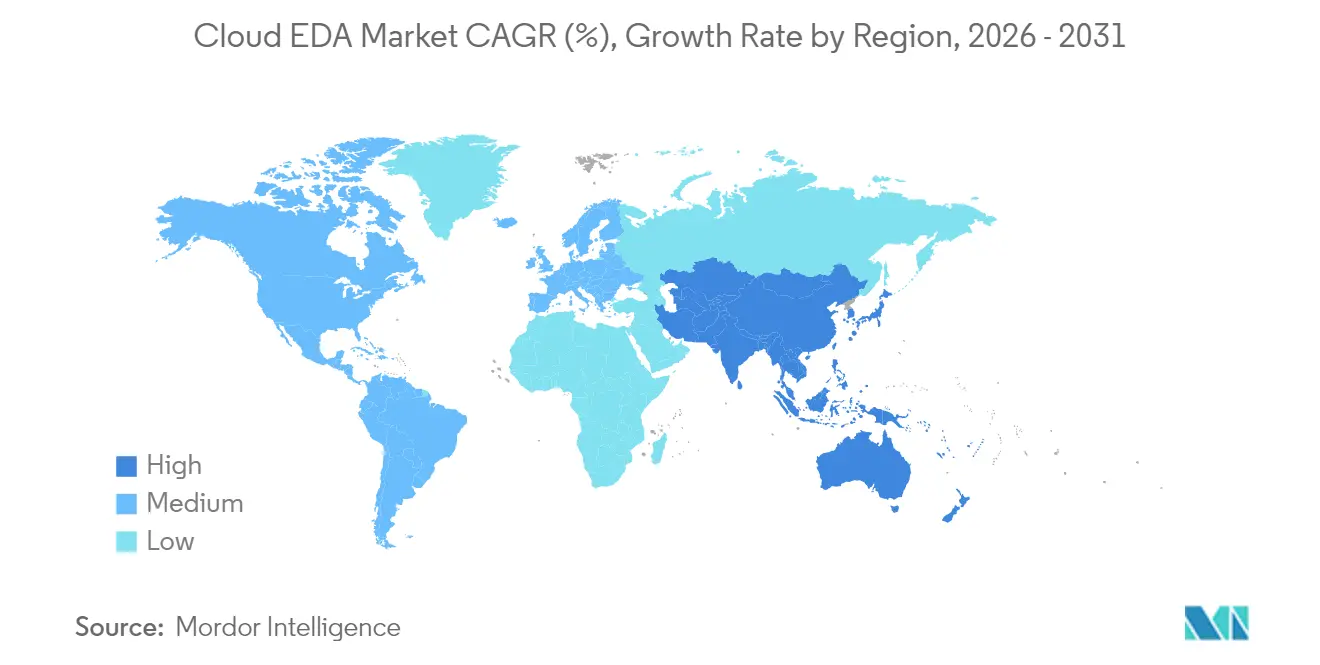

- By geography, the Asia Pacific generated 42.05% of the cloud EDA market's revenue in 2025; it also posts the highest projected regional growth, with a 11.62% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cloud EDA Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating design-node complexity driving compute demand | +1.8% | Global, with concentration in North America and Asia Pacific | Medium term (2-4 years) |

| Pay-as-you-go cloud cost optimization | +1.5% | Global, particularly emerging fabless companies in Asia Pacific | Short term (≤ 2 years) |

| Shrinking time-to-market for AI and HPC chips | +1.6% | North America and Asia Pacific | Short term (≤ 2 years) |

| Rapid adoption of 2 nm and below process technologies | +1.4% | Asia Pacific (Taiwan, South Korea), North America | Medium term (2-4 years) |

| Foundry-backed design-rule-sign-off-as-a-service programs | +1.2% | Asia Pacific, with spillover to North America and Europe | Medium term (2-4 years) |

| Sustainability mandates favoring hyperscale datacenters | +0.7% | Europe, North America, with growing influence in Asia Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Escalating Design-Node Complexity Driving Compute Demand

The verification runtime for TSMC N3E has tripled relative to 5 nm, making on-premise clusters uneconomical for mid-tier firms.[2]TSMC, “Open Innovation Platform,” tsmc.com Samsung’s gate-all-around 2 nm roadmap intensifies this pressure, as nanosheet parasitics require Monte Carlo studies across thousands of process corners. Intel’s 18A backside power delivery introduces new extraction steps that align naturally with distributed cloud simulation. Digital logic for AI accelerators now consumes more than 100,000 CPU hours per tape-out, a threshold at which pay-per-use elasticity outperforms fixed assets. Analog and mixed-signal workloads remain lighter, but the surge in high-performance compute chips keeps overall demand rising.

Pay-as-You-Go Cloud Cost Optimization

Synopsys FlexEDA converted perpetual seats into metered usage, trimming license oversubscription by 30% at several mid-sized customers.[3]Synopsys, “FlexEDA Pay-Per-Use Licensing,” synopsys.com Cadence Cerebrus showed 30% lower total cost of ownership for users running fewer than 50 parallel jobs. Spot instances can reduce simulation expenses by up to 60% for interruptible tasks, although always-on automotive flows may exceed on-premise costs after two years. Hybrid deployments that pin baseline workloads on-site while bursting peak demand to the cloud deliver the most balanced economics for many IDMs.

Shrinking Time-to-Market for AI and HPC Chips

ZeBu Cloud shaved 40% off hardware bring-up for a leading AI start-up, driving eight-month pre-silicon validation cycles. NeuReality taped out its NR1 inference processor entirely on AWS, proving cloud feasibility for first-silicon success. Cloud-based exploration enables architects to test ten times more variants in parallel than on-premise clusters, which is critical for edge-AI devices constrained by tight power envelopes.

Rapid Adoption of 2 nm and Below Process Technologies

TSMC’s N2 design kit became available in the cloud six months before on-premise release, giving early movers a decisive scheduling edge. Samsung’s SAFE program drew 15 new customers to 2 nm gate-all-around flows via cloud access. Intel Foundry Services partnered with Google Cloud to subsidize 18A designs, lowering up-front commitments for first-time advanced-node adopters.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| IP and data-sovereignty concerns | -1.1% | Global, with acute sensitivity in aerospace, defense, and government sectors | Medium term (2-4 years) |

| Legacy on-premise EDA investments | -0.9% | North America and Europe, where installed base is largest | Short term (≤ 2 years) |

| Bandwidth-driven latency and cost unpredictability | -0.7% | Regions with limited high-speed internet infrastructure; emerging markets | Short term (≤ 2 years) |

| Vendor lock-in risk under multi-year cloud contracts | -0.6% | Global, particularly affecting mid-tier fabless companies | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

IP and Data-Sovereignty Concerns

A 2024 SEMI poll found 42% of respondents citing IP security as the top barrier. Confidential VMs, such as AMD SEV-SNP, have a deployment rate below 10%. GDPR and China’s Data Security Law mandate regional hosting, forcing vendors to run costlier sovereign clouds. Synopsys launched an EU-only instance that carries a 25% price premium yet wins aerospace programs that cannot export design data across borders.

Legacy On-Premise EDA Investments

Mid-tier fabless firms often hold USD 50–100 million in depreciating tool assets. Revalidating scripts on cloud flows consumes, on average, nine months, disrupting tape-out calendars. Europe and North America have the largest installed base, heightening reluctance to migrate before depreciation is complete. Asia Pacific newcomers face lower inertia and adopt a cloud-first approach.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Model: Hybrid Architectures Bridge IP Sensitivity and Elastic Compute

The hybrid cloud is expected to post a 10.12% CAGR through 2031, as customers maintain physical design on-site while utilizing burst verification in the public cloud. Public deployments led the cloud EDA market in 2025, with a 57.85% revenue share, supported by AWS, Azure, and Google Cloud's semiconductor zones. Private cloud solutions appeal to IDMs and defense primes that require ITAR compliance, but they often lag in cost efficiency, which curbs their expansion. NXP completed a production SoC entirely in public cloud, signaling growing confidence in end-to-end remote flows.

Hybrid frameworks optimize both spend and governance. Siemens EDA’s synced repositories enable teams to migrate projects on demand, reducing idle license time by 15%. Foundry pilot programs, such as Intel Cloud Alliance, bundle hybrid options that run sign-off locally while housing PDK updates off-site. For AI accelerator designs where tape-out delays erode market opportunities, public cloud remains the first choice, whereas automotive safety ICs often opt for a hybrid approach to meet ISO 26262 documentation standards.

By Tool Type: PCB and MCM Design Accelerates on Collaboration Needs

CAE verification held a 33.55% share of the cloud EDA market size in 2025. Multicore scalability and embarrassingly parallel Monte Carlo tasks make CAE a pioneer in cloud computing. PCB and MCM tools are the fastest-growing, advancing at 11.29% CAGR as hyperscalers internalize board layouts for high-speed interconnect and as automakers co-design electronics with thermal engineers. Cadence’s OrCAD X OnCloud, at USD 99 per user per month, cuts license entry costs by 70%. Flux.ai’s AI-assisted routing engine, funded with USD 15 million Series A, automates placement choices and integrates real-time supply data.

IC physical design transitions more slowly because terabyte-scale databases trigger bandwidth fees, and IP sensitivity remains high. IP and library management moves to the cloud when enterprises seek a single golden repository, yet concerns about repository breaches temper adoption. Vendors address this by embedding zero-trust access controls and replicating data closer to end-users to reduce latency.

By Application: MEMS and Sensors Lead Multiphysics Simulation Uptake

Integrated circuits accounted for 41.35% of the cloud EDA market share in 2025, yet the proliferation of edge AI steers momentum toward MEMS and sensors, forecasted to grow at a 11.95% CAGR through 2031. Quanscient’s Allsolve runs coupled electromagnetic-thermal-mechanical solvers at line-rate on 10,000 cores, cutting MEMS microphone simulation times in half.

PCB workloads migrate for collaboration rather than compute intensity, while FPGA developers exploit cloud emulation to validate high-gate-count images before tape-out. Systems-on-chip integrate analog, digital, and RF domains, demanding cohesive toolchains that remain a roadmap priority for incumbent vendors.

By End User: Foundries Monetize Cloud to Capture Design Starts

Foundries are expected to lead growth at an 11.52% CAGR through 2031 as TSMC, Samsung, and Intel Foundry Services utilize cloud kits to attract smaller design houses. The model bundles IP libraries, certified flows, and sometimes compute credits, reducing upfront commitments for advanced-node aspirants.

Fabless firms still account for 43.10% of demand but exhibit moderating growth following their initial migrations. IDMs selectively burst to the cloud for exploration while retaining volume tape-out on-premise. ODMs and OEMs in the automotive and industrial sectors are beginning to internalize chip design, spurring service partnerships with EDA vendors that embed functional safety analysis.

By Industry Vertical: Automotive Outpaces Consumer Electronics

Consumer electronics accounted for 30.25% of revenue in 2025, but slowing smartphone cycles are easing growth. The automotive industry will accelerate at a 12.76% CAGR as electrification, over-the-air updates, and domain controllers prompt OEMs to co-design hardware-software stacks. Tesla’s Dojo chip and GM’s Ultium battery controller rely on cloud-driven iteration to meet aggressive release windows.

Industrial automation, driven by Industry 4.0 retrofits, utilizes cloud EDA to create application-specific standard products in low-volume, high-mix scenarios, where pay-per-use delivers economic flexibility. Aerospace and defense remain cautious due to export controls, insisting on sovereign or hybrid deployments that meet ITAR restrictions.

Geography Analysis

The Asia Pacific led the cloud EDA market with 42.05% revenue share in 2025 and is expected to grow at a 11.62% CAGR through 2031. China’s USD 47 billion subsidy push and Taiwan’s TSMC-anchored ecosystem shorten sign-off cycles from months to weeks. South Korea’s Samsung and SK Hynix invest in cloud enablement to expand their foundry share, while Japan’s analog specialists utilize the cloud to iterate power management ICs for electric vehicles.

North America held approximately 35.20% of the market share in 2025, supported by Silicon Valley’s concentration of fabless firms and hyperscaler investments. The CHIPS and Science Act earmarks funding for cloud-based design infrastructure that lets start-ups access advanced tool flows without capex. AWS, Azure, and Google Cloud created semiconductor landing zones with low-latency storage tiers, driving 40% year-over-year growth in customer numbers at AWS in 2024. Europe claimed an 17.85% share, constrained by GDPR data residency rules that increase costs by 25-30% compared to standard regions. Germany’s automotive suppliers adopt hybrid models that keep safety-critical blocks on-premise. The European Chips Act’s EUR 43 billion plan includes cloud design funds to double the region’s semiconductor share. The United Kingdom offers 50% cloud EDA grants post-Brexit to attract start-ups. The Middle East and Africa remain nascent but are gaining traction as the UAE and Saudi Arabia invest in sovereign clouds that align with their economic diversification plans.

Competitive Landscape

Cadence, Synopsys, and Siemens EDA retained a 60% combined share in 2024, shaping a moderately consolidated arena. Incumbents pursue land-and-expand plays: Cadence offers discounted seats to start-ups, then upsells AI-driven optimizers once workloads scale. Synopsys FlexEDA meets burst demand with meter-based licenses, while Siemens’ 2024 purchase of Fractal Technologies strengthens analog coverage.[4]Siemens EDA, “Acquisition of Fractal Technologies,” sw.siemens.com

Emerging challengers exploit cloud-native architectures to bypass legacy dependencies. Flux.ai focuses on AI-assisted PCB routing, and Quanscient delivers large-scale multiphysics solvers. Hyperscaler alliances shift dynamics: AWS bundles pre-configured EDA stacks, reducing setup time from weeks to hours; Google Cloud partners with Intel Foundry Services to offer early PDK access that rivals cannot match. Confidential computing now differentiates offerings for defense customers; vendors providing hardware-based encryption see early wins.

Patent filings in cloud EDA increased by 25% in 2024, with a focus on distributed simulation and AI-driven exploration, indicating sharper innovation cycles. Price competition intensifies in China and India, where local vendors target price-sensitive markets with toolchains tailored for trailing-edge nodes, threatening incumbents’ installed bases.

Cloud EDA Industry Leaders

Cadence Design Systems, Inc.

Synopsys, Inc.

Siemens Industry Software Inc. (Siemens EDA)

Ansys, Inc.

Altium Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Synopsys expanded its AI-driven verification platform with the launch of Synopsys.ai Copilot, integrating generative AI capabilities directly into its cloud-based verification flows to automate testbench generation and reduce verification time by up to 40%. The platform leverages large language models trained on decades of design data to suggest optimal verification strategies, addressing a critical bottleneck as chip complexity at 2-nanometer nodes demands exponentially more verification cycles. Early adopters reported that the AI-assisted approach reduced manual scripting effort by 50% while improving functional coverage by 15% to 20% compared with traditional methodologies.

- September 2025: Cadence Design Systems announced a strategic partnership with Microsoft Azure to offer its Cerebrus Intelligent System Design platform as a native Azure service, enabling customers to access advanced physical design and verification tools without migrating data between cloud providers. The integration includes Azure’s confidential computing capabilities, addressing IP security concerns that had previously deterred aerospace and defense customers from adopting the cloud. Cadence disclosed that 8 new customers signed multi-year cloud contracts within the first month of the Azure offering, representing USD 35 million in committed annual recurring revenue.

- August 2025: Intel Foundry Services expanded its Cloud Alliance to include support for its 18A-PT (Performance Tuned) process variant, offering cloud-based design enablement for high-performance computing and AI accelerator applications. The expansion provides fabless customers with early access to advanced packaging options, including Foveros 3D stacking and EMIB die-to-die interconnects, through AWS and Google Cloud platforms. Intel reported that 12 customers initiated 18A-PT design starts in the third quarter of 2025, with 6 targeting production tapeouts in 2026.

- July 2025: Siemens EDA acquired Blue Cheetah Analog Design for USD 180 million, expanding its cloud-based analog and mixed-signal design portfolio to address the growing demand for power management ICs in electric vehicles and edge AI devices. Blue Cheetah’s machine learning-driven layout optimization technology, which reduces analog design cycles by 30% to 40%, will be integrated into Siemens’ Analog FastSPICE platform and offered via cloud subscription. The acquisition positions Siemens to compete more aggressively in the automotive semiconductor market, where analog content is increasing due to the rise of electrification and advanced driver assistance systems.

- June 2025: TSMC launched its N2P (2 nanometer Plus) process design kit on AWS and Microsoft Azure, providing cloud-based access to enhanced performance and power-efficiency variants six months ahead of on-premise availability. The N2P node offers 10% to 15% performance improvement over the standard N2 process, targeting AI inference accelerators and smartphone application processors where power efficiency is critical. TSMC attracted 18 new cloud customers in the second quarter of 2025, including 5 fabless startups that are designing their first advanced-node chips using cloud EDA tools exclusively.

- May 2025: Ansys completed its acquisition of Helic for USD 95 million, adding electromagnetic interference and signal integrity analysis capabilities to its cloud-based simulation portfolio. Helic’s technology addresses critical challenges in high-speed digital design for 5G infrastructure and automotive radar systems, where electromagnetic coupling effects can degrade performance if not properly modeled during early design stages. Ansys plans to integrate Helic’s solvers into its Cloud Direct platform, enabling customers to run coupled electromagnetic-thermal simulations that were previously impractical on on-premise infrastructure due to memory and compute constraints.

- April 2025: Samsung Foundry expanded its SAFE (Samsung Advanced Foundry Ecosystem) program to include 1.4-nanometer gate-all-around process design rules, offering cloud-based design enablement for next-generation AI and high-performance computing applications. The expansion includes partnerships with AWS, Microsoft Azure, and Google Cloud to provide regional data residency options that comply with data sovereignty requirements in the European Union and China. Samsung attracted 22 new customers to its cloud EDA program in the first half of 2025, with 8 committing to 1.4-nanometer production tapeouts scheduled for 2027.

Global Cloud EDA Market Report Scope

| Public Cloud |

| Private Cloud |

| Hybrid Cloud |

| CAE (Simulation and Verification) |

| IC Physical Design and Verification |

| PCB and MCM Design |

| IP and Library Management |

| Other Tool Types |

| Integrated Circuits |

| Field-Programmable Gate Arrays |

| Printed Circuit Boards |

| MEMS and Sensors |

| Systems-on-Chip |

| Fabless Semiconductor Companies |

| Integrated Device Manufacturers |

| Foundries |

| Original Design Manufacturers and OEMs |

| IP Vendors |

| Consumer Electronics |

| Automotive |

| Industrial |

| Aerospace and Defense |

| Telecommunications |

| Healthcare |

| Other Industry Verticals |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Deployment Model | Public Cloud | ||

| Private Cloud | |||

| Hybrid Cloud | |||

| By Tool Type | CAE (Simulation and Verification) | ||

| IC Physical Design and Verification | |||

| PCB and MCM Design | |||

| IP and Library Management | |||

| Other Tool Types | |||

| By Application | Integrated Circuits | ||

| Field-Programmable Gate Arrays | |||

| Printed Circuit Boards | |||

| MEMS and Sensors | |||

| Systems-on-Chip | |||

| By End User | Fabless Semiconductor Companies | ||

| Integrated Device Manufacturers | |||

| Foundries | |||

| Original Design Manufacturers and OEMs | |||

| IP Vendors | |||

| By Industry Vertical | Consumer Electronics | ||

| Automotive | |||

| Industrial | |||

| Aerospace and Defense | |||

| Telecommunications | |||

| Healthcare | |||

| Other Industry Verticals | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Europe | Germany | ||

| France | |||

| United Kingdom | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the cloud EDA market?

The cloud EDA market size is USD 4.15 billion in 2026.

How fast is the market expected to grow?

It is projected to register an 8.11% CAGR over 2026-2031.

Which deployment model is expanding quickest?

Hybrid cloud is forecast to rise at 10.12% CAGR as firms balance IP security with elastic compute.

Why is automotive demand accelerating?

Automakers need rapid co-design of hardware and software for ADAS and EV platforms, pushing automotive growth to a 12.76% CAGR.

What share do the top three vendors hold?

Cadence, Synopsys, and Siemens EDA together capture roughly 60% of revenue.

Which region leads adoption?

Asia Pacific held 42.05% market share in 2025 and is pacing the fastest expansion through 2031.

Page last updated on: