Clostridium Difficile Diagnostics And Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

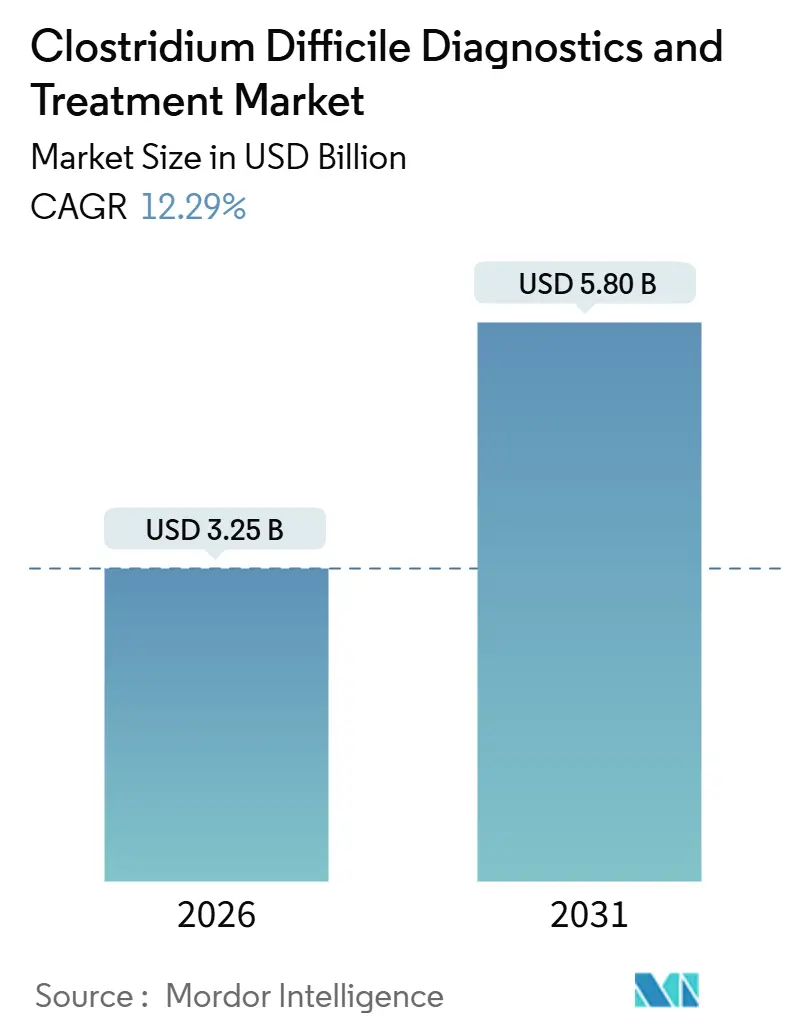

| Market Size (2026) | USD 3.25 Billion |

| Market Size (2031) | USD 5.80 Billion |

| Growth Rate (2026 - 2031) | 12.29% CAGR |

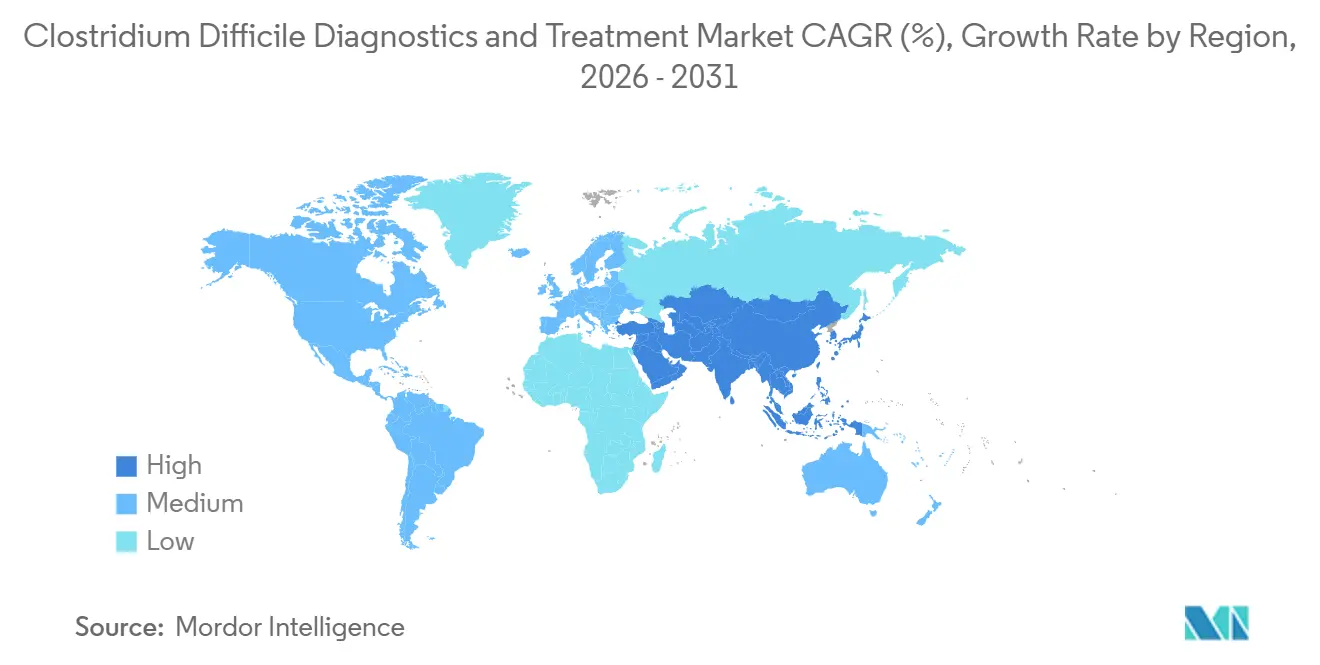

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

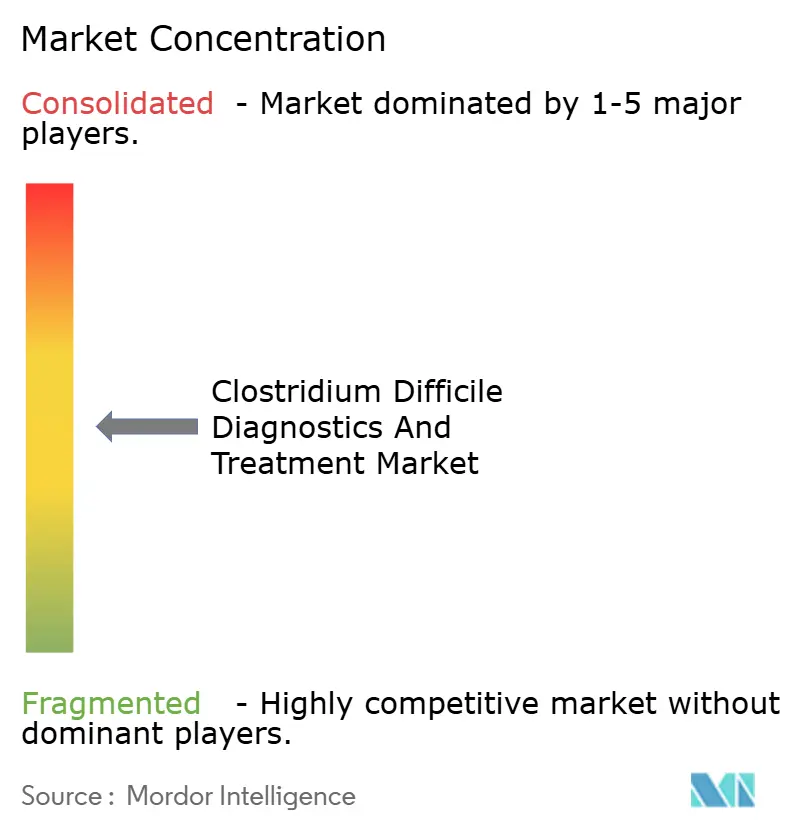

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Clostridium Difficile Diagnostics And Treatment Market Analysis by Mordor Intelligence

The Clostridium Difficile Diagnostics And Treatment Market size is estimated at USD 3.25 billion in 2026, and is expected to reach USD 5.80 billion by 2031, at a CAGR of 12.29% during the forecast period (2026-2031).

Molecular platforms that deliver sub-60-minute results allow infection-control teams to isolate carriers sooner, cutting onward transmission and lowering the hidden costs of prolonged contact precautions. At the same time, guideline elevation of fidaxomicin and live biotherapeutics is compressing recurrence rates, even though the 57-fold price gap with vancomycin fragments reimbursement pathways across payers. Hospitals under value-based purchasing models are linking diagnostic upgrades to penalty avoidance, while manufacturers near-shore cartridge production to dodge tariff shocks and shorten lead times. Competitive focus is shifting from price to analytical sensitivity; AI-enhanced toxin assays and multiplex gastrointestinal panels promise to shrink the gray zone of discordant results that currently drive reflex testing and overtreatment.

Key Report Takeaways

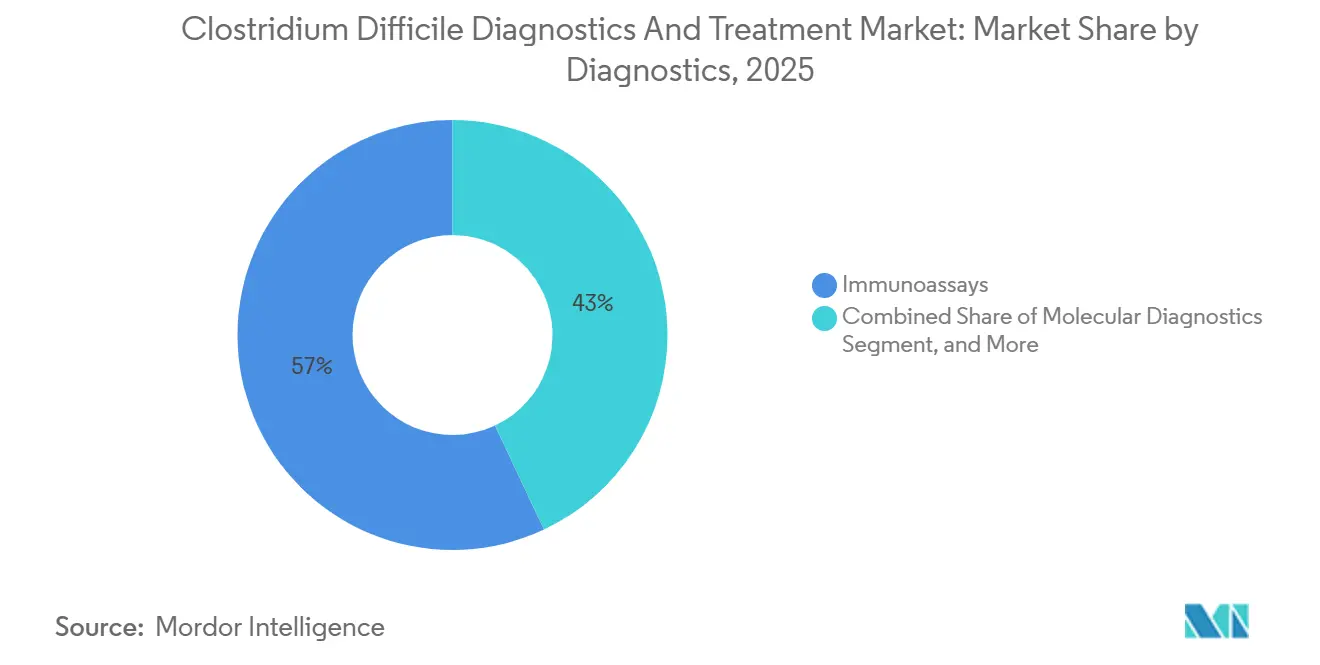

- By diagnostics type, immunoassays led the category with 57.01% revenue share in 2025. Molecular diagnostics represent the fastest-growing diagnostic modality, advancing at a 7.09% CAGR through 2031.

- By treatment type, antibiotic therapy accounted for 71.67% of treatment spending in 2025, while microbiota restoration therapies are expanding at a 7.78% CAGR.

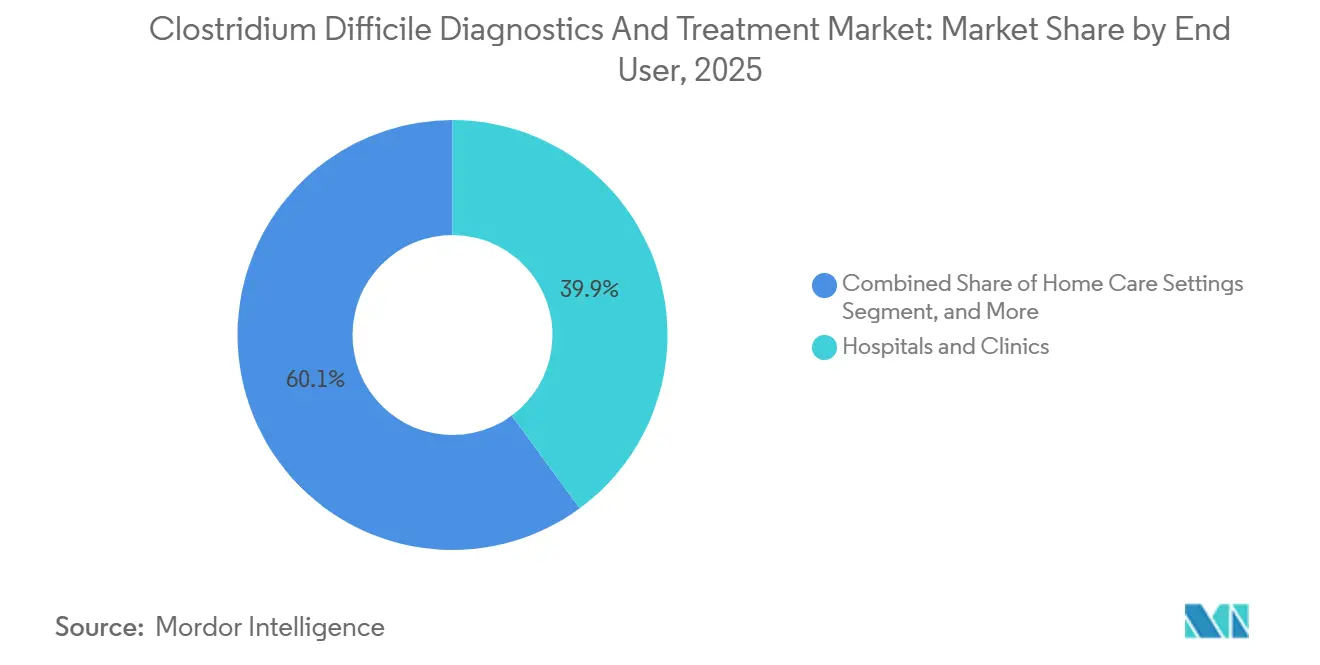

- By end user, hospitals and clinics captured 39.92% of end-user revenue in 2025; home care settings are advancing at a 9.69% CAGR.

- By geography, North America commanded 42.83% of 2025 revenue; Asia-Pacific is forecast to grow at 10.27% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Clostridium Difficile Diagnostics And Treatment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Adoption of NAAT & Multiplex Molecular Panels | +2.8% | Global, with early penetration in North America and Western Europe | Medium term (2-4 years) |

| Increasing CDI Incidence Among Ageing Populations | +3.1% | Japan, South Korea, Western Europe, North America | Long term (≥ 4 years) |

| Guideline Shift to Fidaxomicin & Microbiota Therapies | +2.4% | North America, Europe, Australia; limited APAC and LATAM uptake | Medium term (2-4 years) |

| Hospital Penalties for Healthcare-Associated Infections | +1.6% | United States (CMS HAC program), expanding to select EU markets | Short term (≤ 2 years) |

| AI-Enabled Ultra-Sensitive Toxin Assays Gaining Traction | +1.2% | North America, Germany, UK, Japan | Medium term (2-4 years) |

| Antimicrobial Tariff Shocks Driving Near-Shoring of Test Kit Production | +0.9% | United States, European Union | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Adoption of NAAT & Multiplex Molecular Panels

Hospitals are rapidly replacing enzyme immunoassays with nucleic acid amplification tests that detect tcdA and tcdB, boosting sensitivity above 95% and shortening turnaround to under one hour.[1]U.S. Food and Drug Administration, “Nucleic Acid-Based Tests,” fda.gov Cepheid’s Xpert C. difficile/Epi panel, cleared in January 2026, simultaneously flags hypervirulent ribotype 027 strains, giving infection-control teams an early warning during outbreaks. bioMérieux’s FILMARRAY GI Panel bundles C. difficile with 21 other enteric pathogens, collapsing multiday diagnostic odysseys into a single run and appealing to emergency departments prioritizing throughput. QIAGEN’s cartridge-based QIAstat-Dx GI Panel 2 Mini extends molecular accuracy to point-of-care sites that lack thermal cyclers, meeting rural demand for faster triage. Although reagent costs jump from USD 5 to USD 25 per test, hospitals recoup the premium by cutting isolation days that cost USD 100–150 each.

Increasing CDI Incidence Among Ageing Populations

Japan’s 65-plus cohort already exceeds 29% of the population and continues to grow, creating a reservoir with polypharmacy exposure, disrupted microbiota, and repeated healthcare contacts, all of which elevate CDI risk.[2]Statistics Bureau of Japan, “Population Estimates,” stat.go.jp China and India add millions of older adults annually; tertiary centers in both nations already report CDI incidences ranging from 0.8 to 6.3 per 10,000 patient-days, despite underdiagnosis outside metropolitan hubs. Australia shows similar pressure, with rural hospitals still relying on single-step immunoassays that miss up to 30% of cases. The demographic wave is durable and is pushing laboratories toward isothermal amplification platforms that require minimal capital, easing uptake in community settings serving older, frail populations.

Guideline Shift to Fidaxomicin & Microbiota Therapies

The IDSA/SHEA update moved fidaxomicin to first-line status for both initial and recurrent disease, citing a 15-percentage-point advantage over vancomycin in recurrence. Live biotherapeutics broadened options: Seres Therapeutics’ Vowst delivered an 88% sustained clinical response in the ECOSPOR III trial, while Ferring’s Rebyota achieved 70.6% in the PUNCH CD3 trial, validating microbiota restoration as a one-time solution that can prevent costly recurrences. The American Gastroenterological Association endorsed these products after a single recurrence, shortening the treatment funnel and accelerating payer coverage. Adoption still varies; Medicaid plans often require prior authorization because Vowst’s USD 17,500 price and Rebyota’s USD 20,000 cost dwarf vancomycin’s USD 75 tag, yet commercial insurers increasingly weigh the USD 30,000 burden of each recurrence.

Hospital Penalties for Healthcare-Associated Infections

CMS subjects hospitals in the worst infection-control quartile to a 1% payment reduction, an aggregate USD 350 million hit in fiscal-year 2025.[3]Centers for Medicare & Medicaid Services, “HAC Reduction Program,” cms.gov Administrators therefore invest in rapid molecular panels that cut time-to-isolation from 48 hours to 90 minutes and lower secondary transmissions by 40%. Germany’s quality agency now publishes hospital-specific CDI rates, stoking competitive pressure and reputational risk that accelerate diagnostic upgrades. Institutions able to couple NAAT adoption with antimicrobial stewardship rise out of the penalty quartile, while laggards compound their budget squeeze, creating a virtuous-or-vicious cycle depending on strategic choices.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost of Fidaxomicin & Next-Gen Diagnostics | -1.8% | Global, most acute in emerging markets and U.S. Medicaid populations | Medium term (2-4 years) |

| Diagnostic Overuse Leading to Overtreatment | -1.3% | North America, Western Europe | Short term (≤ 2 years) |

| Withdrawal Of Bezlotoxumab Limits Biologic Adoption | -0.7% | Global | Short term (≤ 2 years) |

| Disparities In Reimbursement Across Emerging Markets | -1.1% | Latin America, Middle East & Africa, South Asia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Cost of Fidaxomicin & Next-Gen Diagnostics

Fidaxomicin’s USD 4,300–5,000 course costs 57 times more than vancomycin, leading insurers to impose prior authorization that can delay therapy and unintentionally raise recurrence risk. Vowst and Rebyota list at USD 17,500 and USD 20,000, relegating them to later-line status except in well-funded systems. Syndromic molecular panels priced at USD 100–150 per run force laboratories to ration testing, limiting deployment to severe diarrhea or immunocompromised cases. Medicaid budgets and out-of-pocket markets, such as India, face particularly steep barriers, so clinicians continue prescribing generic metronidazole despite its removal from guidelines, perpetuating suboptimal outcomes.

Diagnostic Overuse Leading to Overtreatment

Colonization without symptoms affects up to 50% of inpatients, and NAATs cannot distinguish these carriers from those with active infection, leading to unnecessary isolation and antibiotic courses. A 2024 audit of 120 U.S. hospitals showed that 18% of CDI tests were ordered on patients without diarrhea, largely due to reflex protocols embedded in EHR systems. Contact precautions alone cost USD 100–150 per patient-day, amplifying financial waste. Stewardship programs that gate NAAT orders through infectious-disease review cut inappropriate testing by 35% but delayed true-positive diagnoses in 8% of cases, underscoring the delicate balance between access and overuse. Decision-support algorithms mining nursing notes for stool consistency represent a scalable fix, yet adoption remained at only 12% of U.S. hospitals by mid-2025.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Diagnostics: Molecular Platforms Gain Despite Immunoassay Dominance

Immunoassays accounted for 57.01% of diagnostic revenue in 2025, driven by low reagent costs, 15-minute workflows, and broad automation compatibility. However, the Clostridium difficile diagnostics and treatment market anticipates molecular diagnostics will post a 7.09% CAGR through 2031, as laboratories favor 95%-plus sensitivity to capture low-toxin-load cases. The FDA rule phasing out in-house assays is accelerating the shift, pushing community hospitals toward cleared kits that offer regulatory certainty even at higher per-test prices. CMS reinforced the trend by lifting NAAT reimbursement from USD 22 to USD 28 in the 2025 fee schedule, narrowing the cost gap and nudging procurement committees toward molecular upgrades.

Isothermal amplification is carving out a capital-light niche. Quidel’s AmpliVue, cleared in September 2025, uses helicase-dependent amplification to provide 20-minute results from a handheld device, a value proposition for critical-access hospitals lacking PCR equipment. Point-of-care rapid tests, though nascent, resonate with emergency departments that prefer triage speed over marginal gains in analytical sensitivity. As hospitals retire legacy immunoassay analyzers to comply with FDA guidance, vendors bundle training and middleware, smoothing the transition and locking in reagent contracts. Collectively, these shifts support sustained molecular penetration, keeping the clostridium difficile diagnostics and treatment market on an upgrade trajectory through 2031.

By Treatment Type: Microbiota Therapies Reshape Recurrence Management

Antibiotics dominated 2025 spending with a 71.67% share, led by inexpensive vancomycin and generic metronidazole, both of which have reimbursement constraints. Nevertheless, microbiota restoration therapies are expected to expand at a 7.78% CAGR, supported by evidence that each recurrence costs the system USD 30,000, far outweighing the upfront therapy price. Fidaxomicin adoption also grows as commercial plans improve prior-authorization approval to 68%, up from 52% in 2023, reflecting payer recognition of its 15-point recurrence edge.

Live biotherapeutics compress the treatment funnel. Vowst and Rebyota have demonstrated durable responses that reduce the need for prolonged vancomycin tapers, a paradigm shift that the American Gastroenterological Association codified in 2024 guidance. Monoclonal antibodies retreated after Merck withdrew bezlotoxumab in 2024, leaving a gap unlikely to be filled in the short term. The pipeline remains active: Summit Therapeutics’ ridinilazole cut recurrence by 12 points in Phase 3 and, if approved, could further erode vancomycin share, while Acurx’s ibezapolstat pursues a twice-daily dosing regimen that may simplify adherence. These developments keep the clostridium difficile diagnostics and treatment market in flux, with reimbursement policies dictating the pace of therapeutic substitution.

By End User: Home Care Gains as Telehealth Expands Access

Hospitals and clinics held 39.92% of end-user revenue in 2025, reflecting their central role in both diagnosis and initial therapy. Clinical laboratories accounted for 28%, while point-of-care settings contributed 12% as urgent-care chains and skilled nursing facilities adopted cartridge-based systems. Yet the fastest growth belongs to home care, advancing at 9.69% as telehealth platforms integrate at-home stool kits that ship samples to CLIA-certified labs within 48 hours.

Regulatory tailwinds support decentralization. The FDA’s 2024 guidance clarified that at-home collection devices may bypass pre-market review if analysis occurs in a certified lab, encouraging direct-to-consumer entrants. Medicare’s 2025 expansion of remote-patient-monitoring codes now reimburses providers USD 50 per month to track CDI symptom resolution via apps, further monetizing virtual follow-up. Consequently, the Clostridium difficile diagnostics and treatment market continues to shift testing and care to patients’ homes, where convenience and lower facility fees align with payer goals.

Geography Analysis

North America retained the largest regional position with 42.83% of 2025 revenue, anchored by about 450,000 annual CDI cases in the United States and Canada’s universal coverage of molecular testing. The Clostridium difficile diagnostics and treatment market size in North America is projected to expand steadily as CMS penalties reinforce diagnostic upgrades and private insurers begin reimbursing microbiota therapies.

Asia-Pacific is the fastest-growing region, with a 10.27% CAGR through 2031. Japan’s aging curve, China’s hospital construction boom, and India’s private-payer expansion combine to enlarge diagnostic and therapeutic demand. Stewardship programs mandating two-step testing algorithms accelerate molecular uptake, while isothermal platforms appeal to community hospitals that lack capital for PCR. As these dynamics compound, the Asia-Pacific is expected to capture a rising share of the Clostridium difficile diagnostics and treatment market.

Germany publicly posts hospital-level CDI rates, spurring rapid assay replacement, whereas Southern European markets face reimbursement constraints that slow NAAT adoption. The UK reported a total of 8,141 cases in fiscal 2023-24, a 12% decline from 2019-20, illustrating the payoff from stringent fluoroquinolone stewardship. The Middle East & Africa and South America together comprise 14% of revenue, with uptake tied to private-sector investment and accreditation drives in Gulf Cooperation Council states and Brazilian hospital chains, respectively.

Competitive Landscape

The Clostridium difficile diagnostics and treatment market is moderately consolidated. The top five diagnostics suppliers, Roche, Abbott, bioMérieux, Cepheid, and QIAGEN, collectively held significant global revenue, leveraging extensive installed bases and regulatory expertise. Cepheid capitalized on its 2026 clearance for the Xpert C. difficile/Epi panel, which differentiates hypervirulent ribotype 027 strains, strengthening its position in outbreak-prone hospitals. bioMérieux’s syndromic FILMARRAY GI Panel appeals to emergency departments that value single-run answers, while Quidel’s instrument-free AmpliVue targets under-resourced facilities.

Treatment competition is more fragmented. Generic vancomycin dominates volume, but branded fidaxomicin (Merck’s Dificid) captures the premium segment. Seres Therapeutics and Ferring Pharmaceuticals are carving out the high-value recurrence niche with Vowst and Rebyota, respectively, while Summit Therapeutics and Acurx Pharmaceuticals pursue narrow-spectrum antibiotics that preserve microbiota diversity. AI-driven decision-support software emerges as a differentiator; vendors now bundle stewardship dashboards that block inappropriate orders, adding sticky SaaS revenue streams.

Regulatory frameworks such as FDA clearance, ISO 13485, and the EU In Vitro Diagnostic Regulation raise barriers to entry, favoring incumbents with dedicated compliance teams. Tariff-driven near-shoring further advantages firms that can invest in domestic cartridge factories, as evidenced by Roche’s USD 150 million expansion in Indianapolis, which cut lead times to 4 weeks. Collectively, these factors point toward steady, though not absolute, consolidation, positioning the Clostridium difficile diagnostics and treatment market for disciplined yet competitive growth.

Clostridium Difficile Diagnostics And Treatment Industry Leaders

AstraZeneca plc

Becton, Dickinson & Company

bioMérieux SA

Qiagen NV

Siemens Healthineers

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: QIAGEN obtained FDA clearance for the QIAstat-Dx GI Panel 2 Mini, a 70-minute cartridge-based molecular system aimed at point-of-care environments.

- May 2024: Researchers at Digestive Disease Week 2024 reported high discordance rates between CDI diagnosis and true infection status, underscoring the need for better diagnostic accuracy.

Global Clostridium Difficile Diagnostics And Treatment Market Report Scope

The Clostridium Difficile (C. diff) Diagnostics and Treatment Market refers to the global healthcare industry segment that develops, manufactures, and delivers diagnostic tools and therapeutic solutions for Clostridium difficile infection (CDI), a major cause of healthcare-associated diarrhea and colitis.

The Clostridium Difficile Diagnostics and Treatment Market Report is Segmented by Diagnostics (Immunoassays, Molecular Diagnostics, Isothermal Amplification, Point-of-Care Rapid Tests), Treatment Type (Antibiotic Therapy, Monoclonal Antibodies, Microbiota Restoration Therapies, Vaccines), End User (Hospitals & Clinics, Diagnostic Laboratories, Point-of-Care Settings, Home Care Settings), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

| Immunoassays |

| Molecular Diagnostics |

| Isothermal Amplification |

| Point-of-Care Rapid Tests |

| Antibiotic Therapy |

| Monoclonal Antibodies |

| Microbiota Restoration Therapies |

| Vaccines |

| Hospitals & Clinics |

| Diagnostic Laboratories |

| Point-of-Care Settings |

| Home Care Settings |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Diagnostics | Immunoassays | |

| Molecular Diagnostics | ||

| Isothermal Amplification | ||

| Point-of-Care Rapid Tests | ||

| By Treatment Type | Antibiotic Therapy | |

| Monoclonal Antibodies | ||

| Microbiota Restoration Therapies | ||

| Vaccines | ||

| By End User | Hospitals & Clinics | |

| Diagnostic Laboratories | ||

| Point-of-Care Settings | ||

| Home Care Settings | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the Clostridium difficile diagnostics and treatment market in 2026?

The market stood at USD 3.25 billion in 2026 and is forecast to grow at a 12.29% CAGR to 2031.

Which diagnostic modality is expanding the fastest?

Molecular platforms are growing at a 7.09% CAGR as hospitals favor greater sensitivity and faster turnaround times.

What drives uptake of microbiota restoration therapies?

Payers are weighing their USD 17,500–20,000 cost against the USD 30,000 burden of each recurrence, boosting adoption.

Why is Asia-Pacific the fastest-growing region?

Aging demographics, hospital infrastructure expansion, and national stewardship programs push the regional CAGR to 10.27%.

How do CMS penalties influence hospital purchasing?

Hospitals facing 1% payment cuts invest in rapid molecular panels that cut isolation time and improve infection-control rankings.

Page last updated on: