Clinical Trial Management Contract Research Organization (CRO) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

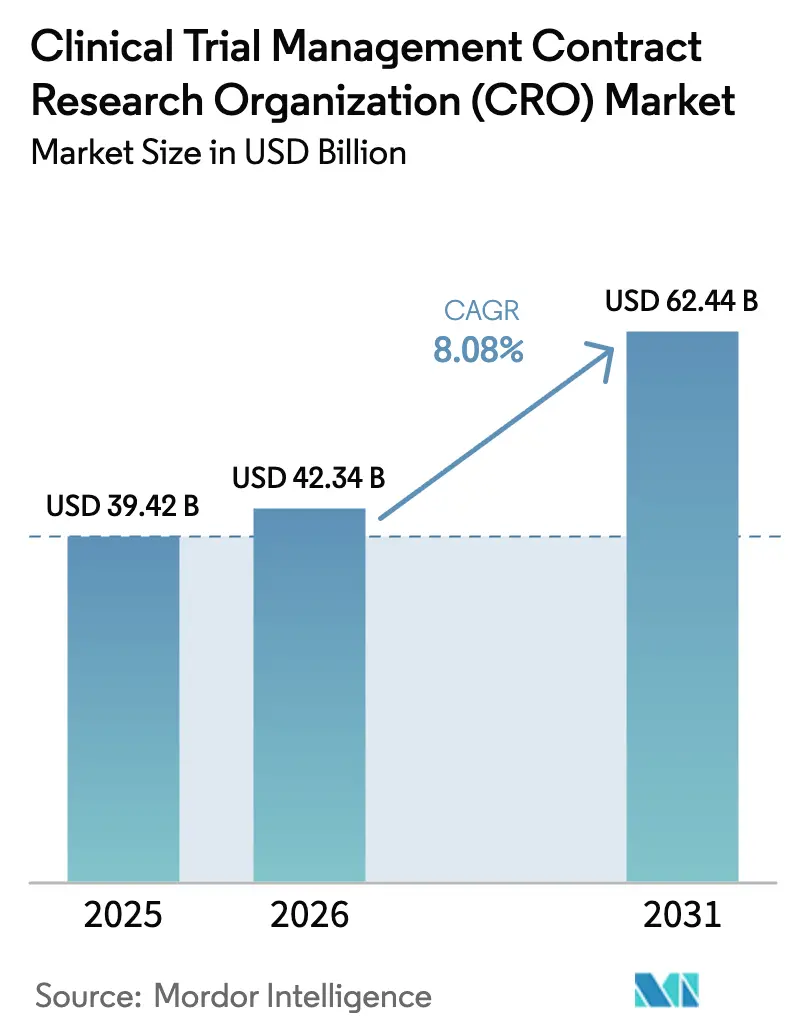

| Market Size (2026) | USD 42.34 Billion |

| Market Size (2031) | USD 62.44 Billion |

| Growth Rate (2026 - 2031) | 8.08% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

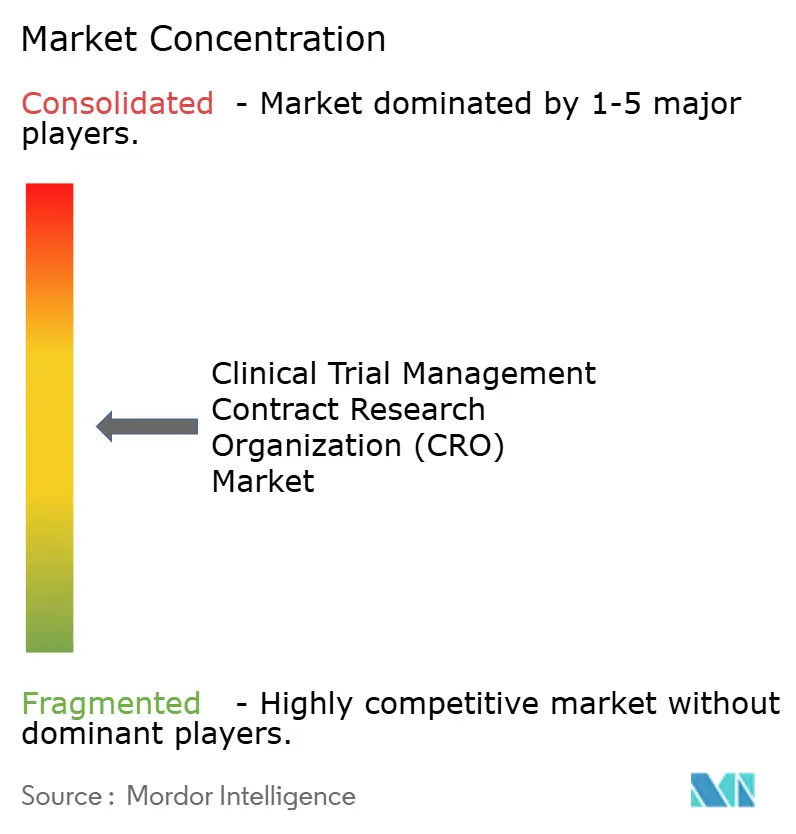

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Clinical Trial Management Contract Research Organization (CRO) Market Analysis by Mordor Intelligence

The Clinical Trial Management Contract Research Organization Market was valued at USD 39.42 billion in 2025 and expected to grow from USD 42.34 billion in 2026 to reach USD 62.44 billion by 2031, at a CAGR of 8.08% during the forecast period (2026-2031).

Growing therapeutic complexity, tighter regulatory oversight, and the escalating costs of in-house trial infrastructure push sponsors toward full-service partners that can coordinate global studies seamlessly. Hybrid and decentralized models, validated by the FDA in 2024, shave 15-25% off per-patient costs and improve retention, making them a centerpiece of sponsor sourcing strategies. Oncology’s capital-intensive protocols, Bayesian adaptive designs, and the surge of GLP-1 cardiovascular outcome studies collectively sustain premium pricing for specialist providers. Meanwhile, AI-enabled patient matching platforms and unified data lakes give technology-forward CROs an edge in bid defense, while sponsors reward end-to-end offerings that compress cycle times and bolster data integrity. Altogether, the Clinical Trial Management CRO market is positioned for durable double-digit expansion as outsourcing shifts from transactional staffing to strategic, analytics-driven partnerships.

Key Report Takeaways

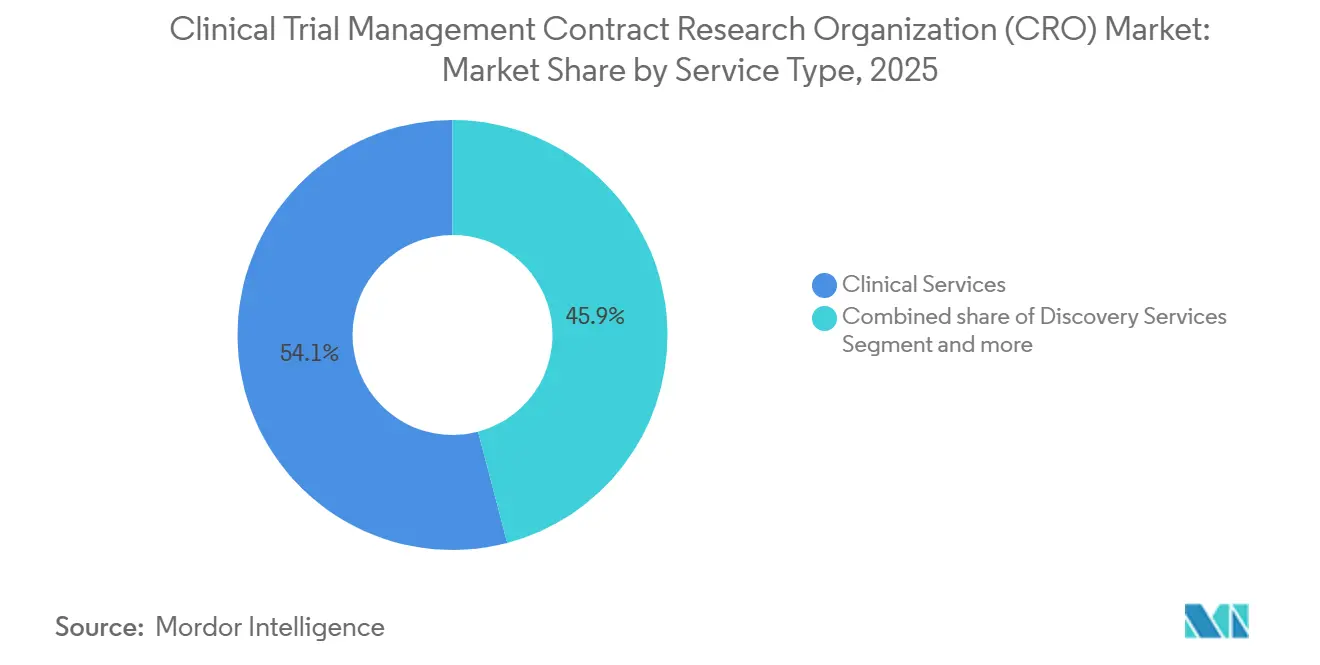

- By service type, Clinical Services commanded 54.1% of the Clinical Trial Management CRO market share in 2025. Discovery services are forecast to expand at a 8.56% CAGR from 2026 to 2031.

- By therapeutic area, oncology contributed 30.40% revenue in 2025, while infectious diseases are projected to grow at a 8.99% CAGR through 2031.

- By clinical phase, Phase III contributed 53.97% revenue in 2025, is projected to grow at a 9.12% CAGR through 2031

- Pharmaceutical and biopharmaceutical companies accounted for 56.30% demand in 2025, yet Academic & Research Institutes are set to climb at a 8.86% CAGR to 2031.

- North America held 38.90% revenue in 2025, whereas Asia-Pacific will progress at a 8.32% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Clinical Trial Management Contract Research Organization (CRO) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing pharmaceutical R&D outsourcing | +2.8% | North America, Europe, and worldwide expansion | Medium term (2-4 years) |

| Rising trial and regulatory complexity | +2.1% | North America, Europe, Japan | Long term (≥ 4 years) |

| Growing chronic-disease trial volume | +1.9% | Asia-Pacific fastest, global effect | Long term (≥ 4 years) |

| Adoption of decentralized and hybrid models | +1.3% | North America and Europe lead, Asia-Pacific scaling | Short term (≤ 2 years) |

| Technological advancements in AI and data analytics for trial optimization | +1.1% | Global, concentrated in North America and Europe with technology infrastructure | Medium term (2-4 years) |

| Expansion of rare-disease and orphan-drug development programs | +0.9% | North America and Europe dominate, with emerging Asia-Pacific participation | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Pharmaceutical R&D Outsourcing to CROs

More than half of all sponsor clinical budgets flowed to external providers in 2024, up 5 percentage points since 2020, as leaner R&D headcounts and pipeline diversity made vertical integration less feasible. Mid-cap biotechs outsourced majority of operations, using milestone-based contracts that shift risk yet accelerate market entry by roughly eight months for oncology assets. The Clinical Trial Management CRO market benefits because sponsors now extend outsourcing upstream into discovery biology and toxicology, enlarging deal scope from individual trials to multi-asset platforms. Risk-sharing terms align incentives but pressure CRO balance sheets, prompting larger players to build cash reserves or secure revolving credit lines. Government grant flows, particularly the NIH’s USD 3.2 billion infrastructure pool in 2024, funnel academic studies toward CRO support, broadening the addressable client base.

Rising Complexity of Clinical Trials and Regulatory Requirements

Median Phase III oncology trials enrolled 800 patients across 150 sites in 2024, as regulators insisted on broader demographic representation [1]U.S. Food and Drug Administration, “Decentralized Clinical Trials Guidance,” fda.gov. Bayesian adaptive designs, codified in FDA guidance in March 2024, require specialized biostatistical skills available to only about one-third of sponsors, increasing reliance on CRO analytics teams. Europe’s Clinical Trial Regulation, fully live from January 2025, will require centralized submission via CTIS and tightened reporting timelines, compelling IT investments that only large CROs can absorb comfortably. Japan’s real-world evidence mandate and China’s alignment with ICH E6(R3) further elevate compliance hurdles. As a result, scale and capital intensity force consolidation, lifting the Clinical Trial Management CRO market entry barrier for smaller firms.

Growing Prevalence of Chronic Diseases Driving Trial Volume

Oncology initiated 38% of all new trials in 2024, while cardiovascular and metabolic studies climbed 14% year over year, propelled by GLP-1 projects enrolling thousands of participants. The World Health Organization expects chronic disease prevalence in Asia-Pacific to jump 35% by 2030, making the region a recruitment hotspot. Yet global investigator workloads rose; U.S. sites averaged 12 concurrent protocols in 2024, inflating deviation risk. CROs, therefore, roll out AI-powered feasibility tools to pre-screen high-performing sites and predict enrollment curves, improving bid competitiveness as sponsors quantify the cost of late timelines.

Adoption of Decentralized and Hybrid Trial Models

The FDA’s January 2024 guidance legitimized tele-visits, e-consent, and local labs, triggering a 42% adoption rate for hybrid Phase II/III studies that year [2]U.S. Food and Drug Administration, “Adaptive Designs Guidance,” fda.gov. Technology-enabled trials carry 15-20% pricing uplifts, a boon for the Clinical Trial Management CRO market. Cybersecurity lapses, evidenced by six FDA warning letters in 2024, however, expose providers to reputational risk, pushing them to invest USD 2-3 million annually in HIPAA-compliant cloud and third-party audits. Regional disparities persist; China still restricts remote consent, curbing scale, though pilot programs indicate a gradual liberalization trajectory by 2027.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Investigator-site capacity and recruitment | -0.9% | Acute in North America, Western Europe | Short term (≤ 2 years) |

| Data-integrity scrutiny of CRO operations | -0.6% | Global, intensified FDA and EMA oversight | Medium term (2-4 years) |

| High costs of clinical trials are limiting sponsor budgets and trial starts | -0.7% | Global, particularly impacting small-to-mid biotech in North America and Europe | Medium term (2-4 years) |

| Shortage of qualified clinical research professionals and investigator burnout | -0.5% | North America and Europe are acute, with emerging skill gaps in the Asia-Pacific markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Investigator Site Capacity Constraints and Patient Recruitment Challenges

North American site availability fell 8% in 2024 because burnout prompted principal investigators to scale back commitments. Activation timelines stretched to 16 weeks, delaying first-patient-in schedules, while oncology recruitment failure hit 37%. Predictive analytics platforms mitigate risk but require multi-year data histories, delaying ROI. India’s 240 newly certified sites and China’s 60-day approvals offer relief, yet linguistic and consent-form nuances slow turn-on, reinforcing site shortfalls that temporarily temper Clinical Trial Management CRO market growth.

Data Integrity Concerns and Regulatory Scrutiny of CRO Operations

The FDA issued 18 warning letters for data manipulation in 2024, with CRO-run trials over-represented, jolting sponsor confidence. May 2024 guidance demanded role-based access controls and immutable audit trails, lifting quality-system costs by USD 2-3 million per provider. Inspections across Europe intensified, and insurance premiums for clinical liabilities ticked up, squeezing mid-tier margins. Sponsors reacted by funneling work to ISO-certified, tech-enabled vendors, nudging the Clinical Trial Management CRO market toward higher concentration among well-capitalized firms.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Full-Service Dominance Against FSP Momentum

Clinical Services captured 54.1% of the Clinical Trial Management CRO market revenue in 2025, reflecting a clear sponsor bias for single-vendor accountability around protocol, data, and regulatory deliverables. The Clinical Trial Management CRO market size for full-service contracts continues to widen as complex oncology and GLP-1 mega-trials reward integrated execution models. Sponsors accept higher fees because unified quality oversight reduces re-work and inspection findings. Discovery outsourcing, forecast at 8.56% CAGR to 2031, gains traction with platform biotechs that lack vivaria or assay labs. Concurrently, pharmacovigilance and medical-writing demand rises as post-marketing commitments multiply under real-world evidence guidelines.

Functional service providers (FSPs) reported significant revenue growth in 2025, supplying embedded biostatisticians, data managers, and medical writers on variable terms that appeal to cash-constrained biotechs. Yet scaling FSP engagements to global Phase III demands hybrid models that blend staff augmentation with centralized governance. AI-driven screening has trimmed labor hours in discovery assays, pressuring margins, so CROs race to patent proprietary cell and disease models that command premium licensing fees. The Clinical Trial Management CRO industry increasingly views technology ownership, not merely headcount, as the determinant of long-run profitability.

By Therapeutic Area: Oncology Complexity Sustains Premium Pricing

Oncology held 30.40% of the Clinical Trial Management CRO market share in 2025. High-dose antibody-drug conjugate protocols require specialized infusion centers and intricate safety monitoring, driving per-study values above USD 100 million. Infectious diseases, while a smaller base, is the fastest-growing segment at 8.99% CAGR as governments invest in pandemic readiness platforms. Cardiovascular-metabolic outcome trials, catalyzed by GLP-1 classes, enroll 5,000+ patients, creating blockbuster engagements with longitudinal follow-up that stick CROs to sponsors for 5-7 years.

Neurology studies struggle with rare-disease recruitment, but the segment remains lucrative because decentralized cognitive assessments lower participant burden and extend geographic reach. Immunology trials increasingly depend on multi-omics biomarkers, pushing CROs to build central lab alliances. Respiratory projects moderated in 2024 after COVID-19 tapering; however, long-COVID and asthma biologics partially offset the dip. Master protocol guidance from April 2024 favors CROs with deep therapeutic benches capable of running multi-arm, multi-drug platforms, enhancing differentiation within the Clinical Trial Management CRO market.

By Clinical Phase: Phase III Capital Intensity Drives Revenue

Phase III accounted for 53.97% of 2025 spending and is set for 9.12% CAGR through 2031. Sponsors pay premium rates for global site networks, data-lock reliability, and inspection readiness, reinforcing revenue concentration among tier-one vendors. The Clinical Trial Management CRO market size attributable to Phase III alone often exceeds USD 20 billion annually. First-in-human oncology projects lift Phase I revenues as genetic safety triggers require continuous telemetry infrastructure. Phase II attrition remains high, prompting milestone-based pricing that aligns cost with proof-of-concept probability.

Phase IV grew notablally in 2024 as regulators and payers demanded real-world comparative evidence, and CROs adapted by partnering with claims and EMR data brokers. Seamless Phase II/III designs, sanctioned by FDA guidance, encourage larger, adaptive programs managed under a single contract. These require advanced biostatistics and regulatory affairs integration, capabilities resting mainly with the upper quartile of providers, reinforcing the Clinical Trial Management CRO industry’s consolidation trend.

By End-User: Academic Partnerships Reshape Demand

Pharmaceutical and biopharmaceutical firms held 56.30% of 2025 billings, yet universities are the breakout growth customers at 8.86% CAGR to 2031 as tech-transfer offices commercialize translational assets. The Clinical Trial Management CRO market responds by creating academic liaison teams versed in grant compliance and institutional review board coordination. Device makers, dealing with long-term implant follow-ups, rely on CROs for imaging core labs and surgeon training, a niche that commands above-average margins.

Government and non-profit organizations remain smaller but strategically important because they seed trials in neglected diseases, expanding therapeutic breadth. Digital health validation surged after the FDA widened device definitions in 2024, channeling software-as-a-medical-device studies into CRO pipelines. Private-equity-backed biotechs, seeking asset-light models, outsource nearly all functions beyond C-suite leadership, providing steady FSP demand within the Clinical Trial Management CRO market.

Geography Analysis

North America generated 38.90% of 2025 revenue as the Clinical Trial Management CRO market anchor, owing to dense investigator networks, high sponsor headcount, and swift FDA guidance cycles. Yet average Phase III per-patient costs reached USD 60,000, motivating geographic diversification. Decentralized models, cleared by the FDA in 2024, cut site visit frequency and leverage EMR-based endpoints, reducing direct costs by about one-fifth. Still, site capacity pressures persist; U.S. centers managed 12 concurrent protocols in 2024, elevating deviation rates that compel CROs to raise monitoring budgets. Asia-Pacific will expand at 8.32% CAGR through 2031, underpinned by China’s 60-day approvals and India’s 240 newly certified sites. Harmonization with ICH E6(R3) in 2024 calmed sponsor concerns about Chinese data acceptability [3]China National Medical Products Administration, “ICH E6(R3) Implementation,” nmpa.gov.cn. India’s corporate hospital networks provide standardized electronic records, but regional ethics committees add cycle time variability. Japan’s English-language pathway, introduced in 2024, trims documentation lead times, though its aging population complicates naïve-patient recruitment. Southeast Asian countries entice early-phase oncology trials with cost savings near 50%, yet regulator capacity lags, extending dossier review.

Europe retained stable share after the January 2025 CTIS launch unified submissions across 27 member states. Centralized portals slice administrative load, but Brexit imposes duplicate filings for U.K. sites, fragmenting what was once a contiguous region. Eastern Europe offers 40-50% lower per-patient costs but geopolitical risk reduced trial placements 12% in 2024. The Middle East & Africa and South America are emerging zones; South Africa’s harmonized ethics approvals and disease epidemiology position it as the sub-Saharan beachhead, while Brazil’s ANVISA backlog remains a gating factor for rapid study start-ups. Collectively, these dynamics ensure the Clinical Trial Management CRO market enjoys balanced regional growth without over-reliance on any single geography.

Competitive Landscape

The top five providers controlled significant share of 2025 revenue, indicating moderate concentration. Full-service incumbents compete on therapeutic acumen, global reach, and integrated platforms combining EDC, e-PRO, and real-world evidence ingestion. Mid-tier specialists thrive by focusing on oncology, CNS, or rare-disease corridors where investigator relationships trump scale. Functional service providers regestered significant growth in 2025 as sponsors opted for variable staffing models, a trend forecast to persist as venture-backed biotechs guard cash.

Technology capability delineates winners. AI-driven patient matching slashed enrollment timelines by up to 20%, prompting patent filings to jump 40% between 2024-2025. Only about one-fifth of CROs currently deliver decentralized visit networks at scale, marking a clear white space. Real-world data integration equally separates contenders; building secure data pipelines with EMR vendors costs upward of USD 10 million, a hurdle that smaller firms seldom cross. ISO 9001 and ICH E6(R3) compliance are now table stakes, while cloud security audits and role-based access controls gain weight in RFP scoring. Collectively, these factors push the Clinical Trial Management CRO market toward deeper consolidation or strategic alliances.

Clinical Trial Management Contract Research Organization (CRO) Industry Leaders

IQVIA

ICON plc

Labcorp Drug Development

Charles River Labs

Parexel

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: IQVIA was named a “front-runner generative AI leader” for life sciences by Everest Group, underscoring competitive differentiation through advanced analytics.

- January 2025: ICON plc expanded its AI toolset with iSubmit, Mapi Research Trust COA, FORWARD+, and OMR AI Navigation Assistant, targeting study start-up and resource forecasting efficiencies

Global Clinical Trial Management Contract Research Organization (CRO) Market Report Scope

As per the scope of the report, a clinical trial management contract research organization is a specialized organization that provides comprehensive management and support services for clinical trials conducted on behalf of pharmaceutical, biotechnology, and medical device companies.

The clinical trial management contract research organization (CRO) market is segmented by service type, therapeutic area, clinical phase, end-users, and geography. By service type, the market is categorized into discovery services, pre-clinical services, clinical services, and others. By therapeutic area, the market is divided into Oncology, CNS / Neurology, Cardiovascular & Metabolic, Infectious Diseases, Immunology / Inflammatory, Respiratory, and Others. By clinical phase, it is segmented into Pre-clinical, Phase I, Phase II, Phase III, and Phase IV. By end-users, the segmentation includes pharmaceutical and biopharmaceutical companies, medical device companies, academic & research institutes, and government & non-profit organizations. Geographically, the market is segmented across North America, Europe, the Asia-Pacific region, the Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Discovery Services |

| Pre-clinical Services |

| Clinical Services |

| Others |

| Oncology |

| CNS / Neurology |

| Cardiovascular & Metabolic |

| Infectious Diseases |

| Immunology / Inflammatory |

| Respiratory |

| Others |

| Pre-clinical |

| Phase I |

| Phase II |

| Phase III |

| Phase IV |

| Pharmaceutical and Biopharmaceutical Companies |

| Medical Devices companies |

| Academic & Research Institutes |

| Government & Non-Profit Organisations |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Service Type | Discovery Services | |

| Pre-clinical Services | ||

| Clinical Services | ||

| Others | ||

| By Therapeutic Area | Oncology | |

| CNS / Neurology | ||

| Cardiovascular & Metabolic | ||

| Infectious Diseases | ||

| Immunology / Inflammatory | ||

| Respiratory | ||

| Others | ||

| By Clinical Phase | Pre-clinical | |

| Phase I | ||

| Phase II | ||

| Phase III | ||

| Phase IV | ||

| By End-Users | Pharmaceutical and Biopharmaceutical Companies | |

| Medical Devices companies | ||

| Academic & Research Institutes | ||

| Government & Non-Profit Organisations | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the Clinical Trial Management CRO market in 2026?

Clinical Trial Management CRO market is expected to reach USD 42.34 billion in 2026.

Why are decentralized trials important for sponsors?

FDA guidance in 2024 validated remote visits and e-consent, lowering per-patient costs by 15-25% and improving retention.

Which therapeutic area delivers the fastest CRO growth to 2031?

Infectious diseases show the quickest pace at a projected 8.99% CAGR as governments fund pandemic readiness.

What region offers the highest future growth for CROs?

Asia-Pacific will post a 8.32% CAGR through 2031, driven by regulatory harmonization in China and India.

Page last updated on: