Cleanroom Gloves Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

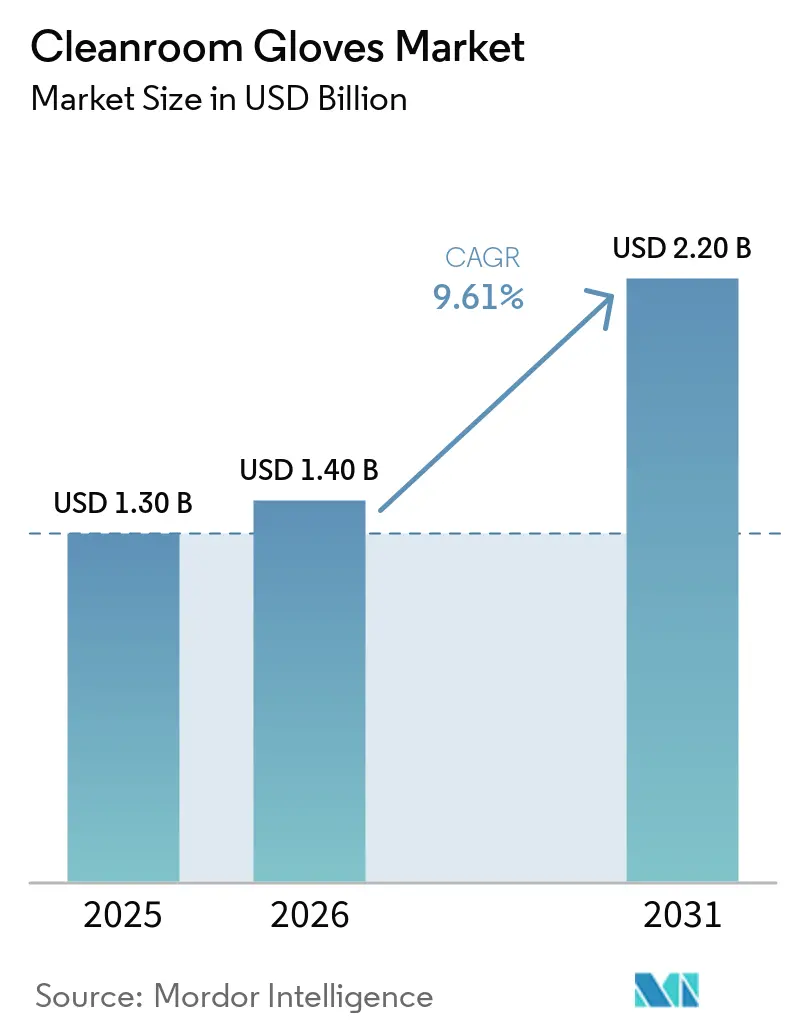

| Market Size (2026) | USD 1.40 Billion |

| Market Size (2031) | USD 2.20 Billion |

| Growth Rate (2026 - 2031) | 9.61% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cleanroom Gloves Market Analysis by Mordor Intelligence

The Cleanroom Gloves Market size was valued at USD 1.30 billion in 2025 and is estimated to grow from USD 1.40 billion in 2026 to reach USD 2.20 billion by 2031, at a CAGR of 9.61% during the forecast period (2026-2031).

Semiconductor fab expansions, tighter pharmaceutical regulations, and the shift from latex to nitrile formulations are converging to raise glove consumption across contamination-sensitive verticals. Nitrile’s puncture resistance, hypoallergenic profile, and electrostatic-dissipative performance underpin its rapid adoption in advanced-node chipmaking, EV-battery dry rooms, and aerospace assembly. The U.S. CHIPS and Science Act, India’s Semiconductor Mission, and Europe’s Chips Act collectively add hundreds of billions of dollars in wafer-fab incentives, magnifying operator-hour demand for ISO Class 1–5 environments [1]U.S. Congress, “H.R.4346 – CHIPS and Science Act,” congress.gov. On the life-science side, EU GMP Annex 1 and USP 797 rewrites mandate more frequent fingertip sampling and sterile-glove integrity tests, lifting per-batch glove requirements by as much as 30%. Moderate supplier concentration, feedstock cost swings, and early adoption of gloveless isolators temper the sector’s upside yet still leave headroom for premium niches such as PFAS-free and ultra-low-ion offerings.

Key Report Takeaways

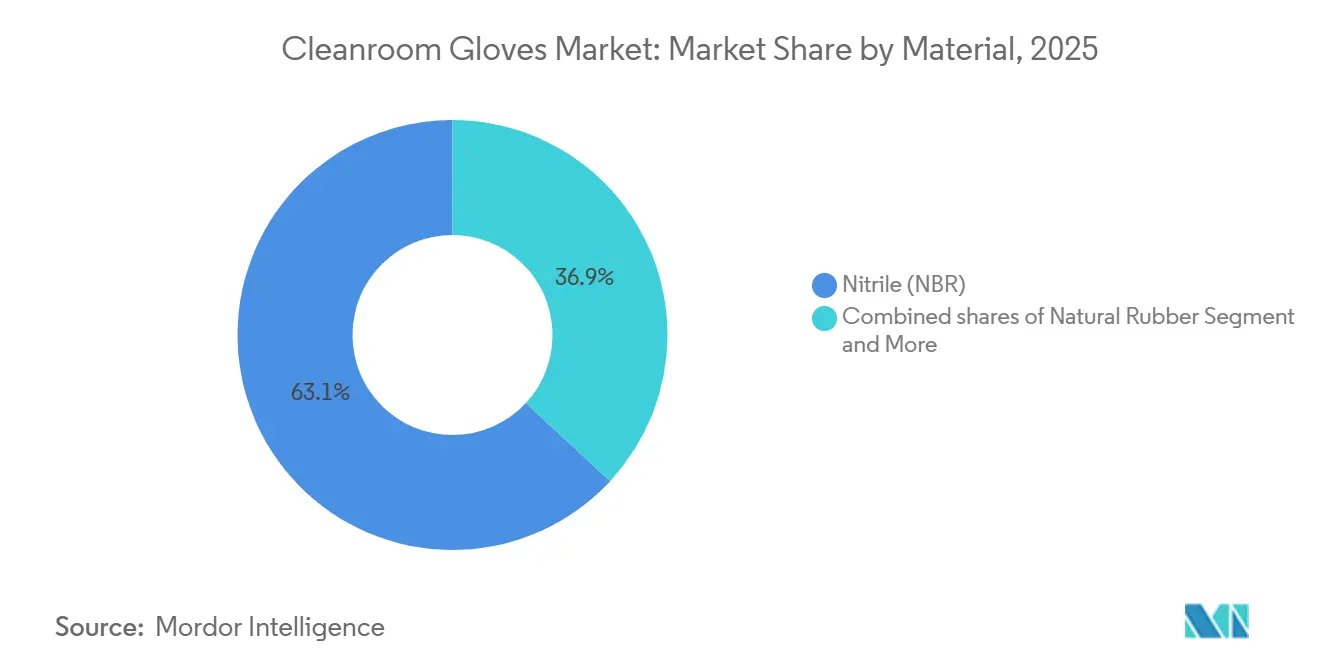

- By material, nitrile led the cleanroom gloves market with 63.10% market share in 2025 and is tracking a 9.95% CAGR to 2031.

- By end-use, biotechnology is projected to post a 10.18% CAGR through 2031, whereas pharmaceuticals held 35.87% market share in 2025.

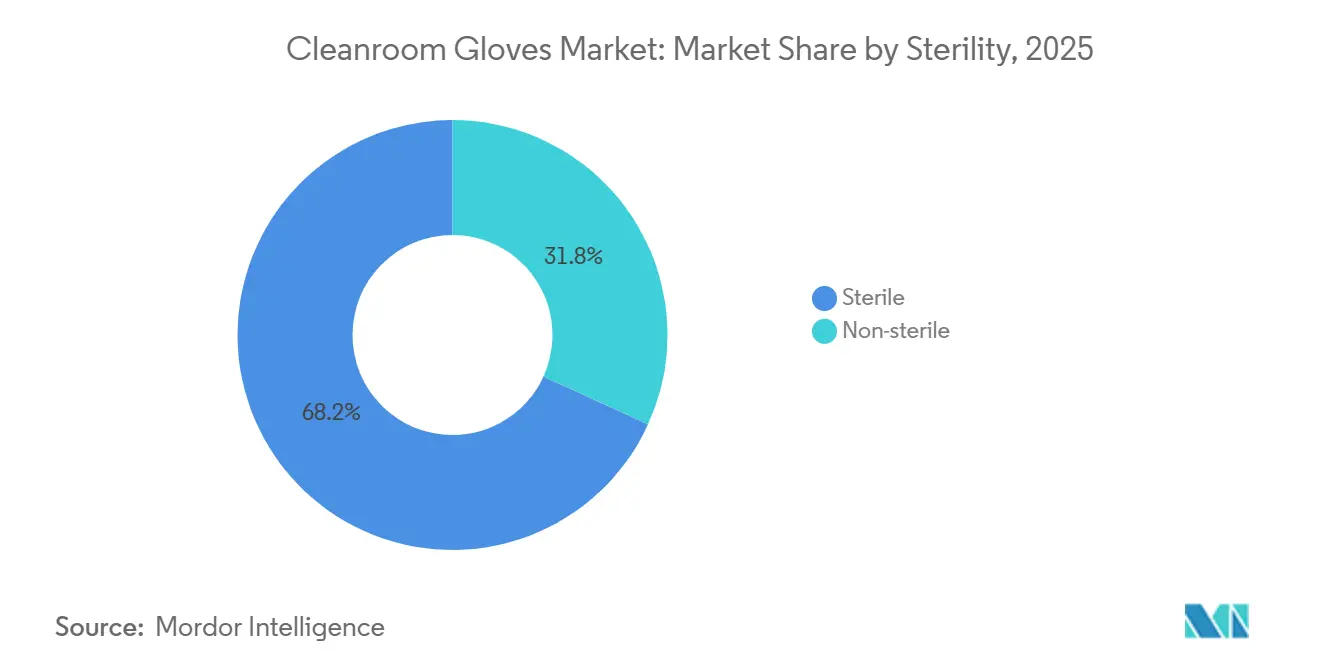

- By sterility, sterile variants commanded 68.19% of market share in 2025 and will advance at a 9.80% CAGR through 2031.

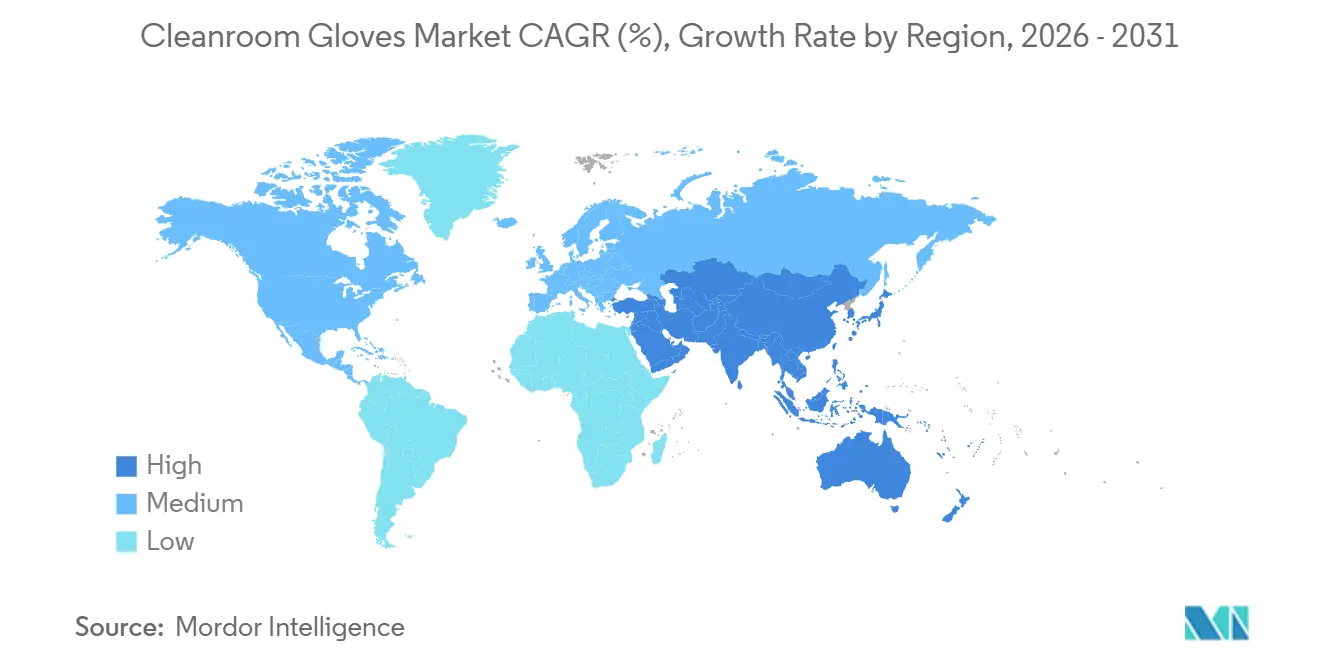

- By geography, North America held 38.19% market share in 2025, and the Asia-Pacific is set to deliver the fastest regional CAGR of 10.15% between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Cleanroom Gloves Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Semiconductor fab expansions and contamination control intensity | +2.0% | Global, led by North America, Asia-Pacific | Long term (≥ 4 years) |

| Biopharma aseptic manufacturing tightening (Annex 1/USP 797) | +1.8% | North America & Europe, spillover to Asia-Pacific | Medium term (2-4 years) |

| Shift from latex to nitrile in cleanrooms (allergy, ESD, extractables) | +1.5% | Global | Short term (≤ 2 years) |

| Growth in cleanroom-intensive medical device manufacturing | +1.3% | North America, Europe, emerging in Asia-Pacific | Medium term (2-4 years) |

| EV battery dry-room buildouts needing ESD-safe gloves | +1.0% | Asia-Pacific core, North America & Europe expansion | Long term (≥ 4 years) |

| PFAS-free and low-ion formulations opening premium niches | +0.8% | Europe (regulatory), North America & Asia-Pacific (adoption) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Semiconductor Fab Expansions And Contamination Control Intensity

Global wafer-fab projects, typified by TSMC’s USD 165 billion Phoenix complex, are scaling from 4 nm toward 2 nm geometries that tolerate fewer than 10 particles ≥0.1 µm per cubic meter. ISO Class 1–2 suites require ESD-safe, low-ion nitrile gloves to preserve yield in copper interconnects and high-k dielectrics, pushing annual glove orders into the tens of millions per megafab. SEMI forecasts a significant percentage CAGR in front-end capacity through 2028, while AI-accelerated nodes grow significantly, translating directly into longer operator hours and higher glove turnover[2]Semiconductor Equipment and Materials International, “Global Fab Capacity Outlook 2024-2028,” semi.org. India’s Micron ATMP plant, validated in February 2026, highlights the geographic spread of advanced packaging and the demand for additive gloves.

Biopharma Aseptic Manufacturing Tightening

Annex 1’s 58-page revision and USP 797’s 2023 update require glove-integrity tests at the start and end of each batch, plus quarterly fingertip sampling for high-risk compounding. Validation data showcased at the ISPE 2026 Aseptic Conference indicate a uplift in glove consumption per batch [3]International Society for Pharmaceutical Engineering, “2026 Aseptic Conference Proceedings,” ispe.org. Modular cleanrooms that commission in two weeks accelerate compliance, intensifying near-term ordering spikes in North America and Western Europe.

Shift From Latex To Nitrile In Cleanrooms

NIOSH estimates latex allergy prevalence among healthcare workers at 8–17%, and the FDA outlawed powdered latex gloves in 2016, making nitrile the de facto cleanroom standard. Nitrile’s triple puncture resistance, superior alcohol resistance, and absence of protein extractables underpin its market share. Top Glove’s halogen-free nitrile variant, released July 2025, removes chlorine and bromine species that corrode semiconductor interconnects.

Growth In Cleanroom-Intensive Medical Device Manufacturing

Over 500,000 sq ft of new ISO Class 8 space came online in North America from 2024 to 2026. MGS Mfg. Group’s Wisconsin site alone spans 140,000 sq ft dedicated to GLP-1 delivery-device sub-assemblies, each requiring sterile gloves for component handling. Outsourced sterility testing at Nelson Labs doubled capacity in 2026, signaling broader demand for validation-grade gloves.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| NBR/acrylonitrile–butadiene feedstock price volatility | -0.7% | Global, acute in Asia-Pacific | Short term (≤ 2 years) |

| Qualification/validation lock-in slows supplier switching | -0.5% | North America & Europe (stringent), Asia-Pacific emerging | Medium term (2-4 years) |

| Particulation/extractables limits raise costs and scrap | -0.4% | Global, most acute in semiconductor & biopharma | Medium term (2-4 years) |

| Robotics and gloveless isolators reducing manual touchpoints | -0.6% | Europe & North America (early adoption), Asia-Pacific lagging | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

NBR/Acrylonitrile–Butadiene Feedstock Price Volatility

NBR spot prices hit USD 3,574/t in Japan during Q4 2025, 40% above U.S. levels, lifting the raw-material cost share to roughly 30% of glove unit economics. Top Glove and Hartalega have responded with captive latex plants and RM 300 million feedstock CAPEX to stabilize margins.

Qualification/Validation Lock-In Slows Supplier Switching

Extractables testing under ISO 10993-12 and USP can take up to 12 months and cost USD 200,000 per SKU, discouraging rapid adoption of new glove lines even when performance gains are evident. Pharmaceutical buyers, therefore, renew multi-year contracts with incumbent vendors to avoid re-validation downtime.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Nitrile Dominance Anchored By ESD And Extractables Advantages

Nitrile held 63.10% of 2025 volume, translating into the largest cleanroom gloves market size among material classes. The segment is projected to expand at a 9.95% CAGR to 2031, outpacing latex, neoprene, polyisoprene, and vinyl. The cleanroom gloves market share leader offers triple the puncture resistance of natural rubber and full compliance with IEC 61340-5-1 electrostatic thresholds that govern semiconductor and battery plants. Top Glove’s halogen-free line, launched in July 2025, exemplifies innovation aimed at eliminating chlorine-based corrosion risks in sub-3 nm wafer nodes, keeping pace with ISO 14644-1 particle ceilings.

Latex continues to retreat on allergy and regulatory grounds, while polyisoprene captures surgical demand by replicating latex feel without protein allergens. Medline’s 2025 SensiCare launch illustrated polyisoprene’s niche ascent in oncology drug preparation thanks to superior chemotherapy permeation resistance. Neoprene remains a specialty choice for aggressive chemical exposure, while vinyl is preferred for low-risk gowning rooms where puncture strength is secondary. Hybrid synthetics like INTCO’s Syntex blend nitrile and vinyl to offer a mid-priced option that meets ISO Class 7 cleanliness for general electronics assembly.

By End-Use Industry: Biotechnology Outpaces Pharmaceuticals On ATMP Momentum

Pharmaceutical manufacturing delivered 35.87% of 2025 revenue, but biotechnology is forecast to log a 10.18% CAGR to 2031, anchored by monoclonal antibodies, antibody–drug conjugates, and autologous cell therapies. The cleanroom gloves market size supporting ATMP fill-finish suites continues to swell as operators still need gloves for format changes despite the rise of gloveless robotic isolators. Semiconductor and microelectronics accounted for the second-largest share of the cleanroom gloves market, underpinned by TSMC’s Arizona and Intel’s Ohio fabs, plus Micron’s India ATMP facility.

Medical device manufacturers added more than 500,000 sq ft of new ISO-Class space in North America between 2024 and 2026. MGS Mfg.’s Wisconsin build, producing hundreds of millions of GLP-1 injector components per year, is emblematic of high-volume glove consumption. Flat-panel display plants and optoelectronics labs require sub-ppm water-vapor environments, driving orders for ultra-low-ion nitrile gloves. Aerospace and defense, typified by Moog’s cleanroom expansion, seeks FOD-free gloves for satellite propulsion assemblies, completing the end-use mosaic.

By Sterility: Regulatory Mandates Lock In Sterile-Segment Dominance

Sterile variants accounted for 68.19% of 2025 shipments and are projected to grow at a 9.80% CAGR through 2031, maintaining the largest share of the cleanroom gloves market by sterility level. USP 797 obligates sterile gloves for all Category 1–3 compounding, with action limits tightened to ≤1 CFU for Category 3 fingertip tests. Annex 1 further stipulates batch-end glove integrity checks, entrenching sterile usage within European plants. Validation inertia and the high cost of re-certification insulate the sterile category, reinforcing vendor stickiness.

Non-sterile gloves remain prevalent in semiconductor, display, and most electronics cleanrooms, where microbial load is secondary to particulate and ion contamination. Ejendals’ ISO Class 5-certified but non-sterile TEGERA 5100 caters to ESD-critical environments, shipped double-bagged for laminar-flow pass-throughs.

Geography Analysis

North America retained 38.19% of 2025 revenue, powered by USD 52.7 billion in CHIPS Act subsidies that catalyzed wafer-fab and advanced-packaging clusters in Arizona, Ohio, and New York. Modular cleanrooms for 503A and 503B pharmacies proliferated after the 2023 USP 797 revision, accelerating the adoption of sterile gloves among the roughly 7,500 compounding facilities nationwide. Canada leveraged medical-device nearshoring to capture incremental demand, and Mexico saw glove shipments rise as automotive battery plants introduced ISO Class 7 dry rooms.

Asia-Pacific posts the fastest trajectory, with a 10.15% CAGR projected to 2031. India’s USD 18.2 billion Semiconductor Mission enabled Micron’s Sanand ATMP launch in February 2026, while Malaysia’s nitrile-glove majors—Hartalega, Riverstone, and Kossan expanded capacity to serve AI-driven data-center buildouts. China’s 25% U.S. tariff exposure and FDA import alerts redirect procurement toward Malaysian and Thai producers, reinforcing regional supply dominance. The cleanroom gloves market in the region is further boosted by Korean and Japanese EV battery gigafactories that specify ESD-rated nitrile gloves.

Europe’s growth benefits from the EU Chips Act’s EUR 43 billion framework and 2023 Annex 1 enforcement. Germany, France, and the U.K. lead new biologics plants, while Scandinavian PFAS regulations are already prompting PFAS-free glove trials. Hartalega and Sempermed recently secured multi-year supply agreements with German vaccine sites, signaling supplier diversification. Eastern Europe emerges as a secondary hub for disposable-glove contract manufacturing as wage-cost differentials narrow against Southeast Asia.

Middle East & Africa and South America remain nascent in volume terms yet show isolated accelerants. Saudi Arabia’s Vision 2030 pharmaceutical push includes sterile insulin-pen production lines that require ISO Class 7 gloves. Brazil’s ANVISA pipeline for orthopedic implants is spurring local cleanroom upgrades, albeit from a small base. Riverstone cited RM 250.7 million in 4QFY25 cleanroom segment revenue, with Latin America and GCC deliveries on the rise, underscoring untapped geographic pockets.

Competitive Landscape

Five suppliers Ansell Limited, Top Glove Corporation Bhd, Riverstone, Hartalega, and Halyard held majority of global revenue in 2025, confirming a moderately concentrated field. Hartalega allocated RM 7 billion to erect 16 fully automated plants in Kedah, aiming for 80 billion pieces of annual capacity by 2030 and targeting lights-out production that slashes labor costs while boosting consistency. Top Glove invested in upstream NBR, sterilization, and a Vietnam vinyl expansion to hedge feedstock risk and tariff exposure.

Innovation hot spots include PFAS-free nitrile, low-halogen semiconductor grades, and biodegradable chemistries. PowerChem’s January 2026 PC-12WT biodegradable glove addresses the 180 billion-pair landfill challenge without sacrificing ISO Class 5 cleanliness. Ejendals’ accelerator-free TEGERA 5100 focuses on electrostatic safety and touchscreen ergonomics for EV battery cells. Automation, AI-driven contamination analytics, and blockchain lot traceability are emerging differentiators as buyers elevate documentation standards.

Tariffs and compliance barriers reshape sourcing. The United States imposed 25% duties on Chinese gloves effective 2026, and CBP import alerts on specific Chinese plants have funneled demand toward Malaysia and Thailand. ISO 14644 and ISO 10993 gatekeeping favors incumbents with multiyear audit histories, while validation lock-in slows market entry for newcomers despite superior technical claims. Overall, the sector balances scale economies with niche specialization, fostering both consolidation and disruptive entrants.

Cleanroom Gloves Industry Leaders

Top Glove Corporation

Hartalega

Halyard

Ansell Limited

Riverstone

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Micron began commercial production at its USD 2.75 billion ATMP facility in Sanand, India, featuring Class 100 cleanrooms staffed by thousands of gowned operators.

- January 2026: PowerChem launched the PC-12WT biodegradable nitrile glove with EcoTek technology for ISO Class 5 semiconductor and pharma suites.

Global Cleanroom Gloves Market Report Scope

As per the scope of the report, cleanroom gloves are specialized personal protective equipment (PPE) designed to minimize the introduction of human-borne contaminants—such as skin flakes, oils, and particles—into highly controlled environments like semiconductor fabrication, pharmaceutical manufacturing, and biotechnology labs.

The cleanroom gloves market is segmented by material, end-user industry, sterility, and geography. By material, the market is segmented into nitrile (NBR), natural rubber (latex), neoprene (polychloroprene), polyisoprene, and vinyl (PVC). By end users industry, the market is segmented into semiconductors & microelectronics, pharmaceuticals, biotechnology, medical device manufacturing, flat panel display & optoelectronics, research laboratories & academia, and aerospace & defense. By sterility, the market is segmented into companion non-sterile and sterile. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Nitrile (NBR) |

| Natural Rubber (Latex) |

| Neoprene (Polychloroprene) |

| Polyisoprene |

| Vinyl (PVC) |

| Semiconductor & Microelectronics |

| Pharmaceuticals |

| Biotechnology |

| Medical Device Manufacturing |

| Flat Panel Display & Optoelectronics |

| Others |

| Non-sterile |

| Sterile |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Material | Nitrile (NBR) | |

| Natural Rubber (Latex) | ||

| Neoprene (Polychloroprene) | ||

| Polyisoprene | ||

| Vinyl (PVC) | ||

| By End-use Industry | Semiconductor & Microelectronics | |

| Pharmaceuticals | ||

| Biotechnology | ||

| Medical Device Manufacturing | ||

| Flat Panel Display & Optoelectronics | ||

| Others | ||

| By Sterility | Non-sterile | |

| Sterile | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What CAGR is forecast for cleanroom gloves through 2031?

The market is projected to grow at 9.61% between 2026 and 2031.

Which material leads global demand?

Nitrile accounts for 63.10% of 2025 volume and is expanding fastest due to puncture resistance and electrostatic safety.

Why are sterile gloves gaining share?

Annex 1 and USP 797 mandate more frequent integrity tests and fingertip sampling, locking in sterile-glove consumption for aseptic drug production.

Which region will grow quickest?

Asia-Pacific is expected to post a 10.15% CAGR between 2026 and 2031, buoyed by semiconductor and EV-battery investments.

Page last updated on: