Clinical Trial Biorepository And Archiving Solutions Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

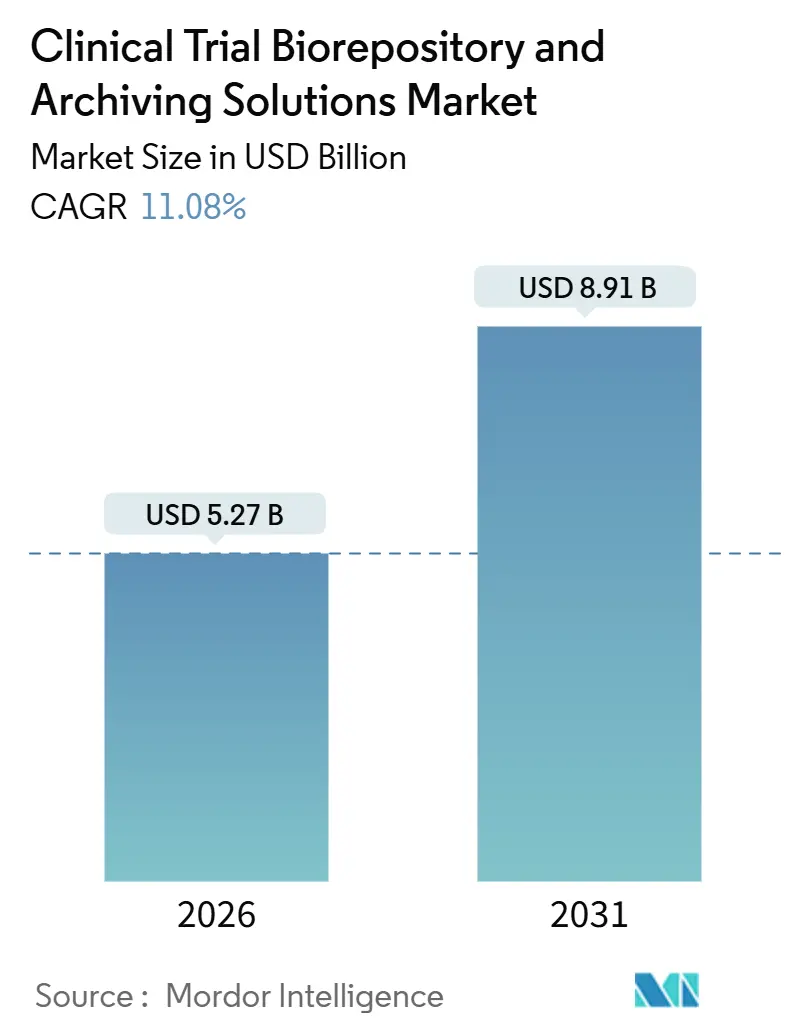

| Market Size (2026) | USD 5.27 Billion |

| Market Size (2031) | USD 8.91 Billion |

| Growth Rate (2026 - 2031) | 11.08% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Clinical Trial Biorepository And Archiving Solutions Market Analysis by Mordor Intelligence

The Clinical Trial Biorepository And Archiving Solutions Market size is estimated at USD 5.27 billion in 2026, and is expected to reach USD 8.91 billion by 2031, at a CAGR of 11.08% during the forecast period (2026-2031).

Rising precision-medicine trial volumes, wider adoption of decentralized and hybrid study models, and growing outsourcing of sample management functions are reshaping how sponsors safeguard biospecimens and related data. Cell and gene therapy pipelines alone generated 91 Regenerative Medicine Advanced Therapy (RMAT) designation requests in fiscal 2025, up 54% from fiscal 2024, thereby amplifying long-term demand for cryogenic storage. Regulatory acceptance of remote specimen procurement, codified by the U.S. FDA in May 2023 and the EMA in December 2022, increases the number of custody handoffs and raises the value of digital chain-of-custody platforms. Meanwhile, energy-efficient ultra-low-temperature (ULT) freezers using hydrocarbon refrigerants are mitigating rising utility costs that can exceed USD 500 per unit annually in mature markets. Competition now pivots on the ability to bundle validated storage infrastructure with tamper-proof electronic archives that satisfy FDA 21 CFR Part 11 and EU GMP Annex 11 requirements.

Key Report Takeaways

- By service type, biorepository services led with a 38.31% market share in the clinical trial biorepository & archiving solutions market in 2025, while digital data management and e-archiving are expanding at a 12.15% CAGR through 2031.

- By phase, pre-clinical programs are advancing at a 12.95% CAGR, outpacing all other stages. In contrast, Phase III trials accounted for 34.71% of the clinical trial biorepository & archiving solutions market in 2025.

- By biospecimen type, blood and blood components accounted for 43.48% of revenue in 2025; cells and cell lines are projected to grow at a 14.13% CAGR through 2031.

- By end user, contract research organizations (CROs) are set to post the fastest growth rate, with a 15.33% CAGR, whereas pharmaceutical and biotech firms accounted for 48.26% of revenue in 2025.

- By geography, North America retained 48.53% revenue share in 2025; Asia-Pacific is forecast to register the quickest 13.93% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Clinical Trial Biorepository And Archiving Solutions Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Genomic-Driven Precision-Medicine Trials Surge | +2.5% | Global, with concentration in North America and EU | Medium term (2-4 years) |

| Rise of Decentralized & Hybrid Trial Models | +1.8% | North America, EU, APAC emerging markets | Short term (≤ 2 years) |

| Long-Term Preservation Demand from Cell & Gene Therapy | +1.9% | Global, particularly North America and EU | Long term (≥ 4 years) |

| CRO Outsourcing Trend Among Small/Mid-Size Biotechs | +1.6% | Global, particularly North America and APAC | Medium term (2-4 years) |

| Stringent GxP Compliance & Audit Readiness Focus | +1.3% | Global, acute in North America and EU | Medium term (2-4 years) |

| AI-Enabled Sample-Integrity Monitoring | +1.2% | North America, EU, with spillover to APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Genomic-Driven Precision-Medicine Trials Surge

Precision oncology and rare-disease programs now collect more biospecimen types per participant, inflating repository capacity requirements two-fold compared with traditional designs.[1]Nature Medicine, “Biospecimen Collection in Basket Trials,” nature.com Tissue-agnostic approvals issued by the FDA’s Oncology Center of Excellence climbed to 16 between 2017 and 2025, each mandating companion diagnostic validation material that must be preserved for retrospective analyses. ISO 20387:2018 certification has become a gating factor for vendors competing to handle these high-value samples, assuring sponsors of end-to-end traceability. Providers that integrate next-generation sequencing (NGS) data with physical storage are capturing premium contracts as sponsors seek unified genomic and clinical datasets for regulatory submissions.

Rise of Decentralized & Hybrid Trial Models

Formal guidance from top regulators now legitimizes home-based phlebotomy and local clinic specimen collection, accelerating patient enrollment yet complicating logistics.[2]U.S. Food and Drug Administration, “Regenerative Medicine Advanced Therapy Designation Requests 2025,” fda.gov A 2025 Clinical Trials Transformation Initiative survey recorded at-home blood draws in 42% of Phase II and III oncology studies, up from 18% in 2022. This shift drives demand for IoT-enabled cold-chain shippers that transmit real-time temperature and location data, allowing repositories to intervene before sample viability is jeopardized. Digital reconciliation tools that fuse data from home, clinic, and central labs are now regarded as mission-critical investments by large sponsors.

CRO Outsourcing Trend Among Small/Mid-Size Biotechs

Cost pressures are pushing biotechs with a market capitalization of under USD 500 million to shed non-core infrastructure. SEC filings show that 64% of such companies outsourced biorepository functions in 2024, up from 48% in 2021. CROs respond by building mega-facilities that combine freezer farms, clinical monitoring, and data management, delivering scale economies that sponsors cannot replicate. Outsourcing is especially attractive in cell and gene therapy, where a single patient may require up to 10 cryovials stored at −150 °C for autologous manufacturing.

AI-Enabled Sample-Integrity Monitoring

Predictive maintenance software launched in 2025 can flag ULT freezer failures up to 3 days before catastrophic failure, reducing unscheduled downtime. AI image analysis detects hemolysis and lipemia in frozen plasma with 94% sensitivity, reducing the need to sacrifice irreplaceable aliquots for quality testing. Regulators now accept validated AI audit logs as compliant evidence under 21 CFR Part 11, accelerating adoption among repositories that manage millions of vials.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost of 24/7 Ultra-Low-Temperature Infrastructure | -1.5% | Global, acute in emerging markets and price-sensitive regions | Short term (≤ 2 years) |

| Fragmented Global Regulatory Requirements | -0.9% | Multi-regional trials spanning North America, EU, APAC | Medium term (2-4 years) |

| Sample-Chain-of-Custody Litigation Risks | -0.7% | Global, particularly North America with high litigation exposure | Medium term (2-4 years) |

| Sustainability Pressures on Energy-Intensive Freezers | -0.6% | EU with F-Gas regulations, spreading to North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Cost of 24/7 Ultra-Low-Temperature Infrastructure

A −80 °C mechanical freezer consumes nearly 20 kWh per day, equating to USD 300–500 in U.S. industrial electricity charges each year, with costs doubling in regions that depend on diesel generators. Liquid-nitrogen vapor systems incur annual nitrogen costs of USD 1,200–2,000 per tank. The total cost of ownership for a 500,000-vial repository over 10 years ranges from USD 2.8 million to USD 4.1 million, a threshold that excludes many academic institutions from participating in the market.[3]International Society for Biological and Environmental Repositories, “Total Cost of Ownership Study 2024,” isber.org New European F-Gas rules require refrigerant retrofits that raise upfront capex even as they lower lifetime operating expenses.

Fragmented Global Regulatory Requirements

Retention timelines vary widely, from two years post-approval under FDA rules to 15 years for pediatric samples in the EU and five years in China, forcing repositories to duplicate inventories and workflows. Divergent electronic record standards push vendors to validate parallel systems, thereby amplifying compliance costs. A 2025 lawsuit linked to freezer failure and biomarker endpoint invalidation settled for USD 18 million, highlighting litigation risks tied to multi-jurisdictional trials.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Digital Platforms Capture Margin as Physical Storage Commoditizes

Biorepository services accounted for 38.31% of the clinical trial biorepository & archiving solutions market revenue in 2025, cemented by demand for validated ULT infrastructure during pivotal studies. Yet aggressive pricing from Asia-Pacific entrants is compressing margins, nudging incumbents toward higher-value digital offerings. Digital data management and e-archiving are set to deliver a 12.15% CAGR, lifted by mandates under FDA 21 CFR Part 11 and EU GMP Annex 11 that prohibit paper-based logs. Digital functions represented 8% of total repository budgets in 2024, doubling their share in three years.

Sample management and logistics businesses are prospering as decentralized trials increase shipment volumes, necessitating IoT containers with GPS and continuous temperature logging. Archiving services meet long retention windows, especially for pediatric programs, where EMA rules stipulate 15 years. Ancillary activities such as disaster recovery and re-aliquoting, though still niche, are growing because sponsors revisit archived material for post-hoc biomarker discovery. The service mix is bifurcating into low-margin bulk storage and premium digital solutions that can command double-digit operating margins.

By Phase: Pre-Clinical Biobanking Accelerates as Sponsors Front-Load Biomarker

Pre-clinical services will grow at a 12.95% CAGR through 2031, the strongest among phases, as companies validate biomarkers earlier to de-risk late-stage attrition. Drugs with supportive preclinical biomarkers posted 28% Phase III success rates, versus 12% without such data, in a 2024 Nature Biotechnology study. The phase generated surging sample volumes from toxicology and efficacy screens, shifting upstream the demand for repository space.

Phase III maintained 34.71% of the clinical trial biorepository & archiving solutions market size in 2025 on the back of large patient cohorts, but is moderating as adaptive designs compress timelines. Phase I remains niche because cohorts stay under 100 participants, yet autologous cell and gene therapies heighten per-patient sampling. Phase II balances enrollment scale with biomarker-based inclusion, sustaining steady repository spend. Post-marketing Phase IV work is expanding, underpinned by FDA guidance that requires five-year retention of real-world safety samples for updated labels.

By Biospecimen Type: Cell and Gene Therapy Pipelines Propel Cryogenic Demand

Blood and blood components delivered 43.48% of 2025 revenue, driven by routine pharmacokinetic and immune-monitoring assays. Cells and cell lines are on track for a 14.13% CAGR to 2031, powered by CAR-T autologous workflows that require −150 °C cryopreservation. The FDA logged 91 RMAT requests in fiscal 2025, reflecting an accelerating pipeline that leverages patient-specific cellular material.

Tissue biopsies remain critical for histopathology and spatial transcriptomics, yet invasive collection techniques limit growth relative to liquid biopsies. DNA, RNA, and genomic materials benefit from basket trials that now collect an average of 7 biospecimen types per patient, more than doubling the repository footprint. Saliva, urine, and cerebrospinal fluid address specialized research niches. ISO 20387:2018 is increasingly mandatory wherever genomic material is processed to assure provenance across multi-site studies.

By End User: CROs Gain Share as Biotechs Divest Infrastructure

Pharma and biotech companies accounted for 48.26% of revenue in 2025, reflecting their legacy in-house freezer farms for late-stage development and pharmacovigilance. CROs are forecast to capture the fastest 15.33% CAGR to 2031, propelled by small-cap biotech outsourcing to conserve capital.

Academic sites contribute steady though modest volumes, hampered by budgetary ceilings that limit access to advanced digital archives. Diagnostic labs and hospitals mainly bank residual clinical material under Institutional Review Board protocols. CROs increasingly package sample storage with clinical monitoring and statistics, achieving economies of scope that sponsors find compelling. Labcorp’s 2024 expansion to 2.5 million-vial capacity in Indianapolis illustrates the capacity race among service providers.

Geography Analysis

North America accounted for 48.53% of 2025 revenue due to a high concentration of trial sponsors, established Good Clinical Practice oversight, and proximity to the FDA, which simplifies audit workflows. Mature reimbursement and high acuity trials sustain volume, yet rising energy costs and stringent sustainability regulations are prompting capacity redistribution to lower-cost regions.

Asia-Pacific is projected to post a 13.93% CAGR through 2031, the quickest across regions. China reduced the review time for new drug applications to 10 months in 2024, down from 18 months in 2020, attracting multinational pivotal studies that require GMP-compliant local storage. India cleared 412 trial applications in 2024, up 23% year on year, reinforcing the need for domestic repositories capable of managing the growing number of multicenter cohorts. Investments in Southeast Asia aim to curb the airfreight of high-value samples to North American facilities, thereby trimming logistics spending.

Europe remains stable with EMA central approvals, but divergent national retention rules induce compliance complexity. Germany’s BfArM imposes supplementary documentation beyond EMA minimums, extending archiving timelines and costs. Eastern European nations offer lower land and utility prices, luring capacity expansion aimed at sponsors priced out of Western European hubs.

The Middle East and Africa are registering rising interest in trials targeting rare diseases. South Africa authorized 18 Phase III protocols in 2024, yet cold-chain gaps limit large-scale repository growth. South America’s momentum stems from Brazil, where ANVISA approved 87 protocols in 2024, but logistics challenges outside core metros curb rapid capacity scale-up.

Competitive Landscape

The top five providers controlled about significant revenue in 2025, indicating moderate concentration. Thermo Fisher Scientific and Labcorp Drug Development secure multi-year contracts leveraging end-to-end portfolios that integrate collection kits, ambient-to-cryogenic storage, and Part 11-compliant electronic archives. Specialized cold-chain logistics firms such as Cryoport and BioLife Solutions compete on IoT shipping and sustainability credentials.

Patent filings reveal 18% of submissions since 2022 address AI-driven predictive maintenance, highlighting differentiation through reliability and sample-loss prevention. White-space opportunities persist in Southeast Asia and Latin America, where local CROs lack ISO-certified infrastructure. Azenta Life Sciences’ USD 87 million acquisition of a European sample-management firm in 2024 underscores consolidation aimed at geographic reach and cross-selling of digital platforms.

Smaller niche players focus on autologous cell therapy workflows, providing bespoke chain-of-custody procedures that large high-volume repositories cannot easily replicate. Barriers to entry remain high due to ISO 20387 certification timelines and the capital-intensive ULT infrastructure, which can take 2 years to validate under sponsor audit protocols.

Clinical Trial Biorepository And Archiving Solutions Industry Leaders

Charles River Laboratories International Inc.

Eurofins Scientific

ICON plc

Lonza Bioscience

Thermo Fisher Scientific Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: ECOG-ACRIN Cancer Research Group and Caris Life Sciences reported first data from an AI multimodal model that improves breast-cancer recurrence prediction using archival tissue from the TAILORx repository.

- December 2025: PreciseMDX partnered with Virchow Medical to launch a genomic ordering platform linked to the Virchow Vault liquid-specimen biorepository, streamlining clinician access to stored companion samples.

- October 2025: COMBINEDBrain and the Medical University of South Carolina opened a pediatric CNS tissue and biofluid biorepository to accelerate translational neuroscience.

- June 2024: Thermo Fisher Scientific inaugurated a GMP-certified ultra-cold site offering ambient-to-cryogenic storage, packaging, and Qualified Person release services.

Global Clinical Trial Biorepository And Archiving Solutions Market Report Scope

The Clinical Trial Biorepository & Archiving Solutions Market Report is Segmented by Service Type (Biorepository Services, Archiving Services, Sample Management & Logistics, Digital Data Management/e-Archiving, Other Service Types), Phase (Pre-clinical, Phase I, Phase II, Phase III, Phase IV/Post-marketing), Biospecimen Type (Tissue Samples, Blood & Blood Components, Cells & Cell Lines, DNA/RNA/Genomic Material, Other Fluids), End User (Pharmaceutical & Biotechnology Companies, Contract Research Organizations, Academic & Research Institutes, Others), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

| Biorepository Services |

| Archiving Services |

| Sample Management & Logistics |

| Digital Data Management / e-Archiving |

| Other Service Types (Ancillary, Disaster-Recovery Services) |

| Pre-clinical |

| Phase I |

| Phase II |

| Phase III |

| Phase IV / Post-marketing |

| Tissue Samples |

| Blood & Blood Components |

| Cells & Cell Lines |

| DNA / RNA / Genomic Material |

| Other Fluids (Saliva, Urine, etc.) |

| Pharmaceutical & Biotechnology Companies |

| Contract Research Organizations |

| Academic & Research Institutes |

| Others (Diagnostic Laboratory, Hospitals) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Service Type | Biorepository Services | |

| Archiving Services | ||

| Sample Management & Logistics | ||

| Digital Data Management / e-Archiving | ||

| Other Service Types (Ancillary, Disaster-Recovery Services) | ||

| By Phase | Pre-clinical | |

| Phase I | ||

| Phase II | ||

| Phase III | ||

| Phase IV / Post-marketing | ||

| By Biospecimen Type | Tissue Samples | |

| Blood & Blood Components | ||

| Cells & Cell Lines | ||

| DNA / RNA / Genomic Material | ||

| Other Fluids (Saliva, Urine, etc.) | ||

| By End User | Pharmaceutical & Biotechnology Companies | |

| Contract Research Organizations | ||

| Academic & Research Institutes | ||

| Others (Diagnostic Laboratory, Hospitals) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What growth rate is expected for clinical trial biorepository services through 2031?

The segment comprising classic biorepository services is projected to grow at a 11.08% CAGR to USD 8.91 billion by 2031, mirroring the overall market trajectory.

Which biospecimen category is set to expand the fastest?

Cells and cell lines are forecast to post a 14.13% CAGR, fueled by cell and gene therapy pipelines that demand −150 °C cryogenic preservation.

Why are CROs gaining share in this space?

Capital-constrained biotechs increasingly outsource sample management to CROs, which operate large-scale freezer farms and provide bundled monitoring and data-management services, delivering a 15.33% CAGR for the CRO end-user segment.

How are decentralized trials influencing repository operations?

Regulatory acceptance of at-home specimen collection multiplies custody handoffs, raising demand for IoT-enabled cold-chain shippers and digital chain-of-custody platforms.

Which region offers the highest growth potential?

Asia-Pacific, buoyed by streamlined Chinese and Indian regulatory timelines, is poised for a 13.93% CAGR, the highest among all regions.

Page last updated on: