Clinical Intelligence Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 10.67 Billion |

| Market Size (2031) | USD 19.02 Billion |

| Growth Rate (2026 - 2031) | 12.25% CAGR |

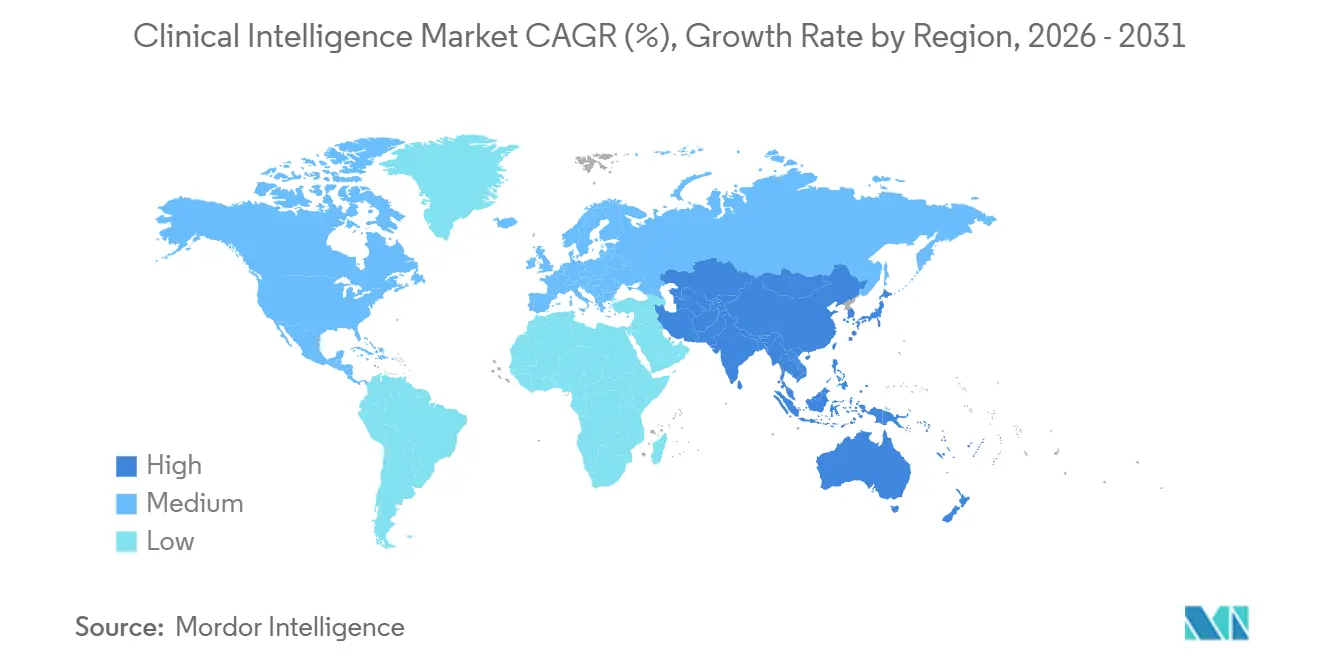

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

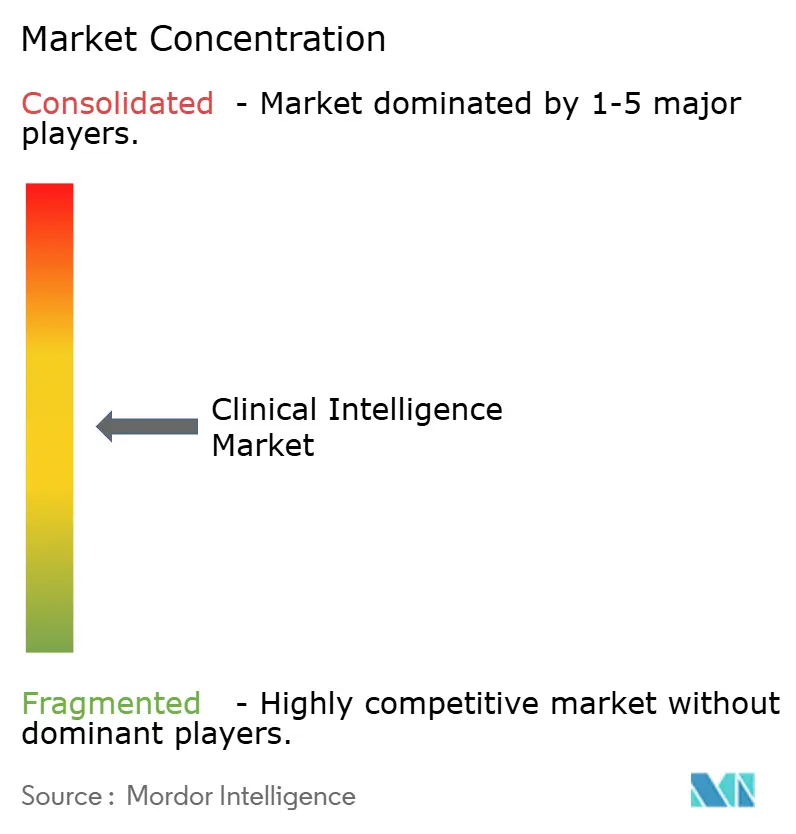

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Clinical Intelligence Market Analysis by Mordor Intelligence

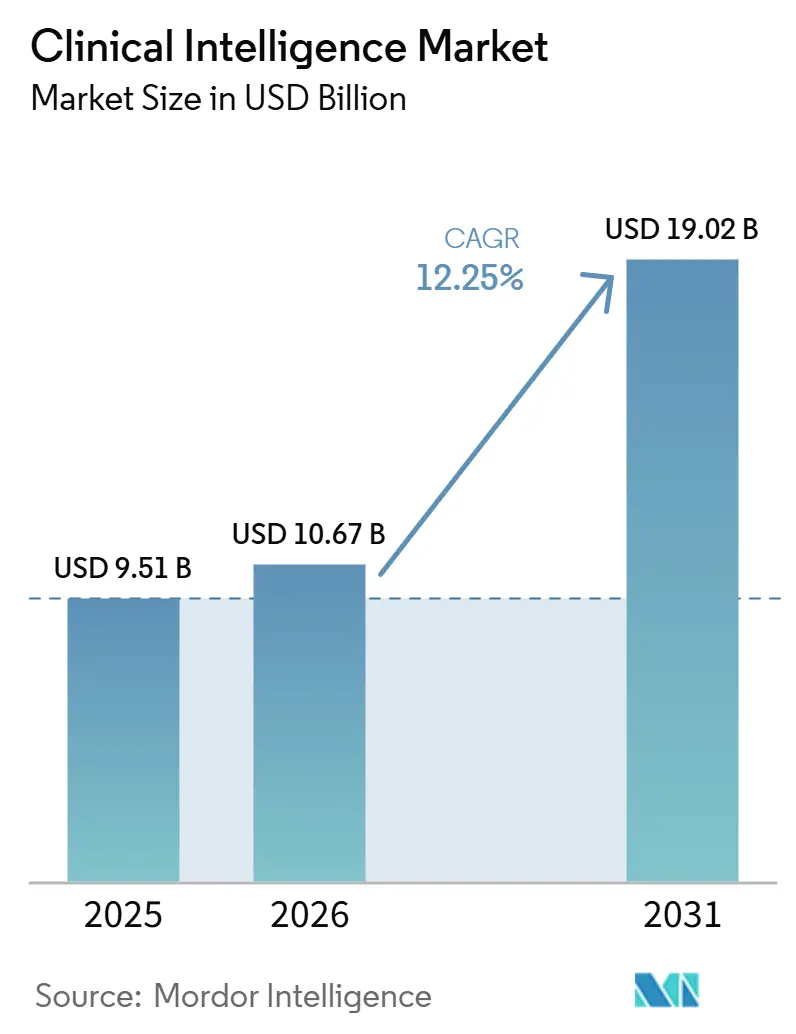

The Clinical Intelligence Market size is projected to expand from USD 9.51 billion in 2025 and USD 10.67 billion in 2026 to USD 19.02 billion by 2031, registering a CAGR of 12.25% between 2026 to 2031.

The Clinical intelligence market is expanding because health systems now use clinical data as an operating tool tied to contract performance, quality targets, and episode-level cost control, instead of treating it only as a compliance record. The broadening mix of EHR data claims streams and social determinants data has lowered data ingestion barriers and widened the set of use cases across care variation management, pharmacogenomics-guided prescribing, trial matching, and real-time population risk stratification. The Clinical intelligence market also reflects a stronger link between value-based care contracting and AI-enabled workflow actioning, which is pulling demand toward platforms that can turn historical and live data into decisions during active care delivery. Software and cloud delivery still anchor the current revenue base, but the Clinical intelligence market is becoming more competitive as EHR vendors, analytics specialists, and cloud-linked platforms push for data proximity, modular pricing, and stronger workflow integration while interoperability gaps, AI validation demands, and slower provider buying cycles continue to limit near-term conversion.

Key Report Takeaways

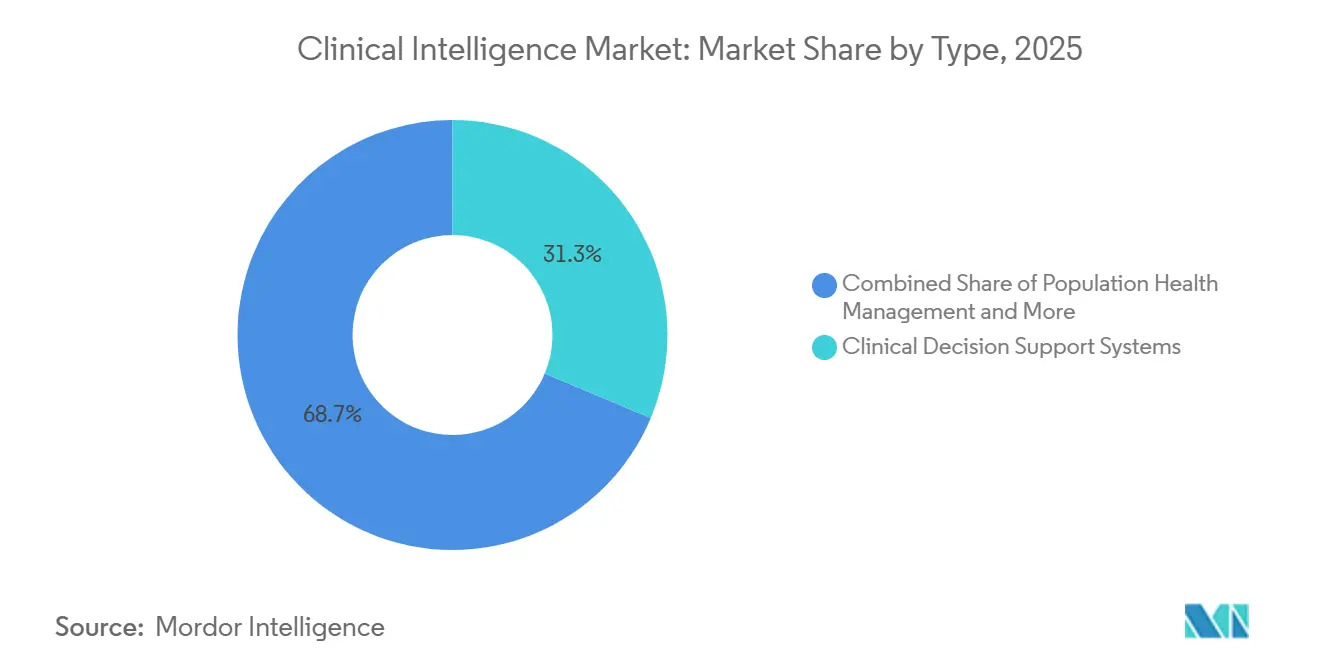

- By type, Clinical Decision Support Systems held 31.31% of revenue in 2025, while Retrospective Performance Management and Predictive Analytics is forecast to expand at a 15.38% CAGR through 2031.

- By component, Software accounted for 56.24% of revenue in 2025, while Services is projected to record the highest CAGR at 16.52% through 2031.

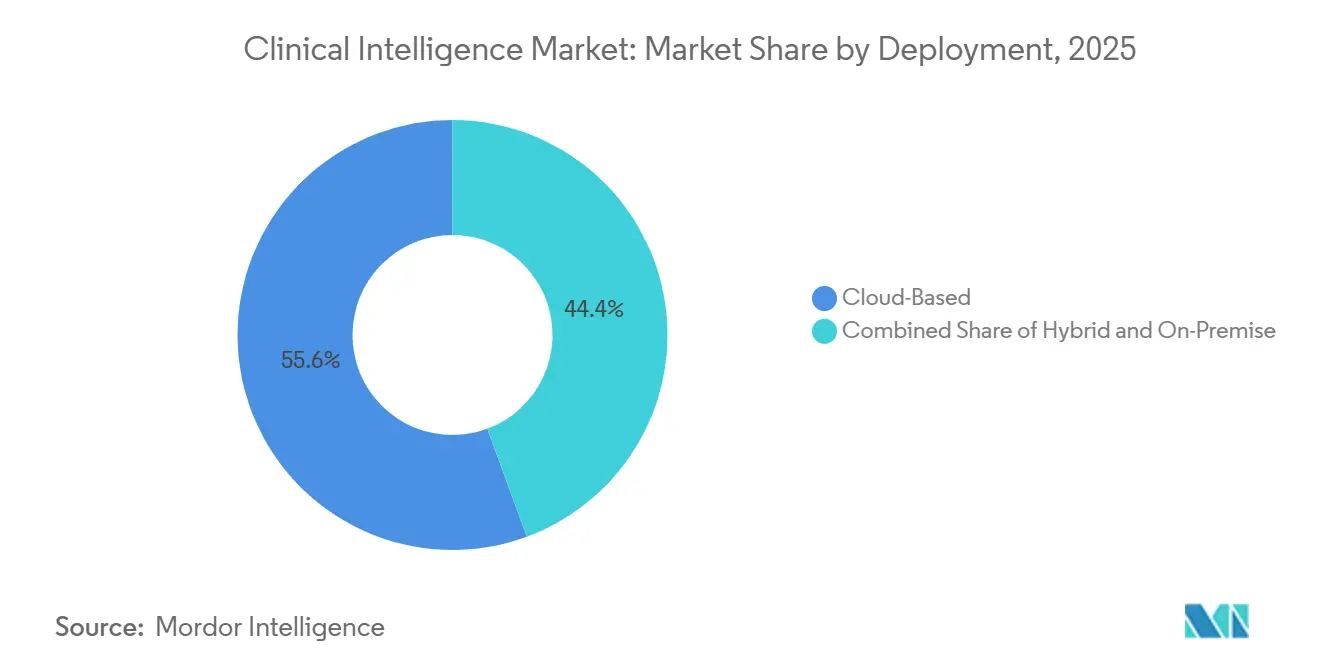

- By deployment, Cloud-based delivery held 55.64% of revenue in 2025, while Hybrid deployment is expected to grow fastest at a 16.62% CAGR through 2031.

- By end user, Hospitals captured 48.26% of revenue in 2025, while Healthcare Providers are forecast to expand at a 15.95% CAGR through 2031.

- By geography, North America accounted for 43.61% share of the market size in 2025, while Asia-Pacific is projected to expand at an 16.15% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Clinical Intelligence Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation Of EHR, Claims, And Clinical Data Lakes | +2.8% | Global, concentrated in North America and Europe | Medium term (2-4 years) |

| Shift From Retrospective Reporting To Real-Time Clinical Actioning | +2.5% | North America, Western Europe, APAC core | Medium term (2-4 years) |

| AI Copilot Adoption In Clinical Workflow Orchestration | +2.2% | North America, APAC emerging | Short term (≤ 2 years) |

| Value-Based Care Contracting Requires Measurable Care Variation Reduction | +1.8% | North America and Europe, spillover to APAC | Medium term (2-4 years) |

| Pharmacogenomics And Precision Medicine Content Expansion | +1.2% | North America, Middle East, APAC emerging | Long term (≥ 4 years) |

| Cross-Enterprise Data Fusion For Trial Matching And Evidence Generation | +1.0% | North America, EU research network, global trial sites | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Proliferation of EHR, Claims, and Clinical Data Lakes

The Clinical intelligence market is gaining structural support from a larger and more distributed clinical data base that now stretches across EHR systems, claims environments, and social determinants inputs. EHR adoption reached 83% across EU member states in 2024, which points to a much denser pool of longitudinal patient data for analytics and model development at institutional scale[1]European Commission / Euronews, “E-santé en Europe, Accès Aux Dossiers Médicaux Et Maîtrise Du Numérique, Qui En Tête,” Euronews, euronews.com. The more important change is that health systems are building federated analytics layers that let them train models and run inference without moving raw records across institutional boundaries. That change reduces the tradeoff between speed and privacy, because organizations can shorten the path from data generation to clinical action while staying within HIPAA and GDPR guardrails. The Clinical intelligence market therefore favors vendors that can govern distributed data fabrics across multiple sources, because those platforms are better positioned than single-instance ingestion tools to support larger contracts and broader use cases.

Shift From Retrospective Reporting To Real-Time Clinical Actioning

The Clinical intelligence market is moving away from retrospective reporting tools built for administrative review and toward real-time systems that can influence decisions during the clinical encounter itself. CMS reported that the BPCI Advanced program reduced per-episode payments by USD 1,014 relative to baseline, with surgical episodes showing reductions of USD 1,694 per episode, which gives providers a measurable reason to adopt tools that act before variation turns into cost leakage[2]Centers for Medicare & Medicaid Services, “BPCI Advanced Evaluation, Sixth Annual Report,” CMS Innovation Center, cms.gov. This is also changing who buys these platforms, because procurement is shifting from quality teams toward finance leaders and value-based contract teams that want visible savings during active performance windows. That raises the evidence threshold for the Clinical intelligence market, since broad dashboards without encounter-level resolution are less useful in contracts where timing matters. The result is a stronger preference for platforms that connect historical care patterns to immediate workflow guidance, especially in systems exposed to bundled payment and accountable care pressures.

AI Copilot Adoption In Clinical Workflow Orchestration

The Clinical intelligence market is also being pushed forward by ambient AI documentation and agent-based workflow tools that place guidance inside the clinician workflow instead of outside it. Microsoft made Healthcare Agent Service in Copilot Studio generally available in 2025, with grounded generative AI answers tied to trusted clinical sources and patient history inside EHR-linked workflows. Epic launched Curiosity in September 2025 and trained it on more than 100 billion patient medical events across Cosmos, with capabilities that include estimating disease risk, length of stay, and treatment outcomes, while virtual lab access opened to researchers from February 2026. These moves shorten the feedback loop between evidence generation and bedside use, which is important for the Clinical intelligence market because clinicians can accept or override recommendations during the same encounter. Vendors that still rely on detached analytics environments face growing displacement risk, even when their underlying models are technically strong, because workflow fit now matters as much as analytic depth.

Value-Based Care Contracting Requires Measurable Care Variation Reduction

The Clinical intelligence market is becoming harder to treat as discretionary software because value-based contracts now place measurable care variation and financial performance inside the same operating frame. Various sources pointed to claims-based evidence showing specialty cohorts with reductions of up to USD 20,000 per episode and chronic disease populations with USD 1,900 lower per-member per-month costs relative to benchmarks, which explains why enterprise buyers are willing to fund platforms tied to performance improvement. It also cited CitiusTech analysis across more than 6,600 patients, where 3% of cases were true clinical outliers associated with 700% higher costs than inlier populations, showing how a small set of cases can drive a large share of waste. That cost concentration supports the Clinical intelligence market because the economic case becomes clearer when platforms can identify the small cohort where intervention has the highest payoff. It is also widening demand beyond large hospital systems, since specialist groups entering capitated and downside-risk arrangements now need the same visibility into variation, utilization, and intervention timing.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Interoperability Friction Across Multi-Vendor Clinical Stacks | -1.5% | Global, most severe in fragmented provider markets | Medium term (2-4 years) |

| Validation Burden For AI-Enabled Clinical Recommendations | -1.0% | North America, Europe | Long term (≥ 4 years) |

| Workflow Alert Fatigue And Low Physician Trust In Black-Box Scores | -0.8% | Global | Short term (≤ 2 years) |

| Budget Compression And Long Sales Cycles In Provider Organizations | -0.7% | North America and Europe, emerging in APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Interoperability Friction Across Multi-Vendor Clinical Stacks

The Clinical intelligence market still faces a major execution barrier because semantic misalignment across EHR, claims, imaging, and other clinical data systems makes deployment slower and more expensive than many vendors suggest. A 2025 systematic review in Frontiers in Health Services found that uneven adoption of HL7 FHIR, SNOMED CT, and LOINC, along with API standardization gaps, continues to create workflow inefficiencies and decision delays. Multi-EHR integration burden across Epic, Oracle Health, and athenahealth, where each added source expands the number of data-handling branches and increases implementation effort. Governance efforts such as TEFCA in the United States and the European Health Data Space in Europe improve trust and access rules. Still, they do not fully resolve the semantic differences inside vendor-specific FHIR implementations. This means the Clinical intelligence market remains easier for large providers with internal engineering depth. At the same time, mid-sized systems face a longer time to value and a lower realized return on platform investment.

Validation Burden For AI-Enabled Clinical Recommendations

The Clinical intelligence market also faces slower buying cycles because providers and vendors still operate in an uncertain validation and compliance environment for AI-enabled clinical support. The FDA revised its CDS guidance in January 2026, and the update clarified some device classification thresholds while still leaving AI-specific regulatory pathways materially undefined. A 2025 Journal of Medical Internet Research study found mean relative AI reliance of only 10.04% among physicians even when AI support improved accuracy, which shows that trust problems are not solved by better model performance alone. As a result, vendors in the Clinical intelligence market must spend more time on validation programs, interface redesign, and governance controls before deployments can scale inside clinical environments. This burden favors larger incumbents with regulatory, quality, and implementation resources, while smaller challengers carry higher execution risk and longer revenue conversion cycles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Retrospective Analytics Disrupts the CDSS-Led Status Quo

Clinical Decision Support Systems held 31.31% of the clinical intelligence market share in 2025, making this the largest type segment in the current revenue mix. That position reflects deep EHR workflow integration and payer-driven evidence-based prescribing requirements that make CDSS difficult for hospitals to avoid. In the Clinical intelligence market, embedded CDSS tools inside Epic and Oracle Health environments benefit from direct data proximity because recommendations can be generated from clinical events at the point of entry instead of after a data transfer lag. Population Health Management remains the second-largest type segment because risk-bearing organizations still need patient panel visibility, though fragmented cross-payer data flows continue to limit the full value of these tools in some markets. Quality Improvement and Performance Measurement Systems are also gaining ground where national quality registries and outcomes-based reimbursement frameworks require stronger reporting discipline, especially across European systems.

Retrospective Performance Management and Predictive Analytics is the fastest-growing type segment, with a 15.38% CAGR from 2026 to 2031, and that pace is well above the broader Clinical intelligence market. This growth reflects demand from providers that need to connect historical care variation with forward-looking cost and outcome forecasts inside active value-based contracts. A 2026 npj Digital Medicine study showing that automated pharmacogenomic recommendation systems can produce evidence-based outputs with speed and consistency that manual review processes cannot match. That matters for the Clinical intelligence industry because retrospective analytics tools are no longer confined to after-the-fact review and are increasingly being built to feed real-time decision support. The practical boundary between retrospective and encounter-level intelligence is therefore narrowing, which means buyers in the Clinical intelligence market are comparing these platforms more directly with CDSS tools than they did in earlier procurement cycles.

By Component: Services Emerge as the High-Value Delivery Layer

Software accounted for 56.24% of revenue in 2025, which kept it as the leading component across the Clinical intelligence market. Providers have continued to direct spending toward platforms that combine data ingestion, governance, analytics, and AI execution in one environment instead of stitching together disconnected tools. That revenue lead is reinforced by subscription licensing and bundling strategies that tie applications to core data infrastructure, which deepens workflow dependence over time. Hardware now represents a smaller portion of spending because more workloads are moving toward cloud environments, though high-performance computing still matters in selected genomics and imaging settings where local processing and data residency remain important. This structure shows that the Clinical intelligence market still monetizes primarily through platforms, even as implementation depth becomes a bigger part of customer value.

Services is the fastest-growing component, with a 16.52% CAGR from 2026 to 2031, because many organizations can buy software but still lack the operating readiness needed to extract value from it. A wide gap in data science capability, workflow redesign capacity, and managed analytics support across the provider landscape. It also referenced UnitedHealth Group's USD 1.5 billion AI investment commitment for 2026 as a sign that large integrated players can internalize capabilities that smaller systems still need to source from external partners. In the Clinical intelligence industry, services work tied to pharmacogenomics integration, multi-source data governance, and workflow embedding carries greater strategic value than legacy reporting setup. That is why the Clinical intelligence market is seeing a stronger services layer emerge around implementation, optimization, and change management rather than around simple technical deployment alone.

By Deployment: Hybrid Architectures Outpace Pure-Cloud Deployments

Cloud-based deployment held 55.64% of revenue in 2025, which made it the dominant delivery model in the Clinical intelligence market. Health systems have increasingly accepted HIPAA-compliant, regionally hosted cloud environments because they remove on-premise upgrade cycles and lower internal IT overhead. The strongest concentration of cloud adoption remains in North America and Western Europe, where large vendor ecosystems across Microsoft Azure Health, AWS HealthLake, and Google Vertex AI Healthcare have already matured. On-premise deployments still persist in settings with strict data residency constraints or public network rules. This means the Clinical intelligence market is not moving toward a uniform cloud model, even if cloud remains the largest revenue base today.

Hybrid deployment is the fastest-growing category, with a 16.62% CAGR from 2026 to 2031, because many buyers now want sensitive patient data to remain on local or sovereign infrastructure while still using cloud-linked AI tools for de-identified workloads. France's National Strategy for AI and Health Data, published in July 2025, explicitly supported sovereign AI hosting and no data transfer outside EU borders, which creates a procurement bias toward hybrid setups. The European Health Data Space entered into force in March 2025 and strengthened cross-border interoperability requirements while preserving national data-residency standards[3]French Ministry of Health / Health Data Hub, “Publication de la Stratégie Nationale sur l’Intelligence Artificielle et les Données de Santé,” Health Data Hub, health-data-hub.fr. In the Clinical intelligence market, this combination of jurisdictional control and analytic flexibility is becoming a practical answer for European providers that need certainty across both storage and AI inference layers. The segment is therefore growing faster than pure cloud, even though cloud still holds the larger installed base.

By End User: Healthcare Providers Scale Faster as Risk Contracts Expand

Hospitals captured 48.26% of revenue in 2025, which kept them as the largest end-user group in the Clinical intelligence market. Their lead comes from higher purchasing power, heavier exposure to quality-reporting mandates, and the presence of complex multi-morbidity populations that create stronger returns on analytics investment. Hospitals also use these platforms across multiple functions, including care variation management, length-of-stay prediction, sepsis alerts, and surgical documentation automation, which lifts average contract values and deepens vendor entrenchment. Pharmacies remain a smaller but rising user group, especially as pharmacogenomics content expands and clinical intelligence tools move closer to medication decisions and dispensing workflows. Foundation Medicine's May 2026 launch of FoundationOne PGx with Fulgent Genetics, covering actionable genes such as CYP2C19, CYP2D6, DPYD, and UGT1A1 for oncology prescribing, shows how precision medicine is widening the edge of demand around medication-related intelligence.

Healthcare Providers are the fastest-growing end-user category, with a 15.95% CAGR from 2026 to 2031, which shows that growth in the Clinical intelligence market is now spreading beyond enterprise hospital systems. This shift to Medicare Advantage and commercial value-based programs that move downside risk into physician groups and other provider organizations that previously had less need for advanced analytics. It also cited Wellsheet's July 2025 launch of a multidisciplinary AI Copilot that cut charting time by 50%, which illustrates how product entry points are moving toward encounter-level workflow automation for non-hospital settings. This broadens the number of target accounts in the Clinical intelligence market, even if revenue per account may be lower than in large hospital contracts. The end-user mix is therefore shifting toward a higher-volume model in which more provider organizations adopt modular capabilities tied directly to daily care delivery and contract performance.

Geography Analysis

North America held 43.61% of the clinical intelligence market share in 2025, which made it the largest regional contributor to revenue. The region benefits from dense value-based care infrastructure, a mature EHR base, and concentrated technology investment by integrated health systems. The United States remains the largest country market because CMS payment models place direct financial consequences on unmanaged care variation and create clear demand for real-time clinical support at the encounter level. Oracle said in March 2026 that its Oracle Health Clinical AI Agent had generated savings of more than 200,000 physician hours across U.S. deployments, and AtlantiCare reported a 41% reduction in documentation time, which gives buyers a tangible workflow benchmark when they assess the Clinical intelligence market. Canada and Mexico add incremental demand, with Canadian provincial systems using predictive analytics to manage elective backlog and long-term care pressure tied to aging demographics.

Europe is the second-largest regional block in the Clinical intelligence market, and Germany and the United Kingdom stand out as the most important growth poles within the region. Germany's GEMEINSAM DIGITAL 2026 strategy, published in February 2026, targets AI-supported clinical documentation in more than 70% of health and care facilities by 2028 and aims to raise active electronic patient record users from 4 million to 20 million by 2030. France's July 2025 national strategy on AI and health data identified automated clinical documentation as the highest-priority near-term AI use case and linked it to sovereign data hosting and European Health Data Space preparation. The United Kingdom is accelerating replacement of legacy analytics systems through NHS interoperability demands, while Italy and Spain remain mid-tier markets where public digitization programs are creating early demand for population health management and benchmarking tools.

Asia-Pacific is the fastest-growing regional segment in the Clinical intelligence market, with a 16.15% CAGR from 2026 to 2031. Government-led health digitization across China, India, South Korea, Australia, and Japan is building a stronger base for analytics adoption and workflow automation. India's National Digital Health Mission is expanding the addressable environment for population health tools by standardizing health identifiers and strengthening the data foundation for AI-linked community health interventions. South Korea's connected hospital investment and Japan's aging population are supporting demand for predictive tools in chronic disease management and elder care. In the Middle East and Africa, the Gulf states lead adoption, and Oracle, Cleveland Clinic, and G42 announced a strategic partnership in May 2025 to launch an AI-based global healthcare delivery platform centered in the UAE, which shows that the Clinical intelligence market is also being treated as a sovereign capability in the region. South America remains a smaller but growing contributor, with Brazil and Argentina moving from EHR buildout toward analytics-led care management through hospital systems and expanding private health plan networks.

Competitive Landscape

The Clinical intelligence market is moderately concentrated, with large integrated vendors such as Epic Systems, Oracle Health, IQVIA Holdings, and Optum competing alongside specialists including Health Catalyst, Veradigm, and InterSystems for enterprise provider contracts. A major source of advantage comes from data proximity, because vendors that operate inside the EHR workflow can accumulate richer training data and feed recommendations back into care delivery with less friction. This dynamic is reinforcing consolidation in the Clinical intelligence market, since embedded intelligence tools can extend existing core system contracts into adjacent analytics categories. Epic's Curiosity, launched in September 2025, illustrates this approach through a medical intelligence layer built on the Cosmos data environment and trained on more than 100 billion patient medical events. Oracle is following a similar path, and its March 2026 update on Clinical AI Agent showed that workflow automation and documentation savings are being used as competitive proof points in live provider environments.

Second-tier vendors in the Clinical intelligence market are responding by focusing on interoperability middleware, specialty data assets, and services-heavy deployment models that reduce the integration burden on providers. CitiusTech and InterSystems as examples of companies gaining ground where buyers operate in heterogeneous EHR environments and need smoother cross-system data handling. IQVIA's March 2026 unveiling of IQVIA.ai also shows how the field is moving toward orchestrated AI agents that can connect clinical, commercial, and real-world data domains inside a unified workflow. Its December 2025 collaboration with AWS further indicates that infrastructure alignment is becoming part of the competitive model rather than a back-end technical choice.

White-space opportunity in the Clinical intelligence market is emerging around health equity analytics, and the current platforms still provide limited race- and income-stratified reporting despite growing regulatory attention. The target account base is also moving downward toward healthcare provider organizations, because cloud-linked delivery and modular product design make smaller risk-bearing groups more commercially viable. This is widening the field of potential deployments, even as it changes pricing and packaging away from large one-time enterprise motions. Regulatory alignment with FDA CDS guidance and the EU AI Act is also shifting from a selling point into a basic qualification requirement, which raises the barrier to entry for smaller challengers. Taken together, these patterns suggest that the Clinical intelligence market will remain competitive, but advantage will increasingly depend on workflow embedding, implementation depth, and regulatory readiness rather than on analytics claims alone.

Clinical Intelligence Industry Leaders

Oracle Corporation

IQVIA Holdings Inc.

Epic Systems Corporation

UnitedHealth Group Incorporated

GE HealthCare Technologies Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Oracle Health partners with Theator to integrate AI-powered surgical video analytics and automated documentation into Oracle's EHR platform, deploying over Oracle Cloud Infrastructure and writing surgical procedure data directly into the EHR with zero manual dictation, extending clinical AI documentation coverage into operating rooms across U.S. hospital networks for the first time within the Oracle ecosystem.

- March 2026: IQVIA unveils IQVIA.ai at NVIDIA GTC, a unified agentic AI platform designed to coordinate AI agents across clinical, commercial, and real-world data domains without human handoffs, with initial release covering high-value use cases across clinical trials, medical affairs, and commercial analytics.

Global Clinical Intelligence Market Report Scope

As per the scope of the report, clinical intelligence is the application of data analytics, artificial intelligence, and machine learning techniques to healthcare data to enhance clinical decision-making, improve patient outcomes, optimize operational efficiency, and support healthcare providers in delivering personalized and evidence-based care. It involves transforming raw clinical data into actionable insights to inform diagnosis, treatment, and health management strategies.

The clinical intelligence market is segmented by type into clinical decision support systems, population health management, retrospective performance management and predictive analytics, clinical benchmarking, and quality improvement and performance measurement systems. By component, the market is segmented into software, services, and hardware. By deployment, the market is segmented into cloud-based, on-premise, and hybrid. By end user, the market is segmented into hospitals, healthcare providers, pharmacies, and other end users. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Clinical Decision Support Systems |

| Population Health Management |

| Retrospective Performance Management and Predictive Analytics |

| Clinical Benchmarking |

| Quality Improvement and Performance Measurement Systems |

| Software |

| Services |

| Hardware |

| Cloud-Based |

| On-Premise |

| Hybrid |

| Hospitals |

| Healthcare Providers |

| Pharmacies |

| Other End Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Type | Clinical Decision Support Systems | |

| Population Health Management | ||

| Retrospective Performance Management and Predictive Analytics | ||

| Clinical Benchmarking | ||

| Quality Improvement and Performance Measurement Systems | ||

| By Component | Software | |

| Services | ||

| Hardware | ||

| By Deployment | Cloud-Based | |

| On-Premise | ||

| Hybrid | ||

| By End User | Hospitals | |

| Healthcare Providers | ||

| Pharmacies | ||

| Other End Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current and forecast value of clinical intelligence?

The Clinical intelligence market size was USD 9.51 billion in 2025, stands at USD 10.67 billion in 2026, and is projected to reach USD 19.02 billion by 2031 at a 12.25% CAGR.

Which type segment leads revenue today?

Clinical Decision Support Systems led the type mix with 31.31% share in 2025 because of deep EHR workflow integration and payer-linked prescribing requirements.

Which part of the market is growing fastest by deployment model?

Hybrid deployment is the fastest-growing deployment segment, with a 16.62% CAGR from 2026 to 2031, as providers balance sovereign data control with cloud-linked AI use.

Why are healthcare providers becoming a faster-growing end-user group?

Healthcare Providers are projected to grow at a 15.95% CAGR because downside-risk contracts are pushing advanced clinical intelligence tools into physician groups and ambulatory settings.

Which region leads revenue and which region grows fastest?

North America led with 43.61% of global revenue in 2025, while Asia-Pacific is expected to record the fastest regional CAGR at 16.15% through 2031.

What is holding back adoption in this space?

The main barriers are interoperability friction across multi-vendor clinical stacks, AI validation uncertainty, physician trust issues, and longer provider budget and buying cycles.

Page last updated on: