CI/CD Tools And Pipeline Automation Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

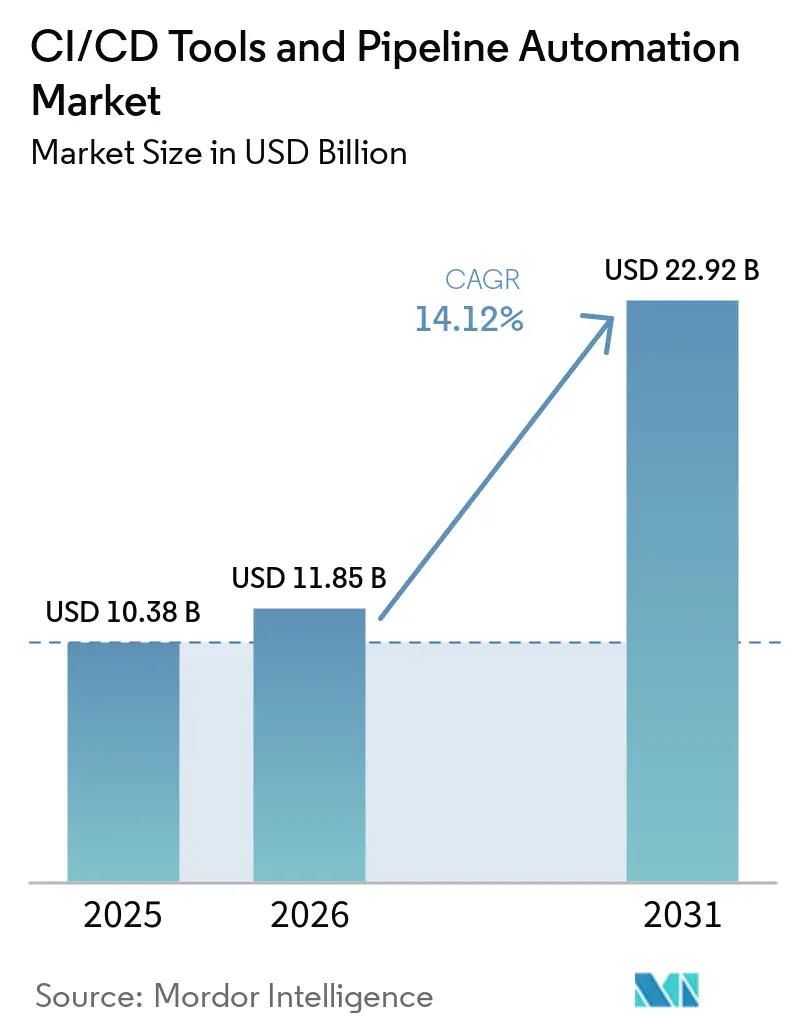

| Market Size (2026) | USD 11.85 Billion |

| Market Size (2031) | USD 22.92 Billion |

| Growth Rate (2026 - 2031) | 14.12% CAGR |

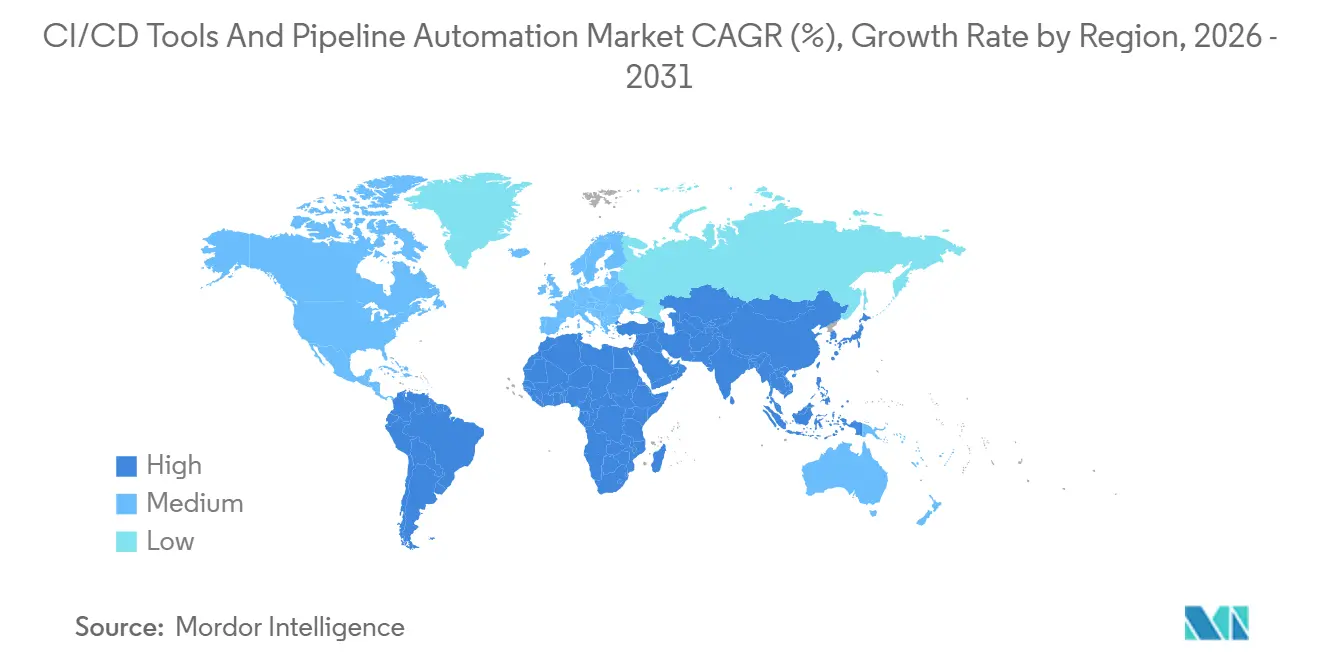

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

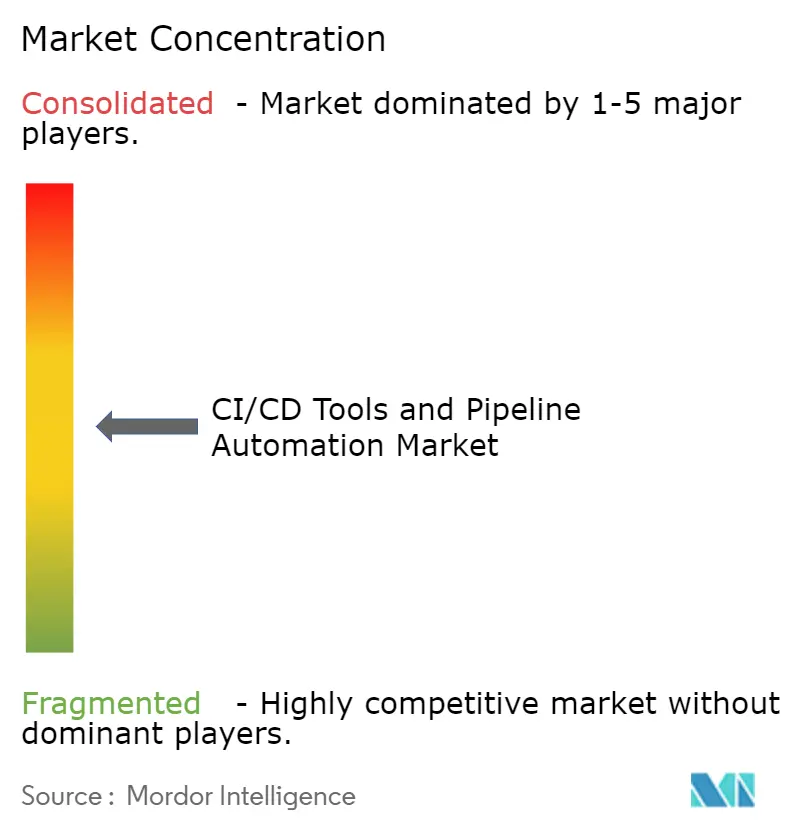

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

CI/CD Tools And Pipeline Automation Market Analysis by Mordor Intelligence

The CI/CD tools and pipeline automation market size is expected to increase from USD 10.38 billion in 2025 to USD 11.85 billion in 2026 and reach USD 22.92 billion by 2031, growing at a CAGR of 14.12% over 2026-2031. Robust expansion reflects enterprises redesigning software-delivery processes around cloud-native stacks, where deployment frequency directly influences revenue velocity. Tools and software platforms still dominate spending, yet demand for managed services is surging as organizations outsource compliance-heavy pipeline orchestration. Cloud deployment remains the baseline architecture, but hybrid models are scaling quickly as regulated sectors balance data-sovereignty rules with elastic capacity. Meanwhile, large enterprises drive most spending, although low-code pipeline builders are putting adoption within reach for small and medium enterprises. Intensifying regulatory mandates, particularly the European Union’s Cyber Resilience Act, are pushing vendors to embed automated security testing, SBOM generation, and vulnerability scanning as default workflows, further supporting growth in the Continuous Integration and Continuous Delivery (CI/CD) tools and pipeline automation market.

Key Report Takeaways

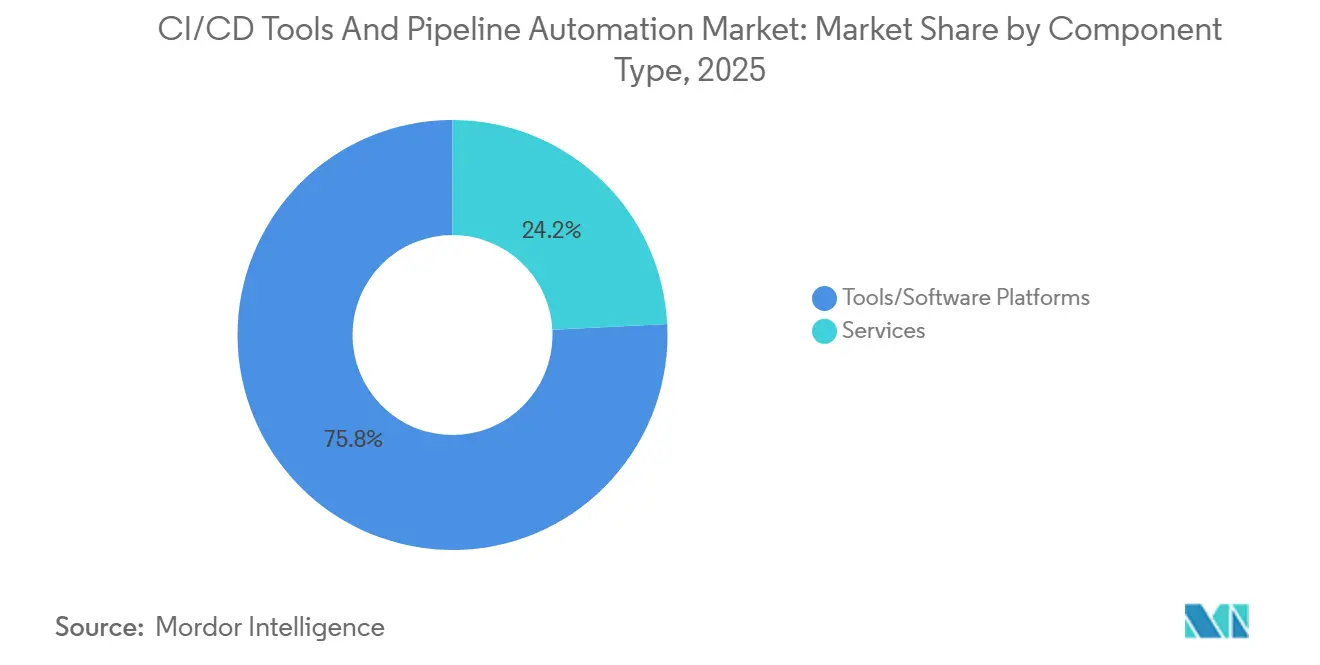

- By component type, tools and platforms led with 75.82% revenue share in 2025, while the services segment is projected to grow at a 16.45% CAGR through 2031.

- By deployment model, cloud-based solutions held 62.11% of the CI/CD tools and pipeline automation market share in 2025; hybrid configurations are advancing at a 15.76% CAGR to 2031.

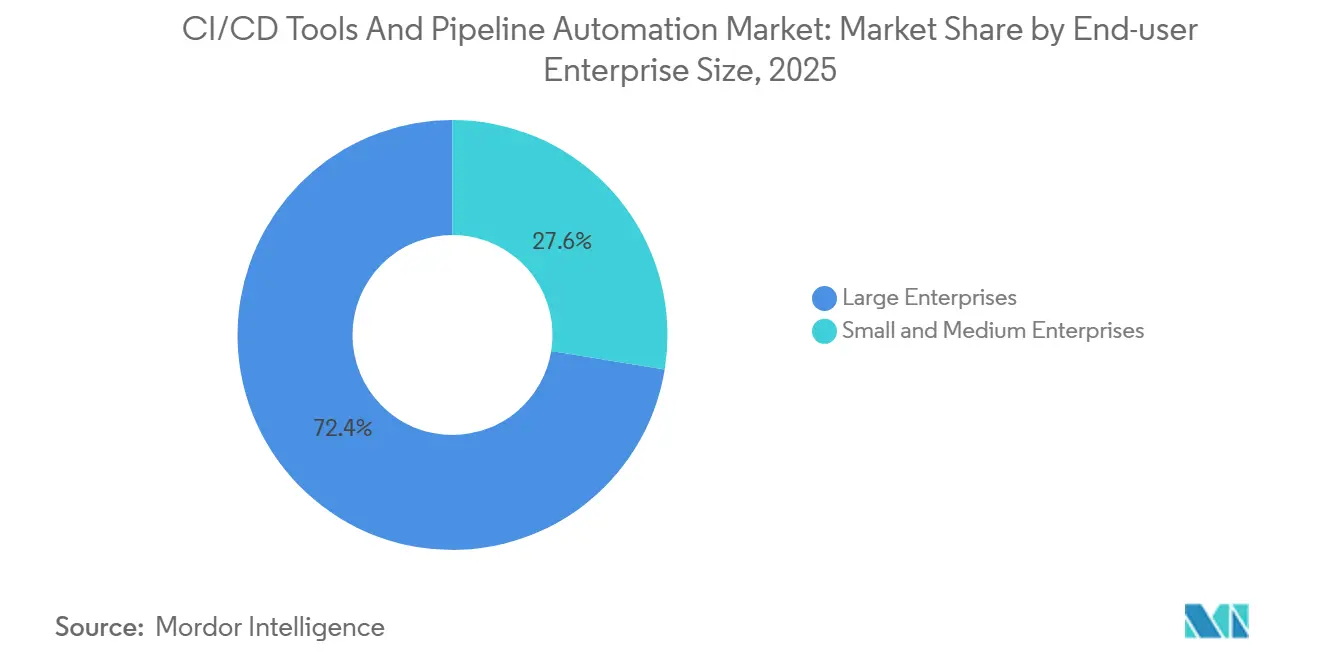

- By end-user enterprise size, large enterprises commanded 72.44% of the CI/CD tools and pipeline automation market size in 2025, whereas SMEs are expanding at a 15.82% CAGR through 2031.

- By end-user industry, IT and telecommunications accounted for 27.80% of revenue share in 2025, and healthcare and life sciences are forecast to expand at a 19.12% CAGR through 2031.

- By geography, North America held 38.20% of 2025 revenue, while Asia-Pacific is on track to register a 17.48% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global CI/CD Tools And Pipeline Automation Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Adoption of DevOps Across Enterprises | +3.2% | Global, led by North America and Europe | Medium term (2-4 years) |

| Growing Preference for Cloud-Native Pipelines | +2.8% | Global, driven by Asia-Pacific and North America | Short term (≤ 2 years) |

| Integration of AI for Predictive Testing | +2.5% | North America and Europe, spill-over to Asia-Pacific | Medium term (2-4 years) |

| Expansion of GitOps and IaC Practices | +2.1% | Global, strong in finance and government sectors | Long term (≥ 4 years) |

| Rising Compliance-Driven DevSecOps Automation | +1.8% | Europe, North America, Asia-Pacific | Short term (≤ 2 years) |

| Surge in Low-Code Pipeline Builders for SMEs | +1.2% | Global, fastest in Asia-Pacific and South America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Adoption of DevOps Across Enterprises

Enterprises now view deployment frequency as a proxy for revenue velocity rather than an internal metric. In 2025, 78% of surveyed organizations reported active GitOps deployments, and 93% planned to expand their use.[1]Cloud Native Computing Foundation, “CNCF Annual Survey 2025,” cncf.io Financial services firms synchronize Kubernetes manifests across dozens of clusters, enabling code approved for compliance to reach production within minutes. The resulting agility forces laggards to accelerate adoption or cede ground, cementing DevOps maturity as a competitive differentiator inside the Continuous Integration and Continuous Delivery (CI/CD) tools and pipeline automation market.

Growing Preference for Cloud-Native and Containerized Pipelines

Containerization has shifted from experiment to foundation, with 82% of enterprises running Kubernetes in production during 2025 and 60% adopting pipelines optimized for cloud-native workloads. Economic drivers dominate, bin-packing can trim compute expense by 30%-40% while preventing environment drift that once consumed significant developer time.[2]Docker Inc., “Container Platform Documentation,” docker.com Kubernetes penetration hit 96% in 2026, compelling vendors to fine-tune for Helm charts, Kustomize overlays, and ephemeral test pods. Outside air-gapped defense workloads, on-premise Continuous Integration and Continuous Delivery (CI/CD) tools are rapidly losing relevance.

Integration of AI for Predictive Testing and Orchestration

Generative AI copilots are moving quality-assurance steps left. Harness’s 2024 rollout of AI-driven root-cause analysis trimmed mean-time-to-resolution by 40% at pilot customers, while CloudBees introduced predictive analytics that flag risky commits before they enter build queues. The healthcare and automotive sectors gain particular value from early defect detection, as it averts costly recalls. These capabilities compress feedback loops from days to minutes, strengthening platform stickiness inside the CI/CD tools and pipeline automation market.

Expansion of GitOps and Infrastructure-as-Code Practices

GitOps adoption reached 78% in 2025, with Argo CD accounting for the majority of implementations. Auditability is the primary draw: each infrastructure change is versioned, satisfying SOX, PCI-DSS, and HIPAA audits without manual paperwork. Finance companies layer policy-as-code controls that, for example, block unsigned container images. The convergence of GitOps with financial-operations telemetry helps teams forecast cloud spend within the pull-request workflow, reinforcing holistic governance.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Legacy System Integration Complexity | -1.5% | Global, especially North America and Europe where mainframes persist | Long term (≥ 4 years) |

| Shortage of Skilled DevOps Professionals | -1.3% | Global, most acute in tier-1 cities across all regions | Medium term (2-4 years) |

| Escalating Tool Sprawl and Governance Gaps | -0.8% | Global, particularly in multinational enterprises | Medium term (2-4 years) |

| Security Risks from Misconfigured Pipelines | -0.6% | Global, with heightened scrutiny in regulated verticals | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Legacy System Integration Complexity

The primary obstacle is organizational inertia rather than pure technical mismatch. Older platforms often lack modern APIs, forcing teams to craft custom adapters that immediately balloon technical debt. Financial institutions frequently report proof-of-concept failures because transaction-processing cores cannot expose real-time data. Vendors offering pre-built connectors for SAP, Oracle, or IBM middleware shorten integration cycles from quarters to weeks, yet the cumulative effort still throttles the trajectory of the Continuous Integration and Continuous Delivery (CI/CD) tools and pipeline automation market.

Shortage of Skilled DevOps Professionals

Median time-to-hire exceeded 90 days in North America and Europe during 2025, with Kubernetes-certified engineers commanding 25%-30% salary premiums.[3]LinkedIn Corporation, “LinkedIn Talent Insights,” linkedin.com Scarcity stems from the multidisciplinary skillset required across container orchestration, security scanning, and observability. Healthcare providers shelved one-fifth of planned automation projects in 2025 due to unfilled roles, signaling that human-capital constraints may clip growth until training pipelines scale.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component Type: Services Scale as Complexity Rises

Tools commanded 75.82% revenue in 2025, yet the services arm of the CI/CD tools and pipeline automation market is poised to expand at 16.45% through 2031. Professional assessments, implementation projects, and managed pipelines are becoming prerequisites for platform adoption as buyers seek proof-of-concept validation. Tata Consultancy Services formalized alliances to deliver AI-powered orchestration, demonstrating how implementation expertise now drives value.

Meanwhile, consolidation is reshaping the tools landscape. GitLab recorded USD 955 million in fiscal-year 2026 revenue, validating demand for unified platforms that merge source control, CI/CD, security, and project management.[4]GitLab Inc., “Fiscal-Year 2026 Results,” ir.gitlab.com Atlassian’s USD 1 billion purchase of DX in 2025 underscores a pivot toward embedded engineering intelligence, while niche vendors like Buildkite carve performance-specific lanes. The shift indicates that strategic advantage now accrues to platforms bundling analytics, security, and deployment into a single control plane.

By Deployment Model: Hybrid Finds a Regulatory Sweet Spot

Cloud solutions held 62.11% share in 2025 because elastic pricing aligns with fluctuating build volumes. Yet hybrid adoption is growing by 15.76% through 2031 as financial, healthcare, and public-sector organizations split sensitive workloads between on-premises clusters and cloud burst capacity. ArgoCD’s declarative synchronization lets teams apply identical policies across both realms, satisfying PCI-DSS or HIPAA audits. By leveraging a GitOps model, it ensures that the desired system state is version-controlled, auditable, and automatically enforced across environments, reducing configuration drift between development, staging, and production.

On-premises systems exist only within air-gapped defense environments, and their relevance continues to wane. Vendors now offer dedicated instances inside customer VPCs, blending SaaS convenience with data control. The trend signals that seamless movement between on-premise, public cloud, and edge locations will become the baseline expectation inside the CI/CD tools and pipeline automation market.

By End-user Enterprise Size: Low-Code Tools Pull SMEs Into the Fold

Large enterprises retained 72.44% spending in 2025 because they manage hundreds of microservices, multiple clouds, and complex governance requirements. The CI/CD tools and pipeline automation market size for SMEs, however, is set to grow rapidly at 15.82% through 2031. Platforms such as Buddy and Semaphore provide unlimited builds at SME-friendly pricing, reducing entry costs by up to 80%.

In Asia-Pacific and South America, digital natives are bypassing on-premise infrastructure altogether, opting for cloud-first stacks. Depot’s container build acceleration, which cuts image compilation times by up to 60%, exemplifies the feature set designed for resource-constrained teams. Conversely, enterprises justify six-figure contracts by demanding granular role-based access, advanced audit logs, and 24/7 support, highlighting a bifurcated demand curve.

By End-User Industry: Healthcare Accelerates Under Regulatory Pressure

IT and telecommunications led with 27.80% revenue in 2025 as high-frequency release cycles are intrinsic to SaaS models. Healthcare and life sciences are now registering the fastest growth, projected at a 19.12% CAGR, as FDA guidance and SBOM mandates require automated vulnerability scanning upfront. Pharmaceutical firms have embedded pipelines into clinical-trial data platforms, ensuring consent workflows remain compliant before deployment.

Banking institutions integrate DevSecOps automation to comply with SOX and PCI-DSS, often blocking non-compliant container images at the pull request level. Retailers deploy as many as 100 updates per day during peak seasons, relying on canary strategies to isolate errors. Automotive manufacturers push over-the-air updates across millions of vehicles, balancing new code with legacy ECUs. The government and defense segments remain anchored to on-premises deployments, though GitOps is gradually improving auditability.

Geography Analysis

North America led with 38.20% revenue in 2025, buoyed by a dense ecosystem of platform providers and Fortune 500 adopters. Venture funding for DevOps startups topped USD 13 billion in 2026, sustaining high competitive churn. Canada and Mexico also scale adoption as cross-border data flows require hybrid models that respect both GDPR and national privacy statutes. Organizations operating across North America increasingly adopt hybrid and multi-cloud CI/CD architectures to ensure data residency, sovereignty, and compliance requirements are met without disrupting development velocity.

Asia-Pacific is on pace for a 17.48% CAGR to 2031, the fastest worldwide. India’s Unified Payments Interface processes more than 10 billion monthly transactions and relies on continuous delivery to update fraud-detection algorithms without downtime.[5]National Payments Corporation of India, “UPI Statistics,” npci.org.in China emphasizes domestic hosting with Alibaba Cloud or Tencent Cloud integrations, while Japan and South Korea embed DevSecOps to meet stringent cyber rules. Singapore, Malaysia, and Indonesia adopt artifact-management services in response to data-localization mandates, illustrating how regulatory nuance fuels demand inside the CI/CD tools and pipeline automation market.

Europe is accelerating under the Cyber Resilience Act, which enforces automated security testing and SBOM generation beginning August 2026. Germany, the United Kingdom, and France lead uptake, helped by deep manufacturing and automotive footprints. Open-source tooling retains popularity, with GitHub Actions, Jenkins, and GitLab capturing much of the share. The Middle East experiences early-stage adoption driven by sovereign cloud mandates, whereas Africa and South America advance more gradually as connectivity and skills improve.

Competitive Landscape

The CI/CD tools and pipeline automation market is moderately consolidated. GitLab’s USD 955 million fiscal-year 2026 revenue validates the all-in-one platform thesis. Atlassian’s purchase of DX integrates engineering intelligence directly into Jira and Bitbucket, reflecting a pivot toward upstream analytics that surface bottlenecks before code hits production. Buildkite, optimized for macOS and GPU workloads, illustrates how targeted performance wins can sustain niche differentiation.

Emerging white-space centers on AI-native orchestration and compliance automation. Harness’s USD 150 million raise funds generative AI copilots that auto-remediate failed builds, while JFrog’s agent-skills registry targets reproducibility for AI model pipelines. Managed-service providers such as Tata Consultancy Services commoditize platform selection by delivering turnkey pipeline-as-a-service packages, shifting differentiation to implementation depth and regional support.

Startups like Entire are betting on conversational deployment workflows that may eventually displace YAML-driven pipelines if developer uptake scales. These approaches aim to abstract pipeline complexity through natural language interfaces, enabling developers and even non-specialist teams to trigger, modify, and debug workflows without deep configuration expertise. If successful, this could significantly lower the barrier to CI/CD adoption in mid-market and less mature engineering organizations. At the same time, questions remain around governance, auditability, and performance at scale, particularly for regulated industries.

CI/CD Tools And Pipeline Automation Industry Leaders

GitLab Inc.

Atlassian Corporation

CloudBees Inc.

Circle Internet Services Inc.

JFrog Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Qodo secured USD 70 million Series B funding to expand its AI-powered code-review and testing platform, targeting European and Asia-Pacific growth.

- March 2026: JFrog launched an agent-skills registry with NVIDIA to govern AI-model artifacts through existing pipelines.

- March 2026: JFrog and iZeno formed a strategic partnership to extend artifact-management services across Southeast Asia.

- February 2026: GitLab added 15 global partners to its Managed Service Provider program, enabling turnkey CI/CD delivery under white-label models.

Global CI/CD Tools And Pipeline Automation Market Report Scope

The CI/CD Tools and Pipeline Automation Market revenue represents the total income generated by vendors from the sale, subscription, and licensing of tools/software platforms that automate continuous integration, continuous delivery, and continuous deployment processes across the software development lifecycle. Market revenue also encompasses earnings from associated services, including implementation, consulting, training, support, and managed CI/CD pipeline services. These services are increasingly critical as enterprises seek to optimize and scale automated development pipelines, particularly in cloud-native and hybrid environments.

The CI/CD Tools and Pipeline Automation Market Report is Segmented by Component Type (Tools/Software Platforms, and Services), Deployment Model (Cloud-Based, On-Premise, and Hybrid), End-User Enterprise Size (Large Enterprises, and Small and Medium Enterprises), End-User Industry (BFSI, Healthcare and Life Sciences, Retail and eCommerce, Automotive and Transportation, IT and Telecommunications, Government and Defense, Manufacturing, and Other End-User Industries), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Tools/Software Platforms |

| Services |

| Cloud-Based |

| On-Premises |

| Hybrid |

| Large Enterprises |

| Small and Medium Enterprises |

| Banking, Financial Services and Insurance (BFSI) |

| Healthcare and Life Sciences |

| Retail and eCommerce |

| Automotive and Transportation |

| IT and Telecommunications |

| Government and Defense |

| Manufacturing |

| Other End-User Industries |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Egypt | |

| Rest of Africa |

| By Component Type | Tools/Software Platforms | |

| Services | ||

| By Deployment Model | Cloud-Based | |

| On-Premises | ||

| Hybrid | ||

| By End-user Enterprise Size | Large Enterprises | |

| Small and Medium Enterprises | ||

| By End-user Industry | Banking, Financial Services and Insurance (BFSI) | |

| Healthcare and Life Sciences | ||

| Retail and eCommerce | ||

| Automotive and Transportation | ||

| IT and Telecommunications | ||

| Government and Defense | ||

| Manufacturing | ||

| Other End-User Industries | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the projected value of the CI/CD tools and pipeline automation market by 2031?

The market is forecast to reach USD 22.92 billion by 2031.

Which deployment model is growing fastest?

Hybrid configurations are advancing at a 15.76% CAGR through 2031 as firms balance compliance with cloud scalability.

Why is healthcare showing rapid adoption of CI/CD pipelines?

Regulatory mandates now require automated vulnerability scanning and SBOM generation, pushing healthcare and life-sciences firms toward CI/CD-driven DevSecOps.

Which region is expected to record the highest growth rate?

Asia-Pacific is forecast to expand at a 17.48% CAGR to 2031, propelled by large-scale digital-government and fintech initiatives.

How are AI capabilities changing CI/CD workflows?

Generative AI copilots predict build failures, auto-generate tests, and accelerate root-cause analysis, reducing mean-time-to-resolution and strengthening pipeline reliability.

What is the biggest restraint on market growth?

Integration complexity with legacy systems remains the major drag, often prolonging migration timelines and inflating project costs.

Page last updated on: