Cloud Backbone Fiber Infrastructure Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 27.19 Billion |

| Market Size (2031) | USD 65.40 Billion |

| Growth Rate (2026 - 2031) | 19.19% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

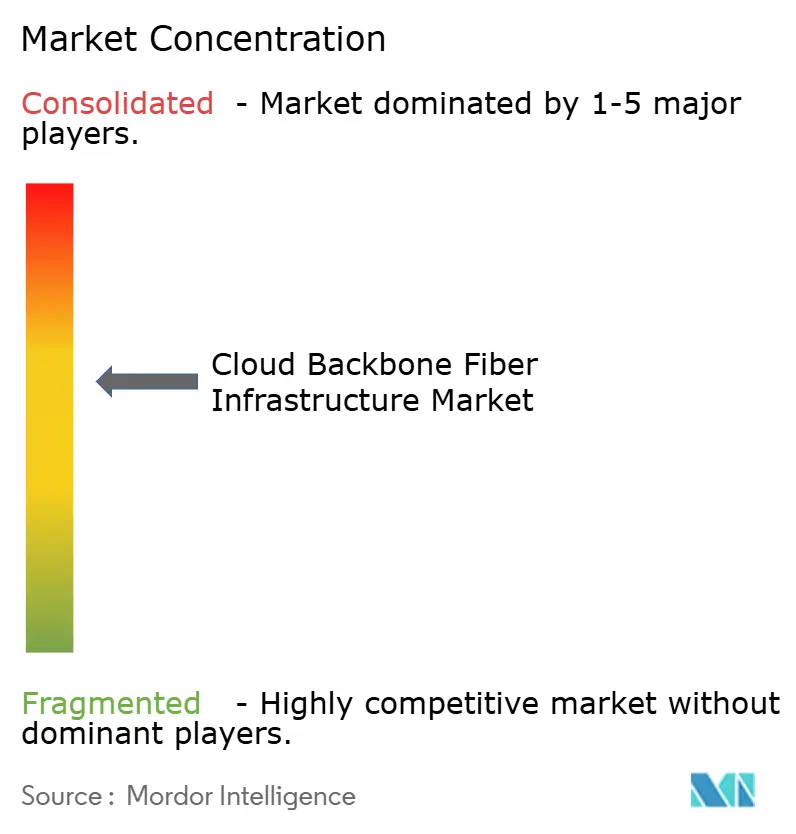

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cloud Backbone Fiber Infrastructure Market Analysis by Mordor Intelligence

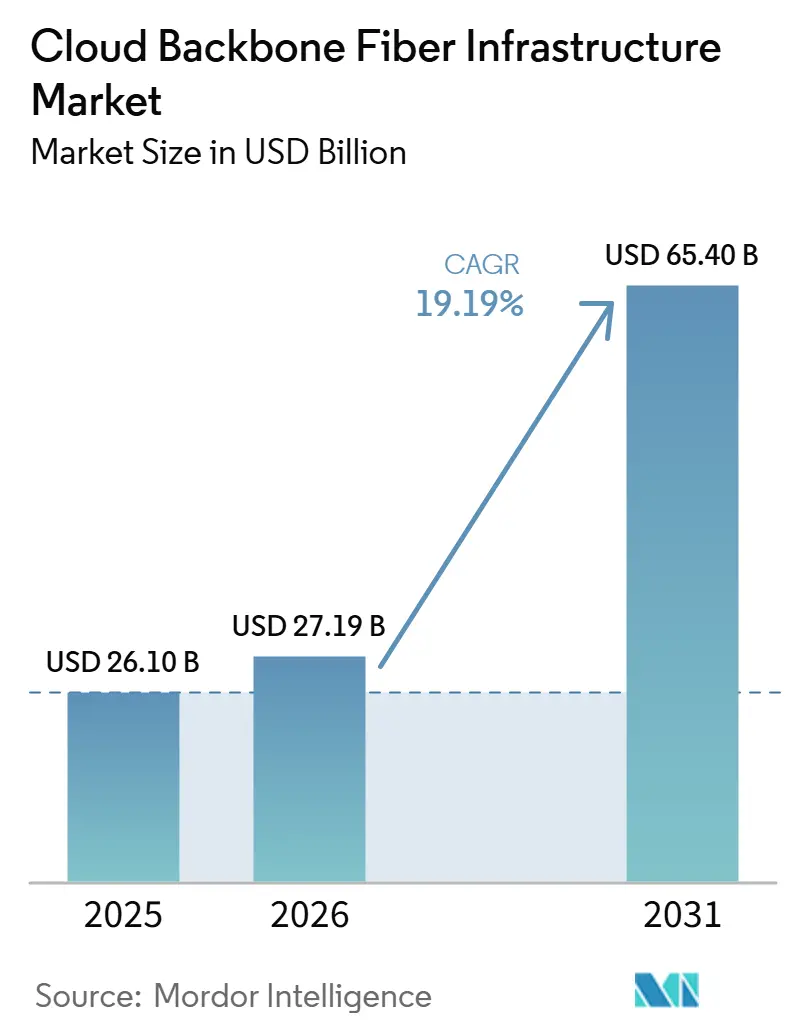

The Cloud Backbone Fiber Infrastructure Market size is expected to grow from USD 26.10 billion in 2025 to USD 27.19 billion in 2026 and is forecast to reach USD 65.40 billion by 2031 at 19.19% CAGR over 2026-2031. Demand is being shaped by a sharp increase in cloud traffic, AI-related workloads, and wider use of multi-cloud architectures, all of which are pushing operators and hyperscalers to secure more long-haul and interconnection fiber capacity. The cloud backbone fiber infrastructure market is also being influenced by the shift toward 400G and 800G network upgrades, which are driving spending toward higher-capacity optical systems, coherent modules, and denser route designs. Buyer concentration remains high because hyperscale operators are placing large, multi-year orders, shifting supplier relationships from short-cycle procurement to long-duration supply agreements. At the same time, the cloud backbone fiber infrastructure market faces pressure from long ribbon fiber lead times, limited skilled labor, and uneven access to route permits, making deployment timelines less predictable for smaller operators. Competitive positions are therefore being shaped not only by product capability, but also by access to photonic manufacturing, cable supply, route assets, and the ability to support complex builds across major AI corridors.

Key Report Takeaways

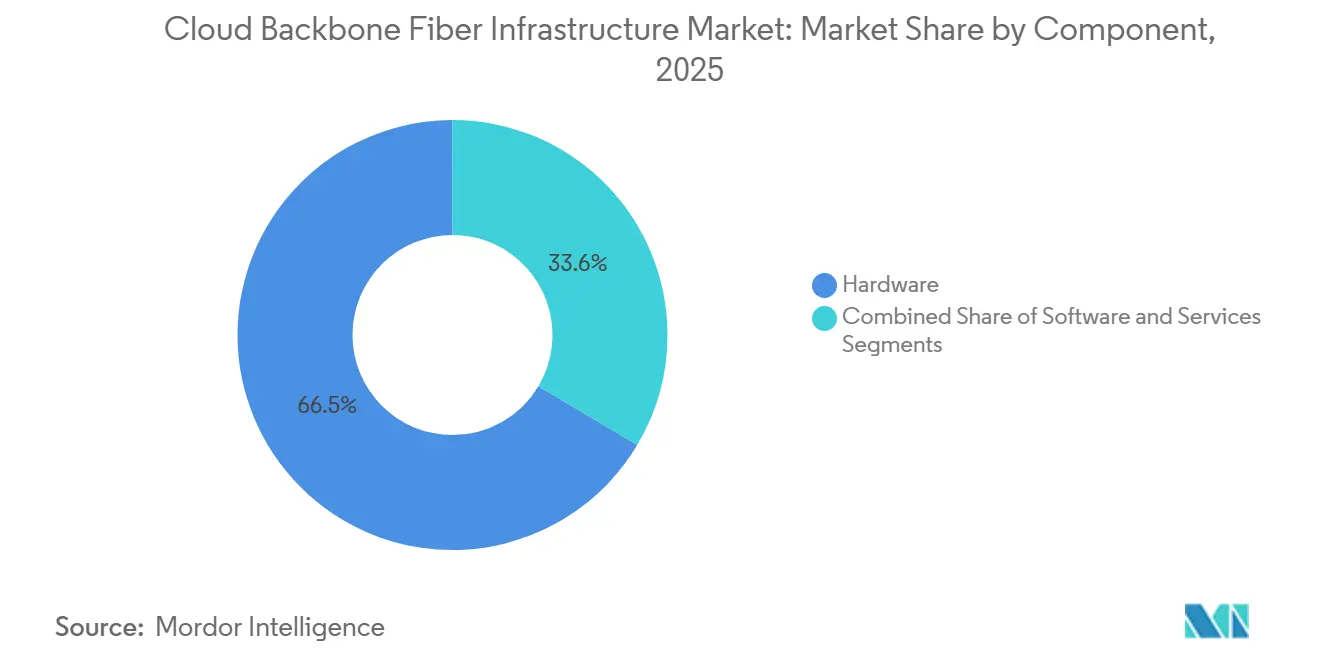

- By component, hardware accounted for 66.45% of revenue share in the cloud backbone fiber infrastructure market in 2025, while software is projected to expand at a 21.30% CAGR through 2031.

- By technology, dense wavelength division multiplexing accounted for 47.98% of revenue share in the cloud backbone fiber infrastructure market in 2025, while Ethernet is projected to expand at a 20.90% CAGR through 2031.

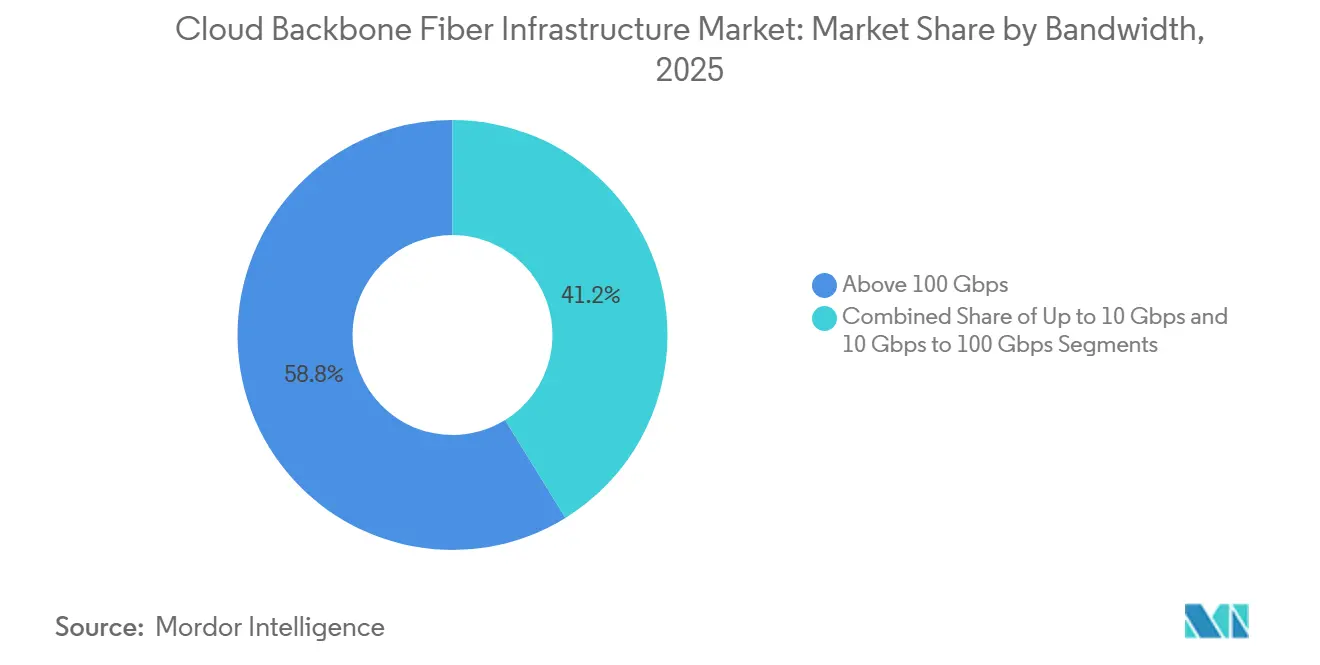

- By bandwidth, above 100 Gbps accounted for 58.81% of revenue share in the cloud backbone fiber infrastructure market in 2025 and is projected to expand at a 22.26% CAGR through 2031.

- By end user industry, communications service providers held 31.16% of revenue share in the cloud backbone fiber infrastructure market in 2025, while hyperscale cloud providers are projected to expand at a 23.28% CAGR through 2031.

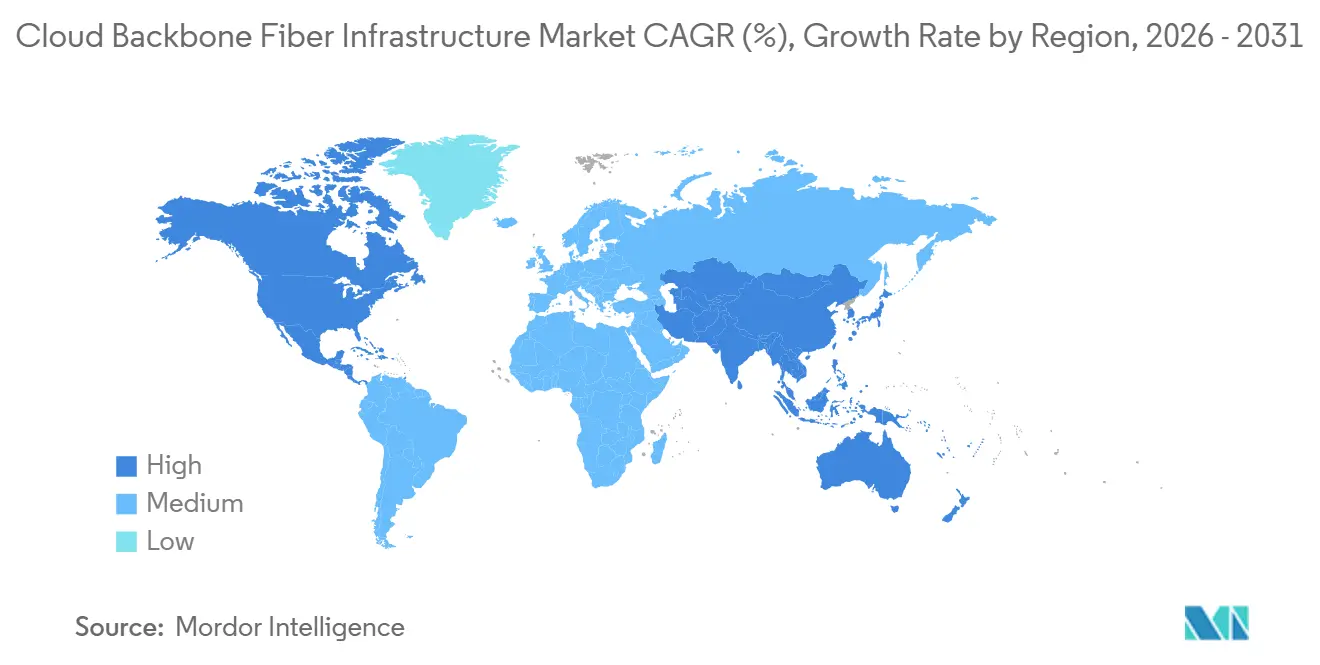

- By geography, North America held 38.49% of revenue share in the cloud backbone fiber infrastructure market in 2025, while Asia-Pacific is projected to expand at a 21.34% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Cloud Backbone Fiber Infrastructure Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AI and Multi-Cloud Traffic Surge Driving Dense Interconnections | +5.8% | Global, concentrated in North America and Asia-Pacific | Short term (≤ 2 years) |

| Hyperscale Data Center Buildouts Expanding Long-Haul Demand | +4.5% | North America and Asia-Pacific core, spill-over to Europe and Middle East and Africa | Short term (≤ 2 years) |

| Shift to 400G and 800G Optical Transport Accelerating Investment | +4.0% | Global | Medium term (2-4 years) |

| Edge Computing and Low-Latency Workloads Increasing Fiber Density | +2.8% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Energy-Efficient Optical Routing and Reduced Active Equipment | +2.0% | Global | Long term (≥ 4 years) |

| Fiber Route Diversity and Supply Continuity Requirements | +1.6% | North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

AI and Multi-Cloud Traffic Surge Driving Dense Interconnections

AI-driven traffic is changing how capacity is planned across the cloud backbone fiber infrastructure market. Fiber procurement is moving away from short planning cycles and toward early volume commitments tied to hyperscale build programs. A 2025 survey of 82 global communications service providers showed that 49% expected AI to exceed 30% of metro network traffic within 3 years, while 29% expected AI to account for more than half of long-haul traffic. That traffic mix matters because AI-related traffic between data centers is more persistent and more symmetric than many older cloud workloads, so fiber use stays elevated for longer periods. This is making interconnection corridors more valuable inside the cloud backbone fiber infrastructure market and is encouraging carriers, equipment vendors, and route owners to focus on paths linked to major AI clusters. It is also helping larger buyers secure better supply terms, because their forecast visibility is stronger and their route priorities are clearer.[1]Ciena Corporation, “Heavy Reading Coherent Pluggable Optics Service Provider Survey 2025,” Ciena Corporation, ciena.com

Hyperscale Data Center Buildouts Expanding Long-Haul Demand

Hyperscalers are taking on a more direct role in the fiber-buying market for cloud backbone infrastructure. Instead of relying mainly on carrier intermediaries, they are increasingly contracting for dark fiber, cable supply, and route builds through direct or anchored agreements. Corning and Meta broke ground in March 2026 on the expansion of Corning’s Hickory, North Carolina, optical cable manufacturing facility, under a multiyear agreement valued at up to USD 6 billion through 2030.[2]Corning Incorporated, “Corning and Meta Celebrate Start of Construction on Cable Manufacturing Expansion in North Carolina to Support AI Buildout,” Corning Incorporated, corning.com The facility is expected to become the world’s largest fiber-optic cable manufacturing plant, underscoring how supply-side investment is now following hyperscaler demand with greater precision. Fiber Broadband Association research also showed that annual fiber mile additions are expected to rise sharply by 2029, reflecting the large route requirements that follow each new hyperscale campus. As a result, the cloud backbone fiber infrastructure market is seeing long-haul demand rise faster than traditional telecom build cycles were designed to handle.

Shift to 400G and 800G Optical Transport Accelerating Investment

The move from 100G to 400G and 800G systems is reshaping investment priorities in the cloud backbone fiber infrastructure market. Cloud operators want more spectral efficiency and lower cost per bit on routes that now carry large AI training and inference flows between distributed compute sites. This shift is also supporting the wider adoption of IP-over-DWDM designs, in which coherent optics are integrated directly into routers and switches rather than handled by separate optical transport platforms. Microsoft’s Fairwater AI campus in Wisconsin, activated in June 2026, connected buildings with 800G Ethernet over commodity switches and a Microsoft-developed transport protocol.[3]Microsoft, “From Wisconsin to Atlanta, Microsoft Connects Datacenters to Build Its First AI Superfactory,” Microsoft, microsoft.com That deployment showed that open, pluggable approaches can support production-scale AI connectivity without depending on fully proprietary transport designs. The result is a faster product cycle in the cloud backbone fiber infrastructure market and a more direct link between router evolution, coherent module adoption, and optical spending.

Edge Computing And Low-Latency Workloads Increasing Fiber Density

Low-latency workloads are extending fiber demand beyond core data center corridors in the cloud backbone fiber infrastructure market. AI inference, financial processing, and latency-sensitive applications are increasing the need for dense local and regional fiber paths close to end users. Spectrum deployed NVIDIA AI Grid infrastructure at network edge sites in June 2026, using 100Gbps low-latency fiber from more than 1,000 edge data centers and hubs. That deployment showed that edge AI economics depend on both route proximity and available fiber density, not only on compute hardware. It also means that operators with strong conduit positions in suburban and secondary corridors may gain leverage as hyperscalers seek inference capacity beyond major metro cores. In practical terms, the cloud backbone fiber infrastructure market is increasingly reliant on networks that connect edge nodes to backbone campuses with low latency and stable throughput.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High CAPEX for Backbone Buildouts and Route Rights | -2.3% | Global, most pronounced in North America and Europe | Long term (≥ 4 years) |

| Permitting Delays and Access Constraints Slowing Long-Haul Deployment | -1.8% | North America and Europe | Medium term (2-4 years) |

| Skilled Optical Network Integration Gaps Raising Deployment Costs | -1.4% | Global | Medium term (2-4 years) |

| Power, Cooling, and Fiber Availability Bottlenecks Limiting Scale | -1.1% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High CAPEX For Backbone Buildouts And Route Rights

Backbone fiber projects remain capital-intensive across the cloud backbone fiber infrastructure market. Operators must fund rights-of-way, conduit construction, amplifier stations, and cable procurement long before revenue begins to flow on a new corridor. This is creating a two-speed funding environment, because large players with anchor tenants can raise capital with more confidence than smaller regional operators working without long-term commitments. Fiber Broadband Association materials noted that ribbon fiber lead times had exceeded 60 weeks, meaning capital is often committed well before construction milestones are secured. Route economics are also uneven because urban builds can be easier to justify than rural or secondary long-haul corridors, even when long-distance capacity is urgently needed. In the cloud backbone fiber infrastructure market, this cost structure favors scale, existing corridor access, and stronger balance sheets over pure demand visibility.

Permitting Delays and Access Constraints Slowing Long-Haul Deployment

Permitting remains a major drag on deployment speed in the cloud backbone fiber infrastructure market. Long-haul routes often cross several jurisdictions, and each authority can slow the process through separate approvals, environmental requirements, or access requirements. The Fiber Broadband Association identified permitting and access constraints as a key bottleneck during the heavy deployment period expected from late 2025 through 2027. The issue becomes more difficult when public broadband programs and hyperscaler-led projects compete for the same rights-of-way, conduit space, and construction windows. Cross-border projects in Europe face added pressure because route resilience and licensing requirements have become more important under recent security frameworks. As a result, the cloud backbone fiber infrastructure market can face delays even when capital and equipment are available, because administrative coordination still moves more slowly than demand.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Hardware Leads While Software Expands Fastest

Hardware accounted for 66.45% of the cloud backbone fiber infrastructure market in 2025, reflecting the large volume of fiber-optic cables, DWDM transponders, optical amplifiers, and coherent transceivers required for hyperscale buildouts. The cloud backbone fiber infrastructure market continued to lean heavily toward the physical layer because route expansion, campus interconnection, and high-capacity transport all require significant spending on cable and optical hardware before software layers can scale. Corning’s Hickory expansion clearly showed this pattern, as the company increased optical cable manufacturing capacity in response to strong hyperscale demand rather than incremental carrier refresh cycles. Hardware dominance also reflected the fact that many backbone projects were still in the construction or upgrade phase, during which cable, transport shelves, line systems, and amplification equipment accounted for most of the upfront budget. Even so, the cloud backbone fiber infrastructure industry is not staying fixed at the hardware layer, as procurement is increasingly tied to integrated deployment models that combine equipment, control software, and services under a single contract.

Software is projected to expand at a 21.30% CAGR through 2031, making it the fastest-growing component as operators adopt open and disaggregated network operating systems and AI-aware optical control tools. In 2026, demand was being shaped by software that could allocate spectral capacity more dynamically, route around congestion, and manage traffic patterns created by inference and training flows with better speed and visibility. This made software more central to the fiber backbone infrastructure market for the cloud, even though its revenue base remained smaller than hardware's. Services played a meaningful role as well, because route planning, optical design, deployment, and maintenance became more difficult in mixed-vendor environments and in regions facing labor shortages. The Fiber Broadband Association and Power and Communication Contractors Association projected a shortfall of 178,000 skilled fiber technicians in the United States through 2032, helping sustain demand for specialized service support during network buildouts. Meta’s LevelUp training model also showed that large buyers are increasingly supporting workforce development directly when contractor capacity becomes a risk to route delivery.

By Technology: DWDM Holds Scale While Ethernet Gains Ground

The Dense Wavelength Division Multiplexing (DWDM) held 47.98% of the cloud backbone fiber infrastructure market in 2025, supported by its long-established role in transporting multiple high-capacity wavelengths across intercity and international routes. The technology remained central because carriers and large network operators still relied on it for high-reach, high-capacity transport across backbone networks where scale and efficiency matter most. OTN also retained importance for regulated carrier and enterprise services that require layered management, protection switching, and strong operational visibility. Even with these strengths, the cloud backbone fiber infrastructure market is shifting part of its technology mix toward Ethernet as the economic logic of pluggable coherent optics improves rapidly. Colt Technology Services reinforced that trend in 2025 when it completed a successful 800G ZR+ coherent optics trial over the 667km Frankfurt-Munich route in its production AS8220 network, showing that long-haul IP-over-DWDM can work on live backbone infrastructure.

Ethernet is projected to expand at a 20.90% CAGR through 2031, supported by architectures where coherent modules are inserted directly into routers and switches rather than managed through separate transport layers. This is important because hyperscalers often favor simpler, more open designs that reduce platform dependence and align optical spending more closely with IP network evolution. The cloud backbone fiber infrastructure market, therefore, faces a structural technology shift, not only a refresh cycle, because design wins are moving toward solutions that are easier to scale in open environments. Nokia’s 2025 activation of KPN’s 800G-ready core and transport network also showed that established carriers are modernizing backbone transport with architectures designed for cloud connectivity and broad service integration. Legacy technologies such as SON continue to support narrow use cases, especially where older carrier systems remain in place, but they no longer define the growth path. The practical effect is that the cloud backbone fiber infrastructure industry is moving toward a model where transport value is increasingly tied to coherent pluggables, open interfaces, and the ability to scale high-capacity routes without heavy platform lock-in.

By Bandwidth: Above 100 Gbps Sets The New Backbone Standard

Above 100 Gbps commanded 58.81% of the cloud backbone fiber infrastructure market share in 2025 and was also the fastest-growing bandwidth tier, with a 22.26% CAGR through 2031. That dual position showed that 400G and 800G had already become the working standard for new backbone deployments rather than a premium layer used only in a few hyperscale corridors. The cloud backbone fiber infrastructure market is now aligning around higher-capacity routes because both carriers and cloud operators need more throughput per fiber pair and better economics per transmitted bit. The 10Gbps to 100Gbps segment still served enterprise WAN links, regional interconnects, and public-sector networks where traffic intensity and budget conditions were lower. Up to 10Gbps remained relevant mainly for residual legacy networks, but its role kept narrowing as application traffic and cloud adoption increased across business and public-sector environments.

Microsoft’s June 2026 Fairwater activation made the direction of travel clearer, because the campus used 800G Ethernet across buildings and treated that capacity as a production requirement rather than a test case. Nokia’s 2025 deployment for KPN pointed in the same direction, with an 800G-ready national backbone designed to connect multiple access types and cloud services at higher scale. This matters for the cloud backbone fiber infrastructure market because cost crossover points are moving, and high-capacity optics are becoming more attractive even on routes that were once served by lower-speed platforms. As manufacturing scale improves, operators may find that the economics of 400G and above become compelling sooner than expected outside first-tier corridors. That creates pressure on mid-bandwidth layers, because part of their traditional demand can migrate upward faster than product and planning cycles had assumed. The bandwidth mix in the cloud backbone fiber infrastructure market is therefore moving toward denser, faster, and more standardized transport across both hyperscale and carrier networks.

By End User Industry: Communication Service Providers (CSPs) Hold Scale While Hyperscalers Drive Growth

Communications service providers held 31.16% of the end-user base in 2025, giving them the largest current share among buying groups in the cloud backbone fiber infrastructure market. Their position reflected longstanding purchases of long-haul DWDM systems, metro transport infrastructure, and backbone capacity to support regulated services, enterprise traffic, and interconnect obligations. Yet the growth pattern was shifting as hyperscale cloud providers increasingly bypassed carrier resale models and secured dark fiber or direct optical capacity for their own interconnection needs. The cloud backbone fiber infrastructure market, therefore, showed a split between incumbents that still controlled large installed bases and hyperscalers that were changing the pace and structure of new spending. Internet content providers and carrier-neutral providers also remained important because they operate interconnection hubs that aggregate traffic from cloud, enterprise, and carrier networks in major metro markets.

Hyperscale cloud providers are projected to expand at a 23.28% CAGR through 2031, reflecting the non-linear data center interconnect demand driven by each new GPU cluster generation. This demand pattern is difficult for traditional resale structures to match, because hyperscalers often need scale, timing, and route control that wholesale wave services do not always provide. Enterprise and colocation data centers also continued to grow as companies added dedicated fiber links between facilities and cloud on-ramps to improve latency and meet sovereignty requirements. Other end-user groups, including government and research institutions, supported steady demand as national AI and digital infrastructure programs created new high-capacity network requirements. In the cloud backbone fiber infrastructure market, this end-user mix is shifting bargaining power toward the buyers with the largest and most predictable route plans. The longer-term implication is that carriers will need to defend their role through managed connectivity, last-mile reach, and software-driven service layers rather than depending only on traditional transport resale.

Geography Analysis

North America held 38.49% of the cloud backbone fiber infrastructure market share in 2025, making it the largest regional segment by current revenue. The region led because it had the deepest concentration of hyperscale campuses, the heaviest AI infrastructure spending, and some of the most active long-haul route programs. Corning’s multiyear agreement with Meta and the related Hickory expansion showed how North American demand was large enough to drive upstream manufacturing decisions directly. Fiber Broadband Association research also pointed to a steep rise in route-mile and fiber-mile requirements in the United States, which helps explain why supply pressure and buyer concentration have become so visible in the region. The cloud backbone fiber infrastructure market in North America also benefited from a strong base of fiber operators, optical suppliers, and data center developers that could respond quickly when AI corridor demand accelerated.

Asia-Pacific is projected to expand at a 21.34% CAGR through 2031, making it the fastest-growing regional segment in the cloud backbone fiber infrastructure market. Growth is being supported by expanding data center development in India, structured cable investment in Japan, and wider demand for sovereign and hyperscale-grade connectivity across regional corridors. Japan’s approval of financing for the Intra-Asia Marine cable system in January 2026 reflected a coordinated approach to digital infrastructure that combines public backing with private sector execution. Europe remained the third-largest region and continued to focus on 800G-ready transport, cloud-linked backbone modernization, and route resilience under evolving security frameworks. Nokia’s work with KPN and the EU cable security framework both showed that European investment was being shaped by both capacity growth and network diversity requirements.

South America was a smaller but advancing part of the cloud backbone fiber infrastructure market, supported by data center growth in Brazil and stronger cross-border connectivity plans. The region’s role was becoming increasingly important as operators sought additional AI traffic routes and broader links between domestic and international data infrastructure. Middle East and Africa remained the most nascent regional block, but demand was rising as Gulf operators sought route diversity and as African landing points continued to matter for international connectivity. In this part of the cloud backbone fiber infrastructure market, investment logic is being shaped by resilience as much as by raw traffic growth, especially where overland alternatives can complement submarine exposure. Taken together, regional patterns showed that capacity growth was no longer concentrated solely in legacy telecom corridors, as AI, sovereignty needs, and route security were expanding the set of geographies that now matter to backbone planning.

Competitive Landscape

The cloud backbone fiber infrastructure market is moderately consolidated at the optical systems layer and more fragmented across dark fiber operations and cable manufacturing. Market structure is shaped by a small group of large transport vendors at the high end, while route ownership and cable supply remain more dispersed by geography and by project type. Nokia’s acquisition of Infinera in February 2025 strengthened its position in optical networking and expanded its access to indium phosphide photonic capabilities, which are important for 800G and higher-capacity coherent systems. At the same time, the cloud backbone fiber infrastructure market continued to favor vendors that could combine transport systems, photonic components, and long-term support for hyperscale-style network designs. This is why strategic scale, product depth, and manufacturing access now carry as much weight as pure feature competition.

Corning’s agreement with Meta was one of the clearest strategic moves in the cloud backbone fiber infrastructure market because it linked a major buyer directly to long-duration manufacturing expansion. Microsoft’s Fairwater deployment was another important move because it showed how cloud providers are validating 800G Ethernet and open transport approaches in production AI environments. Nokia’s 800G-ready deployment for KPN also mattered because it showed that incumbent carriers are modernizing national backbones with architectures designed for cloud-scale service delivery rather than only legacy transport requirements. These moves indicate that competition is no longer limited to selling boxes, because suppliers now compete on manufacturing access, route readiness, software openness, and the ability to fit into buyer-specific transport models. In the cloud backbone fiber infrastructure market, it tends to reward vendors and operators that can support large programs without creating deployment friction for buyers.

There is still room for differentiation in software control, open-line systems, and edge-adjacent route strategies. Smaller vendors remain relevant where carrier-focused metro and access transport require specialization rather than broad hyperscale portfolios. Fiber cable makers also hold favorable positions because long lead times support pricing leverage, even though their own capacity expansion can take years to complete. Dark fiber and interconnection providers can build durable recurring revenue if they control routes near major campuses and can deliver pre-lit or quickly activatable capacity. The competitive picture in the cloud backbone fiber infrastructure market is therefore mixed, with concentration higher in optical transport systems and lower in route operations and fiber construction. This balance helps explain why the market supports both global equipment leaders and regional infrastructure players simultaneously, but it also shows why buyer scale is increasingly shaping who wins the largest contracts.

Cloud Backbone Fiber Infrastructure Industry Leaders

Cisco Systems, Inc.

Ciena Corporation

Nokia Corporation

Huawei Technologies Co., Ltd.

Fujitsu Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Corning Incorporated and Meta Platforms broke ground on the expansion of Corning's Hickory, North Carolina, optical cable manufacturing facility, marking the first construction milestone in their multiyear, up to USD 6 billion supply agreement. When complete, the Hickory facility will be the world's largest fiber-optic cable manufacturing plant, addressing AI infrastructure supply constraints that have extended ribbon fiber lead times beyond 60 weeks.

- January 2026: Japan's Ministry of Internal Affairs and Communications approved up to USD 73 million in Japan ICT Fund financing for the Intra-Asia Marine cable system on January 23, 2026, a 320Tbps link connecting Japan, Malaysia, and Singapore, led by a joint venture of NTT Data, Sumitomo Corporation, and JA Mitsui Leasing. The approval reflects Japan's structured national program to expand sovereign digital infrastructure across Indo-Pacific corridors.

- January 2026: Uniti Wholesale announced a 20-year contract, with a total contract value exceeding USD 500 million, to deploy 1,100 route miles of ultra-high-capacity dark fiber across the South-Central US, including segments from Tulsa to Little Rock and Little Rock to Memphis. Phase One deliveries commenced in January 2026, targeting AI data center connectivity in a region with growing power capacity and emerging hyperscale infrastructure.

Global Cloud Backbone Fiber Infrastructure Market Report Scope

The cloud backbone fiber infrastructure market revenue is generated through the sale of fiber optic infrastructure hardware, optical transport and network management software, and professional services including network design, deployment, system integration, data center interconnect (DCI), cloud connectivity implementation, testing, and maintenance, serving communication service providers, hyperscale cloud providers, internet content providers, carrier-neutral operators, enterprise and colocation data centers, and other large-scale network operators. The cloud backbone fiber infrastructure market is segmented by component (hardware, software, and services), technology (dense wavelength division multiplexing, optical transport network, ethernet, synchronous optical network, and other transmission technologies), bandwidth (up to 10 Gbps, 10-100 Gbps, and above 100 Gbps), end user industry (communications service providers, internet content providers and carrier-neutral providers, hyperscale cloud providers, enterprise and colocation data centers, and other end user industry (government and research, and education, etc.)), and geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The market forecasts are provided in value (USD).

| Hardware (Includes Fiber Optic Cables, Optical Transport Equipment (DWDM/CWDM Systems), Optical Transponders and Muxponders, Coherent Optical Modules (QSFP-DD, OSFP, CFP2-DCO, etc.), Optical Line Systems (OLS), ROADM (Reconfigurable Optical Add-Drop Multiplexer) Systems, Optical Amplifiers (EDFA/Raman)) |

| Software (Includes Network Operating Systems (NOS), Software-Defined Networking (SDN) Controllers, Network Orchestration Platforms, Network Management Systems (NMS), Element Management Systems (EMS), Cloud Network Controllers, Traffic Engineering Software) |

| Services(Includes Network Planning and Design, Fiber Route Engineering, Consulting, Deployment and Installation, System Integration, Data Center Interconnect (DCI) Implementation, Cloud Connectivity Integration, Testing and Commissioning) |

| Dense Wavelength Division Multiplexing |

| Optical Transport Network |

| Ethernet |

| Synchronous Optical Network |

| Other Transmission Technologies |

| Up to 10 Gbps |

| 10 Gbps to 100 Gbps |

| Above 100 Gbps |

| Communications Service Providers |

| Internet Content Providers and Carrier-Neutral Providers |

| Hyperscale Cloud Providers |

| Enterprise and Colocation Data Centers |

| Other End User Industry (Government and Research, and Education, etc.) |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| ASEAN | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of the Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Component | Hardware (Includes Fiber Optic Cables, Optical Transport Equipment (DWDM/CWDM Systems), Optical Transponders and Muxponders, Coherent Optical Modules (QSFP-DD, OSFP, CFP2-DCO, etc.), Optical Line Systems (OLS), ROADM (Reconfigurable Optical Add-Drop Multiplexer) Systems, Optical Amplifiers (EDFA/Raman)) | ||

| Software (Includes Network Operating Systems (NOS), Software-Defined Networking (SDN) Controllers, Network Orchestration Platforms, Network Management Systems (NMS), Element Management Systems (EMS), Cloud Network Controllers, Traffic Engineering Software) | |||

| Services(Includes Network Planning and Design, Fiber Route Engineering, Consulting, Deployment and Installation, System Integration, Data Center Interconnect (DCI) Implementation, Cloud Connectivity Integration, Testing and Commissioning) | |||

| By Technology | Dense Wavelength Division Multiplexing | ||

| Optical Transport Network | |||

| Ethernet | |||

| Synchronous Optical Network | |||

| Other Transmission Technologies | |||

| By Bandwidth | Up to 10 Gbps | ||

| 10 Gbps to 100 Gbps | |||

| Above 100 Gbps | |||

| By End User Industry | Communications Service Providers | ||

| Internet Content Providers and Carrier-Neutral Providers | |||

| Hyperscale Cloud Providers | |||

| Enterprise and Colocation Data Centers | |||

| Other End User Industry (Government and Research, and Education, etc.) | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| ASEAN | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of the Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the cloud backbone fiber infrastructure market in 2026 and where is it heading?

The cloud backbone fiber infrastructure market stood at USD 27.19 billion in 2026 and is forecast to reach USD 65.4 billion by 2031 at a 19.19% CAGR.

Which component category leads spending in cloud backbone fiber infrastructure?

Hardware led in 2025 with 66.45% share because large-scale route builds still require heavy spending on cables, transponders, amplifiers, and coherent optics.

What is driving the fastest growth in backbone fiber demand for cloud networks?

AI traffic growth, hyperscale data center buildouts, and the move to 400G and 800G transport are the main factors increasing long-haul and interconnection fiber demand.

Which technology is growing fastest in this space?

Ethernet is the fastest-growing technology segment and is projected to expand at a 20.90% CAGR through 2031 as IP-over-DWDM designs gain adoption.

Which bandwidth tier is becoming the backbone standard for new deployments?

Above 100Gbps held 58.81% share in 2025 and is projected to expand at a 22.26% CAGR, showing that 400G and 800G are becoming the standard for new routes.

Which region is expanding fastest in cloud backbone fiber infrastructure?

Asia-Pacific is the fastest-growing regional segment and is projected to expand at a 21.34% CAGR through 2031, supported by data center expansion and cable investment across key corridors.

Page last updated on: